Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

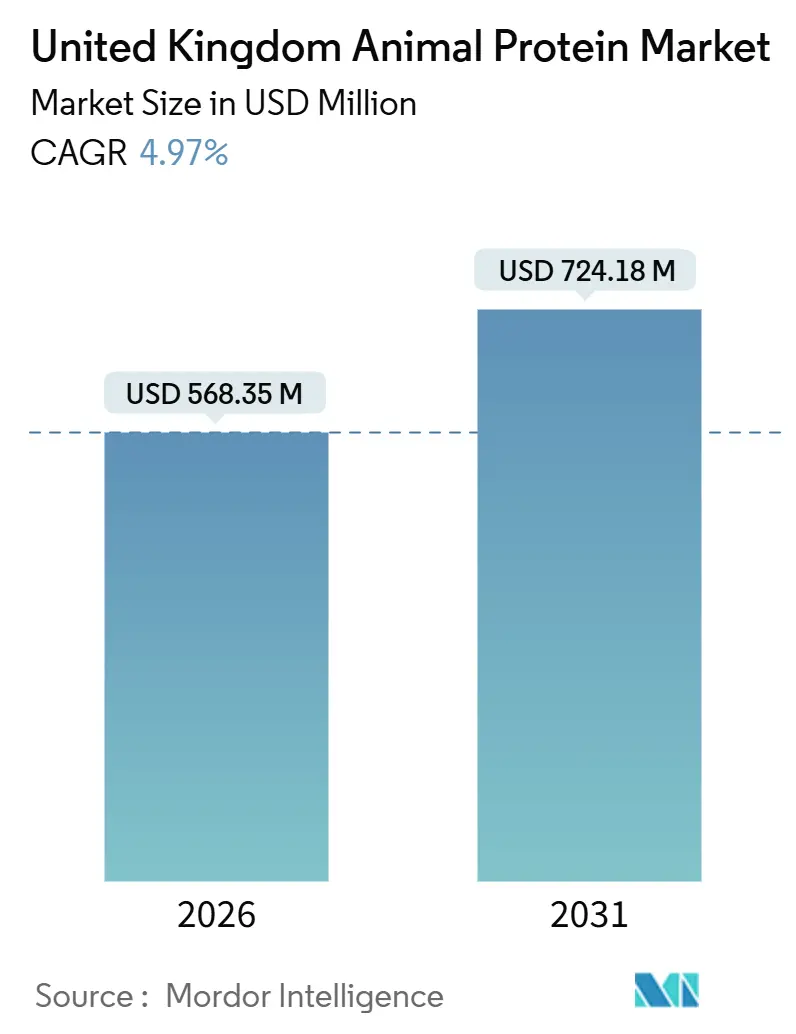

| Market Size (2026) | USD 568.35 Million |

| Market Size (2031) | USD 724.18 Million |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Animal Protein Market Analysis by Mordor Intelligence

The United Kingdom animal protein market size stood at USD 568.35 million in 2026 and is projected to reach USD 724.18 million by 2031, registering a 4.97% CAGR over the period. This advance reflects a structural pivot toward clinical nutrition, beauty-from-within products, and ethically sourced ingredients rather than pure volume expansion. Whey remains the single-largest protein type because of its entrenched role in sports nutrition, infant formula, and bakery fortification, yet collagen peptides are stealing growth momentum as consumers link the ingredient to joint, skin,n and post-surgery recovery benefits. Process technology upgrades, cross-flow microfiltration, enzymatic hydrolysis, and energy-efficient spray drying- continue to lower unit cost while delivering near-flavorless, high-purity isolates that match formulator requirements for beverages, bars, and clinical feeds.

Key Report Takeaways

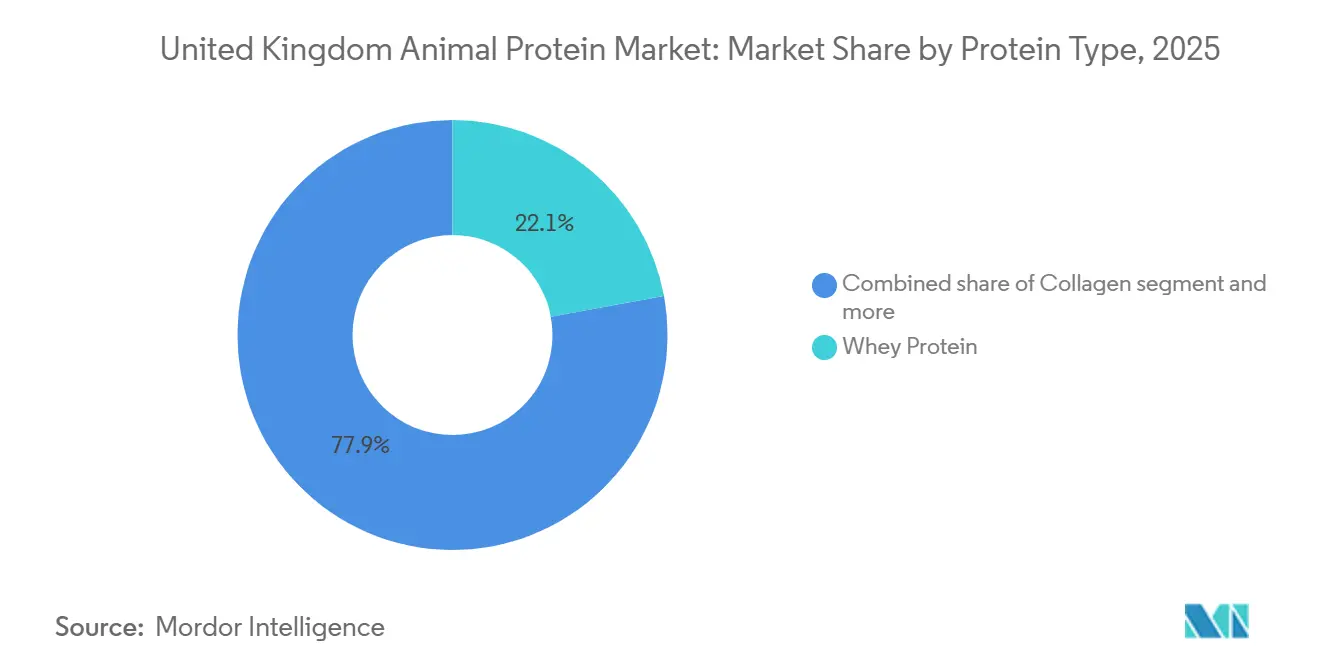

- By protein type, whey protein captured a 22.09% United Kingdom animal protein market share in 2025, while collagen is forecast to expand at a 5.36% CAGR through 2031.

- By category, conventional formats accounted for 76.10% of the United Kingdom animal protein market size in 2025; organic variants are advancing at a 7.79% CAGR.

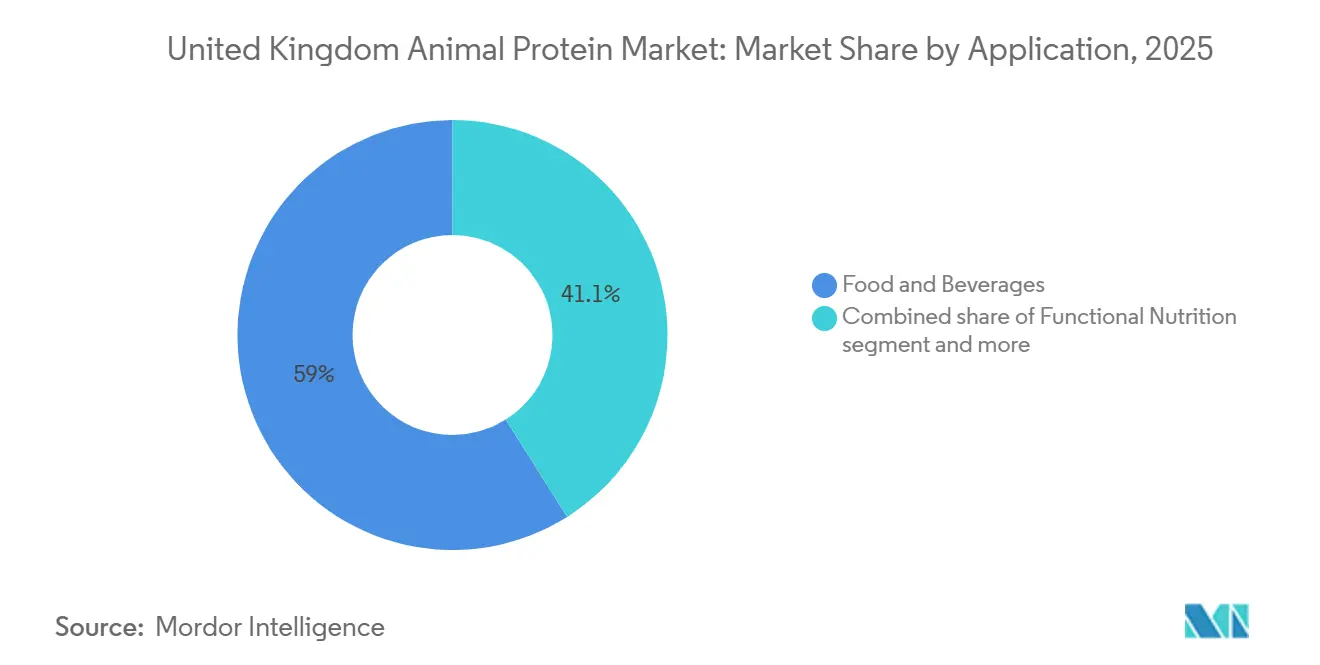

- By application, food and beverages led with 58.95% of value in 2025, but functional nutrition is projected to grow at 6.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Animal Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in convenient and ready-to-eat protein-fortified foods | +1.2% | National, concentrated in Greater London and South East England | Medium term (2-4 years) |

| Growth of the sports and performance nutrition sector | +1.0% | National, with higher penetration in urban centers | Short term (≤ 2 years) |

| Expansion of functional and specialty foods and beverages | +0.9% | National | Medium term (2-4 years) |

| Aging population and clinical nutrition needs | +0.8% | National, pronounced in South West and Wales | Long term (≥ 4 years) |

| Innovation in ingredient processing technologies | +0.7% | National, led by manufacturing hubs in North West England | Medium term (2-4 years) |

| Shift toward clean-label, ethically sourced ingredients | +0.6% | National, strongest in Scotland and South East England | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in convenient and ready‑to‑eat protein‑fortified foods

The increasing demand for convenient and ready-to-eat protein-fortified foods is driving the UK animal protein ingredients market. Busy lifestyles, urbanization, and health awareness are prompting consumers to choose products combining high-quality protein with convenience, such as protein-enriched snacks, beverages, meal replacements, and ready-to-eat meals. Animal-derived proteins like whey, casein, and collagen are preferred for their high biological value, functional versatility, and ability to enhance satiety and muscle support. Food manufacturers are leveraging these ingredients to create on-the-go formats that meet nutritional and functional needs, reinforcing the role of animal proteins in this growing segment. According to the UK National Diet and Nutrition Survey (NDNS) in 2023, convenient, ready-to-eat foods accounted for 51% of energy intake in adults and 68% in children, highlighting a strong market for protein-fortified formats [1]Source: Gov.UK, "Processed foods and health: SACN's rapid evidence update summary", gov.uk. By fortifying meals, snacks, and beverages with whey, casein, or collagen, manufacturers can address protein adequacy and cater to health-conscious consumers while maintaining convenience, taste, and texture. The rising adoption of protein-enriched foods continues to drive growth in the UK animal protein ingredients market.

Growth of the sports and performance nutrition sector

The growth of the sports and performance nutrition segment is driving the UK animal protein ingredients market. Increasing consumer focus on fitness, muscle recovery, and wellness is boosting demand for protein-enriched products like shakes, bars, powders, and functional foods. Animal-derived proteins, such as whey, casein, and collagen, are preferred due to their high biological value, rapid digestibility, and complete amino acid profiles, which support muscle protein synthesis and recovery. Between November 2023 and November 2024, 63.7% of adults met the Chief Medical Officers’ guidelines of 150 minutes or more of moderate-intensity physical activity per week, equating to about 30 million adults in England[2]Source: Sport England Organization, "Record numbers playing sport and taking part in physical activity", sportengland.org. This large, active population sustains demand for protein-rich formulations, encouraging manufacturers to innovate and expand their animal protein offerings. As fitness and wellness trends grow, the sports nutrition segment is expected to remain a key driver of the UK animal protein ingredients market.

Expansion of functional and specialty foods and beverages

The expansion of functional and specialty foods and beverages is driving growth in the UK animal protein ingredients market, as consumers increasingly seek products that offer additional health benefits beyond basic nutrition. Animal-derived proteins such as whey, casein, and collagen are being incorporated into functional beverages, fortified snacks, and specialty foods to deliver benefits like muscle support, joint health, skin wellness, and improved satiety. This trend is fueled by health-conscious consumers who view protein-enriched functional products as a convenient way to integrate wellness into daily routines. Consumer adoption data highlights the scale of this opportunity: around 49% of UK consumers reported consuming some type of functional beverage in the last three months, and this rises to 62% among active adults aged 18–44 in 2025 [3]Source: Glanbia Nutritionals, "Emerging European Functional Beverage Trends for 2025", glanbianutritionals.com. This demonstrates a particularly strong market among younger, health-focused demographics, emphasizing the appeal of protein-fortified functional offerings. Manufacturers are responding by innovating with high-quality animal protein ingredients in formats ranging from ready-to-drink shakes to protein-enriched snacks, positioning functional and specialty products as a key growth driver for the UK animal protein market.

Aging population and clinical nutrition needs

The UK's aging population is driving increased demand for high-quality protein in medical nutrition, elderly care, and home-recovery settings. Sarcopenia, or age-related muscle loss, impacts approximately 10% of UK adults over the age of 70, prompting clinical guidelines to recommend a daily protein intake of 1.2 grams per kilogram of body weight, significantly higher than the 0.8 grams per kilogram standard for younger adults. NHS dietitians are prescribing whey-protein isolates and casein hydrolysates more frequently for post-surgical recovery and chronic disease management, as these proteins provide higher leucine content and better digestibility compared to plant-based alternatives. This trend is further supported by government policy, with the Department of Health and Social Care's 2024 guidance on malnutrition prevention in care homes advocating for protein-fortified meals and snacks, thereby establishing a stable institutional market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from plant and cultivated proteins | -0.9% | National, most pronounced in Greater London and urban centers | Short term (≤ 2 years) |

| Increasing lactose intolerance limiting dairy-based animal proteins | -0.5% | National | Medium term (2-4 years) |

| Consumer skepticism towards insect protein | -0.4% | National | Long term (≥ 4 years) |

| Raw material price volatility | -0.5% | National, with acute impact on dairy and egg processors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying competition from plant and cultivated proteins

Plant-based and cultivated protein alternatives are gaining market share in categories traditionally dominated by animal proteins, prompting established players to compete on price and functionality. These alternatives are nearing cost parity with conventional dairy proteins as fermentation processes scale, posing a challenge to the profit margins of traditional suppliers. Although cultivated meat is not yet commercially available in the UK, it received favorable coverage in The Times and Financial Times during 2025, influencing consumer expectations that animal-free products may soon rival or surpass the sensory qualities of conventional offerings. A study published in Nature in 2024 highlighted that while plant proteins generally have lower levels of essential amino acids compared to animal proteins, fortification strategies are closing the nutritional gap, particularly for lysine and methionine. This convergence diminishes the functional advantage historically held by animal proteins, pushing suppliers to focus on differentiation through bioavailability, taste, and sustainability rather than solely on protein content.

Increasing lactose intolerance limiting dairy‑based animal proteins

Lactose intolerance affects approximately 5% of the UK population, limiting the potential market for whey, casein, and milk-protein concentrates that contain residual lactose even after processing. Although this prevalence is lower compared to East Asian or African populations, it still constitutes a significant segment that prefers lactose-free or plant-based alternatives. This limitation is further exacerbated by self-diagnosis, as many consumers avoid dairy proteins based on perceived intolerance rather than clinically confirmed cases. According to NHS guidance, this behavior often stems from confusion between lactose intolerance and milk-protein allergy. As a result, the lactose-averse segment effectively extends beyond the 5% clinical prevalence, posing challenges for dairy-based ingredients across various application categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Type: Collagen Leads Growth as Whey Dominates Volume

Whey protein accounted for 22.09% of the United Kingdom animal-protein market in 2025, highlighting its established role in sports nutrition, infant formula, and bakery fortification. Collagen is projected to grow at a CAGR of 5.36% through 2031, marking the fastest growth among all protein types. This growth is driven by its use in beauty-from-within supplements, joint-health beverages, and clinical-recovery formulations. Casein and caseinates are utilized in niche applications such as processed cheese and high-protein bars, where their slow-digestion properties support satiety-related claims.

Egg protein remains primarily used in bakery and confectionery products; however, supply disruptions caused by avian influenza outbreaks in late 2024 led some formulators to replace it with whey or pea isolates. Gelatin competes with collagen in gummy vitamins and pharmaceutical capsules, but its growth is limited by increasing consumer preference for vegetarian alternatives such as pectin and carrageenan. The segmentation of protein types reveals a clear division: commodity proteins like whey and casein compete based on price and functional performance, while collagen and specialty proteins focus on differentiation through bioavailability and health benefits.

By Category: Organic Gains Momentum Despite Conventional Dominance

Conventional animal proteins accounted for 76.10% of the market in 2025, supported by cost advantages and well-established supply chains catering to mass-market food and beverage applications. In contrast, organic variants are projected to grow at a CAGR of 7.79% through 2031, marking the fastest growth rate within the category segmentation. Organic whey and casein are increasingly used in premium infant formulas and sports-nutrition powders, where brands utilize certification logos to justify price premiums of 25% to 35% over conventional alternatives.

However, the organic segment faces challenges such as limited farmland availability and higher feed costs, which hinder supply scalability. Regulatory oversight by the Food Standards Agency, requiring clear labeling of organic status and prohibiting misleading claims, strengthens consumer trust in certified products. This category division highlights a two-speed market: volume growth in conventional proteins driven by cost-sensitive applications, and value growth in organic proteins driven by premiumization and sustainability considerations.

By Application: Functional Nutrition Outpaces Food and Beverages

In 2025, food and beverage applications accounted for 58.95% of the demand, encompassing bakery fortification, ready-to-eat meals, dairy alternatives, breakfast cereals, condiments, sauces, confectionery, and ready-to-cook products. These products utilize whey isolates, egg whites, and caseinates to enhance texture, shelf life, and nutritional value. Functional nutrition, which includes baby food and infant formula, elderly nutrition, medical nutrition, and sports/performance nutrition, is projected to grow at a CAGR of 6.14% through 2031, marking the fastest growth rate among application segments.

Personal care and cosmetics represent a smaller but high-margin application area, with marine collagens sourced from Mowi Scotland's certified salmon farms being used by ingredient formulators. While animal feed falls outside the scope of human nutrition, it utilizes lower-grade protein fractions and by-products, contributing to circular-economy models for processors. The application segmentation highlights that although food and beverage volumes dominate, the faster growth and higher margins of functional nutrition are influencing supplier priorities and R&D investments.

Geography Analysis

The South-East and Greater London account for the largest share of spending, driven by higher disposable incomes and a dense retail presence. The concentration of gyms and premium coffee chains in urban boroughs further supports the consumption of sports and functional protein products. In Greater London, the market share for whey in the United Kingdom's animal protein market remains above the national average, reflecting strong penetration among fitness-focused consumers.

Northern England and the Midlands show moderate adoption levels but lead in processing capacity. The presence of Arla’s innovation center and Müller’s Skelmersdale expansion in the North-West enhances localized supply, reducing freight costs and carbon footprints. Organic protein penetration in these regions is lower compared to the South-East; however, Soil Association certifications are increasing rapidly among dairy farms in Yorkshire.

The South-West and Wales are emerging as the fastest-growing regions due to aging demographics. Both regions have a population aged 65 and above exceeding 22%, compared to the national average of 18.7% in 2024. Care homes and NHS trusts in these areas are increasingly sourcing high-leucine medical-nutrition shakes, driving demand for collagen and milk protein. Retailers in Cardiff and Bristol report double-digit growth in collagen beverages marketed for joint health, highlighting the influence of demographic trends.

Competitive Landscape

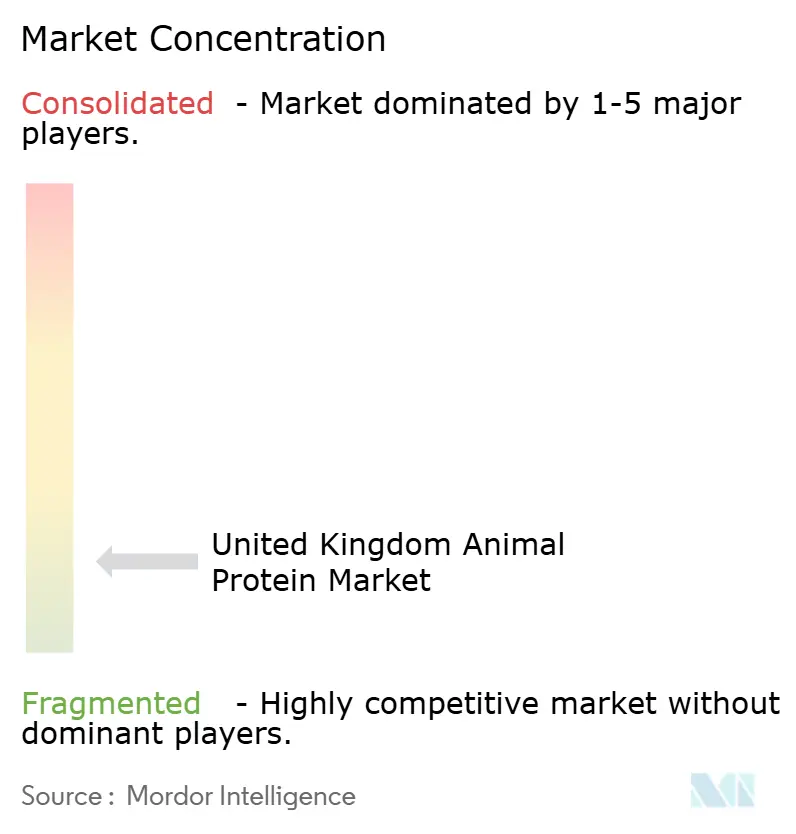

The United Kingdom animal-protein market is marked by low concentration, with significant fragmentation across dairy cooperatives, meat processors, marine-protein specialists, and ingredient traders. No single company dominates the market, with no player holding more than a 15% share. Additionally, the top five companies collectively account for less than 40% of total revenue. This fragmented structure creates opportunities for regional processors and niche innovators to coexist alongside multinational ingredient suppliers, fostering a competitive and diverse market environment.

Growth opportunities in the market are centered around high-value products such as lactose-free whey isolates, marine collagens with verified sustainability credentials, and organic egg proteins. These products command premium pricing due to their specialized nature but require substantial investments in advanced processing technologies. For example, lactose-free whey isolates and marine collagens necessitate capital-intensive upgrades to meet quality and sustainability standards. Such innovations are increasingly critical as consumer demand shifts toward products with added health benefits and environmental considerations.

Technology adoption is emerging as a key competitive differentiator in the market. Companies are leveraging advanced processes to enhance efficiency and reduce environmental impact. For instance, Arla Foods Ingredients introduced cross-flow microfiltration in 2024, achieving 95% protein purity in whey isolates while reducing water consumption by 18%. This not only lowered production costs but also minimized the environmental footprint. Looking ahead, the competitive landscape is expected to consolidate modestly by 2031, with mid-tier processors either acquiring niche capabilities or transitioning to plant-protein portfolios. Meanwhile, leading players are likely to focus on process innovations to sustain margins in a market characterized by increasingly fragmented demand.

United Kingdom Animal Protein Industry Leaders

-

Darling Ingredients Inc.

-

Glanbia PLC

-

Arla Foods Ingredients Group

-

Fonterra Co-operative Group Ltd

-

FrieslandCampina Ingredients

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Arla Foods Ingredients introduced a range of high-protein dairy and whey concepts at Fi Europe 2025, highlighting how its milk and whey protein ingredients can support product innovation for health-conscious consumers. The company showcased five new application ideas: a high-protein transparent yoghurt, a drinking yoghurt containing 25 g of hydrolysed whey protein per serving, a carbonated whey-based Milky Spark drink, a gluten-free high-protein cookie, and a high-protein brownie. Each product combines taste with functional nutrition.

- June 2025: The premium sports nutrition brand Isopure by Glanbia launched in the UK, introducing two key products: Isopure Whey Protein Isolate and Isopure Collagen. These products are developed with a minimal-ingredients approach, containing only essential components without artificial additives or fillers.

United Kingdom Animal Protein Market Report Scope

Casein and Caseinates, Collagen, Egg Protein, Gelatin, Insect Protein, Milk Protein, Whey Protein are covered as segments by Protein Type. Animal Feed, Food and Beverages, Personal Care and Cosmetics, Supplements are covered as segments by End User.

By Protein Type

| Casein and Caseinates |

| Collagen |

| Egg Protein |

| Gelatin |

| Insect Protein |

| Milk Protein |

| Whey Protein |

| Other Animal Protein |

By Category

| Conventional |

| Organic |

By Application

| Animal Feed | |

| Personal Care and Cosmetics | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Products | |

| RTE/RTC Food Products | |

| Dietary Supplements | |

| Others | |

| Functional Nutrition | Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition | |

| Sport/Performance Nutrition |

| By Protein Type | Casein and Caseinates | |

| Collagen | ||

| Egg Protein | ||

| Gelatin | ||

| Insect Protein | ||

| Milk Protein | ||

| Whey Protein | ||

| Other Animal Protein | ||

| By Category | Conventional | |

| Organic | ||

| By Application | Animal Feed | |

| Personal Care and Cosmetics | ||

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Products | ||

| RTE/RTC Food Products | ||

| Dietary Supplements | ||

| Others | ||

| Functional Nutrition | Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms