Workplace Safety Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

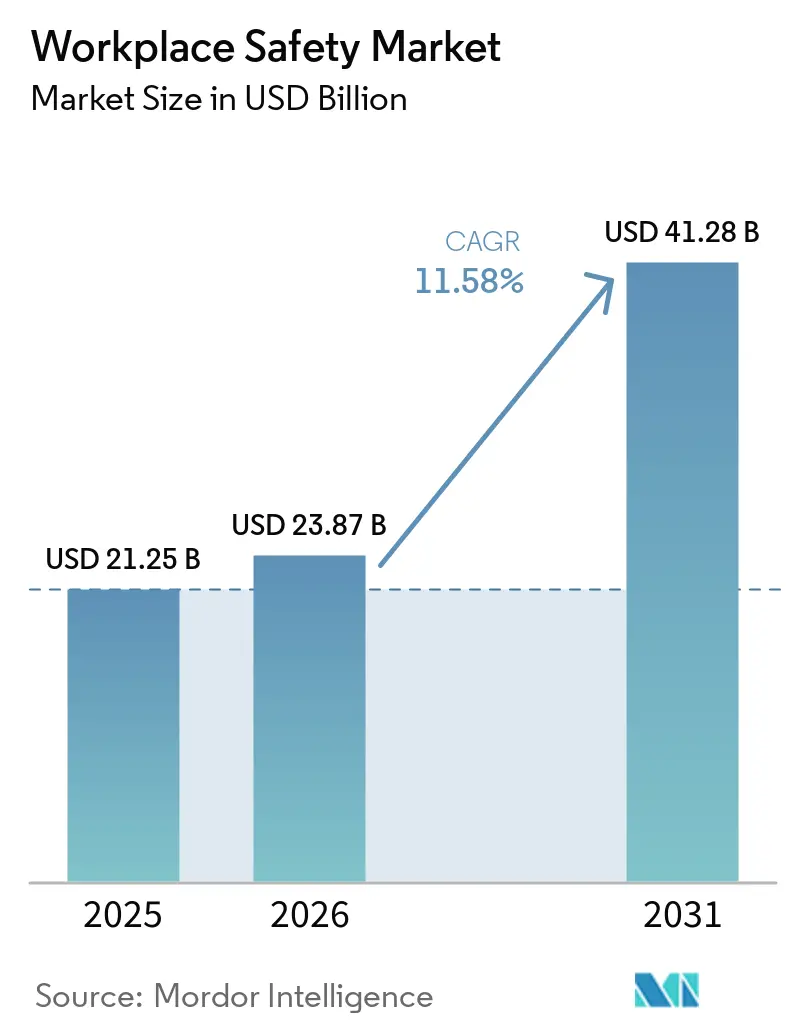

| Market Size (2026) | USD 23.87 Billion |

| Market Size (2031) | USD 41.28 Billion |

| Growth Rate (2026 - 2031) | 11.58% CAGR |

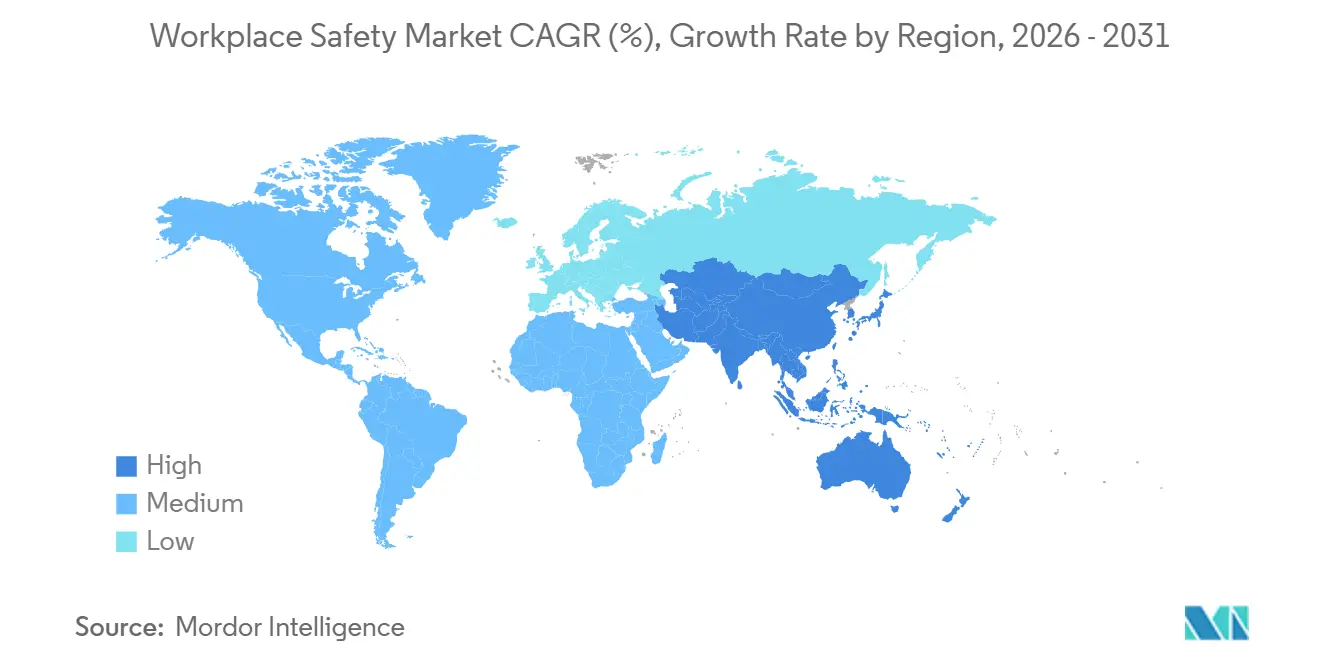

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

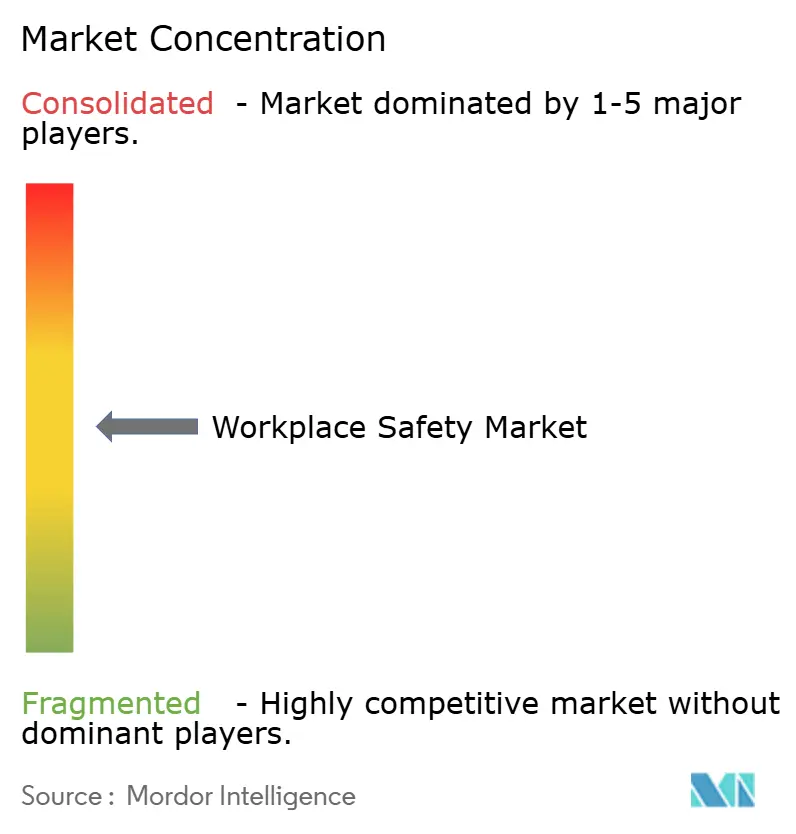

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Workplace Safety Market Analysis by Mordor Intelligence

The workplace safety market size was valued at USD 21.25 billion in 2025 and estimated to grow from USD 23.87 billion in 2026 to reach USD 41.28 billion by 2031, at a CAGR of 11.58% during the forecast period (2026-2031). Enterprises are shifting from compliance-only spending toward proactive risk prevention, embedding AI-enabled vision systems, safety digital twins, and connected wearables into day-to-day operations. Tighter regulations, higher liability costs, and ESG-linked lending terms are transforming safety metrics into balance-sheet variables, accelerating adoption of software-centric solutions. Integrated platforms that connect incident data, predictive analytics, and audit documentation are displacing siloed point tools, while subscription-based pricing is attracting small and medium enterprises. Competitive intensity is rising as nimble software vendors challenge incumbent hardware leaders, but the top five suppliers still command roughly one-third of global revenue.

Key Report Takeaways

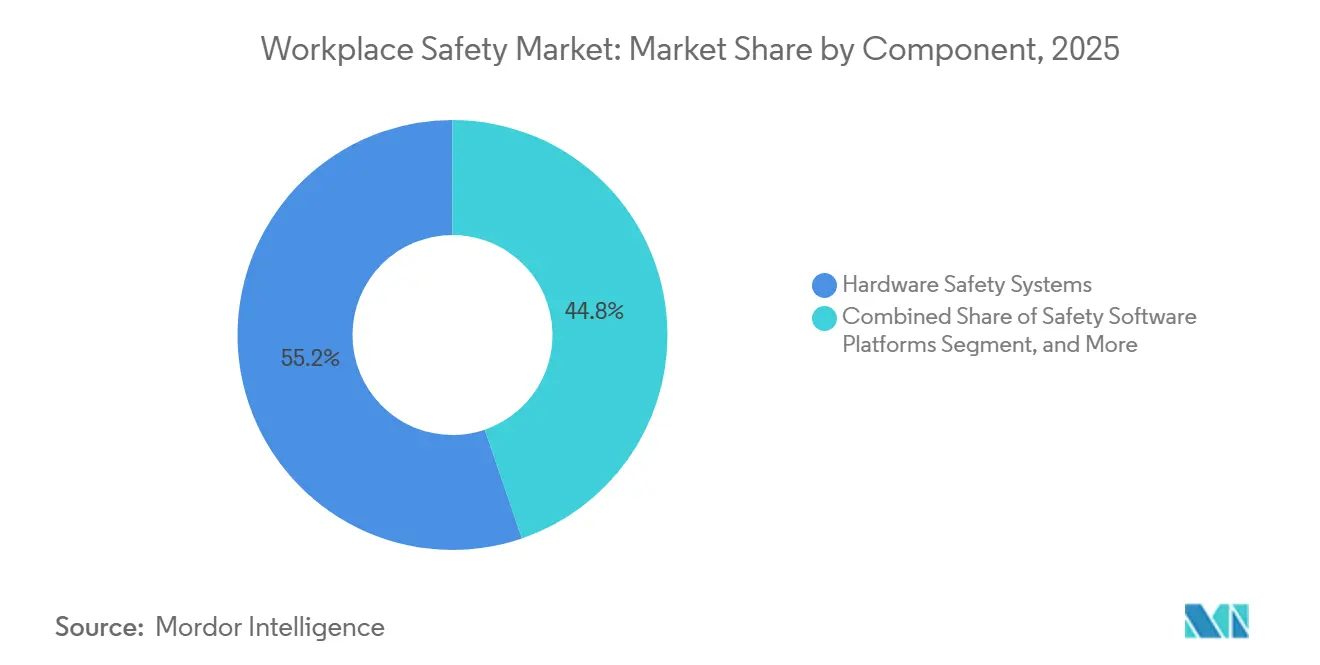

- By component, hardware safety systems led with 46.19% of 2025 revenue, whereas safety software platforms are expanding at a 12.28% CAGR and are the fastest component category through 2031.

- By technology, IoT and connected wearables accounted for 34.72% share of the workplace safety market size in 2025, and digital twins and simulation are projected to record the highest 12.33% CAGR to 2031.

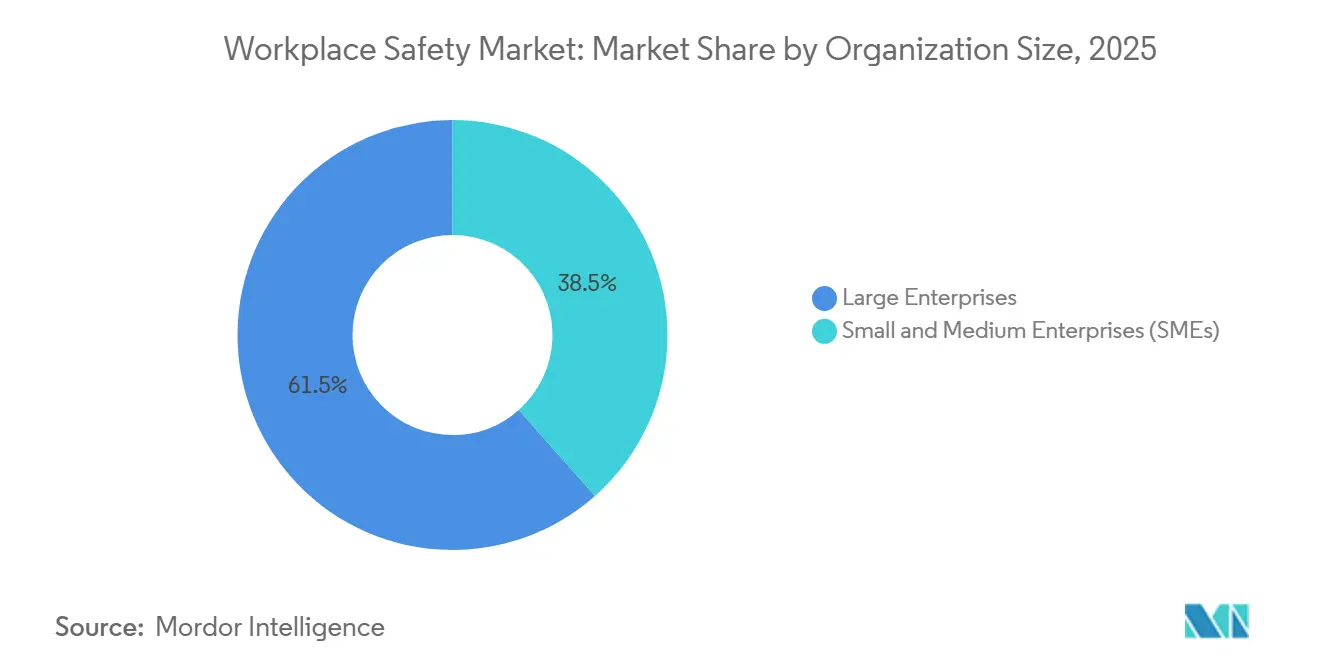

- By organization size, large enterprises held 61.53% of 2025 spending, but small and medium enterprises are forecast to grow at an 11.97% CAGR on the back of cloud-native EHS subscriptions.

- By end-use industry, manufacturing captured 23.72% of 2025 turnover, while healthcare is advancing at a 12.12% CAGR as the fastest-growing vertical through 2031.

- By region, North America retained 33.49% of global revenue in 2025, yet Asia-Pacific is set to expand at a 12.06% CAGR, the quickest regional pace to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Workplace Safety Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Tightening of Occupational Safety Standards | +2.5% | Global | Medium term (2-4 years) |

| Rising Workplace-Accident Costs and Liability Exposure | +2.0% | Global | Short term (≤ 2 years) |

| Expansion of High-Risk Industries in Emerging Economies | +1.8% | Asia-Pacific, Middle East and Africa, South America | Medium term (2-4 years) |

| ESG-Driven Investor Scrutiny Linking Safety Metrics to Financing | +1.5% | Global, primarily North America and Europe | Medium term (2-4 years) |

| Integration of AI-Enabled Vision Systems for Real-Time Hazard Detection | +1.3% | Global | Short term (≤ 2 years) |

| Adoption of Safety Digital Twins for Pre-Construction Risk Elimination | +1.0% | Global, primarily North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Tightening of Occupational Safety Standards

Governments are raising penalties and widening inspection rights, making continuous compliance a business necessity. OSHA increased its maximum fine for serious violations to USD 16,131 in 2026 and broadened its heat-illness National Emphasis Program to cover warehousing in addition to construction and agriculture.[1]Occupational Safety and Health Administration, “Penalty Adjustments and NEP Updates,” osha.gov The agency also reinstated its walkaround rule, granting union or third-party representatives the right to join inspections, which has lifted citation volumes. In Europe, the Corporate Sustainability Due Diligence Directive, which becomes effective in 2027, compels firms with more than 500 employees to audit tier-two suppliers, pushing safety accountability deep into global value chains. China’s 14th Five-Year Plan obliges coal mines to deploy IoT sensors and AI analytics by 2027, threatening license suspension for non-compliance.[2]State Council of the People’s Republic of China, “14th Five-Year Plan for Safety Production,” gov.cn These measures are catalyzing demand for unified EHS platforms that automate incident capture, corrective-action tracking, and audit reporting.

Rising Workplace-Accident Costs and Liability Exposure

Medical inflation and cumulative-trauma claims are lifting the price tag of accidents faster than general inflation. California recorded a 127% combined workers’ compensation loss ratio in 2025, signaling insurer payouts of USD 1.27 for every USD 1 in premiums.[3]California Department of Insurance, “Workers’ Compensation Loss Ratios,” insurance.ca.gov Liability carriers now embed safety-performance covenants that shave 10-15% off premiums for companies deploying connected wearables. Construction and oil and gas operators face settlement ranges of USD 5 million to USD 10 million for a single fatality, reinforcing the business case for exoskeleton pilots, ergonomic analytics, and near-miss predictive models.

Expansion Of High-Risk Industries in Emerging Economies

Rapid industrialization is concentrating labour in manufacturing, mining, and megaproject construction across India, Saudi Arabia, and Southeast Asia. India’s amended Factories Act raised maximum fines to INR 500,000 (USD 6,000) and mandated third-party audits for plants employing over 250 workers. Saudi Vision 2030 requires ISO 45001 certification and monthly dashboard submissions before milestone payments are released. Belt and Road contractors are rolling out AI video analytics on overseas sites to satisfy both host-nation rules and parent-company risk frameworks. Collectively, these forces are boosting hardware demand and accelerating the adoption of cloud-connected wearables in regions that traditionally relied on paper logbooks.

ESG-Driven Investor Scrutiny Linking Safety Metrics to Financing

Safety KPIs have become credit covenants. The Corporate Sustainability Reporting Directive obliges European issuers to disclose lost-time and total recordable incident rates with external assurance from 2026. Over USD 120 trillion in assets is now managed under the UN Principles for Responsible Investment framework, which classifies occupational health and safety as a material factor. Loan agreements penalize borrowers with above-median injury rates by 15-25 basis points, driving demand for real-time dashboards that feed boardrooms and lenders alike. Digital twins let executives visualize safety outcomes across multiple capex scenarios, adding quantitative rigor to spend approvals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Advanced Safety Technologies | -1.2% | Global, particularly SMEs | Short term (≤ 2 years) |

| Compliance Fatigue among SMEs from Fragmented Standards | -0.8% | Global | Short term (≤ 2 years) |

| Data-Privacy Concerns over Continuous Worker Monitoring | -0.5% | Europe, North America | Short term (≤ 2 years) |

| Shortage of Certified Industrial Hygienists and Safety Professionals | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Safety Technologies

Capital intensity deters smaller firms. Camera infrastructure, edge processors, and annual licenses push AI vision deployments to USD 50,000-150,000 per facility, while custom VR modules add USD 75,000-150,000 for 15-minute courses. UK data show SMEs must invest GBP 10,000-50,000 (USD 12,700-63,500), with payback periods longer than 3 years. Satellite connectivity for offshore rigs or remote mines can tack on USD 500-1,000 monthly, making SaaS wearables less economical outside cellular coverage. Vendors are countering with lease-to-own models and bundling insurance rebates, yet sticker shock remains a drag on broad uptake.

Compliance Fatigue Among SMEs From Fragmented Standards

Overlapping mandates sap management bandwidth. Exporters juggle OSHA rules, EU Regulation 2016/425, China’s GB 2626, and Japan’s Industrial Safety and Health Act, each with unique labelling and recertification cycles. The EU’s 2025 chemical reclassification forced relabelling of inventory, while ANSI R15.06-2025 harmonized cobot rules but left legacy machines under earlier standards. SMEs now allocate 15-20% of EHS budgets to tracking updates, crowding out funds for digital solutions. Voluntary ISO 45001 certification demands 12-18 months and USD 20,000-50,000 in audit costs, a hurdle many view as non-essential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Outpace Hardware Growth

Safety software revenue is rising at a 12.28% CAGR, even as hardware retained 46.19% of workplace safety market share in 2025. The pivot reflects insurer discounts for real-time incident dashboards and board demand for ESG-grade reporting. Personal protective equipment still moves the largest unit volumes, yet commoditization is pressuring margins, prompting suppliers to bundle analytics subscriptions with gear packages.

Enterprises favour unified SaaS suites that collapse incident logging, audit checklists, and corrective-action workflows into a single pane, replacing spreadsheets and siloed point tools. Hardware innovation continues in gas detection and machine guarding, but spending momentum is clearly with software, especially among cloud-ready SMEs. The workplace safety market size attached to services such as VR-based training and third-party audits is expanding steadily as mandates like New York’s 2026 workplace-violence law require recurring instruction.

By Technology: Digital Twins Lead the Innovation Wave

Digital twins and simulation applications are forecast for a 12.33% CAGR, edging past connected wearables that already held 34.72% share of 2025 revenue. Construction, oil and gas, and nuclear operators are leveraging virtual replicas to rehearse high-risk tasks, cutting crane collisions and maintenance errors before ground is broken. AI vision and IoT sensors remain foundational, feeding twin models with live data to refine predictive accuracy.

Cobots, now certified under ISO 10218 revisions, are penetrating electronics and automotive assembly lines to mitigate ergonomic stress, while VR and AR training modules deliver fourfold faster skill acquisition than classrooms. Emerging tools exoskeletons, drones, blockchain credentials are in pilot phases but underscore how the workplace safety market is evolving from static PPE toward intelligent, connected ecosystems.

By Organization Size: SMEs Accelerate Cloud Adoption

Large enterprises controlled 61.53% of outlays in 2025, yet SMEs will post the fastest 11.97% CAGR as subscription models strip out capex. Software vendors now ship wearables bundled with cellular data on monthly plans, letting mid-tier contractors scale devices with headcount.

Regulations in India and the UAE impose identical safety obligations on mid-market factories, narrowing the parity gap with multinationals. Insurance carriers reinforce adoption by linking premiums to digitized injury dashboards, converting safety spend into measurable ROI. The workplace safety market size for custom digital twins still tilts toward Fortune 500 giants, but SME accessibility is improving through low-code configurators and templated libraries.

By End-Use Industry: Healthcare Emerges as Growth Leader

Manufacturing delivered 23.72% of 2025 revenue, tapping AI vision for lockout-tagout compliance and robotic paint booths to mitigate chemical exposure. Healthcare, however, is racing ahead at a 12.12% CAGR, propelled by state and federal violence-prevention rules that require incident logging and de-escalation training. Construction remains the second-largest spender on fall-protection gear, proximity beacons, and BIM-integrated twins that flag hazards before crews mobilize.

Oil and gas outfits equip offshore teams with real-time gas detectors and predictive fatigue analytics, capping the cost of catastrophic events. Mining operators, under China’s 2027 IoT mandate, are fitting haul trucks with collision-avoidance radars and underground networks. Retail and hospitality trail in spending intensity but are rolling out basic mobile apps for slip-trip-fall reporting.

Geography Analysis

North America commanded 36.0% of workplace safety market share in 2024, supported by stringent OSHA oversight, mature insurance frameworks, and strong capital expenditure on automation. The January 2025 proper-fit PPE rule intensifies compliance workloads, keeping demand elevated for documentation platforms and audit-ready dashboards.[3]Occupational Safety and Health Administration, “Personal Protective Equipment in Construction,” osha.gov ESG integration into corporate finance reinforces investment, as lenders reward firms with low recordable-incident frequencies through reduced borrowing costs.

Asia-Pacific is the fastest-growing region at a 13.5% CAGR, propelled by rapid industrialization and government directives that align emerging markets with global norms. China’s August 2025 chemical classification standard and Singapore’s machinery hazard updates typify the region’s push for harmonization. Local enterprises, unburdened by legacy systems, leapfrog directly to AI-enabled monitoring, while policy incentives encourage deployment of connected-worker platforms in new factories.

Europe maintains steady expansion backed by the EU Machinery Regulation’s cybersecurity clauses and new exposure limits on lead and diisocyanates that protect 4.2 million workers. The EU AI Act’s governance rules favor vendors with robust compliance architectures, creating a premium for integrated platforms with auditable algorithmic transparency.

Competitive Landscape

Honeywell, 3M, MSA Safety, DuPont, and Ansell controlled around 35-40% of the 2025 workplace safety market share, reflecting a moderately consolidated core but fragmented software and services tiers. Portfolio reshuffles dominate strategy: 3M and Bain Capital folded Madison Fire and Rescue into Scott Safety for USD 1.95 billion, pivoting toward high-margin respiratory and fire gear. Platinum Equity scooped up Honeywell’s commodity PPE lines for USD 1.3 billion, allowing Honeywell to double down on connected devices and analytics.

MSA Safety grew Q4 2025 revenue 3% to USD 417 million on strength in the Americas and EMEA, offsetting flat Asia performance. Ansell’s 6% organic decline to USD 1.55 billion led it to launch cost-takeout projects under new CEO Neil Salmon. Growth pockets revolve around predictive analytics and cloud-connected wearables, where Guardhat and Blackline Safety posted double-digit gains by integrating gas detection, lone-worker alerts, and AI fatigue scoring into single dashboards.

Regulatory fluency and third-party certification are emerging differentiators. Vendors that preload jurisdiction-specific templates, multilingual training, and automated submission tools are winning Asia-Pacific and European tenders burdened by fragmented standards. ISO 45001 compliance now functions as a market passport, filtering out smaller suppliers that lack audit budgets. Hardware incumbents are infusing sensors, edge compute, and subscription models into traditional PPE, blurring historical lines between gear and software.

Workplace Safety Industry Leaders

Honeywell International Inc.

Siemens AG

ABB Ltd.

3M Company

Rockwell Automation, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: 3M and Bain Capital formed a joint venture, purchased Madison Fire and Rescue for USD 1.95 billion, merged it with Scott Safety, and refocused on respiratory and fire-safety equipment.

- March 2026: Honeywell introduced an AI control-room assistant that cut false alarms 40% in pilot oil and gas deployments.

- March 2026: EON Reality released Genesis 3.0, a cloud digital-twin platform for simulating chemical releases and structural failures.

- December 2025: New York adopted a workplace-violence prevention law for healthcare and social-service employers, effective Sep 2026.

Global Workplace Safety Market Report Scope

The Workplace Safety Market Report is Segmented by Component (Hardware Safety Systems, Personal Protective Equipment, Safety Software Platforms, Safety Services and Training), Technology (IoT and Connected Wearables, AI and Computer-Vision Analytics, Robotics and Cobots, VR/AR Training, Digital Twins, Other Technologies), Organization Size (Large Enterprises, SMEs), End-Use Industry (Manufacturing, Construction, Oil and Gas, Mining, Healthcare, Transportation and Logistics, Chemicals, Food and Beverage, Utilities, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware Safety Systems |

| Personal Protective Equipment (PPE) |

| Safety Software Platforms |

| Safety Services and Training |

| IoT and Connected Wearables |

| AI and Computer-Vision Analytics |

| Robotics and Cobots for Hazard Mitigation |

| Virtual / Augmented-Reality Training |

| Digital Twins and Simulation |

| Other Technologies |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Manufacturing |

| Construction |

| Oil and Gas |

| Mining |

| Healthcare |

| Transportation and Logistics |

| Chemicals |

| Food and Beverage |

| Utilities |

| Others End-Use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware Safety Systems | ||

| Personal Protective Equipment (PPE) | |||

| Safety Software Platforms | |||

| Safety Services and Training | |||

| By Technology | IoT and Connected Wearables | ||

| AI and Computer-Vision Analytics | |||

| Robotics and Cobots for Hazard Mitigation | |||

| Virtual / Augmented-Reality Training | |||

| Digital Twins and Simulation | |||

| Other Technologies | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-Use Industry | Manufacturing | ||

| Construction | |||

| Oil and Gas | |||

| Mining | |||

| Healthcare | |||

| Transportation and Logistics | |||

| Chemicals | |||

| Food and Beverage | |||

| Utilities | |||

| Others End-Use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the workplace safety market expected to grow between 2026 and 2031?

Mordor Intelligence projects an 11.58% CAGR for the workplace safety market over 2026-2031, lifting value from USD 23.87 billion in 2026 to USD 41.28 billion by 2031.

Which component category is expanding the quickest?

Safety software platforms are forecast to grow at a 12.28% CAGR, outpacing hardware systems through 2031, according to Mordor Intelligence.

Which end-use industry shows the highest growth potential?

The healthcare sector is projected to register a 12.12% CAGR through 2031, driven by new violence-prevention mandates, per Mordor Intelligence.

What region is set to record the fastest expansion?

Asia-Pacific is expected to post a 12.06% CAGR up to 2031 as China, India, and South Korea tighten safety enforcement, based on Mordor Intelligence research.

Who are the leading players in the workplace safety space?

Honeywell, 3M, MSA Safety, DuPont, and Ansell collectively hold about 35-40% of the global workplace safety market share, according to Mordor Intelligence.

Page last updated on: