Zinc Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

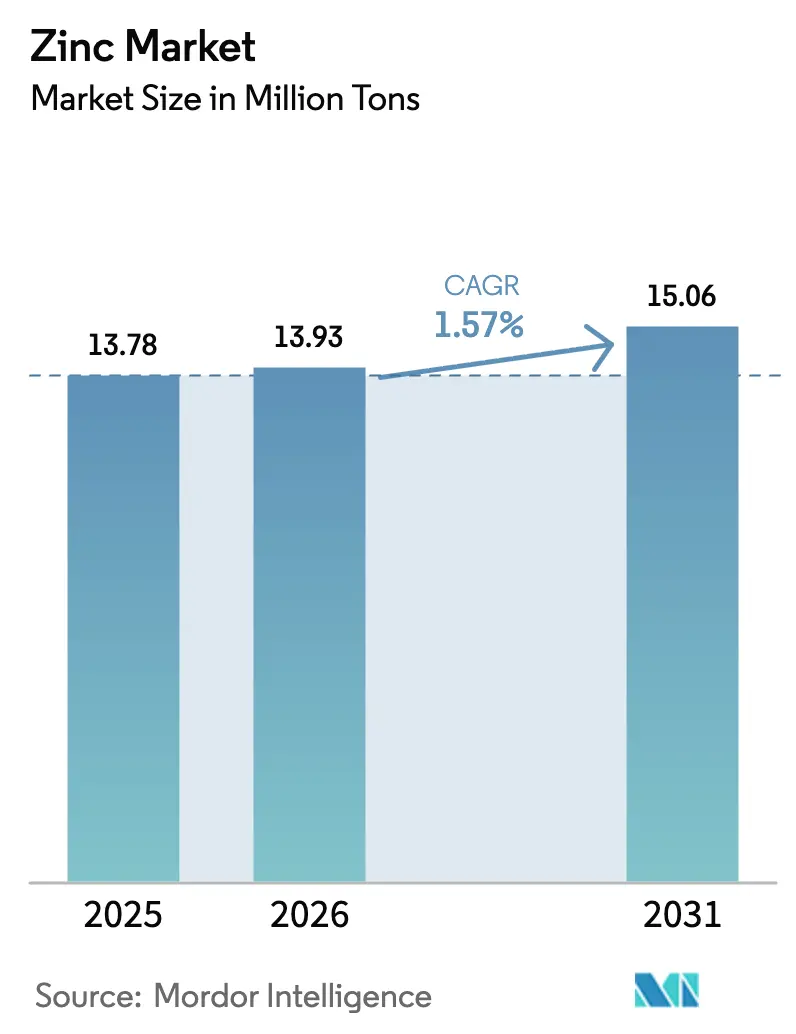

| Market Volume (2026) | 13.93 Million tons |

| Market Volume (2031) | 15.06 Million tons |

| Growth Rate (2026 - 2031) | 1.57% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zinc Market Analysis by Mordor Intelligence

The Zinc Market size was valued at 13.78 Million tons in 2025 and is estimated to grow from 13.93 Million tons in 2026 to reach 15.06 Million tons by 2031, at a CAGR of 1.57% during the forecast period (2026-2031). Demand resilience rests on public-sector infrastructure pipelines, rising penetration of corrosion-resistant steel in electric vehicles and renewable-energy hardware, and the steady uptake of zinc-based fertilizers across micronutrient-deficient soils. Improved secondary-recycling economics, spurred by the European Union’s Carbon Border Adjustment Mechanism, are nudging smelters toward lower-carbon feedstocks even as mine-supply concentration injects price risk. Meanwhile, pilot deployments of zinc-ion and zinc-air batteries signal an emergent outlet for specialty compounds that could add up to 100,000 tons of incremental offtake by 2031.

Key Report Takeaways

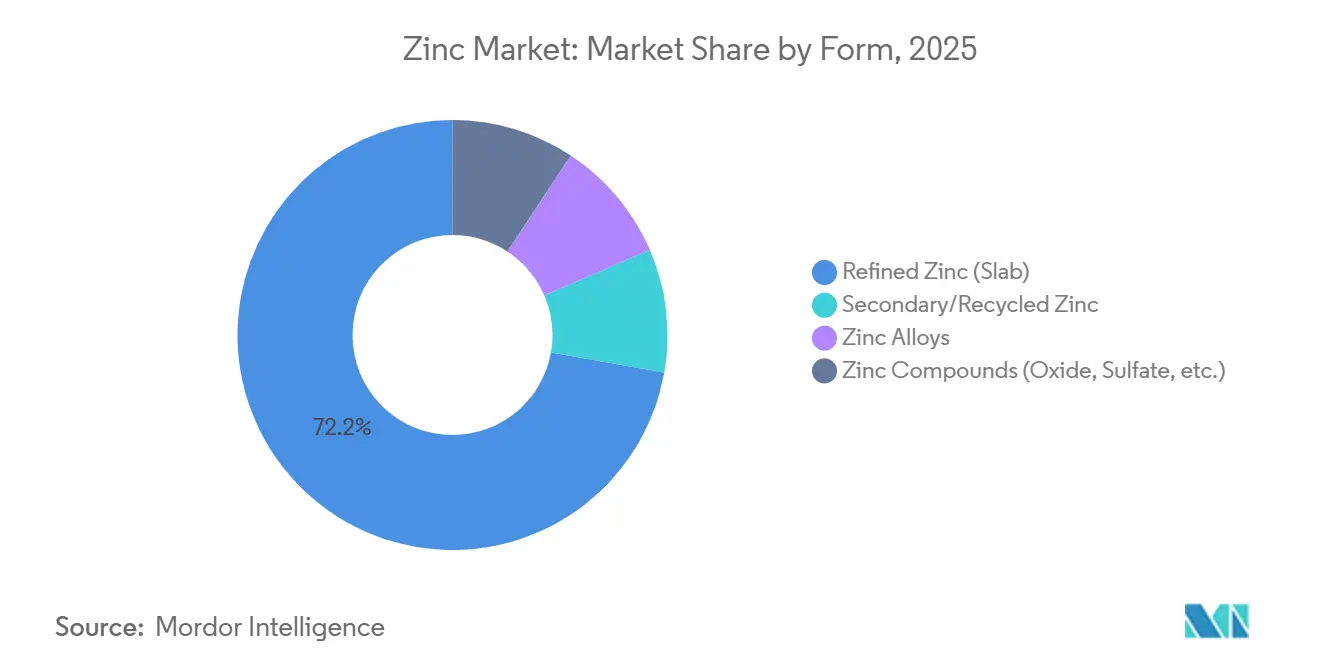

- By form, refined zinc (slab) led with 72.21% of zinc market share in 2025, while zinc compounds are projected to advance at a 2.89% CAGR through 2031.

- By production process, primary production accounted for 65.62% of the zinc market share in 2025; secondary production is on track for the fastest 2.71% CAGR to 2031.

- By application, galvanizing captured 52.37% of the zinc market size in 2025, whereas zinc oxide and chemicals are poised for a 2.77% CAGR over 2026-2031.

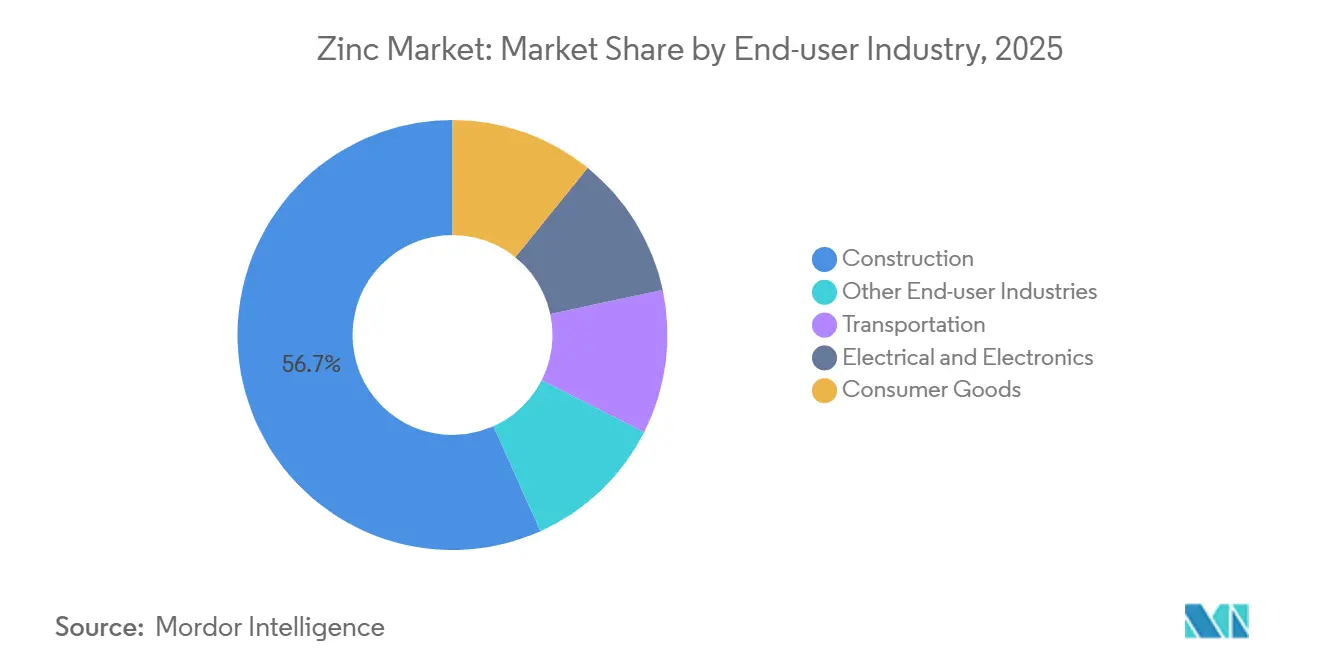

- By end-user industry, construction dominated with a 56.71% share in 2025; electrical and electronics are expected to rise at a 2.42% CAGR to 2031.

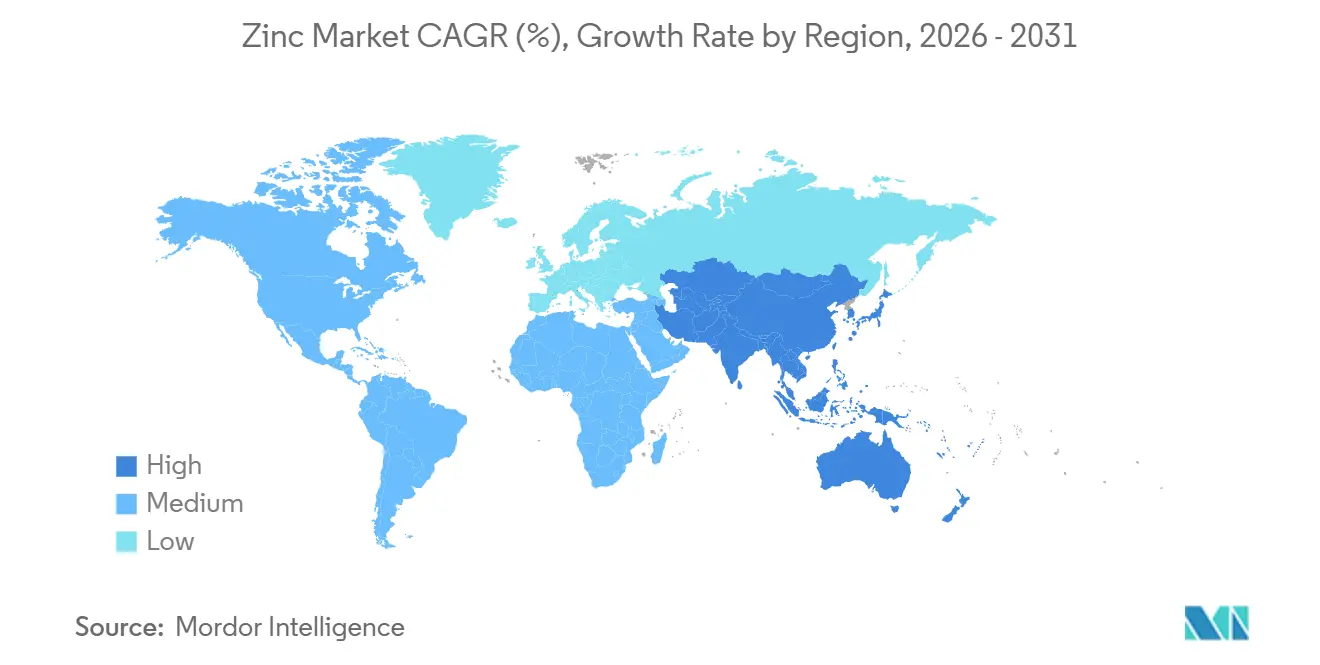

- By geography, Asia-Pacific commanded 62.86% of 2025 volume and is also projected to register the quickest 2.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Zinc Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-led galvanizing demand surge | +0.4% | Asia-Pacific core, spillover to Middle-East and Africa | Medium term (2–4 years) |

| Growth of corrosion-resistant steel in EV and renewables | +0.3% | Global, concentrated in North America, Europe, China | Long term (≥4 years) |

| Expansion of zinc-based fertilizers in micronutrient-deficient soils | +0.2% | South Asia, Sub-Saharan Africa, Latin America | Long term (≥4 years) |

| Emergence of zinc-ion and zinc-air batteries | +0.1% | North America, Europe (pilot deployments) | Long term (≥4 years) |

| EU drinking-water zinc-coated plumbing mandate | +0.1% | Europe, with adoption spillover to Middle-East | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Galvanizing Demand Surge

Multiyear public-capital programs are locking in visibility for galvanizers across Asia and North America. India’s USD 1.4 trillion National Infrastructure Pipeline, ASEAN expressway corridors, and the U.S. Infrastructure Investment and Jobs Act require hundreds of thousands of tons of coated steel that must comply with ISO 1461 and ASTM A123 thickness norms. Galvanized coatings deliver service lives of 50-100 years in rural zones, cementing their status as the preferred corrosion barrier where lifecycle economics dominate.

Growth of Corrosion-Resistant Steel in EV and Renewables

Battery-electric platforms specify Zn-Ni and Zn-Mg alloy coatings to withstand road salt and thermal cycling, while offshore-wind monopiles rely on hot-dip galvanizing plus organic topcoats to fight chloride attack. Although thinner high-strength steels reduce coating per ton, total coated-steel tonnage rises fast enough to maintain volume growth, reinforcing long-run support for the zinc market[1]International Renewable Energy Agency, “Wind Offshore Foundations 2025,” irena.org.

Expansion of Zinc-Based Fertilizers in Micronutrient-Deficient Soils

Roughly half of global cereal soils lack bioavailable zinc, depressing yields by 10-30%. India’s Soil Health Card initiative now recommends zinc application below 0.6 ppm thresholds, and HarvestPlus biofortification programs demonstrate 15-20% yield gains with zinc-enhanced seed. While regional heavy-metal limits vary, demand for zinc sulfate, oxide, and chelates continues to climb in South Asia and Sub-Saharan Africa.

Emergence of Zinc-Ion and Zinc-Air Batteries

The U.S. DOE’s Long Duration Energy Storage Earthshot aims for 10-hour systems at USD 0.05 kWh by 2030. Zinc-ion chemistries offer theoretical 400 Wh kg energy densities without flammability hazards. Pilot projects by Urban Electric Power and Zinc8 are surpassing 1,000 cycles in controlled runs, although dendrite mitigation and electrolyte stability remain hurdles. Successful scale-up could redirect a modest yet material slice of lithium-ion demand toward the zinc market.

Restraints Impact Analysis of Zinc Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental and ESG regulations | -0.3% | Global, acute in Europe and China | Medium term (2–4 years) |

| Price volatility from supply shocks and surpluses | -0.2% | Global, amplified in import-dependent regions | Short term (≤2 years) |

| Fertilizer heavy-metal limits curbing zinc sulfate | -0.1% | Europe, North America, select Asian jurisdictions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental and ESG Regulations

CBAM certificates priced near EUR 85 tCO₂ raise landed costs for non-EU refined zinc by USD 130-240 t. China’s dual-carbon roadmap shut 30 small smelters in 2024, erasing 200,000 t of capacity and underscoring a shift toward low-emission supply that already trades at 3-5% premiums. Scope 3 audits under the EU Corporate Sustainability Reporting Directive elevate certified smelters and disadvantage high-carbon peers.

Fertilizer Heavy-Metal Limits Curbing Zinc Sulfate

Germany and the Netherlands apply precautionary heavy-metal thresholds to soil amendments, and synthetic zinc compounds face exclusion from organic protocols. Chelated alternatives free of co-contaminants cost 2-3× more than zinc sulfate, throttling uptake among smallholders in price-sensitive regions until Codex standards converge by 2027[2]United States Department of Agriculture, “National Organic Program Handbook 2025,” usda.gov .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Zinc Market Segment Analysis

By Form:

Refined Slabs Anchor Supply, Compounds Capture Specialty GrowthRefined zinc (slab) controlled 72.21% of 2025 volume, underpinning galvanizing, die-casting, and brass-mill demand. In contrast, zinc compounds will rise at 2.89% CAGR, buoyed by zinc-oxide activators in tires, UV-blocking pharmaceutical grades, and transparent-conductor films for flexible electronics. The zinc market size linked to recycled feed is widening as Waelz-kiln expansions in Europe and India reclaim oxide from electric-arc-furnace dust at 75% lower CO₂ intensity.

Secondary zinc enjoys policy tailwinds from CBAM credits and corporate Scope 3 targets. Integrated miners are therefore pivoting toward compounds and alloys that earn double-digit premiums, diversifying revenue away from commodity slabs amid persistent Chinese oversupply.

By Production Process:

Primary Dominance Erodes as Recycling ScalesPrimary production held 65.62% of output in 2025, but its 1.5-2.5 t CO₂ tZn footprint faces escalating carbon costs. Mine delays and the fact that the top ten sites supply 40% of concentrates add another layer of risk. Conversely, secondary production (recycling) is growing at 2.71% CAGR capture zinc market share as hydrometallurgical leaching upgrades recovery from EAF dust and brass skimmings. European Waelz kilns now process 500,000 t of waste annually, and India is adding capacity to process 4 million t of dust generated by its steel sector.

By Application:

Galvanizing Leads, Zinc Oxide Chemicals AccelerateGalvanizing commanded 52.37% of the zinc market size in 2025, supported by ISO-compliant coating layers that extend steel life on bridges, towers, and metro rail. Continuous lines adopting Zn-Al-Mg baths cut recoating intervals by 30-50%. Meanwhile, zinc oxide and chemicals will post a 2.77% CAGR as tire, pharma, and electronics sectors scale. Aluminum-doped zinc oxide films on solar cells and foldable displays strengthen forward demand visibility.

By End-user Industry:

Construction Dominates, Electronics OutpacesConstruction absorbed 56.71% of 2025 demand, sustained by India’s housing, ASEAN expressways, and U.S. bridge rehabilitation. Electrical and electronics, forecast at 2.42% CAGR, rides on zinc-oxide varistors in EV chargers and transparent conductors in displays. Automotive OEMs meanwhile adopt Zn-Mg coatings up to 15 µm thick for battery-tray corrosion warrants, cushioning tonnage even as per-unit steel use in vehicles declines.

Geography Analysis

APAC Zinc Market

Asia-Pacific accounted for 62.86% of global tonnage in 2025 and is set for the highest 2.50% CAGR as China’s grid-modernization and India’s USD 1.4 trillion infrastructure pipeline absorb coated steel. ASEAN mega-projects such as Indonesia’s Nusantara capital city multiply galvanized demand, while Japan and South Korea supply Zn-Al-Mg coating know-how. Regulatory pushes, China’s dual-carbon smelter closures, and India’s soil-health fertilizer incentives reinforce regional consumption.

North America Zinc Market

North America benefits from the U.S. infrastructure law and Canada’s low-carbon Trail smelter upgrade. South32’s Hermosa project will add 150,000 t of refined output in 2027, reducing import reliance. Mexico’s export-oriented auto lines keep galvanizers running near capacity, anchoring regional zinc flows.

Europe Zinc Market

Europe’s CBAM, enforceable from 2026, lifts demand for certified low-carbon metal from Nyrstar, Boliden, and other compliant smelters. At the same time, Implementing Decisions 2024/367-368 compel plumbing manufacturers to validate zinc release below 5 mg L under the revised Drinking Water Directive, spurring alloy reformulations.

Competitive Landscape

The zinc market hosts a moderate structure: top five players hold roughly 45% of capacity, while fast-moving Chinese smelters fill price-driven supply gaps. Glencore’s Red Dog maintenance and Teck’s Trail upgrade briefly tightened supply, yet rapid Chinese output ramping restored balance, underscoring elastic capacity outside the OECD. Certified low-carbon producers command 3-5% premiums as downstream buyers track Scope 3 emissions.

Recyclers reclaiming zinc from EAF dust cut carbon by 75% and enjoy CBAM advantages, while specialty converters target battery-grade oxide and Zn-Mg alloys that receive higher margins. Patent activity in zinc-ion battery electrolytes surged past 200 filings in 2025, indicating intensifying R&D competition among battery start-ups and incumbent material firms.

Zinc Industry Leaders

Glencore

Nyrstar

Teck Resources Limited

KOREAZINC

Vedanta Limited

- *Disclaimer: Major Players sorted in no particular order

Zinc Market Companies Covered in this Report

- Boliden Group

- Glencore

- Grupo Mexico

- Hudbay Minerals Inc.

- IVANHOE MINES

- KOREAZINC

- MMG Australia Limited

- Nexa

- Nyrstar

- South32

- Teck Resources Limited

- Vedanta Limited

- Volcan

Recent Industry Developments in Zinc Market

- February 2026: Hindustan Zinc, subsidiary of Vedanta Limited signed a Memorandum of Understanding (MoU) with Tripura Group to operationalize a manufacturing unit within the company's flagship Zinc Park at Khankhala, Bhilwara district of Rajasthan. The agreement marked an important milestone in Hindustan Zinc's plan to build India's first integrated downstream industrial hub dedicated to zinc-based value chains.

- July 2024: IVANHOE MINES officially restarted the high-grade Kipushi zinc mine in the Democratic Republic of the Congo. The mine is expected to produce over 278,000 tonnes of zinc annually in its first five years, establishing itself as Africa's largest and one of the world's top four zinc producers.

Global Zinc Market Report Scope

Zinc is a bluish-white metal that is brittle at room temperature but becomes malleable when heated. Zinc is found in nature as a mineral in the Earth's crust, and it is commonly used as a coating for iron and steel to protect against corrosion.

The zinc market is segmented by form, production process, application, end-user industry, and geography. By form, the market is segmented into refined zinc (slab), zinc alloys, zinc compounds (oxide, sulfate, etc.), and secondary/recycled zinc. By production process, the market is segmented into primary production (mining and smelting) and secondary production (recycling). By application, the market is segmented into galvanizing, die-casting, brass, zinc oxide and chemicals, and other applications. By end-user industry, the market is segmented into construction, transportation, electrical and electronics, consumer goods, and other end-user industries. The report also covers the market size and forecasts for zinc in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

Segmentation Overview

| Refined Zinc (Slab) |

| Zinc Alloys |

| Zinc Compounds (Oxide, Sulfate, etc.) |

| Secondary/Recycled Zinc |

| Primary Production (Mining and Smelting) |

| Secondary Production (Recycling) |

| Galvanizing |

| Die-Casting |

| Brass |

| Zinc Oxide and Chemicals |

| Other Applications |

| Construction |

| Transportation |

| Electrical and Electronics |

| Consumer Goods |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Spain | |

| Turkey | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Form | Refined Zinc (Slab) | |

| Zinc Alloys | ||

| Zinc Compounds (Oxide, Sulfate, etc.) | ||

| Secondary/Recycled Zinc | ||

| By Production Process | Primary Production (Mining and Smelting) | |

| Secondary Production (Recycling) | ||

| By Application | Galvanizing | |

| Die-Casting | ||

| Brass | ||

| Zinc Oxide and Chemicals | ||

| Other Applications | ||

| By End-user Industry | Construction | |

| Transportation | ||

| Electrical and Electronics | ||

| Consumer Goods | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Malaysia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the zinc market?

The zinc market size stands at 13.93 million tons in 2026 and is forecast to reach 15.06 million tons by 2031, with a CAGR of 1.57% through 2031.

Which region leads consumption of zinc?

Asia-Pacific commanded 62.86% of 2025 volume and is set to remain the dominant consumer.

Why is secondary production (recycling) of zinc gaining momentum?

Recycling via Waelz kilns cuts carbon footprints by 75% and benefits from EU CBAM incentives, driving a 2.71% CAGR to 2031.

How will EU plumbing rules affect zinc alloys?

Implementing Decisions 2024/367-368 force brass-fitting makers to reduce lead below 0.2% and validate zinc migration, spurring alloy reformulation ahead of the December 2026 deadline.

Page last updated on: