Machine Safety Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.13 Billion |

| Market Size (2031) | USD 9.79 Billion |

| Growth Rate (2026 - 2031) | 9.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

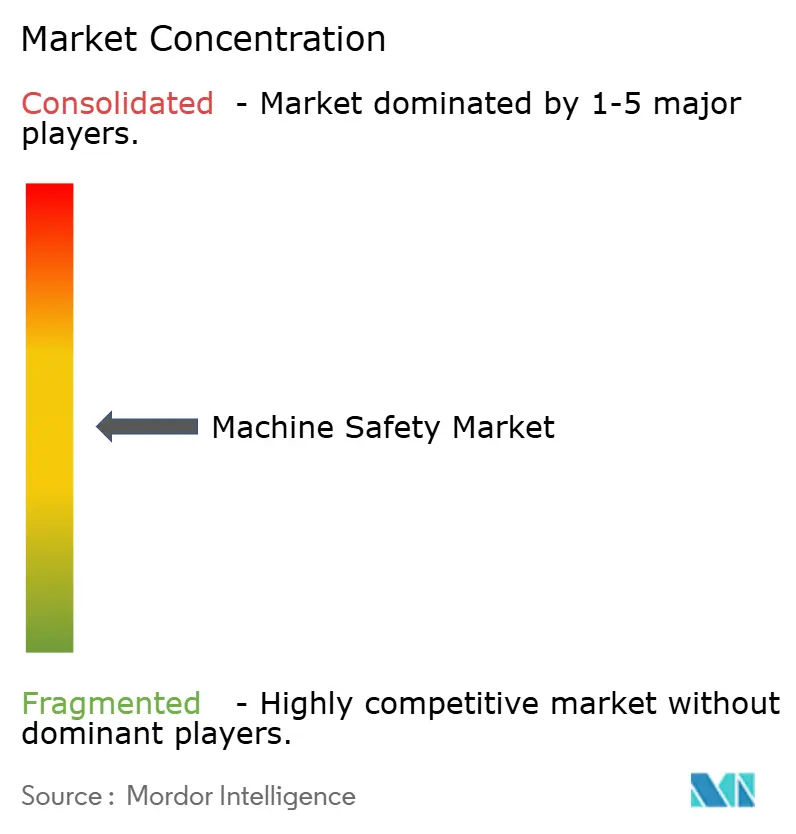

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Machine Safety Market Analysis by Mordor Intelligence

The machine safety market size was valued at USD 5.58 billion in 2025 and estimated to grow from USD 6.13 billion in 2026 to reach USD 9.79 billion by 2031, at a CAGR of 9.83% during the forecast period (2026-2031). Heightened regulatory pressure, rapid industrial automation and the growing convergence of functional-safety with cybersecurity are the core forces behind this growth. Europe’s upcoming Machinery Regulation 2023/1230 is compelling manufacturers worldwide to embed Performance Level e functions and to harden safety systems against digital threats ec.europa.eu. Asia-Pacific’s expanding electronics and automotive bases are accelerating demand for adaptive safeguarding, while North American food and beverage processors are pursuing digital retrofits that combine Industry 4.0 data flows with safety compliance automate.org. Vendors that can offer integrated safety PLCs, predictive-maintenance analytics and certified cyber-secure architectures are capturing share as end-users transition from hard-wired relays to software-defined safety logic.

Key Report Takeaways

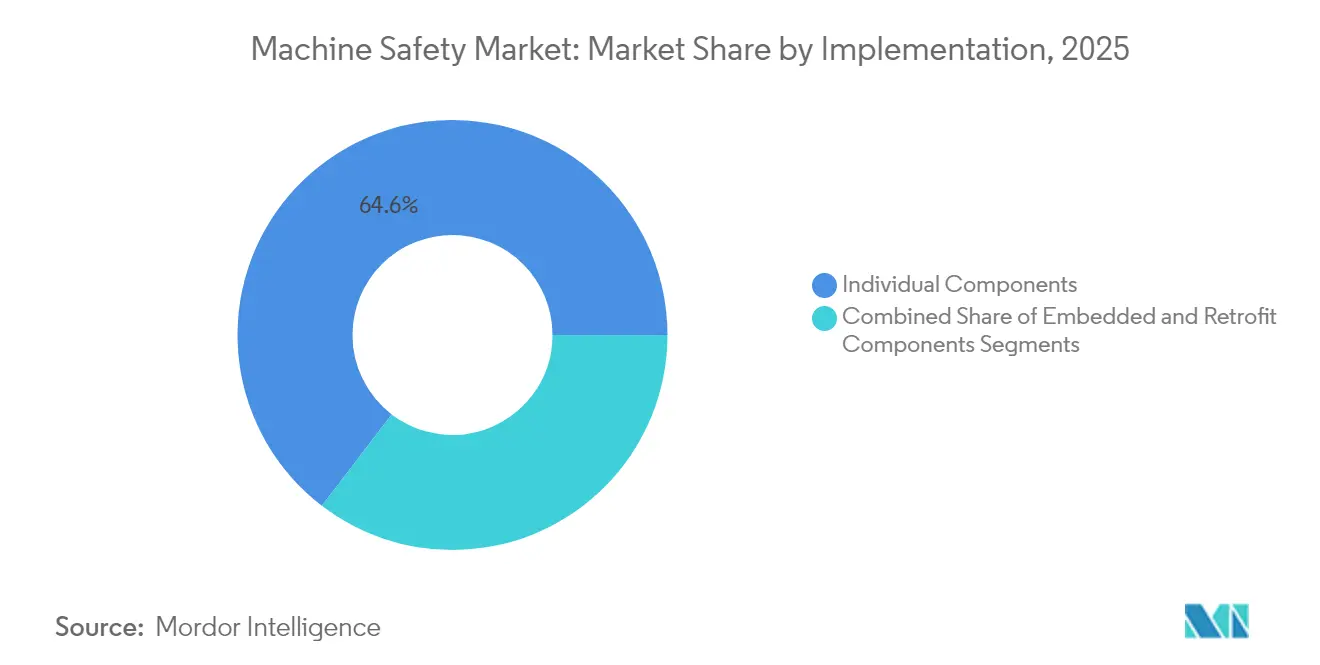

- By implementation, individual components led with 64.60% machine safety market share in 2025, while embedded components are set to expand at an 11.55% CAGR through 2031.

- By component, presence-sensing safety sensors held 29.50% of the machine safety market size in 2025; safety PLCs are projected to grow the fastest at a 12.3% CAGR to 2031.

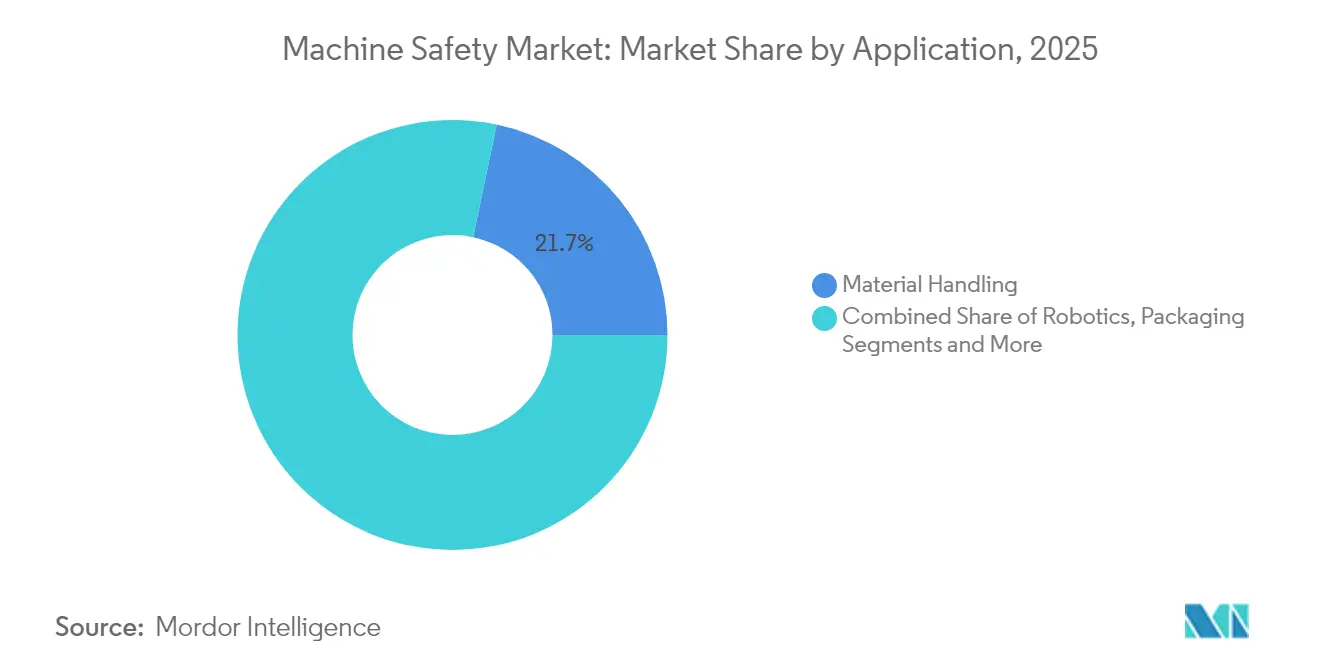

- By application, material handling commanded 21.70% of 2025 revenue, whereas robotics & collaborative robots are advancing at a 13.75% CAGR during 2026-2031.

- By end-use industry, automotive retained 23.60% share of the machine safety market in 2025; pharmaceuticals & healthcare show the highest growth at a 12.7% CAGR to 2031.

- By region, Europe dominated with a 30.70% share in 2025, while Asia-Pacific is expected to register an 11.35% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Machine Safety Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated Adoption of Collaborative Robots in Electronics Assembly Lines across East Asia | 2.2% | East Asia, with spillover to North America and Europe | Medium term (2-4 years) |

| EU Machinery Regulation 2023/1230 Mandating Performance Level e Safety Functions in New Equipment from 2027 | 2.5% | Europe, with global impact on exporters to EU | Long term (≥ 4 years) |

| Rapid Brownfield Digital Retrofit Programs in North American Food & Beverage Plants Incorporating Safety I/O-Link Sensors | 1.8% | North America, with adoption spreading to Europe | Medium term (2-4 years) |

| Surge in LNG Megaprojects in Middle East Elevating Demand for SIL-3 Rated Emergency Shutdown Systems | 1.5% | Middle East, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Rising Insurance Premium Penalties for Plant Injuries Above OSHA TRIR Thresholds Pushing US SMEs toward Category 4 Safety Solutions | 1.2% | North America, particularly United States | Short term (≤ 2 years) |

| Shift from Hard-wired Relays to Software-Configurable Safety PLCs Enabling Flexible Packaging Lines in Europe | 1.0% | Europe, with adoption spreading globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Collaborative Robots in Electronics Assembly Lines across East Asia

Electronics producers in China, South Korea and Taiwan are replacing isolated industrial robots with collaborative units that share workspaces with operators. Dynamic presence-sensing light curtains and 3D vision guard zones now stop cobots only when a person is at risk, lifting overall line productivity by 18% while cutting recordable incidents by 27%. AI-powered safety logic embedded in the robot controller enables speed-and-separation monitoring rather than hard stops, which further shortens cycle times. Component vendors supplying certified safety scanners, safe torque off drives and software-configurable PLCs are therefore experiencing outsized order growth from contract electronics manufacturers. The wave of cobot deployment is expected to peak over the next three years as electronics assemblers race to offset regional labor shortages and maintain export competitiveness.[1]Association for Advancing Automation, “Collaborative Robot Adoption Statistics 2025,” automate.org

EU Machinery Regulation 2023/1230 Mandating Performance Level e Safety Functions in New Equipment from 2027

The regulation, entering force on 20 January 2027, introduces legally binding PL-e requirements for critical functions and embeds explicit cybersecurity clauses that classify hacking-induced malfunction as a safety hazard. Machine builders supplying the EU must therefore validate that safety-related control parts withstand both random hardware faults and intentional attacks. This dual compliance need is fueling demand for integrated safety-security controllers and certified secure remote-update mechanisms. Because the rule applies directly without national transposition, suppliers can scale one architecture across all 27 member states, streamlining product-development pipelines. Preparatory spending on risk assessments, software patch management and digital-twin simulation is already evident among German and Italian OEMs looking to avoid last-minute redesigns.

Rapid Brownfield Digital Retrofit Programs in North-American Food & Beverage Plants Incorporating Safety I/O-Link Sensors

Processors of meat, dairy and beverages are combining safety upgrades with Industry 4.0 telemetry by swapping legacy wiring for I/O-Link-ready light curtains, interlock switches and pressure mats. The protocol’s bidirectional data let maintenance teams pull diagnostic health status, reducing unplanned downtime and shrinking changeover windows by 35%. Retrofit kits preserve older conveyors and fillers yet raise them to Category 3 or 4, helping operators avoid OSHA penalties linked to higher incident rates. The program model favors scalable investment: lines can be modernized cell-by-cell over planned shutdowns, minimizing capital shock while creating a digital foundation for later AI-driven predictive maintenance.

Surge in LNG Megaprojects in the Middle East Elevating Demand for SIL-3 Rated Emergency Shutdown Systems

Qatari and Emirati liquefaction trains valued at more than USD 150 billion are specifying triple-modular-redundant ESD controllers, intrinsically safe pressure transmitters and SIL-3 fire-and-gas loops. Contractors favor integrated platforms that unify process-control and safety-instrumented functions, simplifying proof-testing and spare-parts management. Standardized safety designs have cut nuisance trips by 42%, which previously cost operators millions of USD per hour in lost LNG export revenue. Given multiyear project schedules, suppliers of certified valves, logic solvers and field devices have line-of-sight to stable demand through 2030.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Integration Complexity of Safety Networks with Legacy Control Architecture in Brownfield Sites | -1.5% | Global, with higher impact in mature industrial markets | Medium term (2-4 years) |

| Capital Budget Freezes in Automotive Tier-2 Suppliers Amid EV Demand Volatility | -1.2% | North America, Europe, and East Asia | Short term (≤ 2 years) |

| Limited Skilled Workforce to Program Functional-Safety Software per IEC 61508/62061 in Emerging Markets | -1.0% | Asia-Pacific (excluding Japan and South Korea), Latin America, Middle East & Africa | Medium term (2-4 years) |

| Perception of Over-Engineering and ROI Uncertainty for Category-4 Safety Systems among Southeast-Asian SMEs | -0.8% | Southeast Asia, with spillover to other emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity of Safety Networks with Legacy Control Architecture in Brownfield Sites

Many 1980s-era distributed-control systems use proprietary buses lacking deterministic bandwidth for safety traffic. Integrators therefore resort to protocol gateways and shadow controllers, inflating project costs by up to 65% and extending commissioning windows. Continuous-process plants resist such downtime, opting for minimum-compliance fixes that slow the adoption of networked safety. Although vendors are releasing “plug-in” migration bridges and simulation-based validation tools, the structural mismatch between legacy hardware and modern functional-safety standards will persist until large-scale control-system overhauls occur.[2]MDPI Journal, “Challenges in Integrating Safety Networks with Legacy Systems,” mdpi.com

Capital Budget Freezes in Automotive Tier-2 Suppliers Amid EV Demand Volatility

Fluctuating EV order books have tightened liquidity for small metal-stamping and plastic-molding firms, prompting a 35% postponement of planned Category 4 safety upgrades in 2024-2025. While OEMs insist on adherence to ISO 13849, tier-2 suppliers are prioritizing immediate tooling changes over safety investments that lack short-term payback. Some federal and state subsidies cover robot adoption yet exclude ancillary safety hardware, further discouraging spend. As EV production forecasts stabilize, pent-up demand for collaborative-robot safeguarding and safe-motion drives could rebound, but the immediate effect is a drag on global market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Implementation: Embedded Components Gain Momentum

Individual components continued to dominate in 2025 with a 64.60% machine safety market share due to their plug-and-play compatibility with brownfield equipment. However, embedded components are forecast to outpace at an 11.55% CAGR as PLCs, drives and HMIs ship with integrated safety firmware, trimming cabinet space and wiring. Automotive body-in-white lines illustrate the trend: a single controller now hosts both standard motion profiles and PL-e interlock logic, eliminating duplicate processors. In electronics assembly, microcontroller-based safety co-processors handle reaction times below 10 ms, satisfying the machine safety market size requirement for high-speed pick-and-place equipment. Suppliers that certify combo-control chips under both IEC 61508 and ISO 26262 are positioned to capture OEM design wins as cost parity with discrete relays approaches.

The retrofit arena still favors discrete light curtains and interlocks because installers can swap hardware during weekend shutdowns without revalidating the base PLC code. Yet even here, “slice” I/O modules with dual-channel safety inputs are edging in, allowing cabinets to host standard and safety wiring on one backplane. Regulatory harmonization across Europe and the Americas is also tilting investment toward embedded solutions; once a safety CPU is certified, software changes can be field-downloaded rather than rewiring physical relays, delivering faster ROI especially in seasonal packaging operations.

By Component: Safety PLCs Drive Intelligent Protection

Presence-sensing safety sensors accounted for 29.50% of revenue in 2025, underpinning virtually every safeguarding scheme from press brakes to palletizers. Optical and radar variants now incorporate muting logic that differentiates payload from personnel, minimizing nuisance stops in conveyor systems. Safety PLCs represent the fastest-growing sub-segment at 12.3% CAGR because flexible manufacturing demands programmable zones and high-speed logic reconfiguration. The transition from hard-wired contacts to parameterized function blocks reduces electrical drawings by up to 60% and enables digital twins that validate changes before deployment.

Modern safety PLCs also embed secure-boot firmware and encrypted communications, satisfying the dual requirement of cybersecurity and functional safety posed by the EU Machinery Regulation. The machine safety market size for safety PLCs is further lifted by the migration of OEMs to unified control panels where one CPU executes both standard IEC 61131 tasks and SIL-3 diagnostics. Component suppliers are bundling pre-certified libraries for safe torque off, safe limited speed and safe position, shortening application development time for machine builders.

By Application: Robotics Revolution Reshapes Safety Paradigms

Material-handling lines held a 21.70% revenue share in 2025, reflecting the high density of conveyors, stackers and human pickers in warehouses and production logistics. Their continued dominance stems from standards such as ANSI B11.19 that prioritize access-prevention devices over emergency stops, driving steady purchases of safety fences, doors and muting sensors. Robotics & collaborative robots are slated to grow at a 13.75% CAGR, redefining safety architectures by requiring real-time monitoring of dynamic human-machine interaction zones. ISO 10218-2025 now obliges integrated functional-safety in robot controllers, accelerating orders for dual-processor servo drives that can switch to safe-limited speed within 10 ms.

Packaging & palletizing lines are also upgrading to light-grid scanners that automatically resize protected fields to match box height, eliminating manual resets between stock-keeping units and boosting uptime. In cutting, forming & machining, safety retrofits center on servo-presses where closed-loop safe-motion control replaces hydraulic overload clutches, yielding both energy savings and faster cycle times. As more machining centers integrate safe limited direction and safe brake control, the boundary between motion control and machine safety market continues to blur.

By End-Use Industry: Pharmaceutical Sector Accelerates Safety Innovation

Automotive remained the single largest consumer with 23.60% share in 2025, leveraging decades-long experience with robot guarding and lockout systems. Electric vehicle battery lines now introduce new hazards such as thermal-runaway risk during assembly, driving adoption of temperature-integrated safety interlocks. The pharmaceutical & healthcare segment, in contrast, is forecast to expand at a 12.7% CAGR as aseptic filling and high-potency drug compounding require glove-box isolators equipped with CAT 4 access control. Safety PLCs that interface with cleanroom HVAC to coordinate safe-vent modes are becoming standard.

Food & beverage processors are coupling hygienic design with safety by choosing stainless-steel light curtains rated to IP69K washdown, satisfying both USDA sanitation and functional-safety rules. Electronics and semiconductor fabs demand low-profile safety switches that withstand Class 10 cleanroom requirements, whereas oil & gas operators prioritize SIL-rated flameproof devices to prevent ignition in Zone 1 areas. Each vertical therefore exerts distinct specifications, yet all require verifiable documentation trails that cloud-based safety lifecycle platforms now automate.

Geography Analysis

Europe’s 30.70% share in 2025 underscores its role as regulatory pacesetter and automation pioneer. German automotive, chemical and machine-tool builders integrate networked safety backbones on virtually every new line, and 68% of installations already stream diagnostic data to central dashboards. Italian packaging OEMs export PL-e compliant fillers to North and South America, amplifying Europe’s technology spillover. The United Kingdom mirrors EU norms to protect export access, while French aerospace plants deploy collaborative-robot guarding to co-locate humans and robots in wing-assembly cells.

Asia-Pacific, projected to post an 11.35% CAGR, is the pivotal growth arena. China’s electronics assemblers rush to meet both domestic GB safety codes and CE marking for export, driving volume orders of light curtains and safe-motion drives. Japan’s robotics makers embed dual-channel torque sensors in arms, enabling built-in ISO 13849 compliance and boosting acceptance of humans and robots in shared workstations. India sees multinational pharma and automotive OEMs installing Category 3 and 4 systems at new greenfield sites, lifting local awareness and triggering supplier localization. South Korean chip fabs procure SIL-rated valve-manifolds for ultrapure chemical lines, combining functional-safety with low-particulate construction to safeguard both personnel and wafers.

North America remains a technology leader, yet growth is steadier. US processors upgrade safety to mitigate liability and insurance costs, with 42% of food plants planning major modernizations in 2025. Canada’s mining sector adopts wireless SIL-3 emergency-stop networks for haul-truck corridors. Latin American adoption is uneven: Brazil’s automotive clusters align with EU and US customer mandates, whereas smaller factories delay investments. The Middle East & Africa region expands fastest in high-risk energy sectors, installing integrated fire-and-gas plus ESD systems at refineries and LNG terminals.

Regulatory Landscape

Machine safety demand is anchored by functional-safety and cybersecurity compliance obligations across major industrial regions. In the European Union, Regulation (EU) 2023/1230 replaces the Machinery Directive 2006/42/EC and shifts machinery compliance to a directly applicable regulation across all 27 member states, tightening expectations for safety-related control systems and documentation practices. Full mandatory application begins on 20 January 2027, while parts of the framework have applied since 20 January 2024, including processes around notifying conformity assessment bodies, which has pushed earlier design and documentation updates among machine builders supplying the EU market.

In North America, OSHA continues to shape machine-guarding enforcement through rulemaking and standards-aligned guidance, alongside broader workplace safety updates that affect guarding, markings, and audit requirements in manufacturing sites. OSHA scheduled informal public hearings beginning 19 August 2026 for a large set of proposed rules, reinforcing compliance planning cycles for end users and integrators. Taken together, these regulatory signals increase the value of pre-certified safety components (SIL/PL-rated sensors, controllers, and drives) and software tooling that supports risk assessment, validation, and traceable change control.

Value Chain Analysis

The machine safety value chain runs from sensor and semiconductor inputs (optoelectronics, radar/ultrasonic transducers, safety-rated ICs) through device OEMs producing presence-sensing sensors, interlocks, E-stops, safety relays/modules, safety PLCs, and safe-motion drives, then to system integrators and OEM machine builders that engineer safety functions and document for end users. Distribution typically splits between direct enterprise sales for multi-site manufacturers and channel partners for retrofit-heavy SMEs, with lifecycle services (risk assessment, validation, training, and periodic proof testing) increasingly bundled into projects as plants migrate from hard-wired relay architectures to software-configurable safety PLCs.

Certification and standards compliance act as gates at multiple tiers, influencing procurement and shortening integration cycles when components are pre-qualified to SIL/PL targets. Recent component-level certification milestones, such as Sonair’s ADAR One 3D ultrasonic sensor reaching SIL 2 and PL d for human-robot collaboration use cases in July 2026, show how upstream vendors are positioning drop-in devices to reduce validation burden in cobot cells. On the demand side, brownfield modernization programs in sectors like food and beverage prioritize retrofit kits and diagnostic-ready devices, including I/O-Link-capable safety sensors, pulling more value toward integrators and software layers that can connect safety events to maintenance workflows while meeting audit requirements.

Competitive Landscape

The top five providers—Rockwell Automation, Siemens, Schneider Electric, Omron and Sick AG—hold roughly 45% global revenue, illustrating a moderately concentrated field where scale in R&D, certification and global distribution matters. Hardware breadth alone no longer differentiates; software ecosystems that automate risk assessment, configuration and validation are emerging as decisive factors. Leading vendors bundle cloud-based digital twins that model stop-time graphs and reachable distances, cutting design cycles by 30%.

Strategic moves center on combining functional-safety with cybersecurity. Siemens’ new safety PLCs ship with secure-boot, encryption and anomaly detection, meeting both PL-e and IEC 62443, thus addressing EU machinery mandates in one SKU. ABB’s acquisition of Sick’s machine-vision arm positions it to deliver safety-rated 3D vision for collaborative robots, a high-growth niche. Niche players such as Pilz and Fortress Safety differentiate through specialized interlock architectures and cloud-based documentation that reduce auditing overhead.

Pricing pressure persists in emerging markets where smaller factories demand “right-sized” solutions. To defend margins, global suppliers leverage modular designs and localized assembly to cut delivery costs. Meanwhile, software-centric entrants offer functionally safe plug-ins for mainstream PLC platforms, threatening hardware incumbents unless they open APIs or forge partnerships. The competitive intensity is therefore shifting from component specs toward lifecycle-service wrappers and secure interoperability.

Machine Safety Industry Leaders

Rockwell Automation, Inc.

Siemens AG

Schneider Electric SE

Omron Corporation

Sick AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace sits at the intersection of functional safety, connected machinery, and cybersecurity-focused compliance, where end users are standardizing on architectures that pair safety integrity with secure communications, update mechanisms, and evidence trails. EU-driven timelines provide concrete pull, with the Machinery Regulation 2023/1230 reaching full application on 20 January 2027. Industry guidance around connected equipment is also moving, including VDMA communication that from 1 July 2026, network-connected CNC systems placed on the EU market must align with DIN EN ISO 13849-1:2026 targets, including Performance Level considerations. This is expanding opportunities for vendors that package safety PLCs, safe drives, and networked sensors with tooling for PFH calculation, validation, and documentation suited to digital-first workflows.

Collaborative robotics and high-mix automation are also creating room for differentiated sensing and safety logic beyond traditional light curtains and interlocks. Evidence of this shift includes Sonair’s July 2026 announcement that its ADAR One 3D ultrasonic sensor achieved SIL 2 and PL d ratings aimed at human-robot collaboration, indicating supplier investment in alternative modalities for dynamic safeguarding. In parallel, standards updates and technical publications such as ISO/TR 13849-3:2026, published March 2026, add more rigorous methods including Markov-model-based approaches for reliability calculations. This tends to favor engineering software and pre-certified function blocks that reduce integration complexity in brownfield sites and shorten commissioning time for robotics, packaging, and material-handling applications.

Recent Industry Developments

- July 2026: Schneider Electric announced a definitive agreement to acquire Cognite for USD 3.1 billion, adding an industrial data and AI software platform to its automation portfolio. The deal strengthens software-layer differentiation that connects operational data, safety events, and compliance documentation in multi-site industrial environments.

- May 2026: Omron signed a strategic collaboration agreement with Comau to deploy industrial automation solutions across electronics, semiconductors, and medical manufacturing. The partnership supports higher-density automation deployments where integrated safeguarding, safety-rated sensing, and validated control architectures become critical to scaling cobot and robotics cells.

- May 2025: Rockwell Automation launched the GuardLogix 6000 safety controller platform with integrated cybersecurity features designed to address EU Machinery Regulation 2023/1230 requirements. The launch aligns safety PLC upgrades with cyber-secure architectures, supporting migration from hard-wired relays toward software-defined safety in new-build and retrofit projects.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The machine safety market is defined as the revenue generated from dedicated safety products that help prevent or reduce machine-related injuries and unplanned downtime in industrial settings, mainly by sensing hazards, stopping motion, and controlling safe operation.

Scope exclusions: Standalone programmable safety systems and two-hand safety controls are treated outside this market scope.

Segmentation Overview

- By Implementation

- Individual Components

- Embedded Components

- Retrofit Safety Upgrades

- By Component

- Presence-Sensing Safety Sensors

- Safety Light Curtains

- Safety Laser Scanners

- Emergency Stop Devices

- Safety Interlock Switches

- Safety Controllers / Modules / Relays

- Safety PLCs

- Two-Hand Controls and Enabling Switches

- Other Components (Mats, Edges, Bumpers)

- By Application

- Material Handling

- Robotics and Collaborative Robots

- Packaging and Palletizing

- Cutting, Forming and Machining

- Assembly and Pick-and-Place

- By End-Use Industry

- Automotive

- Food and Beverage

- Electronics and Semiconductor

- Oil and Gas

- Pharmaceuticals and Healthcare

- Chemicals

- Metals and Mining

- Aerospace and Defense

- Packaging Industry

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the basic market frame and to gather consistent reference data that can be checked by anyone. We reviewed public materials such as the International Labor Organization (ILO) safety statistics, OSHA guidance and incident reporting references, Eurostat manufacturing indicators, and national statistics on industrial production and employment (including the US Census Bureau series). We also cross-checked standards and compliance signals from bodies such as ISO and IEC, so adoption assumptions align with how plants certify and operate equipment.

On the supply and trade side, we used sources such as UN Comtrade and customs releases to understand cross-border movement patterns for relevant categories, and we reviewed patents and technical publications to track where sensing and control technologies are heading. We also examined company filings, annual reports, investor presentations, and reputable industry press to map product availability and pricing direction. For areas where public disclosure was thin, select paid subscriptions for company financials and patent databases were used to speed up company-level validation. The sources listed here are illustrative only, and many other public references were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with automation and safety practitioners, distributors, system integrators, and end users across discrete manufacturing and process environments. We used these discussions to confirm what is typically purchased together (sensor to controller to actuation), how replacement cycles behave in practice, and how pricing changes when standards, audits, or automation upgrades accelerate demand across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 53% |

| Mid tier: 49% | Functional/Unit leaders: 41% | EMEA: 29% |

| Smaller Players: 18% | Managers: 47% | Americas: 18% |

Market-Sizing & Forecasting

Our sizing starts from a top-down demand pool build that ties machine safety spending to industrial automation activity, compliance intensity, and the installed base of machinery that needs safeguarding. Country totals are reconstructed using a mix of manufacturing output, machinery shipments, and sector employment indicators, then adjusted using primary feedback on safety adoption levels and typical protection architectures.

To keep the totals realistic, we corroborate results with selective bottom-up approximations, such as sampled average selling price ranges for key component groups and volume proxies from channel checks and publicly visible product mix. Inputs that commonly move the model include automation capex trends, plant retrofit versus greenfield split, safety standard enforcement cycles (including audit frequency), replacement and maintenance cadence for sensors and interlocks, and the ramp of robotics and collaborative cells that require additional safeguarding. Where local data is missing, gaps are handled by using proxy industries with similar machine intensity, then normalizing with expert interviews before figures are finalized.

For forecasting, scenario analysis is used so adoption can be flexed under different manufacturing output paths and compliance tightening speeds, and then refined by expert consensus on how quickly safety upgrades will be bundled into broader controls modernization. The outcome is a repeatable value model that can be traced back to practical indicators rather than narrative expectations.

Data Validation & Update Cycle

Validation is done through multiple checks so the final numbers do not rely on a single signal. We compare outputs against independent indicators such as manufacturing production direction, automation investment tone, and observed pricing movement for common safety components, then investigate outliers at the country and regional levels.

Before sign-off, the model and assumptions go through step-by-step analyst reviews, and respondents are re-contacted when a variance cannot be explained by visible demand drivers. Reports are refreshed annually, and interim updates are added when major regulatory shifts, macro events, or large demand shocks materially change the outlook. Right before delivery, a final review pass is performed so clients receive the most current view available.

Mordor Intelligence's Machine Safety Market Estimate Compared With Other Published Estimates

Published market sizes for machine safety often do not match because each study draws the line differently on what counts as a safety product and how the demand pool is built across industries and regions. Differences also come from base year selection, currency conversion timing, and whether the forecast assumes a steady replacement market or a faster retrofit wave.

Two-hand safety controls sit outside Mordor Intelligence's machine safety scope, and that exclusion can shift totals when other publishers bundle them into broader safety component revenue, along with related programmable safety categories. The spread can widen further when some estimates apply a uniform growth rate to the whole market, instead of tying adoption to indicators such as manufacturing output, robotics expansion, and audit-driven retrofit cycles that were validated through interviews.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.13 B (2026) | |

| Regional Consultancy A | USD 6.14 B (2025) | Uses a different base year and may include adjacent safety categories under a broader component bucket, which changes the starting value before forecasting. |

| Industry Research Group B | USD 5.59 B (2024) | Earlier base year and limited visibility on explicit inclusions and exclusions, which can undercount retrofit driven demand and regional mix effects. |

The table shows that year selection and scope boundaries explain most of the gap, and the remaining difference usually comes from how fast retrofit adoption is assumed to rise. By keeping the model tied to observable manufacturing and automation signals, then pressure-testing assumptions through primary feedback, we get a balanced market size that can be recreated and checked.

Key Questions Answered in the Report

What is the current size of the machine safety market?

The machine safety market stands at USD 6.13 billion in 2026 and is projected to reach USD 9.79 billion by 2031 at a 9.83% CAGR.

Which region leads the machine safety market?

Europe holds the largest regional share at 30.70% in 2025 thanks to stringent regulations and a mature automation base.

Which segment is growing the fastest?

Safety PLCs are the fastest-growing component segment, expanding at a 12.3% CAGR between 2026 and 2031.

How does the EU Machinery Regulation 2023/1230 affect suppliers?

Suppliers must implement Performance Level e functions and cybersecurity safeguards, increasing demand for integrated safety-security controllers

Why are collaborative robots influencing machine safety investments?

Cobots require dynamic, programmable safety systems that allow humans and robots to share workspaces, boosting orders for advanced sensors and safety PLCs.

What is driving machine safety upgrades in North-American food plants?

Digital retrofit programs using I/O-Link sensors enable real-time diagnostics, reduce changeover times by 35% and help meet OSHA compliance, encouraging rapid adoption.

Page last updated on: