Dry-Mix Mortar Additives And Chemicals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

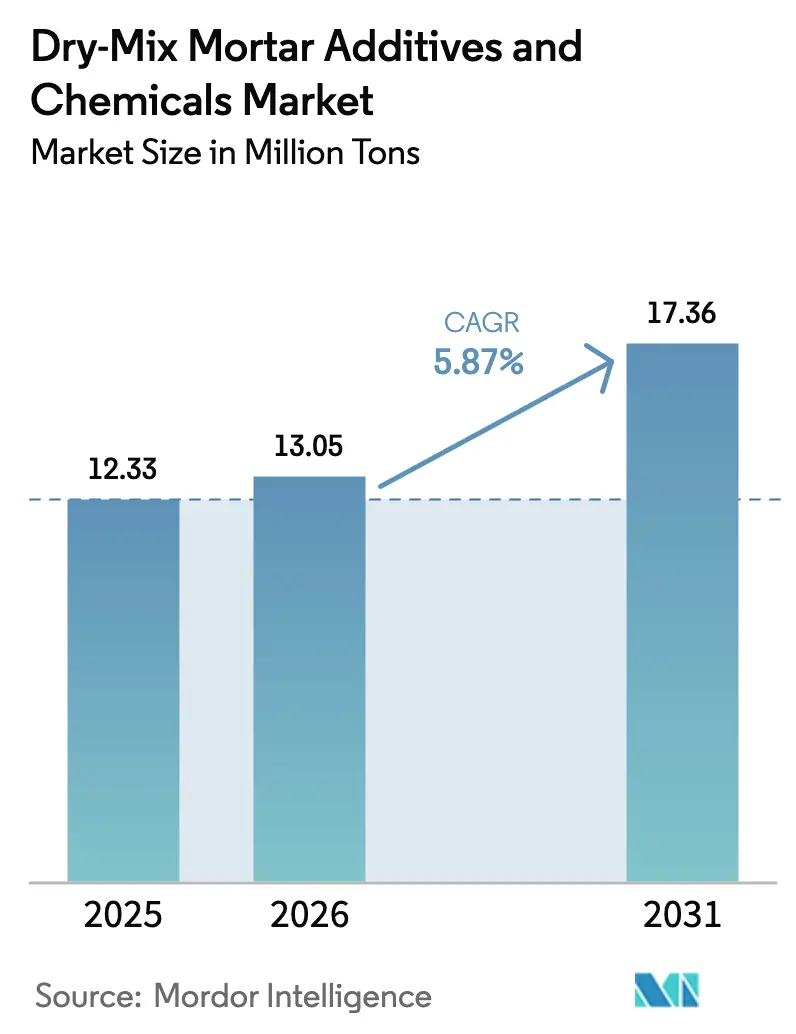

| Market Volume (2026) | 13.05 Million tons |

| Market Volume (2031) | 17.36 Million tons |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

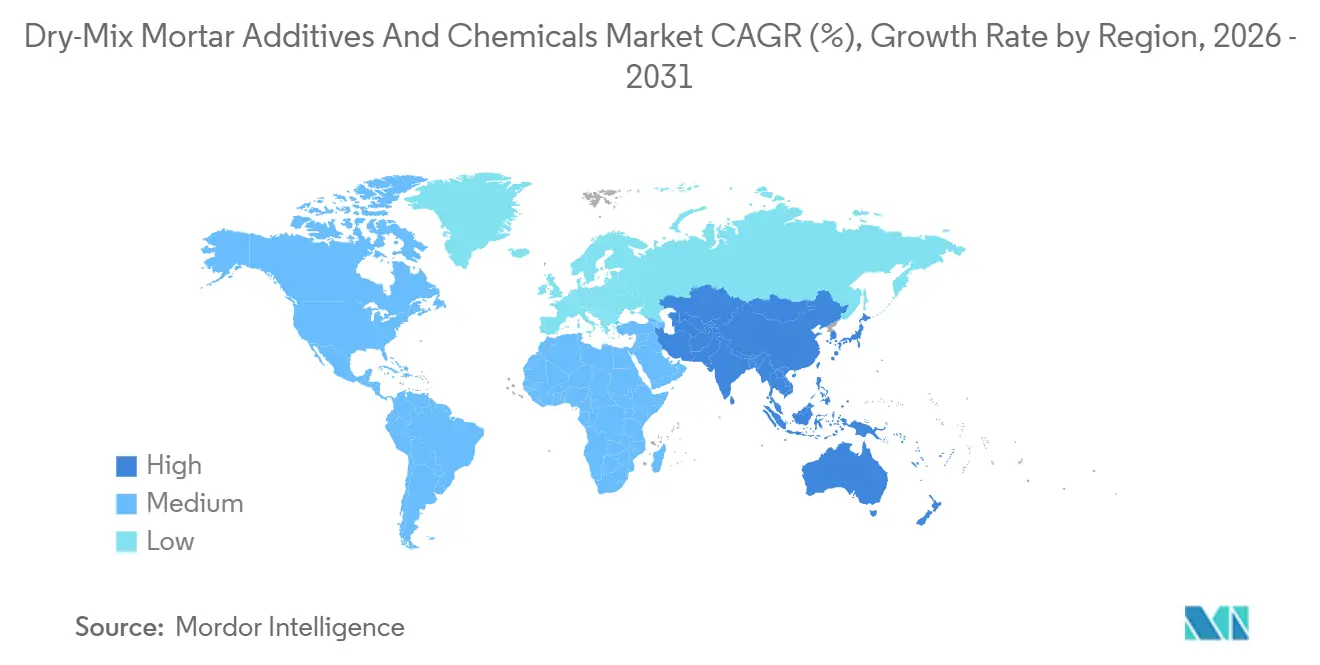

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

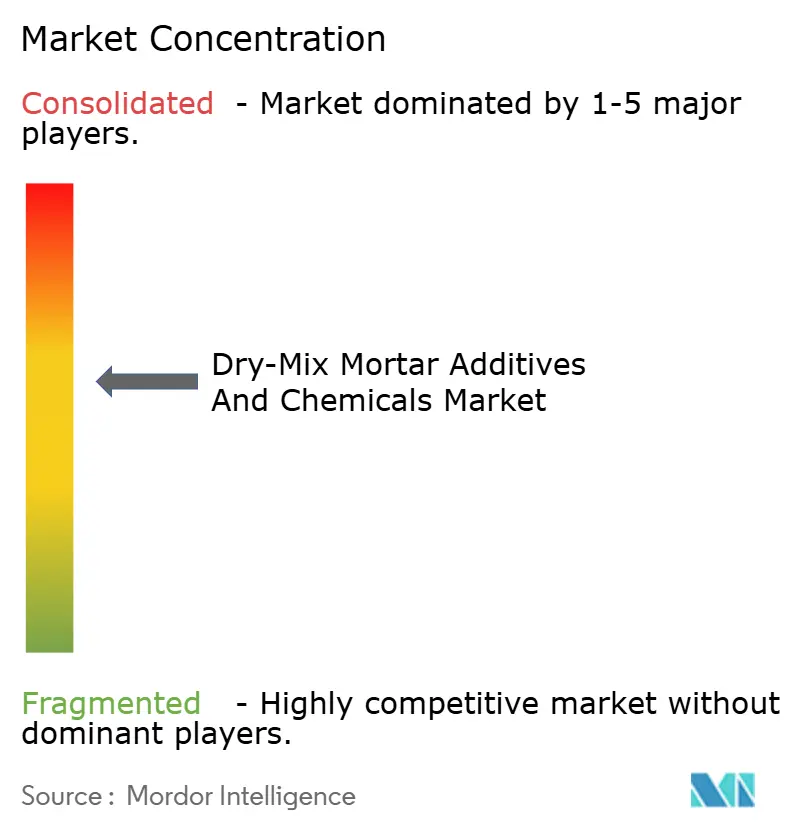

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dry-Mix Mortar Additives And Chemicals Market Analysis by Mordor Intelligence

The Dry-Mix Mortar Additives and Chemicals Market size is expected to increase from 12.33 million tons in 2025 to 13.05 million tons in 2026 and reach 17.36 million tons by 2031, growing at a CAGR of 5.87% over 2026-2031. Robust public-sector spending in India and accelerated industrial works in China underpin volume gains, while dust-control ordinances in the United States and European renovation mandates institutionalize factory-blended mortars as the default procurement path. Producers with vertically integrated polymer chains absorb raw-material volatility better than regional blenders, securing long-term contracts for metro-rail, bridge-deck, and EIFS retrofits. Vinyl acetate monomer and acrylic acid price swings remain the chief margin threat, although suppliers hedged by in-house monomer production shield end-users from quarterly list-price shocks. Equipment-intensive dry-mix plants act as a deterrent for new entrants, effectively locking in incumbents’ technical-service relationships across Asia-Pacific transport megaprojects and Europe’s Retrofit Wave.

Key Report Takeaways

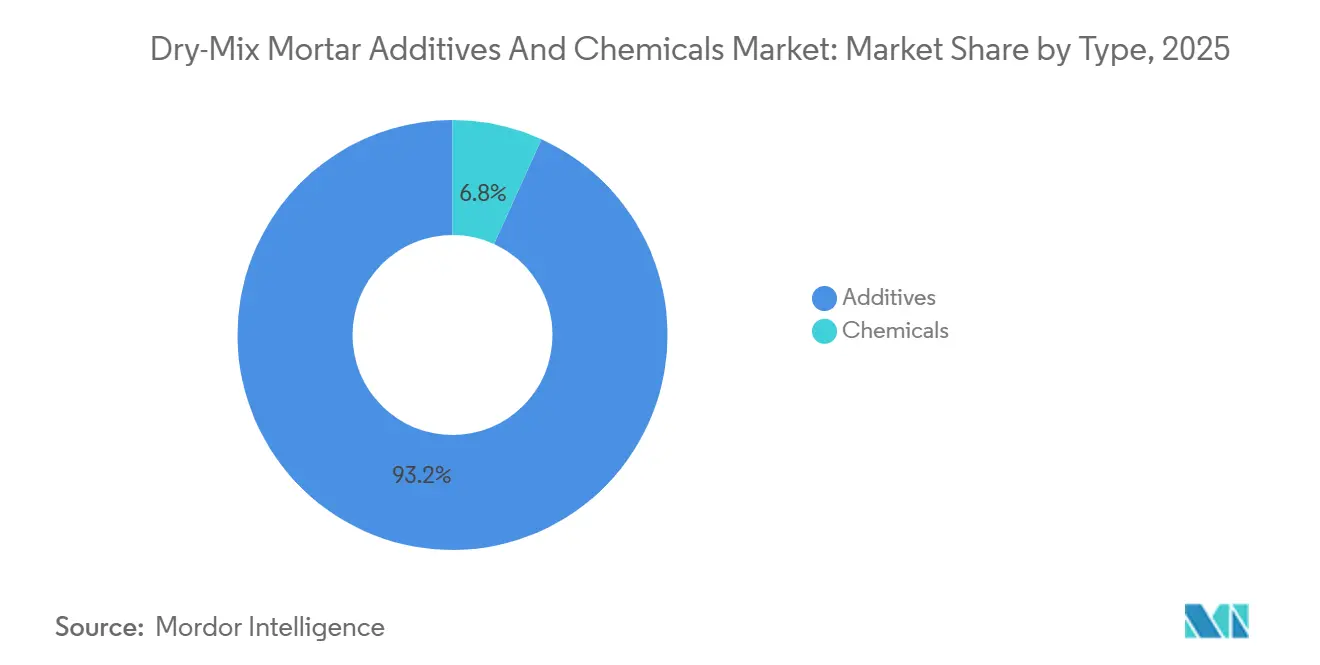

- By type, additives captured 93.20% of the Dry-Mix Mortar Additives and Chemicals market share in 2025 and are forecast to register a 5.94% CAGR during the forecast period (2026-2031).

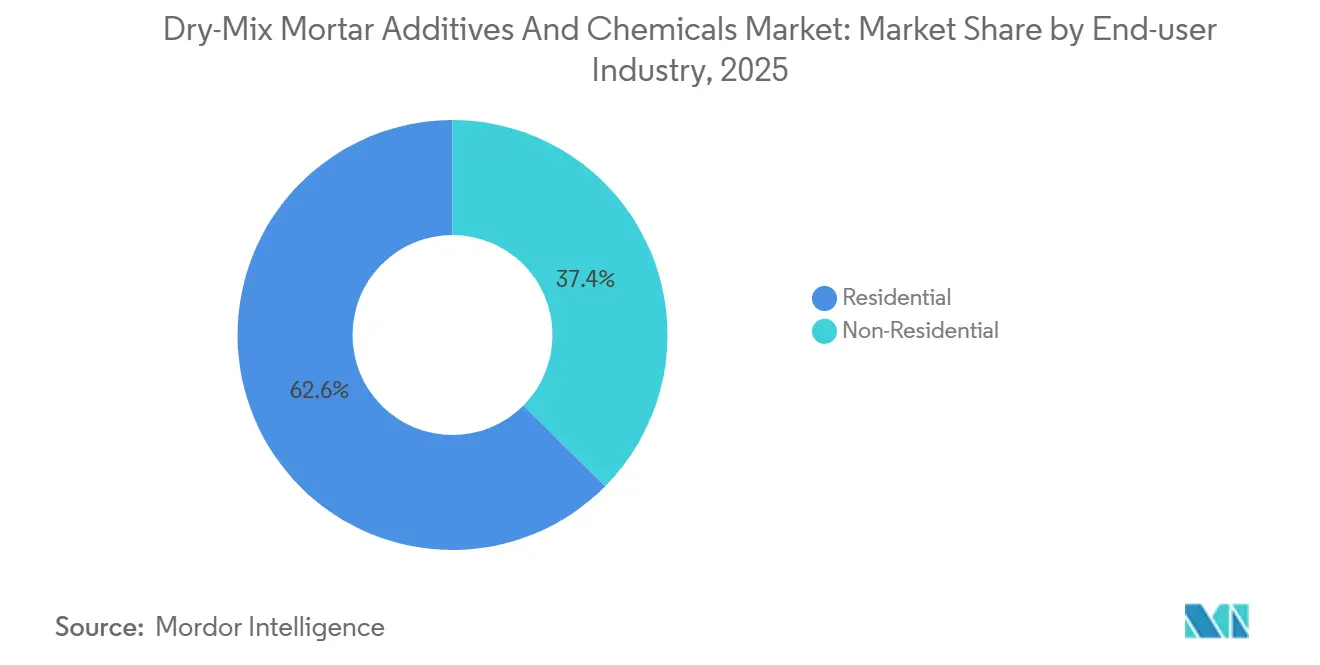

- By end-user industry, residential applications held 62.57% share of the Dry-Mix Mortar Additives and Chemicals market size in 2025 and are projected to expand at a 5.95% CAGR during the forecast period (2026-2031).

- By geography, the Asia Pacific held the market share of 36.59% in 2025, and this is expected to grow with a CAGR of 6.65% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dry-Mix Mortar Additives And Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising construction activity in Asia-Pacific | +1.8% | China, India, Southeast Asia | Medium term (2–4 years) |

| Long-term cost efficiency in construction | +1.2% | Global, early gains in North America, Europe | Long term (≥4 years) |

| Growing renovation demand in Europe | +1.0% | Germany, France, United Kingdom, Italy | Medium term (2–4 years) |

| Government dust-control mandates | +1.3% | North America, Europe, Australia | Short term (≤2 years) |

| 3D-printing and modular construction synergy | +0.6% | North America, Middle East, Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Construction Activity in Asia-Pacific

India's Union Budget 2026 allocated INR 12.2 lakh crore (USD 146 billion) for capital expenditure, with ₹5.98 lakh crore for transport infrastructure and INR 85,522 crore for urban development, driving demand for high-performance construction materials like tile adhesives and waterproofing mortars[1]Ministry of Finance, “Union Budget 2026 Capital Expenditure,” finmin.nic.in. China's construction sector, despite a 10.6% property-investment decline in 2024, is shifting toward industrial and logistics facilities, leveraging dry-mix mortars for efficiency amid a shrinking workforce. Southeast Asia, led by Vietnam and Indonesia, is adopting pre-mixed formulations to meet World Bank–mandated ASTM C1714 standards for infrastructure projects. However, supply-chain risks, such as typhoons disrupting polymer-powder shipments, pose challenges. The region's 6.65% forecast CAGR depends on sustained public-sector capex, though fiscal constraints in debt-laden provinces may slow new tenders after 2028.

Long-Term Cost Efficiency in Construction

Contractors using factory-blended dry-mix mortars have reduced material waste to under 2%, saving USD 8,000-12,000 annually for mid-sized residential projects. Labor productivity has improved, saving 3-4 hours per 1,000-square-foot application by eliminating on-site batching errors. These benefits, significant in wage-inflated markets like the United Arab Emirates (UAE) and Singapore, require an upfront investment of USD 150,000-250,000 in silo storage and pneumatic systems, limiting adoption in fragmented markets like India's Tier-2 cities. A 2025 study by IIT (Indian Institute of Technology) Delhi showed polymer-modified renders extended facade-maintenance cycles from 7 to 12 years, cutting lifecycle costs by 23%. This has driven procurement committees to favor pre-qualified dry-mix suppliers, strengthening incumbents with established technical-service networks.

Growing Renovation and Retrofit Demand in Europe

The EU Renovation Wave strategy mandates energy-performance upgrades for 35 million buildings by 2030, with Germany's Building Energy Act (GEG) requiring thermal transmittance (U-value) reductions that necessitate exterior insulation finishing systems (EIFS) anchored by polymer-modified base coats. France’s MaPrimeRénov dispensed EUR 2.4 billion in 2025, boosting cellulose-ether offtake in adhesive mortars for EPS insulation.

Government Dust-Control Mandates

Nevada's Clark County adopted Section 94 dust-control regulations in 2024, prohibiting on-site cement mixing within 500 feet of occupied structures and mandating factory-blended mortars for all commercial projects exceeding 10,000 square feet, a rule that converted 40% of Las Vegas-area contractors to dry-mix systems within 18 months. European Union member states transposing the Carcinogens and Mutagens Directive (CMD) have set binding occupational exposure limits (BOEL) for respirable crystalline silica at 0.1 mg/m³, a level unattainable with traditional site mixing, thereby institutionalizing demand for pre-mixed mortars.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for dry-mix plants | -0.8% | Emerging markets, Tier-2 Asia cities | Short term (≤2 years) |

| Volatile specialty-polymer prices | -1.1% | Global, acute in Europe and North America | Short term (≤2 years) |

| Stringent VOC and dust regulations | -0.5% | North America, Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capex for Dry-Mix Plants

Establishing a 200,000-ton-per-year dry-mix mortar plant requires USD 50–70 million in capital expenditure, covering silo arrays, computerized batching systems, and ISO 14001-compliant dust-collection infrastructure. High financing rates (9–12%) in markets like Indonesia and the Philippines deter regional players. Smaller formulators often lease toll-manufacturing capacity, losing 15–20% margins and control over formulation IP, limiting customization. Wacker's Nanjing facility, operational since 2024, exemplifies scale economies with a EUR 80 million (USD 87 million) investment supporting 60,000 tons of dispersible-polymer-powder capacity through multi-year offtake agreements. In contrast, mid-tier suppliers in Gujarat and Tamil Nadu operate smaller plants (20,000-40,000 tons/year) with batch variability, disqualifying them from precast-concrete tenders. The top 10 producers control 55% of global capacity, while over 200 regional blenders share the remaining 45%.

Volatility in Specialty-Polymer Prices

In 2024–2025, vinyl acetate monomer (VAM) spot prices ranged from USD 1,250 to USD 1,620 per ton, driven by ethylene feedstock fluctuations and outages at Celanese's Clear Lake facility, which supplies 18% of North America's VAM[2]Celanese Corporation, “Operational Update 2025,” celanese.com. Redispersible polymer powder producers without long-term VAM contracts faced 12–15% input-cost inflation but couldn't fully pass on costs, reducing EBITDA margins from 22% in 2023 to 17% by mid-2025. Acrylic acid prices rose 19% in Q1 2025 after a force majeure at a Shandong, China, facility, forcing costly airfreight for European formulators. Volatility has shifted margin risks to additive suppliers, discouraging R&D in bio-based alternatives. Mid-tier players without vertical integration are most affected, while BASF and Dow mitigate risks through internal hedging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polymer-Driven Additives Dominate Formulation Economics

Additives represented 93.20% of volume in 2025 and are set to grow with a CAGR of 5.94% during the forecast period (2026-2031). Redispersible polymer powders remain the anchor sub-segment, essential for EN 12004-C2 tile adhesives across Asia-Pacific’s residential towers. Hydroxypropyl methylcellulose, at USD 3,200-4,500/ton, underpins self-leveling screeds in data centers, enabling ±3 mm flatness over 2 m spans. Air-entraining agents see episodic spikes in Canada’s freeze-thaw bridge works, yet trail polymer powders in volume.

Chemicals power niche roles. Anhydrite shrinkage compensators curb cracking in automated-warehouse slabs, while accelerators support winter pours in the Baltics. EU REACH (European Union Registration, Evaluation, Authorisation and Restriction of Chemicals) compliance fees of EUR 200,000-500,000 per variant deter mid-tier innovation, consolidating supply around multi-national incumbents.

By End-User Industry: Residential Renovation Offsets New-Build Slowdown

In 2025, residential applications held a dominant 62.57% share of the Dry-Mix Mortar Additives and Chemicals market, with a projected CAGR of 5.95% during the forecast period (2026-2031). Regional trends drive this growth: India’s tower completions boost demand for tile adhesives and plasters, Germany’s façade retrofits consume polymer-modified base coats, and the United States multi-family projects rely on pre-bagged mortars despite high mortgage rates. In China, affordable housing in Tier-3 cities sustains demand for interior screeds, offsetting reduced new launches. Renovation activities in mature economies are compensating for weaker new-build momentum, maintaining steady residential demand.

Non-residential construction accounted for the rest of the market in 2025, with growth tied to mega-project schedules. The Middle East sees rising commercial activity, with Saudi tourism complexes using high-performance mortars, while Canada’s data centers and cold-storage hubs require thermal-shock-resistant screeds. Industrial and institutional projects, like Singapore’s pharmaceutical plants, prefer premium epoxy-modified mortars, increasing revenue per ton. Infrastructure projects, including India’s expressways, United States bridge-deck overlays, and European Union rail extensions, drive demand for polymer-modified repair mortars, though public-sector delays may push volumes beyond 2027. Non-residential demand remains sensitive to fiscal delays but generates significant orders when activated, causing quarterly tonnage fluctuations.

Geography Analysis

Asia-Pacific held a 36.59% share in 2025, advancing with a CAGR of 6.65% during the forecast period (2026-2031). India’s expressways and metros consume polymer-modified mortars at rates 30-40% above estimates because of monsoon-driven rework. China’s state enterprise pipeline shifts volume into industrial parks and high-speed rail depots. Southeast Asia imports 25–35% of pre-mixed mortars due to ISO 9001 gaps, inflating landed costs but guaranteeing ASTM-grade quality.

Europe’s Renovation Wave props stable but slower growth; Germany’s Exterior Insulation and Finish Systems (EIFS) retrofits demand up to 15 kg base coat m², while UK BS 8414 fire tests narrow the supplier base to three certified producers. North American infrastructure funds back-load demand, with bridge-deck overlays peaking post-2027. Saudi Arabia’s USD 1.3 trillion Vision 2030 program injects episodic but premium-priced spikes, offset by project-timeline slippage.

Competitive Landscape

The Dry-Mix Mortar Additives and Chemicals Market is moderately consolidated. The top-10 players control about 55% of global capacity, a mid-level concentration partly solidified by Sika’s USD 6.2 billion MBCC acquisition, which merged admixtures and dry-mix under one roof. Mid-tier firms pivot toward bio-based cellulose ethers targeting LEED v4.1 credits, carving 12–15% pricing headroom yet lacking scale. AI-assisted formulation is emerging as a differentiator: it reduces trial batches by 50%, a USD 2–3 million barrier for regional blenders.

Dry-Mix Mortar Additives And Chemicals Industry Leaders

Wacker Chemie AG

Dow

Sika AG

BASF

Mapei S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: MAPEI Corporation (United States) unveiled Mapeair 154, a multi-component air-entraining admixture designed to ensure a stable and consistent air-void system during every phase of concrete production.

- October 2025: Bhageria Industries Limited, aiming to diversify its offerings, secured the green light to begin commercial production of new plasticizers and ethoxylates, responding to the surging market demands.

Global Dry-Mix Mortar Additives And Chemicals Market Report Scope

Dry-mix mortar additives and chemicals are added to the mortar to enhance the chemical properties, thereby improving the performance, such as structural strength, flexibility, bonding strength with various substrates, compressive strength, and abrasion resistance.

The Dry-mix Mortar Additives and Chemicals Market is segmented by type, end-user industry, and geography. By type, the market is segmented into additives (redispersible polymer powder, plasticizers, defoamers, cellulose ether, air entraining agents, and other additives) and chemicals (shrinkage (anhydrites), retarders, and accelerators). By end-user industry, the market is segmented into residential and non-residential (commercial, industrial and institutional, and infrastructure). The report also covers the market size and forecasts for the bio-based polymers market in 15 countries across major regions. The report offers market sizes and forecasts for each segment based on volume (tons).

| Additives | Redispersible Polymer Powder |

| Plasticizers | |

| Defoamers | |

| Cellulose Ether | |

| Air Entraining Agents | |

| Other Additives | |

| Chemicals | Shrinkage (Anhydrites) |

| Retarders | |

| Accelerators |

| Residential | |

| Non-Residential | Commercial |

| Industrial and Institutional | |

| Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Additives | Redispersible Polymer Powder |

| Plasticizers | ||

| Defoamers | ||

| Cellulose Ether | ||

| Air Entraining Agents | ||

| Other Additives | ||

| Chemicals | Shrinkage (Anhydrites) | |

| Retarders | ||

| Accelerators | ||

| By End-User Industry | Residential | |

| Non-Residential | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast will the Dry-Mix Mortar Additives and Chemicals market grow through 2031?

Volumes are forecast to advance from 13.05 million tons in 2026 to 17.36 million tons by 2031, equal to a 5.87% CAGR during the forecast period (2026-2031).

Which region is expected to post the strongest volume growth?

Asia-Pacific leads with a projected 6.65% CAGR during the forecast period (2026-2031)., powered by India’s transport megaprojects and China’s pivot to industrial and logistics facilities.

Who are the primary suppliers shaping competitive dynamics?

Sika, BASF, Wacker, Mapei, Dow, Nouryon, Evonik, Ashland, Celanese, and Saint-Gobain collectively control about 55% of global capacity.

How do dust-control regulations influence adoption of factory-blended mortars?

US and EU rules that cap respirable silica to 0.1 mg/m³ effectively prohibit on-site cement mixing, pushing contractors toward pre-bagged or silo-fed dry-mix systems for compliance.

What raw-material risks most threaten profit margins?

Price swings in vinyl acetate monomer and acrylic acid, both fluctuated 18-22% quarter-over-quarter during 2024-2025, create cost shocks that independent additive blenders struggle to pass through.

Page last updated on: