Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.10 Billion |

| Market Size (2026) | USD 8.36 Billion |

| Market Size (2031) | USD 9.81 Billion |

| Growth Rate (2026 - 2031) | 3.25% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Food Sweetener Market Analysis by Mordor Intelligence

Japan food sweeteners market size in 2026 is estimated at USD 8.36 billion, growing from 2025 value of USD 8.10 billion with 2031 projections showing USD 9.81 billion, growing at 3.25% CAGR over 2026-2031. This growth reflects demographic aging, rising diabetes prevalence, and strong regulatory oversight that together reshape consumer and manufacturer behavior. Sucrose remains the largest product category, yet reformulation pressure is steering beverage, dairy, and dessert brands toward high-intensity and plant-based alternatives. Manufacturers rely on domestic research and development capabilities to improve extraction yields and flavor profiles, while strict additive approvals sustain entry barriers that favor incumbents. Export-oriented processors also adopt advanced enzymatic and fermentation technologies to meet foreign labeling norms, reinforcing Japan’s role as a premium ingredient innovator. The Japan food sweeteners market continues to balance cost competitiveness with health-driven differentiation, giving natural solutions a measurable edge.

Key Report Takeaways

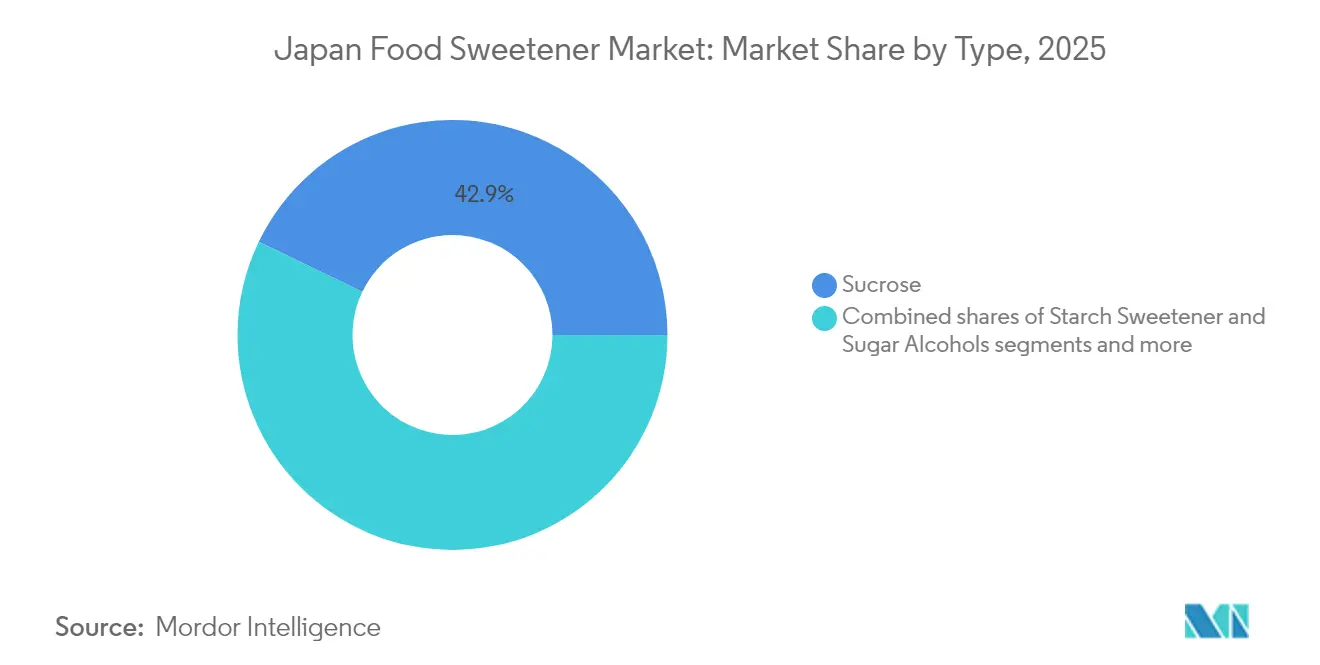

- By product type, sucrose led with 42.86% of the Japanese food sweeteners market share in 2025; high-intensity sweeteners are projected to post the fastest 5.22% CAGR through 2031.

- By source, artificial sweeteners accounted for a 42.31% share of the Japanese food sweeteners market size in 2025, while plant-based alternatives are set to expand at a 4.44% CAGR to 2031.

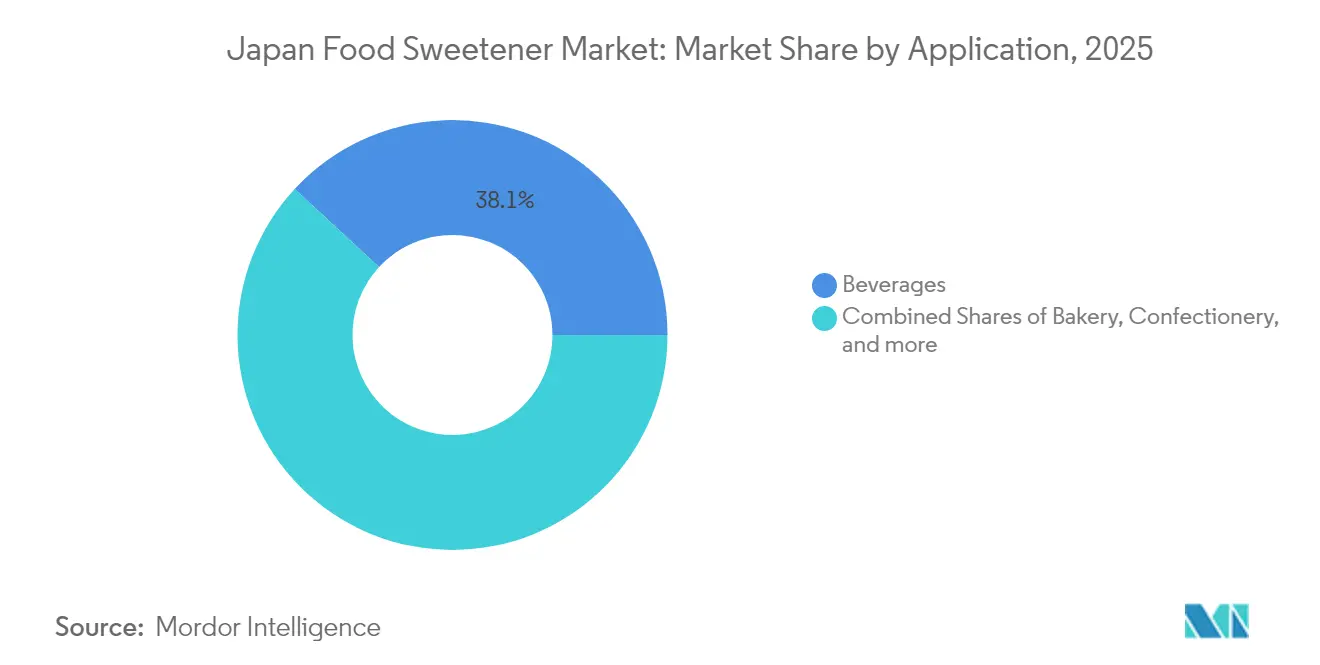

- By application, beverages held 38.12% of the Japanese food sweeteners market in 2025; dairy and desserts are advancing at a 4.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Food Sweetener Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Low-Calorie Sweeteners | +1.2% | National, concentrated in urban centers | Medium term (2-4 years) |

| Expansion of processed food and beverage manufacturing | +0.8% | National, with manufacturing hubs in Kanto and Kansai | Long term (≥ 4 years) |

| Rising Demand for Clean-Label Formulations | +0.7% | National, led by premium retail channels | Medium term (2-4 years) |

| Technological Advancements in Extraction and Processing | +0.5% | National, centered on research and development facilities | Long term (≥ 4 years) |

| Strong regulatory support for the use of Natural Sweeteners | +0.3% | National regulatory framework | Short term (≤ 2 years) |

| Market growth fueled by imports of specialty and fermentation-derived sweeteners. | +0.5% | National, with increasing global reach | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Low-Calorie Sweeteners

With Japan's aging population and growing health awareness, the demand for low-calorie sweeteners is rapidly increasing. The National Institute of Health and Nutrition's Health Japan 21 initiative seeks to reduce obesity rates among males aged 20-60 from 31.2% to 28% by 2025, driving the adoption of sugar alternatives[1]Source: National Institute of Health and Nutrition, “Health Japan 21 Analysis and Assessment Project,” nibn.go.jp. Consumer surveys indicate that 73% of Japanese adults now prefer zero-sugar or low-sugar products. This preference extends beyond beverages to confectionery, where major retailers have reported a remarkable 209% growth in zero-sugar products, while traditional sugary options have declined by 9%. Japan's Gen Z demographic is particularly embracing this trend, with SHIBUYA109 lab surveys showing a strong preference for "no-guilt" desserts made with natural sweeteners. Additionally, regulatory support from the Foods for Specified Health Use (FOSHU) system validates the use of low-calorie sweeteners in functional food categories.

Expansion of Processed Food and Beverage Manufacturing

Japan's processed food market is experiencing significant growth, driving increased demand for a wide range of sweetening solutions as manufacturers adapt their products to align with shifting consumer preferences. The ready-to-drink (RTD) tea segment serves as a prominent example of this trend, with the emphasis on convenience encouraging the incorporation of sweeteners into new product categories. According to Cross Marketing's 2024 consumer survey, polyethylene terephthalate (PET) bottle formats are the most preferred packaging option due to their "easy to drink" features and resealability, which favor pre-sweetened formulations over consumer-added sugar. Substantial investments by major food processors, such as Nisshin OilliO's "Value UpX" business plan, which extends through the fiscal year 2028 (FY2028), underscore ongoing capacity expansion efforts. This growth particularly benefits high-intensity sweeteners, which deliver cost efficiencies in large-scale production while maintaining flavor consistency across a variety of applications. Additionally, Japan's strategic role as a regional export hub for processed foods further strengthens this trend, as manufacturers seek sweetening solutions that meet both domestic consumer preferences and international regulatory standards.

Rising Demand for Clean-Label Formulations

In Japan, the growing preference for clean-label products is transforming the sweetener market, fueled by increasing skepticism toward artificial additives. To address this shift, Japan's Consumer Affairs Agency has banned the use of the terms "artificial" and "synthetic" on food labels. This regulatory change significantly benefits plant-based sweeteners, with stevia and monk fruit gaining popularity in premium product segments. The clean-label movement extends beyond individual preferences, influencing institutional procurement as well. The Health Japan 21 initiative aims to increase the number of registered corporations providing low-salt and low-fat products from 14 in 2012 to 100 by 2025, according to the National Institute of Health and Nutrition. Manufacturers are adopting precision fermentation technologies to scale the production of "natural" sweeteners. For example, Tate & Lyle has partnered with Manus Bio to produce stevia Reb M through bioconversion, ensuring compliance with clean-label standards. This trend is particularly evident in the confectionery sector, where health-conscious consumers are driving the reformulation of traditional sugar-heavy products to balance indulgence with healthier choices.

Strong Regulatory Support for the Use of Natural Sweeteners

Japan is enhancing its regulatory framework to promote the adoption of natural sweeteners. The Ministry of Health, Labour and Welfare (MHLW) has implemented a positive list system for food additives, streamlining the approval process for natural sweeteners while maintaining stringent safety standards. This system pre-approves specific additives, thereby reducing the time and complexity required for approval, which is particularly beneficial for manufacturers aiming to introduce innovative products to the market. Furthermore, the Foods with Function Claims (FFC) system, which is designed to facilitate the commercialization of functional food products, supports this initiative by enabling eligible natural sweeteners to complete the notification process within a timeframe of 5.5 to 9.5 months. This represents a significant improvement compared to the traditional approval timeline for food additives. The FFC system provides a structured and transparent approach for manufacturers to scientifically validate and communicate the functional benefits of their products, thereby fostering innovation and encouraging competition in the natural sweeteners market. Japan's efforts to align its regulatory framework with international standards are evident through its active participation in global standards development initiatives. This commitment was highlighted at the International Food Ingredients and Additives/Health Food Exposition and Conference Japan (IFIA/HFE JAPAN) 2024 exhibition, which placed a strong emphasis on the Foods with Function Claims guidelines [2]Source: ifia/HFE JAPAN, “ifia/HFE JAPAN 2024 Show Report,” ifiajapan.com. The regulatory environment in Japan is particularly advantageous for stevia-based products, with the Japan Stevia Association playing a pivotal role in developing industry standards and offering clear guidance to manufacturers. In contrast, synthetic alternatives face more complex and time-consuming approval processes, posing significant challenges for synthetic suppliers and further strengthening the competitive position of natural sweetener providers in Japan's increasingly health-conscious market.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent additive approval and labeling rules | -0.9% | National regulatory framework | Long term (≥ 4 years) |

| Consumer skepticism on artificial sweetener safety | -0.6% | National, amplified through social media | Medium term (2-4 years) |

| Growing preference on calorie reduction | -0.4% | National, concentrated in health-conscious segments | Short term (≤ 2 years) |

| Rising type 2 diabetes linked to high sugar consumption | -0.3% | National, with regional variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Additive Approval & Labeling Rules

Japan's rigorous food additive regulations create substantial challenges for sweetener manufacturers, prolonging product development timelines and complicating market entry. The Ministry of Health, Labour and Welfare enforces a positive list system that requires extensive safety documentation, often resulting in multi-year approval processes for novel sweeteners, particularly synthetic alternatives. Recent regulatory issues underscore the cautious approach of Japanese authorities. For example, in February 2025, the Consumer Affairs Agency addressed concerns about the Red No. 3 dye, stating "no data" on health risks despite warnings from the FDA. The Food Safety Commission requires comprehensive toxicology studies for risk assessments, a process that can take 3-5 years and cost millions of dollars. These regulatory barriers are especially challenging for international sweetener suppliers aiming to enter Japan's market. They must navigate complex documentation requirements while competing with established domestic players who already have regulatory approval. Additionally, these strict regulations can delay product reformulations. Manufacturers must secure regulatory clearance for new sweetener combinations, limiting their ability to quickly adapt to changing consumer trends.

Consumer Skepticism on Artificial Sweetener Safety

Consumer wariness toward artificial sweeteners is growing, driven by safety concerns amplified through social media and advocacy groups, which is limiting market growth. A February 2025 petition to ban aspartame in Europe, citing IARC's classification of it as "possibly carcinogenic," highlights how global safety debates influence Japanese consumer perceptions, even when domestic regulators approve the product. Activism by organizations such as the Consumers Union of Japan, which opposes genome-edited foods and artificial additives, further intensifies skepticism toward synthetic sweeteners. Incidents like the July 2024 safety concerns over erythritol in weight-loss drinks have further undermined consumer trust in artificial sweeteners. This skepticism is particularly evident in the high-intensity sweetener segment, where products like aspartame and sucralose face increasing resistance despite their advantages in food processing. Consequently, manufacturers are heavily investing in consumer education and transparent labeling while redirecting product development efforts toward natural alternatives. These natural options, while commanding premium prices, offer limited scalability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sucrose Dominance Faces High-Intensity Challenge

In 2025, traditional sucrose holds a significant 42.86% share of the market, highlighting Japan's strong confectionery traditions and the indispensable role of sugar's functional properties. At the same time, high-intensity sweeteners are experiencing rapid growth, with a projected CAGR of 5.22% through 2031, driven by beverage reformulations and regulatory support for low-calorie alternatives. Starch sweeteners and sugar alcohols maintain a balanced position. Sorbitol, in particular, is gaining prominence in Japan's food-grade market, currently valued at USD 0.22 billion and expected to reach USD 0.29 billion by 2031, reflecting a 4.71% CAGR. Beyond its traditional food uses, sorbitol is establishing itself in pharmaceutical and cosmetic applications. This evolving market underscores Japan's dual structure: traditional applications continue to drive sucrose demand, while health-conscious consumers are fueling the rise of high-intensity sweeteners.

Within the high-intensity sweetener segment, stevia leads as the preferred natural option, while sucralose dominates among synthetic alternatives. JK Sucralose Inc. stands out with its compliance with Japanese standards and a strong global presence. Neotame and Ace-K cater to specialized markets, where their intense sweetness justifies premium pricing, particularly in pharmaceutical formulations designed to mask bitterness. The Food Safety Commission of Japan significantly influences product development, prioritizing natural high-intensity sweeteners with faster approval processes over synthetic options. This regulatory environment provides a competitive advantage to stevia and monk fruit suppliers, positioning them ahead of traditional artificial alternatives.

By Application: Beverages Lead While Dairy Accelerates

In 2025, beverages hold a leading 38.12% share of the market, highlighting Japan's thriving ready-to-drink sector, where convenience and consistent taste significantly influence sweetener choices. Dairy and desserts are experiencing notable growth, with a 4.41% CAGR projected through 2031, driven by health-conscious trends as consumers seek indulgent yet guilt-free options. A 2024 survey by Cross Marketing indicates a strong preference for PET bottle formats, valued for their resealability and portability. This preference supports pre-sweetened formulations, which are favored over consumer-added alternatives. Japan's application landscape reflects a unique combination of on-the-go convenience and high-quality expectations, driving demand for premium sweeteners.

Despite the rise of health trends, confectionery products continue to see stable demand. This stability is attributed to Japan's traditional sweets culture, which still relies on sucrose, even as modern confections increasingly adopt alternative sweeteners. The bakery sector faces reformulation challenges as initiatives like Health Japan 21 promote reduced sugar consumption. However, this shift creates opportunities for sugar alcohols, which help maintain the texture and browning properties essential for baked goods. Additionally, sauces, dressings, and spreads are emerging as key applications. In these categories, sweeteners serve dual purposes, enhancing taste while also contributing to preservation and texture modification. Advances in enzymatic processing technology are enabling the development of customized sweetness profiles tailored to specific culinary applications.

Geography Analysis

Japan's food sweeteners market navigates a complex landscape, balancing domestic production with import dependencies. Major cities like Tokyo, Osaka, and Nagoya serve as the epicenters of sweetener consumption, housing both food processing facilities and a discerning consumer base. While urban centers swiftly embrace alternative sweeteners, rural areas maintain a stronger affinity for traditional sugar. This geographic distribution mirrors Japan's industrial landscape, with leading food manufacturers strategically positioned near port cities for easy access to imported raw materials and proximity to consumers. The use of sweeteners is increasing in various applications such as bakery, beverages, and others due to their popularity. According to the Ministry of Internal Affairs and Communications (Japan) data from 2023, the per capita consumption volume of carbonated drinks was 30.4 liters.

Key players, including Ajinomoto Co., Inc., headquartered in Tokyo, and Matsutani Chemical Industry Co., Ltd., based in Hyogo Prefecture, leverage Japan's advanced biotechnology infrastructure to develop proprietary sweetener technologies that cater to evolving market requirements. Despite the implementation of protective trade policies designed to support domestic industries, Japan faces significant agricultural limitations, including restricted arable land and climatic challenges, which necessitate a heavy reliance on imported raw materials such as raw sugar and corn-based sweeteners. A comprehensive analysis by the United States Department of Agriculture (USDA) underscores Japan's complex tariff structures, which are strategically crafted to encourage domestic production while controlling the flow and pricing of imports. Additionally, the Agriculture and Livestock Industries Corporation (ALIC) enforces a surcharge system that imposes price premiums on imports, thereby providing a competitive edge to domestically produced alternatives, as highlighted by the USDA Economic Research Service.

In a strategic move, Mitsui DM Sugar partnered with Toray Industries in Thailand for cellulosic sugar production, underscoring the trend of Japanese firms broadening their horizons to tap into diverse feedstock sources. This evolving strategy leans more towards technological innovation than mere cost competition, with Japanese entities capitalizing on local R&D to craft premium sweeteners, reaping higher margins both at home and abroad.

Regulatory Landscape

Japan regulates food sweeteners primarily under the Food Sanitation Act through a positive list system, so only additives designated by the competent authority can be sold or used in foods. In practice, designation and updates to use standards are handled through submissions to the government, with risk assessment by the Food Safety Commission of Japan (FSCJ) and specifications and use standards maintained in the Specifications and Standards for Foods, Food Additives, etc. (commonly referenced through the 9th Edition and subsequent amendments). These documents define use standards for sweeteners including aspartame, saccharin, sucralose, and xylitol.

Recent compliance-related updates have tightened the quality of submissions and assessment requirements rather than easing them. FSCJ revised its food additive risk assessment guidelines in 2024, and the Food Additives Designation Consultation Center (FADCC, NIHS) updated in 2025 its guidance for preparing application documents for designation and revisions of use standards, including category-specific instructions. Together, these changes reinforce science-based documentation expectations for both domestic and imported products, supporting entry barriers for novel sweeteners and for reformulations that require changes in permitted uses or specifications.

Value Chain Analysis

The Japan food sweetener value chain begins with agricultural and industrial feedstocks, including imported raw sugar for refining, domestic sugarcane and sugar beet in limited regions, and starch-based inputs for syrup and polyol pathways. It then moves through refining and processing into ingredient formulation, testing and compliance activities, and downstream food manufacturing.

Imports are central to the standard sugar supply, with logistics concentrated around major port and industrial areas that support bulk handling and onward distribution to food and beverage manufacturers. Specialty sweeteners and functional ingredients, by contrast, follow more technical supply chains tied to dedicated processing capabilities. Midstream, processors and ingredient suppliers operate within a tightly regulated additive system and rely on technical standards and industry infrastructure such as the Japan Food Chemical Research Foundation (JFCRF) compilation of additives and related standards used by manufacturers for compliance. Downstream, large beverage, dairy and dessert, confectionery, and processed-food manufacturers convert sweeteners into finished products, with packaging and retail channels amplifying demand for pre-formulated sweetness profiles. Regulatory administration changes also feed into the chain, including the April 1, 2024 transfer of food additive regulatory jurisdiction from the Ministry of Health, Labour and Welfare (MHLW) to the Consumer Affairs Agency (CAA), which shapes how companies manage labeling, evaluation, and ongoing compliance workflows.

Competitive Landscape

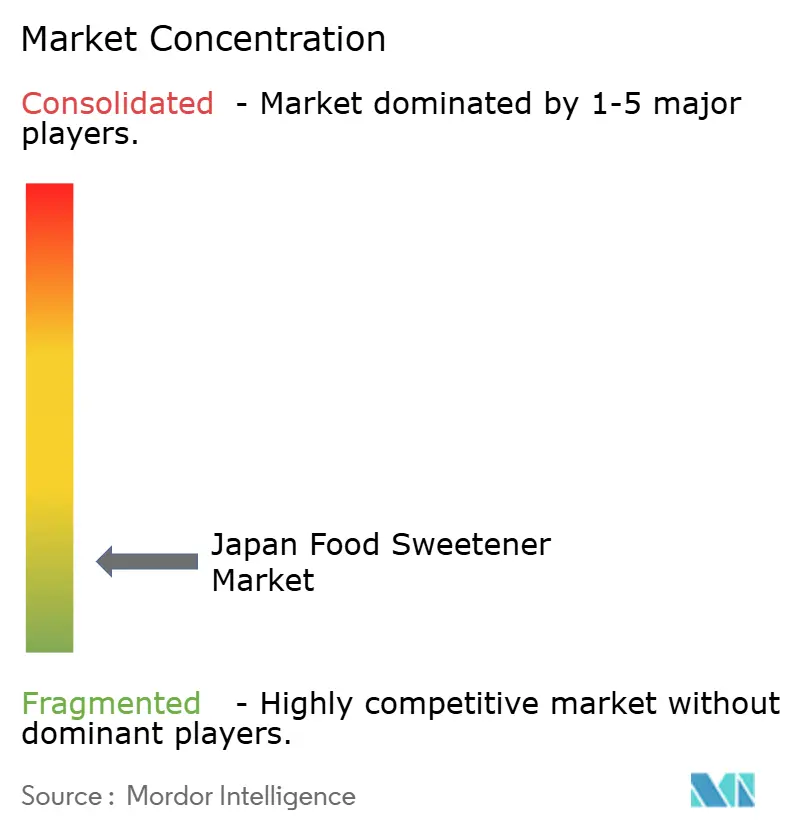

Japan's sweeteners market showcases significant fragmentation. This not only highlights the diverse technological and regulatory expertise needed for success but also opens doors for potential consolidation. While the market's fragmented nature is evident, competition remains at a moderate intensity. Established players, armed with regulatory know-how and robust customer ties, effectively fend off challenges from newcomers. Companies are increasingly prioritizing technological innovation over mere price competition. For instance, Matsutani Chemical's proprietary enzymatic processes for allulose production underscore a move towards sustainable competitive edges.

Furthermore, there's a notable gap in precision fermentation technologies and rare sugar production. Here, Japanese firms, tapping into local biotech strengths, have the chance to seize emerging market segments ahead of global rivals. Biotechnology firms are emerging as key disruptors, harnessing precision fermentation for sweetener production. A testament to this trend is the collaboration between Tate & Lyle and Manus Bio, focusing on stevia Reb M. The industry's technological focus leans heavily on enzymatic processing and fermentation, pivotal for scaling natural sweetener production.

Patent filings further underscore the industry's commitment, pointing to significant R&D investments in bioconversion technologies. Japan's regulatory landscape plays a crucial role, favoring natural sweeteners and erecting hurdles for synthetic counterparts. This not only bolsters domestic firms' clean-label appeal but also underscores the importance of regulatory compliance and customer rapport. Given the intricate approval processes for new sweeteners, these relationships and compliance capabilities translate into substantial switching costs, safeguarding established players from price-driven competition.

Japan Food Sweetener Industry Leaders

Cargill, Incorporated

Mitsubishi Corporation

Mitsui DM Sugar Holdings Co., Ltd

Nagase & Co. Ltd

Tate and Lyle Plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product reformulation and portfolio premiumization create room for high-intensity sweeteners, plant-based alternatives, and functional sugar-derived ingredients that help manufacturers pursue calorie-reduction and clean-label objectives while maintaining taste and texture. A near-term signal is ongoing investment in functional materials and sugar-derived technologies. In April 2026, Wellneo Sugar transferred production of cyclodextrin (CI) from its Okinawa lab to the Mihama Bioplant, expanding capacity by roughly tenfold, which points to scaled output for higher-value, sugar-derived functional ingredients that can be used across food and beverage applications.

Operational restructuring among established sugar and sweetener players is also opening space for new ingredient formats and more targeted go-to-market models in Japan. In June 2026, Wellneo Sugar outlined nationwide factory consolidation and logistics optimization, and it disclosed an October 2026 merger with subsidiary Toyo Seito alongside the creation of a Functional Materials Headquarters. This supports a shift away from commodity sugar toward functional ingredients and sugar-transfer technologies, which is aligned with Japan's additive regime and helps brand owners tailor flavor masking and sugar-like profiles using established standards and government frameworks.

Recent Industry Developments

- May 2026: Mitsui DM Sugar announced a business transfer agreement to move sales of functional ingredients, including Palatinose, Palatinit, and bamboo fiber, to its wholly owned subsidiary Taisho Technos, effective October 1, 2026. The agreement supports a more specialized sales platform focused on value-added sweetener-adjacent ingredients and improves channel focus versus commodity sugar routes. It also strengthens channel traceability and regulatory alignment across domestic and export markets.

- April 2025: Mitsui DM Sugar completed an internal reorganization by merging Mitsui DM Sugar Co., Ltd. (subsidiary) into the parent and changing the name from Mitsui DM Sugar Holdings Co., Ltd. to Mitsui DM Sugar Co., Ltd. The simplification is intended to support faster decision-making across sweetener and functional ingredient activities in a market shaped by strict additive rules and rapid reformulation cycles. The change positions the group to respond quickly to regulatory updates and supply-chain dynamics affecting labeling and designation processes.

- June 2024: Saraya Japanese Middle East for Industrial Investment inaugurated a USD 12 million factory complex in the Sokhna Integrated Zone within the Suez Canal Economic Zone (SCZone), including lines for packaging the sugar-free sweetener Lakanto for export to Europe and Asia. The added overseas packaging and production footprint supports supply continuity and scale for monk fruit-based sweetener formats used by Japanese-linked brands and distributors. The facility strengthens regional logistics and expands sourcing options for Japanese brands serving Europe and Asia.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Japan food sweetener market covers the value of food grade sweeteners sold for use in packaged foods and beverages within Japan, including caloric and non-caloric options used for sweetness, taste balance, and reformulation needs.

Scope exclusions: It does not count tabletop sweeteners sold mainly as retail consumer packs, or non-food uses where the ingredient is primarily used for pharma or industrial purposes.

Segmentation Overview

- Product Type

- Sucrose

- Starch Sweeteners & Sugar Alcohols

- Dextrose

- High-Fructose Corn Syrup (HFCS)

- Maltodextrin

- Sorbitol

- Xylitol

- Other Starch Sweeteners & Sugar Alcohols

- High-Intensity Sweeteners (HIS)

- Sucralose

- Aspartame

- Saccharin

- Cyclamate

- Ace-K

- Neotame

- Stevia

- Other High-Intensity Sweeteners

- Application

- Bakery Products

- Confectionery Products

- Dairy and Desserts

- Sauces Dressings and Spreads

- Beverages

- Other Applications

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand context and the operating boundaries of the market before any modeling assumptions were locked. We leaned on public sources such as Japan Ministry of Agriculture, Forestry and Fisheries publications, Japan Customs trade statistics, the Statistics Bureau of Japan, and relevant food labeling or standards guidance from Japanese authorities. Together, these helped us frame category activity, volume direction, and import dependence where applicable.

To avoid building the model on one single data stream, we also reviewed company filings and investor decks for ingredient and food manufacturers, association websites related to sugar, starch, and food ingredients, and reputed press coverage on reformulation and sugar reduction. For cross-checking company presence and product footprint, we used a paid subscription focused on company financials and intelligence, along with a separate subscription for patents to see how innovation activity was shifting across sweetener types. These are illustrative sources only, and other references were used throughout data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on validating what actually drives sweetener purchases in Japan, especially how food and beverage formulators balance cost, taste profile, labeling claims, and regulatory compliance. We spoke with a mix of ingredient suppliers, distributors, and end users across key application areas like beverages, bakery, dairy, and confectionery. Respondent input was used to confirm usage intensity, substitution trends, and typical pricing mechanics, including contract timing versus spot buying.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | |

| Mid tier: 41% | Functional/Unit leaders: 37% | |

| Smaller Players: 22% | Managers: 48% |

Market-Sizing & Forecasting

Sizing used a top-down and bottom-up approach, where the main build starts from Japan food and beverage production and ingredient usage patterns, then is reconstructed into sweetener demand pools by application. Once those demand pools were formed, we applied penetration and inclusion rules for each sweetener family, followed by price logic that reflects how sweeteners are bought and specified in Japan.

A few key inputs shaped the model, including the mix shift between sucrose and high-intensity sweeteners in reformulated recipes, the pace of sugar-reduction activity in beverages and bakery, import and domestic supply signals for sugar and starch-derived ingredients, typical dosage intensity by application, and average selling price movement by sweetener group. The price movement reflects input costs and contract renewal cycles. After the top-down totals were obtained, we added selective bottom-up checks using supplier and channel checks, plus sampled price points multiplied by plausible volume bands. This helped correct gaps when some categories had limited public disclosure.

For forecasting, scenario analysis was used around reformulation speed and pricing pass-through. We also applied trend smoothing on historical series to prevent short-term swings from overstating the outlook. Assumptions were re-tested with experts when discontinuities appeared, such as sudden cost shifts or accelerated labeling-driven reformulation.

Data Validation & Update Cycle

Validation was done through multiple checks, starting with internal consistency tests across application demand, implied sweetener intensity, and price ranges that practitioners consider normal. We also compared outputs with independent signals such as import patterns, category growth in packaged foods and beverages, and observed reformulation activity. Outliers were investigated before sign-off.

A second analyst review was run to challenge core assumptions, and we re-contacted selected respondents when pricing, mix, or inclusion rules moved materially. Reports are refreshed annually, with interim updates when major events affect input costs, regulation, or demand. A final pre-delivery review is completed so clients receive the latest updated view.

Mordor Intelligence's Japan Food Sweetener Market Market Size Versus Other Published Estimates

Published market sizes for Japan food sweeteners often differ because the scope boundary is not consistent, and because pricing is handled in different ways across time. Some sources blend retail sugar and tabletop products into the same pool, while others focus only on food manufacturing demand, which changes the denominator before any forecasting even begins.

A second gap driver is how prices are converted and refreshed, since yen movements and contract renewal timing can shift a USD value even when volumes are steady. When ASP logic is updated using the latest contract-driven price resets and cross-checked against trade and production signals, the resulting 2025 value stays anchored to what formulators are buying, which is a refresh-led difference applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.10 B (2025) | |

| Industry Publisher A | USD 4.30 B (2025) | Uses a narrower value pool that appears closer to select sweetener categories and applications, and it likely applies a different USD conversion timing, which can understate a Japan total when yen rates shift. |

| Industry Portal B | USD 1.96 B (2025) | Looks aligned to a sugar-substitutes style scope (natural, artificial, sugar alcohols) and may exclude mainstream sucrose and some starch-based sweeteners, which pulls down the counted demand base before pricing is applied. |

The spread in the table is mainly explained by what is counted as a food sweetener in Japan, and when prices and currency are normalized to a single year. By keeping the inclusion rules explicit and by rechecking ASP and demand signals during updates, the estimate stays traceable to repeatable steps instead of being driven by one assumption.

Key Questions Answered in the Report

What is the projected value of the Japan food sweeteners market in 2031?

The market is forecast to reach USD 9.81 billion by 2031.

Which product category is expanding the fastest?

High-intensity sweeteners are projected to grow at a 5.22% CAGR through 2031.

How large is the beverage segment within the market?

Beverages accounted for 38.12% of total market value in 2025, the largest among all applications.

Why are plant-based sweeteners gaining traction?

Regulatory support and consumer demand for clean-label products propel plant-based options, which are growing at a 4.44% CAGR.

Page last updated on: