Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

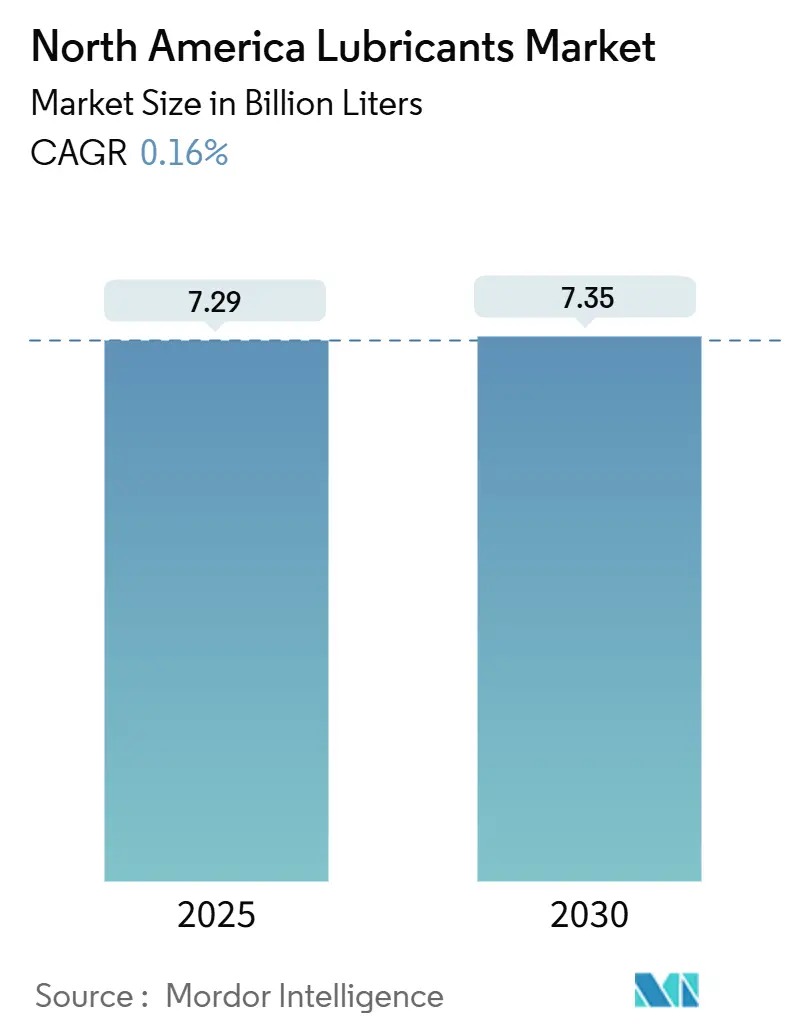

| Market Volume (2025) | 7.29 Billion liters |

| Market Volume (2030) | 7.35 Billion liters |

| Growth Rate (2025 - 2030) | 0.16% CAGR |

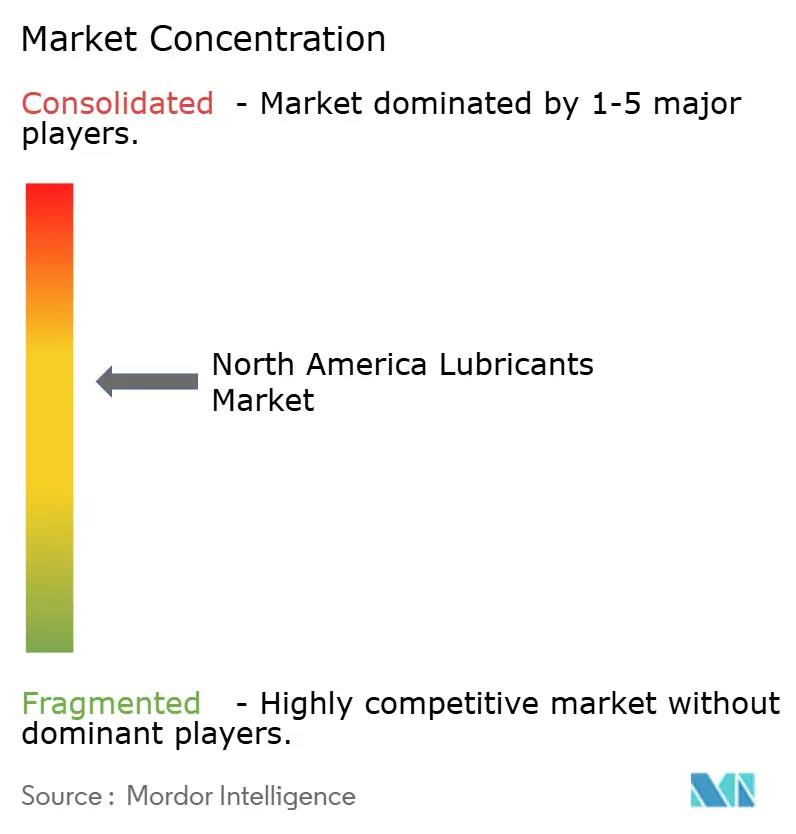

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Lubricants Market Analysis by Mordor Intelligence

The North America Lubricants Market size is estimated at 7.29 billion liters in 2025, and is expected to reach 7.35 billion liters by 2030, at a CAGR of 0.16% during the forecast period (2025-2030). The mature demand profile stems from long-cycle industrial assets, slower fleet turnover, and the initial impact of electric-vehicle adoption. Growth pockets nonetheless arise from synthetic formulations that enable extended drain intervals, data-center cooling fluids, and bio-based products aligned with new sustainability mandates. Competitive differentiation centers on base-stock security, additive innovation, and omnichannel distribution that cater to the shift toward the do-it-yourself aftermarket. Consolidation among integrated oil majors and specialist blenders raises the bargaining power of the largest suppliers and tightens access to premium channels.

Key Report Takeaways

- By product type, automotive engine oil led with 39.6% of the North American lubricants market share in 2024, while industrial engine oil is forecast to expand at a 0.67% CAGR through 2030.

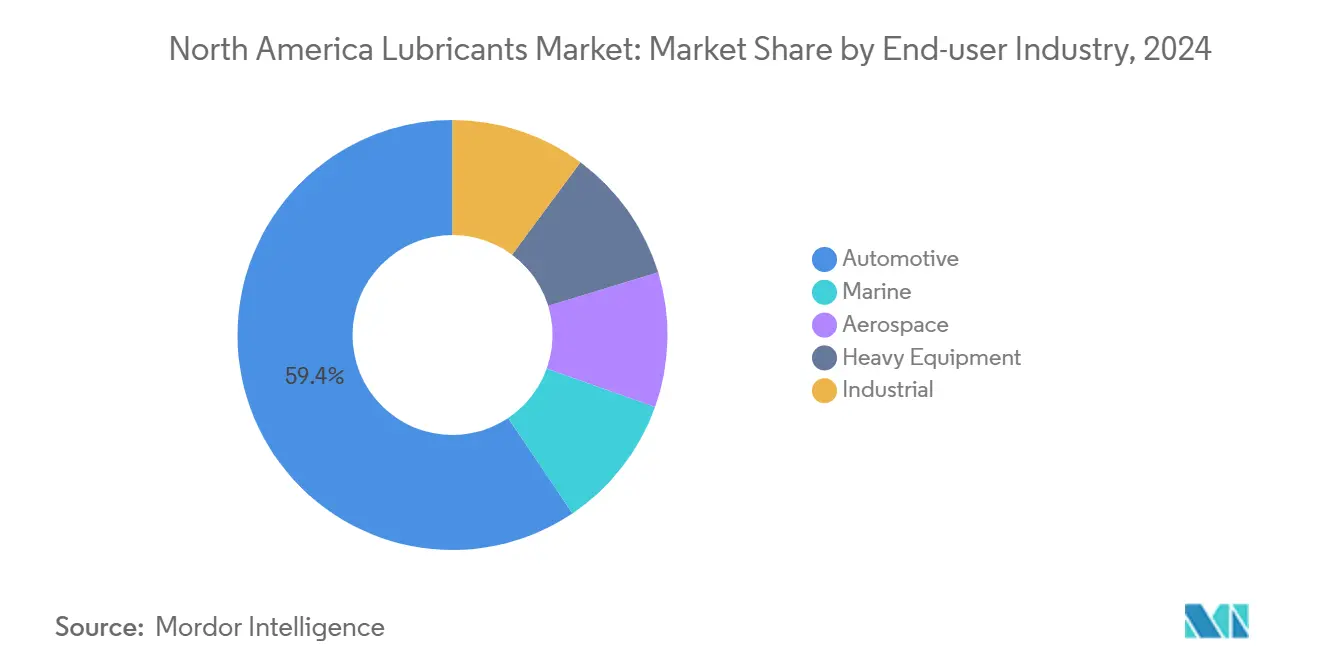

- By end-user industry, the automotive segment commanded 59.42% share of the North American lubricants market size in 2024, whereas the industrial segment is projected to advance at a 0.54% CAGR through 2030.

- By base stock, mineral-oil offerings held 64.78% share of the North American lubricants market size in 2024, while bio-based lubricants are anticipated to grow at a 0.89% CAGR to 2030.

- By geography, the United States accounted for 71.31% of the regional volume in 2024, and Mexico is expected to register the highest CAGR of 3.05% during 2025-2030.

North America Lubricants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Synthetic-lubricant demand surge | +0.8% | United States industrial and automotive hubs | Medium term (2-4 years) |

| Industrial output rebound | +0.6% | U.S. core and Mexican manufacturing corridors | Short term (≤ 2 years) |

| Tightening CAFE and EPA rules | +0.4% | U.S.; policy harmonization expected in Mexico | Long term (≥ 4 years) |

| Expansion of e-commerce DIY channels | +0.3% | Suburban and rural North America | Medium term (2-4 years) |

| Growth in dielectric cooling fluids | +0.2% | U.S. data-center clusters; Canada emerging | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Synthetic-Lubricant Demand Surge

Synthetic products earn a share across the automotive and industrial equipment sectors because they reduce downtime and extend oil-change intervals, which increases asset utilization and lowers lifecycle costs. Shell reports that hyperscale data-center operators are switching to its immersion-cooling fluids to handle rising chip-level heat loads[1]Shell Global, “Immersion Cooling Fluids for Data Centers,” shell.com. The American Petroleum Institute’s SQ gasoline-engine oil category, introduced in 2024, requires thermally stable synthetic base stocks, and the ILSAC GF-7 standard slated for 2025 reinforces this shift. OEM warranty terms are increasingly specifying synthetic grades, thereby strengthening pull-through demand in the North American lubricants market. Producers with captive Group III and PAO capacity capitalize on narrowing price gaps versus premium mineral stocks. Greater thermal efficiency also supports decarbonization targets in transport and stationary engines.

Industrial Output Rebound

Construction, mining, and general manufacturing, which rebounded from the 2023 trough, bolsters lubricant consumption in hydraulic systems, gearboxes, and metalworking operations. Public-sector infrastructure outlays stimulate demand for off-highway machinery that relies on low-ash fluids, which are compatible with modern emission controls. Mining companies favor synthetic greases that lengthen relubrication intervals in abrasive environments. Metalworking-fluid uptake follows tooling upgrades as vehicle makers convert lines for battery housing and e-motor production. Mexico’s nearshoring inflows magnify factory lubricant demand, lifting the medium-term outlook for the North American lubricants market.

Tightening CAFE and EPA Rules

The Corporate Average Fuel Economy framework mandates lower fleet emissions, forcing automakers to recommend 0W-16 and 0W-12 grades that can only be blended with high-purity synthetics. Commercial fleets gain from measurable fuel-economy savings, and bulk buyers prefer long-drain formulations that limit service downtime. Lubricant suppliers invest in additive chemistries that prevent oxidation and wear at reduced viscosities. The regulation heightens the importance of certificate-of-analysis traceability, rewarding firms that integrate blending and packaging inside North America. These policies sustain volume for value-added SKUs even as electric-vehicle substitution caps overall lubricant tonnage.

Expansion of E-Commerce DIY Channels

Digital retail is capturing a rising share of passenger-car lubricant sales as consumers favor doorstep delivery and subscription replenishment. Interactive fitment tools reduce product-selection risk, and influencers share step-by-step oil-change videos that boost DIY confidence. Private-label brands leverage platform algorithms to offer competitive pricing, prompting conventional retailers to expand their omnichannel offerings. Rural customers in the North American lubricants market rely on online bulk purchasing to offset the limited assortment available at brick-and-mortar locations. Producers streamline pack sizes and shelving-reserve packaging to meet parcel weight limits, re-shaping distribution economics.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude- and base-oil price volatility | -0.40% | Global, with acute impacts on US Gulf Coast refineries | Short term (≤ 2 years) |

| Accelerating electric-vehicle parc lowers ICE-oil volumes | -0.60% | US and Canada early adoption markets | Long term (≥ 4 years) |

| Tight PFAS and micro-plastics rules threatening some additive chemistries | -0.30% | North America regulatory mandate, EU alignment expected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude- and Base-Oil Price Volatility

Closures of Group I and Group II units on the U.S. Gulf Coast reduce supply flexibility and magnify the impact of refinery turnarounds on posted prices. Seasonal gasoline demand spikes incentivize refiners to maximize fuel output, tightening base-stock availability and forcing independents to pay spot premiums. Integrated majors absorb feedstock swings but pass costs downstream when Brent widths persist. Bio-based base-oil economics fluctuate with tallow and used-cooking-oil pricing, complicating procurement planning. Distributors hedge inventories yet risk carrying high-priced stocks when futures soften, weighing on near-term margins across the North American lubricants market.

Electric-Vehicle Fleet Expansion

Electric-vehicle penetration erodes internal-combustion engine oil volumes, particularly in premium passenger car segments where early adopters tend to cluster. Engine oil fill reductions are only partially offset by nascent e-fluid applications in gearboxes and battery thermal loops. Commercial-vehicle electrification advances more slowly, providing a transitional buffer, but policy incentives accelerate the adoption of buses and last-mile vans in metropolitan areas. Suppliers refocus on industrial and specialty niches to offset revenue declines, yet capacity utilization challenges arise at plants designed for high-volume PCMO output. The structural shift paves the way for long-term growth in the North American lubricants market, despite innovation in adjacent fluid categories.

Segment Analysis

By Product Type: Engine Oils Hold Scale While Industrial Fluids Lead Growth

Automotive engine oils accounted for 39.6% of the North American lubricants market size in 2024, as light-duty and heavy-duty vehicles continue to dominate the rolling stock. The subsegment’s value mix tilts toward synthetics that command price premiums, softening the revenue impact of gradual volume decline. Industrial engine oils, although smaller in absolute liters, post the quickest 0.67% CAGR thanks to machinery modernization across metal-cutting, power generation, and agricultural fleets. Transmission-fluid demand shows a bifurcated path: conventional automatics decline, yet purpose-designed e-drive lubricants emerge, carrying a higher unit value. Gear oils benefit from mining and wind-turbine gearboxes that mandate extreme-pressure performance, and hydraulic fluids gain from infrastructure build-outs that specify low-toxicity, fire-resistant grades.

Resilient niche classes add balance to the North American lubricants market. Greases capture opportunities in electric drivetrain bearings, wind turbine pitch systems, and food-processing equipment requiring NSF H1 certification. Metalworking fluids rebound in step with automakers' tooling up for aluminum body-in-white and battery-case machining. Specialty dielectric fluids for data-center immersion cooling, although currently less than 1 % of total liters, grow at a double-digit pace and reinforce the strategic value of high-margin formulations. OEM service-fill contracts act as a lock-in mechanism, making first-fill approvals a critical battleground for suppliers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Automotive Dominates but Industrial Users Accelerate

The automotive cohort accounted for 59.42% of total liters in 2024, underpinning the North American lubricants market; however, its growth profile flattens as EV adoption accelerates. Light-duty passenger cars are migrating to longer drain intervals, and heavy-duty trucking fleets are optimizing oil-analysis programs to stretch service cycles. Industrial end users expand their volume at a 0.54% CAGR, driven by the recovery of construction, mining, and manufacturing. Lubricant demand in marine engines stabilizes in response to IMO sulfur limits that require new detergent packages, while aerospace fluids edge higher on fleet renewal in business aviation and defense.

Equipment rental firms and owner-operators recognize the lifetime cost advantage of synthetics, which yields higher per-liter revenue even when volumes remain stable. Data-center operators add a unique growth node, adopting dielectric fluids and specialized greases for fan-motor bearings. Renewable-energy maintenance contracts boost demand for hydraulic fluids in solar trackers and gear oils in onshore wind turbines. These mixed dynamics keep the North American lubricants market diversified across industrial verticals and mitigate the drag from declining ICE vehicle count.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Base Stock Type: Mineral Oils Prevail as Bio-Based Grades Gain Traction

Mineral oil products accounted for 64.78% of the North American lubricants market size in 2024 due to their cost advantage and established supply chains. Group II and Group III refining upgrades add quality headroom, allowing premium mineral blends to meet mainstream performance standards. Synthetic lubricants steadily win share in high-duty and temperature-extreme environments, aided by the lower viscosity targets in tomorrow’s engine-oil categories. Semi-synthetic formulations bridge the gap between budget and performance needs, often serving quick-lube outlets where consumers accept modest premiums.

Bio-based lubricants, although accounting for only a few percentage points of volume, are expected to register the fastest growth rate of 0.89% CAGR through 2030. Federal procurement guidelines and state mandates push biodegradable hydraulic fluids in forestry, marine, and municipal fleets[2]U.S. Department of Agriculture, “BioPreferred Program Guidelines,” usda.gov . Feedstock swings in tallow and plant oils introduce margin risk, but technology gains in oxidative stability close previous durability gaps. Producers invest in enzyme-catalyzed esterification and improved antioxidant systems to extend service life, which helps the North American lubricants market meet circular economy targets without compromising equipment protection.

Geography Analysis

The United States anchors the North American lubricants market, accounting for 71.31% of the 2024 volume and boasting a broad distribution footprint that reaches every vehicle segment and industrial cluster. Federal fuel-economy policy and rapid consumer adoption of synthetic oil keep the value share elevated, even as total liters trend flat. High data-center density in Virginia, Texas, and Oregon stimulates demand for dielectric fluids, while shale-basin drilling activity sustains consumption of drilling mud additives and compressor oils. The market also benefits from extensive interstate logistics, which underpins high mileage and frequent maintenance cycles for Class 8 trucks.

Mexico delivers the fastest 3.05% CAGR on the continent as manufacturers relocate supply chains nearer to US buyers. Automotive and electronics assembly lines are concentrated in the Bajío and Northern states, driving demand for metal-forming fluids, industrial engine oils, and maintenance greases. Public-private partnerships channel funds into highways, airports, and power projects, expanding hydraulic-fluid and gear-oil consumption. Growing middle-class vehicle ownership supports an aftermarket that increasingly embraces synthetic blends, thereby widening product mix opportunities within the North American lubricants market.

Canada contributes a stable but smaller volume anchored in resource extraction and winter-oriented transport. Alberta’s oil-sands operations require heavy-duty engine oils and specialized extreme-pressure greases that remain pumpable at sub-zero temperatures. Forestry and mining operations in Quebec and British Columbia specify biodegradable hydraulics around sensitive waterways, aligning with federal environmental safeguards. Cross-border regulatory harmonization simplifies product certification, permitting seamless flow of approved SKUs between Canadian and US distributors. The regional balance keeps the North American lubricants market diversified and cushions macro-sector swings.

Competitive Landscape

The North America Lubricants Market is moderately consolidated, with integrated majors and a handful of regional specialists controlling most high-value channels in the North American lubricants industry. ExxonMobil, Chevron, Shell, and TotalEnergies leverage captive base-oil supply, additive co-development, and national service-station networks to lock in first-fill and top-up volumes. Competitive intensity pivots on supply-chain resilience amid base-stock volatility. Firms with backward-integrated Group III and PAO lines secure margin insulation, while independents negotiate toll-blending contracts to stabilize input costs.

North America Lubricants Industry Leaders

-

Chevron Corporation

-

ExxonMobil Corporation

-

Valvoline Inc.

-

BP p.l.c

-

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Pennzoil-Quaker State Company, a subsidiary of Shell PLC, and Blue Tide Environmental, LLC, announced the completion of a used re-refining facility in Baytown, Texas, which will produce high-quality, eco-friendly base oils and expand Shell's sustainable lubricant offerings.

- October 2024: Hindustan Petroleum Corporation Limited (HPCL) achieved a significant milestone by exporting HP LUBRICANTS to the United States for the first time, extending its global presence. This development is expected to increase competition in the US market, diversify lubricant options, and drive innovation with high-quality alternatives for consumers.

North America Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the North American lubricants market in 2025?

The North American lubricants market size is 7.29 billion liters in 2025 and is expected to reach 7.35 billion liters by 2030.

Which product type leads regional lubricant consumption?

Automotive engine oil retains the top position, accounting for 39.6 % of 2024 volume, though industrial engine oil is the fastest grower.

What is the outlook for bio-based lubricant demand?

Bio-based grades expand at a 0.89% CAGR through 2030, supported by federal procurement mandates and improved ester-chemistry durability.

Why are synthetic lubricants gaining share?

Synthetics meet stringent low-viscosity and high-temperature engine-oil specifications, extend drain intervals, and support data-center cooling applications.

Which country is the fastest-growing market within North America?

Mexico posts the highest 3.05% CAGR between 2025 and 2030, driven by manufacturing nearshoring and infrastructure investment.

Page last updated on: