Builders Joinery And Carpentry Of Wood Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

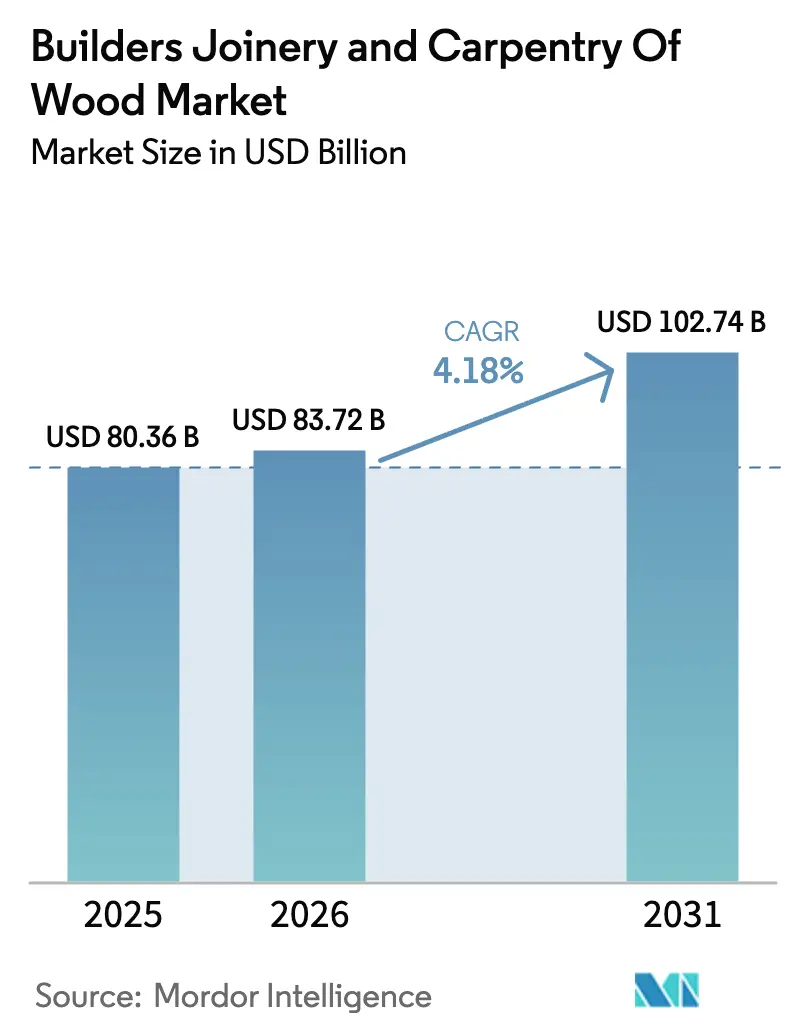

| Market Size (2026) | USD 83.72 Billion |

| Market Size (2031) | USD 102.74 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

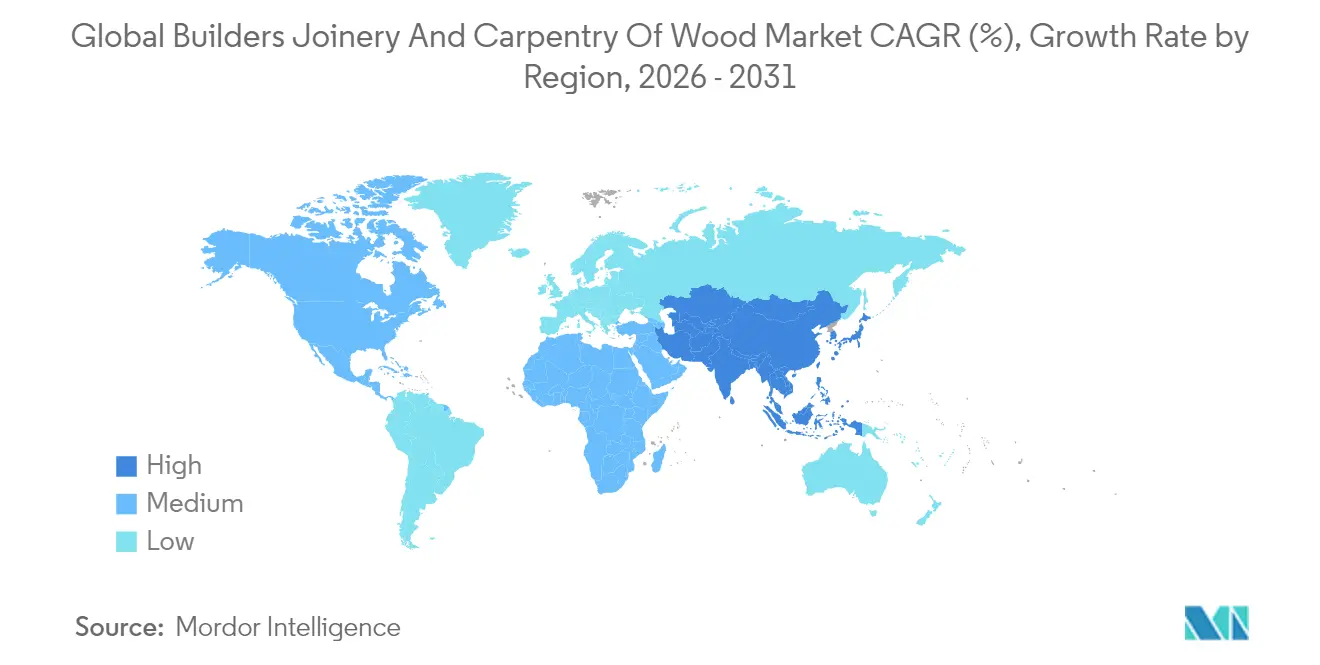

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Builders Joinery And Carpentry Of Wood Market Analysis by Mordor Intelligence

builders joinery and carpentry of wood market size in 2026 is estimated at USD 83.72 billion, growing from 2025 value of USD 80.36 billion with 2031 projections showing USD 102.74 billion, growing at 4.18% CAGR over 2026-2031. The expansion is fueled by green-building regulations, engineered-wood innovation, and digital manufacturing that compresses lead times while cutting waste. Mass-timber code upgrades unlock taller structures, and carbon-credit monetization converts embodied carbon into cash flow, enhancing project yields even as raw-material volatility and labor scarcity persist. Consolidation among large building-materials groups contrasts with a surge of tech disruptors introducing composites that rival steel on strength-to-weight metrics, reshaping competitive dynamics across the builders' joinery and carpentry of the wood market. However, wildfire-driven supply shocks and skilled-trade shortages strain execution, off-site prefabrication and circular-economy incentives offset near-term headwinds and anchor a resilient growth trajectory through 2030[1].Associated Builders and Contractors, “2025 Construction Workforce Shortage,” abc.org

Key Report Takeaways

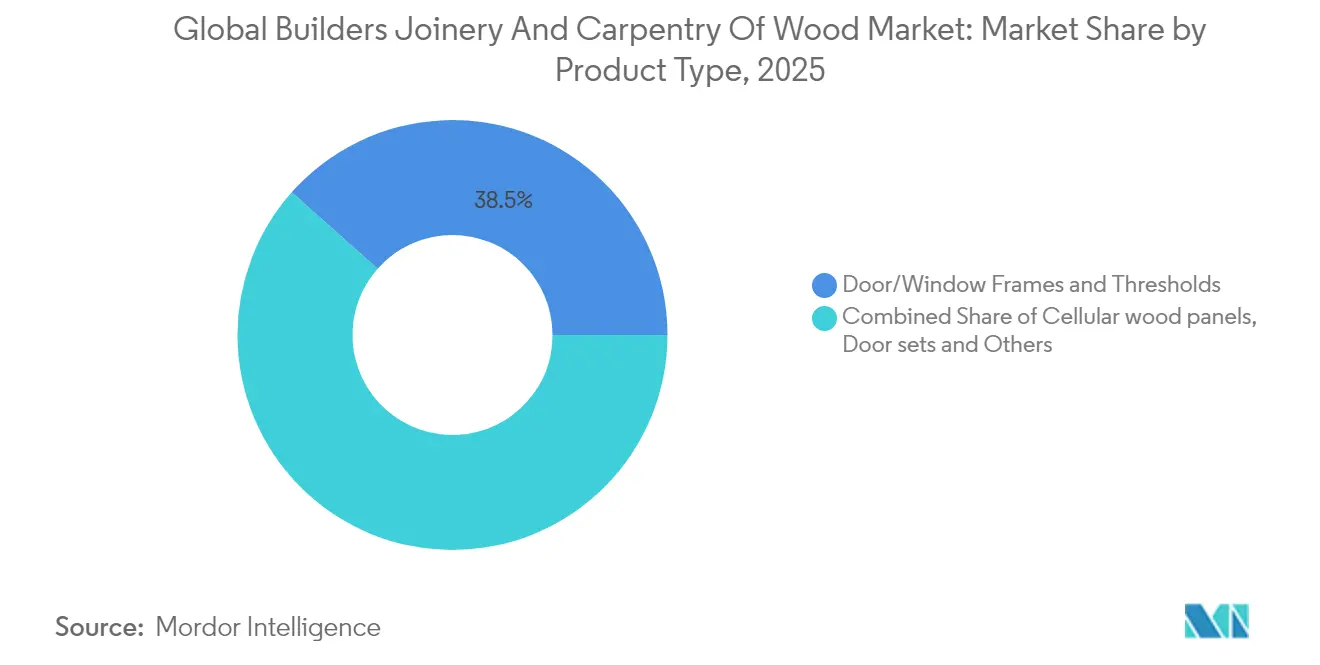

- By product type, door and window frames captured 38.45% of the builders joinery and carpentry of wood market share in 2025. The builders' joinery and carpentry of wood market size for cellular wood panels is projected to grow at a 6.52% CAGR between 2026 and 2031.

- By material, engineered wood commanded 53.05% of 2025 revenue. The builders joinery and carpentry of wood market size for engineered solutions is forecast to expand at a 5.62% CAGR through 2031.

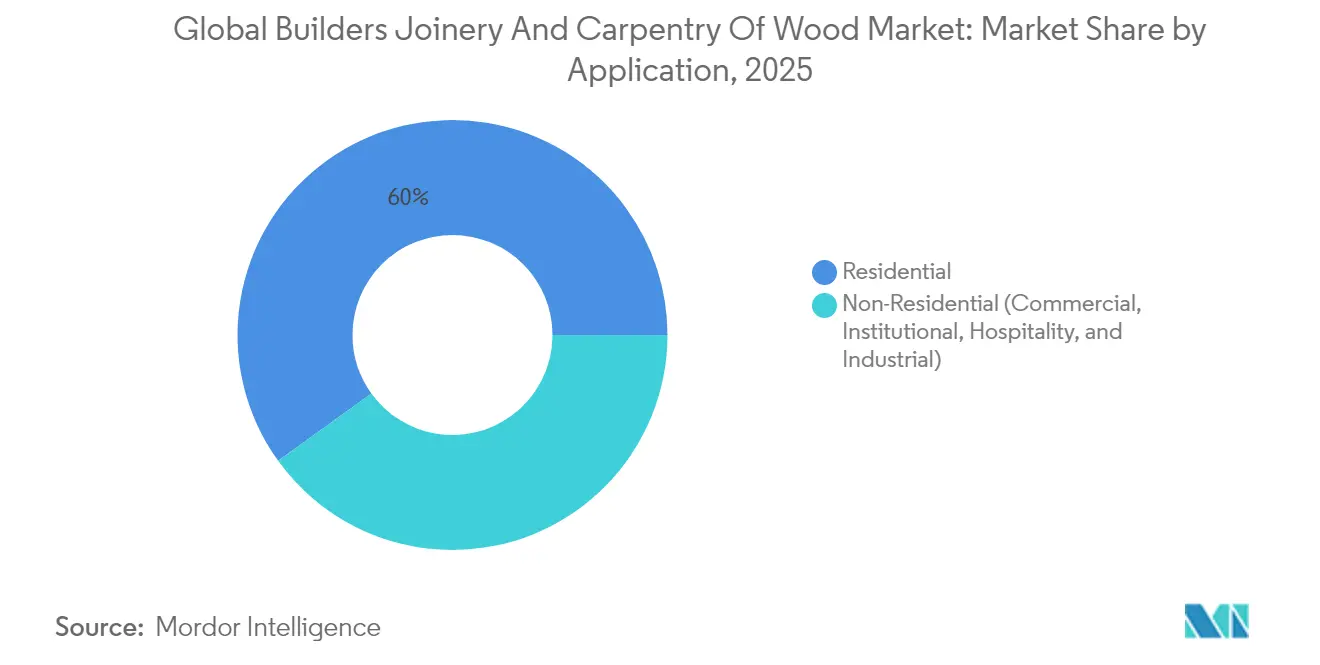

- By application, residential construction generated 59.95% of 2025 sales. Non-residential demand is advancing at a 5.74% CAGR as mass timber penetrates office and institutional projects.

- By geography, Asia-Pacific held 47.10% of the builders joinery and carpentry of wood market share in 2025. The region’s builders' joinery and carpentry of wood market size is expected to rise at a 6.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Builders Joinery And Carpentry Of Wood Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable construction & green-building mandates | +1.2% | Global, with early leadership in EU, California, Asia-Pacific | Medium term (2-4 years) |

| Rapid urbanisation fuelling new residential starts | +0.8% | APAC core, spill-over to MEA, Latin America urban centers | Long term (≥ 4 years) |

| Digital design-for-manufacture (DfMA) adoption by off-site builders | +0.6% | North America, Northern Europe, Japan, Australia | Short term (≤ 2 years) |

| High-rise timber engineering (mass-timber) proof-of-concept projects | +0.5% | North America, Europe, Singapore, Australia | Medium term (2-4 years) |

| Circular-economy demand for reclaimed timber systems | +0.4% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Carbon-credit monetisation for bio-based materials | +0.3% | Global, with early adoption in North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainable Construction & Green-Building Mandates

Regulations such as France’s RE2025 and California’s CALGreen elevate embodied-carbon limits, nudging architects toward certified wood over steel or concrete. The 2021 International Building Code allows 19-story mass-timber structures, transforming lofty prototypes into mainstream procurement options[2]International Code Council, “Tall Wood Provisions Expand Building Opportunities,” iccsafe.org. Developers now monetize stored biogenic carbon via platforms like Riverse, layering an incremental revenue stream on top of rent yields and green-bond eligibility. Municipal sourcing criteria award scoring premiums to bio-based envelopes, helping wood outcompete higher-carbon assemblies in public tenders. ESG-driven investors track embodied-carbon disclosures, institutionalizing demand for low-emission products. Insurers, once wary, revise underwriting after large-scale fire tests prove performance parity, broadening access to project finance. Certification programs such as FSC and PEFC verify responsible forestry, closing transparency gaps and qualifying projects for sustainable-finance tax breaks. Together, these policies, financial, and risk-management levers translate into a 1.2-percentage-point lift in forecast CAGR across the builders' joinery and carpentry of wood market.

Rapid Urbanisation Fuelling New Residential Starts

Asia-Pacific adds nearly 70 million urban residents annually, straining housing stock and compelling authorities to approve high-density multifamily projects that favor fast-install engineered panels. BIM-enabled layouts cut site labor by roughly one-third, a critical offset as wage inflation outpaces GDP in megacities. India’s Smart Cities Mission bundles infrastructure and housing approvals, compressing timelines and channeling demand toward prefabricated wall and floor systems. Brazil’s 20% export surge in October 2024 signals Latin American mills scaling output to feed global urban-housing booms, while U.S. multifamily starts remain resilient despite interest-rate volatility. Tokyo developers pioneer hybrid timber–steel frames that meet seismic codes while retaining wood’s low-carbon profile. Demographic momentum, cost pressure, and schedule risk together sustain high panel volumes well into the 2030s. Completion rates still hinge on easing skilled-labor gaps, yet modular assembly helps bridge supply-chain bottlenecks. Overall, intensified urbanization adds an estimated 0.8 percentage points to global CAGR within the builders' joinery and carpentry of wood market.

Digital Design-for-Manufacture Adoption by Off-Site Builders

Cloud-based BIM platforms let architects, engineers, and fabricators co-edit models in real time, eliminating RFIs that once stalled framing for weeks. Automated routers translate live drawings into cut files with millimeter precision, pushing yield rates above 90% and slashing scrap-disposal fees. Controlled factory settings enable two-shift operations immune to weather delays, granting schedule certainty prized by institutional investors. Early adopters report a 15–20% margin uplift as work shifts from variable job-sites into predictable production cells. Rising digital dependence, however, exposes plants to malware that can corrupt toolpaths and damage equipment, prompting insurers to require cyber-risk audits before underwriting builder's risk policies. Governments in Japan and Australia now offer tax credits for modular plants, accelerating technology diffusion among mid-tier contractors. Higher capital outlays deter some firms, but financing options improve as lenders see demonstrated productivity gains. As labor shortages worsen, DfMA adoption is expected to lift sector-wide CAGR by 0.6 percentage points.

High-Rise Timber Engineering (Mass-Timber) Proof-of-Concept Projects

Success in 2-hour fire-resistance testing of encapsulated CLT panels cleared regulatory paths for 19-story towers in multiple U.S. states. Flagship builds, such as Singapore’s 25-story composite office, provide full-scale data that reassure risk-averse financiers and municipal inspectors. Performance-based design shows seismic parity with concrete, broadening mass-timber’s appeal in quake-prone markets. Prefabricated core walls shorten crane cycles, reducing urban disruption and improving community acceptance. University architecture programs now teach tall-wood studio modules, expanding the talent pipeline. Manufacturing standards like ANSI/APA PRG-320 synchronize global quality benchmarks, enabling cross-border sourcing without bespoke tests. Schedule savings and carbon-credit revenue collectively narrow cost premiums to near-parity with steel frames, particularly on sites constrained by logistics or noise curfews. These validation milestones add about 0.5 percentage points to the medium-term CAGR of the builders' joinery and carpentry of wood market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-carpenter shortage & wage inflation | -0.9% | Global, with acute impacts in North America, Europe, Japan | Short term (≤ 2 years) |

| Volatile soft-wood prices driven by climate-linked supply shocks | -0.6% | North America, Northern Europe, supply-dependent regions | Short term (≤ 2 years) |

| Fire-safety code uncertainty for tall-timber structures | -0.4% | Global, with regulatory variations across jurisdictions | Medium term (2-4 years) |

| Digital IP & cyber-security risks in CAD-CAM joinery files | -0.2% | North America, Europe, technologically advanced markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled-Carpenter Shortage & Wage Inflation

The U.S. construction sector requires an extra 501,000 workers in 2024 and 454,000 in 2025 above normal hiring levels, with carpentry posting the steepest deficits. Europe shows one in three construction vacancies unfilled after 90 days, and 14 countries classify carpenters as high-severity shortages. Japan’s construction workforce shrank 20% in a decade, and nearly 40% of those remaining are over 55, foreshadowing a retirement wave by 2030. Rising wage bids swell framing budgets by USD 8 to10 per square foot on complex builds, forcing developers to reassess feasibility. Smaller contractors struggle to compete for talent, risking project cancellations that reverberate through supply chains. Apprenticeship incentives expand, yet long training cycles mean relief lags demand peaks. Automation offsets certain gaps, but robotic cells require capital that some firms cannot access under current lending conditions. Tight labor markets also increase safety incidents as overstretched crews work extended hours. Collectively, these factors subtract 0.9 percentage points from the projected CAGR in the builders' joinery and carpentry of wood market.

Volatile Soft-Wood Prices Driven by Climate-Linked Supply Shocks

Wildfires across Western Canada erased roughly 8 billion board feet of harvests in 2024, spiking lumber futures 45% within months and disrupting budget assumptions mid-project. Beetle infestations prompt salvage logging that gluts mills for a season yet leaves long-term supply short, injecting whiplash into price curves. Tariff frictions between major exporters and importers add policy risk, swinging delivered costs by triple-digit USD per thousand board feet. Small builders lack credit lines for margin calls that accompany hedging, leaving them exposed to spot spikes. Developers respond by substituting hybrid frames, yet redesign delays permitting and escalates engineering fees. Insurers raise course-of-construction premiums to reflect material volatility, adding to soft-cost burdens. Mills invest in fire-hardening and diversified log supply, but paybacks stretch out under current pricing structures. Persistent turbulence thus slices 0.6 percentage points from global CAGR expectations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cellular Panels Drive Innovation

Door and window frames generated 38.45% of 2025 revenue within the builders joinery and carpentry of wood market, supported by steady remodeling cycles and new-build demand across geographies. Despite dominance, their growth lags the overall curve as energy-efficient replacements and smart-sensing upgrades saturate mature markets. Cellular panels, conversely, chart a 6.52% CAGR through 2031 on the back of weight savings, rapid installation, and compatibility with robotic fabrication lines. The builders' joinery and carpentry of wood market size for cellular panels is forecast to climb from USD 19.74 billion in 2025 to nearly USD 28.82 billion by 2031, fueled by InventWood’s SuperWood, which offers 10× strength-to-weight gains and Class A fire ratings. Expanding panel widths let contractors span greater floor areas with fewer seams, reducing weather-seal leakage and inspection costs. Apex adopters in prefab housing stack pre-cut window openings that slash finish-carpentry labor by 40%, countering trade shortages. Meanwhile, Harvey Windows’ sensor-enabled entry door launch exemplifies innovation in the leading product class by merging IoT modules with lower U-values. Flooring, pergolas, shutters, and specialty façades deepen product diversity, allowing suppliers to cross-sell packages that lift average order values and dampen commodity rivalry.

Demand for assembled parquet panels grows alongside interior-design trends favoring warm, biophilic aesthetics in commercial lobbies and hospitality spaces. Producers targeting upscale residential clients offer FSC-certified tropical veneers laminated onto domestically sourced cores to navigate deforestation scrutiny. Digital CAD-CAM systems accelerate bespoke stair-stringer fabrication, allowing boutique builders to deliver complex geometries cost-effectively. In emerging markets, project-home builders still favor solid-wood doors for perceived durability, yet rising labor costs trigger a gradual shift toward pre-hung engineered alternatives. Regulatory tightening around energy codes drives uptake of triple-glazed timber windows in colder climates, pushing suppliers to expand insulated-glass capacity. Looking ahead, composite panel formats embedding phase-change materials promise improved thermal management, positioning panel suppliers for future building-performance mandates within the builders' joinery and carpentry of the wood market.

By Material & Construction: Engineered Dominance Accelerates

Engineered systems from CLT to laminated veneer lumber held 53.05% of 2025 revenue across the builders joinery and carpentry of wood market, and are on track for a 5.62% CAGR through 2031. Uniform mechanical properties, standardized fire ratings, and short installation time appeal to volume homebuilders and commercial developers alike. California’s Chapter 23 mandates AWPA treatment marks and corrosion-resistant fasteners for engineered elements, favoring suppliers with stringent quality controls. International buyers seek ANSI/APA PRG-320 and JAS-SE-11 certifications to de-risk structural liability, concentrating demand among mills capable of third-party auditing. Digital twin models map moisture gradients across thick glulam beams, enabling predictive maintenance that appeals to institutional asset managers. Lifecycle analyses reveal embodied-carbon savings up to 60% compared with concrete frames, a selling point now codified in procurement templates by global contractors. Supply-side economies of scale drop panel costs 15–18% as line speeds increase and scrap declines.

Solid wood retains a 46.95% share amid niche appeal in heritage restoration and high-end interiors, where grain aesthetics and acoustic warmth command premiums. European artisans integrate reclaimed oak from century-old barns into bespoke staircases, capitalizing on circular-economy storytelling. EU-funded LIFE EcoTimberCell advances biodegradable binder research to fuse local softwoods into cellular units, targeting CE marking and Environmental Product Declaration credentials for mid-rise structures. Luxury residential developers pair solid-wood millwork with engineered load-bearing frames, creating hybrid packages that blend authenticity and performance. Outside affluent markets, local carpenters prize solid timber’s forgiving workability, sustaining baseline demand even as engineered penetration rises. Over the forecast window, a gradual migration from solid to engineered formats is likely, yet co-existence remains as designers differentiate spaces via tactile materiality. Overall, engineered dominance accelerates but does not eliminate solid-wood niches, maintaining material diversity that broadens supplier revenue streams across the builders' joinery and carpentry of wood market.

By Application: Non-Residential Momentum Builds

Residential projects accounted for 59.95% of 2025 sales in the builders joinery and carpentry of wood market, buoyed by suburban renovation and emerging-market housing drives. Replacement windows and multi-slide patio doors dominate North American renovation budgets, while Europe’s Fit-for-55 directive spurs thermal retrofit programs that specify triple-glazed timber units. In Asia, governments promote industrialized construction systems to meet affordable-housing targets, accelerating demand for panelized wall kits. Aging housing stock in Japan triggers refurbishment cycles where cross-laminated sash frames reduce air leakage and cut heating bills, aligning with nationwide decarbonization goals. DIY retailers leverage modular pergola kits and cabinetry lines to capture discretionary spend, widening the channel mix. Despite robust volume, growth moderates as household formation slows in mature economies, shifting momentum toward non-residential sectors.

Non-residential demand is projected to grow at a 5.74% CAGR through 2031, propelled by mass-timber penetration into offices, schools, hotels, and logistics facilities. U.S. commercial construction is slated to climb 7% in 2025, and institutional segments such as military barracks and nursing homes are expected to expand 56.4% and 36.5% respectively. Developers cite faster erection and lower embodied carbon among the chief reasons for adopting engineered-wood superstructures. Hospitality brands favor wood interiors for the biophilic ambiance that drives higher guest satisfaction scores, while office landlords market exposed CLT ceilings as premium ESG features. Industrial developers test hybrid glulam–steel portals that balance clear spans with carbon performance, appealing to e-commerce tenants’ sustainability pledges. In higher-education projects, mass-timber labs attract STEM students while doubling as living-learning exhibits on climate-smart construction. The builders' joinery and carpentry of the wood market thus evolves from housing-centric to a balanced portfolio serving a wider range of end-users.

Geography Analysis

Asia-Pacific dominated 2025 revenue with a 47.10% stake in the builders joinery and carpentry of wood market, driven by rapid urban migration, infrastructure stimulus, and expanding manufacturing clusters in China, India, and ASEAN. Beijing’s 14th Five-Year Plan emphasizes prefabricated construction to cut urban pollution, prompting municipal builders to specify engineered panels that arrive sealed against moisture. India’s Production-Linked Incentive scheme subsidizes laminated veneer lumber plants, reducing import reliance and fostering regional panel hubs in Andhra Pradesh and Gujarat. Japan’s Expo 2025 showcases a 675-meter timber ring, demonstrating large-span wood engineering despite workforce constraints. Indonesia promotes certified tropical hardwood exports, supplying raw veneer to panel mills across the region, while Singapore’s Gaia building illustrates tall-timber feasibility in humid tropics. Localized supply chains shorten lead times and stabilize currency exposure, yet climate-driven log shortages in Western Australia underscore resource risk. Digital-fabrication start-ups in Vietnam leverage cloud-BIM to service regional residential developers, signaling rising tech adoption.

North America captures considerable value through established forest assets, deep prefab expertise, and regulatory tailwinds from the 2021 IBC that legitimize 19-story mass-timber towers. State-level code uptake spreads eastward, with Michigan’s April 2025 enactment delivering critical certainty for Great Lakes developers. Canada’s boreal forest fuels integrated CLT plants, though wildfire-related shutdowns curb output and reveal supply fragility. U.S. lumber futures fluctuations push builders toward long-term offtake contracts, locking in panel volumes for multi-family pipelines. Venture-backed robotic framing start-ups cluster around Seattle and Toronto, feeding innovation spillovers into regional subcontractor networks. Federal tax credits under the Inflation Reduction Act reward low-carbon materials, further privileging wood over steel, especially in public works. Rising cyber-risk prompts mills to adopt zero-trust networks, enhancing resilience but adding overhead. Educational outreach by trade associations targets code officials, smoothing approval for upcoming tall-wood bids.

Europe combines a stringent decarbonization policy with a rich craft heritage, but labor scarcity hampers output even as demand climbs. The EURES dashboard lists carpentry among the top three high-severity shortages in 14 member states. Germany’s timber-frame volumes expand under subsidies for energy-positive schools, while Scandinavian sawmills pioneer bio-epoxy bonded panels compatible with circular-economy design. The Nordic Wood Declaration commits governments to public-sector timber quotas, anchoring predictable demand. In Central and Eastern Europe, wage-inflation pressures accelerate investment in robotic joinery lines to sustain export competitiveness. France’s RE2025 reinforces life-cycle carbon accounting, tightening specs that favor manufacturers offering Environmental Product Declarations. The United Kingdom, post-Brexit, aligns building regulations with Eurocode updates yet lags in mass-timber adoption due to fire-safety debates. Overall, Europe’s policy clarity offsets workforce constraints, keeping CAGR on par with global averages and cementing the continent’s role as a technology incubator for the builders' joinery and carpentry of the wood market.

Middle East & Africa and Latin America, while smaller contributors, post above-average growth. Saudi Arabia’s megaprojects Neom and the Red Sea developments specify biophilic resorts using engineered-wood façades to moderate desert climates. South Africa’s public-housing backlog channels funding into modular timber-frame units that assemble rapidly and meet energy-efficiency codes. Brazil leverages abundant plantation pine and eucalyptus to supply both domestic builds and exports; its October 2024 20% export jump signals strengthening global linkage. Chile’s seismic-resilient glulam plants target U.S. West Coast builders seeking alternative suppliers to mitigate wildfire disruptions. African coastal nations, rich in tropical hardwoods, trial certified small-diameter timber in coastal resorts, provided procurement aligns with anti-deforestation pledges. These regions collectively add diversity and resource depth that hedge geopolitical concentration risk in the builders' joinery and carpentry of the wood market.

Competitive Landscape

Fragmentation persists despite intensifying M&A, leaving ample room for regional specialists alongside global conglomerates. James Hardie’s USD 8.75 billion acquisition of AZEK in March 2025 merges siding, decking, and panel lines into an integrated portfolio with coast-to-coast distribution. Holcim’s USD 136 million purchase of OX Engineered Products in October 2024 injects sheathing and insulation into its low-carbon-materials thesis, illustrating cement majors’ pivot toward wood-based offerings. The top five players account for roughly 28% of worldwide turnover, signaling a moderately concentrated but still contestable field. Inventory strategies shift toward make-to-order after COVID-era bullwhips; mills install AI-driven yield-optimization scanners to raise throughput and shrink unsold stock. Tech disruptors such as InventWood will enter commercial production of SuperWood in mid-2025, leveraging venture capital to scale high-strength composites that could supplant aluminum curtain walls.

Regional champions fortify positions through product localization and just-in-time service. German firms offer factory-finished CLT modules sized for urban infill, while Australian mills certify bushfire-resistant panels in response to climate-linked hazard codes. Japanese conglomerates retrofit plants with robotic finishing cells that cut person-hours 40%, cushioning wage pressure. North American cooperatives bundle forest-management services and carbon-credit brokerage, monetizing vertically integrated chains. Cybersecurity evolves into a differentiator; Nordic groups market ISO 27001-compliant design portals that reassure insurers and secure enterprise contracts. Marketing narratives tilt toward circularity, with companies touting reclaimed-timber lines that meet EU taxonomy rules and attract green investors. Supplier collaboration with architects via digital configurators accelerates specification, shifting influence upstream toward manufacturers.

Price competition remains stiff in commodity door and moulding lines, yet value migrates to certified, pre-finished, and digitally traceable products. Strategic partnerships emerge between panel makers and modular-home builders to lock in demand and co-develop proprietary connectors, raising switching costs for competitors. Litigation around patent infringement of puzzle-joint systems creeps up as barriers to entry tighten. Equipment OEMs bundle preventative-maintenance analytics, embedding themselves deeper into mill operations and generating recurring revenue that shields against construction downturns. Ultimately, competitive intensity balances innovation and consolidation, fostering a dynamic but disciplined terrain for stakeholders in the builders' joinery and carpentry of the wood market.

Builders Joinery And Carpentry Of Wood Industry Leaders

Masonite International

JELD-WEN Holding Inc

Andersen Corporation

ASSA ABLOY

Pella Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: James Hardie closed its USD 8.75 billion acquisition of AZEK, creating a diversified exterior-products leader poised for deeper penetration in residential and commercial channels.

- January 2025: InventWood confirmed summer-2025 start-up of SuperWood production in Maryland after raising USD 50 million, including a USD 15 million Series A first close.

- October 2024: Holcim bought OX Engineered Products for USD 136 million, expanding its North American engineered-wood footprint and reinforcing its decarbonization roadmap

- September 2024: Harvey Windows introduced its smart Entry Door System, featuring integrated sensors and improved R-values for residential retrofits.

Global Builders Joinery And Carpentry Of Wood Market Report Scope

Carpentry and joinery are both construction trades. In its simplest and most traditional sense, joiners ‘join’ wood in a workshop, whereas carpenters construct the building elements on-site.

The global builders joinery and carpentry of wood market is segmented by type (cellular wood panels, windows, assembled parquet panels, doors, and other types), by application (furniture, building, and other applications), and by geography (North America, Latin America, Europe, Asia Pacific, and Middle East & Africa).

The report offers the market size for the global builders' joinery. The report offers market size for global builders' joinery and carpentry of wood market in value (USD) for all the above segments.

| Cellular Wood Panels |

| Door/Window Frames & Thresholds |

| Assembled Parquet Panels / Wood Flooring |

| Doors (interior & exterior) & Sets |

| Others (Staircases & Stair Parts, Shutters, Blinds, Louvres, cladding/sidings, pergolas, fence panels, etc) |

| Solid wood |

| Engineered wood |

| Residential |

| Non-Residential (Commercial, Institutional, Hospitality, and Industrial) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Cellular Wood Panels | |

| Door/Window Frames & Thresholds | ||

| Assembled Parquet Panels / Wood Flooring | ||

| Doors (interior & exterior) & Sets | ||

| Others (Staircases & Stair Parts, Shutters, Blinds, Louvres, cladding/sidings, pergolas, fence panels, etc) | ||

| By Material & Construction | Solid wood | |

| Engineered wood | ||

| By Application | Residential | |

| Non-Residential (Commercial, Institutional, Hospitality, and Industrial) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the builders joinery and carpentry of wood market today

The sector was valued at USD 83.72 billion in 2026 and is projected to reach USD 102.74 billion by 2031.

What is the current Global Builders Joinery And Carpentry Of Wood Market size?

In 2026, the Global Builders Joinery And Carpentry Of Wood Market size is expected to reach USD 83.72 billion.

What product category is gaining share most rapidly?

Cellular wood panels post the fastest expansion at a 6.52% CAGR on superior strength-to-weight ratios and quick installation cycles.

Why are engineered-wood systems overtaking solid wood?

Uniform strength, code-certified fire ratings, and eligibility for carbon credits help engineered panels outpace solid-wood alternatives.

What is the main headwind facing suppliers?

Acute carpenter shortages and wage inflation raise project costs and limit capacity, reducing forecast CAGR by roughly 0.9 percentage points.

Page last updated on: