Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

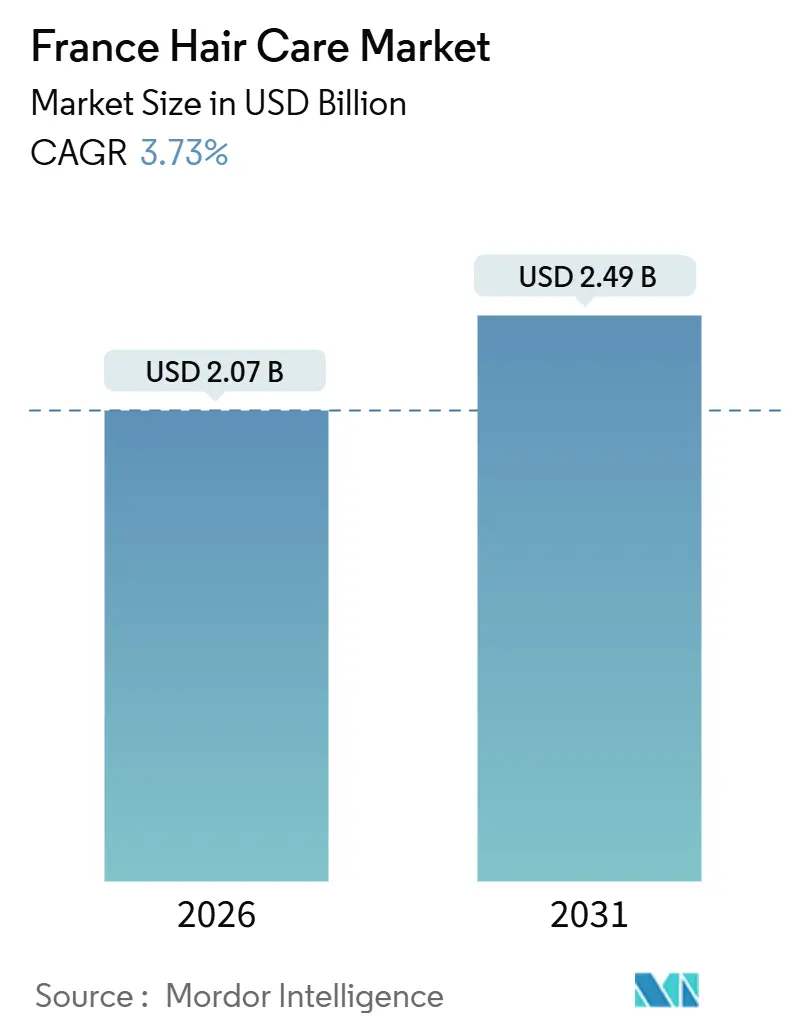

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 2.49 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Hair Care Market Analysis by Mordor Intelligence

The France hair care market was valued at USD 2.07 billion in 2026 and is projected to reach USD 2.49 billion by 2031, growing at a CAGR of 3.73% during the forecast period. Recognized as one of Europe's most advanced beauty markets, the French hair care industry is witnessing growth driven by premiumization and evolving consumer preferences. Five key trends are shaping the market dynamics: the shift toward premium products, rising demand for natural and organic solutions, a focus on scalp health through "skinification," the adoption of beauty-tech for personalized solutions, and sustainability initiatives influencing product formulations and packaging. Despite the increase in value sales, market growth faces challenges from cost-conscious consumers opting for home remedies and the prevalence of counterfeit products, which erode brand trust. The competitive landscape is becoming more intense as established multinational companies contend with agile indie brands that are targeting niche segments through focused innovation. Additionally, the convergence of beauty and wellness is creating new opportunities, particularly in medicated shampoos and scalp health products, which are increasingly viewed as essential by French consumers.

Key Report Takeaways

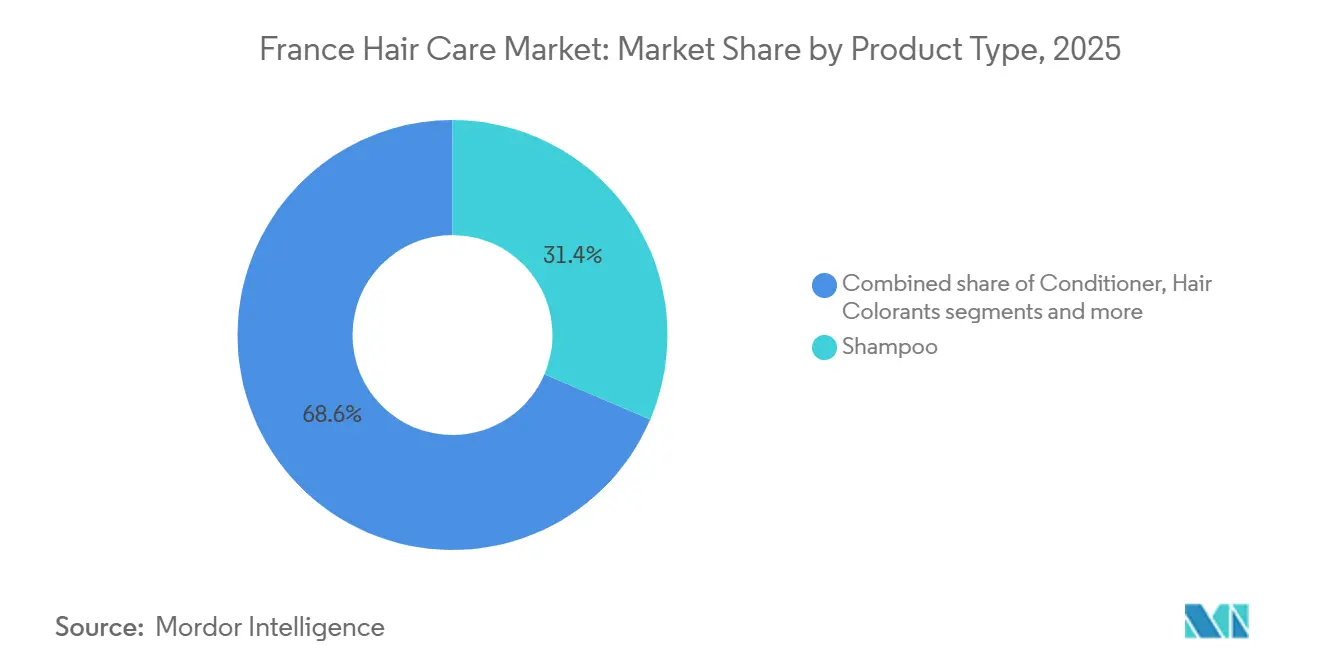

- By product type, shampoo led with 31.43% of the France hair care market share in 2025; hair styling products are projected to expand at a 4.23% CAGR through 2031.

- By category, mass products held 72.32% of the France hair care market in 2025, while premium hair care is poised for a 4.46% CAGR to 2031.

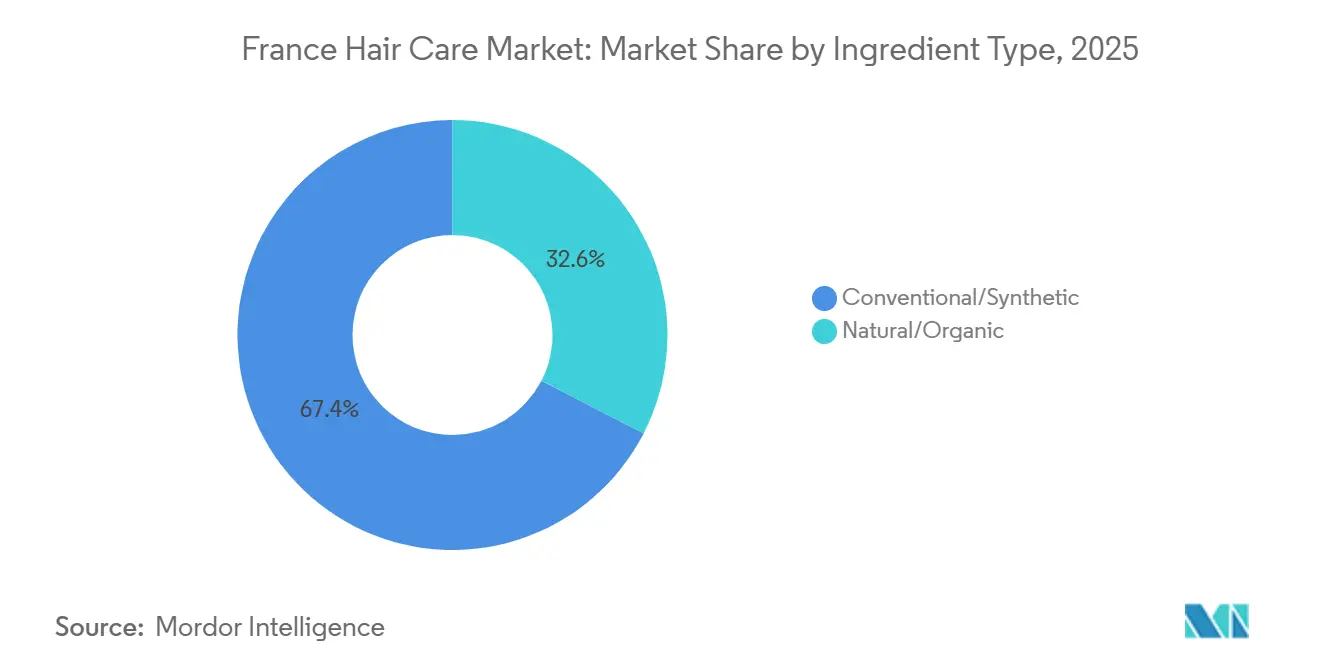

- By ingredient type, conventional/synthetic formulations accounted for 67.43% of 2025 sales; natural/organic lines are set to grow at a 4.78% CAGR through 2031.

- By distribution channel, supermarkets/hypermarkets captured 60.34% of the revenue in 2025; online retail stores are rising at a 5.03% CAGR as digital shopping gains traction.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Hair Care Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and organic formulations | +1.2% | France (strongest in major cities) | Medium term (2-4 years) |

| Growing scalp-health focus driving medicated shampoo | +0.9% | France (pharmacies and salons nationwide) | Short to medium term (1-3 years) |

| Demand for clean, sustainable, and ethical products | +0.8% | France (nation-wide; amplified by retailer pledges) | Medium term (2-4 years) |

| Technological innovations in product formulations | +0.6% | France (research and development hubs and premium salons) | Long Term (3-5 years) |

| Rising popularity of premium hair care products | +0.5% | France (notably Île-de-France) | Medium term (2-4 years) |

| Increased awareness of hair damage from environmental factors | +0.30% | France (urban pollution corridors) | Medium to long term (3-6 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and organic formulations

The France hair care market is undergoing significant changes, driven by a growing consumer preference for products made with natural and organic ingredients over synthetic alternatives. This trend is primarily influenced by increased awareness of ingredient safety and a stronger emphasis on environmental sustainability. Consumers in France are paying closer attention to product labels and demanding greater transparency from brands to make informed purchasing decisions. This shift is particularly pronounced among younger consumers, who are willing to pay a premium for hair care products they consider safer, cleaner, and more environmentally friendly. In response to these evolving preferences, L’Oréal has enhanced its focus on incorporating natural ingredients and ensuring sustainable sourcing. The company's 2023 Universal Registration Document highlights its commitment to Green Sciences and sustainable innovation, demonstrating its strategic alignment with changing consumer demands in the market.

Growing scalp-health focus driving medicated shampoo

Awareness of the link between scalp health and hair quality is increasingly influencing the France hair care market. Consumers, particularly younger individuals and those experiencing hair thinning, sensitivity, or scalp irritation, are shifting their focus toward therapeutic and preventive solutions rather than purely cosmetic products. This trend, often referred to as the “skinification” of hair care, mirrors the adoption of skincare-inspired routines, including multi-step processes such as cleansing, exfoliation, and targeted treatments. Consequently, the demand for medicated shampoos and scalp-focused formulations has grown significantly. These products incorporate ingredients aimed at addressing issues like dandruff, dryness, inflammation, and hair fall, while also promoting hair growth and shine. Brands such as L’Oréal Paris, with products like Elvive Glycolic Gloss, are utilizing science-backed ingredients to cater to both scalp and hair care needs, combining functional benefits with a premium market position. This emphasis on scalp health is driving innovation, premiumization, and increased consumer investment in products that deliver tangible results, positioning medicated shampoos as one of the fastest-growing segments in the France hair care market.

Demand for clean, sustainable, and ethical products

In the France hair care market, sustainability has evolved from a selling point to a core consumer expectation. This shift is reflected in various areas, including the use of responsibly sourced ingredients, eco-friendly packaging, greener manufacturing practices, and stronger commitments to social responsibility. Groupe Rocher has set notable goals, such as reducing greenhouse gas emissions by 67% by 2030 and improving transportation operations to minimize environmental impact. The market is witnessing growing demand for eco-friendly innovations, such as solid shampoos and refillable formats, which not only reduce waste but also align with consumer preferences for convenience and sustainability. Brands like Yves Rocher are responding to this demand by introducing sulfate-free product lines made with sustainably sourced ingredients, including organic chestnut milk and algae, which cater to the growing preference for natural and environmentally friendly formulations. This transformation is largely driven by the strong environmental values of French consumers, who are among the most eco-conscious in Europe, consistently prioritizing products that align with their sustainability principles.

Technological innovations in product formulations

The France hair care market is experiencing a notable transformation, driven by technological advancements that support the creation of new product categories and enhance existing formulations. For example, L’Oréal is leading this shift by leveraging its focus on Beauty Tech and Green Sciences to deliver innovative, science-based solutions. Through its Professional Products Division, L’Oréal has launched products such as Kérastase Première and Redken Acidic Color Gloss, which provide salon-quality results at home and set new benchmarks for performance and effectiveness. A prominent trend in the market is the integration of skincare-inspired ingredients into hair care products. Ingredients such as hyaluronic acid, niacinamide, and ceramides are being incorporated to address concerns like scalp health, hydration, and barrier repair. Premium products like Kérastase Nutritive combine plant-based proteins with niacinamide to enhance both hair fiber and scalp condition, demonstrating the convergence of skincare and haircare science. Furthermore, the adoption of AI-powered personalization tools is driving additional innovation in the market. These tools enable brands to offer highly customized hair care solutions tailored to individual consumer needs, including specific scalp conditions and hair textures. This development marks a new era of precision and personalization in the hair care industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of traditional at-home hair care solutions | -0.7 % | France (more pronounced in rural areas) | Medium term (2-4 years) |

| Proliferation of counterfeit products | -0.5 % | France (online marketplaces) | Short term (1-2 years) |

| High cost of premium hair care products | -0.4 % | France (price-sensitive households) | Short to medium term (1-3 years) |

| Stringent regulations on cosmetic ingredients | -0.3 % | France (European Union and national compliance) | Long term (3-5 years) |

| Source: Mordor Intelligence | |||

Adoption of traditional at-home hair care solutions

The France hair care market faces challenges from a segment of consumers, particularly older individuals and those in rural areas, who continue to prefer traditional at-home remedies over commercial products. These consumers often rely on generational knowledge and household ingredients, such as vinegar rinses, herbal infusions, and oil treatments, which directly compete with natural and organic hair care products. These remedies are perceived as cost-effective, easily accessible, and free from synthetic chemicals, making them appealing to this demographic. Although demand for natural and clean-label products is increasing, a portion of the market remains inclined toward DIY solutions, limiting the adoption of commercial alternatives. This trend poses a challenge for manufacturers aiming to expand in the natural segment, as their products must either align with or complement these traditional practices to effectively engage this consumer group. Additionally, building trust and educating these consumers on the benefits of commercial natural products may be necessary to encourage a shift in preferences.

Proliferation of counterfeit products

The France hair care market faces growing challenges from counterfeit products, which undermine consumer trust and damage brand equity, particularly in the premium segment. High-value products from luxury brands such as Kérastase and L’Oréal Professionnel are especially vulnerable, as counterfeiters exploit price differences to attract buyers. The expansion of e-commerce and social media marketplaces has exacerbated this issue, allowing counterfeiters to directly and widely access consumers. These platforms often lack stringent monitoring mechanisms, making it easier for counterfeit products to be listed and sold alongside genuine items, further confusing consumers. In addition to revenue losses, counterfeit hair care products pose significant safety concerns due to the use of unregulated ingredients and substandard manufacturing practices. Such products may contain harmful chemicals that can cause allergic reactions, skin irritation, or long-term health issues. According to the European Union Intellectual Property Office, counterfeit cosmetics and personal care products result in billions of euros in annual economic losses [1]Source: The European Union Intellectual Property Office (EUIPO), "Counterfeit goods cost EU industries billions of euros and thousands of jobs annually", euipo.europa.eu . France, known for its luxury beauty industry, is disproportionately affected, with its reputation for high-quality products at risk. Addressing this issue requires coordinated efforts from brands, retailers, and regulatory authorities to safeguard consumers, enforce stricter regulations, and preserve market integrity.

Segment Analysis

By Product Type: Shampoo Dominates While Styling Innovates

In 2025, the shampoo segment remains the largest category in the France hair care market, accounting for a 31.43% share and serving as a key component of daily hair care routines across various demographics. Its market leadership is supported by ongoing innovations in formulations, particularly in medicated, anti-dandruff, and scalp-focused shampoos, addressing consumer concerns such as hair thinning, scalp sensitivity, and overall scalp health. The segment also reflects a trend toward premiumization, with brands incorporating natural, clean-label, and sustainably sourced ingredients to align with evolving consumer preferences. Meanwhile, hair styling products are emerging as the fastest-growing segment, with a projected compound annual growth rate (CAGR) of 4.23% between 2026 and 2031. This growth is driven by technological advancements that enhance product performance, such as improved hold, reduced breakage, and enhanced natural shine and texture.

Trends like “glass hair” styles, anti-frizz treatments, and salon-inspired looks are gaining popularity, particularly among younger, fashion-conscious consumers. Leading brands, including Kérastase and L’Oréal Professionnel, are expanding their premium styling product lines with formulations inspired by skincare, combining styling benefits with nourishing and protective ingredients for the scalp and hair fibers. The segment is further benefiting from the adoption of AI-driven personalization tools, smart applicators, and multifunctional products, enabling consumers to achieve professional-quality results at home. This combination of performance, wellness, and personalization positions hair styling products as a high-growth category in the France market, complementing the established dominance of the shampoo segment.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Premium Segment Outpaces Mass Market

In 2025, mass-market products are projected to maintain their dominance in the France hair care market, representing 72.32% of the market share. However, the premium segment is anticipated to grow at a faster CAGR of 4.46% between 2026 and 2031, indicating a gradual shift in consumer preferences toward higher-quality, performance-oriented hair care products. This trend aligns with broader skincare-inspired consumer behaviors, as French consumers increasingly prioritize products that offer a combination of efficacy, innovation, and indulgence. Hair care remains a significant growth driver for major companies, for example, L’Oréal’s Consumer Products Division recorded a 12.6% like-for-like growth in 2023, highlighting the strategic importance of this segment.

The distinction between mass and premium categories is becoming less defined. Mass-market brands are introducing premiumized product lines featuring advanced formulations, innovative ingredients, and higher price points to appeal to aspirational consumers. In urban areas such as Paris, luxury hair care products are prominently showcased in specialized boutiques and department store beauty halls. These locations emphasize curated selections, immersive brand experiences, and personalized services, reinforcing the premium positioning and justifying higher price tags. This blending of accessibility and luxury is transforming competitive dynamics, as both mass-market and prestige brands aim to attract consumers who value quality, effectiveness, and experiential elements in their hair care products.

By Ingredient Type: Natural Formulations Gaining Ground

In 2025, the conventional/synthetic ingredient segment is expected to maintain its dominance in the France hair care market, accounting for a 67.43% share. However, natural/organic formulations are anticipated to grow at a higher CAGR of 4.78% from 2026 to 2031, reflecting a shift in consumer preferences toward cleaner, safer, and more environmentally sustainable products. This trend is driven by increasing awareness of ingredient safety and sustainability, with younger consumers, particularly Gen Z, playing a significant role by prioritizing eco-friendly practices in their purchasing decisions.

Industry players are actively adapting to this changing landscape. For instance, Yves Rocher introduced six new sulfate-free hair care lines in March 2023, incorporating botanical ingredients such as white lupin, ginseng, and organic chestnut milk. While natural formulations have historically struggled to match the performance of synthetic ingredients, particularly in areas like styling and hold, recent technological advancements, such as plant-based silicone alternatives and green preservatives, are addressing these challenges. These innovations are enabling brands to offer high-performance, sustainable products that meet evolving consumer demands, positioning natural and organic hair care as a rapidly growing segment in the France market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Distribution Channel: Digital Transformation Reshapes Retail

In 2025, supermarkets/hypermarkets dominate the France hair care distribution market, accounting for a 60.34% share. This dominance is attributed to their extensive product range and convenience for everyday shoppers. However, online retail is emerging as the fastest-growing distribution channel, with a projected CAGR of 5.03% from 2026 to 2031, reflecting evolving consumer purchasing behaviors. E-commerce is already a significant contributor to sales for major players. For instance, L’Oréal reports that 27% of its global sales currently come from online channels, with plans to increase this figure to 50% in the near future. Additionally, EuroCommerce data shows that the proportion of French consumers purchasing consumer goods online, including hair care products, rose from 77% in 2020 to 83% in 2023, highlighting the growing preference for digital shopping [2]Source: Euro Commerce, "EUROPEAN E-COMMERCE REPORT 2023", eurocommerce.eu.

Retailers in France are adapting to this shift by implementing omnichannel strategies, such as online ordering combined with click-and-collect services, to merge the convenience of digital shopping with the immediacy of physical stores. Specialty stores continue to hold relevance by offering curated product selections and expert guidance, particularly for premium and professional hair care lines, catering to consumers seeking personalized advice. Brands like L’Oréal are utilizing Beauty Tech innovations, such as virtual try-on tools and personalized diagnostics, to enhance in-store experiences and engage digitally savvy consumers, effectively bridging the gap between online convenience and offline expertise.

Geography Analysis

The France hair care market showcases considerable regional differences that influence product preferences and purchasing behaviors across the nation. Cities like Paris and Lyon serve as key innovation hubs where premium products and international trends are first introduced before spreading to smaller towns and rural areas. These urban markets, marked by higher disposable incomes and greater exposure to global beauty trends, act as strategic entry points for new brands and product innovations. The market's expansion is supported by France's deeply rooted beauty culture and a sophisticated consumer base that prioritizes quality and performance over price.

Variations in water hardness across different regions of France create diverse consumer requirements. In areas with harder water, there is a demand for specialized products to address issues such as mineral buildup and color fading. This has led to the development of chelating shampoos and protective treatments tailored to these specific needs. The distribution network also varies by region, with specialty and department stores being more prominent in urban areas, while supermarkets and hypermarkets dominate suburban and rural regions. For instance, the International Trade Administration reported that France had over 5,716 supermarkets in 2023 [3]Source: International Trade Administration, "France Country Commercial Guide", trade.gov. E-commerce has emerged as a vital channel, bridging geographic disparities and enabling consumers across the country to access a wider variety of products regardless of their location.

The France hair care market also benefits from the country's prominent position in the global beauty industry, with Paris acting as a trendsetting center that influences product development and marketing strategies worldwide. This status attracts significant investment in research and innovation, with leading companies like L'Oréal operating advanced research facilities in France. French consumers exhibit distinct hair care preferences, with studies indicating that individuals in France experience higher stress and reduced well-being due to damaged or dry hair compared to consumers in other countries. This has fueled strong demand for reparative and moisturizing treatments within the market.

Competitive Landscape

The France hair care market is predominantly controlled by multinational corporations and is currently undergoing a phase of high concentration. L'Oréal stands as the leading player in this market, offering a diverse range of products that span mass-market, premium, and professional categories. Alongside L'Oréal, other major companies such as Unilever, Procter & Gamble, Beiersdorf, and Pierre Fabre are intensifying their efforts to innovate and develop new products aimed at attracting and retaining a loyal consumer base. A key trend shaping the market is the increasing emphasis on premiumization, where mass-market brands are introducing upscale product lines to align with the growing consumer preference for superior-quality hair care products. This shift reflects a broader trend of consumers seeking enhanced value and performance in their hair care routines.

Within the market, niche segments addressing specific consumer needs, such as products for curly and textured hair, are emerging as highly promising areas for growth. These segments are witnessing a surge in demand, driven by a growing awareness and appreciation for tailored solutions that cater to diverse hair types. This trend has not gone unnoticed by major players, who are beginning to invest in these underserved categories. A notable example is the launch of Innovative Beauty Group's Curls Matter, which debuted in 150 Monoprix stores across France in February 2025. This development underscores the untapped potential within this segment and highlights the increasing focus on inclusivity and diversity in product offerings.

Technological advancements are playing a pivotal role in reshaping the dynamics of the French hair care market. L’Oréal has been at the forefront of this transformation, leveraging its Beauty Tech ecosystem to integrate advanced technologies such as AI diagnostics, personalized e-commerce platforms, and sustainable refillable packaging solutions. These innovations are powered by real-time consumer insights, enabling the company to streamline product development processes and deliver a more tailored and engaging customer experience. This tech-driven approach not only enhances operational efficiency but also strengthens consumer loyalty by addressing their evolving needs and preferences. In response to these advancements, other leading companies in the market are making significant investments in specialized digital platforms and forming partnerships with data science startups. These initiatives aim to accelerate innovation, improve adaptability to rapid digital changes, and maintain competitiveness in an increasingly technology-oriented market environment.

France Hair Care Industry Leaders

-

L'Oréal S.A.

-

Unilever PLC

-

Procter and Gamble Company

-

Pierre Fabre Group

-

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Innovative Beauty Group’s (IBG) brand incubator, IBG Lab, has launched a curly hair care range, Curls Matter, in France. This product line is now available in approximately 150 Monoprix stores across the country. It is designed to cater to all curl types, ranging from loose waves to tight coils, through a three-step system comprising Wash, Treat, and Define products. The range is formulated to meet the specific needs of curly hair, featuring naturally derived, vegan formulas with a minimum of 90% natural ingredients. The products are free from silicones and mineral oils, aiming to nourish, protect, and define curls. Additionally, the packaging incorporates sustainability principles, using at least 30% recycled plastics and a design focused on recyclability.

- February 2024: L'Oréal has unveiled Kérastase Première, a luxurious hair care product line, in France. This range of products is designed with advanced molecular technology aimed at repairing the structural integrity of hair. The introduction of this line is regarded as the company's most significant innovation in product development over the last five years.

- November 2024: Vichy's Dercos brand has introduced a new anti-dandruff haircare collection, expanding its offerings to include conditioner and serum formulations in addition to shampoo. This range utilizes proprietary hair science developed by L’Oréal. The anti-dandruff shampoo contains micronized selenium sulfide to address dandruff at its source, along with niacinamide and glycerin to soothe and hydrate the scalp. The collection is formulated to address scalp concerns and is suitable for various hair and scalp types, including sensitive and color-treated hair.

- May 2023: Luxury French beauty brand Guerlain, a subsidiary of LVMH, has entered the prestige hair care market with a new premium product line. The Abeille Royale Scalp and Hair Collection, introduced in June 2023, expands the brand’s renowned Abeille Royale skincare technology to hair care. This range incorporates black bee honey repair technology into formulations designed to address both hair and scalp needs. The collection features a shampoo, conditioner, hair mask, and a scalp brush, all positioned at premium price points and targeting consumers seeking luxury performance and scalp health solutions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the France hair care market as retail and salon purchases of shampoos, conditioners, colorants, styling products, scalp treatments, and allied leave-in or rinse-off formats formulated for human hair. Devices, straighteners, and purely therapeutic pharmaceuticals fall outside this boundary, letting us keep the lens squarely on finished cosmetic formulations.

Scope exclusion: Packs sold strictly as hotel amenities or medical prescriptions are not counted.

Segmentation Overview

-

By Product Type

- Shampoo

- Conditioner

- Hair Colorants

- Hair Styling Products

- Other Product Types

-

By Category

- Premium Products

- Mass Products

-

By Ingredient Type

- Natural/Organic

- Conventional/Synthetic

-

By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

Detailed Research Methodology and Data Validation

Primary Research

Multiple touchpoints with French dermatologists, salon owners, specialty store buyers, and R&D chemists in Paris, Lyon, Marseille, and Lille help us validate penetration of natural formulas, premium price elasticity, and online channel momentum before consolidating our assumptions.

Desk Research

Our analysts first draw quantitative anchors from public domains such as INSEE retail turnover files, Eurostat import-export codes for HS 330510/330520, and French Customs shipment logs, which reveal volume flows and average unit values. Trade bodies including Fédération des Entreprises de la Beauté and Cosmetics Europe supply brand-level shipment shares and regulatory updates that shift ingredient demand. Scientific context comes from journals like the International Journal of Cosmetic Science alongside patent counts accessed through Questel, while D&B Hoovers provides company revenue splits that bridge brand sales to category totals. This list is illustrative; numerous other open publications and paid databases inform the desk work.

A second sweep reviews earnings calls, investor decks, key retailer catalogs, and advertising spend trackers, thereby capturing new product launches and pricing dispersion ahead of our model build.

Market-Sizing & Forecasting

The top-down model starts with 2024 household expenditure on beauty, adjusts for hair care's share, and is rebuilt through a "volume × average selling price" roll-up for shampoos, conditioners, colorants, and styling aids to cross-check totals. Key variables include salon visitation rate per capita, online share of beauty sales, launches of sulfate-free SKUs, scalp health incidence, average shampoo ASP, and disposable income growth. Where distributor or brand data are partial, interpolations use three-year moving averages that are then tested against supplier order books gathered in primary calls.

For 2025-2030, we employ multivariate regression with CPI-Beauty, e-commerce penetration, premium share shift, and per capita salon spend as predictors, supplemented by scenario analysis for economic shocks.

Data Validation & Update Cycle

Outputs pass variance checks against customs values, Nielsen channel indices, and historic Euromonitor splits. A senior reviewer at Mordor Intelligence signs off after anomaly resolution, and the file is refreshed annually or sooner if price controls, VAT shifts, or raw material shocks alter the outlook.

Why Our France Hair Care Baseline Holds Firm

Published estimates differ because firms choose dissimilar product baskets, currency baselines, and refresh cadences.

Our disciplined scope and annual update cadence minimize volatility.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.07 B (2025) | Mordor Intelligence | - |

| USD 2.47 B (2024) | Regional Consultancy A | Includes scalp care pharmaceuticals and hair loss devices, inflating totals |

| USD 2.84 B (2024) | Trade Journal B | Counts duty-free and hotel amenity volumes; conversion at fixed €1 = USD 1.10, ignoring 2024 FX swings |

These comparisons show how Mordor's focused scope, live exchange rates, and dual-path validation give decision makers a balanced, transparent baseline they can reliably build upon.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the France hair care market in 2026?

The France hair care market size reached USD 2.07 billion in 2026 and is on track to hit USD 2.49 billion by 2031 at a 3.76% CAGR.

Which product type is growing fastest?

Hair styling products are forecast to register the fastest 4.23% CAGR through 2031, outperforming traditional cleansing segments.

What drives the shift toward natural formulations?

Consumer label scrutiny and COSMOS ORGANIC certification standards, combined with REACH restrictions on synthetics, push natural/organic SKUs to a projected 4.78% CAGR.

Which region spends most on premium hair care?

Île-de-France leads prestige consumption thanks to higher disposable incomes, dense pharmacy networks, and tourist traffic.