South Africa Paints And Coatings Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

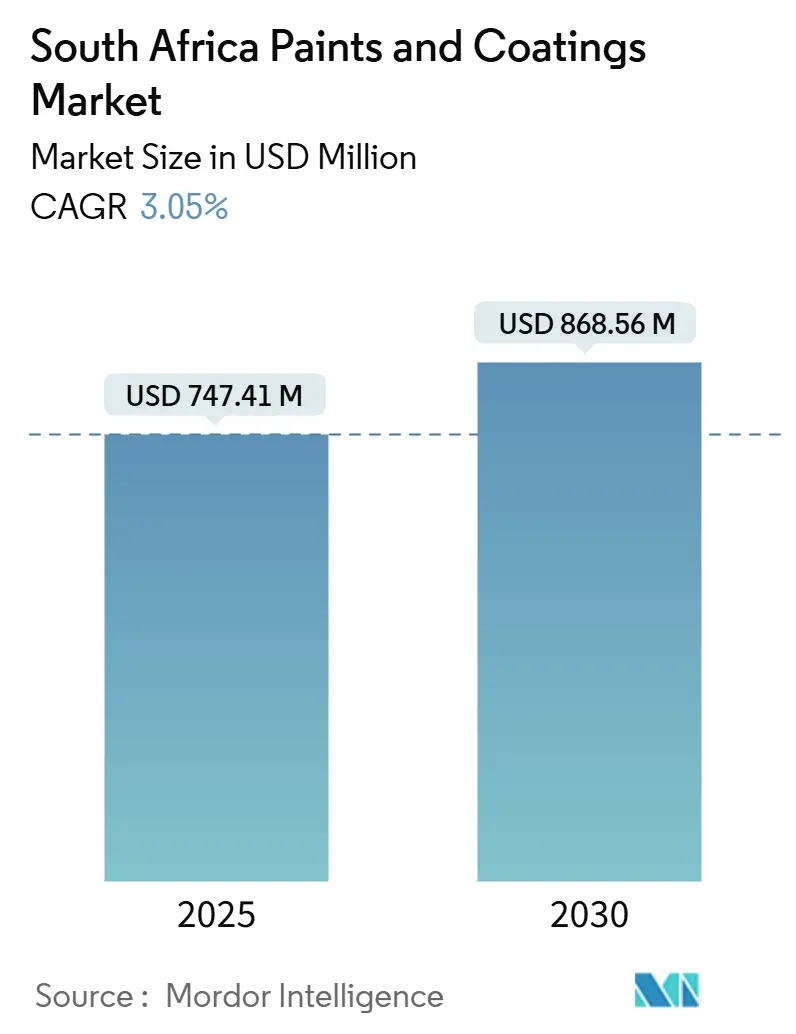

| Market Size (2025) | USD 747.41 Million |

| Market Size (2030) | USD 868.56 Million |

| Growth Rate (2025 - 2030) | 3.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Paints And Coatings Market Analysis by Mordor Intelligence

The South Africa Paints and Coatings Market size is estimated at USD 747.41 million in 2025, and is expected to reach USD 868.56 million by 2030, at a CAGR of 3.05% during the forecast period (2025-2030). Demand benefits from a USD 54.5 billion public-sector infrastructure pipeline, an end to power-supply interruptions, and progressive environmental regulation that accelerates water-borne and bio-based technology adoption. Local OEM vehicle production is scaling up, spurring high-performance refinish demand, while the renewable-energy build-out opens niche opportunities for corrosion-resistant protective systems. Input-cost pressures tied to titanium dioxide volatility and escalating carbon-tax liabilities temper margins, yet they also encourage reformulation and operational efficiencies. Competitive intensity remains pronounced as multinational leaders and well-resourced local firms emphasize sustainable product portfolios, robust distribution, and digital color-matching tools to cultivate customer loyalty.

Key Report Takeaways

- By resin type, acrylic formulations held 38.18% of the South Africa paints and coatings market size in 2024, and polyurethane resins are forecast to grow the fastest at a 3.08% CAGR.

- By technology, water-borne systems captured 50.22% of the South Africa paints and coatings market share in 2024 while advancing at a 4.27% CAGR through 2030.

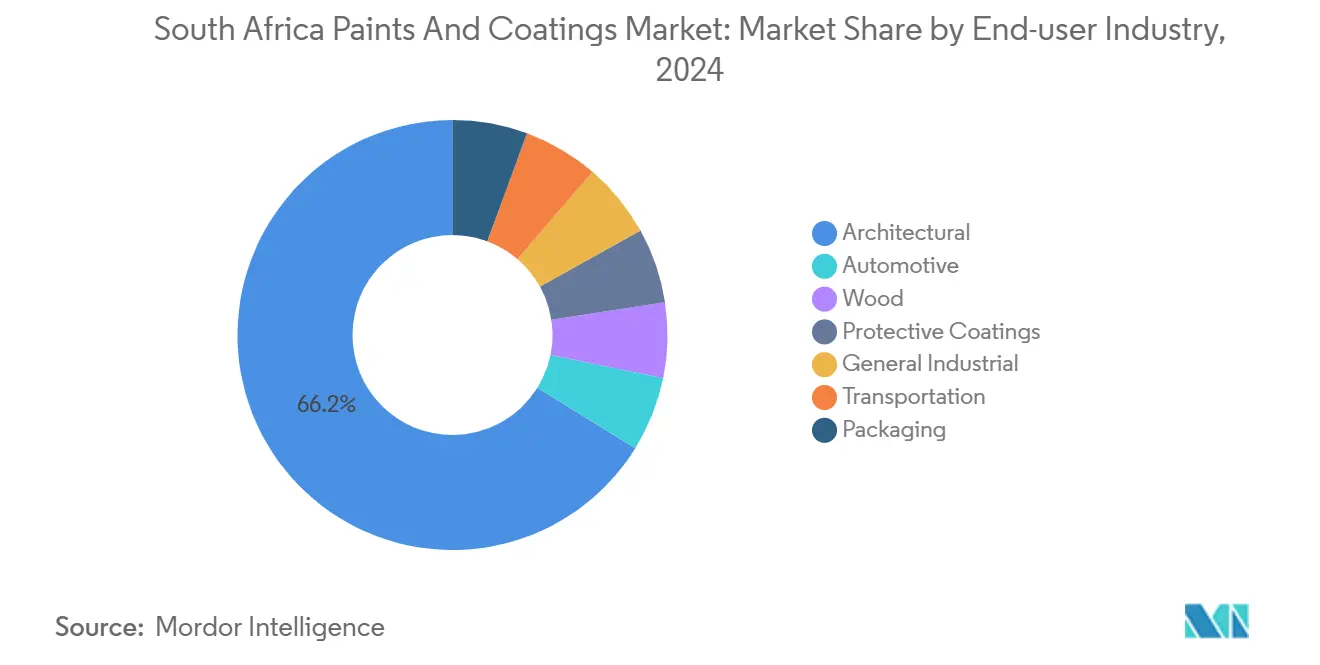

- By end-user industry, automotive applications posted the highest projected growth at a 3.47% CAGR to 2030, whereas architectural coatings retained 66.16% revenue share in 2024.

South Africa Paints And Coatings Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising construction and infrastructure pipeline (2025–2030) | +1.2% | National, concentrated in Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Expanding automotive OEM and aftermarket paint demand | +0.8% | National, centered in Gauteng automotive hub | Medium term (2-4 years) |

| Surge in water-borne and bio-based formulations post-carbon-tax | +0.6% | National, with early adoption in major industrial centers | Short term (≤ 2 years) |

| Growth in renewable-energy assets needing corrosion protection | +0.4% | Northern Cape, Western Cape renewable energy corridors | Long term (≥ 4 years) |

| OEM warranty extension spurring high-performance refinish | +0.3% | National, focused on major metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Construction and Infrastructure Pipeline Drives Protective Coatings Demand

Government commitments totaling USD 54.5 billion through 2027 encompass transport corridors, power generation, and water projects that all require large coating volumes. Municipal wastewater upgrades, such as Cape Town’s ZAR 45 billion program, need chemical-resistant linings, while national highway refurbishments consume high-build alkyd alternatives. Renewable-energy corridors call for UV-stable and anti-corrosive systems that withstand arid conditions. These multipronged programs extend through 2030, ensuring predictable demand even though execution delays and funding constraints could soften annual volumes.

Automotive Sector Expansion Accelerates OEM and Refinish Growth

Vehicle output climbed to 667,399 units in 2024 as BMW, Stellantis, and others invested nearly ZAR 7 billion to expand or retool local plants[1]“South Africa - Automotive,” U.S. Commercial Service, trade.gov. The Automotive Production Development Program’s localization incentives funnel procurement toward domestic coating suppliers that can meet OEM performance specifications. A 13.3 million-unit vehicle parc sustains aftermarket repaint volumes, while prolonged ownership cycles and extended warranties increase the need for higher-end polyurethane clearcoats. Although battery-electric vehicles represent under 1% of new sales, specialized insulative and thermal-management coatings are gaining traction among Tier-1 suppliers.

Water-Borne Formulation Adoption Accelerated by Environmental Compliance

Water-borne systems already dominate with a 50.22% share, and Kansai Plascon has commercialized sub-5 g/L VOC products that align with emerging air-quality norms. Domestic startups such as A-Gain leverage industrial byproduct streams to formulate eco-friendly coatings certified by Agrément South Africa. Market acceptance is accelerating because water-borne chemistries now offer comparable durability, better indoor-air quality, and increasingly competitive cost of application.

Renewable-Energy Infrastructure Creates Specialized Coatings Opportunities

The government targets a 49% renewable share in the power mix by 2030, complemented by a green-hydrogen roadmap that could add 3.6% to GDP[2]Rico Salgmann et al., “Green shipping fuels made in South Africa,” World Bank Blogs, worldbank.org . Northern Cape electrolyzer projects and coastal ammonia bunkering terminals require advanced epoxy and polysiloxane coatings capable of withstanding chemical attack and salt-spray corrosion. Wind-turbine towers and solar tracker systems demand UV-stable polyurethane topcoats that can handle thermal cycling in desert climates. Certification needs and higher technical complexity narrow supplier pools, allowing experienced players to secure premium pricing and long-term service agreements.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ and solvent input prices | -0.9% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Tightening VOC and HAP regulations | -0.4% | National, with stricter enforcement in major metros | Medium term (2-4 years) |

| Load-shedding-related production downtime | -0.2% | National, historically concentrated in industrial hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Titanium Dioxide Price Volatility Pressures Manufacturing Margins

TiO₂ comprises 20-30% of the typical formulation cost, and delivered prices rose 2024-2025 as EU anti-dumping duties redirected Chinese surplus toward Africa. Logistics bottlenecks at Durban and Cape Town ports raised freight surcharges by 12-18%. Limited global producer diversity constrains bargaining power, forcing local manufacturers either to absorb costs or risk market-share erosion if they raise prices. Margin compression diverts funds from research and development and capacity expansion, especially for small and midsize firms.

Environmental Regulations Increase Compliance Costs and Reformulation Requirements

A 90 ppm lead limit became mandatory in May 2025, obliging producers to test every new batch and issue declarations of conformity. VOC emission standards under the National Environmental Management: Air Quality Act require continuous monitoring and annual reporting, entailing capital outlays for abatement systems. Carbon-tax escalation further burdens solvent-based operations. Firms lacking research and development scale or environmental engineers may exit or merge, elevating compliance barriers and potentially reducing customer choice.

Segment Analysis

By Resin Type: Acrylic Dominance Faces Polyurethane Momentum

Acrylic formulations retained 38.18% of the South Africa paints and coatings market share in 2024 because they pair well with water-borne systems and offer superior weatherability for architectural façades. Polyurethane demand is rising at a 3.08% CAGR, mainly from automotive clearcoats, industrial maintenance, and protective topcoats that must resist abrasion, chemicals, and UV degradation. Alkyd volumes are easing as long-drying, high-VOC profiles become untenable under stricter air-quality rules. Epoxy systems hold niche but critical slots in chemical plants, offshore rigs, and potable-water tanks where adhesion and barrier performance outweigh price premiums. Polyester resins sustain a limited foothold in powder-coating lines, while silicones and fluoropolymers address extreme-temperature or anti-graffiti needs.

Polyurethane’s ascent mirrors a market preference for coatings that extend maintenance intervals, thereby reducing lifecycle costs for infrastructure owners and fleet operators. Formulators leverage aliphatic grades for color-fast exterior applications and aromatic grades in factory floors and heavy-equipment primers. As OEM warranties lengthen, collision-repair shops gravitate toward higher-solids polyurethane clearcoats that can restore factory gloss in fewer layers, keeping labor inputs low and throughput high.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Water-Borne Systems Lead a Broad Environmental Transition

Water-borne coatings controlled 50.22% of the South Africa paints and coatings market in 2024 and hold the fastest growth trajectory at a 4.27% CAGR, underscoring regulatory pull and performance parity with solvent-borne equivalents. Solvent-borne products retain share in automotive metallics, marine systems, and certain industrial lines where flow and chemical resistance remain paramount, but continuous solvent-reduction innovations are chipping away at these bastions. Powder coatings carve out volumes in appliances, metal furniture, and vehicle rims, offering zero-VOC credentials and near-100% material utilization. UV-cured coatings are gaining mindshare for plastic parts and flooring because instantaneous curing accelerates production, though adoption is tempered by equipment costs.

Capital expenditure on water-borne scale-up—such as new resin reactors and stainless-steel pipes—presents an entry barrier, favoring incumbents with balance-sheet strength. Technological collaboration with multinational raw-material suppliers accelerates local know-how transfer, enabling domestic firms to supply compliant, performance-verified products without importing finished goods.

By End-User Industry: Architectural Base with Accelerating Automotive Upside

Architectural applications accounted for 66.16% of 2024 revenue thanks to recurring repaint cycles, commercial property refurbishments, and public-sector housing programs. The automotive vertical is set to grow the quickest at a 3.47% CAGR as new OEM lines ramp up and a sizable vehicle parc demands refinishing. Protective-coating volumes rise alongside energy, water, and transport mega-projects, requiring epoxy-polyamide primers and polysiloxane topcoats to mitigate corrosion. Wood-coating demand benefits from a resilient furniture export segment and timber-frame housing trials, while general industrial coatings mirror trends in machinery production and packaging. Transportation coatings for railcars and buses register stable demand, although electrification creates new material compatibility requirements.

Vehicle-parc aging in lower-income segments spurs more frequent refinishing, encouraging distributors to stock faster-curing, weather-resistant polyurethane lines. Meanwhile, indoor-air-quality standards in public buildings are driving low-VOC architectural solutions, nudging brands to expand odor-free emulsion ranges.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Gauteng remains the single largest demand node, combining Johannesburg’s financial district, Pretoria’s administrative hub, and Rosslyn’s automotive cluster into a dense consumption ecosystem spanning OEM coatings, industrial maintenance, and architectural refurbishments. Water-borne demand here is particularly robust because metropolitan air-quality officers enforce VOC caps stringently.

KwaZulu-Natal’s coastal humidity and petrochemical plants create niche corrosion-protection opportunities, while its proximity to the Port of Durban simplifies feedstock imports for nearby manufacturers. Northern Cape’s renewable-energy corridor is an emerging but strategic outlet for polysiloxane, epoxy, and thermally conductive coatings applied to solar trackers, wind towers, and planned green-hydrogen electrolysis units. Eastern Cape’s automotive factories generate predictable OEM volumes, and Limpopo’s mining complexes use heavy-duty protective systems to mitigate acid-mine drainage effects on steel.

Although rural districts exhibit lower per-capita consumption, government-backed housing grants and road resurfacing projects keep baseline architectural and traffic-marking demand intact. Coastal regions, exposed to salt-laden winds, lean toward higher-grade solvent-borne or hybrid polysiloxane topcoats to extend service life.

Competitive Landscape

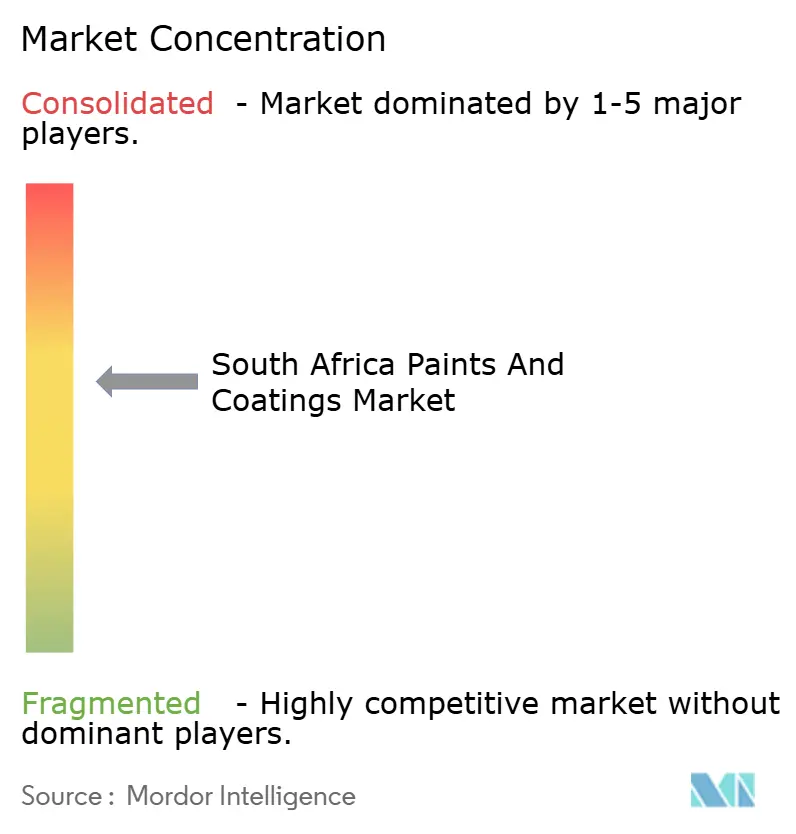

South Africa's paints and coatings market is moderately fragmented. Multinationals such as AkzoNobel (Dulux), PPG, Sherwin-Williams, BASF, and Axalta vie against entrenched local producers, including Kansai Plascon, Atlas Paints, and Dekro Paints, for contracts across retail, industrial, and OEM channels. Acquisition attempts, illustrated by AkzoNobel’s aborted bid for Kansai Paint Africa, signal global players’ appetite for market scale but also reveal antitrust sensitivities. Operational efficiency gains feature prominently; AkzoNobel announced 2,000 global job cuts to streamline supply chains, while BASF equipped its Boksburg plant with onsite solar generation and battery storage to hedge against residual load-shedding.

South Africa Paints And Coatings Industry Leaders

-

Akzo Nobel N.V.

-

PPG Industries, Inc.

-

The Sherwin-Williams Company

-

Atlas Paints

-

Kansai Plascon

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: South Africa’s Minister of Health published regulations capping lead in paint at 90 ppm and requiring declarations of compliance for each batch.

- November 2023: AkzoNobel canceled its plan to acquire Kansai Paint’s African businesses after the South African Competition Tribunal blocked the transaction over monopoly concerns.

South Africa Paints And Coatings Market Report Scope

Paints and coatings are thin materials applied to a surface to safeguard, decorate, or enhance the underlying layer's functionality. Coatings often refer to solvent-based systems, whereas paints typically refer to aqueous systems. They are often applied with a brush, roller, sprayer, or applicator. They are made of resins, pigments, solvents, and other ingredients.

South Africa's paints and coatings market is segmented by resin type, technology, and end-user industry. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types (polyvinyl alcohol, fluoropolymers, etc.). By technology, the market is segmented into water-borne, solvent-borne, powder coatings, and UV Cured Coatings. By end-user Industry, the market is segmented into architectural, automotive, wood, protective coatings, general industrial, transportation, and packaging.

Each segment's market sizing and forecasts are based on value (USD).

| Acrylic |

| Alkyd |

| Epoxy |

| Polyurethane |

| Polyester |

| Other Resin Types |

| Water-borne |

| Solvent-borne |

| Powder Coatings |

| UV Cured Coating |

| Architectural |

| Automotive |

| Wood |

| Protective Coatings |

| General Industrial |

| Transportation |

| Packaging |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyurethane | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder Coatings | |

| UV Cured Coating | |

| By End-User Industry | Architectural |

| Automotive | |

| Wood | |

| Protective Coatings | |

| General Industrial | |

| Transportation | |

| Packaging |

Key Questions Answered in the Report

What is the current value of the South Africa paints and coatings market?

The South Africa paints and coatings market size stands at USD 747.41 million in 2025.

How fast is the market expected to grow through 2030?

The market is projected to record a 3.05% CAGR, reaching USD 868.56 million by 2030.

Which technology segment is expanding the quickest?

Water-borne formulations hold both the largest share and the fastest growth, advancing at a 4.27% CAGR.

Why are polyurethane resins gaining traction?

Polyurethane resins combine superior durability and chemical resistance, making them ideal for automotive clearcoats and industrial maintenance.

What drives demand in the automotive coatings segment?

Rising local vehicle production, extended ownership cycles, and longer OEM warranties are boosting both OEM and refinish coating consumption.

How does environmental regulation affect manufacturers?

Carbon-tax escalation and tighter VOC limits are steering producers toward low-emission, water-borne coatings and raising compliance costs for solvent-based lines.

Page last updated on: