GCC Concrete Blocks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

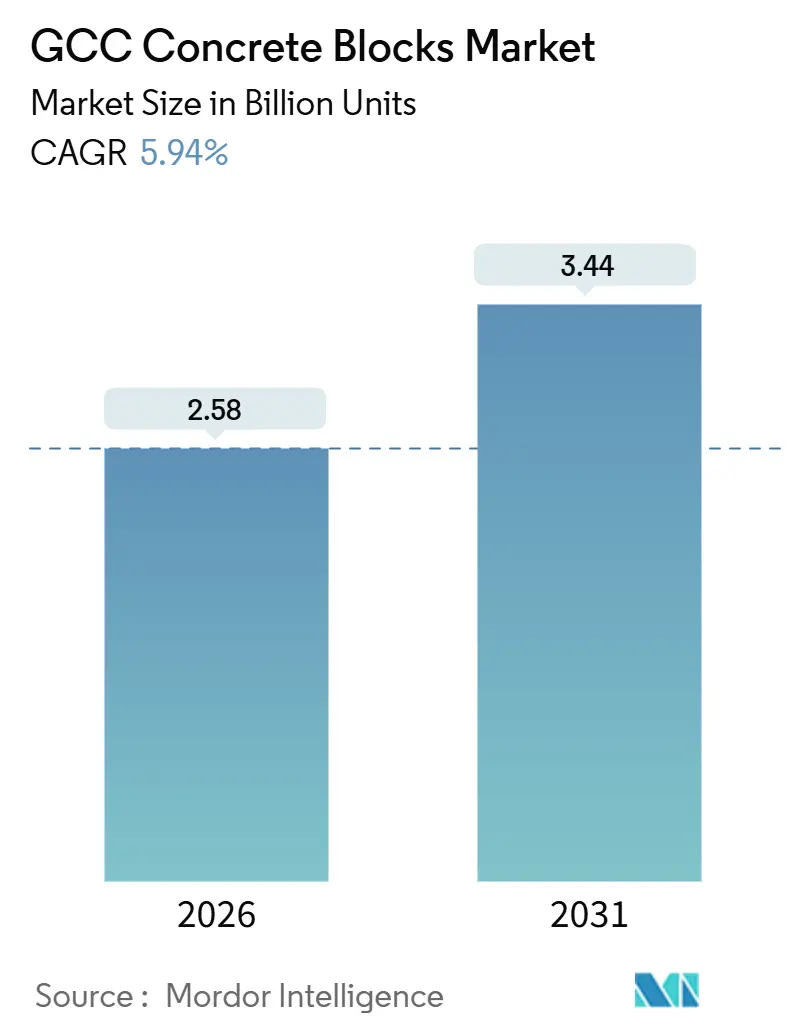

| Market Volume (2026) | 2.58 Billion units |

| Market Volume (2031) | 3.44 Billion units |

| Growth Rate (2026 - 2031) | 5.94% CAGR |

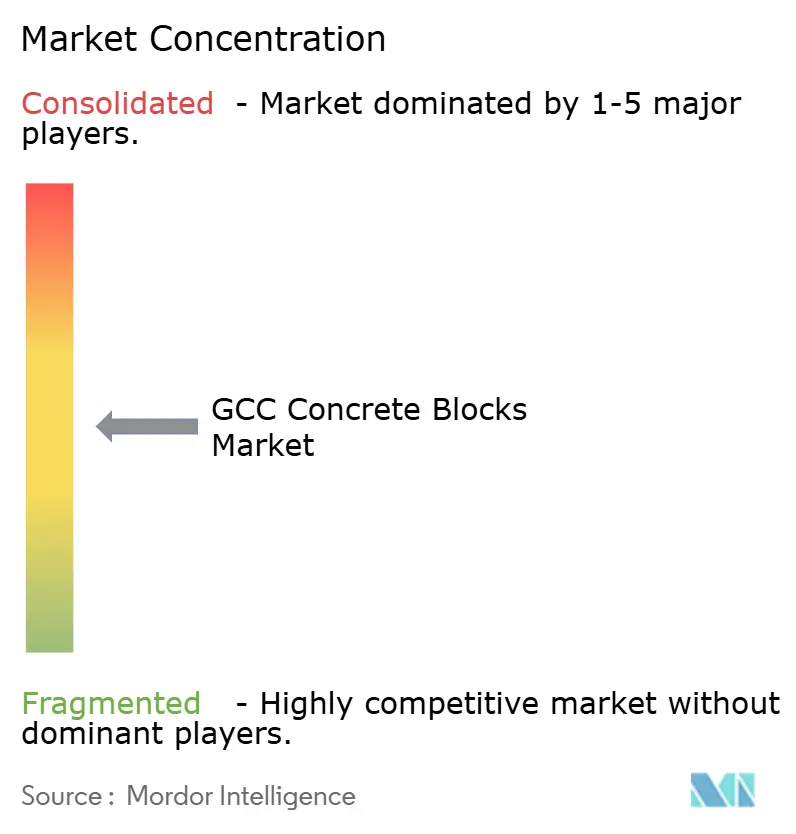

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Concrete Blocks Market Analysis by Mordor Intelligence

The GCC Concrete Blocks Market size is estimated at 2.58 billion units in 2026, and is expected to reach 3.44 billion units by 2031, at a CAGR of 5.94% during the forecast period (2026-2031). This expansion mirrors the region’s commitment to Vision-linked megaprojects, rapid urban migration, and stricter sustainability codes that elevate demand for energy-efficient masonry solutions. Saudi Arabia’s USD 181.5 billion near-term infrastructure outlay, the UAE’s post-Expo airport and logistics expansions, and Qatar’s LNG-driven civil works together anchor a steady order pipeline for hollow and solid units. Simultaneously, government mandates that cap wall U-values and require carbon disclosure are steering producers toward lightweight, recycled-aggregate, and thermally insulated blocks, even as cement price volatility trims margins. Competitive pressures from autoclaved aerated concrete (AAC), light-steel framing, and early 3D-printing pilots are forcing incumbents to modernize curing systems, automate batching, and secure alternate raw materials to protect share in the GCC concrete blocks market.

Key Report Takeaways

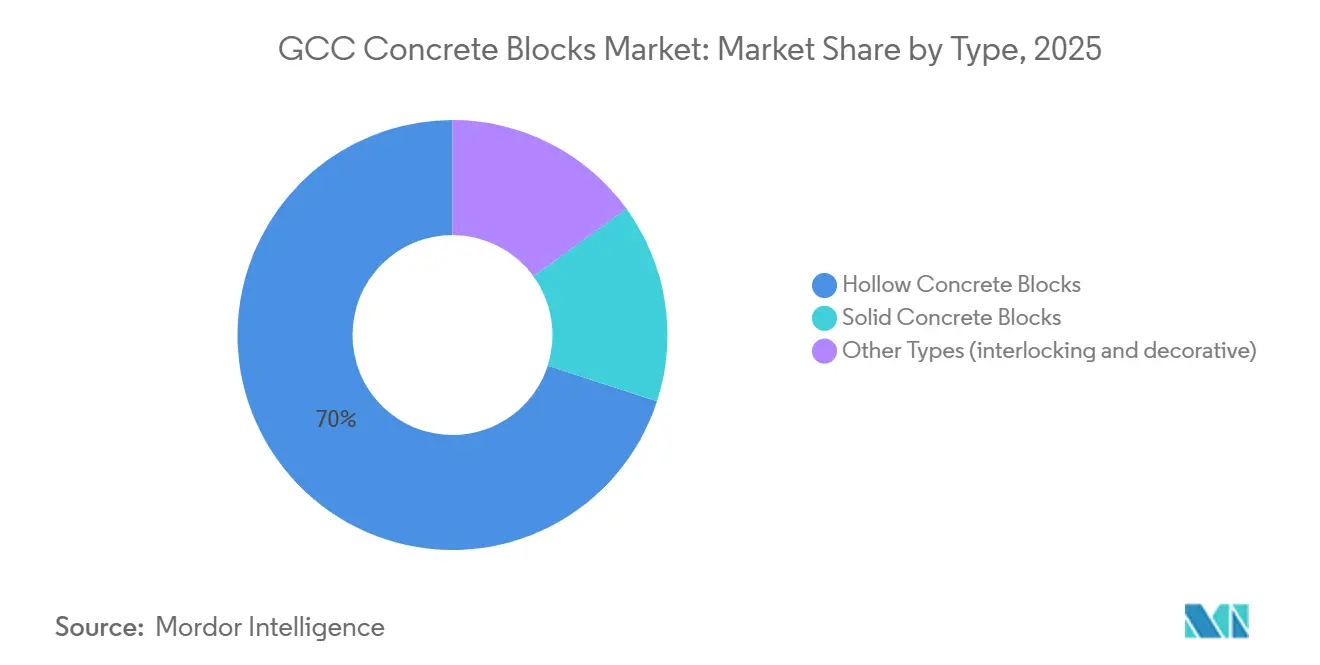

- By type, hollow concrete blocks commanded 70.01% GCC concrete blocks market share in 2025 and are forecast to post a 6.31% CAGR through 2031.

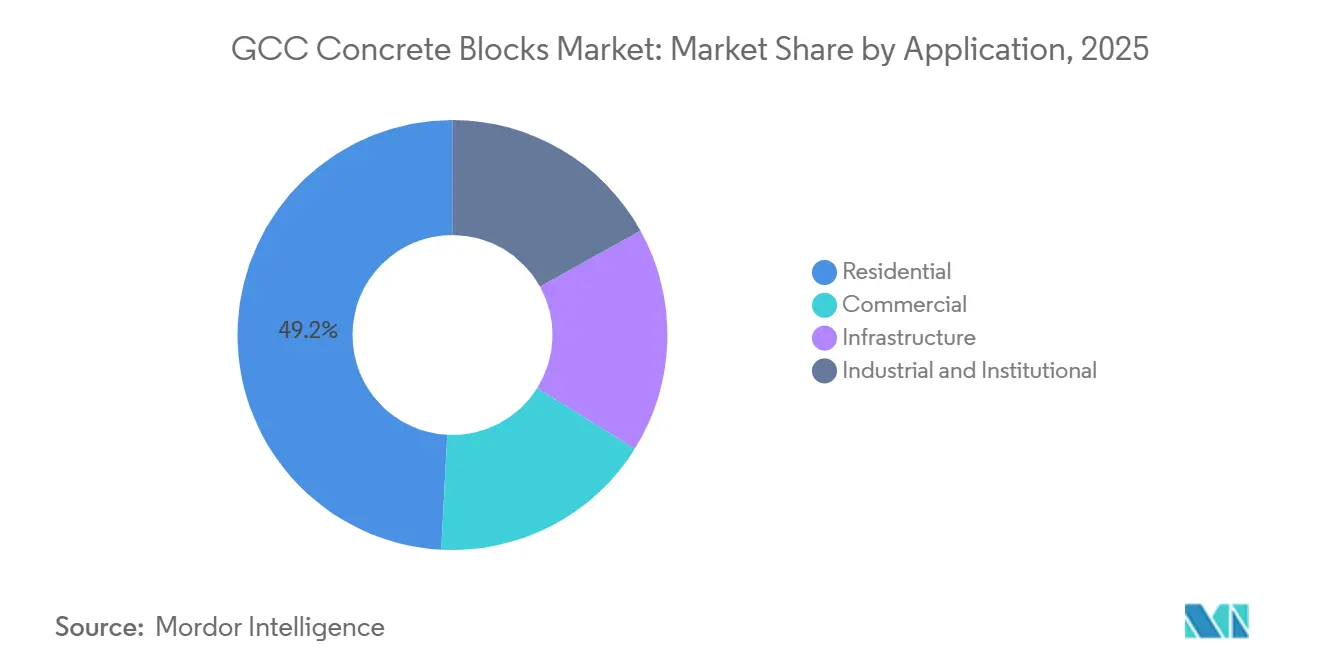

- By application, the residential segment accounted for 49.17% of the GCC concrete blocks market size in 2025 and is projected to expand at a 6.39% CAGR over the same period.

- By geography, Saudi Arabia dominated with 71.21% GCC concrete blocks market share in 2025, while it is also slated to register a 6.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Concrete Blocks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision-linked infrastructure megaproject pipeline | +1.5% | Saudi Arabia, UAE, Qatar (core); spillover to Oman | Long term (≥ 4 years) |

| Housing demand from rapid urbanization and population growth | +1.3% | Saudi Arabia, UAE (primary); Qatar, Oman (secondary) | Medium term (2-4 years) |

| Shift toward prefabricated and modular construction | +0.9% | UAE, Saudi Arabia (early adopters); Qatar, Oman (followers) | Medium term (2-4 years) |

| Sustainability push for energy-efficient green blocks | +0.8% | UAE (Estidama), Saudi Arabia (SGBC), Qatar (GSAS) | Long term (≥ 4 years) |

| Early adoption of 3D-printed concrete elements | +0.4% | UAE (Dubai), Qatar (pilot projects), Saudi Arabia (NEOM) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision-Linked Infrastructure Megaproject Pipeline

Vision-aligned public spending underpins a durable demand floor in the GCC concrete blocks market. Saudi Arabia earmarked USD 181.5 billion for delivery by 2028, with NEOM’s The Line alone expected to absorb 500 million block equivalents. Qiddiya and Red Sea tourism zones require decorative and interlocking variants that satisfy both aesthetics and durability standards. In the UAE, the Al Maktoum International Airport expansion and Dubai South logistics district continue to draw hollow unit volumes even as residential activity normalizes. Qatar’s North Field East LNG build-out uses non-structural hollow blocks for worker accommodation, peaking near 15 million units annually through 2027[1]QatarEnergy, “North Field Expansion Progress Report 2025,” qatarenergy.com. Oman’s USD 100 billion Vision 2040 project list favors precast and modular solutions that compress timelines on transport corridors and industrial zones.

Housing Demand from Rapid Urbanization and Population Growth

Regional population expands 1.8% each year, keeping residential demand atop the GCC concrete blocks market hierarchy. Saudi Arabia’s Sakani program handed over 220,000 homes in 2025, pulling an estimated 450 million hollow and solid units. The UAE approved 85,000 new dwellings in 2025 as expatriate inflows lifted Dubai and Abu Dhabi occupancy rates, with lightweight blocks preferred on reclaimed coastal plots where soil bearing capacities are low. Qatar targets 10,000 homes per year through 2030 under its National Housing Program, specifying thermal-insulated masonry that satisfies its GSAS energy benchmarks. Oman’s social housing scheme seeks 25,000 units by 2028 and mandates hollow units that comply with updated seismic codes.

Shift Toward Prefabricated and Modular Construction

Labor scarcity and wage inflation—construction wages climbed 12% in 2025—are accelerating modular adoption in the GCC concrete blocks market. The UAE’s Consent Group used prefab block panels to deliver a 500-unit Sharjah project six months ahead of traditional schedules. Saudi Arabia approved modular systems for 15% of Sakani units in 2025, citing improved quality control and cost certainty. EMSTEEL logged a 25% jump in prefab orders, while Qatar’s Barwa Real Estate trimmed material waste by 18% on LNG worker housing through precision panel manufacturing.

Sustainability Push for Energy-Efficient Green Blocks

Abu Dhabi’s Estidama and the Saudi Green Building Code cap exterior wall U-values at 0.57 W/m²K, steering demand toward hollow units with integrated insulation[2]Department of Municipalities and Transport, “Estidama Pearl Rating System v2,” dmt.gov.ae. ACICO’s 30% recycled-aggregate hollow block, launched in 2025, registers thermal conductivity of 0.45 W/m²K and meets LEED Gold and Estidama 2 Pearl thresholds. The UAE’s carbon labeling rule obliges disclosure of embodied CO₂ per cubic meter, encouraging clinker replacement at Saudi Readymix plants to cut emissions by 20%. Qatar’s 2025 code revision mandates 15% post-consumer recycled input in non-structural units, accelerating the adoption of reclaimed aggregate blends. ISO 16757 compliance is now a prerequisite for public tenders, widening the moat for certified producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cement and aggregate price volatility | -0.6% | Saudi Arabia, UAE, Qatar (high exposure); Oman (moderate) | Short term (≤ 2 years) |

| Competition from AAC and light-steel framing systems | -0.5% | UAE, Saudi Arabia (high-rise residential and commercial) | Medium term (2-4 years) |

| Water-scarcity constraints on block production | -0.4% | UAE, Qatar (acute); Saudi Arabia, Oman (emerging) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cement and Aggregate Price Volatility

Cement traded between SAR 200 and SAR 250 per tonne in 2025, shaving 8-12% off producer margins in the GCC concrete blocks market. Heidelberg Materials noted a 15% hike in clinker costs as natural gas and carbon levies rose in the UAE, prompting investment in waste-heat recovery. Aggregate scarcity in coastal sites forces reliance on recycled concrete that carries a 20-30% premium yet slices embodied carbon by 25%. Qatar’s limestone imports bear freight volatility; shipping rates advanced 18% in 2025 amid Red Sea route disruptions. Oman tightened domestic supply via a 5% export duty that further inflated input costs for regional buyers.

Competition from AAC and Light-Steel Framing Systems

AAC blocks marketed by ACICO and Xella weigh 20% less than hollow units, trimming steel tonnage and foundation loads. Saudi authorities authorized AAC for 8% of Sakani homes in 2025, citing superior thermal and fire ratings. EMSTEEL’s light-steel panels deliver 35% faster installation in the UAE’s villa segment, though they carry a 15% upfront premium. The UAE’s 2024 fire code mandates 2-hour resistance for mid-rise walls, a benchmark AAC meets more readily than standard hollow blocks. Traditional producers now invest in fire-retardant additives and testing to defend their share in the GCC concrete blocks market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hollow Blocks Retain Leadership Through Thermal Advantage

Hollow units captured 70.01% GCC concrete blocks market share in 2025 and are forecast to record a 6.31% CAGR to 2031, a lead cemented by their 0.45-0.55 W/m²K thermal range that satisfies Estidama and Saudi code thresholds. This dominance secures a steady 2026-2031 cumulative demand exceeding 11 billion units, anchoring the GCC concrete blocks market. Developers benefit from lower HVAC loads, realizing energy savings of 18% in Saudi Arabia’s Sakani homes using ACICO’s recycled-aggregate hollow design. Solid blocks trail, serving low-rise load-bearing jobs where unit weight and seismic ratings take precedence. Niche interlocking and decorative offerings, while below 5% of the GCC concrete blocks market size, enjoy double-digit growth in premium landscape projects that value rapid, mortar-free assembly and customized textures.

Hollow units also give producers supply-chain flexibility. Lightweight formulations allow 25% clinker reduction, easing CO₂ disclosure under UAE labeling mandates. In parallel, modifiable core geometries help manufacturers tailor compressive strength from 7.5 MPa to 15 MPa without altering external dimensions, a trait valued in NEOM’s mixed-use zoning that spans high-rise, hospitality, and social infrastructure. As certification agencies tighten ISO 16757 verification, the testing pedigree of hollow units further extends their competitive moat. Interlocking products, though emerging, cut labor by 25% and appeal to disaster-response agencies in Oman and Bahrain, suggesting a small but resilient upside.

By Application: Residential Builds Anchor Volume Growth

Residential construction accounted for 49.17% of the GCC concrete blocks market size in 2025 and is on track for a 6.39% CAGR through 2031 as housing programs tackle persistent deficits. Saudi Arabia alone could consume 2.8 billion units across the forecast window, reinforcing the GCC concrete blocks market’s residential backbone. The UAE and Qatar replicate this story at smaller scales, with developers adopting lightweight blocks to lower foundation loads on reclaimed land. Hollow units with integrated insulation permit code compliance without extra layers, trimming façade thickness, and expanding net sellable floor area.

Commercial builds are buoyed by post-Expo logistics hubs, retail expansions, and Vision-aligned tourism assets. Prefab block panels here reduce on-site crews by 40%, critical as regional visa reforms lift labor costs. Infrastructure and institutional segments, spanning utilities, schools, and hospitals, favor precast and modular solutions that slash schedules in public procurement where penalties for delay are steep. Omani industrial zones demand fire-resistant blocks that meet Eurocode EN 1996 equivalence, opening a specialty niche of blended-aggregate units incorporating basalt fibers for enhanced thermal shock resistance.

Geography Analysis

Saudi Arabia leads the GCC concrete blocks market with 71.21% share in 2025 and is set to grow at 6.27% CAGR through 2031. The USD 1.7 trillion Vision 2030 capital plan and a 1.2 million-unit housing deficit guarantee sustained block orders, peaking at 1.8 billion units a year by 2028. Sakani delivered 220,000 dwellings in 2025 and continues to preference thermal hollow units for exterior envelopes. Although cement price swings compress margins, producers offset by adopting slag and fly-ash blends that lower clinker ratios by 20%. The Saudi Green Building Code’s U-value cap further cements demand for insulated hollow blocks, reinforcing local supply chains.

The UAE ranks second and demonstrates faster technological shifts. Labor costs rose 12% in 2025, spurring the adoption of modular panels and AAC alternatives. Dubai South logistics district and Al Maktoum airport expansion sustain commercial block demand, while Abu Dhabi’s Estidama preserves hollow unit volume in residential sites. Water stress compels investment in closed-loop curing, with producers claiming 40% water savings. EMSTEEL’s light-steel frames gain villa traction, signaling competitive leakages the GCC concrete blocks market must monitor.

Qatar’s share benefits from North Field LNG phasing, which draws up to 15 million hollow units yearly for worker camps. Its 10,000-unit annual housing commitment specifies insulated blocks aligned with GSAS. The state piloted 3D-printed school walls that cut costs 22%, hinting at disruptive pathways. Oman pursues USD 100 billion of Vision 2040 infrastructure, with mandates on closed-loop water recycling potentially raising the cost floor yet securing long-term ecological compliance. Bahrain and Kuwait remain smaller contributors but deliver steady orders from national housing schemes and early works at Kuwait’s Silk City.

Competitive Landscape

The GCC Concrete Blocks market is moderately consolidated. ACICO runs 12 plants rated at more than 400 million units a year, specializing in recycled-aggregate hollow blocks that qualify for LEED Gold and Estidama 2 Pearl certifications. Saudi Readymix invested USD 15 million to dose slag and fly ash, curbing CO₂ by 20% to align with the UAE’s carbon labeling rule. EMSTEEL diversified into light-steel framing in response to villa-segment demand, advertising 35% faster build times. Technology differentiation widens as top-tier producers deploy automated batching and robotic palletizing that cut labor 15% and improve consistency.

GCC Concrete Blocks Industry Leaders

ESPAC

RAKNOR LLC

Saudi Readymix

KRB

Bucomac

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Oman inaugurated the Global Precast Industries Factory in Halban, Nakhal. The factory, set up with an investment of OMR 2 million (USD 5.2 million), boasts a production line of precast concrete solutions, including hollow core slabs, columns, beams, curbstones, interlock tiles, and concrete fencing solutions.

- January 2025: Alomaier Trading and Contracting Company (OTC) expanded its operations, leveraging the state-of-the-art RH 2000-4 MVA concrete block and paver plant from HESS Group and SR Schindler. The expansion also includes a fully automated line for Shot Blasting, Curling, and Coating. In recent years, Hess Group and SR Schindler have notably bolstered their presence in the Saudi Arabian market.

GCC Concrete Blocks Market Report Scope

A concrete block is a building block composed entirely of concrete, which is then mortared to create an impressive, long-lasting structure. It comes in various shapes and sizes and can be solid or hollow. Concrete blocks are made of cement, aggregate, and water. The ratio of cement and aggregate in concrete blocks is 1:6. The product is used in partition walls due to their quick and easy installation.

The GCC concrete block market is segmented by type, application, and geography. By type, the market is segmented into solid and hollow concrete blocks. By application, the market is segmented into commercial, residential, infrastructure, and industrial & institutional. The report covers the market size and forecast in five countries across the GCC region. For each segment, the market sizing and forecasts are done based on volume (units).

| Solid Concrete Blocks |

| Hollow Concrete Blocks |

| Other Types (e.g., interlocking, decorative) |

| Residential |

| Commercial |

| Infrastructure |

| Industrial and Institutional |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Rest of GCC |

| By Type | Solid Concrete Blocks |

| Hollow Concrete Blocks | |

| Other Types (e.g., interlocking, decorative) | |

| By Application | Residential |

| Commercial | |

| Infrastructure | |

| Industrial and Institutional | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Oman | |

| Rest of GCC |

Key Questions Answered in the Report

What is the current size of the GCC concrete blocks market?

What is the current size of the GCC concrete blocks market?

How fast is demand expected to grow?

The market is projected to register a 5.94% CAGR over the 2026-2031 period, led by Saudi Vision 2030 megaprojects and housing programs.

Which block type leads sales?

Hollow concrete blocks held 70.01% share in 2025 because their thermal efficiency meets regional green-building codes.

Why is residential construction so important?

Housing deficits, especially in Saudi Arabia, and population growth of 1.8% annually drive nearly half of total block consumption.

What are the main industry challenges?

Input-cost volatility, water scarcity, and competition from AAC, light-steel framing, and 3D-printing technologies weigh on margins and market share.

Page last updated on: