Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

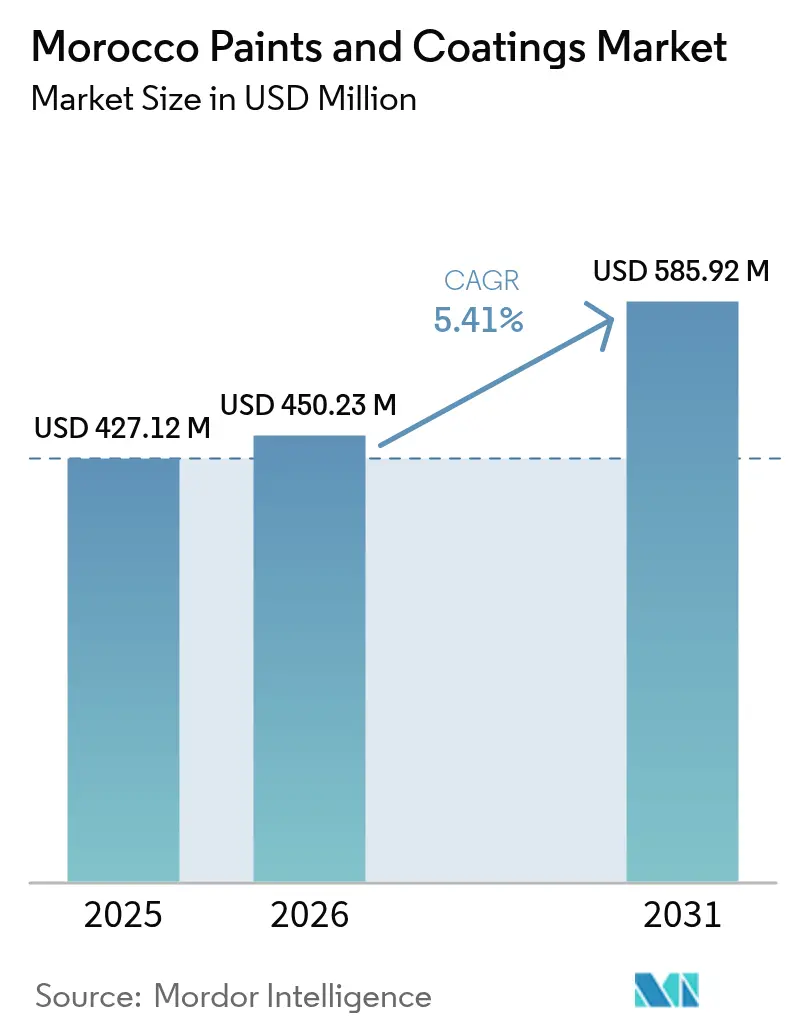

| Base Year Market Size (2025) | USD 427.12 Million |

| Market Size (2026) | USD 450.23 Million |

| Market Size (2031) | USD 585.92 Million |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

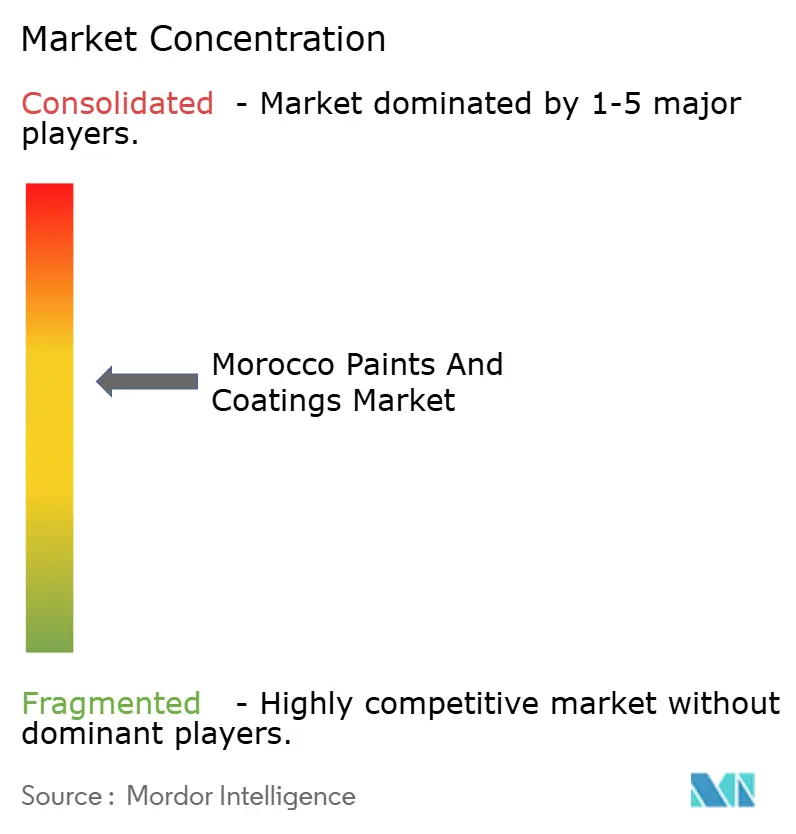

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Paints And Coatings Market Analysis by Mordor Intelligence

The Morocco Paints and Coatings Market size is expected to increase from USD 427.12 million in 2025 to USD 450.23 million in 2026 and reach USD 585.92 million by 2031, growing at a CAGR of 5.41% over 2026-2031. As OEM automotive build rates increase and investments in phosphate processing grow, public-sector green-procurement rules are further driving demand. However, raw-material volatility and competition from informal sources are limiting margin growth. While architectural applications continue to dominate in terms of value, OEM automotive lines are expanding at a faster pace. This growth is primarily driven by Stellantis and Renault, which are leading export-oriented clusters that require EU-aligned VOC limits and superior corrosion performance. Morocco is aligning its regulatory framework with Europe and leveraging UNIDO-funded projects aimed at hazardous-chemical abatement. Simultaneously, the technology mix is shifting toward water-borne and powder chemistries. Additionally, polyurethane and powder formulations are gaining traction in high-performance segments such as engine components and phosphate conveyors. The competitive landscape is intensifying as AkzoNobel merges with Axalta, Jotun upgrades its North-African capacity, and domestic players like Colorado strengthen their distribution networks through targeted research and development and ISO-certified quality standards.

Key Report Takeaways

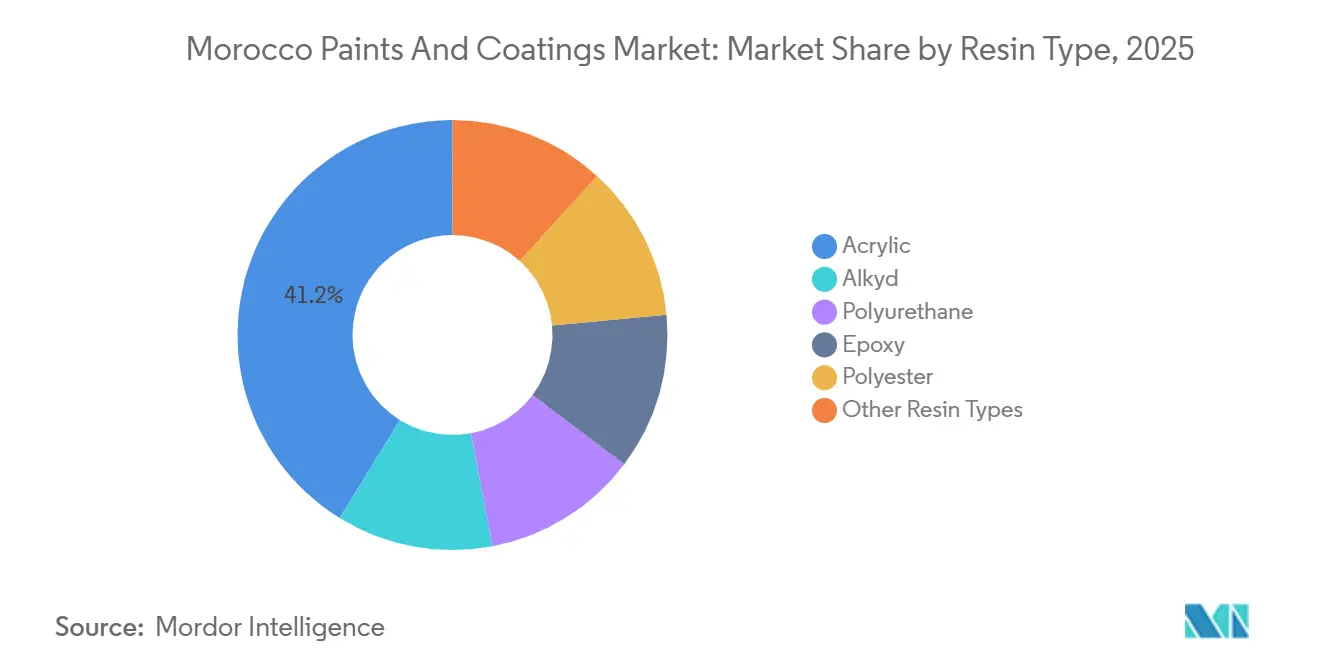

- By resin type, acrylic captured 41.22% of Morocco Paints and Coatings market share in 2025, while polyurethane is forecast to post a 6.07% CAGR through 2031.

- By technology, water-borne systems commanded 53.44% of the Morocco Paints and Coatings market size in 2025; powder coating is advancing at a 5.72% CAGR through 2031.

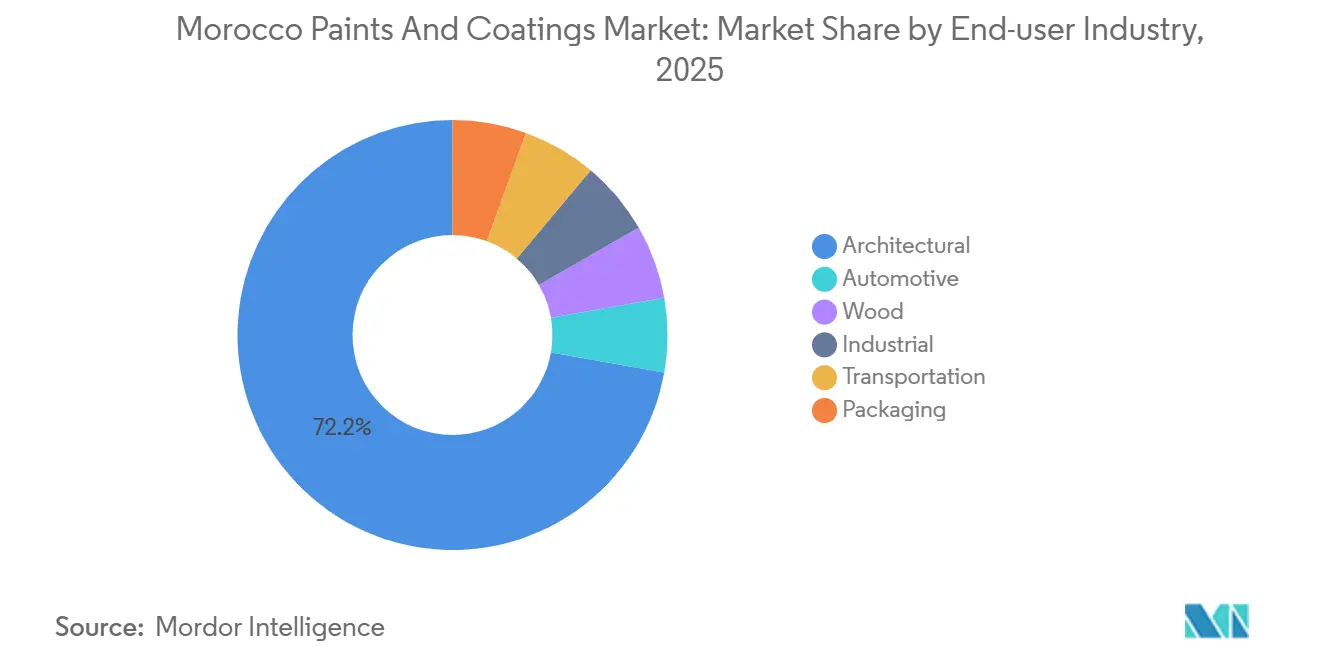

- By end-user industry, architectural applications accounted for 72.21% of the Morocco Paints and Coatings market size in 2025, and automotive demand is projected to climb at a 5.91% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Morocco Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of domestic wood and furniture manufacturing | +0.6% | National, concentrated in Casablanca-Settat and Fès-Meknès regions | Medium term (2-4 years) |

| Accelerating shift toward eco-label low/zero-VOC coatings | +0.9% | National, with early adoption in Rabat-Salé-Kénitra and Casablanca urban zones | Short term (≤ 2 years) |

| Automotive free-trade zone OEM coatings pull (Tangier MED) | +1.4% | Tangier-Tétouan-Al Hoceïma and Kenitra industrial zones | Short term (≤ 2 years) |

| Phosphate-processing corrosion-protection demand (OCP projects) | +0.8% | National, with concentration in Khouribga, Jorf Lasfar, and Safi phosphate hubs | Medium term (2-4 years) |

| Green-public-procurement bill favouring bio-based resins | +0.5% | National, pilot implementation in Rabat and Casablanca public works | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Domestic Wood and Furniture Manufacturing

Morocco's woodworking industry faces challenges due to a coatings volume cap. However, targeted upgrades at mills are enabling the production of higher-grade finishes. Morocco's annual timber output satisfies only a fraction of its consumption, leading the nation to depend on costlier imports. This reliance is tightening the margins of local cabinetmakers. In a bid to expand, CEMA Bois de l'Atlas is making substantial investments to increase its panel capacity. As a result, there is an anticipated surge in demand for fast-drying sealers and UV topcoats, especially with the new production lines set to launch in 2027. Local laboratory tests on castor-oil-modified alkyds have yielded impressive results: Class 1 adhesion and a pendulum hardness of 128 seconds[1]Springer, “Synthesis of castor oil-modified alkyd resins and investigation of their effect on the impact resistance of polyurethane coatings,” springer.com. This advancement positions local formulators advantageously, allowing them to produce premium furniture varnish in line with upcoming procurement regulations. Nevertheless, the industry's growth trajectory is closely linked to forestry yields and essential logistics reforms.

Accelerating Shift Toward Eco-Label Low/Zero-VOC Coatings

To enhance environmental standards, a mandatory eco-label now covers construction paints. This move has prompted resin suppliers to hasten their upgrades to acrylic emulsions and to import bio-polyols. In support of these initiatives, organizations have allocated a budget to assist smaller plants in phasing out lead dryers and high-aromatic solvents. Notably, pilot audits for this initiative have already been conducted in Rabat and Casablanca. While the share of water-borne paints surged to 53.44% in 2025, the adoption rate remains inconsistent. Urban public works sites are mandated to comply with the new label, but rural projects still permit the use of aromatic alkyds. BASF's Sovermol 830 polyol showcases a significant advancement: it achieves Shore D 60 hardness in a solvent-free PU floor coating that dries quickly, within 24 hours, making it foot traffic-ready. This underscores a pivotal shift in the industry: high performance can now be attained without volatile organic compounds (VOCs). However, the rapid pace of these regulatory changes is outstripping the research and development capabilities of small and medium-sized enterprises (SMEs), pushing them toward licensing agreements or joint ventures.

Automotive Free-Trade-Zone OEM Coatings Pull

By February 2026, Tangier MED processed a significant number of vehicles, while Stellantis expanded Kenitra's capacity to produce more units and added a production line for engines annually. This move has established Kenitra as a major demand center for OEM primers and clearcoats. Dürr's RoDip pretreatment system now rotates vehicle bodies, reducing immersion length and subsequently cutting down on water and heating requirements[2]Dürr, “Dürr builds an energy-efficient paint shop for Stellantis with repurposed robots,” durr.com. Meanwhile, EcoInCure's electric ovens have achieved a notable reduction in CO₂ emissions in paint shops compared to traditional gas kilns. As a result, the Moroccan paints and coatings market is now tasked with supplying low-conductivity e-coats, water-borne basecoats, and PU clears that align with Stellantis's European standards, all without imposing price premiums. Additionally, Renault's feasibility studies for an EV plant at Nador West Med hint at a potential demand surge on the eastern seaboard, contingent on timely localization by suppliers.

Phosphate-Processing Corrosion-Protection Demand

OCP Group is channeling investments into green initiatives at its sites in Khouribga, Jorf Lasfar, and Safi. Facing challenges such as phosphate slurry, sulfuric acid mist, and coastal salinity, the need for C4–C5 specification coatings becomes paramount. Even when subjected to the harsh marine conditions of the North-African region, anti-corrosive powder formulations can maintain their efficacy for several years. The growing preference for powder coatings stems from their zero-VOC curing, allowing them to sidestep the tightening effluent permits that impose penalties on solvent lines. Resin selections, made with an eye on longevity and locked in for the 2026–2027 period, offer early adopters a lucrative decade of revenue. However, there is a significant risk: if the film's integrity is compromised, these early adopters might grapple with substantial liabilities.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ and petro-feedstock prices | -1.2% | Global, with acute impact on import-dependent Moroccan formulators | Short term (≤ 2 years) |

| Informal/grey-market paint penetration | -0.7% | National, concentrated in rural and peri-urban construction zones | Medium term (2-4 years) |

| Water-scarcity-driven effluent permits raising CapEx | -0.5% | National, with highest compliance costs in Casablanca-Settat and Marrakech-Safi industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ and Petro-Feedstock Prices

In June 2025, both Europe and North America experienced elevated TiO₂ prices. These surging prices played a pivotal role in driving up the costs for high-opacity architectural whites. Morocco, which depends heavily on imports for almost all its pigments and resins, was quick to feel the brunt of freight and foreign-exchange fluctuations on its local EBITDA. Meanwhile, in Colorado, there was a partial hedge against this exposure. However, monthly decisions were required - absorb the financial blows or adjust list prices. This choice became even more complex in a market where grey-trade cartons could significantly undercut the prices of established brands.

Informal/Grey-Market Paint Penetration

Non-certified producers avoid ISO audits, forgo VOC testing, and evade effluent fees. This translates into discounted shelf prices at small hardware stores. While public projects tighten standards, rural masons prioritize the lower sticker cost over scrub resistance, allowing informal gallons to still command a sizable demand. Consequently, the landscape is divided: regulated players bear the burden of higher compliance costs, while grey market makers suppress the average selling price and hinder the shift toward premium products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Meets Polyurethane Ambitions

In 2025, acrylics secured a 41.22% market share, driven by their cost efficiency and performance meeting EU standards for façades and DIY walls. Dominating the majority of water-borne architectural formulas, any tightening of eco-labels leads to a surge in acrylic demand. Meanwhile, polyurethanes are set to expand at a 6.07% CAGR during the forecast period of 2026–2031, fueled by their superior abrasion and chemical resistance. These qualities make them indispensable for OEM clearcoats, industrial floors, and topcoats on phosphate equipment. Local coaters are now venturing into bio-polyols, striving for zero-VOC thresholds while maintaining Shore D hardness. The Moroccan market for polyurethane systems, serving both OEM exteriors and heavy-duty interiors, is on an upward trajectory, underscoring its importance. While alkyds serve the price-sensitive solvent segment, they are witnessing a decline due to stricter NM eco-label regulations. Epoxies and polyesters, though limited to niche applications - epoxy in acid rigs and floors, and polyester in powder coatings for coastal steel - together represent a small fraction of the 2025 market value.

Future growth is contingent on boosting local resin production. Presently, a majority of PU pre-polymers and acrylic emulsions make their way in ISO-tanks from Europe or Asia-Pacific. By setting up even a modest capacity for monomers or dispersions, producers stand to cut costs in comparison to gray market competitors and insulate themselves from freight price swings. Until such measures are taken, formulators remain heavily dependent on imports and vulnerable to currency shifts.

By Technology: Water-Borne Systems Lead, Powder Coatings Accelerate

In 2025, swift regulatory changes propelled water-borne systems to capture 53.44% of the market value. By the forecast period of 2026–2031, their dominance is expected to strengthen further, driven by public-project tender rules enforcing NM eco-labels and an increasing buyer focus on indoor-air-quality scoring. Stellantis is pivoting to an ultra-low VOC water-borne basecoat for its wet-on-wet lines and new EV plants. This basecoat adeptly manages metallic flop, and curtails bake energy - a complex chemistry still predominantly controlled by multinationals. Powder coatings, celebrated for their zero-VOC nature and superior edge coverage, are leading the charge with a robust 5.72% CAGR during the forecast period of 2026-2031. OCP has opted for the Interpon C5-grade for its latest slurry pipe racks. Appliance exporters, including Whirlpool at its Tangier assembly, are increasingly outsourcing major components to Tunisian job-coaters, who are rapidly adopting powder coatings. While the market share of solvent-borne systems in Morocco's paints and coatings sector is on the decline, it is not vanishing immediately. Informal builders continue to favor these systems, drawn by their cost-effective spray equipment and quick flash-off times.

UV-cure technology, though still a niche, is being explored by furniture exporters. They are adopting roll-coat and vacuum-application lines, leading to notable reductions in cycle time and energy use. Should timber capacity grow, UV's modest market presence might witness a boost after 2028. Electro-coat, mainly serving OEM chassis and white-goods casings, is poised to benefit from a rise in export demand.

By End-User Industry: Architectural Anchors, Automotive Accelerates

In 2025, architectural applications commanded a significant 72.21% market share, driven by robust activities in residential construction, infrastructure undertakings, and the commercial real estate sector. Automotive coatings, supported by Stellantis' expansion in Kenitra and Renault's electric vehicle initiatives at the Nador West Med port, are projected to grow at a CAGR of 5.91% during the forecast period of 2026–2031. Morocco's ongoing infrastructure investments, including stadium renovations, airport capacity enhancements, and urban transit expansions, are fueling increased demand for architectural coatings, particularly primers, sealers, and topcoats. While wood coatings face challenges due to Morocco's dependence on timber imports, capacity expansions and investments in local furniture manufacturing present opportunities for growth. Industrial coatings cater to phosphate processing, food and beverage, and general manufacturing sectors, with demand driven by active green investment initiatives and capital projects. Meanwhile, transportation and packaging coatings remain niche markets, with limited growth expected through 2031.

The automotive sector's projected CAGR of 5.91% during 2026–2031 depends on whether Morocco evolves into a hub for value-added OEM finishing or remains primarily an assembly center. Stellantis' Kenitra facility has improved production efficiency by utilizing advanced paint shop technology that reduces emissions and heating time. Renault's Tangier plant and the potential establishment of another major OEM coatings hub at the Nador site could further transform the sector. Architectural coatings' dominant 72.21% market share reflects Morocco's urbanization and public expenditure trends, although informal competition poses challenges to margin growth. Bio-based performance enhancements in polyurethane wood varnishes offer promising opportunities for local formulators. As Morocco diversifies its manufacturing landscape, industrial coatings are expected to benefit, while transportation and packaging coatings are likely to remain confined to their niche status.

Geography Analysis

In 2025, Morocco's paints and coatings market saw significant contributions from Casablanca-Settat, Rabat-Salé-Kénitra, and Tangier-Tétouan-Al Hoceïma. Casablanca-Settat, fueled by projects such as commercial towers, airport upgrades, and the Benslimane World-Cup stadium (notably opting for low-VOC elastomeric roof coatings), emerged as a major consumer. Rabat-Salé-Kénitra, hosting Stellantis’s Kenitra complex, witnessed a boost in automotive OEM coatings demand, thanks to stable production and an uptick in engine output. By 2026, Kenitra's paints and coatings market had expanded considerably, with forecasts suggesting continued growth during the 2026–2031 period as Tier-1 suppliers began localizing bumper, wheel, and trim finishing.

Tangier-Tétouan-Al Hoceïma capitalized on Tangier MED, the premier hub for European Union-bound vehicle exports. After receiving powder topcoats and e-coat in Kenitra, vehicle bodies were transported north for final assembly. With Renault’s plant pivoting to electric small cars, there was a heightened demand for battery-pack-resistant primers. This region recorded the kingdom's swiftest growth. Meanwhile, smaller areas such as Marrakech-Safi and Béni Mellal-Khénifra made their mark in industrial coatings, particularly through OCP acid plants. Here, powder and high-build epoxies commanded premium average selling prices (ASPs) due to their durability against harsh chemical attacks.

Water stress poses a significant challenge. Casablanca-Settat and Marrakech-Safi faced steep discharge fees, prompting plants to adopt closed-loop rinsing and waterless powder solutions. Although desalination facilities are planned along the Atlantic corridor by 2045 to alleviate future water constraints, the current costs of effluent management remain burdensome. In regions such as Souss-Massa and Drâa-Tafilalet, where enforcement is more lenient, informal production clusters have emerged, resulting in a higher ratio of solvent-borne sales compared to officially recorded water-borne gallons.

Competitive Landscape

The Morocco Paints and Coatings Market is moderately consolidated. As the industry evolves, there is a pronounced shift towards green chemistry and localized investments. Benteler's newly operational smart factory in Kenitra is amplifying the local demand for e-coats and powders, attracting a slew of Tier-1 suppliers. In a bid to navigate market fluctuations, smaller Moroccan formulators are toying with blends of Chinese TiO₂. However, this strategy is not without its pitfalls; the risk of opacity drift looms large, potentially sparking warranty disputes on public projects.

Morocco Paints And Coatings Industry Leaders

Colorado

ATLAS PEINTURES

Akzo Nobel N.V.

PPG Industries, Inc.

Hempel A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Benteler Group launched construction of a smart automotive plant in Morocco’s Kenitra Free Zone, aiming to strengthen its global footprint. The automotive component company will invest a mid-double-digit million-euro amount during the plant’s ramp-up phase. Once operational in 2026, the site is expected to significantly support the coatings demand in the country.

- September 2024: AkzoNobel has unveiled its latest offering, the Interpon D2525 Low-E powder coatings range, emphasizing sustainability and environmental friendliness. Furthermore, the recent product introductions in Morocco's paints and coatings sector are poised to invigorate the industry, broadening customer choices and potentially spurring growth and innovation.

Morocco Paints And Coatings Market Report Scope

Paints and coatings are materials, available in liquid or powder form, that are applied to surfaces to form a protective or decorative solid film. They are composed of binders (film-formers), pigments (for color and opacity), solvents (to adjust viscosity), and additives. "Paints" are primarily designed for aesthetic purposes with pigmentation, while "coatings" are formulated for performance, providing features such as corrosion resistance, durability, and specialized functional properties like electrical conductivity.

The coatings market is segmented by resin type, technology, and end-user industry. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, powder coating, and UV-cured coating. By end-user industry, the market is segmented into architectural, automotive, wood, industrial, transportation, and packaging. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coating |

| UV-Cured Coating |

By End-user Industry

| Architectural |

| Automotive |

| Wood |

| Industrial |

| Transportation |

| Packaging |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder Coating | |

| UV-Cured Coating | |

| By End-user Industry | Architectural |

| Automotive | |

| Wood | |

| Industrial | |

| Transportation | |

| Packaging |

Key Questions Answered in the Report

How large is the Morocco paints and coatings market today?

The Morocco Paints and Coatings Market size is expected to increase from USD 427.12 million in 2025 to USD 450.23 million in 2026 and reach USD 585.92 million by 2031, growing at a CAGR of 5.41% over 2026-2031.

Which end-user segment is expanding the fastest?

OEM automotive coatings are growing the quickest, tracking a 5.91% CAGR to 2031 as Stellantis and Renault ramp exports.

What technology is gaining the most share?

Powder coatings show the strongest momentum, forecast at 5.72% CAGR, because they deliver zero VOCs and high corrosion resistance.

What regulatory trends shape future demand?

Tightening NM eco-labels and forthcoming bio-content mandates are pushing the market toward water-borne, powder, and bio-based chemistries.

Page last updated on: