Market Overview

| Study Period | 2021 - 2031 |

|---|---|

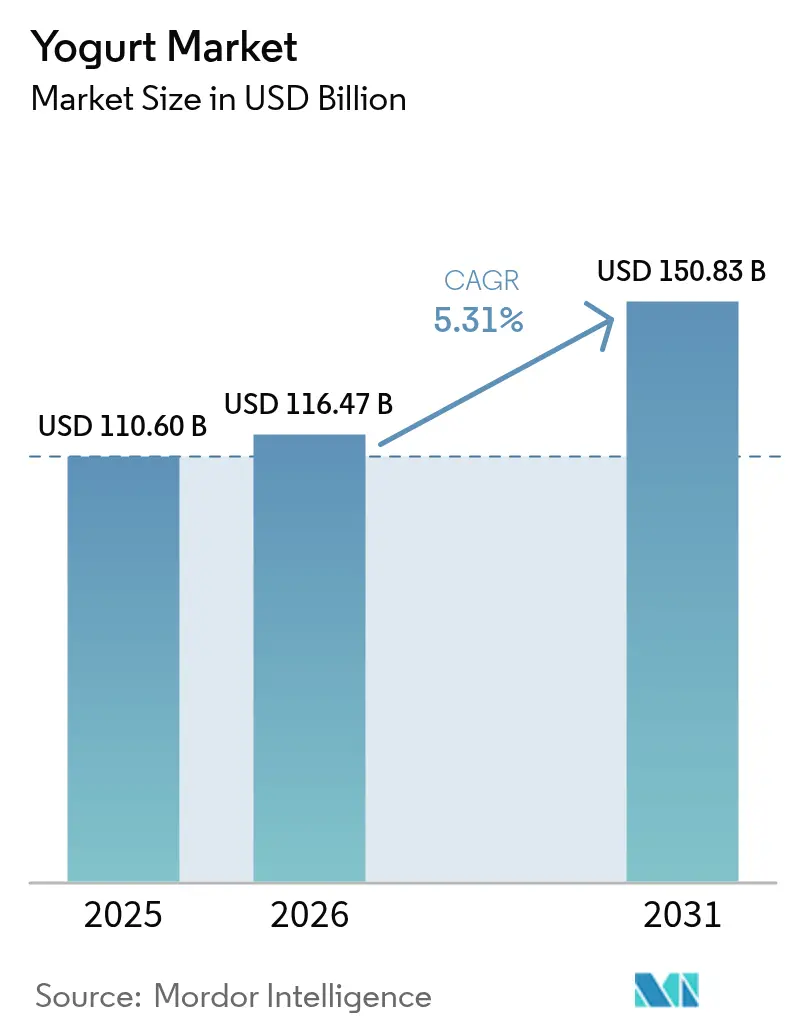

| Market Size (2026) | USD 116.47 Billion |

| Market Size (2031) | USD 150.83 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Yogurt Market Analysis by Mordor Intelligence

Yogurt market size in 2026 is estimated at USD 116.47 billion, growing from 2025 value of USD 110.60 billion with 2031 projections showing USD 150.83 billion, growing at 5.31% CAGR over 2026-2031. The yogurt market continues to benefit from a proven link between clinically validated probiotic strains and measurable gut-health outcomes, encouraging premiumization and fostering steady category resilience. Manufacturers have adopted advanced fermentation technologies that keep beneficial bacteria alive through digestion, supporting functional-food positioning and sustaining consumer willingness to trade up. Strong disposable-income growth across emerging economies and rising interest in immune support further reinforce demand, while digital commerce accelerates product discovery and subscription-based replenishment. Expanding foodservice penetration—especially in cafés and convenience stores—broadens usage occasions, and technological breakthroughs in shelf-stable packaging extend reach into markets lacking cold-chain infrastructure.

Key Report Takeaways

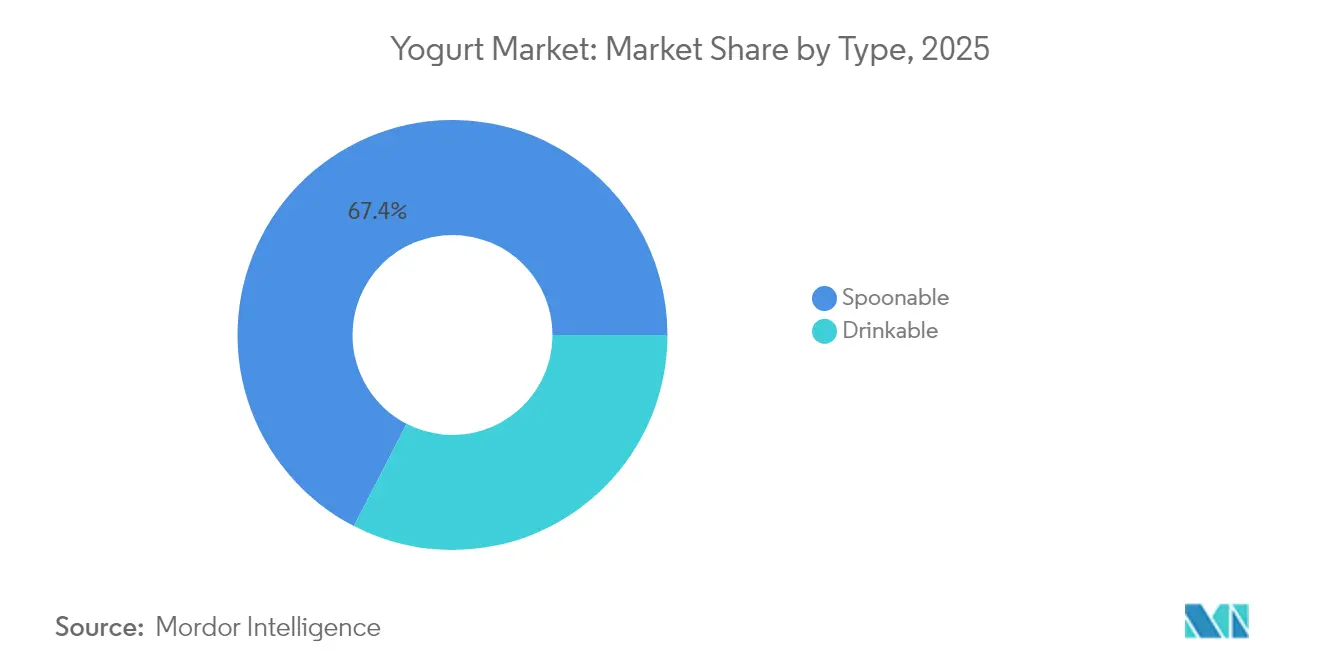

- By type, spoonable yogurt captured 67.42% of the yogurt market share in 2025, whereas drinkable yogurt is expanding at a 6.86% CAGR through 2031.

- By source, dairy-based products accounted for 53.95% of the yogurt market size in 2025; plant-based alternatives are forecast to advance at 7.78% CAGR to 2031.

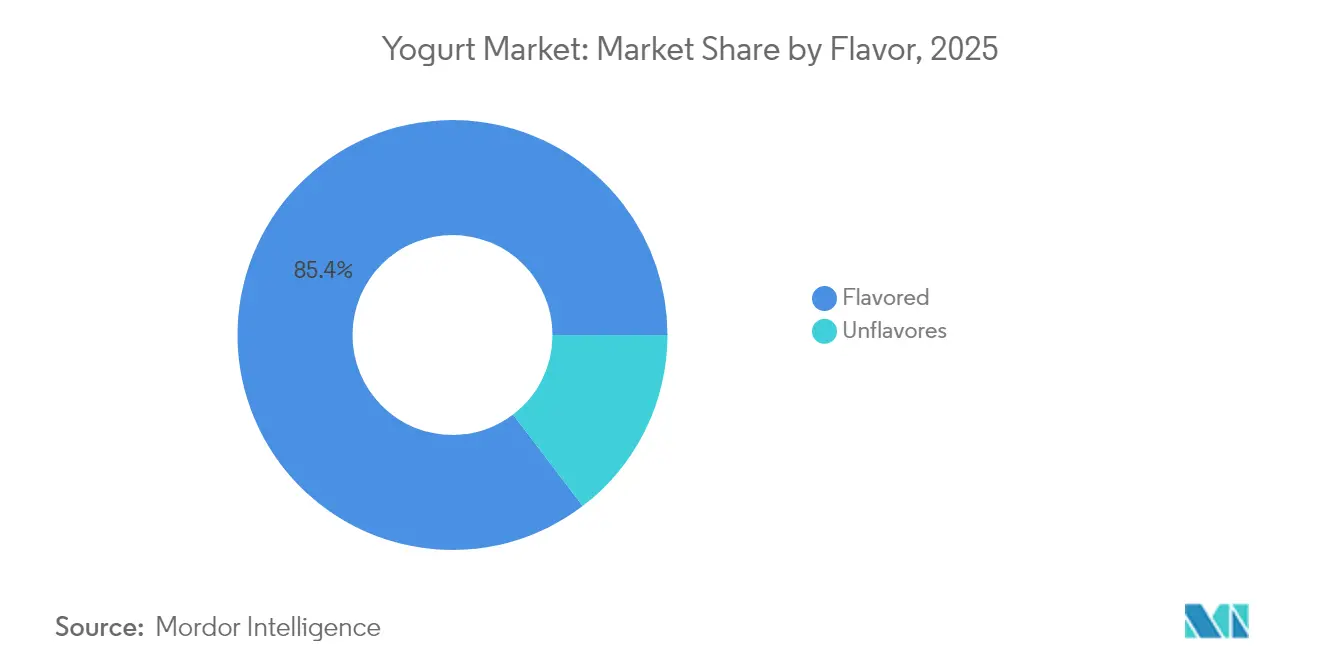

- By flavor, flavored varieties held 85.35% revenue share in 2025; unflavored formats are projected to rise at a 5.14% CAGR between 2026 and 2031.

- By distribution channel, off-trade sales represented 53.61% of the yogurt market size in 2025, and this channel is set to grow at a 7.29% CAGR through 2031.

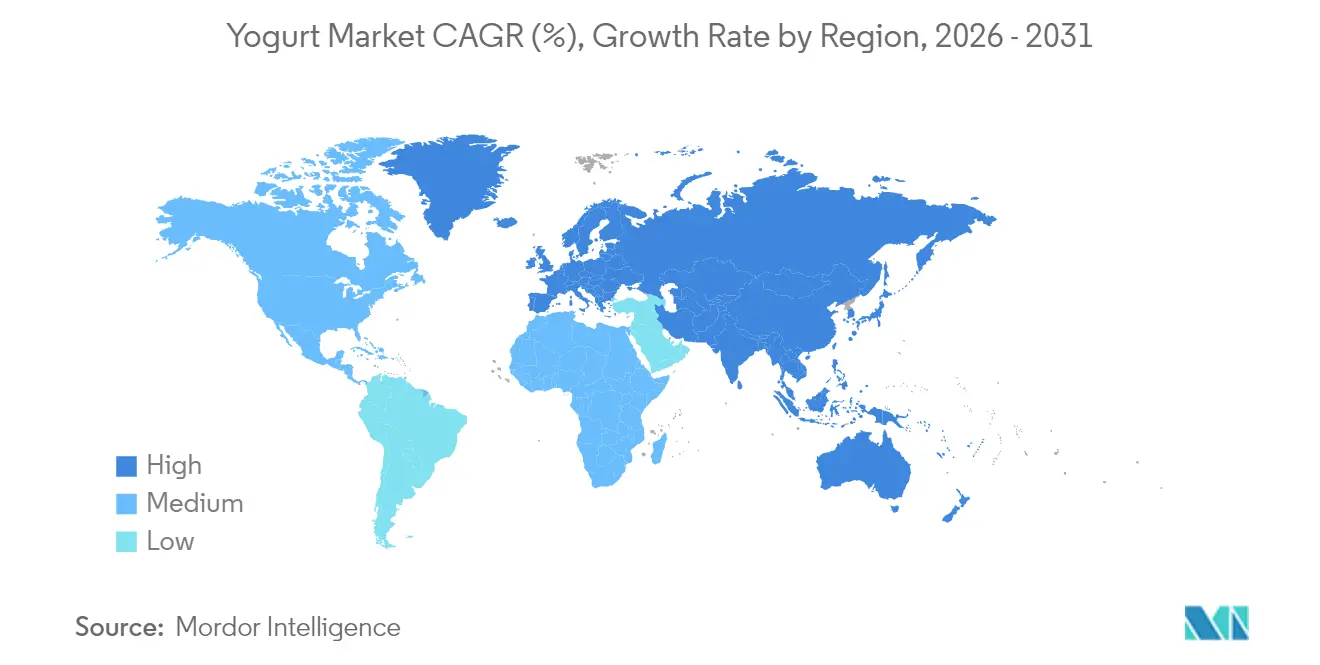

- By geography, the Asia Pacific led with 55.78% yogurt market share in 2025 and is poised to post a 11.9% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Yogurt Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer focus on gut health, probiotics, and immunity | +1.2% | Global, with strongest adoption in North America & Europe | Medium term (2-4 years) |

| Development of functional and fortified yogurts with added nutrients | +0.8% | North America & EU core, expansion to APAC | Long term (≥ 4 years) |

| Rising use in cafes, QSRs, and convenience outlets | +1.5% | Global, led by urban centers in APAC and North America | Short term (≤ 2 years) |

| Rising E-commerce expansion | +0.9% | Global, with accelerated penetration in APAC | Short term (≤ 2 years) |

| Advanced fermentation techniques and shelf-stable packaging innovations | +1.1% | Global, technology transfer from developed to emerging markets | Long term (≥ 4 years) |

| High-protein Greek & Icelandic lines broaden usage occasions | +0.6% | North America & EU, emerging adoption in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Focus on Gut Health, Probiotics, and Immunity

Probiotic strains are redefining yogurt's role from a simple indulgence to a therapeutic nutrition option. Clinical studies have confirmed the effectiveness of specific bacterial cultures, such as Lactobacillus acidophilus and Bifidobacterium lactis, in enhancing immune function and digestive health. Research indicates that these strains can reduce the duration of respiratory infections by up to two days and strengthen gut barrier function, as reported by the National Center for Biotechnology Information[1]National Center for Biotechnology Information, “Probiotics and Their Health Benefits,” NCBI, ncbi.nlm.nih.gov. With this scientific backing, manufacturers can justify premium pricing for probiotic-enriched products while building consumer trust through proven health benefits. As global healthcare expenses rise, functional yogurt is gaining traction as a preventive nutrition that offers tangible wellness outcomes. Additionally, regulatory bodies are increasingly approving health claims for specific probiotic strains, providing a competitive advantage to companies that prioritize clinical research and strain innovation.

Development of Functional and Fortified Yogurts with Added Nutrients

Yogurt is being redefined as a wellness product, with manufacturers adding protein isolates, omega-3 fatty acids, vitamins, and minerals to address specific nutritional deficiencies in consumer diets. Advanced microencapsulation technologies now protect sensitive nutrients during fermentation and storage, ensuring the stable delivery of heat-sensitive compounds like probiotics and vitamins, as acknowledged by the Food and Drug Administration. Leveraging these advancements, single-serve yogurt products now provide 20-25 grams of protein along with a complete vitamin profile, directly competing with traditional supplements. This strategy is particularly effective in regions with identified nutritional deficiencies, positioning fortified yogurt as an accessible source of essential nutrients. Regulatory approval processes for fortification claims create entry barriers that benefit established manufacturers with expertise in regulatory compliance and clinical validation.

Rising Use in Cafes, QSRs, and Convenience Outlets

Quick-service restaurants and convenience stores are boosting yogurt demand by transforming it from a home-consumed product to a convenient nutritional option. This transformation is evident in breakfast menus, smoothie offerings, and grab-and-go formats. As traditional breakfast routines shift toward mobile consumption, the need for portable yogurt products that provide both nutrition and satiety during commutes is increasing, as noted by the U.S. Department of Agriculture[2]United States Department of Agriculture, "Food Expenditure Series", www.fas.usda.gov. Convenience store partnerships allow yogurt brands to capture impulse purchases and expand consumption beyond typical meal times. Quick-service restaurants (QSRs) particularly benefit from integrating high-protein and Greek-style yogurts into their menus, offering healthier alternatives to traditional fast-food options. This channel diversification reduces reliance on grocery retail while leveraging the higher-margin pricing structures of foodservice channels.

Rising E-commerce Expansion

Digital commerce is revolutionizing yogurt distribution by enabling direct-to-consumer connections, subscription models, and distinctive product offerings—features that traditional retail cannot fully support due to shelf space limitations. E-commerce platforms are driving the availability of niche probiotic strains, organic options, and customized nutrition products, addressing specific health requirements and dietary preferences, as noted by the U.S. Census Bureau[3]U.S. Census Bureau, " QUARTERLY RETAIL E-COMMERCE SALES 2nd QUARTER 2025", www.census.gov. This channel plays a pivotal role in premium and functional yogurt categories, where consumer education and comprehensive product details influence purchasing decisions. Subscription services provide consistent revenue streams while lowering customer acquisition costs through automated replenishment. Advancements in cold-chain logistics ensure the reliable delivery of refrigerated yogurt, extending market access to areas with limited traditional retail presence.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices and irregular supply of milk | -0.7% | Global, with acute impact in regions dependent on milk imports | Short term (≤ 2 years) |

| Compliance with regional food safety, labeling, and health claim regulations | -0.5% | Global, with varying intensity across regulatory jurisdictions | Medium term (2-4 years) |

| Rising prices of raw materials and energy increase production | -0.9% | Global, with higher impact in energy-intensive manufacturing regions | Short term (≤ 2 years) |

| Competition from non-dairy alternatives like almond or oat milks | -0.4% | North America & EU primarily, expanding to urban APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices and Irregular Supply of Milk

Milk price volatility compresses margins and disrupts supply chains, compelling manufacturers to implement dynamic pricing strategies while addressing consumer price sensitivity in competitive retail markets. USDA forecasts indicate that milk prices will remain between USD 22-24 per hundredweight through 2025, reflecting 15-20% volatility that directly affects yogurt production costs. Weather-related supply disruptions, increasing feed costs, and dairy herd consolidation result in inconsistent milk availability, complicating production planning and inventory management. Smaller yogurt producers face greater challenges due to limited bargaining power with dairy suppliers and reduced capacity to mitigate commodity price risks through financial instruments. Additionally, the geographic concentration of dairy production in specific regions increases susceptibility to localized supply disruptions, impacting global yogurt manufacturing networks.

Rising Prices of Raw Materials and Energy Increase Production

In 2024, industrial electricity costs rose by 12-15% in major manufacturing regions, according to the U.S. Energy Information Administration. This increase directly affected operations such as refrigerated storage, pasteurization, and packaging, which are significant contributors to overall production costs. Yogurt manufacturing, already highly sensitive to energy price fluctuations due to its refrigeration and processing requirements, now faces compounded challenges. Energy cost inflation across electricity, natural gas, and transportation fuels places substantial pressure on yogurt producers. Additionally, rising costs of petroleum-based plastics and aluminum have driven packaging material inflation, further squeezing profit margins. Manufacturers must carefully balance these increased costs against consumer price acceptance. Higher transportation fuel prices add another layer of complexity, impacting the delivery of raw materials and the distribution of finished products, particularly for companies serving geographically dispersed markets. These challenges create advantages for producers with energy-efficient manufacturing processes and vertical integration, while smaller players may be forced to exit the market or consolidate operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Convenience Drives Drinkable Innovation

In 2025, spoonable yogurt holds a commanding 67.42% market share, supported by strong consumer preferences and its versatility across various consumption occasions, including breakfast, snacking, and dessert. Its success is largely driven by the benefits of portion control and the ability to customize with mix-ins, toppings, and a wide range of flavors, which enhance both the sensory appeal and the perceived value of the product. On the other hand, drinkable yogurt is experiencing the fastest growth in the market, with a projected CAGR of 6.86% through 2031. This growth is primarily attributed to the increasing demand for convenient, on-the-go nutrition solutions that align with the fast-paced lifestyles of modern consumers.

Innovative packaging technologies have played a crucial role in the growth of drinkable yogurt by ensuring the viability of probiotics while extending shelf life, which facilitates broader distribution networks. The drinkable yogurt segment is also benefiting significantly from the expansion of foodservice channels, as cafes and convenience stores increasingly prefer liquid formats. These formats integrate effortlessly into existing beverage operations and require minimal preparation, making them an attractive option for businesses. Additionally, while the FDA supports health claims for both spoonable and drinkable yogurt formats, drinkable varieties face stricter scrutiny, particularly regarding sugar content and nutritional labeling. This regulatory focus is influencing product formulation strategies, pushing manufacturers to innovate and meet evolving consumer and regulatory expectations.

By Source: Plant-Based Alternatives Reshape Category Boundaries

In 2025, the dairy-based segment holds a significant 53.95% market share, driven by its traditional manufacturing expertise and robust supply chains. These strengths ensure consistent quality and competitive pricing in global markets. Consumers' familiarity with dairy products, along with their natural complete proteins, enhances health positioning and supports nutritional claims. On the other hand, plant-based alternatives are experiencing remarkable growth, with a projected CAGR of 7.78% through 2031. This growth is attributed to increasing awareness of lactose intolerance, heightened environmental sustainability concerns, and evolving dietary preferences, which collectively expand the total addressable market, as highlighted by the National Center for Biotechnology Information.

Advancements in plant protein isolation and fermentation technology have enabled non-dairy yogurts to replicate the texture and taste of traditional dairy products while offering similar probiotic benefits. Almond, oat, and coconut bases provide distinct nutritional profiles and flavor characteristics, appealing to diverse consumer segments and usage occasions. However, the plant-based segment faces regulatory challenges, particularly regarding protein content claims and probiotic strain viability. These issues require specialized manufacturing processes and rigorous quality control, posing significant entry barriers for smaller producers.

By Flavor: Unflavored Growth Signals Premium Positioning

In 2025, flavored yogurt varieties hold a significant 85.35% market share, highlighting changing consumer preferences. Once considered a basic dairy product, yogurt has transformed into an indulgent treat, often competing with traditional desserts. This shift is driven by continuous innovation in the flavored segment. By utilizing natural and artificial flavoring systems, brands introduce seasonal offerings, limited editions, and region-specific flavors, encouraging both trial and repeat purchases. On the other hand, unflavored yogurts are experiencing steady growth, with a 5.14% CAGR projected through 2031. This growth reflects a more sophisticated consumer base that increasingly favors natural, minimally processed products. These unflavored options not only serve as standalone items but also act as versatile ingredient bases, enabling customized consumption experiences, as noted by the Food and Drug Administration.

Health-conscious consumers are increasingly choosing unflavored yogurts, prioritizing their protein content and probiotic benefits over flavor enhancements. This trend creates opportunities for premium positioning and higher profit margins. It aligns with the rising demand for clean labels and ingredient transparency, as consumers prefer products with shorter ingredient lists and minimal processing. Additionally, unflavored yogurts are widely used in commercial and foodservice applications, where they function as ingredients rather than standalone products, thereby expanding their usage occasions.

By Distribution Channel: Off-Trade Dominance Reflects Retail Evolution

Off-trade channels maintain commanding market leadership with 53.61% share in 2025 while simultaneously driving growth at 7.29% CAGR through 2031, demonstrating the channel's adaptability to evolving consumer shopping patterns and the category's retail optimization success. Supermarkets and hypermarkets within the off-trade segment benefit from extensive refrigerated display space, promotional capabilities, and the ability to offer a wide variety of selection that supports household stocking behavior and bulk purchasing. E-commerce platforms within off-trade channels experience particularly rapid expansion, enabling subscription models and direct-to-consumer relationships that bypass traditional retail margins while providing detailed product information and consumer education.

Convenience stores emerge as a critical growth driver within off-trade channels, capturing impulse purchases and extending consumption occasions beyond traditional meal times through strategic product placement and grab-and-go packaging formats. The channel's success reflects yogurt's positioning as both a planned grocery purchase and a spontaneous nutrition solution that serves diverse consumption needs. On-trade channels, while smaller in overall share, provide valuable brand exposure and trial opportunities that influence subsequent retail purchasing decisions, creating synergistic effects across distribution strategies.

Geography Analysis

In 2025, Asia Pacific holds a dominant 55.78% market share and exhibits a leading growth rate of 11.9% projected through 2031. This growth stems from the region's mix of traditional fermented food practices and the rapid adoption of Western-style yogurt across varying economic stages. Urbanization in China and India is driving higher disposable incomes and greater health awareness, fueling regional expansion. Meanwhile, established markets like Japan and South Korea focus on premium probiotic innovations and functional nutrition. The region's dairy production capabilities, along with the rise of plant-based alternatives, address diverse dietary needs and the widespread prevalence of lactose intolerance. However, regulatory frameworks in Asia Pacific vary widely: some countries enforce strict probiotic strain requirements, while others adopt more flexible health claim standards, influencing product development strategies.

Europe, though a mature market, remains strategically important in the yogurt industry. Consumers in the region favor organic, premium, and artisanal yogurt products, which often command higher prices and drive innovation within the category. Europe's well-established dairy infrastructure and rigorous food safety regulations provide local producers with competitive advantages while setting global quality benchmarks. Countries such as Germany, France, and the Netherlands lead in per capita consumption and maintain strong export capabilities. Additionally, European consumers increasingly prioritize sustainable packaging and environmentally friendly production methods, shaping supply chain decisions and brand strategies.

North America maintains a significant market presence, leading in innovations related to functional nutrition, high-protein options, and convenient packaging formats that cater to the region's on-the-go consumption habits. The U.S. and Canada benefit from advanced retail and e-commerce infrastructures, enabling rapid product launches and consumer education efforts that support premium brand positioning. Regulatory support for health claims and probiotic benefits fosters the development of functional yogurt products. Established relationships with foodservice channels further drive demand, particularly in restaurants and convenience stores. The region's focus on protein and fitness culture strongly supports the popularity of Greek and Icelandic yogurts, known for their enhanced nutritional profiles.

Competitive Landscape

The yogurt market, with a concentration rating of 6 out of 10, presents a competitive landscape where multinational corporations, regional specialists, and emerging plant-based players compete for market share. This moderate concentration allows large companies to benefit from scale advantages while enabling smaller firms to innovate and quickly adapt to shifting consumer preferences. Companies such as Danone and Chobani are heavily investing in vertical integration, focusing on manufacturing and supply chain management to address cost pressures and ensure consistent quality across global operations.

Technology adoption plays a pivotal role, with industry leaders utilizing advanced fermentation monitoring, innovative packaging, and efficient cold-chain logistics to reduce waste and extend product shelf life. Opportunities in personalized nutrition are expanding, as companies leverage consumer health data and genetic insights to develop tailored probiotic strains and nutritional profiles that align with individual wellness goals. Simultaneously, emerging players are prioritizing plant-based alternatives and sustainable packaging to attract environmentally conscious consumers and address lactose intolerance and diverse dietary needs.

The competition for intellectual property is intensifying, highlighted by increased patent filings in fermentation technologies and probiotic strain development, which offer sustainable competitive advantages and premium market positioning. As food safety standards and health claim regulations become more stringent, expertise in regulatory compliance is increasingly critical, favoring companies with strong regulatory affairs capabilities and investments in clinical research.

Yogurt Industry Leaders

-

China Mengniu Dairy Company Ltd

-

Danone SA

-

Inner Mongolia Yili Industrial Group Co. Ltd

-

Nestlé SA

-

Yakult Honsha Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Danone's probiotic yogurt brand Activia launched a new product line called Activia Proactive. This new low-fat yogurt is thick and creamy, featuring billions of live probiotics and 3g of prebiotic fiber per serving, along with 10g of protein.

- June 2025: French frozen yogurt chain Yogurt Factory has entered the Indian retail market through a partnership with FranGlobal, the international business arm of Franchise India. This collaboration aims to introduce Yogurt Factory’s low-fat frozen yogurt and wider menu offerings to health-conscious Indian consumers.

- April 2025: Britannia Industries officially launched its Greek yogurt range, marking the company's entry into the premium dairy segment in India. The new product line features authentic, high-protein Greek yogurt with bold flavors and functional nutrition benefits, catering to evolving consumer preferences for healthier and protein-rich dairy options.

- October 2024: Chobani launched its new High Protein Greek Yogurt line. The range includes Greek yogurt cups with 20 grams of protein each and drinks offering 15, 20, or 30 grams of protein per serving. These products are made with natural ingredients, real fruit, contain no added sugars, and are lactose-free.

Global Yogurt Market Report Scope

Flavored Yogurt, Unflavored Yogurt are covered as segments by Product Type. Off-Trade, On-Trade are covered as segments by Distribution Channel. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.

Type

| Drinkable Yogurt |

| Spoonable Yogurt |

Source

| Dairy-based |

| Non-dairy based |

Flavour

| Flavoured |

| Un-flavoured |

Distribution Channel

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others (Warehouse clubs, gas stations, etc.) |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Belgium |

| France | |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Turkey | |

| United Kingdom | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| South Korea | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Morocco | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| Type | Drinkable Yogurt | |

| Spoonable Yogurt | ||

| Source | Dairy-based | |

| Non-dairy based | ||

| Flavour | Flavoured | |

| Un-flavoured | ||

| Distribution Channel | On-trade | |

| Off-trade | Convenience Stores | |

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| On-line Retail | ||

| Others (Warehouse clubs, gas stations, etc.) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Belgium | |

| France | ||

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Morocco | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Market Definition

- Butter - Butter is a yellow-to-white solid emulsion of fat globules, water, and inorganic salts produced by churning the cream from cows’ milk

- Category - Milk

- Country - All

- Dairy - Dairy product include milk and any of the foods made from milk, including butter, cheese, ice cream, yogurt, and condensed and dried milk.

- Distribution Channel - All

- Frozen Desserts - Frozen dairy dessert means and includes products containing milk or cream and other ingredients which are frozen or semi-frozen prior to consumption, such as ice milk or sherbet, including frozen dairy desserts for special dietary purposes, and sorbet

- Industry - Dairy Alternatives

- Product Type - All

- Region - Asia Pacific

- Report - United Kingdom Dairy Alternatives Market

- Sour Milk Drinks - Sour milk is thick, curdled milk, with a sour taste, obtained from the fermentation of milk. Sour milk drinks such as kefir, laban, buttermilk have been considered in the study

- Sub-type - All

- Sub_distribution Channels - All

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

- Report title - Europe Dairy Alternatives Market

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms