Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

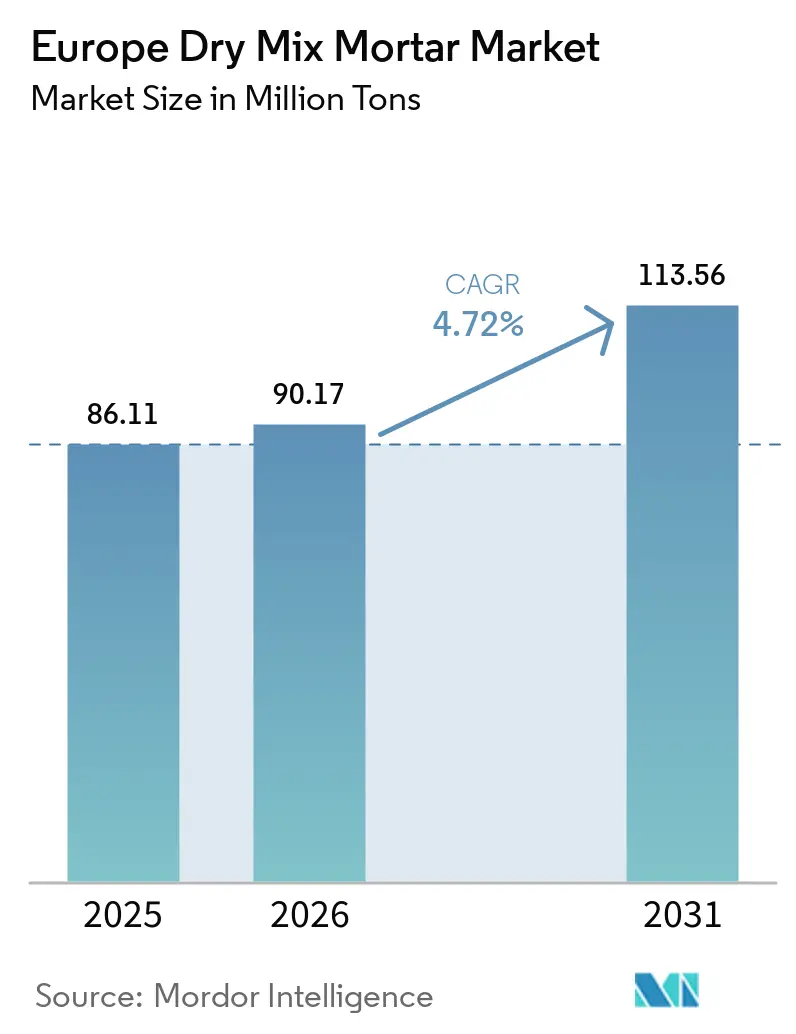

| Base Year Market Size (2025) | 86.11 Million tons |

| Market Volume (2026) | 90.17 Million tons |

| Market Volume (2031) | 113.56 Million tons |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

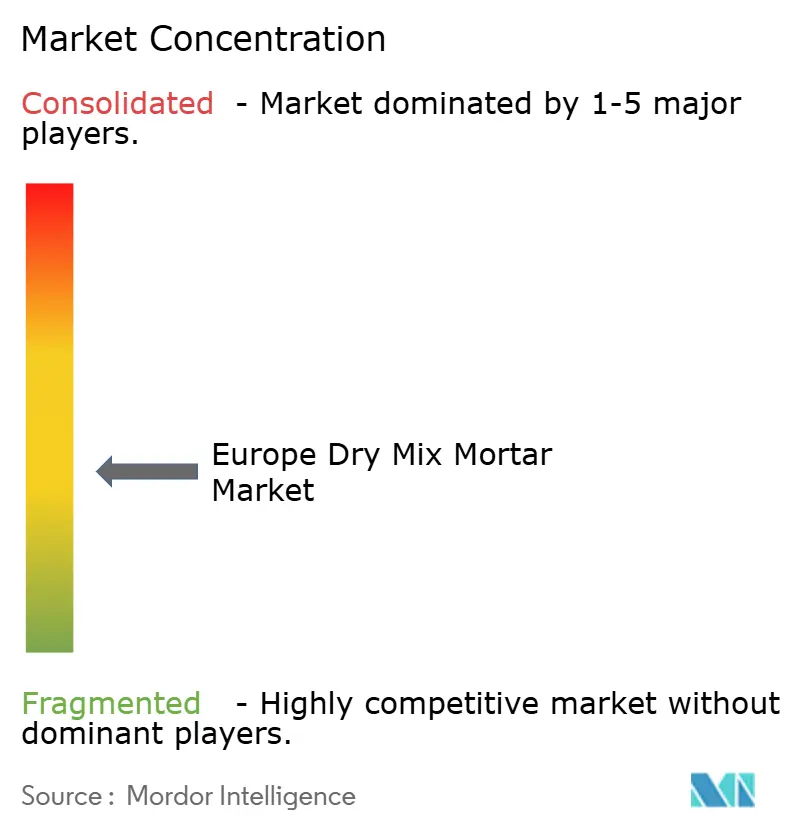

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Dry Mix Mortar Market Analysis by Mordor Intelligence

The Europe Dry Mix Mortar Market size is projected to expand from 86.11 million tons in 2025 and 90.17 million tons in 2026 to 113.56 million tons by 2031, registering a CAGR of 4.72% between 2026 to 2031. The structural demand is shifting toward factory-batched formulations that reduce on-site variability, a change reinforced by the Energy Performance of Buildings Directive, national retrofit subsidies, and labor-saving robotics. Commercial real estate developments such as logistics hubs and data centers favor rapid-set screeds and high-performance adhesives, helping the segment outpace residential renovations. Product innovation now concentrates on low-carbon binders, aerogel-enhanced renders, and encapsulated bacteria repair mortars that align with EU Taxonomy carbon limits. Suppliers able to guarantee lambda values, low-VOC performance, and real-time silo telemetry gain preferred-bid status on tender lists, widening the margin gap with commodity bagged mixes.

Key Report Takeaways

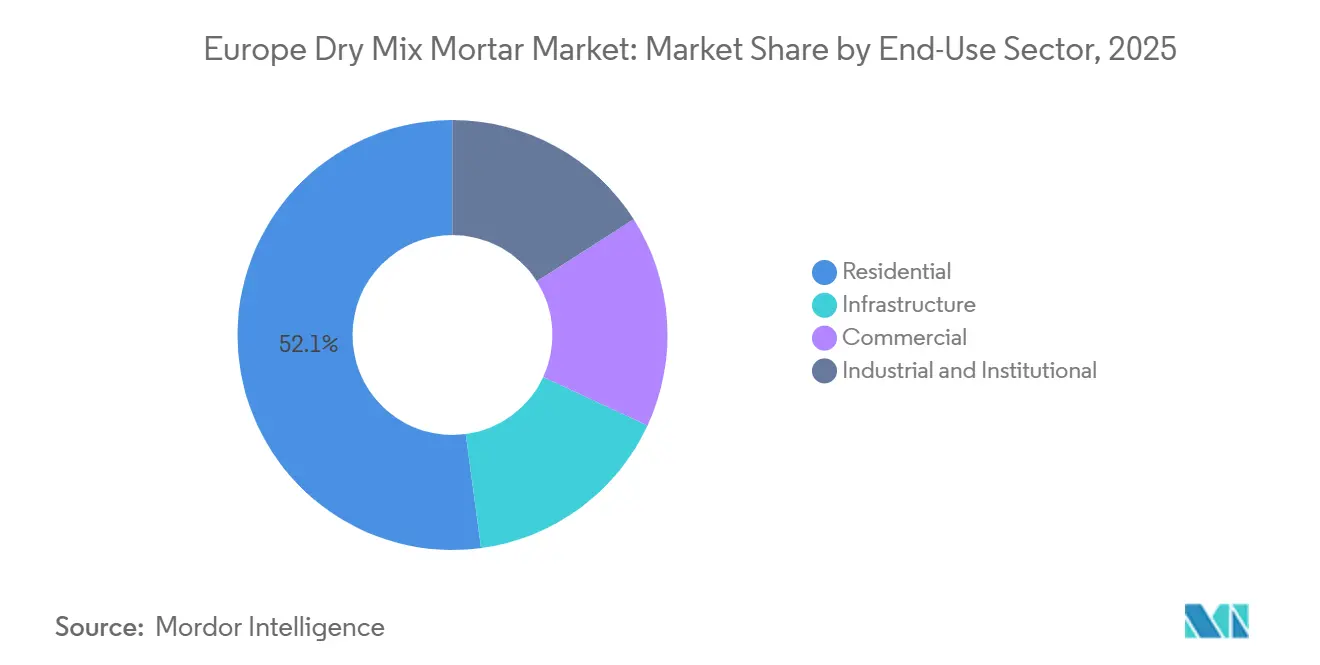

- By end-use sector, residential construction led with 52.11% revenue share in 2025, while commercial applications are projected to expand at a 6.22% CAGR through 2031.

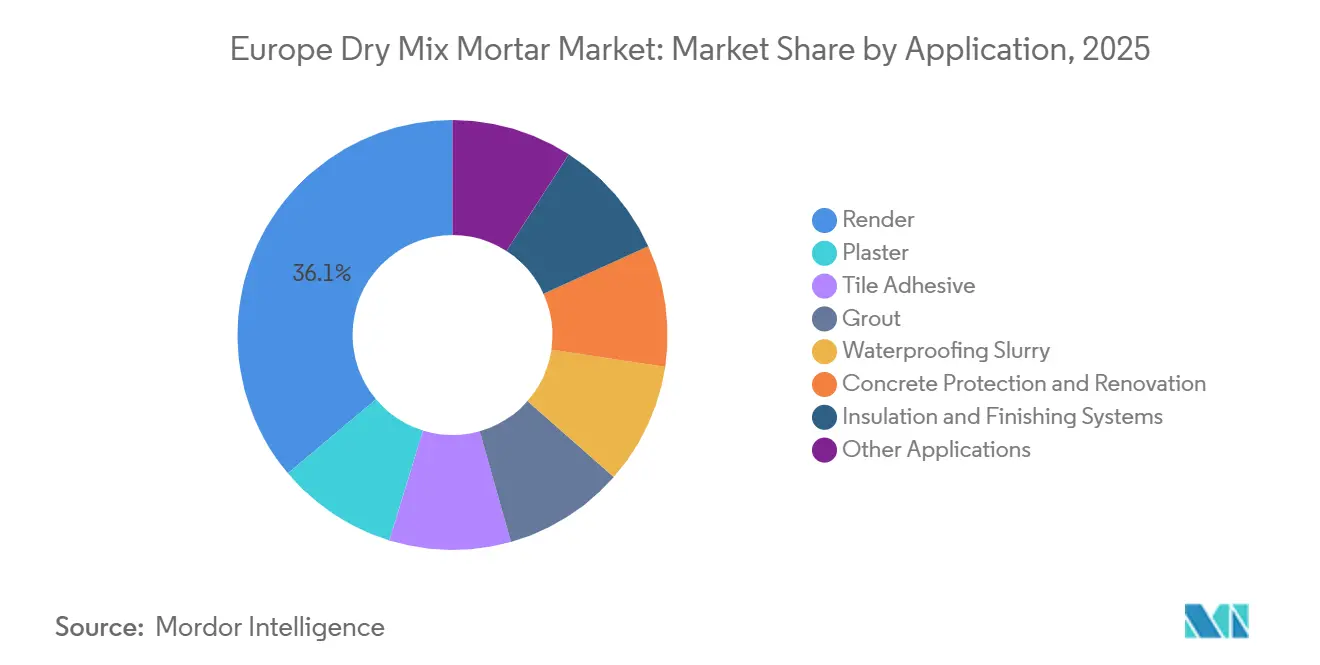

- By application, render systems accounted for 36.12% of the European dry mix mortar market share in 2025, whereas concrete protection and renovation mortars are advancing at a 5.96% CAGR to 2031.

- By country, Germany captured 20.13% of the European dry mix mortar market size in 2025, and Italy is forecast to post the fastest national CAGR at 5.67% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Dry Mix Mortar Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European Union decarbonisation and energy-efficiency directives | +1.2% | EU-27, with highest compliance pressure in Germany, France, Netherlands | Medium term (2-4 years) |

| Growth in prefabricated/off-site construction | +0.9% | Nordic countries, Germany, UK; spillover to Central Europe | Medium term (2-4 years) |

| Post-pandemic green-infrastructure stimulus | +0.7% | EU-wide, concentrated in Southern Europe (Italy, Spain, Portugal) | Short term (≤ 2 years) |

| Automated silo-batching and job-site robotics uptake | +0.6% | Western Europe core markets (Germany, Netherlands, Belgium) | Long term (≥ 4 years) |

| Niche bio-based binder innovations for heritage restoration | +0.3% | Italy, Portugal, Greece, Spain (UNESCO heritage zones) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Decarbonisation and Energy-Efficiency Directives Reshape Formulation Priorities

In February 2026, the revised EPBD set a 2030 deadline for all new constructions to meet zero-emission standards. The mandate also stipulates that a segment of public buildings must undergo annual renovations to achieve at least an EPC-B rating. As a result of these regulations, developers are increasingly adopting dry-mix renders enhanced with aerogel microspheres. These advanced materials can attain lambda values under 0.04 W/mK without necessitating thicker wall assemblies. For 2025, retrofit subsidies are contingent on third-party lambda testing, accelerating the industry's transition from conventional site-batched cement-lime to more dependable factory-certified mortars. Concurrently, research and development investments are shifting focus toward geopolymer and calcined-clay binders. These innovative materials not only comply with the EU Taxonomy’s rigorous carbon dioxide emission limits but also challenge the pace of slower producers in the market.

Prefabricated and Off-Site Construction Drives Demand for Precision-Batched Mortars

In 2025, Sweden and the Netherlands experienced a significant increase in new residential starts, with modular housing accounting for a prominent share. Factory settings, which rely on mortars with specific rheology and extended open times - characteristics inherent to pre-blended products - have begun transitioning to silo-delivered mixes. Following this shift, these factories reported a marked reduction in both mortar waste and defect rates. As a result of these improvements, top-tier contractors across Europe are increasingly favoring suppliers that provide real-time inventory telemetry and just-in-time deliveries.

Green-Infrastructure Stimulus Channels Capital into Envelope Upgrades

In 2025, the European Investment Bank introduced a facility linking loan approvals to a mandate of achieving a minimum of 30 percent savings in primary energy[1]European Investment Bank, “EUR 12 Billion Renovation Wave Financing Launched,” EIB.ORG. This initiative directs projects toward ETICS render assemblies. Italy has extended its Ecobonus deduction until 2026. Concurrently, Spain has allocated a significant budget for social-housing retrofits, emphasizing the preference for render-based ETICS.

Automated Silo-Batching and Robotics Reduce Labor Dependency

By the forecast period 2026–2031, large commercial sites in Germany and the Netherlands have adopted robotic plastering platforms at a notable scale. These platforms have demonstrated a significant ability to reduce labor hours and minimize material waste. Although the adoption process is capital-intensive, the development of leasing models and standardized nozzle interfaces indicates strong potential for long-term growth.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and respirable-silica regulations | -0.8% | EU-27, with strictest enforcement in Germany, France, Nordics | Short term (≤ 2 years) |

| Skilled spray-plaster labour shortage | -0.5% | France, Spain, Italy, Poland (acute in urban centers) | Medium term (2-4 years) |

| Competition from on-site wet-mix mortars in low-cost markets | -0.4% | Eastern Europe (Poland, Romania, Bulgaria), Southern periphery (Greece, Portugal) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

VOC and Respirable-Silica Regulations Elevate Compliance Costs

In 2026, the Industrial Emissions Directive reduced the permissible VOCs in renders to 10 g/L and mandated the monitoring of silica dust[2]European Commission, “Industrial Emissions Directive Amendment 2024,” EUROPA.EU. This reformulation process is increasing production costs, placing pressure on mid-tier suppliers. Additionally, Germany's TRGS 559 regulation is promoting the use of pelletized or pre-wetted formats, which is expected to result in three regional exits in Spain by 2025.

Skilled Labor Shortage Constrains Application Capacity

In late 2025, France faced a significant shortage of certified plasterers, and Spain experienced a surplus of unfilled facade-finishing roles. Meanwhile, Germany witnessed a decline in apprenticeship enrollments. While commercial projects with high profit margins can invest in robotics and premium labor, cost-sensitive residential projects risk delays or a reversion to traditional wet mixes, which could dampen short-term demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-Use Sector: Commercial Outpaces Residential Despite Smaller Base

Residential construction led with a 52.11% share in 2025, while commercial applications are projected to expand at a 6.22% CAGR through 2031. In the same year, logistics facilities experienced significant expansion, particularly in the Netherlands, Germany, and Poland, where rapid-set screeds were the preferred choice. Meanwhile, data centers, healthcare facilities, and institutional projects are opting for antimicrobial grouts and fire-rated renders, which come with a notable price premium. Infrastructure demand remains strong, supported by a substantial finishing budget for the Grand Paris Express station.

Commercial ventures are leading the market, leveraging performance-based procurement and capitalizing on certifications with low-VOC adhesives. Industrial clients demonstrate a clear preference for 24-hour curing screeds, while infrastructure tenders are increasingly specifying self-healing mortars, a trend validated by field tests in the Netherlands. Conversely, residential renovations, influenced by consumer confidence and cost per square meter, are experiencing slower growth.

By Application: Concrete Protection Gains as Render Dominates

By application, render systems accounted for 36.12% of the European dry mix mortar market share in 2025, whereas concrete protection and renovation mortars are advancing at a 5.96% CAGR to 2031. Render systems held a significant share of Europe's dry mix mortar market, highlighting their critical role in ETICS and facade restoration. As numerous European bridges exceeded their intended lifespan, the demand for concrete protection and renovation mortars increased. In March 2025, Sika introduced a fiber-reinforced repair mortar, supported by a long-term guarantee, making it particularly appealing to municipal owners.

Italy's renovation index has driven a higher demand for tile adhesives and grouts. In Germany, new regulations have increased the share of waterproofing slurries, particularly in groundwater-sensitive regions. While plaster mixes face strong competition from gypsum sprays, decorative renders are advancing. A notable example is MAPEI's June 2025 launch of a TiO₂-doped product, emphasizing the industry's shift toward photocatalytic, self-cleaning surfaces.

Geography Analysis

In 2025, bolstered by KfW retrofit subsidies tied to third-party lambda certification, Germany captured a 20.13% share of the regional volume. Italy, expanding at a 5.67% CAGR through 2031, took advantage of prolonged Ecobonus deductions and introduced new hotel rooms in UNESCO Zones, albeit with restrictions on polymer additives. France, holding the position of the second-largest market, allocated resources through MaPrimeRénov but faced labor shortages, leading to delays in some facade projects.

Spain is witnessing a resurgence, registering a boost in housing starts for 2025. The United Kingdom, navigating a landscape with reduced European Union imports, celebrated the opening of a Baumit plant in Birmingham in August 2025. While Russia's construction sector is experiencing growth, it is hindered by sanctions, resulting in a lack of access to advanced polymer additives. Across the rest of Europe - spanning Poland, the Netherlands, Belgium, and the Nordics - demand remains robust, with Poland hosting multiple plants operated by industry leaders Saint-Gobain and Knauf.

Country-specific regulations further complicate the landscape. The Netherlands has mandated the use of recycled or bio-based content in public projects, leading to a surge in demand for slag-cement and mycelium binders. In response to rising labor costs, Sweden and Denmark have adopted robotic plastering, which now accounts for a significant share of their commercial projects. Furthermore, Portugal is directing a major portion of its cohesion fund allocation for social housing retrofits specifically towards ETICS.

Competitive Landscape

The European dry mix mortar market is moderately fragmented. Digital distributors made significant progress, capturing market share in Germany and the Netherlands by consolidating regional formulators on next-day e-commerce platforms. As procurement strategies shift from focusing solely on the lowest price to considering a broader life-cycle cost perspective, producers offering extended warranties and transparent Environmental Product Declarations (EPDs) are experiencing increased demand.

Europe Dry Mix Mortar Industry Leaders

Saint-Gobain

Sika AG

MAPEI S.p.A.

Ardex Group

Holcim

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Hoffmann Green Cement Technologies, an industrial company dedicated to reducing carbon emissions in the construction industry, specialized in the design and marketing of innovative, cold-produced, clinker-free cements. The company announced the signing of an exclusive preliminary agreement with Bruil, a prominent company in the Dutch ready-mix concrete market, to establish a licensing arrangement in the Netherlands.

- June 2025: Heidelberg Materials inaugurated the world’s first industrial-scale carbon-capture facility at Brevik, Norway, enabling net-zero evoZero cement products for European customers.

Europe Dry Mix Mortar Market Report Scope

Dry mix mortar, a pre-mixed blend of cement, graded sand, and specialized chemical additives, is produced in factories and supplied in powder form. On-site, it only needs water for immediate use in masonry, plastering, and tile fixing. This material guarantees consistent, high-quality construction, enhances efficiency, and minimizes waste and labor.

The dry mix mortar market is segmented by end-use sector, application, and country. By end-use sector, the market is segmented into commercial, industrial and institutional, infrastructure, and residential. By application, the market is segmented into plaster, render, tile adhesive, grout, waterproofing slurry, concrete protection and renovation, insulation and finishing systems, and other applications. The report also covers the market size and forecasts in 6 countries across the European region. For each segment, the market sizing and forecasts have been done based on volume (Tons).

By End-Use Sector

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

By Application

| Plaster |

| Render |

| Tile Adhesive |

| Grout |

| Waterproofing Slurry |

| Concrete Protection and Renovation |

| Insulation and Finishing Systems |

| Other Applications |

By Country

| France |

| Germany |

| Italy |

| Russia |

| Spain |

| United Kingdom |

| Rest of Europe |

| By End-Use Sector | Commercial |

| Industrial and Institutional | |

| Infrastructure | |

| Residential | |

| By Application | Plaster |

| Render | |

| Tile Adhesive | |

| Grout | |

| Waterproofing Slurry | |

| Concrete Protection and Renovation | |

| Insulation and Finishing Systems | |

| Other Applications | |

| By Country | France |

| Germany | |

| Italy | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- END-USE SECTOR - Dry mix mortar consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, consumption of dry mix mortar products for plaster, render, tile adhesive, grouts, waterproofing slurries, concrete protection and renovation, insulated and finishing systems along with other applications are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms