Cosmetovigilance Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 11.90 Billion |

| Market Size (2030) | USD 15.10 Billion |

| Growth Rate (2025 - 2030) | 4.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosmetovigilance Market Analysis by Mordor Intelligence

The cosmetovigilance market size reached USD 11.9 billion in 2025 and is projected to increase to USD 15.1 billion by 2030, representing a 4.90% CAGR over the forecast period. Rising regulatory scrutiny following the United States' Modernization of Cosmetics Regulation Act of 2022 (MoCRA), parallel tightening in the European Union under Regulation EC 1223/2009, and China’s new May 2025 safety-dossier mandate have prompted manufacturers to adopt always-on safety monitoring rather than episodic compliance checks. Contract outsourcing, social media data mining, and AI-powered signal detection now form the core pillars of growth as companies race to meet 15-day adverse-event reporting deadlines while extracting insights from consumer-generated content. Smaller brands that once viewed compliance as optional are adopting outsourced platforms that bundle blockchain traceability, real-world evidence collection, and global database connectivity. Simultaneously, liability insurers are writing stricter wording into product-recall coverage, prompting proactive safety analytics investments that increasingly differentiate bids in retail and private-label negotiations.

Key Report Takeaways

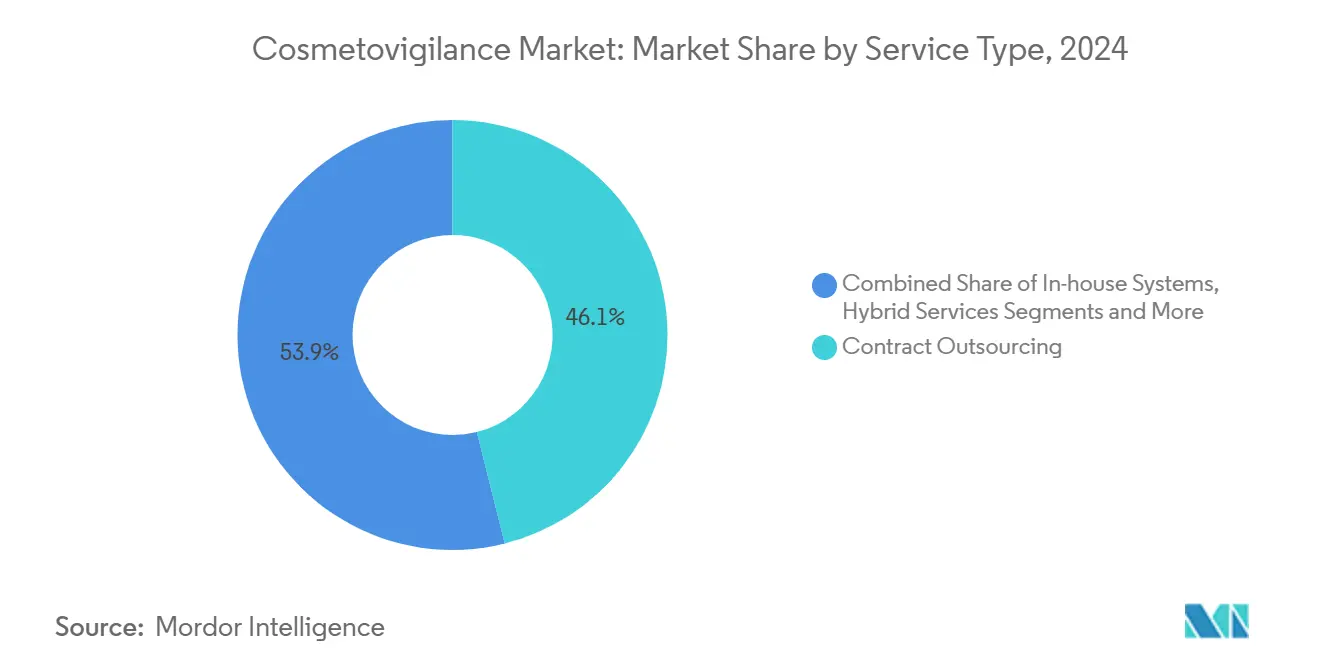

- By service type, contract outsourcing held 46.1% of the cosmetovigilance market share in 2024, while hybrid/co-managed models are forecast to expand at a 4.2% CAGR through 2030.

- By reporting method, spontaneous consumer submissions accounted for 52.3% of the cosmetovigilance market size in 2024; social-media and real-world data mining is set to grow at a 5.4% CAGR to 2030.

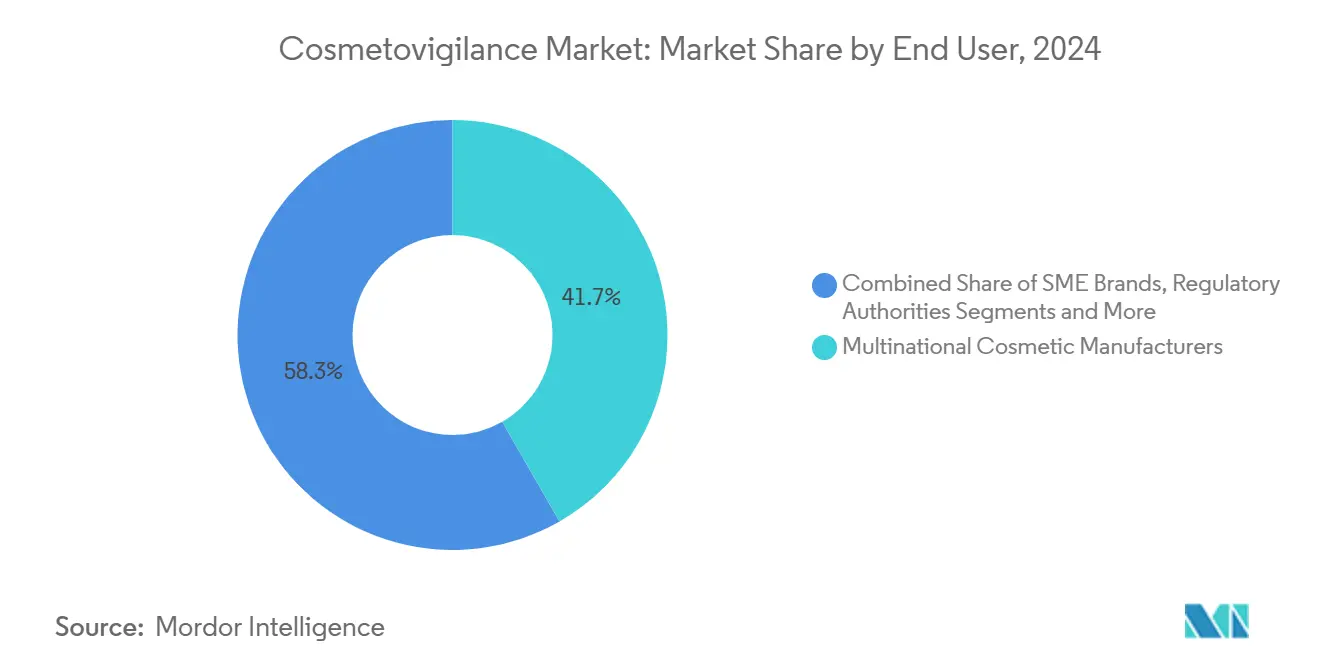

- By end user, multinational manufacturers commanded 41.7% revenue share in 2024, whereas small and medium brands are advancing at a 5.1% CAGR during 2025-2030.

- By application, skin-care monitoring represented 38.9% of the cosmetovigilance market size in 2024, while CBD and nano-cosmetics are projected to rise at a 4.6% CAGR through 2030.

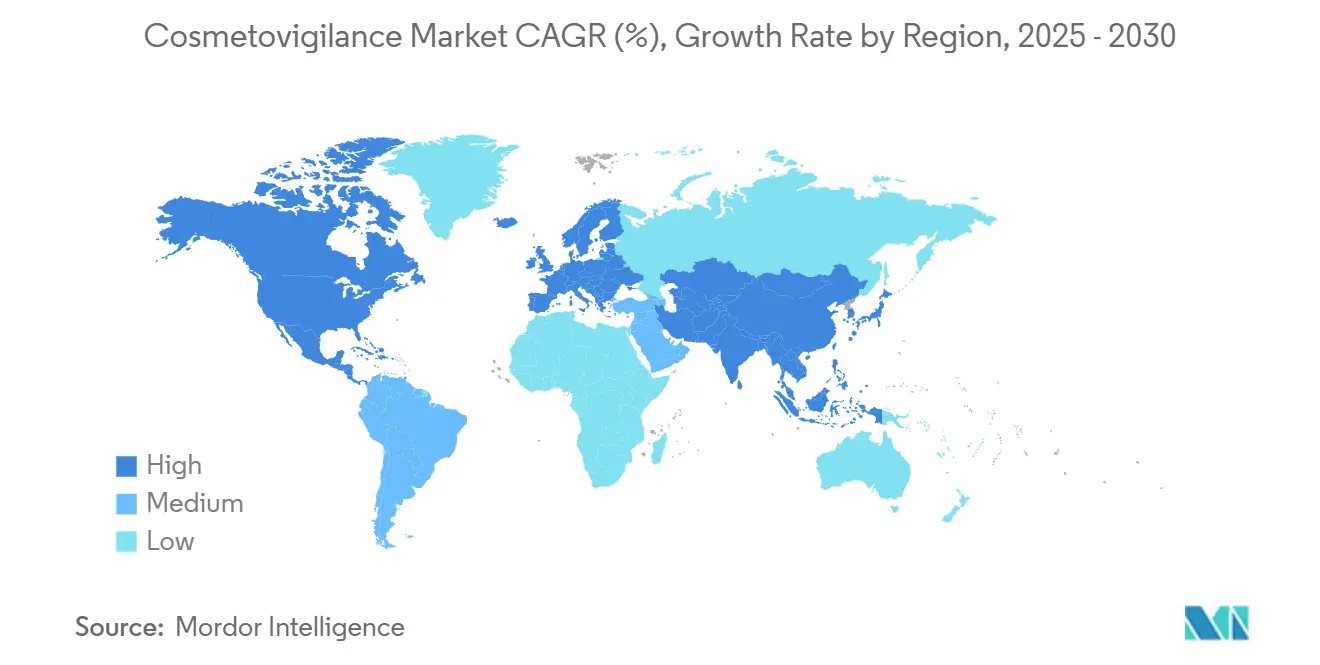

- By geography, Europe led with 33.7% of cosmetovigilance market share in 2024, while Asia Pacific posted the fastest growth, with a 5.6% CAGR projected through 2030.

Global Cosmetovigilance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global post-market surveillance | +1.20% | North America, EU first movers, global ripple | Medium term (2-4 years) |

| Rising incidence & reporting of adverse events | +0.80% | Developed markets with dense digital penetration | Short term (≤ 2 years) |

| Boom in clean/vegan/organic launches | +0.60% | North America, EU core, expanding into APAC | Long term (≥ 4 years) |

| AI-enabled early-warning analytics | +0.40% | Digital-ready regions | Medium term (2-4 years) |

| Blockchain anti-counterfeit integration | +0.40% | High-counterfeit corridors in LATAM & APAC | Long term (≥ 4 years) |

| Insurer-driven liability controls | +0.30% | North America, EU gradually global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Cosmetic-Safety Regulations & Post-Market Surveillance Mandates

Global regulators have synchronized major updates, leaving little room for staggered compliance. MoCRA in the United States compels every facility—domestic or foreign—to register, list products, and transmit serious adverse events within 15 business days.[1]U.S. Food and Drug Administration, “Modernization of Cosmetics Regulation Act: Frequently Asked Questions,” fda.gov The European Union simultaneously tightened nanomaterial disclosure rules, demanding detailed safety dossiers for all nano-enabled formulations. China’s May 2025 safety-assessment file requirement extends comparable rigor to the world’s second-largest beauty market, eliminating former leniencies for “general cosmetics”. Taiwan adopted an EU-style restricted ingredient list in July 2024, underscoring converging global standards. This alignment forces brands to implement unified, cloud-based safety databases capable of country-specific extracts while preserving a single source of truth for auditors and customs authorities.

Rising Incidence & Reporting of Adverse Cosmetic Events

Digital platforms have turned consumers into frontline safety sentinels. FDA’s CAERS database shows a year-over-year jump in cosmetic adverse-event filings after MoCRA publicity, but still captures only a fraction of social-media complaints. Studies reveal that reports on X (formerly Twitter) surface trends days before formal submissions, prompting agencies to test natural-language models that triage posts with dermatological keywords. Clinics corroborate the under-recognition gap; a UAE pilot logged a 1.58% incidence of cutaneous reactions, identifying shampoos as the top culprit, yet fewer than one-third of incidents reached national authorities. Brands now mine public posts for signal detection, but the flood of anecdotal stories introduces noise that can mask genuine toxicity signals without algorithmic filtering.

Boom in Clean/Vegan/Organic Product Launches Requiring Tighter Safety Oversight

Clean beauty brands position formulations as safer by excluding perceived “toxins,” yet regulators increasingly demand proof. Washington State’s Toxic-Free Cosmetics Act, effective January 2025, bans lead and 13 other substances, while California, Colorado, and Minnesota prohibit intentional PFAS in beauty products. Europe’s chemical agency found that 6.4% of cosmetics surveyed still contained hazardous substances, highlighting the compliance gap even in mature markets.[2]EcoMundo Editorial Team, “Cosmetics Compliance: Closing Regulatory Gaps to Ensure Safety and Sustainability,” EcoMundo, ecomundo.eu Because botanical extracts and bio-derived preservatives have scant historical toxicology, brands must conduct post-launch surveillance to spot sensitization trends. Litigation risk rises as class actions challenge “all-natural” claims, incentivizing early signal detection to pre-empt recalls.

AI-Enabled Signal Detection for Early-Warning of Adverse Events

Regulators now encourage artificial-intelligence augmentation rather than resist it. FDA’s January 2025 draft guidance outlines risk-based validation of machine learning across product lifecycles, opening the door for neural networks that parse social chatter, electronic health records, and unstructured call-center logs. Large language models reach F1-scores of 0.978 when spotting drug-induced liver injury within labeling documents, illustrating potential uplift in cosmetic surveillance where narrative descriptions dominate. Early adopters such as Spore. Bio uses AI to quantify microbial loads in finished goods, alerting quality managers long before standard plate counts are complete. Adoption hurdles include infrastructure cost and governance safeguards to prevent hallucinated signals, but pilots show reduced case-assessment cycle times and better triage accuracy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Under-reporting & low awareness of reporting channels | –0.7% | Higher in emerging markets | Short term (≤ 2 years) |

| High implementation cost for SMEs | –0.5% | Global, acute in developing regions | Medium term (2-4 years) |

| Lack of harmonized global coding & database interoperability | –0.4% | Fragmented across all regions | Long term (≥ 4 years) |

| Regulatory ambiguity around “cosmeceuticals” definitions | –0.3% | Jurisdiction-specific discrepancies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Under-Reporting & Low Consumer Awareness of Reporting Channels

Even where online portals exist, many mild reactions never convert into formal reports. FDA still accepts fax and mail submissions, signaling uneven digital maturity. Healthcare practitioners rarely connect dermatitis flares with cosmetic use, leaving early indicators unrecorded in electronic medical records. Media coverage spikes can skew perceptions by temporarily inflating complaint volumes for high-profile products, complicating baseline trend analysis. Emerging-market consumers face language barriers and limited internet access, further thinning data streams. Without sustained public-health campaigns, under-reporting will persist, constraining the feedback loop that underpins timely regulatory intervention.

High Implementation Cost for SMEs

EU conformity checks, safety assessments, and periodic audits absorb more than 20% of total product costs for smaller exporters, according to USITC estimates.[3]U.S. International Trade Commission, “Trade Barriers Affecting U.S. SME Exports to the EU,” usitc.gov MoCRA offers a narrow small-business exemption capped at USD 1 million in annual sales. Yet, many independent labels now surpass that threshold through online channels, pushing them into full compliance without the scale to amortize overhead. Outsourcing mitigates complexity but carries subscription fees for AI dashboards, traceability modules, and multilingual case processing. Venture funding helps offset early spending, but profitability remains sensitive to shifting rule interpretations across markets. As a consequence, some SMEs limit geographic expansion, dampening overall growth until cost curves decline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Outsourcing Dominates Safety Expertise

Contract outsourcing accounted for 46.1% of cosmetovigilance market revenue in 2024. Multinationals historically ran in-house safety teams, but rising data-science requirements for AI, blockchain, and cross-border regulatory filing encourage blended models. In 2025, SGS deepened clinical testing reach by acquiring IEC, enabling combined lab and adverse-event case processing under one contract, a template many mid-tier players now emulate.

Enterprises opting for hybrid arrangements retain brand risk oversight while offloading technical sub-tasks such as natural-language model training or EU Cosmetic Product Safety Report updates. This flexibility underpins a 4.2% CAGR projection, positioning hybrid offerings to bridge the price gap between full outsourcing and building proprietary capability. Conversely, pure in-house teams persist mainly at top-five global beauty groups that already integrate pharmacovigilance, medical affairs, and cosmetovigilance under shared governance.

By Reporting Method: Digital Transformation Accelerates

Spontaneous consumer submissions still dominate, accounting for 52.3% of the cosmetovigilance market share in 2024. However, social-media mining and real-world evidence extraction are expanding fastest, harnessing a 5.4% CAGR through 2030. Brands link listening tools to safety databases so that a TikTok post mentioning “rash” plus a product name auto-generates a preliminary case file. FDA’s development of electronic Structured Product Labeling (eSPL) for MoCRA reporting further nudges companies toward API-enabled pipelines.

Active surveillance—post-marketing epidemiological studies—remains mandatory for high-risk formats such as aerosol sprays and tattoo pigments. Pharmacies and dermatology clinics supply richer clinical detail than consumer narratives, balancing signal accuracy. Yet the long tail of mild irritation reported online increasingly influences formulation tweaks, ingredient substitutions, and even marketing claims.

By End User: SME Growth Outpaces Multinationals

Large enterprises still underpin the cosmetovigilance market, but SMEs post the most rapid gains. The segment’s 5.1% CAGR stems from rising DTC indie brands leveraging cloud-based safety portals previously affordable only to conglomerates. Outsourcers now offer tiered packages that embed multilingual chatbots, blockchain batch traceability, and auto-translated EU Safety Data Sheets.

Regulatory agencies also constitute a modest but growing user subset. China’s NMPA publishes periodic summary analyses that guide ingredient bans and testing priorities, sourcing data directly from manufacturer submissions. Dermatology clinics and hospitals, while crucial for severe cases, under-report due to unfamiliarity with cosmetic causality chains, a gap that collaborative education programs aim to close.

By Application: Emerging Segments Drive Innovation

Skin-care monitoring dominates because of the category’s large volume and direct skin contact, representing 38.9% of the cosmetovigilance market size in 2024. Color cosmetics and hair products follow, but the most pronounced innovation occurs in CBD and nano-enabled formulas. Regulatory grey zones around cannabidiol claim substantiation oblige post-market tracking of dermal absorption and sensitization indices.

Nanocosmetics have unique physicochemical behavior; EU rules demand separate exposure assessments for each nanoingredient, thereby triggering bespoke safety protocols. Blockchain paired with spectroscopy now let’s labs confirm nanoparticle identity from supply to shelf, supporting dossier submissions to the EU’s Cosmetic Product Notification Portal and China’s ingredient registry. Such specialized workflows underpin the category’s forecast of 4.6% CAGR.

Geography Analysis

Europe led the cosmetovigilance market with 33.7% in 2024, driven by the mature post-market surveillance requirements outlined in Regulation EC 1223/2009. Continuous updates—such as mandatory digital Product Information Files and heightened labeling of nanomaterials—sustain demand for high-end safety consultancies. Brexit introduced dual systems; companies now file Serious Undesirable Effects separately with the UK’s Office for Product Safety and Standards while maintaining EU CPNP entries, doubling the administrative workload. The forthcoming EU Product Liability Directive, effective December 2026, enlarges disclosure obligations, compelling earlier hazard identification to pre-empt litigation.

Asia-Pacific records the fastest regional expansion at a 5.6% CAGR. China’s May 2025 dossier rule equalizes scrutiny between “special” and “general” cosmetics, demanding periodic re-evaluation of ingredient safety and risk mitigation plans. Indonesia’s BPOM Regulation 8/2024 requires adverse-event monitoring for cosmetic clinical trials. At the same time, SGS partnered with BPOM to share lab data across a new Indonesian Cosmetic Laboratory Network, illustrating public-private synergy. ASEAN alignment initiatives further compress timelines for ingredient notification, stimulating regional outsourcing uptake.

North America gains momentum from MoCRA’s shift from voluntary to mandatory reporting. The FDA now issues Form 3911 guidance for electronic serious-event reporting and audits facility registrations, pushing brands toward centralized compliance platforms. State-level rules create additive complexity: California’s Proposition 65 produced nearly 5,000 violation notices in 2024, especially for titanium dioxide and diethanolamine, signaling aggressive enforcement. Washington State’s Toxic-Free act and Canadian alignment with EU allergen disclosure keep demand brisk for cross-border advisory and analytics.

Competitive Landscape

The cosmetovigilance market remains moderately fragmented. SGS, Intertek, and Eurofins possess global laboratory footprints and leverage mergers and acquisitions (M&A), such as SGS’s acquisition of IEC, to secure integrated clinical and in vitro testing pipelines. Registrar Corp’s 2025 acquisition of Personal Care Regulatory Group created a USD 900 million consumer compliance platform spanning North America and Europe, highlighting consolidation in advisory niches.

Specialists differentiate through technology. IQVIA utilizes large language models to identify safety signals across various multimodal data streams. At the same time, ProductLife Group’s Halloran purchase brings U.S. regulatory affairs depth to its European base, including start-ups like Spore. Bio addresses microbiological contamination with AI-guided optical sensors that cut detection time from days to minutes. Blockchain proofs of origin, offered by several mid-tier firms, help combat counterfeit infiltration in LATAM-APAC corridors.

Pricing pressure intensifies as insurers factor surveillance rigor into liability premiums. Service providers that supply dashboard evidence of early-warning capability negotiate more favorable coverage terms, creating a virtuous cycle that elevates technologically advanced vendors. Yet white-space persists in emerging markets where local language support and region-specific coding standards remain scarce, an opening for agile players able to localize global best practices.

Cosmetovigilance Industry Leaders

SGS SA

Intertek Group plc

Eurofins Scientific SE

Bureau Veritas SA

IQVIA Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Registrar Corp acquired Personal Care Regulatory Group, creating a cross-Atlantic compliance platform.

- November 2024: ProductLife Group bought Halloran Consulting, expanding into North America.

- February 2024: Spore.Bio introduced AI bacterial-load detection for cosmetics and other products.

Global Cosmetovigilance Market Report Scope

| In-house Cosmetovigilance Systems |

| Contract Outsourcing |

| Hybrid / Co-managed Services |

| Spontaneous Consumer Reporting |

| Active Surveillance (Post-Marketing Studies) |

| Digital & App-based Reporting Platforms |

| Social-Media & Real-World Data Mining |

| Other Structured Channels (Pharmacies, Clinics) |

| Multinational Cosmetic Manufacturers |

| Small & Medium Cosmetic Brands |

| Regulatory Authorities & Public-Health Agencies |

| Third-party Testing & Certification Bodies |

| Healthcare Providers & Dermatology Clinics |

| Skin Care |

| Hair Care |

| Color Cosmetics |

| Fragrances & Deodorants |

| Emerging Categories (CBD, Nano-cosmetics) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | In-house Cosmetovigilance Systems | |

| Contract Outsourcing | ||

| Hybrid / Co-managed Services | ||

| By Reporting Method | Spontaneous Consumer Reporting | |

| Active Surveillance (Post-Marketing Studies) | ||

| Digital & App-based Reporting Platforms | ||

| Social-Media & Real-World Data Mining | ||

| Other Structured Channels (Pharmacies, Clinics) | ||

| By End User | Multinational Cosmetic Manufacturers | |

| Small & Medium Cosmetic Brands | ||

| Regulatory Authorities & Public-Health Agencies | ||

| Third-party Testing & Certification Bodies | ||

| Healthcare Providers & Dermatology Clinics | ||

| By Application | Skin Care | |

| Hair Care | ||

| Color Cosmetics | ||

| Fragrances & Deodorants | ||

| Emerging Categories (CBD, Nano-cosmetics) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the cosmetovigilance market in 2025?

The cosmetovigilance market size totaled USD 11.9 billion in 2025 and is on track to reach USD 15.1 billion by 2030.

Which service model is most popular for safety monitoring?

Contract outsourcing leads with 46.1% cosmetovigilance market share as of 2024, reflecting brands preference for external expertise and flexible cost structures.

Why is Asia-Pacific growing faster than Europe?

Asia-Pacific posts a 5.6% CAGR because China's May 2025 safety-dossier rule and broader ASEAN alignment are rapidly elevating compliance requirements, spurring outsourcing demand.

How does MoCRA change U.S. compliance?

MoCRA mandates facility registration, product listing, and 15-day serious adverse-event reporting for all cosmetics sold in the United States, transitioning from a voluntary to a compulsory framework.

What technologies are reshaping safety surveillance?

AI-driven natural-language processing for social-media mining, blockchain traceability to deter counterfeits, and rapid microbiological sensors are the leading innovations transforming cosmetovigilance workflows.

Which product categories require the most intense monitoring?

Skin care dominates monitoring volume, but CBD and nano-enabled formulations are under the closest scrutiny due to limited historical safety data and evolving regulatory guidance.

Page last updated on: