Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 2.99 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

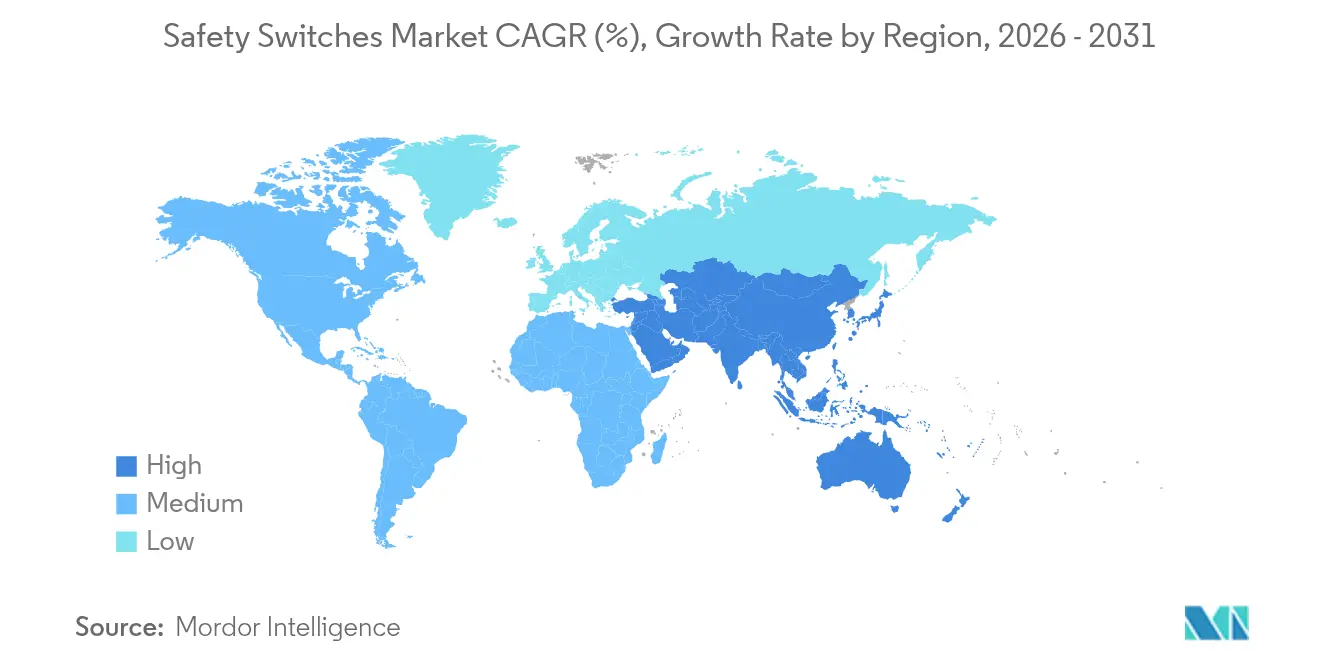

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Safety Switches Market Analysis by Mordor Intelligence

The safety switches market size is expected to grow from USD 2.2 billion in 2025 to USD 2.32 billion in 2026 and is forecast to reach USD 2.99 billion by 2031 at 5.23% CAGR over 2026-2031. Growth is underpinned by aggressive factory-automation investments, stricter machine-safety laws and a rapid shift toward collaborative robot workspaces. End users now demand devices that combine tamper resistance, self-diagnostics and fieldbus connectivity, pushing suppliers to embed RFID coding, IoT sensors and predictive-maintenance analytics. Asia-Pacific holds the largest regional position, benefitting from large-scale smart-factory programs, while the Middle East is set for the quickest rise on the back of oil-and-gas modernization and explosion-proof mandates. Competitive focus has moved toward solution-oriented portfolios that integrate hardware, software and services, enabling quicker compliance and reduced total cost of ownership. Device makers able to bridge functional safety and real-time data visibility are expected to capture the next wave of opportunities in the safety switches market.

Key Report Takeaways

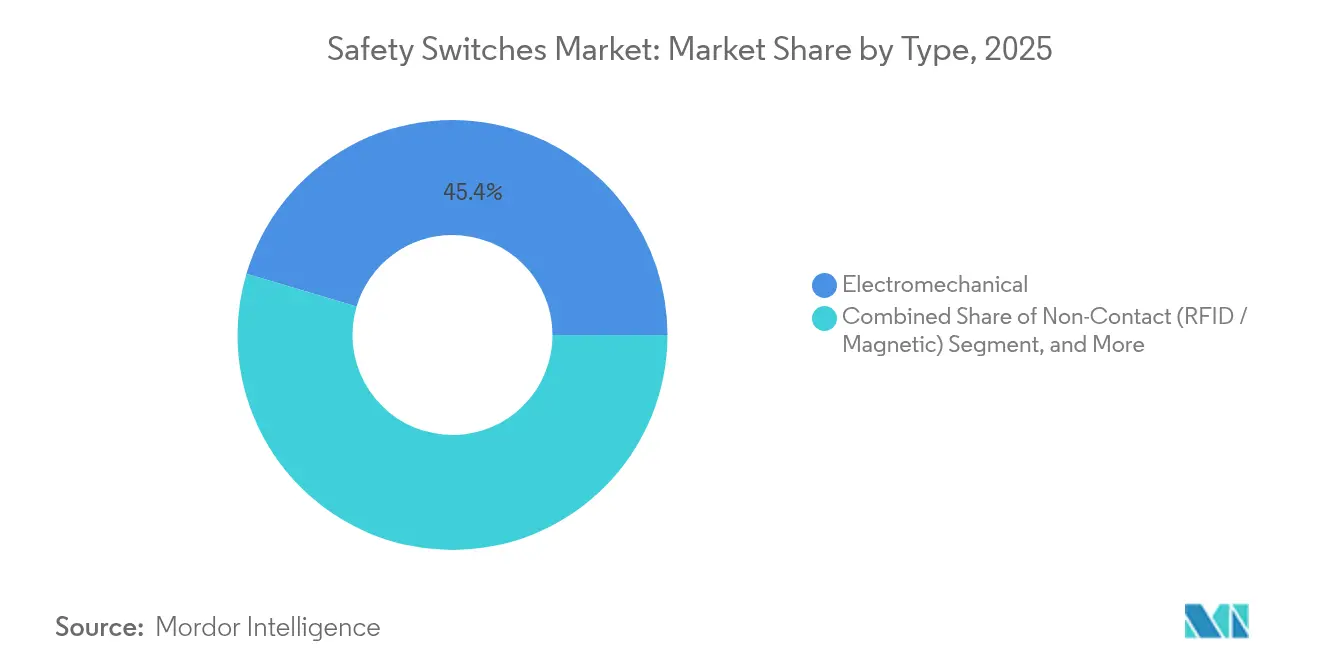

- By product type, electromechanical units led with a 45.40% share of the Safety switches market size in 2025, whereas RFID/magnetic variants are projected to grow at 7.45% CAGR to 2031.

- By actuator, key-operated interlocks retained 37.30% revenue share in 2025; RFID-coded solutions record the highest forecast CAGR at 9.1% through 2031.

- By installation, panel-mounted products dominated with 53.20% share in 2025, while DIN-rail offerings will expand fastest at 6.42% CAGR.

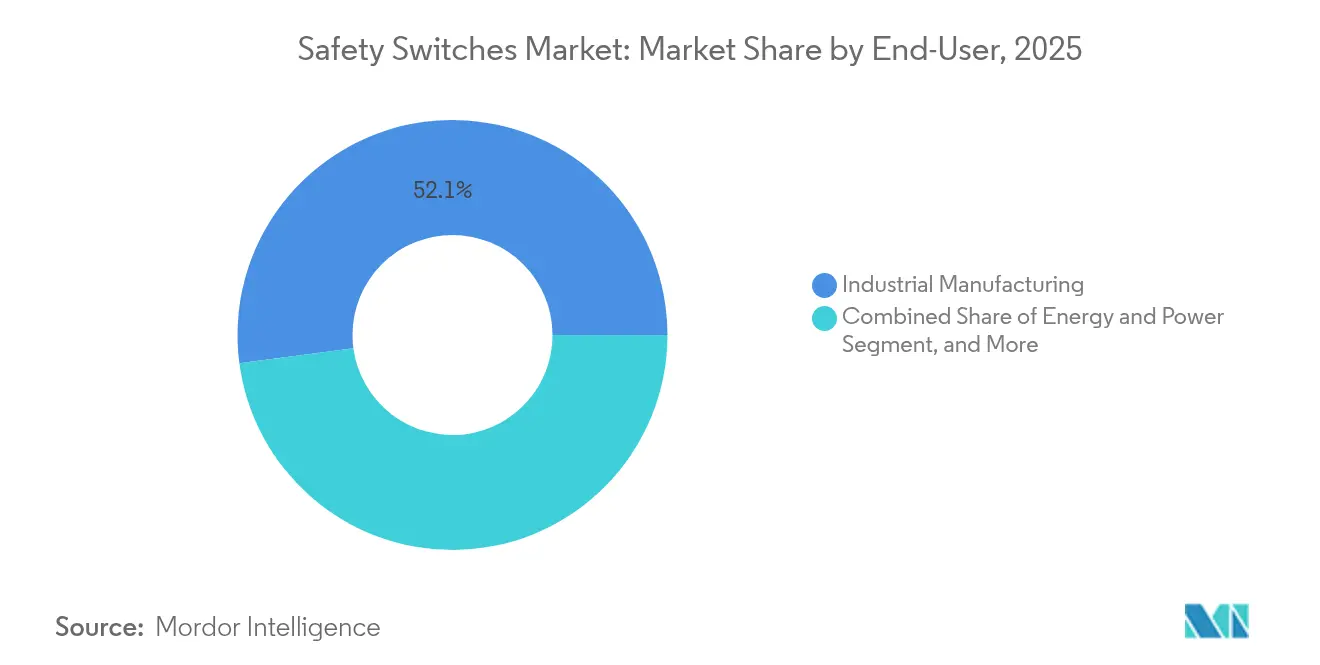

- By end user, industrial manufacturing captured 52.10% of the Safety switches market share in 2025; logistics and warehousing is the fastest-growing segment, advancing at 8.05% CAGR to 2031.

- By region, Asia-Pacific accounted for 37.90% of 2025 revenue; the Middle East is poised to climb at 8.75% CAGR, the steepest regional increase.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Safety Switches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automation-driven safety requirements | +1.2% | Asia-Pacific | Medium term (2-4 years) |

| Collaborative-robot adoption | +1.4% | North America and Europe | Medium term (2-4 years) |

| Mandatory machinery retrofits | +0.8% | Europe | Short term (≤2 years) |

| Explosion-proof demand in oil and gas | +1.1% | Middle East | Medium term (2-4 years) |

| RFID interlocks in high-potency pharma | +0.7% | US and EU | Medium term (2-4 years) |

| Conveyor safety for e-commerce warehouses | +0.9% | North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Expanding automation-driven safety requirements in Asia

Asia's manufacturing sector is experiencing a fundamental shift in safety paradigms as automation adoption accelerates, creating substantial demand for sophisticated safety switches. Countries like China, Japan, and South Korea are implementing stricter workplace safety regulations that mandate the use of certified safety devices in automated production lines. This regulatory evolution coincides with the region's push toward smart manufacturing, where safety switches serve as critical components in ensuring human-machine coexistence. The integration of safety switches with factory automation systems has become a strategic priority for manufacturers seeking to balance productivity with worker protection, particularly as labor costs rise and skilled worker shortages persist.[1]IDEC Corporation, “Switches - IDEC - APAC,” IDEC, apac.idec.com According to IDEC, demand for safety switches in Asia has grown by over 30% since 2024, with non-contact varieties seeing the highest adoption rates in electronics manufacturing.

Rise in collaborative robots necessitating integrated safety solutions

The proliferation of collaborative robots (cobots) across manufacturing environments is fundamentally transforming safety system requirements, creating significant opportunities for advanced safety switch technologies. Unlike traditional industrial robots that operate in caged environments, cobots work alongside humans, necessitating sophisticated safety mechanisms that can dynamically adjust protection parameters based on proximity and operation mode. The revision of ISO 10218 standard for industrial robot safety in 2024 has established clearer functional safety requirements for collaborative applications, driving demand for safety switches that can interface with robot control systems. Despite their inherent safety features, cobots still require complementary guarding solutions to address residual risks such as pinch points and programming errors. PowerSafe Automation reports that properly integrated safety switches can reduce cobot-related incidents by up to 85% while maintaining operational efficiency, making them essential components in Industry 4.0 implementations.[2]Shawn Mantel, “Smart Factory Automation: Cobots, Robotics & Guarding Explained,” PowerSafe Automation, powersafeautomation.com

Mandatory Retrofit of Legacy Machinery in Europe's Process Industries

Europe's process industries are undergoing a significant safety upgrade cycle driven by the enforcement of the Machinery Directive's latest amendments, creating substantial demand for replacement safety switches. The directive now requires older equipment to meet contemporary safety standards, effectively mandating retrofits for machinery that may have been compliant when installed but falls short of current requirements. This regulatory push coincides with the industry's broader digital transformation initiatives, prompting manufacturers to not merely replace outdated safety components but to upgrade to smart, connected alternatives. The retrofit market is particularly robust in chemical, pharmaceutical, and food processing sectors, where equipment lifespans typically exceed two decades. According to Pilz, approximately 65% of industrial machinery in operation across Europe requires safety system upgrades to achieve compliance with current standards, representing a substantial addressable market for safety switch manufacturers.

Demand Surge for Explosion-Proof Devices in Middle-East Oil & Gas

The Middle East oil and gas sector is experiencing unprecedented demand for explosion-proof safety switches as operators modernize aging infrastructure while expanding production capacity. These specialized devices, designed to prevent ignition in hazardous atmospheres, are becoming critical components in the region's energy infrastructure as safety standards become more stringent and enforcement more rigorous. The unique operating conditions in Middle Eastern facilities, including extreme temperatures and corrosive environments, are driving innovation in materials and design, with manufacturers developing switches that can withstand temperatures from -55°C to +55°C. Eaton's CEAG GHG 981 explosion-protected safety switches, which feature IP66 ingress protection and are available in robust materials like fiberglass-reinforced polyester and stainless steel, exemplify the specialized solutions gaining traction in the region. The Gas Exporting Countries Forum projects that natural gas production in the Middle East will increase by 33% by 2050, creating sustained demand for safety equipment capable of operating in potentially explosive environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher ASPs of Non-Contact Switches in Cost-Sensitive SMEs | -0.7% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Complex Certification Cycles Across Multi-Jurisdictional Plants | -0.5% | Global, with emphasis on multinational operations | Medium term (2-4 years) |

| Compatibility Gaps with Industry-Specific Safety Fieldbuses | -0.4% | Global, with concentration in advanced manufacturing hubs | Medium term (2-4 years) |

| Counterfeit Low-Cost Imports Undermining Brand Adoption (APAC) | -0.6% | Asia-Pacific, with spillover to global supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher ASPs of Non-Contact Switches in Cost-Sensitive SMEs

RFID sensors cost two to three times more than electromechanical models, discouraging rapid swap-outs in small workshops where budget and technical skills are limited.[3]Schmersal Group, “Devices for Ex Zones at Schmersal,” Schmersal, products.schmersal.com Consequently, penetration of advanced units among SME machine builders remains below 25%, tempering near-term uptake across the Safety switches market.

Complex Certification Cycles Across Multi-Jurisdictional Plants

Multinational manufacturers face significant challenges in implementing standardized safety switch solutions due to divergent certification requirements across jurisdictions, increasing both implementation timelines and compliance costs. The lack of global harmonization in safety standards creates a complex web of requirements that companies must navigate when deploying safety systems across their international operations. For instance, a safety switch certified under European standards (EN ISO 13849-1) may require additional testing and documentation to meet North American requirements (UL 508) or Asian specifications. This certification complexity extends beyond the initial installation to ongoing maintenance and replacement cycles, where companies must maintain region-specific inventories of approved components. According to Logic Fruit, the certification process for safety-critical components can add 4-6 months to implementation timelines for global deployments, creating significant operational inefficiencies and potentially delaying critical safety upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: RFID technology reshapes manipulation protection

Electromechanical models still lead the safety switches market thanks to proven durability in dusty, high-vibration sites. Yet non-contact RFID sensors show the swiftest momentum, expanding at 7.45% CAGR as OEMs look to curb bypassing and gain live diagnostic data. In 2025, electromechanicals held a 45.40% revenue share, while RFID uptake in pharma lines rose sharply after regulators tightened tampering rules. The Safety switches market size for non-contact devices is projected to reach USD 1.11 billion by 2031, mirroring wider adoption in robotic assembly cells.

RFID sensors also unlock predictive-maintenance analytics; embedded memory logs cycle counts, enabling service alerts before failure. Explosion-proof housings and stainless-steel variants are broadening use in corrosive and hazardous settings, expanding supplier addressable revenue pools. Continuous miniaturization further allows multi-sensor arrays inside compact cobot grippers, reinforcing future demand within the safety switches market.

By Actuator Type: Coded solutions drive anti-tampering innovations

Key-operated interlocks retain widespread use due to mechanical simplicity and low unit cost. Still, RFID-coded and magnetic actuators now set the pace, especially in Category 4, PLe applications that prohibit guard cheating. These designs cascade up to 32 nodes over a single cable, shrinking installation time. Pharmaceutical cleanrooms and food-processing lines favor non-contact formats to eliminate crevices where contaminants might lodge, spurring fresh volume in the Safety switches market.

Functional safety over Ethernet is also emerging. Vendors bundle actuator and safety-relay functions in the same housing, streaming diagnostics to MES dashboards. This virtualizes traditional hard-wired chains and supports flexible cell reconfiguration, a core Industry 4.0 requirement. Consequently, actuator innovation will remain pivotal to value capture within the Safety switches market.

By End-User: Manufacturing drives core demand

Industrial manufacturing generated 52.10% of all 2025 revenue, underpinned by tight accident-reduction targets and rising robot density. Automotive body-shops specify redundant tongue interlocks for every weld-cell door, while beverage fillers opt for IP69K stainless units that withstand caustic washdowns. The Safety switches market size linked to manufacturing is forecast to surpass USD 1.62 billion by 2031, maintaining segment dominance.

Logistics and warehousing shows the fastest climb at 8.05% CAGR; large e-commerce operators retrofit kilometre-long conveyor loops with cable-pull e-stops and light-grid guards. Growth is further lifted by autonomous-mobile-robot fleets that trigger zone muting via RFID gates to balance throughput and worker safety. This dual push from omnichannel retail and labor shortages cements warehouses as the headline expansion arena for the Safety switches market.

By Sales Channel: System integrators enhance value proposition

Complex safety-PLC architectures and stringent audit trails make integrators indispensable to SMEs and multinationals alike. Engineering-led distributors now bundle risk assessment, validation and training into hardware quotes, capturing service margins and driving loyalty. This partner-centric model accelerates commissioning cycles, boosting device replacement frequency across the Safety switches market.

Direct OEM contracts still dominate high-volume machinery builders in automotive and packaging. Suppliers provide custom pins, housing colors and firmware, locking in multiyear agreements. Hybrid go-to-market strategies that blend integrator reach with OEM depth appear best suited to maximize penetration and after-sales revenue streams inside the Safety switches market.

Geography Analysis

Asia-Pacific generated 37.90% of 2025 revenue, led by Chinese and South Korean electronics clusters. Factory upgrades under national “smart manufacturing” plans specify RFID interlocks and IO-Link diagnostics, lifting average selling prices. Government subsidies for automated lines in India and Vietnam will sustain regional leadership of the safety switches market.

The Middle East is forecast to grow at 8.75% CAGR through 2031. National oil companies in UAE and Saudi Arabia now demand ATEX or IECEx-certified switchgear for gas compression, refining and LNG export trains. Suppliers offering -55 °C to +55 °C temperature ratings and stainless-steel enclosures have secured multiyear framework deals, catalyzing swift market expansion.

Europe and North America remain mature but opportunity rich. EU Machinery Directive revisions compel chemical and food processors to retrofit older mixers and conveyors within two years; this short-cycle demand inflates replacement volumes. In the US, e-commerce fulfillment centers adopt network-ready switches that feed safety data to cloud WMS platforms, preserving steady unit growth in the safety switches market.

Regulatory Landscape

Machine-safety compliance for safety switches is anchored in globally referenced standards and region-specific enforcement. In 2024, IEC published IEC 60947-5-1:2024 (5th edition) for electromechanical control-circuit devices, and ISO released ISO 14119:2024 covering the design and selection of interlocking devices associated with guards. Together, these references influence safety-switch design, testing, and documentation for OEMs and retrofitters.

In Europe, the Machinery Regulation (EU) 2023/1230 is the governing framework for machinery and safety components, with the consolidated text reflecting updates effective May 2026, including software-based safety functions in the definition of safety components. In the United States, OSHA 29 CFR 1910.212 continues to require machine guarding to protect operators from hazards, reinforcing ongoing demand for interlocked guards and compliant switching solutions across manufacturing sectors.

Value Chain Analysis

The safety switches value chain begins with raw materials and subcomponents, including silver-alloy contacts for arc management, copper alloys for current-carrying parts, polymers for housings, and magnets or RFID elements for non-contact devices. For coded and diagnostic-capable variants, suppliers also prepare PCBs and microelectronics. These inputs are converted into switches and safety subassemblies through processes such as stamping, injection molding, PCB assembly, and precision machining, followed by verification activities that align with functional-safety and machinery requirements, commonly referenced standards including ISO 13849 and EN 60204-1.

Downstream, OEMs and machine builders integrate safety switches into guards, doors, conveyors, and robotic cells. Distributors and system integrators increasingly bundle risk assessment, validation, and commissioning services to meet audit and documentation needs across multi-jurisdictional plants. Aftermarket replacement, periodic inspections, and upgrades toward connected diagnostics (fieldbus-capable or network-integrated architectures) create a recurring revenue layer, with lead-time resilience supported by practices such as dual sourcing and, for some manufacturers, vertical integration of tooling and test capabilities to reduce dependency on external suppliers.

Competitive Landscape

The safety switches market is moderately fragmented. Top multinationals-Schneider Electric, Rockwell Automation and ABB-leverage global channels and broad portfolios, collectively holding roughly 45% revenue. Mid-tier specialists such as Schmersal, Euchner and SICK AG carve out niches by innovating RFID coding, stainless-steel hygienic housings and integrated diagnostics. New entrants focus on software-defined safety layers that overlay conventional hardware, hinting at future convergence between OT and IT safety.

Portfolio expansion continues via M&A and co-development. ABB’s purchase of Siemens’ wiring-accessory line in China expanded its reach to 230 cities, while Schneider launched Acti9 Active Safety to embed real-time monitoring into low-voltage breakers. Banner Engineering and IDEM target flexible manufacturing with daisy-chainable RFID switches that reduce cable cost by 30%. Competitive intensity is forecast to stay high as firms race to marry functional safety with Industry 4.0 analytics, shaping long-term dynamics across the safety switches market.

Safety Switches Industry Leaders

Schneider Electric

Rockwell Automation

Siemens AG

Omron Corporation

Honeywell International

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is expanding where buyers want higher manipulation protection, hygienic design, and richer diagnostics without adding wiring complexity, particularly in cobot cells, high-throughput warehousing conveyors, and regulated process lines. Product activity in 2026 reflects this shift toward compact, higher-integrity safety architectures: Phoenix Contact released the PSRcompact safety relay family (SIL 3 and PL e) to reduce cabinet space and simplify connections, while BERNSTEIN AG introduced the SLO electronic safety lock switch with RFID coding, IP69 protection, and high locking force to support tamper-resistant, washdown-capable guarding.

Opportunity also sits at the intersection of functional safety and software-defined control, as plant owners and OEMs move from hardwired chains to configurable and networked safety zones with centralized diagnostics. In June 2026, CODESYS partnered with Mesco Engineering on a software-based Virtual Safe Control approach targeting SIL 3 capability, while SICK deployments using Flexi Soft modular safety controllers and network-wide diagnostics show the push for scalable, configurable safety systems across larger facilities. These moves support vendor strategies spanning integrated hardware, software, and lifecycle services, especially for multinational manufacturers operating under complex certification and change-control requirements.

Recent Industry Developments

- July 2026: CBS ArcSafe launched the RSK-SACE3 remote switch kit for ABB/SACE EMAX2 air circuit breakers, enabling operation from 30 to 50 feet away. The launch supports safer maintenance and switching procedures in energized environments, reinforcing demand for engineered solutions that reduce personnel exposure during switching and troubleshooting.

- June 2026: Rockwell Automation introduced the 140ME Motor Protective Switching Device for branch motor control, combining electronic overload protection with digital connectivity features. The release reinforces integrated motor control and protection architectures that share diagnostics over industrial networks, a purchasing pattern that increasingly influences adjacent safety switching and panel safety designs.

- March 2026: steute Technologies completed the acquisition of KIEPE Industry from Kiepe Electric GmbH, expanding its industrial switching and safety solutions portfolio. The deal broadens product and application coverage for machine-safety and industrial control customers, adding scale to specialist offerings in a market where OEMs value portfolio breadth and long-term supply assurance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the safety switches market covers revenues earned from safety-rated switching devices used to stop or prevent hazardous machine motion by interrupting power or control signals in industrial and related facilities. We count revenue at the point of sale by manufacturers and authorized channels.

Scope exclusions: We exclude general-purpose electrical switches, consumer-grade breakers, and non-safety control components that are not designed and marketed for machine safety use.

Segmentation Overview

- By Type

- Electromechanical Safety Switches

- Non-Contact (RFID / Magnetic) Safety Switches

- Explosion-Proof / Heavy-Duty Safety Switches

- Other Types

- By Actuator Type

- Key-Operated Interlock

- Hinge-Operated Interlock

- RFID-Coded Interlock

- Magnetic Actuator

- By Installation Configuration

- Panel-Mounted

- DIN-Rail Mounted

- By End-User

- Industrial Manufacturing

- Automotive

- Food and Beverage

- Chemicals and Pharmaceuticals

- Aerospace and Defense

- Metals and Mining

- Energy and Power

- Oil and Gas

- Power Generation

- Commercial and Institutional

- Building Automation

- Logistics and Warehousing

- Healthcare

- Others

- Industrial Manufacturing

- By Sales Channel

- Direct OEM

- Distributor / System Integrator

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of Latin America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Middle East and Africa

- Turkey

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia Pacific

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base around industrial activity, automation adoption, and safety compliance trends that influence demand for safety switches. We typically refer to public and official sources, including the International Labor Organization for workplace safety context, ISO and IEC publications for relevant safety standards, and national statistics portals (such as the US Bureau of Labor Statistics and Eurostat) for manufacturing and industrial production indicators.

To ground the commercial side, we also reviewed company annual reports, investor presentations, product catalogs, and press releases that describe safety switch portfolios and route-to-market changes. In parallel, patent databases were checked to understand design direction for non-contact sensing, actuator mechanisms, and integrated diagnostics, and these findings were used for assumption checks. The sources cited above are illustrative, and additional public sources were used during data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with manufacturers, distributors, automation partners, plant-level users, and safety and compliance specialists across the Americas, EMEA, and APAC. Respondent input was used to confirm how purchasing decisions are made, how pricing changes by specification and certifications, and where demand is coming from, new equipment builds versus retrofit and maintenance cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 43% |

| Mid tier: 58% | Functional/Unit leaders: 37% | EMEA: 31% |

| Smaller Players: 14% | Managers: 50% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where industrial output, automation spending signals, and safety compliance intensity by region are used to reconstruct the addressable demand pool for safety switches. That pool is then converted into value using typical replacement and new-install rates. To keep totals realistic, we also run selective bottom-up approximations using sampled average selling prices multiplied by estimated unit volumes for common switch types, then confirm reasonableness through channel checks with distributors and system integrators.

Key model inputs include manufacturing production indices, machinery and automation investment cues, installed base growth of automated equipment, typical safety retrofitting frequency, and price steps linked to safety rating, mounting configuration, and non-contact sensing adoption. Where data is thin for smaller countries, we use proxy indicators (such as industrial employment and production mix) and then re-anchor results to regional interview feedback.

For forecasting, scenario analysis is applied so growth can be adjusted based on automation cycle strength and the pace of regulatory enforcement. The outputs are then smoothed into a consistent outlook that matches what respondents describe for order books and pricing behavior over the forecast period.

Data Validation & Update Cycle

Validation is done through multiple checks that compare model outputs with independent demand signals, followed by a review of sharp year-to-year moves before sign-off. When a regional result looks unusual, we re-check the assumptions behind industrial activity, adoption rates, and pricing, and then re-contact select experts to confirm whether the change is real or driven by model mechanics.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as major standard changes, supply constraints, or a sudden shift in factory investment. Before delivery, an analyst performs a final refresh pass so clients receive the latest updated view aligned to recent public releases and interview learnings.

Mordor Intelligence's Global Safety Switches Market Size Compared Against Other Published Estimates

It is common to see different market sizes for safety switches, even when sources use similar wording. The boundary of what counts as a safety switch can shift, and the year selected for the base value affects the resulting math. Differences also come from how prices are treated across product grades and how much of the value chain is included.

By tracking installation configuration, safety-rated type coverage, and end-user demand checks, Mordor Intelligence keeps the total focused on machine-safety use cases, instead of counting adjacent electrical switchgear purchased for general power distribution.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.32 B (2026) | |

| Industry Research Group A | USD 2.58 B (2024) | Uses an earlier base year and appears to apply a broader product definition, which can pull in general electrical safety devices alongside machine-safety switches, and this inflates the addressable pool. |

| Industry Publisher B | USD 1.63 B (2025) | Starts from a narrower demand base that leans on contact and industrial-only applications, with limited clarity on retrofit volumes and pricing steps across configurations, which can compress the value estimate. |

Taken together, the spread is mainly explained by scope boundaries, base-year selection, and how pricing progression is applied across switch types and use cases. Our approach stays traceable to clear demand indicators and practical assumption checks, which helps users reproduce the logic and understand what is being counted and what is not.

Key Questions Answered in the Report

What is the current value of the safety switches market?

The market is valued at USD 2.32 billion in 2026.

How fast will the Safety switches market grow by 2031?

It is projected to expand at a 5.23% CAGR, reaching USD 2.99 billion.

Which region holds the largest share of the safety switches market?

Asia-Pacific leads with 37.90% of 2025 revenue.

Why are RFID safety switches gaining traction?

They offer superior tamper resistance and real-time diagnostics, supporting Industry 4.0 and collaborative-robot applications.

Which end-user segment grows fastest through 2031?

Logistics and warehousing is expected to rise at 8.05% CAGR driven by e-commerce automation.

What restrains adoption in small and medium enterprises?

Higher prices of non-contact models and limited in-house technical expertise delay upgrades among SMEs.

Page last updated on: