Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

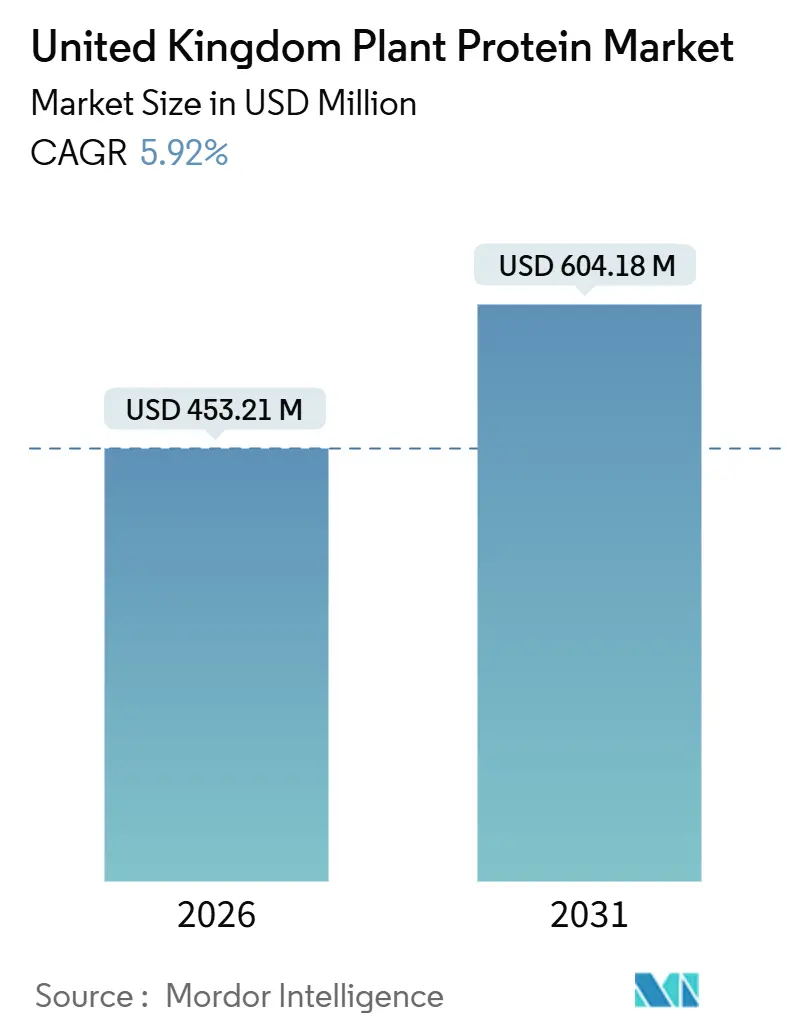

| Market Size (2026) | USD 453.21 Million |

| Market Size (2031) | USD 604.18 Million |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

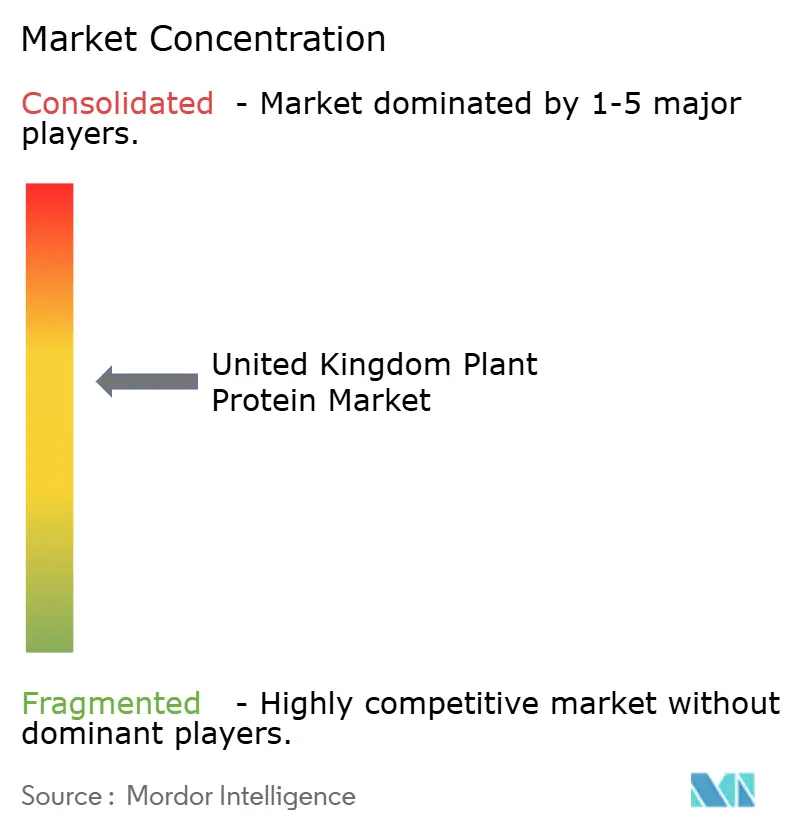

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Plant Protein Market Analysis by Mordor Intelligence

The United Kingdom plant-based protein market size was valued at USD 453.21 million in 2026 and is expected to grow to USD 604.18 million by 2031, registering a CAGR of 5.92% during the forecast period. This moderate growth follows a period of rapid expansion characterized by numerous brand launches and increased retailer shelf space. Collaborative efforts between ingredient suppliers and cereal cooperatives have streamlined development cycles for advanced texturates and high-dispersion isolates, enabling brand owners to simplify formulations and reduce capital expenditures. Additionally, updated allergen regulations introduced by the Food Standards Agency (FSA) in March 2025 have imposed stricter cross-contact controls, increasing compliance costs and intensifying consolidation pressures on small and mid-sized manufacturers.

Key Report Takeaways

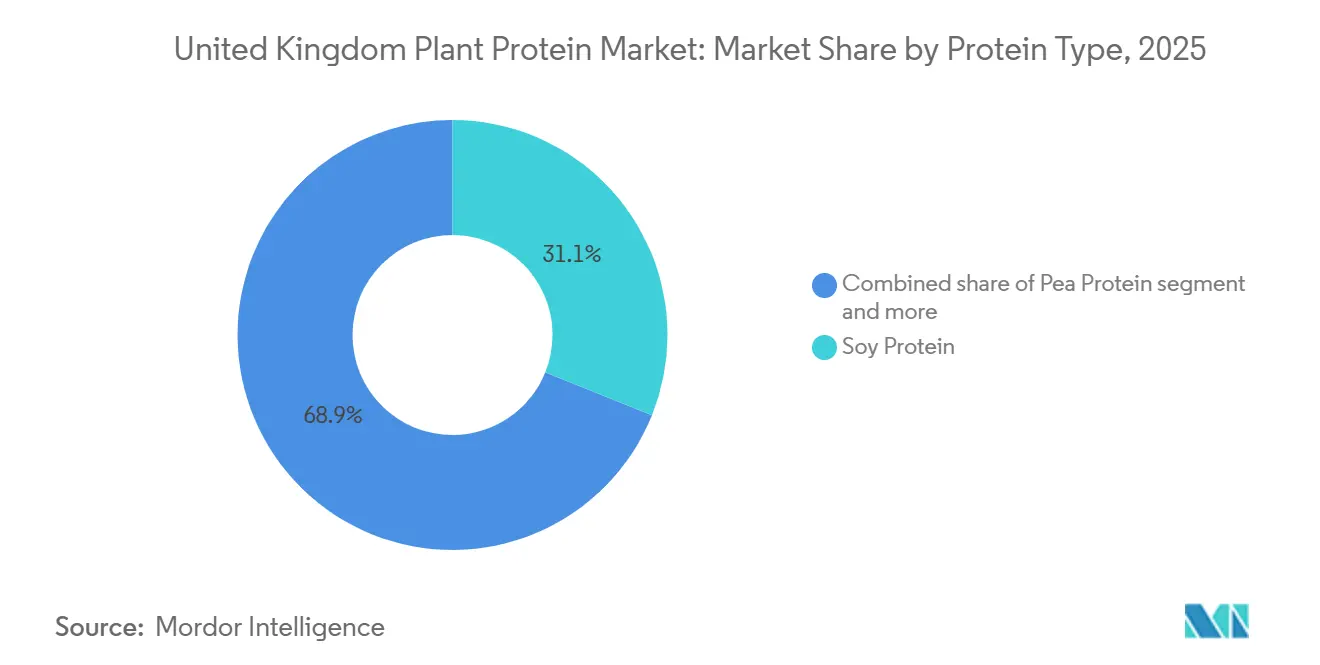

- By protein type, soy led with 31.09% share in 2025 while pea protein is poised for a 6.36% CAGR through 2031 as the fastest-growing segment across the UK plant-based protein market.

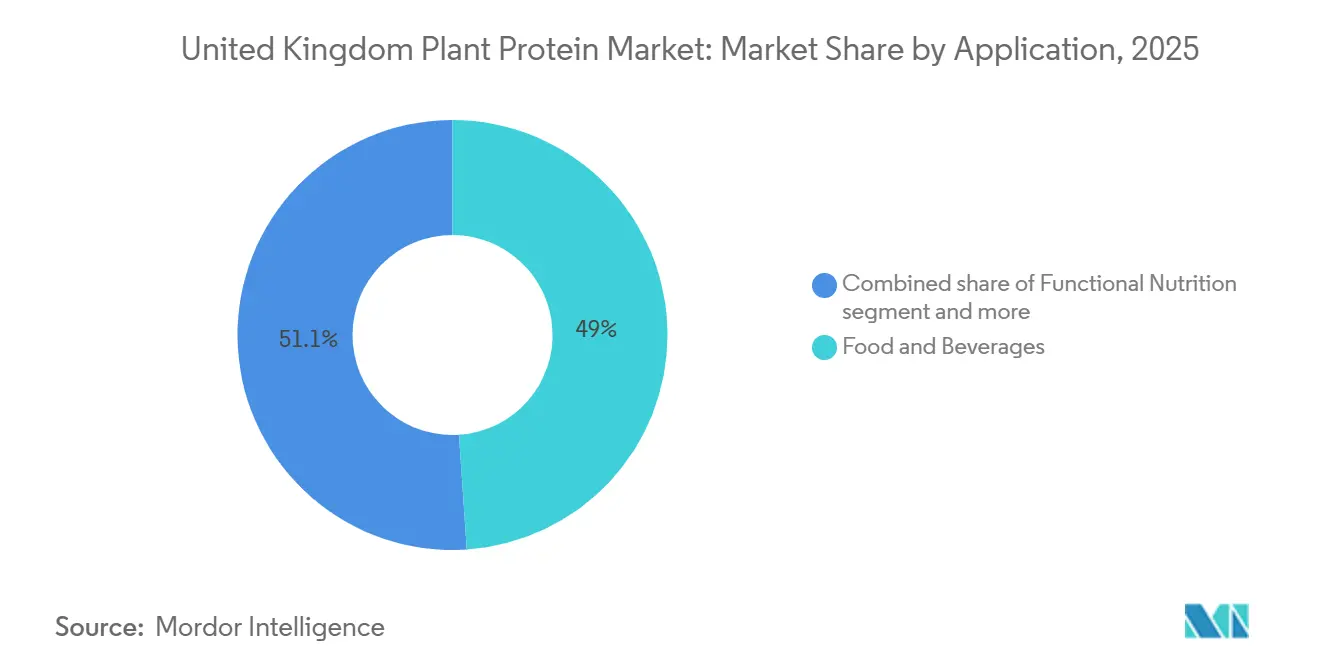

- By application, food and beverages accounted for 48.95% revenue share in 2025, whereas functional nutrition products are on track for a 7.14% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Plant Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong shift toward plant-based, vegan, and flexitarian lifestyles | +1.2% | United Kingdom-wide, with higher penetration in urban centers (London, Manchester, Edinburgh) | Medium term (2-4 years) |

| Consumer preferences for clean-label and digestible products | +0.9% | United Kingdom national, aligned with FSA labeling reforms | Short term (≤ 2 years) |

| Rising demand for lactose-free protein alternatives | +0.7% | United Kingdom national, particularly among millennials and Gen Z cohorts | Short term (≤ 2 years) |

| Domestic pulse acreage expansion post-Brexit subsidies | +0.5% | England and Scotland (primary arable regions under DEFRA/Scottish Government schemes) | Long term (≥ 4 years) |

| Technological advancements in protein extraction and processing | +1.0% | United Kingdom manufacturing hubs; European supply chain integration | Medium term (2-4 years) |

| Rising innovation in new plant protein sources | +0.8% | United Kingdom research and development centers and ingredient suppliers; global innovation transfer | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong shift toward plant-based, vegan, and flexitarian lifestyles

The growing adoption of plant-based, vegan, and flexitarian lifestyles is a significant factor driving the expansion of the UK plant protein ingredients market. Increasing consumer awareness regarding health, sustainability, and ethical concerns is encouraging individuals to reduce or replace animal protein with plant-based alternatives. Manufacturers are focusing on innovations to enhance taste, texture, and digestibility, making plant-based products more appealing to a wider audience. The UK’s vegan population has reached 2.5 million, accounting for 4.7% of adults adhering to a plant-based diet. This marks a substantial increase of 1.1 million individuals between 2023 and 2024, highlighting the rapid growth of plant-focused consumer groups [1]Source: Vegconomist, "UK Vegan Population Estimated to Have Risen by 1.1 Million in a Year", vegconomist.com. The rising popularity of flexitarian and vegan lifestyles is further boosting demand for high-quality plant protein ingredients such as pea, fava bean, soy, and rice protein. This shift positions the UK as a dynamic and fast-growing market for plant-based formulations. Additionally, this consumer trend supports not only volume growth but also drives innovation in functional, clean-label, and fortified plant-based products.

Consumer preferences for clean-label and digestible products

The increasing consumer preference for clean-label and easily digestible products is a key factor driving the UK plant protein ingredients market. Modern consumers are prioritizing ingredient transparency, minimal processing, and natural formulations, favoring products that are free from artificial additives, stabilizers, and unnecessary fillers. Plant protein ingredients such as pea, fava bean, rice, and soy isolates or concentrates align well with these preferences, offering high protein content, functional versatility, and enhanced digestibility in a clean-label format. In response, manufacturers are developing plant-based foods and beverages that combine nutritional benefits with simplified ingredient lists, appealing to health-conscious and ethically aware consumers. Consumer data highlights the significance of this trend: as of 2023, six out of ten UK consumers reported increased attention to ingredient listings over the past year, according to Puratos Company reports [2]Source: Puratos, "What drives consumers to clean-label foods?", puratos.co.uk . This demonstrates a growing segment of the population actively evaluating products based on transparency and digestibility, driving demand for plant protein ingredients that meet clean-label and functional criteria. As a result, this trend is fostering product innovation and adoption across various plant-based categories, including beverages, snacks, and meat and dairy alternatives, thereby strengthening the UK plant protein market.

Rising demand for lactose-free protein alternatives

The increasing demand for lactose-free protein alternatives is a key factor driving the growth of the UK plant protein ingredients market. Rising awareness of lactose intolerance, digestive sensitivities, and dairy-related allergies has led consumers to opt for protein sources that are naturally free from lactose. Plant proteins such as pea, soy, fava bean, and rice isolates provide high-quality protein without lactose, making them suitable for applications in beverages, dairy alternatives, protein powders, and fortified snacks. Beyond being lactose-free, these ingredients offer flexibility for clean-label formulations and functional uses, aligning with the nutritional and sensory preferences of health-conscious consumers. As of 2024, approximately one in every 10 older children and adults in the UK is estimated to have lactose intolerance, representing a significant target demographic for lactose-free protein solutions[3]Source: Bupa, "Lactose intolerance", bupa.co.uk. This expanding consumer base is driving the adoption of plant-based proteins as a viable alternative to whey or milk-derived proteins. As a result, the demand for lactose-free, plant-based protein ingredients is fostering innovation, product development, and market growth across categories such as beverages, bakery, dairy alternatives, and nutritional supplements in the UK.

Domestic pulse acreage expansion post-Brexit subsidies

The UK Agricultural Transition Plan's move from area-based Basic Payments to environmental land management schemes and productivity grants has changed financial incentives for farmers. This shift may encourage the integration of legumes into agroecological rotations due to their soil nitrogen benefits and contributions to biodiversity. According to 2024 data on agriculture in the United Kingdom, pulse acreage remains limited. Yield trends and regional distribution indicate that domestic production is currently insufficient to meet the demands of UK plant-based protein manufacturing at scale, maintaining reliance on imports for soy and pea protein concentrates. The long-term impact will depend on the continuity of policies, farmer participation in environmental schemes, and investments in domestic processing infrastructure, such as cleaning, milling, fractionation, and protein extraction, to retain value within the country rather than exporting raw crops.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility | -0.8% | United Kingdom national; global commodity market exposure (soy, pea, wheat) | Short term (≤ 2 years) |

| Taste, texture, and sensory limitations | -1.1% | United Kingdom consumer markets; product development and reformulation cycles | Medium term (2-4 years) |

| Allergenicity and labeling hurdles | -0.4% | United Kingdom regulatory environment (FSA compliance); manufacturing and foodservice | Short term (≤ 2 years) |

| Higher production costs compared to conventional proteins | -0.9% | United Kingdom manufacturing and supply chain; competitive pricing pressure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Taste, texture, and sensory limitations

Sensory parity gaps remain a significant barrier to adoption, with systematic reviews identifying taste, flavor, and texture as key factors driving low acceptance of many plant-based analogs. Commonly reported issues in consumer studies include off-flavors (such as beany or bitter notes), dryness, and inconsistent texture. Astringency, characterized by mouthfeel dryness and roughness, poses a particular challenge for legume proteins. Research conducted in December 2025 highlighted neural and cellular mechanisms involved in the perception of plant protein astringency and validated processing methods, such as polyphenol removal, heat treatment, and enzymatic hydrolysis, that reduce astringency markers and enhance consumer acceptance. Consumer segment heterogeneity further complicates product development. Flexitarians and environmentally conscious consumers are more willing to accept sensory compromises, whereas meat-eaters demand closer sensory parity with animal-based products. This necessitates a balance between broad market appeal and targeted positioning. Additionally, shelf-life considerations introduce further challenges, as sensory quality can degrade over time due to lipid oxidation, color changes, and texture deterioration. Addressing these issues often requires innovations in packaging and formulation, such as the use of antioxidants or modified atmospheres, which may conflict with clean-label objectives.

Allergenicity and labeling hurdles

Soy, peanuts, tree nuts, gluten-containing cereals, and lupin are classified as declarable allergens under UK law. The FSA's March 2025 guidance requires clear emphasis on these allergens within ingredient lists (e.g., bold or capitalized text), accurate allergen information for non-prepacked foods, and stringent cross-contact controls in manufacturing and foodservice operations. Manufacturers face operational challenges when managing shared facilities that process both plant-based and allergen-containing products. These challenges necessitate validated cleaning protocols, dedicated production lines or scheduling, and detailed supplier allergen specifications to prevent the presence of undeclared allergens. Reformulating products to exclude major allergens, such as replacing soy with pea or fava, presents technical difficulties in matching functional properties and may lead to increased ingredient costs. Additionally, "free-from" product positioning requires rigorous testing and robust supply chain controls to validate claims. Non-compliance with allergen regulations can result in enforcement actions by local authorities, product recalls, reputational damage, and consumer safety incidents. These regulatory requirements add complexity, potentially slowing innovation and delaying market entry for new plant-protein formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Type: Pea Protein Gains on Soy Dominance

Soy protein accounted for 31.09% of the UK market in 2025while pea protein is poised for a 6.36% CAGR through 2031 as the fastest-growing segment across the United Kingdom plant-based protein market, driven by its long-standing use in meat analogs, dairy alternatives, and protein fortification applications. Its functional properties, such as emulsification, gelation, and water-holding capacity, along with cost competitiveness supported by global supply chains, have contributed to its market dominance. Wheat protein (gluten) retains a niche position due to its viscoelastic properties, which enable the creation of fibrous meat-analog textures. However, its allergenic nature (gluten-containing cereals are classified as declarable allergens under FSA regulations) limits its market to non-celiac consumers, restricting broader adoption despite its functional benefits.

Potato and rice proteins are favored for hypoallergenic formulations and neutral sensory profiles, making them suitable for applications in beverages, infant formula, and medical nutrition, where mitigating off-flavors is essential. However, their lower protein density compared to legume proteins necessitates blending or fortification to meet target specifications. Research published in January 2025 highlights advancements in dry fractionation technologies, enabling the sustainable production of functional, nutritional, and palatable grain legume protein ingredients without relying on heavy solvent use. These developments support UK manufacturers in producing clean-label, lower-impact domestic ingredients while improving economic viability through co-product valorization.

By Application: Functional Nutrition Outpaces Food and Beverages

The food and beverages segment accounted for 48.95% of the market share in 2025. This category includes meat alternatives (such as burgers, sausages, and mince), dairy alternatives (milk, yogurt, cheese), bakery products, beverages, breakfast cereals, condiments, sauces, confectionery, and ready-to-eat products where plant proteins are used as primary or supplementary ingredients. The Functional Nutrition segment is projected to grow at a compound annual growth rate (CAGR) of 7.14% through 2031. In sports nutrition, pea and rice protein blends are gaining traction due to their complete amino acid profiles and rapid absorption.

Within the food and beverages segment, meat and poultry alternatives face challenges in achieving sensory parity with traditional meat products. Systematic reviews identify taste and texture as key barriers to mainstream adoption. Continued innovation in formulation and processing is necessary to improve consumer acceptance, particularly among meat-eaters, as opposed to committed flexitarians. In the animal feed segment, lower-grade plant protein meals and concentrates are used as partial replacements for soy meal in livestock and aquaculture rations. However, this segment operates under distinct quality specifications and pricing dynamics compared to human food-grade proteins. The personal care and Cosmetics segment represents a niche application for plant proteins.

Geography Analysis

The United Kingdom market operates within a European framework influenced by EU Commission initiatives aimed at reducing plant protein deficits. These initiatives focus on increasing domestic production, promoting crop diversification, and expanding processing capacities. Policy measures targeting both feed and human food protein markets may impact UK supply chains through trade flows and regional competition. Scotland's scheduled review of livestock feed controls in October 2024 highlights ongoing regulatory developments that could affect the allocation of plant proteins between animal feed and human food applications, potentially influencing the competitiveness of plant-based alternatives.

Regional production in England and Scotland, particularly for arable crops such as pulses and oilseeds, plays a significant role in determining logistics and processing hub locations. Data from "Agriculture in the United Kingdom 2024" provides insights into hectares cultivated, tonnes produced, yield per hectare, and regional shares, which are critical for evaluating domestic feedstock availability and associated costs. Urban centers like London, Manchester, and Edinburgh show higher penetration of plant-based products, driven by younger demographics, higher education levels, and greater retail and foodservice availability. These factors position urban areas as key growth markets for premium and innovative plant-protein products.

DEFRA's quantitative review in June 2025 on sustainable novel food production will offer regulatory context and sustainability metrics, influencing UK policy support, investment decisions, and lifecycle assessment frameworks for buyers prioritizing ESG credentials. Trade dynamics with the EU and global markets significantly affect ingredient availability and pricing. The UK's reliance on imports for soy and pea protein concentrates exposes the market to global commodity price volatility and trade-related challenges, such as tariffs and logistics issues. These factors contribute to higher input costs compared to domestically produced animal proteins.

Competitive Landscape

The United Kingdom plant protein market demonstrates moderate concentration, with established multinational companies such as ADM, Cargill, Kerry, Roquette, Ingredion, Glanbia, Tate & Lyle, and DSM-Firmenich dominating ingredient supply chains. These companies leverage global sourcing networks, advanced processing capabilities, and application development expertise.

Opportunities exist in emerging categories like plant-based seafood and egg analogs, which are experiencing faster growth despite lower absolute volumes and fewer established players. These segments present potential entry points for agile innovators capable of addressing formulation complexities and overcoming limited consumer familiarity. Technological advancements are driving differentiation in the market. Key areas include fermentation (e.g., ENOUGH's mycoprotein scale-up, which has attracted interest from major meat companies), precision fermentation for novel proteins and fats, advanced texturization techniques such as high-moisture extrusion and shear-cell technology, and clean-label formulation expertise.

Patent activity highlights ongoing innovation in processing technologies. For instance, patent WO2016172418A3 outlines apparatus and process flows for scalable extraction and purification of plant proteins suitable for food applications. Such advancements could be adopted by UK processors or ingredient suppliers to enhance local value addition and improve product quality.

United Kingdom Plant Protein Industry Leaders

-

Archer Daniels Midland Company

-

Cargill Incorporated

-

Ingredion Incorporated

-

Kerry Group PLC

-

Roquette Frères S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: AB Mauri, a prominent supplier of bakery ingredients with an established presence in the UK, has entered into a strategic technical and supply collaboration with Croatian foodtech company Nutris. This partnership aims to develop innovative fava bean-based ingredient solutions for the UK and Ireland. Nutris utilizes an advanced fractionation process to separate fava beans into protein, starch, and fiber fractions, enabling the creation of clean-label, functional plant protein ingredients with enhanced nutritional and performance characteristics.

- November 2024: Atura, through Deltagen UK, launched ATURA FP80 Organic, a high-protein, low-viscosity fava bean protein isolate. This product is designed for use in beverages, dairy alternatives, snacks, and fortified foods, addressing the growing demand for locally sourced, high-quality plant proteins.

- May 2024: Roquette introduced NUTRALYS Fava S900M, its first fava bean protein isolate, signifying a notable expansion of its plant protein portfolio in Europe and North America. This ingredient contains 90% protein and features a clean taste, light color, and robust functional properties, including high gel strength, viscosity control, and stability. These attributes make it suitable for applications in meat substitutes, non-dairy alternatives, and baked goods.

United Kingdom Plant Protein Market Report Scope

Hemp Protein, Pea Protein, Potato Protein, Rice Protein, Soy Protein, Wheat Protein are covered as segments by Protein Type. Animal Feed, Food and Beverages, Personal Care and Cosmetics, Supplements are covered as segments by End User.

By Protein Type

| Hemp Protein |

| Pea Protein |

| Potato Protein |

| Rice Protein |

| Soy Protein |

| Wheat Protein |

| Others Protein |

By Application

| Animal Feed | |

| Personal Care and Cosmetics | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternatives Products | |

| RTE/RTC Food Products | |

| Meat/Poultry/Seafood and Alternatives | |

| Dietary Supplements | |

| Others | |

| Functional Nutrition | Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition | |

| Sport/Performance Nutrition |

| By Protein Type | Hemp Protein | |

| Pea Protein | ||

| Potato Protein | ||

| Rice Protein | ||

| Soy Protein | ||

| Wheat Protein | ||

| Others Protein | ||

| By Application | Animal Feed | |

| Personal Care and Cosmetics | ||

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternatives Products | ||

| RTE/RTC Food Products | ||

| Meat/Poultry/Seafood and Alternatives | ||

| Dietary Supplements | ||

| Others | ||

| Functional Nutrition | Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms