Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 313.11 Billion |

| Market Size (2026) | USD 325.33 Billion |

| Market Size (2031) | USD 391.45 Billion |

| Growth Rate (2026 - 2031) | 3.77% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Construction Market Analysis by Mordor Intelligence

The UK construction market size is USD 325.33 billion in 2026 and is forecast to reach USD 391.45 billion by 2031 at a 3.77% CAGR. Contractors shift resources to civil engineering packages associated with rail nodes, strategic roads, and regulated utility upgrades, while private developers concentrate on rental housing, logistics corridors, and data-led commercial assets. Adoption of digital twins and consistent ISO 19650 information management raises data quality at handover and supports lifecycle performance, which aligns with government client priorities on risk reduction and value. Off-site manufacturing grows where building safety, speed, and repeatability improve program certainty. The delivery model increasingly blends traditional and off-site approaches with standardized design kits, which support capacity and governance across complex projects.[1]https://www.ukbimframework.org/standards/

Key Report Takeaways

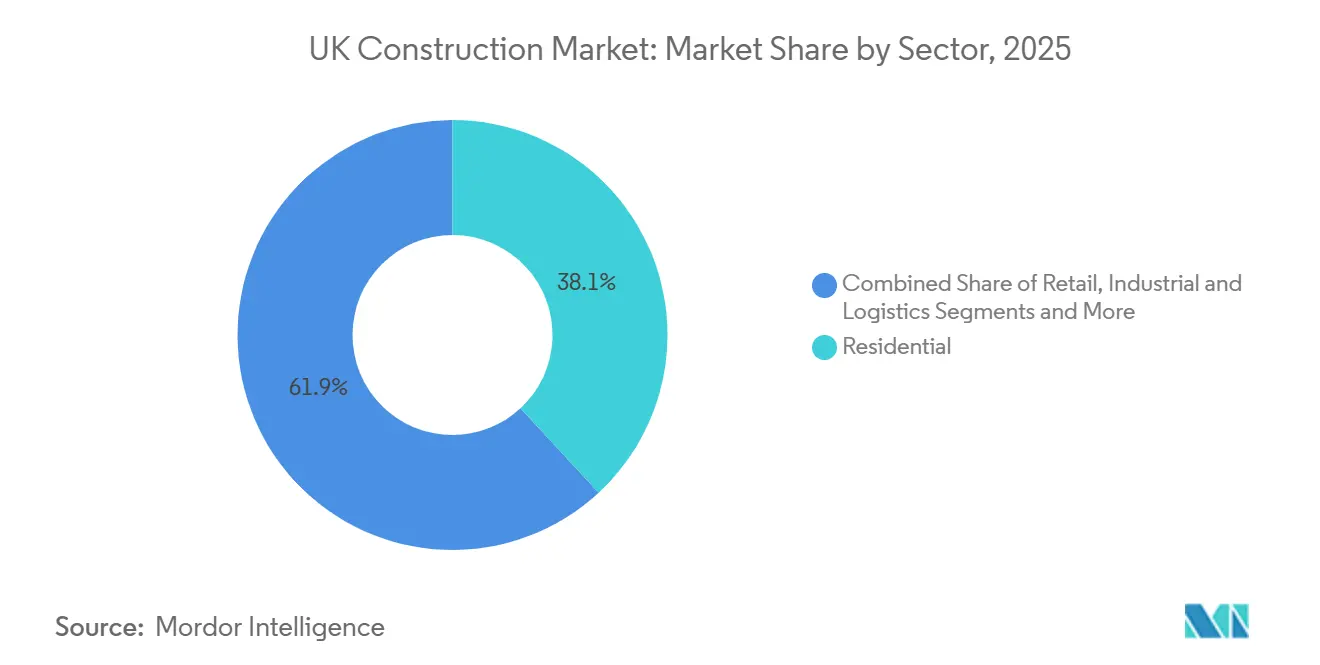

- By sector, residential led with 38.10% revenue share in 2025, while infrastructure is forecast to expand at a 7.90% CAGR to 2031.

- By construction type, new construction held 55.10% of the UK construction market share in 2025, while renovation recorded the highest projected CAGR at 7.20% through 2031.

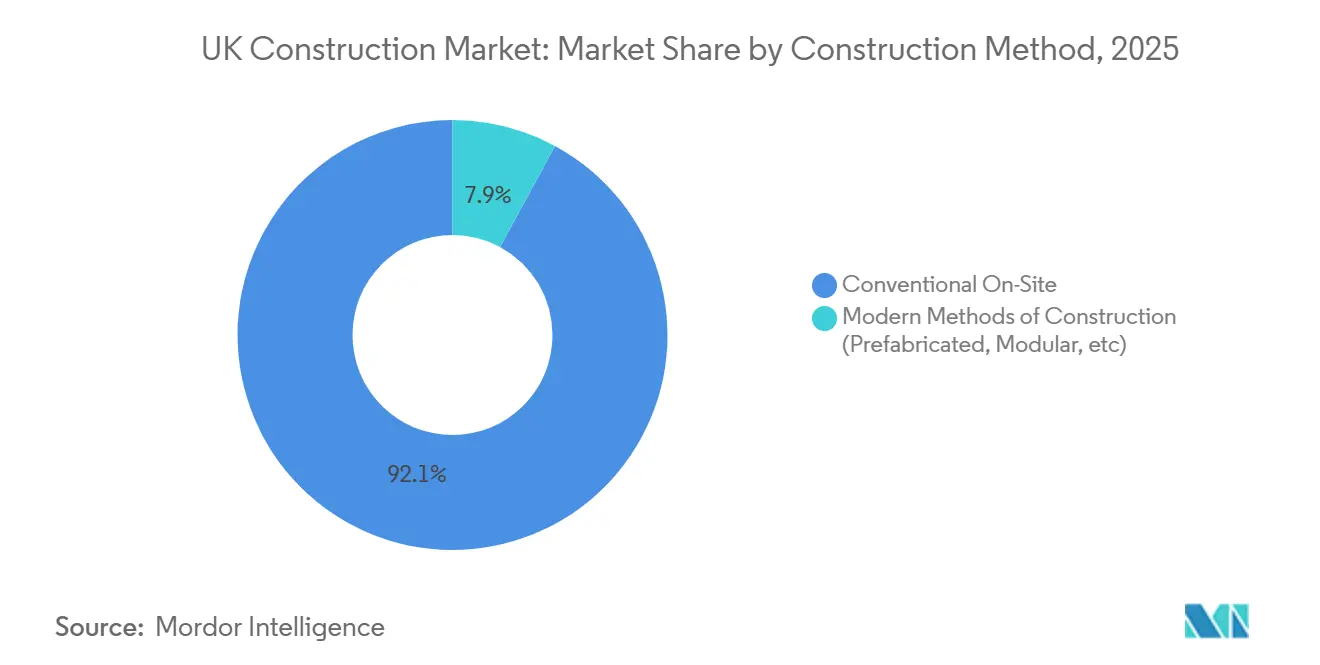

- By construction method, conventional on-site accounted for 92.10% share of the UK construction market size in 2025, while modern methods of construction are projected to grow at a 10.40% CAGR to 2031.

- By investment source, private investment accounted for a 75.10% share in 2025, while public spending is projected to grow at an 8.20% CAGR to 2031.

- By country, England held 79.55% of the UK construction market share in 2025, while Northern Ireland recorded the highest projected CAGR at 6.10% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UK Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic housing shortfall pushing residential starts | +1.1% | UK-wide, higher pressure in England’s growth centres | Medium term (2-4 years) |

| Government mega-projects boosting civil-engineering backlog | +1.0% | UK-wide, with a concentration in England’s strategic corridors | Long term (≥ 4 years) |

| Net-Zero 2050 targets stimulating green retrofit demand | +0.9% | UK-wide across the public estate and private housing | Long term (≥ 4 years) |

| Off-site and modular building uptake post-Building Safety Act | +0.5% | UK-wide, concentrated in public estate and education | Medium term (2-4 years) |

| Infrastructure secondary-market M&A by global PE and pension funds | +0.3% | UK-wide across regulated assets and PPP portfolios | Medium term (2-4 years) |

| Digital-twin adoption improving project delivery efficiency | +0.3% | UK-wide in major programs and asset-heavy clients | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Housing Shortfall Pushing Residential Starts

Housing demand remains elevated relative to supply capacity, with household formation and urban regeneration priorities putting attention on mixed-tenure delivery and brownfield land. Planning performance and infrastructure servicing shape the pace of starts, while fire safety remediation and quality standards influence design choices and project sequencing. Homes England programs and local authority partnerships provide routes for enabling works, site assembly, and affordable tenures, which support throughput where consents are granted. Build-to-rent and later living continue to draw institutional capital that values stable yields and operational platforms. The pressure on supply continues to direct the UK construction market toward scalable solutions and platform-based delivery for repeatable housing types.[2]https://www.hs2.org.uk/building-hs2/

Government Mega-Projects (HS2, RIS2) Boosting Civil-Engineering Backlog

Large transport and enabling works continue to anchor civil engineering workloads in 2026, with HS2 works in the south, strategic road upgrades, and associated station and regeneration sites shaping contractor backlogs. Program governance and information requirements promote higher digital maturity and emphasize safety, tracing, and material provenance. Government clients maintain standardized procurement and delivery protocols that favor teams with integrated design, construction, and manufacturing capability. The resulting pipeline supports multi-year resourcing, fleet investment, and supplier development to meet repeatable work packages. This driver reinforces the UK construction market's focus on predictable throughput and outcome-based performance.

Net-Zero 2050 Targets Stimulating Green Retrofit Demand

The legally binding 2050 target sustains demand for energy upgrades, heat decarbonization, and building fabric improvements across public and private estates. Government guidance and standards push consistent information capture and asset performance reporting, which aligns retrofit outcomes to carbon and energy metrics. Public sector frameworks continue to scale building retrofit, schools decarbonization, and hospital energy improvements, with delivery structured around long-term performance. On the private side, owners and operators advance net-zero pathways for offices, logistics, and energy-intensive assets, prioritizing reduced operational costs and compliance. The UK construction market aligns supply chains to heat pumps, fabric-first interventions, and smart controls that underpin low-carbon upgrades.[3]https://www.hse.gov.uk/building-safety/index.htm

Off-Site and Modular Building Uptake Post-Building Safety Act

Building safety reforms change how design, manufacturing, and assembly information is planned and verified, which supports higher adoption of off-site and modular solutions in suitable asset classes. Platform kits of parts and standardized assemblies improve predictability and compliance while allowing traceable quality controls. Public estate programs in education, healthcare, and justice continue to specify modern methods where they enhance safety and speed. Contractors invest in factory-enabled workflows that combine digital design with assured manufacturing processes and quality data at handover. This shift supports the UK construction market in delivering safer, more consistent outcomes on repeatable building types.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour shortage and aging workforce | -1.2% | UK-wide across all trades and professions | Long term (≥ 4 years) |

| Lengthy planning and permitting timelines | -0.9% | UK-wide, concentrated in high-demand areas | Long term (≥ 4 years) |

| Material-price volatility and supply-chain disruption | -0.7% | UK-wide with exposure to imported inputs | Medium term (2-4 years) |

| Cybersecurity risks in BIM-centric projects | -0.2% | UK-wide across project supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labour Shortage and Aging Workforce

Persistent skills gaps restrict delivery capacity, especially in qualified trades, site supervision, digital engineering, and building control. Training programs expand, yet experience profiles take time to rebalance, and competition for specialist roles raises cost and delivery risk. Productivity tools and standardized design reduce pressure, but certain projects still require rare skills and accreditation, which are difficult to scale quickly. Public bodies and industry groups call for apprenticeships and mid-career transition pathways, with a focus on modern methods and digital competencies. The constraint continues to shape tendering strategies and workforce planning across the UK construction market.

Lengthy Planning and Permitting Timelines

Planning delays increase holding costs and push out starts on site, especially for complex urban mixed-use, logistics schemes near strategic corridors, and major infrastructure requiring development consent orders. Local authority resourcing and statutory consultee workflows create variability in approval durations and conditions. Government reform efforts aim to streamline processes and digitize planning, although capabilities and data standards are still in transition. Developers respond with phased applications and early enabling works to de-risk long lead items where possible. These timing issues affect pipeline visibility and sequencing across the UK construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Residential Is the Largest Share, Infrastructure Is the Fastest Growing

Residential leads the sector composition with a 38.10% contribution in 2025, supported by demand for urban living, mixed-tenure delivery, and quality upgrades of the existing stock. Institutional capital continues to prioritize build-to-rent and later living formats with operational stability. Design and productization enable platform-build approaches that improve predictability, safety, and cost. Local authorities and Homes England programs enhance site assembly and affordable delivery pipelines, with a focus on quality and build safety. The UK construction market supports these requirements with standardized components, strong digital records, and assured building control compliance.

Infrastructure is the fastest-growing sector through 2031, reflecting strategic road renewals, station and urban realm upgrades, and enabling works for energy and utility networks. Contractors deploy integrated teams that combine civils, structures, and M&E to deliver complex staging around live operations. Information management and asset data handover are critical to lifecycle performance targets set by public clients. Skills and plant strategy align to tunneling, earthworks, and large structures where delivery risk is highest. The UK construction market, therefore, concentrates resources where civil engineering programs require proven multidisciplinary capabilities.

By Construction Type: New Build Leads, Renovation Expands with Energy Retrofits

New construction holds the largest share in 2025 at 55.10%, reflecting live residential schemes, commercial repurposing, and strategic infrastructure packages. New build supports modern specifications for energy performance, fire safety, and digital documentation across asset types. Platform kits and off-site systems are applied where they reduce rework and accelerate commissioning without compromising safety. Contractors mix traditional trades with factory-enabled solutions based on site conditions and client objectives. This balanced model sustains throughput across the UK construction market.

Renovation records the fastest projected growth to 2031 as owners and public bodies target decarbonization, remediation, and longevity of existing assets. Programs in schools, hospitals, and local authority estates scale energy upgrades and safety improvements. Digital surveys, point-cloud models, and asset information requirements guide interventions and reduce risk during work on occupied buildings. Contractors combine building fabric upgrades with services modernization, controls, and heat decarbonization options. This renovation wave extends the service life of assets and shifts resources within the UK construction market to retrofit capabilities.

By Construction Method: Conventional Dominates Today, Modern Methods Accelerate

Conventional on-site methods account for 92.10% share of the UK construction market size in 2025, reflecting the breadth of one-off and complex projects that still rely on site-based trades. Traditional delivery remains essential for constrained urban sites, heritage assets, and bespoke design outcomes. Contractors invest in digital field management and model-based coordination to raise productivity and safety under conventional routes. Qualified supervisory roles and certified trades remain central to quality and compliance. The UK construction market blends conventional trades with digital oversight to deliver assured outcomes.

Modern methods of construction are the fastest-growing approach, scaling in education, healthcare, logistics, and standardized housing applications. Platform kits enable consistent quality, faster assembly, and improved traceability that aligns with building safety information requirements. Manufacturers work with Tier 1 contractors to coordinate design for manufacture and assembly, integrate cyber-secure data flows, and standardize quality assurance. Resulting programs capture repeatable efficiencies while meeting safety and energy standards. This supports a wider shift in the UK construction market toward productized delivery where feasible.

By Investment Source: Private Capital Leads, Public Programs Drive Growth

Private sources hold a 75.10% share in 2025, anchored by rental housing, logistics, and mission-critical commercial assets. Investors prioritize deliverability, resilience, and carbon performance to protect long-term value. Planning certainty and grid connections steer site selection, while pre-let and forward-funding arrangements manage risk. Platform-based design and modular components enhance speed to revenue on repeatable assets. These priorities sustain the private share across the UK construction market.

Public spending delivers the fastest growth into 2031 through multi-year programs for transport resilience, hospital upgrades, and public estate decarbonization. Procurement reform strengthens transparency and assurance, while framework models encourage collaboration and early supplier engagement. Strong information requirements and safety oversight remain consistent features of public works. Delivery partners with mature digital and off-site capabilities gain competitive positioning in these programs. This trajectory supports continued depth in the UK construction market pipeline from public clients.

Geography Analysis

England accounts for the largest share at 79.55% in 2025, concentrated around major urban centers and strategic corridors under active programs. Policy-driven regeneration near stations, strategic road upgrades, and investments in utilities and social infrastructure increase the density of work in specific regions. Local planning and infrastructure capacity influence the sequencing of starts. Standardized procurement and information protocols support consistency across regional delivery. England’s allocation anchors the near-term pipeline for the UK construction market.

Scotland, Wales, and Northern Ireland present varied profiles shaped by devolved policy and program governance. Program delivery in transport, health, and education remains central, with net zero and safety demands reflected in specifications. Regional planning frameworks and consenting regimes drive differences in timelines and work types. Offshore wind, grid reinforcements, and local energy systems add layers of infrastructure delivery in select locations. These patterns keep regional suppliers active within a coordinated UK construction market.

Northern Ireland records the fastest projected growth into 2031, reflecting targeted programs and pipeline expansion from devolved authorities. Program governance emphasizes transparency and delivery assurance, which supports mobilization and resourcing. Planning certainty and investment in enabling works can further unlock capacity for starts. Regional contractors and supply chains coordinate to meet digital and safety requirements set by public clients. These improvements lift regional momentum and contribute to a balanced UK construction market outlook.

Competitive Landscape

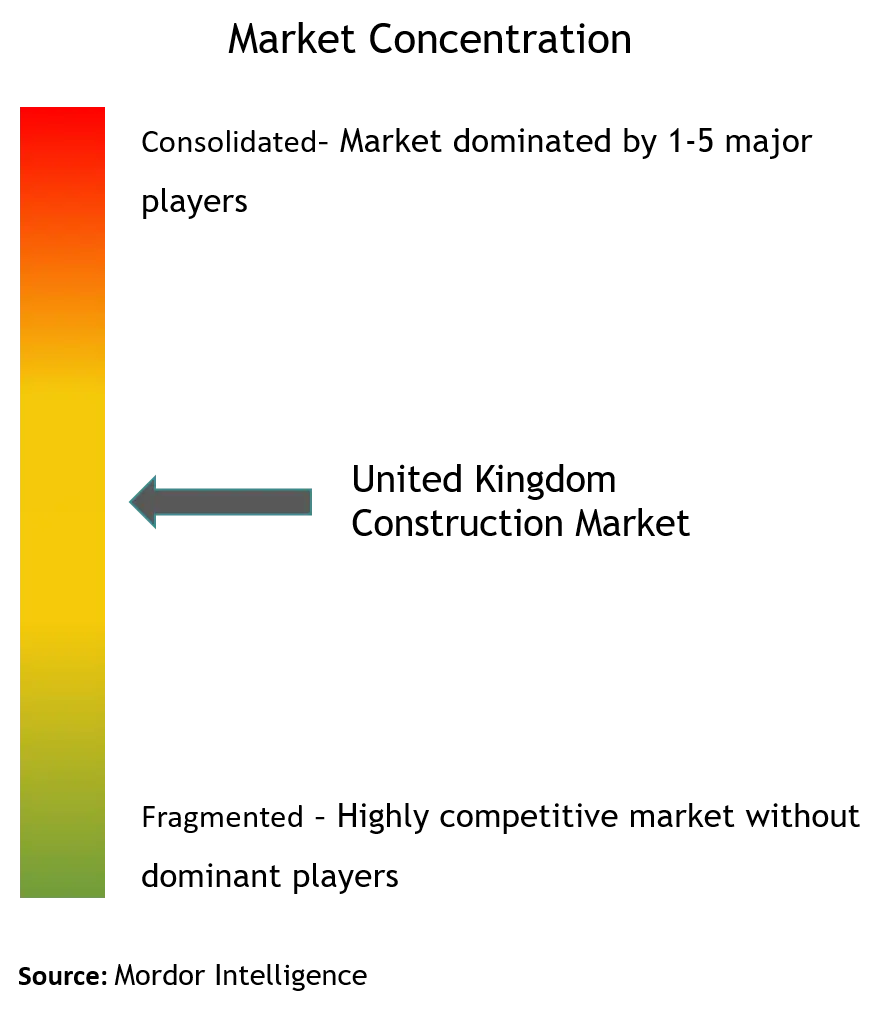

The United Kingdom construction market shows moderate fragmentation. Competition clusters around Tier 1 contractors, diversified construction groups, and leading housebuilders that meet safety, digital, and financial thresholds for large programs. Differentiation rests on proven delivery in civil engineering, strong building safety governance, and ISO 19650-aligned information management at scale. Contractors increase off-site capability through in-house manufacturing or long-term partnerships with platform component suppliers. Enterprise risk frameworks emphasize cybersecurity and data integrity, bridging project delivery with asset operations. These features drive selection decisions across high-stakes work in the UK construction market.

Strategic moves among market leaders show investment in digital and manufacturing capability. Balfour Beatty and partners deliver complex rail stations and civils packages under rigorous safety and information protocols on HS2. Kier and Morgan Sindall expand roles across education and defense estates using standardized components and collaborative frameworks. Laing O’Rourke and Skanska scale modern methods tied to factory processes for repeatable hospital and public estate assets. These examples reflect the UK construction market shift toward platform delivery, secure data flows, and consistent quality assurance.

Housebuilders coordinate land, planning, and productization to improve delivery and safety compliance. Large groups strengthen fire safety remediation and building control processes across their portfolios. Product platforms and supply chain partnerships improve build speed and consistency while supporting fabric standards. Engagement with planning and infrastructure providers remains vital to unlock serviced plots. These priorities keep housebuilders aligned with the evolving standards that define the UK construction market.

UK Construction Industry Leaders

Balfour Beatty PLC

Kier Group PLC

Morgan Sindall Group PLC

Laing O'Rourke PLC

ISG PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Anglian Water appointed AtkinsRéalis, Mace, and Turner & Townsend to deliver its USD 14.3 billion five-year capital program, forming one of the UK’s largest infrastructure alliances.

- February 2025: KKR tabled a USD 5.2 billion buyout proposal for Thames Water, aiming to stabilize operations amid a USD 20.8 billion debt load.

- January 2025: United Utilities chose the Strabag-Equitix venture for the Haweswater Aqueduct modernization, reinforcing Continental contractors’ profile in UK water projects.

- June 2024: Balfour Beatty secured a USD 249.6 million contract to construct three substations supporting Scottish renewable-energy integration.

UK Construction Market Report Scope

Construction is the installation, maintenance, and repair of buildings and other stationary structures, as well as the construction of roadways and service facilities that form fundamental components of structures and are required for their operation. Construction encompasses the processes involved in constructing buildings, infrastructure, industrial facilities, and related operations from start to finish. A complete background analysis of the UK construction market, including an assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and the COVID-19 pandemic’s impact, is covered in the report.

The UK construction market is segmented by sector (residential, commercial, industrial, infrastructure, and energy and utilities) and key regions (England, Northern Ireland, Scotland, and Wales). The report offers market sizes and forecasts for all the above segments in value (USD).

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the size and growth outlook for the UK construction market through 2031?

What is the size and growth outlook for the UK construction market through 2031?

Which segments lead the UK construction market in 2025?

Residential is the largest sector with a 38.10% share in 2025, new construction leads by type at 55.10%, and conventional on-site methods account for a 92.10% share.

Which parts of the UK show the strongest presence in construction activity?

England accounts for 79.55% share in 2025, with activity concentrated around major urban centers and strategic corridors. Northern Ireland has the fastest projected growth at 6.10% CAGR.

What are the top growth drivers for the UK construction market to 2031?

Government mega-projects in transport, the housing shortfall, net-zero retrofit demand, and scaling of modern methods of construction are key growth drivers.

What regulatory changes most impact delivery and procurement?

The Building Safety Act regime, the Procurement Act 2023, and planning reform under the Levelling Up and Regeneration Act are the most influential regulatory changes.

Where are the best opportunities for near-term wins?

Energy retrofits across public estates, standardized education and healthcare buildings, logistics nodes, and station-led regeneration represent high-visibility opportunities.

Page last updated on: