Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

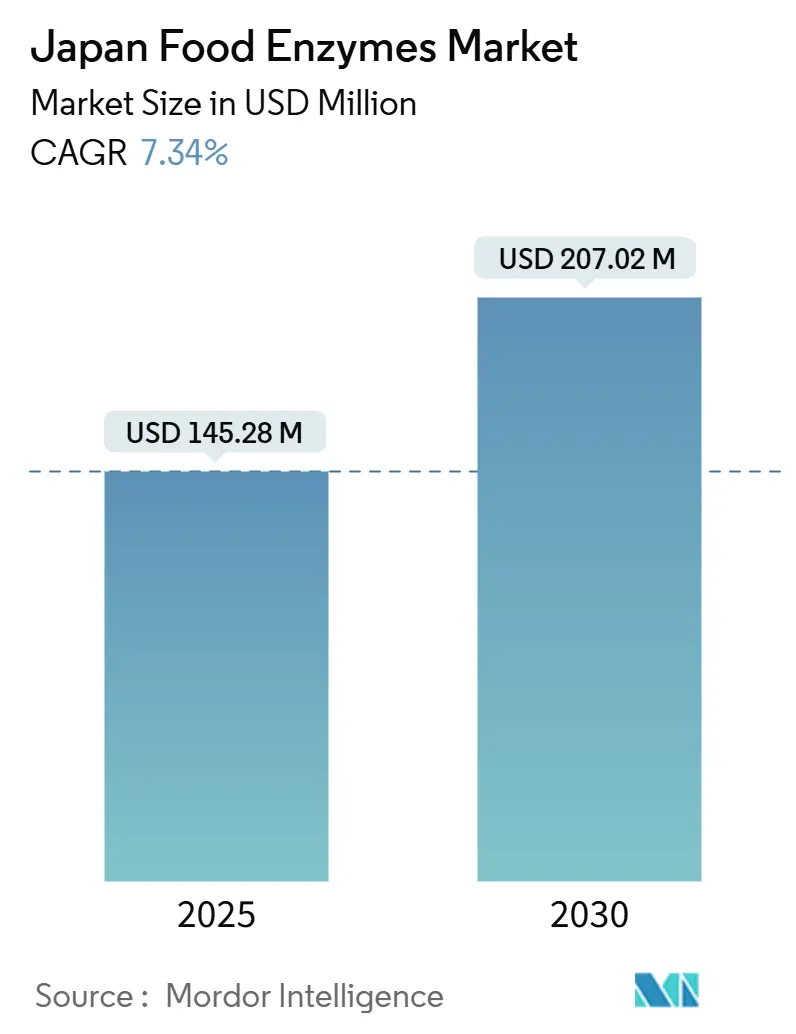

| Market Size (2025) | USD 145.28 Million |

| Market Size (2030) | USD 207.02 Million |

| Growth Rate (2025 - 2030) | 7.34% CAGR |

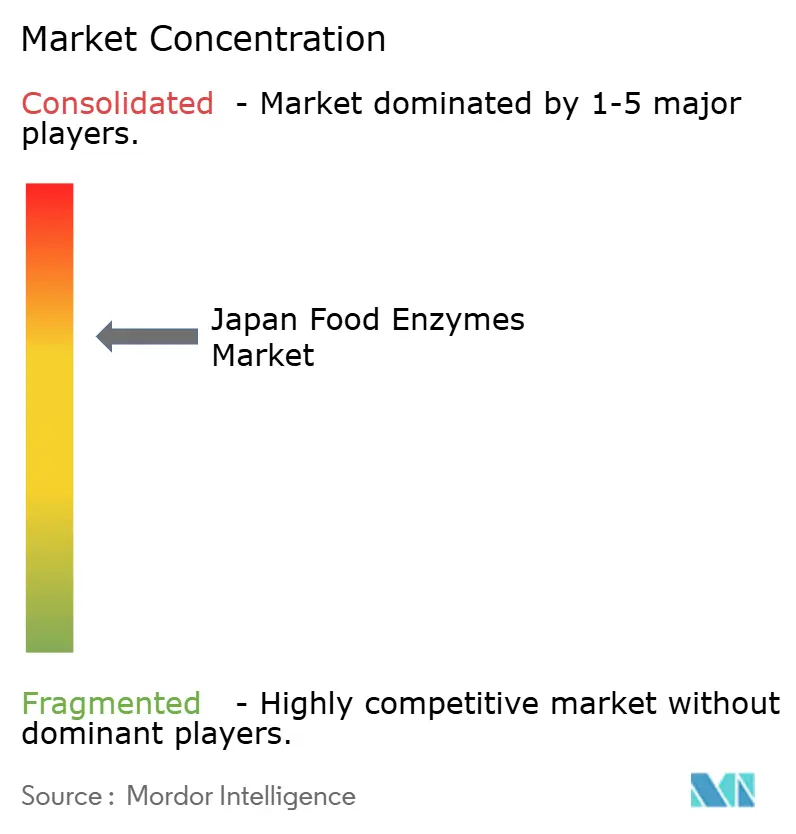

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Food Enzymes Market Analysis by Mordor Intelligence

The Japan food enzymes market size stood at USD 145.28 million in 2025 and is projected to reach USD 207.02 million by 2030, advancing at a 7.34% CAGR during the forecast period. Robust demand stems from the country’s centuries-old fermentation heritage, sustained investments in biocatalyst engineering, and an aging demographic that values digestibility and nutrient bioavailability. Carbohydrases dominate value because amylases improve starch processing economics in the USD 12 billion bakery sector, while lipases record the fastest momentum as confectionery and infant-formula producers replace chemical hydrogenation. Clean-label regulation, rising energy prices, and corporate moves toward process efficiency underpin enzyme substitution for chemical additives.

Key Report Takeaways

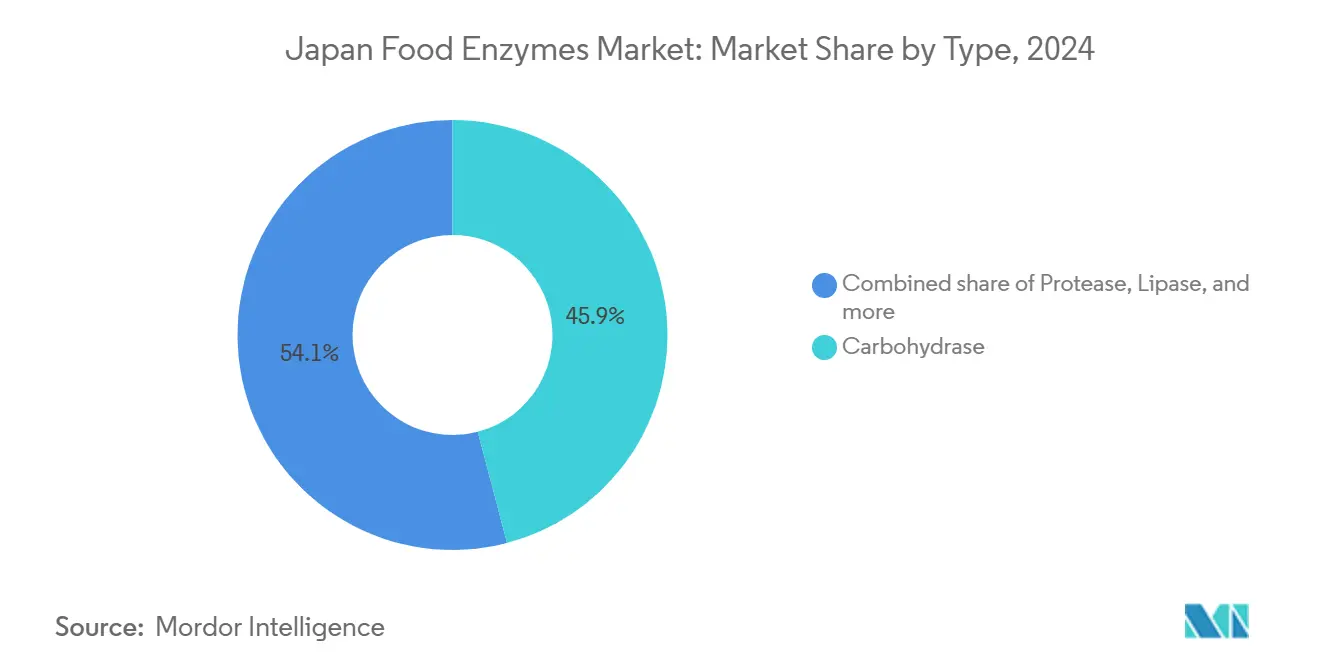

- By type, carbohydrases held 45.92% of the Japan food enzymes market share in 2024; lipases are forecast to grow at a 7.81% CAGR to 2030.

- By form, powders captured 59.20% share of the Japan food enzymes market size in 2024, while liquids are projected to expand at an 8.52% CAGR through 2030.

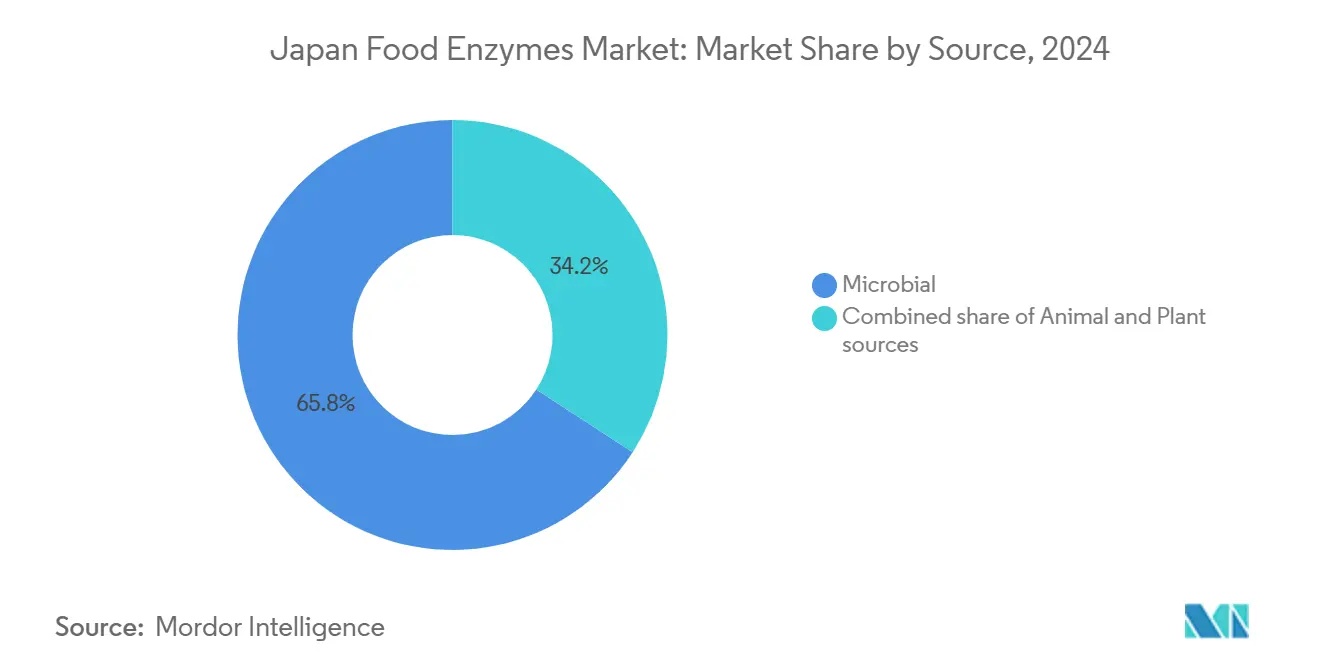

- By source, microbial enzymes accounted for 65.81% of the Japan food enzymes market size in 2024 and animal-derived enzymes are advancing at an 8.93% CAGR to 2030.

- By application, bakery and confectionery led with 35.14% value in 2024; beverages are the fastest riser at a 7.92% CAGR up to 2030.

Japan Food Enzymes Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and quality focus in bakery and traditional products | +0.9% | Tokyo, Osaka, Nagoya metropolitan areas | Medium term (2-4 years) |

| Strong tradition of fermented foods relying on enzyme technology | +1.2% | Heritage clusters in Kyoto, Ishikawa, Akita | Long term (≥4 years) |

| Shift toward clean-label formulations replacing chemical additives | +1.4% | National, premium retail channels | Short term (≤2 years) |

| Aging population driving demand for digestible and nutrient-enhanced foods | +1.1% | Rural prefectures with 35%+ elderly | Long term (≥4 years) |

| Innovation blending traditional fermentation with modern enzymes for premium products | +0.8% | Craft hubs in Kyoto, Kanazawa, Takayama | Medium term (2-4 years) |

| Increased usage of enzymes to enhance process efficiency, yield, and energy saving | +1.0% | Large-scale manufacturing hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Premiumization and Quality Focus in Bakery and Traditional Products

Japan's bakery sector is moving towards premiumization, where enzyme technology is now seen as a tool to enhance quality rather than just reduce costs. Consumers are paying 30-50% more for artisan breads that stay soft for longer. This demand is encouraging bakers to use maltogenic amylases, which prevent staling by slowing down starch retrogradation—something mass-market producers often ignore. In wagashi production, enzyme-modified starches help confectioners create the desired mochi-like texture (Q-elasticity). Previously, this texture required 72 hours of fermentation, but enzymes have reduced the process time by 60% without affecting the quality, allowing these products to sell for USD 8-12 per 100g. UNESCO's 2024 recognition of traditional sake-brewing techniques as an Intangible Cultural Heritage has also increased interest in enzyme-assisted fermentation. As a result, 23 new sake breweries have started enzyme-optimized production lines in 2024 to meet a 14% year-on-year rise in export demand[1]UNESCO, "Traditional knowledge and skills of sake-making with koji mold in Japan", ich.unesco.org.

Strong Tradition of Fermented Foods Relying on Enzyme Technology

Japan's fermentation industry, which includes products like sake, miso, soy sauce, and natto, generates USD 6.2 billion in annual revenue. This strong market ensures a steady demand for enzyme suppliers, unlike the fluctuations often seen in Western markets. Aspergillus oryzae, also known as the koji mold, plays a key role in these processes by producing over 50 enzymes, including proteases, amylases, and lipases. This has created a cultural understanding of enzyme use, making it easier to adopt enzymes in other food categories. In 2024, the Ministry of Economy, Trade and Industry identified fermentation technology as a priority sector in its biotechnology roadmap. To support this, it allocated USD 81 million in subsidies to increase enzyme production capacity and promote R&D collaborations between traditional brewers and biotech companies.

Shift Toward Clean-Label Formulations Replacing Chemical Additives

Regulatory changes and growing consumer activism are reducing Japan's reliance on synthetic food additives, creating opportunities for enzymes, which are seen as "natural processing aids" by consumers. In 2024, the Consumer Affairs Agency updated food labeling rules, requiring front-of-pack disclosure for 12 chemical emulsifiers and preservatives that were previously exempt. This change has led to reformulation efforts for 40% of packaged food SKUs[2]Consumer Affairs Agency Japan. "Food Labeling Guidelines." caa.go.jp. Enzymes like phospholipase and transglutaminase are now replacing chemical emulsifiers, with phospholipase used in mayonnaise and transglutaminase in processed meats. Although manufacturers have faced an 8-12% increase in costs, they have offset this by charging 15-20% more for products labeled "additive-free." In 2024, Amano Enzyme launched a plant-based transglutaminase, addressing concerns about animal-origin ingredients in traditional formulations. Within nine months, this product captured 18% of Japan's USD 45 million meat-binder market, showing how enzyme innovations can outperform chemical alternatives when aligned with clean-label trends.

Aging Population Driving Demand for Digestible and Nutrient-Enhanced Foods

Japan's aging population is driving the demand for enzymes that improve digestive health and nutrient absorption. In 2024, 29.1% of the population is aged 65 or older, and this figure is expected to rise to 35% by 2040, making Japan one of the most aged societies globally. To meet the needs of this demographic, food manufacturers are incorporating proteases and lactases into their products to reduce digestive strain and enhance nutrient uptake. Research shows that enzyme-supplemented meals can increase protein absorption by 30% in elderly individuals, addressing a critical nutritional challenge in this age group. In 2024, Japan's Ministry of Health, Labour and Welfare approved seven new enzyme-enhanced "Foods for Specified Health Uses" (FOSHU)[3]Ministry of Health, Labour and Welfare (MHLW). "Food Safety and FOSHU Approvals." mhlw.go.jp. Among these, a lactase-fortified yogurt stood out, generating USD 56 million in its first year by catering to the 40% of elderly Japanese who are lactose intolerant. This trend highlights the growing importance of functional foods in addressing the health needs of Japan's aging population.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approvals and labeling | -0.7% | National, governed by MHLW and Consumer Affairs Agency | Medium term (2-4 years) |

| Supply chain dependency and batch inconsistency | -0.5% | National, acute for imported enzyme preparations | Short term (≤ 2 years) |

| Cheaper chemical additive substitutes | -0.4% | National, concentrated in cost-sensitive food manufacturing segments | Short term (≤ 2 years) |

| Intellectual property and patent-related disputes in enzyme technology | -0.3% | National, with spillover effects from global patent litigation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approvals and Labeling

Japan's enzyme approval framework presents significant technical and economic challenges, delaying market entry by 18-36 months compared to the EU and US. The Ministry of Health, Labour and Welfare requires new enzyme preparations to undergo a toxicological review by the Food Safety Commission. This process includes 90-day feeding studies and allergenicity tests, costing USD 200,000-400,000 per submission. These high costs give an advantage to established companies with extensive dossier libraries. Additionally, the Consumer Affairs Agency's 2024 labeling rules now require ingredient panels to specify the source organisms of enzymes (e.g., "derived from Aspergillus niger"). This change has caused consumer confusion, leading to a 12-15% drop in sales for products using less-recognized microbial strains. As a result, the stringent regulations have created a two-tier market. Approved enzymes are priced 20-30% higher than chemically equivalent alternatives, while innovative but unapproved enzymes, despite offering better performance, remain unused in the market.

Supply Chain Dependency and Batch Inconsistency

Japan depends on imports for 60% of its enzyme concentrates, leaving manufacturers exposed to risks like supply disruptions and inconsistent quality, which affect process reliability. The 2024 Red Sea shipping crisis significantly increased lead times for European enzyme shipments, rising from 35 days to 68 days. As a result, Japanese food processors had to increase their safety stock levels from the standard 45 days to 90-120 days, tying up USD 180 million in working capital across the industry. Additionally, microbial fermentation often results in batch-to-batch enzyme activity variations of ±15-20%, forcing manufacturers to use 25% more enzymes to meet minimum performance requirements. This practice eliminates 30-40% of potential cost savings. In February 2024, Kerry Group acquired Chr. Hansen's lactase business for €150 million (USD 163 million). This acquisition aims to localize enzyme production for Asian customers, highlighting the growing importance of supply chain resilience as a key competitive advantage.

Segment Analysis

By Type: Carbohydrase Dominance Anchored in Starch Processing, Lipase Gains in Specialty Fats

In 2024, carbohydrase enzymes contributed 45.92% to the market value, highlighting Japan's position as the world's third-largest starch processor. Japan produces 2.8 million tons of starch annually, primarily used in glucose syrup, maltodextrin, and modified starch applications. Amylases, particularly α-amylases, dominate this segment by enabling liquefaction at 95°C, which is lower than the 105°C required for acid hydrolysis. This process reduces energy costs by JPY 1,200 per ton of starch processed, resulting in significant savings across Japan's 47 starch refineries. Pectinases and cellulases, while niche, play a crucial role in fruit juice clarification. These enzymes increase juice yield by 8-12% and reduce filtration time by 40%, which is essential for processors handling 2.1 billion liters of juice annually, especially during seasonal production peaks that strain capacity.

Lipase enzymes are experiencing the fastest growth among enzyme types, with a 7.81% CAGR projected through 2030. This growth is driven by their use in producing structured lipids for infant formula and enzymatic interesterification in confectionery fats. In 2024, Fuji Oil Holdings adopted immobilized lipases to produce cocoa butter equivalents. This innovation reduced trans-fat content to below 0.5% while maintaining the desired snap and melt profile, which previously required chemical hydrogenation with 2-4% trans-fat levels. This breakthrough allowed compliance with Tokyo's 2025 trans-fat labeling mandate without incurring reformulation costs. Additionally, in April 2024, Nagase acquired Hayashibara for JPY 40 billion (USD 270 million), expanding its lipase production capacity. This acquisition targets the USD 180 million structured lipid market, where the enzymatic synthesis of 1,3-dioleoyl-2-palmitoylglycerol (OPO) for infant formula commands a premium price of USD 45-60 per kilogram, compared to USD 12-18 for conventional vegetable oils.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Powder Stability Dominates, Liquid Gains in Automated Dosing Systems

In 2024, powder enzymes accounted for 59.20% of the market share, primarily due to Japan's humid subtropical climate. Liquid enzyme formulations tend to lose 20-30% of their activity over a 6-month shelf life, whereas spray-dried powders stored at ambient temperatures only experience a 5-10% loss. Powder enzymes also align well with Japan's just-in-time manufacturing practices. For example, 25-kilogram bags of powder require 60% less warehouse space compared to equivalent liquid volumes. This not only saves space but also eliminates the need for cold-chain logistics, which can add JPY 800-1,200 per ton to distribution costs. Additionally, the bakery and confectionery industries, which represent 35.14% of total enzyme demand, prefer powder enzymes. Powders blend easily with flour and sugar in ribbon mixers, while liquid enzymes risk uneven distribution and the formation of hot spots.

Liquid enzyme formulations are growing rapidly, with an 8.52% CAGR projected through 2030. This growth is driven by beverage and dairy processors adopting inline dosing systems, which reduce labor costs by 15-20% in facilities processing over 50,000 liters daily. In cold-pressed juice production, liquid pectinases and cellulases enable 30-40% faster substrate penetration, cutting enzymatic treatment times from 4-6 hours to just 90-120 minutes. This shorter cycle time increases daily throughput by 25% without requiring additional tank investments. In February 2024, Kerry Group acquired lactase enzyme assets for USD 163 million, including liquid formulation technology designed for ultra-high-temperature dairy processing. This acquisition targets Japan's USD 8.5 billion dairy market, where lactose-free products have grown from a 7% to a 12% market share between 2020 and 2024.

By Source: Microbial Enzymes Dominate on GRAS Status, Animal Enzymes Resurge in Artisanal Applications

In 2024, microbial-sourced enzymes accounted for 65.81% of the market value, driven by Japan's regulatory support for Generally Recognized as Safe (GRAS) biocatalysts. This preference aligns with Japan's long-standing expertise in using Aspergillus oryzae for traditional products like sake, miso, and soy sauce. Aspergillus niger and Bacillus subtilis strains dominate the production of industrial amylases and proteases, contributing 70% of the supply. These strains achieve fermentation yields of 150-200 grams of enzyme per liter of broth, enabling competitive pricing of USD 8-12 per kilogram compared to USD 25-40 for animal-derived enzymes. In 2024, the Ministry of Health, Labour and Welfare approved 7 new microbial enzyme preparations for FOSHU (Foods for Specified Health Uses) status. This approval further strengthened the position of microbial enzymes, as the 12-18 month clinical trial requirement favors established microbial platforms over newer animal-based alternatives.

Animal-derived enzymes are experiencing the fastest growth among enzyme sources, with a CAGR of 8.93% projected through 2030. This growth is fueled by demand from artisanal cheese makers and premium meat processors who value the authentic flavors that microbial enzymes cannot replicate. For example, rennet derived from calf stomach lining remains the preferred choice for producing Parmigiano-Reggiano-style hard cheeses. It is priced at USD 180-240 per kilogram, significantly higher than the USD 40-60 for microbial chymosin. Despite the cost difference, 15% of Japan's craft cheese producers justify this premium through Protected Designation of Origin-style branding. Similarly, porcine pepsin and trypsin are gaining popularity in premium cured meat production. These enzymes provide specific proteolytic activity that enhances umami intensity by 30-40% compared to microbial proteases. This improvement supports retail prices of JPY 8,000-12,000 per kilogram for artisanal salami and prosciutto.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Bakery Leads on Volume, Beverages Accelerate on Health Positioning

In 2024, bakery and confectionery applications accounted for 35.14% of enzyme demand, driven by Japan's high bread consumption of 45 kilograms per capita annually and the growing use of enzyme-modified starches in wagashi (traditional sweets) for better texture. Maltogenic amylases extended bread softness from 2-3 days to 5-7 days, reducing waste by 15-20% in convenience store networks with 180,000 outlets daily. This efficiency saved the retail sector JPY12-18 billion (USD 81-122 million) annually. Xylanases improved dough machinability by cutting water absorption and mixing time by 12-18%, enabling production lines to increase output from 8,000 to 10,000 loaves per hour without extra investment. In the dairy sector, lactose-free products captured 12% of Japan's USD 8.5 billion dairy market in 2024. Lactase-treated milk, priced at JPY 280-340 per liter (USD 1.90-2.30), commanded a 50-60% premium over conventional milk, appealing to the 40% of elderly Japanese with lactose intolerance.

The beverage sector was the fastest-growing application, with a 7.92% CAGR projected through 2030. Pectinase and cellulase adoption in cold-pressed juice production drove 18% year-on-year growth in 2024, as health-conscious consumers paid 40-60% premiums for enzyme-clarified products with longer shelf lives. Enzyme treatment increased juice yield by 8-12% and reduced filtration time by 40%, helping processors manage peak production during the June-August citrus harvest. In the meat sector, proteases improved tenderization, while transglutaminase achieved 95% protein binding efficiency in restructured products like ham and sausages, outperforming phosphate-based binders by 15-20 percentage points amid clean-label demand. In oil and fats processing, lipases enabled structured lipid synthesis and interesterification, reducing trans-fat content to below 0.5%, compared to 2-4% with chemical hydrogenation. This ensured compliance with Tokyo's 2025 trans-fat labeling mandate.

Geography Analysis

Tokyo, Osaka, and Nagoya, the key hubs of Japan's metropolitan industrial corridors, dominate enzyme consumption due to their strong food manufacturing presence and proximity to R&D facilities. These factors enable quick customization of enzyme formulations. Tokyo's Kanto region, which houses most of Japan's food processing plants, serves as the main testing ground for enzyme innovations. Suppliers in this region are strategically located within a 2-hour transit of major clients, ensuring a fast 4-6 week product development cycle. This level of responsiveness gives urban manufacturers a significant edge over rural competitors. Osaka's Kansai region, with its 400-year history in producing sake, miso, and soy sauce, has embraced enzymes in traditional fermentation processes. The region's expertise in cultivating Aspergillus oryzae has led to advanced enzyme integration techniques.

Rural areas like Tohoku, Hokkaido, and Kyushu face challenges such as aging populations, 35-42% of residents are over 65 years old, and limited access to technical enzyme support, which urban manufacturers benefit from. However, these regions are emerging as growth areas for digestive enzyme applications. Local food cooperatives are reformulating products for elderly consumers by using proteases and lactases to improve nutrient absorption. This strategy is supported by data from the Ministry of Health, Labour and Welfare, which shows that malnutrition rates among the rural elderly are 27.2%, compared to 18.4% in urban areas. Hokkaido, which produces 54% of Japan's raw milk, is increasingly adopting lactase enzymes to create lactose-free products. In 2024, lactose-free dairy products accounted for 15% of Hokkaido's regional dairy sales, surpassing the national average of 12%. This trend reflects the growing focus on digestibility among aging farmers and consumers.

Traditional fermentation hubs in Kyoto, Ishikawa, and Akita prefectures are becoming high-value enzyme markets. Craft producers in these regions combine traditional koji cultivation methods with precise enzyme dosing to create premium products that sell for 3-5 times the price of industrial alternatives. Kyoto, with over 180 artisan miso and soy sauce breweries, is using exogenous proteases to reduce umami development time from 18 months to just 6 months while maintaining flavor complexity. These enzyme-enhanced products are exported to European and North American markets at prices ranging from USD 40-60 per kilogram. In Ishikawa, sake breweries in the Noto Peninsula began using glucoamylases in 2024 to address an 8% annual decline in Yamada Nishiki rice harvests caused by climate change. This adoption has helped maintain alcohol yields while preserving the mineral-rich flavor profiles that win Gold medals at the International Wine Challenge sake competitions.

Competitive Landscape

The Japan food enzymes market is moderately consolidated, with a limited number of major multinational and domestic players shaping competition through technological expertise, targeted innovation, and long-standing relationships with food manufacturers. Global enzyme leaders such as Novozymes A/S, DSM-Firmenich AG, Nagase & Co., Ltd., AB Enzymes GmbH, and Amano Enzyme Inc. maintain a strong foothold in the country, leveraging advanced R&D capabilities and tailored enzyme solutions for bakery, dairy, beverage, and processed food applications. Their ability to deliver customized functional performance—whether improving texture, enhancing shelf life, or enabling cleaner labels—positions them as preferred partners for large Japanese food producers.

Domestic firms and regional enzyme blenders also contribute to the market structure, offering niche or application-specific enzyme products designed for traditional Japanese foods such as miso, soy sauce, fish products, and fermented beverages. While smaller players lack the scale of multinational competitors, they often thrive by catering to highly localized needs and aligning with Japan’s strong emphasis on precision, quality, and consistency. This creates a complementary competitive landscape where both global and local companies coexist, each addressing different segments of demand.

Market consolidation is reinforced by high entry barriers, including strict regulatory standards, the need for sophisticated fermentation and production technologies, and the high expectations of food manufacturers for performance consistency. As Japan’s food industry continues shifting toward automation, clean-label formulations, and efficiency improvements, established enzyme players with proven technical reliability are expected to maintain their dominant positions. However, increased interest in specialty enzymes and innovations supporting plant-based, reduced-sugar, and high-protein foods may create new opportunities for emerging competitors and collaborative partnerships.

Japan Food Enzymes Industry Leaders

-

Novozymes A/S

-

DSM-Firmenich AG

-

Nagase & Co., Ltd.

-

AB Enzymes GmbH

-

Amano Enzyme Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Novonesis announced its plan to acquire DSM-Firmenich’s stake in the Feed Enzyme Alliance for EUR 1.5 billion (USD 1.6 billion), marking a significant strategic move that strengthens its position in the global enzyme market, including Japan.

- January 2024: The merger of Novozymes and Chr. Hansen has completed, forming of Novonesis, a unified global biosolutions leader with an expanded and highly specialized portfolio in food enzymes. The combined entity brings together Novozymes’ deep expertise in industrial enzyme innovation and Chr. Hansen’s strong capabilities in cultures and fermentation, creating a powerful platform for advancing enzyme solutions across bakery, dairy, beverages, and processed foods

Japan Food Enzymes Market Report Scope

The Japan Food Enzymes Market is segmented by typeand by application. Based on type the market is segmented into carbohydrase, protease, lipase and others. Based on application the market is segmented into bakery, dairy & frozen products, beverages, meat poultry & sea food products, confectionery and others.

By Type

| Carbohydrase | Amylases |

| Pectinases | |

| Cellulases | |

| Other | |

| Protease | |

| Lipase | |

| Other Enzymes |

By Form

| Powder |

| Liquid |

By Source

| Plant |

| Microbial |

| Animal |

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Oil and Fats |

| Other Applications |

| By Type | Carbohydrase | Amylases |

| Pectinases | ||

| Cellulases | ||

| Other | ||

| Protease | ||

| Lipase | ||

| Other Enzymes | ||

| By Form | Powder | |

| Liquid | ||

| By Source | Plant | |

| Microbial | ||

| Animal | ||

| By Application | Bakery and Confectionery | |

| Dairy and Desserts | ||

| Beverages | ||

| Meat and Meat Products | ||

| Oil and Fats | ||

| Other Applications |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Japan food enzymes market in 2025?

It is valued at USD 145.28 million and is set to reach USD 207.02 million by 2030.

Which enzyme type leads revenue?

Carbohydrases, holding 45.92% share in 2024 driven by starch processing needs.

Which application segment grows fastest?

Beverages, expanding at a 7.92% CAGR through 2030 due to cold-pressed juice demand.

Who are leading domestic suppliers?

Amano Enzyme and Nagase leverage local customization and rapid technical support to retain significant share.

Page last updated on: