Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 340 Million |

| Market Size (2030) | USD 419 Million |

| Growth Rate (2025 - 2030) | 4.27% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Plant Protein Market Analysis by Mordor Intelligence

The United Kingdom Plant Protein Market size is estimated at 340 million USD in 2025, and is expected to reach 419 million USD by 2030, growing at a CAGR of 4.27% during the forecast period (2025-2030).

The UK plant protein industry is experiencing a significant transformation driven by changing consumer preferences and retail dynamics. Major retailers are expanding their plant-based protein market offerings, with companies like Tesco and Waitrose partnering with manufacturers to produce white-labeled versions of plant protein products to reach larger scales. In 2022, approximately 33% of UK consumers regularly consumed plant-based protein drinks, demonstrating the mainstream acceptance of these alternatives. The retail landscape continues to evolve with the integration of both traditional and online channels, creating a seamless shopping experience for plant protein products.

Product innovation and technological advancements are reshaping the industry landscape, particularly in meat and dairy alternatives. Manufacturers are investing in research and development to improve the taste, texture, and nutritional profiles of plant protein products. The emergence of new technologies like 3D printing of meat alternatives using pea protein formulations represents a significant advancement in the sector. These innovations are particularly resonating with health-conscious consumers, as evidenced by the fact that in 2022, British consumers spent an average of USD 16.13 per month on protein ingredients powders and sports supplements.

The industry is witnessing a notable shift in consumer behavior patterns, particularly in home consumption and dietary preferences. In 2022, approximately 73% of British people preferred eating at home, leading to increased demand for plant-based protein products market suitable for home preparation. This trend has prompted manufacturers to develop more convenient and versatile plant protein products that cater to home cooking needs. The pet food sector has also emerged as a significant market for alternative protein, with about 52% of British adults owning pets in 2022, driving demand for plant-based pet food alternatives.

Supply chain optimization and sustainability initiatives are becoming increasingly crucial in the industry. The UK feed industry's heavy reliance on imports, with over 70% of its maize, soy, and rapeseed requirements sourced internationally, has led to an increased focus on developing local supply chains. Currently, approximately 90% of soy in the country is directed towards animal feed, highlighting the significant role of the agricultural sector in the UK plant-based market. Companies are increasingly investing in sustainable sourcing practices and working closely with farmers to ensure a consistent supply while meeting environmental standards.

United Kingdom Plant Protein Market Trends and Insights

The growth of plant protein consumption fuels opportunities for key players in the ingredients segment

- The recommended intake of proteins for adults in good health is 0.83 g/kg/d. The average intake of protein consumption ranges from 0.83 to 2.2 g/kg/d for an adult under 60 years of age. The average daily intake of proteins for adult women is 74 g, and for adult men, it is 100 g. Millennials and Gen Z are particularly driving the growing demand for plant-based diets and supplements. This is primarily because plant-based proteins are rapidly becoming the only source of all the essential amino acids that can replace animal protein. The protein segment's emergence can potentially reduce the environmental impact associated with the country's reliance on animal protein.

- The top users of plant-based foods are young and urban customers who believe consuming less meat is better for their health and the environment. An increasing number of people in the United Kingdom are expected to give up meat or adopt a vegetarian or vegan diet in the coming year. The UK government promotes a healthy lifestyle and diet among its consumers. This offers an opportunity for the soy protein ingredient, which is considered organic, pure, and healthful. The per capita consumption of soy protein favorably increased by 4.6% in 2022 from 2016.

- In the United Kingdom, the average amount of rice consumed per person per week from 2019 to 2020 was 111 grams. Rice contains essential nutrients such as thiamine, riboflavin, niacin, vitamin E, zinc, potassium, iron, and fiber. The average British citizen consumes about 5.6 kg of rice annually, with white rice accounting for 80% of purchases. Due to the country's expanding ethnic population and increased dietary variety, rice consumption in the United Kingdom is anticipated to increase significantly.

Understand The Key Trends Shaping This Market

Download PDF

The United Kingdom is concentrating on enhancing its wheat and pea production capabilities

- The graph depicts the production data for raw materials such as dry peas, rice, wheat, and soya beans produced in the United Kingdom. The country is the key producer of wheat and peas. In 2021, the volume of wheat produced reached approximately 14 million metric ton, aided by regular rainfall and the temperate climate. Similarly, the fall planting conditions of the previous year were considerably better, resulting in a better wheat yield in 2020, thereby encouraging further winter wheat planting over spring crops like barley. In terms of pea production, the country is 90% self-sufficient.

- The country's unfavorable environment and concomitant harvesting issues restrict soy production. However, the rising demand from the food and animal feed sectors has piqued the interest of farmers, significantly increasing the crop's potential in the United Kingdom. In 2021, the total croppable area increased by 0.5% to 6.1 million hectares, boosting soy production.

- In increasing numbers, consumers purchase plant-based foods, especially protein alternatives in the meat and dairy aisles. Sales of meat alternatives, in particular, have jumped by 60% over the past two years, driven by better tastes and the wider availability of products. Currently, 14% of adults in the United Kingdom (7.2 million) follow a meat-free diet. A further 8.8 million people planned to go meat-free in 2022 (the highest figure in four years). As a result, the production of soy species is increasing in line with the adequate climate conditions in the United Kingdom. In the 12 months ending June 2022, soybean imports amounted to about 688 thousand metric tons, higher than the previous year's data.

Understand The Key Trends Shaping This Market

Download PDF

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Market maturation and declining birth rates are accountable for the slow growth rate

- Functional beverages to play a key role in future market growth

- The growing ex-pat population in most countries globally has impacted the sale of condiments and sauces on a global scale

- The demand for dairy alternatives is expected to boost market growth

- Meat alternatives are expected to register a significant growth rate

- The demand for savory snacks spiked in the United Kingdom

- There is an increasing demand for animal-sourced products

- Artisanal and gluten-free products are supporting the bakery industry

- Changing lifestyles and a thriving food industry in the United Kingdom bolster the demand for convenient food products such as breakfast cereals

- Sugar reduction programs to hinder segmental growth during the forecast period

- Increasing awareness of nutritious products in the United Kingdom, coupled with growing product availability and investments in the industry, is driving market demand

- The plant-based ready-to-eat packaged food market is projected to grow during the forecast period

- Millennials' inclination toward fitness emerges as the major market driver

- Skinimalism trend is expected to be in high demand in the United Kingdom

Segment Analysis: Protein Type

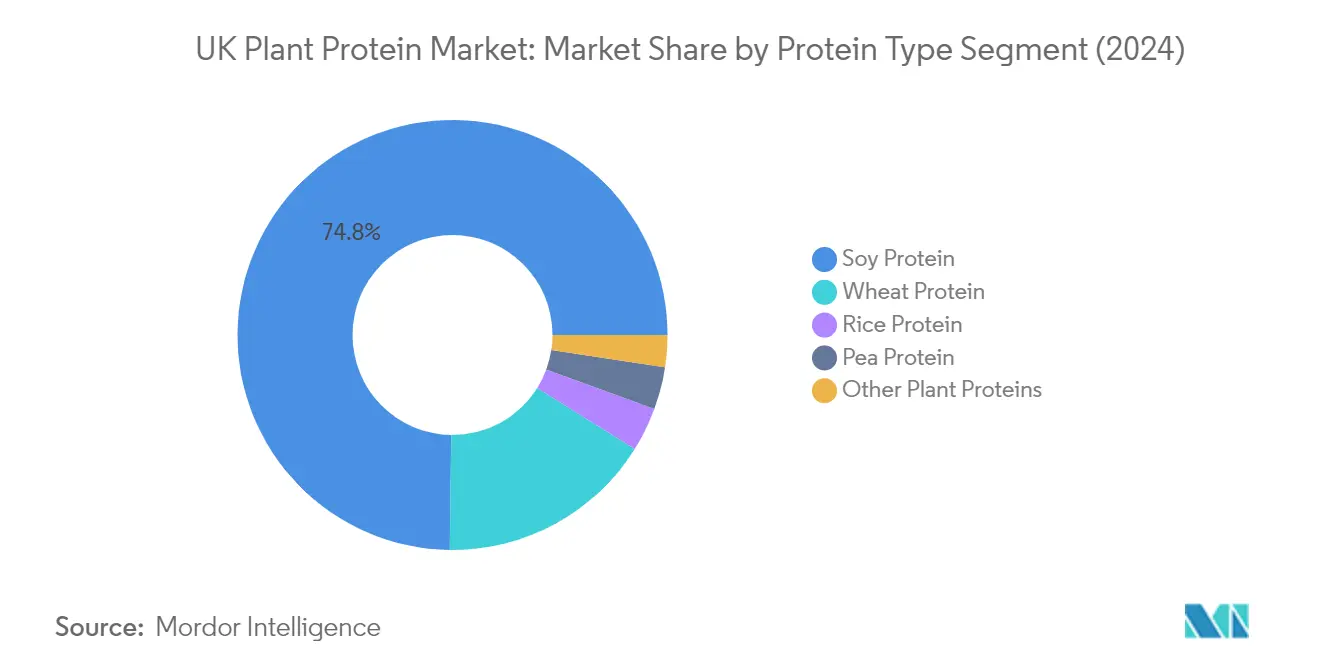

Soy Protein Segment in UK Plant Protein Market

Soy protein dominates the UK plant protein market, commanding approximately 75% market share in 2024. This significant market position is attributed to its versatile applications across various end-user industries, particularly in meat alternatives and dairy substitutes. The segment's dominance is reinforced by soy protein's superior nutritional profile, containing essential amino acids comparable to meat proteins, making it an ideal choice for manufacturers developing plant-based products. Additionally, soy protein's lower cost compared to other protein alternatives and its improved functionalities in terms of texture, taste, and processing capabilities have contributed to its widespread adoption in the food and beverage industry.

Pea Protein Segment in UK Plant Protein Market

The pea protein segment is experiencing remarkable growth in the UK plant protein market, projected to grow at approximately 9% during 2024-2029. This accelerated growth is driven by increasing consumer preference for allergen-free protein sources and pea protein's superior functional properties in various applications. The segment's expansion is further supported by its sustainable production practices and lower environmental impact compared to other protein sources. Manufacturers are increasingly incorporating pea protein into their product formulations due to its neutral taste profile, excellent solubility, and high protein content, which is about 25% higher than wheat protein and rice protein.

Remaining Segments in Protein Type

The UK plant protein market encompasses several other significant segments including wheat protein, rice protein, hemp protein, potato protein, and other plant proteins. Wheat protein has established itself as a crucial ingredient in the bakery and meat alternative sectors due to its unique functional properties. Rice protein has gained traction among consumers seeking hypoallergenic options, while hemp protein is emerging as a premium option in the sports nutrition segment. Potato protein, though smaller in market share, serves specific applications in the food industry, particularly in specialized dietary products. These diverse protein sources collectively contribute to the market's depth and cater to varying consumer preferences and application requirements.

Segment Analysis: End User

Food & Beverages Segment in UK Plant Protein Market

The Food & Beverages segment dominates the UK plant protein market, commanding approximately 52% market share in 2024. This significant market position is primarily driven by the growing demand for meat and dairy alternatives amid rising veganism in the country. The segment's dominance is particularly evident in applications such as meat alternatives, dairy alternatives, bakery products, and beverages. The increasing consumer preference for plant protein isolate and plant protein concentrate as alternatives to animal proteins, coupled with the rising number of product launches in plant-based categories by major food manufacturers, has strengthened this segment's market leadership. Major retailers in the UK are expanding their plant-based product portfolios, particularly in categories like ready meals, where about 16% of products sold in UK supermarkets are plant-based products.

Supplements Segment in UK Plant Protein Market

The Supplements segment is emerging as the fastest-growing category in the UK plant protein market, projected to grow at approximately 8% CAGR from 2024 to 2029. This remarkable growth is primarily driven by the increasing adoption of vegetable protein in sports nutrition products and the rising consumer focus on health and fitness. The segment's growth is particularly notable in sports and performance nutrition applications, where consumers are increasingly shifting toward vegan sports nutrition products to improve performance and maintain healthier, more sustainable lifestyles. In the United Kingdom, a significant portion of sports nutrition users believe that sports nutrition products made with plant proteins are healthier, driving manufacturers to innovate and expand their plant-based supplement offerings.

Remaining Segments in End User Segmentation

The Animal Feed and Personal Care & Cosmetics segments complete the UK plant protein market landscape, each serving distinct industrial applications. The Animal Feed segment maintains a substantial presence in the market, driven by the increasing demand for sustainable and plant-based feed alternatives in livestock production. The Personal Care & Cosmetics segment, while smaller in market share, is gaining traction due to the rising demand for natural and plant-based protein ingredients in cosmetic formulations. Both segments are benefiting from ongoing research and development activities, leading to innovative applications and improved functionality of plant proteins in their respective fields.

Competitive Landscape

Top Companies in United Kingdom Plant Protein Market

The plant protein market in the United Kingdom is characterized by intense competition among major players who are actively pursuing innovation and expansion strategies. Companies are focusing on developing novel protein ingredients, particularly in the pea protein and soy protein categories, to meet the growing demand for meat and dairy alternatives. Product development efforts are centered around improving taste, texture, and functionality while maintaining a clean label status. Operational agility is demonstrated through investments in R&D centers and production facilities, particularly in strategic locations across Europe to serve the UK market efficiently. Strategic moves include partnerships with regional clients and agricultural cooperatives to ensure sustainable sourcing of raw materials. Companies are expanding their presence through both organic growth and acquisitions, with particular emphasis on strengthening their position in emerging segments like sports nutrition and plant-based supplements.

Fragmented Market with Strong Global Players

The UK plant protein market exhibits a fragmented structure with a mix of global conglomerates and specialized manufacturers. Major multinational companies like Archer Daniels Midland Company, International Flavors & Fragrances Inc., and Kerry Group PLC maintain significant market presence through their extensive distribution networks and diverse product portfolios. These global players leverage their research capabilities and technological expertise to maintain competitive advantages. Local players and specialists focus on niche segments and regional distribution channels, often competing through product customization and customer service excellence.

The market is experiencing ongoing consolidation through mergers and acquisitions, particularly as larger companies seek to expand their plant protein capabilities and geographic reach. Strategic acquisitions are focused on companies with specialized technologies or unique product offerings in emerging segments like pea protein and textured vegetable proteins. Companies are also forming strategic alliances with ingredient suppliers and food manufacturers to strengthen their market position and expand their customer base. The trend toward consolidation is expected to continue as companies seek to achieve economies of scale and expand their product portfolios.

Innovation and Sustainability Drive Future Success

For incumbent companies to maintain and increase their market share, a focus on product innovation and sustainability initiatives is crucial. Market leaders are investing heavily in research and development to improve protein functionality, taste profiles, and application versatility. Sustainable sourcing practices and transparent supply chains are becoming increasingly important for maintaining customer trust and market position. Companies are also expanding their production capabilities and distribution networks while developing closer relationships with end-users to better understand and meet their specific requirements.

New entrants and challenger brands can gain ground by focusing on specialized market segments and innovative product offerings. Success factors include developing unique value propositions, establishing strong relationships with local distributors, and maintaining agility in responding to changing consumer preferences. The regulatory environment, particularly regarding protein content claims and labeling requirements, continues to shape market dynamics. Companies must also address the growing demand for organic and non-GMO plant-based protein while managing substitution risks from emerging protein alternatives. Building strong relationships with food and beverage manufacturers, particularly in the growing plant-based meat and dairy alternatives segments, will be crucial for long-term success.

United Kingdom Plant Protein Industry Leaders

Archer Daniels Midland Company

Cargill Incorporated

Ingredion Incorporated

International Flavors & Fragrances Inc.

Kerry Group PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2022: Roquette, a plant-based protein manufacturer, released two novel rice proteins to address the market demand for meat substitute applications. The new Nutralys rice protein line includes a rice protein isolate and a rice protein concentrate.

- May 2021: Lantmannen's subsidiary, Lantmännen Agroetanol, invested SEK 800 million in a biorefinery in Norrköping. It will strengthen Lantmännen’s position in the market for grain-based food ingredients, specifically gluten production. The new production line is planned to be fully operational during the second quarter of 2023.

- April 2021: Ingredion Inc. launched two new ingredients to its plant-based pea protein segment. It launched VITESSENSE pulse 1853 pea protein isolate and Purity P 1002 pea starch, which are 100% sustainably sourced from North American farms.

United Kingdom Plant Protein Market Report Scope

Hemp Protein, Pea Protein, Potato Protein, Rice Protein, Soy Protein, Wheat Protein are covered as segments by Protein Type. Animal Feed, Food and Beverages, Personal Care and Cosmetics, Supplements are covered as segments by End User.Protein Type

| Hemp Protein |

| Pea Protein |

| Potato Protein |

| Rice Protein |

| Soy Protein |

| Wheat Protein |

| Other Plant Protein |

End User

| Animal Feed | ||

| Food and Beverages | By Sub End User | Bakery |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternative Products | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Supplements | By Sub End User | Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

| Protein Type | Hemp Protein | ||

| Pea Protein | |||

| Potato Protein | |||

| Rice Protein | |||

| Soy Protein | |||

| Wheat Protein | |||

| Other Plant Protein | |||

| End User | Animal Feed | ||

| Food and Beverages | By Sub End User | Bakery | |

| Beverages | |||

| Breakfast Cereals | |||

| Condiments/Sauces | |||

| Confectionery | |||

| Dairy and Dairy Alternative Products | |||

| Meat/Poultry/Seafood and Meat Alternative Products | |||

| RTE/RTC Food Products | |||

| Snacks | |||

| Personal Care and Cosmetics | |||

| Supplements | By Sub End User | Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | |||

| Sport/Performance Nutrition | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF