Concrete Bonding Agent Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

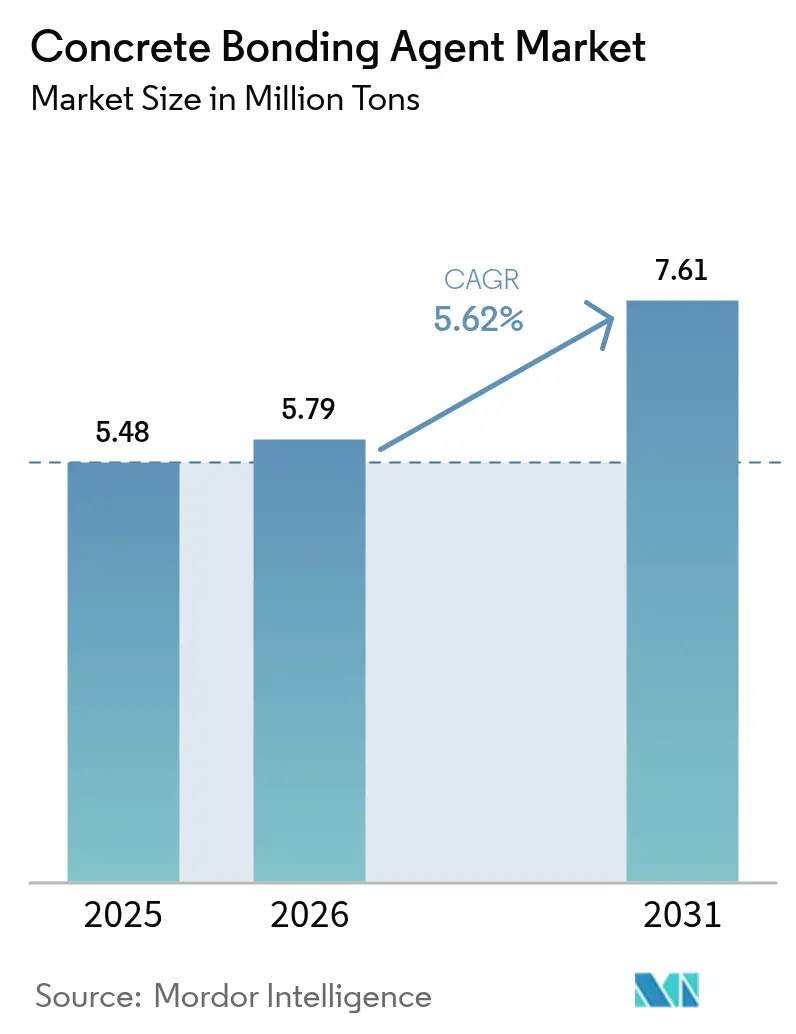

| Market Volume (2026) | 5.79 Million tons |

| Market Volume (2031) | 7.61 Million tons |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

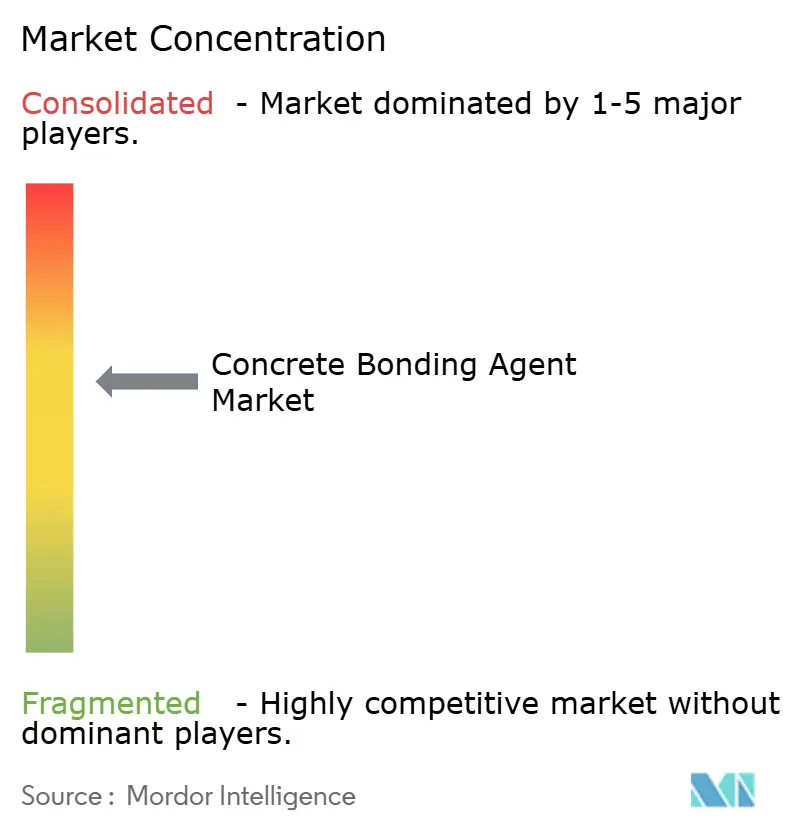

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Concrete Bonding Agent Market Analysis by Mordor Intelligence

The Concrete Bonding Agent Market size is expected to grow from 5.48 Million tons in 2025 to 5.79 Million tons in 2026 and is forecast to reach 7.61 Million tons by 2031 at 5.62% CAGR over 2026-2031. Robust demand comes from governments and private owners that now favor rehabilitation over demolition because life-cycle studies show a 15–20% cost advantage when sound structures are upgraded instead of replaced. Added momentum stems from stricter low-Volatile Organic Compound (VOC) rules, nano-silica research breakthroughs that boost flexural adhesion by 16.7%, and a widening pool of two-component repair mortars able to reach structural strength within an hour. Asia-Pacific’s 46.91% 2024 volume share highlights how rapid 1980–2000 buildouts are now cycling into repair mode, backed by India’s USD 134 billion infrastructure allocation for 2024/25 and China’s pivot toward green urban renewal. The consolidation wave led by Saint-Gobain and Sika AG shows that scale is essential to fund research and development (R&D), comply with multi-jurisdictional regulations, and secure raw materials such as styrene-butadiene latex whose price reached USD 1,654 per ton in 2024.

Key Report Takeaways

- By bonding agent type, cementitious latex solutions held 53.62% of the Concrete Bonding Agents market share in 2025, while the same segment is forecast to expand at a 6.39% CAGR through 2031.

- By technology, one-component systems captured 64.05% of the Concrete Bonding Agents market size in 2025, whereas two-component systems are projected to grow at a 6.18% CAGR between 2026 and 2031.

- By application, infrastructure repairing accounted for 37.02% of the 2025 volume; waterproofing and other niche uses are advancing at a 6.27% CAGR to 2031.

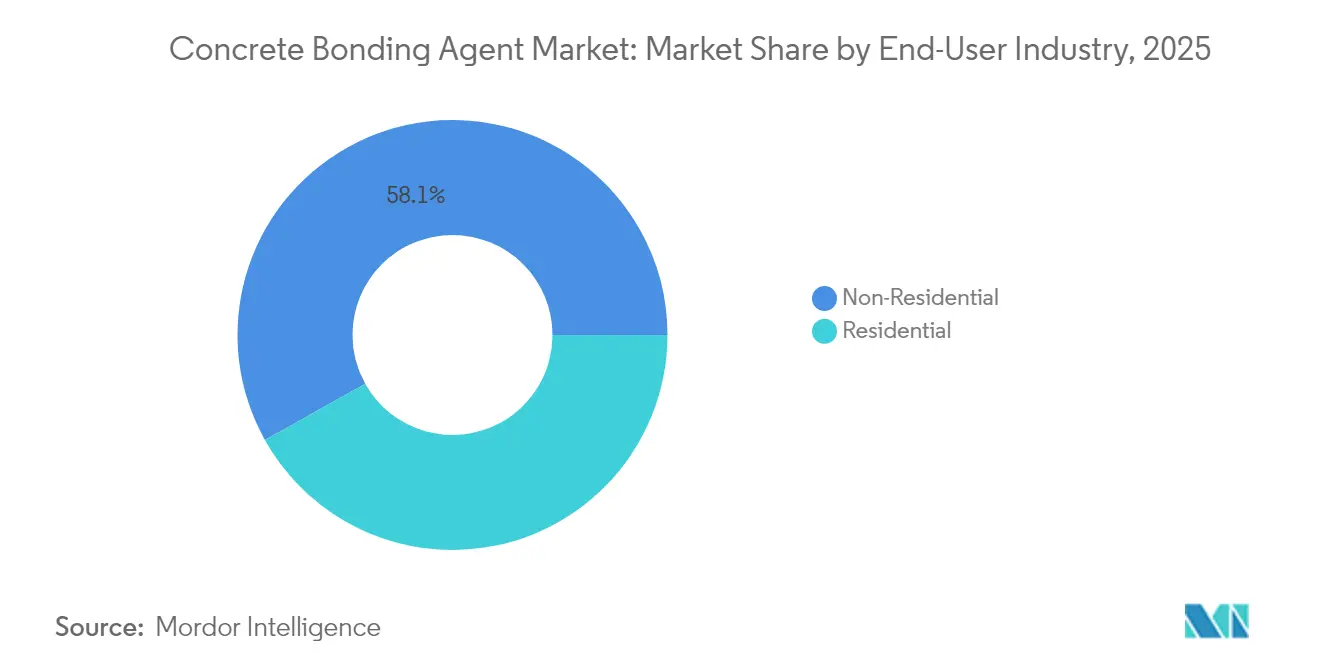

- By end-user industry, non-residential construction led with a 58.12% share in 2025; the same segment is expected to post a 5.97% CAGR over the forecast window.

- By geography, Asia-Pacific dominated with a 46.55% volume share in 2025, and the region is on track for a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Concrete Bonding Agent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Concrete Repair & Rehabilitation Projects | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid Urban Infra-upgrading Mandates | +1.2% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Compatibility With Portland & Blended Cements | +0.9% | Global | Short term (≤ 2 years) |

| Proliferation of Ready-mix Repair Mortars | +0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Increasing Demand for Nano-silica-enhanced Bonding Chemistries | +0.6% | APAC core, early adoption in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Concrete Repair & Rehabilitation Projects

Municipal agencies that built roads, bridges, and flood-control dams in the 1960s and 1970s now face end-of-life deterioration, so they prioritize rehabilitation that can extend service lives by 20–30 years [1]BASF Construction Solutions, “Latex-Modified Concrete Overlays: 50-Year Field Data,” basf.com. The Third Avenue Bridge case in New York proved that targeted overlays using latex-modified concrete can add five decades of durability at one-fifth the replacement cost. Agencies adopt asset-management protocols that quantify whole-life cost, and those models consistently rank advanced bonding agents ahead of basic patching mortars because adhesion failure leads to rework. Insurance underwriters also weigh in; many now require documented interface testing before they approve coverage for capital-intensive bridges and tunnels. As owners embed such specifications, the concrete bonding agents market keeps widening its addressable base across both public and private portfolios.

Rapid Urban Infra-upgrading Mandates

Cities from Mumbai to Manila are retrofitting transport corridors to lift resilience scores and reduce congestion, an effort funded through public–private partnerships that stipulate strict uptime metrics. Because rehab work occurs in live traffic zones, contractors prefer bonding agents that cure fast, adhere to damp substrates, and remain compatible with Portland cement so that standard crews can handle installation. China’s 2025 policy documents pivot away from adding greenfield highways toward reinforcing existing structures against seismic and flood risks. This reshaped demand pattern favors polymer-rich formulations that boost flexural strength without altering concrete’s thermal expansion profile. Suppliers report double-digit sales growth in spray-applied acrylics designed for narrow nighttime maintenance windows on subways and elevated rail viaducts.

Compatibility With Portland & Blended Cements

Field engineers still default to Type I/II cement, so any bonding agent that forces exotic batching seldom gets specified. Laboratory tests on epoxy-reinforced mortars showed 16.7% higher flexural bonding and 29.8% better interface shear while using standard cementitious blends. Fly-ash and slag additions complicate hydration kinetics, yet current latex and epoxy blends are engineered to tolerate those supplementary cementitious materials. Ready-mix suppliers therefore market all-purpose bonding primers that suit both traditional and eco-optimized mixes. Because these products run through the same trucks and sprayers used for conventional jobs, site crews can adopt them without extra capital spend, accelerating market penetration.

Proliferation of Ready-Mix Repair Mortars

Although generic ready-mixed concrete deliveries in Great Britain fell 17.4% in 2024, specialized factory-blended repair mortars gained share because owners want certified mix designs that minimize on-site variability. MAPEI S.p.A. invested in Denver, Houston, and Chicago plants to localize logistics and deliver next-day shipments of classed mortars that integrate bonding polymers. Plant batch control ensures the target polymer-cement ratio, which is critical for achieving tensile adhesion above 2 MPa on diamond-ground substrates. Contractors value this consistency, especially where warranties hinge on adhesion pull-off tests. The value proposition outweighs the 8–10% price premium versus site-blended mixes, sustaining a robust growth channel for the concrete bonding agents market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility of Epoxy & Latex Feedstocks | -1.4% | Global, acute in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Low Contractor Awareness in Emerging Markets | -0.8% | APAC emerging, MEA, Latin America | Medium term (2-4 years) |

| Carbon-footprint Scrutiny of Polymer Dispersions | -0.6% | EU, North America, expanding to APAC developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Epoxy & Latex Feedstocks

Styrene-butadiene rubber and bisphenol-A-based epoxy rely on petroleum derivatives whose prices swing with refinery turnarounds and geopolitical disruptions. During 2024, high-performance latex reached USD 1,654 per ton, eroding contractor margins in low-bid environments. Emerging markets often delay bridge deck overlays when feedstock spikes push procurement beyond budget ceilings. To hedge risk, formulators explore bio-based epoxies derived from cashew nutshell liquid, yet scale remains nascent and costs vary with crop yields. Forward-buy contracts offer partial relief but require healthy balance sheets that smaller distributors lack. The volatility therefore curbs near-term volume growth in price-sensitive segments of the concrete bonding agents market.

Low Contractor Awareness in Emerging Markets

In parts of Southeast Asia and Sub-Saharan Africa, many contractors still equate bonding agents with simple PVA glue, overlooking performance nuances that dictate long-term adhesion. Magna Prime in the Philippines holds monthly workshops to close that knowledge gap, yet attendance remains skewed to tier-one builders [2]Magna Prime Corporation, “Technical Training Programs for Polymer Admixtures,” magnaprime.com. Limited awareness translates into low tender uptake for high-grade agents even when owners specify them, because bidders assume higher material costs will make them uncompetitive. Regional distributors often lack technical staff to demonstrate pull-off tests, so they revert to commodity cementitious grouts. Unless training scales, adoption rates for advanced systems will lag, limiting growth potential especially for premium two-component epoxies within the concrete bonding agents market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bonding Agent Type: Latex Formulations Drive Market Evolution

Latex-modified, cement-compatible agents accounted for 53.62% of 2025 volume, the largest slice within the Concrete Bonding Agents market share. The same cohort is on a 6.39% CAGR path, rendering it both the dominant and fastest-growing class. This rare dual positioning reflects latex chemistry that marries workability with mechanical uplift: scanning electron microscopy reveals three-dimensional polymer films that bridge voids and blunt micro-crack propagation. Field data from the Virginia Department of Transportation show 22–26 year service lives for latex overlays versus 15–19 years for unmodified systems. Epoxy-based products keep a firm presence in chemically aggressive or structurally critical environments such as wastewater headworks and offshore platforms.

Performance considerations steer procurement. Latex agents yield higher elongation, easing stress concentrations caused by thermal cycling on wide deck plates, whereas epoxies excel in compressive zones that demand extreme shear transfer. VOC regulation trends favor water-borne latex, yet next-generation low-odor epoxies aim to re-balance the equation. Suppliers increasingly bundle both chemistries in modular systems, letting contractors pair a latex primer with an epoxy topcoat to optimize adhesion and chemical resistance. This hybrid approach expands the concrete bonding agents market because owners get specification flexibility without adding stock keeping unit (SKU) complexity.

By Technology: Single-Component Systems Dominate Through Simplicity

One-component products held 64.05% of 2025 shipments and remain the mainstay for everyday patching and floor screeding. These pre-mixed liquids or powders need only water or mechanical stirring, limiting job-site errors. Two-component kits, although just 35.95% by volume, show a brisk 6.18% CAGR because they unlock higher bond strengths above 3 MPa and resist cyclic loading on heavily trafficked viaducts. The differential speaks to user segmentation: smaller contractors gravitate to single-bag convenience, while infrastructure specialists budget extra labor time for mixing precision.

Innovation is trimming the hassle gap. Foil-pack cartridges now keep resin and hardener separate until on-site extrusion into static mixers, shaving set-up time by 30% while cutting waste. Rapid-cure two-component epoxies can hit traffic-ready strength in one hour, a boon for overnight runway slab repairs at busy airports. Meanwhile, sensor-enabled packaging that changes color when mixing is incomplete may soon migrate from premium to mid-tier price points. As such features spread, two-component adoption could accelerate, further expanding the concrete bonding agents market size in value terms even if unit volumes stay modest.

By Application: Infrastructure Repair Drives Market Fundamentals

Repairing applications commanded 37.02% of 2025 demand because governments funnel fiscal resources into asset preservation. The Commodore Barry Bridge upgrade used ultra-high-performance concrete overlaid with polymer-rich bonding layers to slash future maintenance by 40%. That case illustrates how bonding agents transition from ancillary add-on to mission-critical element in capital planning. Flooring stays a mature but resilient niche, sustained by pharma plants and food processing lines that need chemical-resistant toppings every 7–10 years. Decorative overlays claim smaller tonnage but higher margins, pushing suppliers to develop color-stable polymers that withstand ultraviolet (UV) at theme parks and retail podium decks.

Emerging categories, notably moisture-vapor emission control under resilient flooring, grow fastest at 6.27% CAGR because building codes now require sub-slab water mitigation. Combined with tight project schedules, that code evolution forces adoption of fast-gel primers that lock down residual moisture within four hours. Market education continues to stress that failure to use bonding primers in wet slabs can void floor covering warranties costing multiples of the primer’s price. Such economics underpin the long-run expansion of the concrete bonding agents market.

By End-User Industry: Non-Residential Sector Leads Through Complexity

Non-residential end-user industry had a market volume share of 58.12% in 2025 and is expected to grow with a 5.97% CAGR through 2031, fueled by data centers, hospitals, and transit hubs that cannot afford downtime. High-rise developers specify polymer-modified repair mortars for annex podiums because façade access stages are costly to erect again if early spalls appear. Saint-Gobain targeted this opportunity by buying Fosroc, citing India’s surge in industrial parks and Middle East mega-projects as growth vectors. Residential uptake remains steadier as homeowner awareness diffuses, yet product simplicity rules: one-component acrylic bonding agents dominate do-it-yourself retail shelves.

Green-building programs such as Leadership in Energy and Environmental Design (LEED) v5 drive change in both segments. Credits for material transparency elevate low-VOC latex while penalizing solvent-rich epoxies in enclosed areas. Manufacturers thus tweak formulations, swapping non-ylide accelerators for benzyl alcohol and adding bio-based defoamers. Because these tweaks do not alter installation protocols, contractors accept them readily, keeping sales momentum intact across the concrete bonding agents industry.

Geography Analysis

Asia-Pacific anchored 46.55% of global market volume share in 2025 and is pacing toward a 6.12% CAGR through 2031, magnifying the Concrete Bonding Agents market footprint across China, India, Indonesia, and the Philippines. China’s infrastructure outlays, while moderating, now emphasize seismic retrofits and carbon reduction, which require high-performance bonding agents to integrate recycled aggregates without compromising adhesion. India’s USD 134 billion 2024/25 allocation accelerates projects under the Gati Shakti corridor, compelling contractors to adopt rapid-cure primers that can turn lanes back to traffic overnight.

North America remains a technology testbed, buoyed by the USD 1.2 trillion Infrastructure Investment and Jobs Act that channels funds into bridge rehabilitation, dam spillway enlargement, and port berth reinforcement. California’s Air Resources Board tightened VOC caps to 30 g/L for architectural adhesives in 2024, nudging suppliers toward water-borne dispersion and higher-solids epoxy blends. Progressive Epoxy Polymers introduced a solvent-free deck overlay that cures at 5°C, aiming at winter-maintenance windows in the Upper Midwest.

Europe commands a sophisticated user base demanding tight emission profiles and proof-tested structural performance. The 17.4% drop in Great Britain’s generic ready-mix deliveries masks a switch toward bespoke repair mortars with factory-certified binder-polymer ratios. Saint-Gobain-Fosroc now controls production nodes in the United Kingdom and United Arab Emirates, letting it funnel European know-how into Gulf petrochemical refurbishments that require fire-retardant epoxy primers. Southern Europe’s seismic retrofit programs invite viscous thixotropic agents that cling to vertical columns without sag, an area where Italian labs drive formulation advances. South America and the Middle East & Africa trail in aggregate volume but post double-digit growth pockets. Brazil’s port concession upgrades deploy polymer-rich grouts under crane rails. Such region-specific technical needs broaden adoption corridors for the Concrete Bonding Agents market.

Competitive Landscape

The Concrete Bonding Agents market is moderately consolidated with the presence the major players including Sika AG, Henkel AG & Co. KGaA, MAPEI S.p.A., Saint-Gobain, and RPM International Inc. These companies deploy mergers and acquisitions (M&As) to secure feedstock, R&D depth, and multi-region regulatory compliance. Saint-Gobain’s purchase of Fosroc in February 2025 fused complementary product lines, lifting the combined portfolio to about USD 6.8 billion in construction chemicals revenue. Sika AG, meanwhile, deepened its infrastructure specialty by buying Kwik Bond Polymers, inheriting epoxy overlays approved by most United States states. Competitive playbooks emphasize vertical integration, digital job-site support, and sustainability labeling.

Concrete Bonding Agent Industry Leaders

Sika AG

RPM International Inc.

Henkel AG & Co. KGaA

MAPEI S.p.A.

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saint-Gobain completed the acquisition of Fosroc, Inc., a Dubai-based construction chemicals company and a prominent supplier of concrete bonding agents. The acquisition enhances Saint-Gobain's presence in high-growth markets like India, the Middle East, and Asia-Pacific.

- June 2024: White Cap Supply Holdings, LLC announced the acquisition of Dayton Superior Corporation, a concrete bonding agent manufacturer. The acquisition expands White Cap's one-stop shop services through its extensive distribution network.

Global Concrete Bonding Agent Market Report Scope

Bonding agents are natural, compounded, or synthetic materials used to enhance the joining of individual members of a structure without employing mechanical fasteners. Concrete bonding agents are often used in repair applications such as bonding fresh concrete, sprayed concrete, or sand/cement repair mortar to hardened concrete.

The concrete bonding agent market is segmented by bonding agent type, application, end-user industry, and geography. By bonding agent type, the market is segmented into cementitious latex-based and epoxy-based. By application, the market is segmented into repairing, flooring, decorative, and other applications (waterproofing, etc.). By end-user industry, the market is segmented into residential and non-residential. The report also covers the market size and forecasts for the concrete bonding agent market in 15 countries across major regions.

For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Cementitious Latex-based |

| Epoxy-based |

| One-component |

| Two-component Systems |

| Repairing |

| Flooring |

| Decorative |

| Other Applications (Waterproofing & Damp-proofing, etc.) |

| Residential |

| Non-Residential |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Bonding Agent Type | Cementitious Latex-based | |

| Epoxy-based | ||

| By Technology | One-component | |

| Two-component Systems | ||

| By Application | Repairing | |

| Flooring | ||

| Decorative | ||

| Other Applications (Waterproofing & Damp-proofing, etc.) | ||

| By End-User Industry | Residential | |

| Non-Residential | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Concrete Bonding Agent Market size?

The Concrete Bonding Agent Market size is 5.79 Million tons in 2026 and is projected to reach 7.61 Million tons by 2031, reflecting a 5.62% CAGR.

Which region leads demand for concrete bonding agents?

Asia-Pacific holds 46.55% of global volume in 2025 and is also the fastest-growing region with a 6.12% CAGR through 2031.

How does feedstock price volatility impact the market?

Epoxy and latex price swings, such as latex at USD 1,654 per ton in 2024 compress contractor margins and can delay projects, subtracting an estimated 1.4 percentage points from forecast CAGR.

What role does regulation play in product development?

VOC caps, especially in California, push suppliers toward waterborne latex and low-solvent epoxies, accelerating R&D investment in greener chemistries that still meet demanding adhesion criteria.

How consolidated is the supplier landscape?

After recent acquisitions by Saint-Gobain and Sika, the top five firms control just under 60% of shipments, indicating moderate consolidation but leaving room for regional specialists to thrive.

Page last updated on: