Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

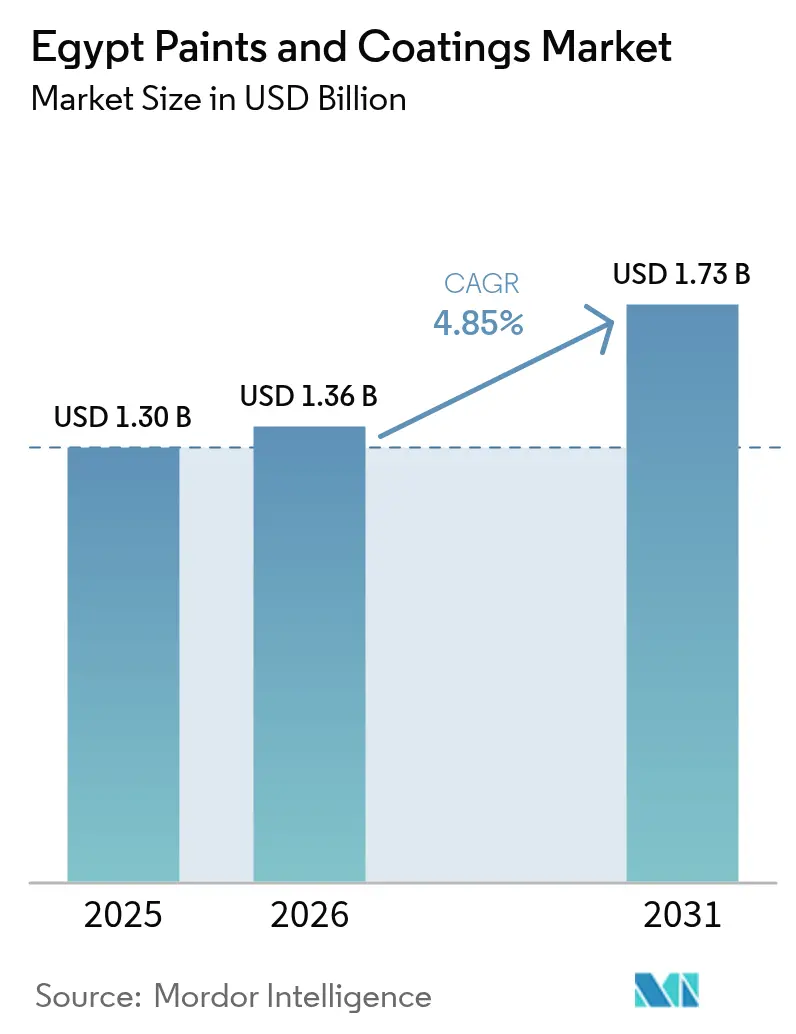

| Base Year Market Size (2025) | USD 1.30 Billion |

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

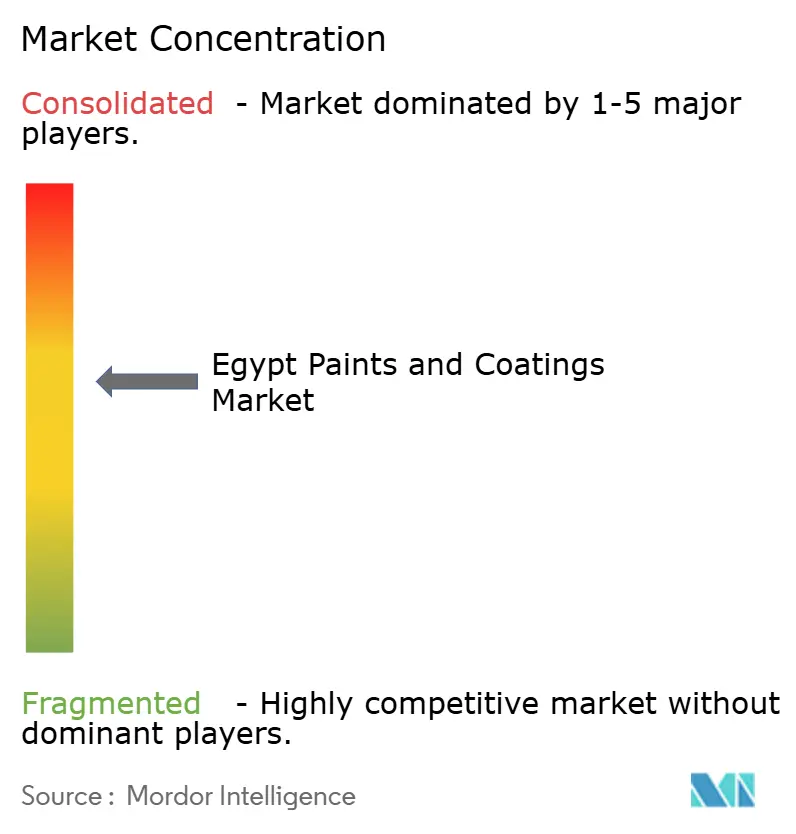

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Paints And Coatings Market Analysis by Mordor Intelligence

The Egypt paints and coatings market size is expected to grow from USD 1.30 billion in 2025 to USD 1.36 billion in 2026 and is forecast to reach USD 1.73 billion by 2031 at 4.85% CAGR over 2026-2031. Robust public-sector spending on housing, transport corridors, and petrochemical complexes anchors demand even as foreign-exchange volatility challenges input costs. Continued rollout of green building rules accelerates the shift toward water-borne technologies, while the petrochemical build-out in the Suez Canal Economic Zone strengthens domestic feedstock supply and underpins industrial coatings uptake. Automotive localization initiatives add incremental volume for OEM refinishing, and research advances using locally sourced silica-fume signal future innovation pathways. Intensifying competition among global multinationals and nimble regional players is spurring capacity expansions, product differentiation, and selective mergers, all reshaping competitive dynamics.

Key Report Takeaways

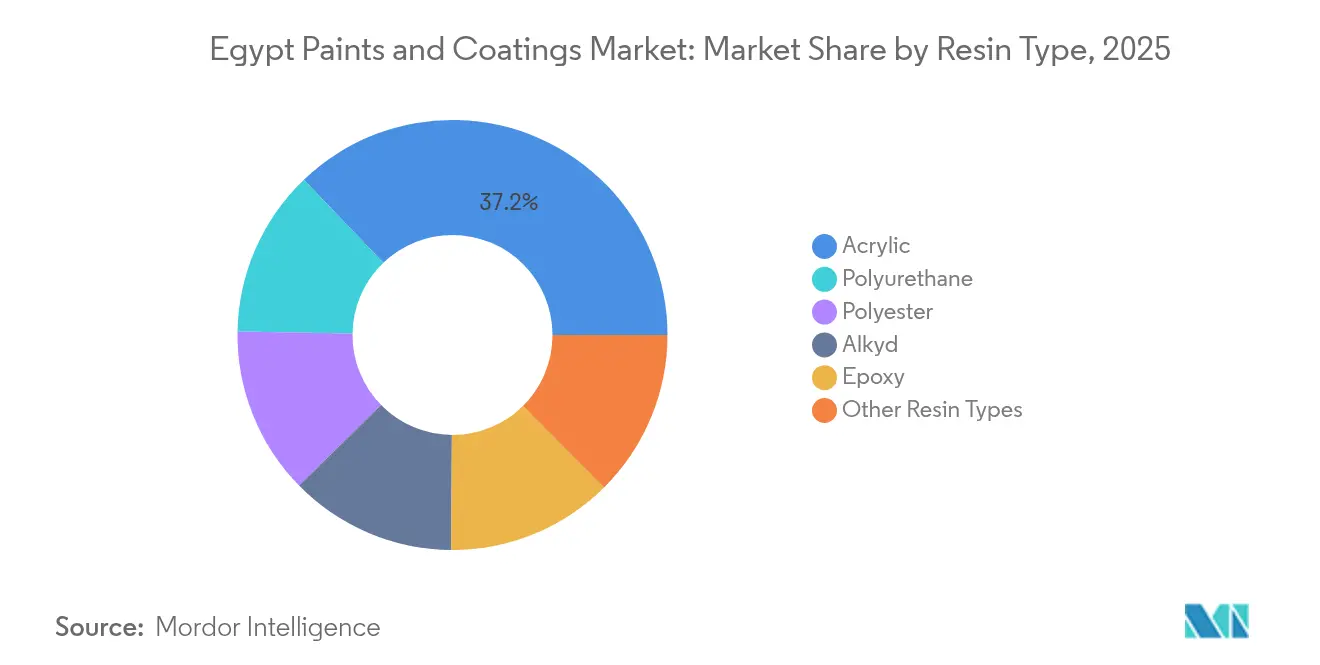

- By resin type, acrylic captured 37.15% of Egypt paints and coatings market share in 2025, and is registering the fastest growth at a 6.15% CAGR through 2031.

- By technology, water-borne systems held 49.55% share of the Egypt paints and coatings market size in 2025, and the segment is projected to expand at a 6.05% CAGR during 2026-2031.

- By end-user industry, architectural applications led with 64.80% revenue share in 2025; protective coatings are forecast to post the highest 5.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential mega-housing boom under New Urban Communities Authority | +1.8% | National, concentrated in New Administrative Capital, New Alamein, New Mansoura | Medium term (2-4 years) |

| Expansion of oil and gas downstream (Midor, Red Sea Petrochem) | +1.2% | Suez Canal Economic Zone, Alexandria, Red Sea governorates | Long term (≥ 4 years) |

| VOC-curbing environmental rules spur water-borne adoption | +0.9% | National, with stricter enforcement in Cairo, Alexandria metropolitan areas | Short term (≤ 2 years) |

| OEM refinishing demand from local-content automotive push | +0.7% | Industrial zones in Giza, Badr, 6th of October City | Medium term (2-4 years) |

| Nano-enhanced antimicrobial coatings using Egyptian silica-fume | +0.4% | National, with research concentration in Cairo universities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Residential Mega-Housing Boom Under New Urban Communities Authority

Government-backed cities such as the New Administrative Capital, New Alamein, and New Mansoura are reshaping Egypt’s urban footprint and fueling a continuous flow of architectural coatings demand. The New Administrative Capital alone encompasses landmark structures—including the Parliament Building and Al-Fatah Al-Aleem Mosque—that require high-performance finishes tailored to desert heat and sand abrasion. Construction schedules spanning 2025-2028 assure steady volumes for interior and exterior paints, primers, and sealers. Demand for heat-reflective and self-cleaning formulations is rising as developers seek energy-efficient building envelopes. Suppliers able to certify low-VOC and high-solar-reflectance products gain procurement preference under Egypt Vision 2030’s sustainability criteria. Parallel housing programs in satellite cities extend the opportunity beyond Cairo, anchoring long-term growth for the Egypt paints and coatings market.

Expansion of Oil and Gas Downstream Operations

A USD 10.9 billion petrochemical complex inside the Suez Canal Economic Zone will host 11 factories that supply key monomers, solvents, and additives used in coatings, reducing import reliance and improving input cost visibility. At the same time, these facilities, along with existing Midor and Red Sea Petrochem projects, need high-build, chemically resistant coatings to safeguard tanks, pipelines, and jetties. Employment creation for 48,000 workers prompts ancillary housing and commercial developments, broadening architectural demand. Egypt’s LNG export hubs at Damietta and Idku generate a fresh need for marine and maintenance coatings that withstand saline environments[1]“Country Analysis Brief: Egypt,” U.S. Energy Information Administration, eia.gov . Combined, these investments create a self-reinforcing cycle of raw-material supply growth and downstream consumption, strengthening the Egypt paints and coatings market.

VOC-Curbing Environmental Rules Spur Water-Borne Adoption

The Egyptian Environmental Affairs Agency enforces stringent VOC ceilings, and the August 2024 launch of Africa’s first carbon market adds a monetary incentive for low-emission products. Public agencies now tender projects that mandate water-borne or other green technologies, accelerating conversion from solvent-borne lines. With half of government capital expenditure earmarked for green projects by 2025, coating suppliers that certify compliance capture priority status. New formulation work integrates locally sourced silica-fume nanoparticles to deliver antimicrobial and heat-reflective benefits, further differentiating water-borne offerings. Rapid regulatory enforcement in Cairo and Alexandria compresses transition timelines and cements water-borne dominance inside the Egypt paints and coatings market.

OEM Refinishing Demand from Local-Content Automotive Push

Geely’s CKD plant in Giza and Stellantis’ Jeep Grand Cherokee L assembly line in Cairo underscore Egypt’s pivot from vehicle importation to local manufacturing. Each unit rolling off these lines consumes multiple coating layers, such as e-coat, primer, base coat, and clear coat, driving factory throughput for high-gloss, scratch-resistant systems. The national automotive strategy favors electric vehicle output, prompting the development of coatings with electromagnetic shielding and battery-thermal-management properties. Component suppliers such as Leoni’s new wiring-harness plant in Badr expand industrial-coating requirements for machinery and building infrastructure. As automotive volumes climb, authorized body shops invest in fast-curing refinishing products, adding depth to the Egyptian paints and coatings market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive production slump and import curbs | -0.8% | Industrial zones in Greater Cairo, Alexandria | Short term (≤ 2 years) |

| FX-driven raw-material price volatility | -1.1% | National, with higher impact on import-dependent manufacturers | Medium term (2-4 years) |

| Water-scarcity risks for water-borne lines | -0.6% | Upper Egypt, desert industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FX-Driven Raw-Material Price Volatility

The Egyptian pound’s March 2024 float triggered sharp cost spikes for imported pigments, solvents, and specialty additives that account for most formulation expenses. Electricity tariff hikes following the removal of industrial discounts compound operating costs, forcing manufacturers to either absorb margin compression or raise prices, which can delay construction and industrial maintenance schedules. Shorter procurement cycles, hedging challenges, and greater working-capital needs elevate credit risk, particularly for small and mid-size firms that collectively serve a sizable slice of the Egypt paints and coatings market.

Water-Scarcity Risks for Water-Borne Lines

Egypt ranks among the world’s most water-stressed nations, and intermittent shortages in Upper Egypt and arid industrial estates threaten the continuous operation of water-intensive coating lines. Academic studies show escalating water-quality deterioration in certain clusters, raising treatment costs and complicating discharge compliance[2]“Utilization of affordable nanocomposites,” Nature, nature.com . While powder or high-solids alternatives can mitigate usage, capital retrofits are expensive, potentially delaying technology upgrades and moderating the otherwise strong trajectory of the Egypt paints and coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Driven by Climate Adaptability

Acrylic systems commanded 37.15% of Egypt paints and coatings market share in 2025, underpinned by excellent color retention and adhesion in environments where surface temperatures top 60 °C. The Egypt paints and coatings market size for acrylic resins is projected to grow at a 6.15% CAGR as residential, commercial, and infrastructure projects demand durable yet environmentally compliant finishes.

Polyurethane enjoys premium uptake in petrochemical and automotive lines thanks to superior chemical resistance, while epoxy remains the go-to for secondary containment and floorings in harsh industrial sites. Alkyd retains a foothold in cost-sensitive masonry but faces tightening VOC caps. Polyester-based powder systems gain momentum in appliance and metal-fabrication niches that value solvent-free curing, and nano-enhanced water-borne formulations incorporating Egyptian silica-fume position local producers for future specialty growth.

By Technology: Water-Borne Solutions Lead Environmental Transition

Water-borne coatings held 49.55% of the Egypt paints and coatings market size in 2025, benefiting from rapid public-sector uptake and consumer awareness. Regulatory mandates on VOC ceilings and the carbon-credit system solidify their lead, with segment volume forecast to rise at 6.05% CAGR through 2031. Solvent-borne lines persist in heavy-duty marine and industrial applications, though new high-solids chemistries aim to retain performance while lowering emissions.

Powder coatings gain foothold in appliances, furniture, and automotive metal parts, rising in tandem with Egypt’s export-oriented manufacturing drive. Digital finishing lines at new factories in 10th of Ramadan City and Badr illustrate capital investment in cleaner technologies as firms future-proof production against forthcoming stricter regulations. Yet, persistent water scarcity forces producers to optimize rinse cycles and recycle process water, spurring research into ultra-low-water formulations and closed-loop systems.

By End-User Industry: Architectural Anchors Growth While Protective Accelerates

Architectural uses absorbed 64.80% of the Egypt paints and coatings market share in 2025, mirroring surging residential and mixed-use construction under the New Urban Communities Authority. General industrial and industrial wood segments take advantage of the rise in textile and furniture exports, sustaining a steady consumption baseline.

Protective coatings lead growth at a 5.12% CAGR, fueled by ongoing refinery upgrades, LNG terminals, and the large-scale petrochemical complex near Ain Sokhna. Automotive volumes remain uneven given import restrictions and supply-chain kinks, yet localized assembly lines and after-sales refinishing invest in higher-spec coatings to meet OEM warranty and color-match expectations. As multinational manufacturers adopt ISO 12944 and ISO 9001 standards across Egyptian plants, demand tilts toward certified, high-durability coating systems, further professionalizing the Egypt paints and coatings market.

Geography Analysis

Cairo and its satellite cities concentrate most of the Egypt paints and coatings market demand, energized by the New Administrative Capital’s mixed-use clusters, metro extensions, and social-housing projects. Architectural contractors operating here specify large volumes of acrylic emulsions, primers, and interior finishes that withstand desert dust and ultraviolet exposure. Alexandria and the Mediterranean coastal belt's consumption is driven by port expansions and a shipyard maintenance drive, marine-grade and anti-fouling paint uptake.

Meanwhile, the Suez Canal Economic Zone evolves into an industrial coating hotspot; the petrochemical complex at Ain Sokhna alone requires tank linings, pipeline wraps, and intumescent fireproofing across 11 integrated plants. Diversification initiatives such as New Alamein’s silicon complex and Upper Egypt’s Kom Ombo solar farm introduce new industrial activity clusters that recalibrate geographic demand patterns. Coupled with anticipated recovery in global trade flows, these projects foster a balanced distribution of consumption, reducing Cairo’s historic dominance and enlarging the total addressable Egypt paints and coatings market size nationwide.

Competitive Landscape

The Egypt paints and coatings market hosts a mix of global majors and agile local firms, yielding moderate fragmentation. Competitive advantage hinges on product customization for Egypt’s climatic extremes and regulatory specifics. Jotun’s “Jotashield Extreme” employs heat-reflective pigments that minimize interior cooling loads, gaining traction in social-housing tenders. Start-ups collaborating with Cairo universities exploit silica-fume nanotechnology to deliver antimicrobial, self-cleaning exterior paints that lower maintenance cycles. Meanwhile, domestic producers such as Pachin, now 81% owned by UAE-based National Paints, leverage regional distribution and price flexibility to defend share in mass-market emulsions.

Egypt Paints And Coatings Industry Leaders

Asian Paints

Jotun

KAPCI Coatings

NATIONAL PAINTS FACTORIES CO. LTD.

UBMC Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Asian Paints International acquired an additional 24.3% stake in SCIB Paints, Egypt for USD 4.13 million, demonstrating continued international investment confidence in Egypt's coatings market.

- September 2023: Jotun inaugurated a USD 100 million, 70 million-liter factory in 10th of Ramadan City built with advanced energy-saving systems.

Egypt Paints And Coatings Market Report Scope

The Egyptian paints and coatings market is segmented by resin type, technology, and end user. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types), technology (waterborne, solvent-borne, and other technologies. By end user, the market is segmented by architectural, automotive, wood, protective, general industrial, and other end users. The report offers market size and forecasts for Egypt's paints and coatings market in revenue (USD million) for all these segments.

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

| Other Technologies |

By End-User Industry

| Architectural |

| Automotive |

| Industrial Wood |

| Protective Coatings |

| General Industrial |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| Other Technologies | |

| By End-User Industry | Architectural |

| Automotive | |

| Industrial Wood | |

| Protective Coatings | |

| General Industrial | |

| Other End-user Industries |

Key Questions Answered in the Report

What factors are driving near-term demand for decorative paints in Egypt?

Accelerated housing projects under the New Urban Communities Authority and stringent green-building mandates are lifting volumes for low-VOC decorative paints, particularly in Cairo-area megacities.

How big is the opportunity for protective coatings linked to petrochemicals?

The downstream oil and gas expansion, led by the USD 10.9 billion complex in the Suez Canal Zone, is propelling protective-coating demand at a 5.12% CAGR through 2031.

Which technology segment is gaining the most share?

Water-borne systems already hold 49.55% share and continue to outpace the overall market thanks to VOC rules and carbon-credit incentives.

How are currency swings affecting raw-material costs?

The March 2024 pound float raised prices for imported pigments and resins, shaving an estimated 1.1% from forecast CAGR as firms juggle margin protection with price sensitivity.

Are water-scarcity concerns reshaping technology choices?

Yes, producers are investing in powder and high-solids lines and recycling systems to mitigate long-term water-risk exposure in arid zones.

Page last updated on: