Earbuds Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

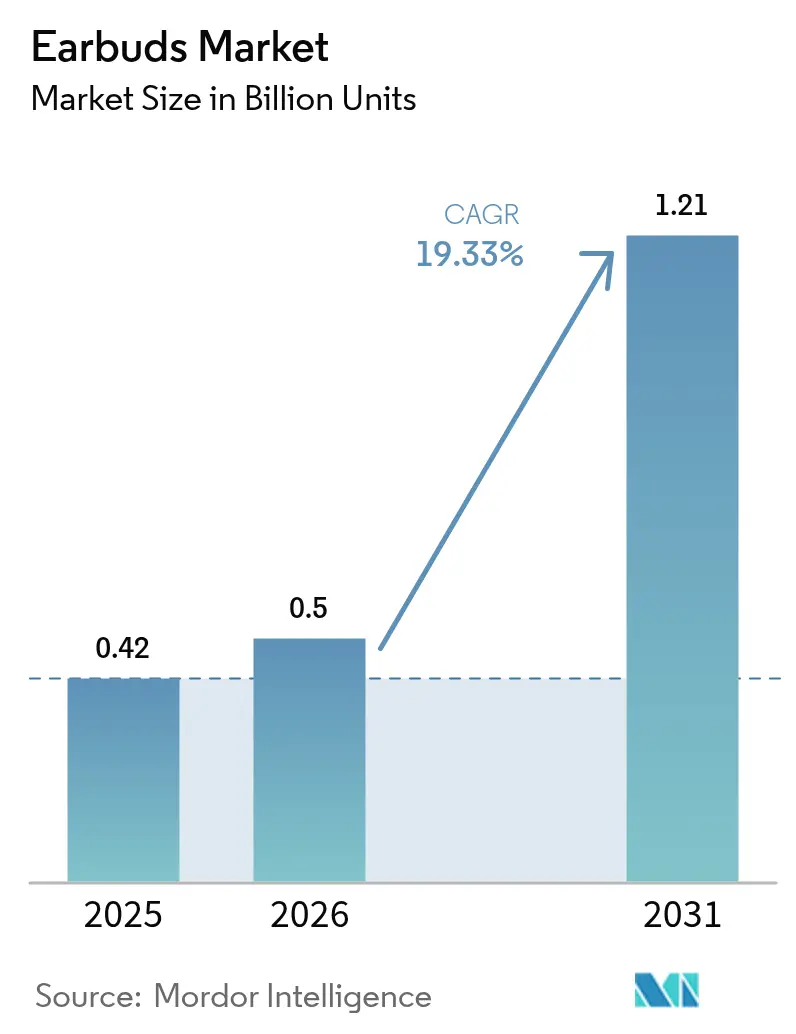

| Market Volume (2026) | 0.5 Billion units |

| Market Volume (2031) | 1.21 Billion units |

| Growth Rate (2026 - 2031) | 19.33% CAGR |

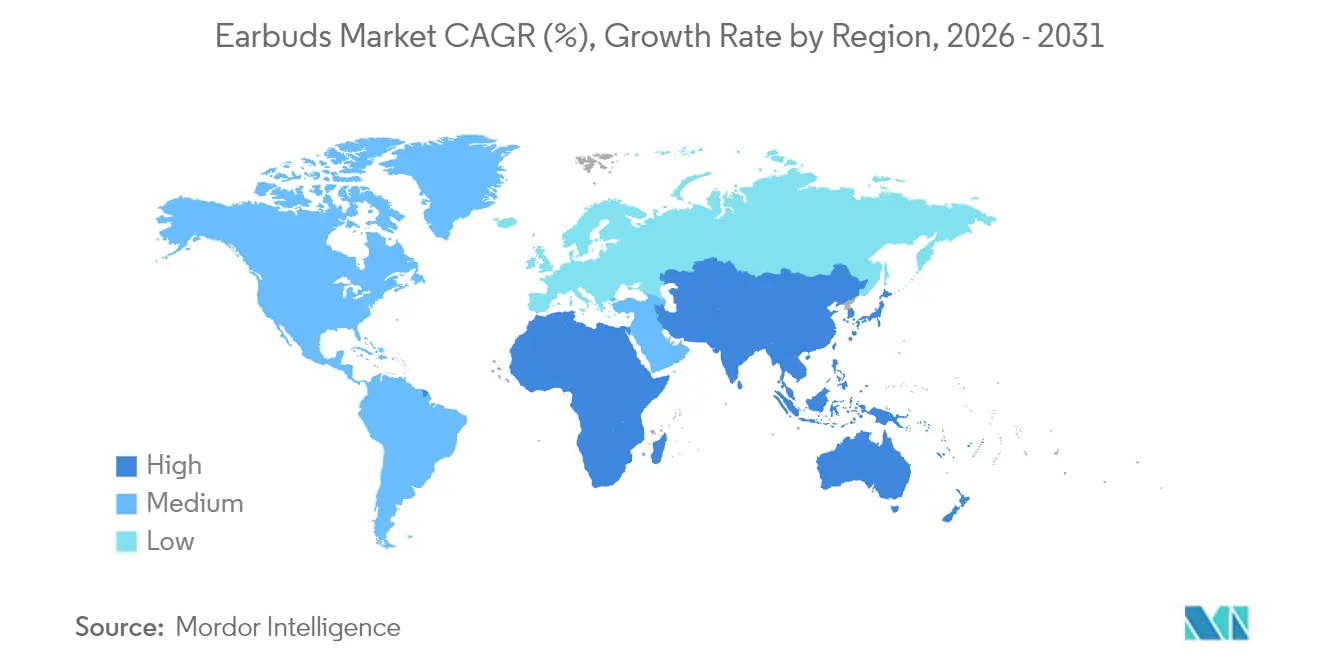

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

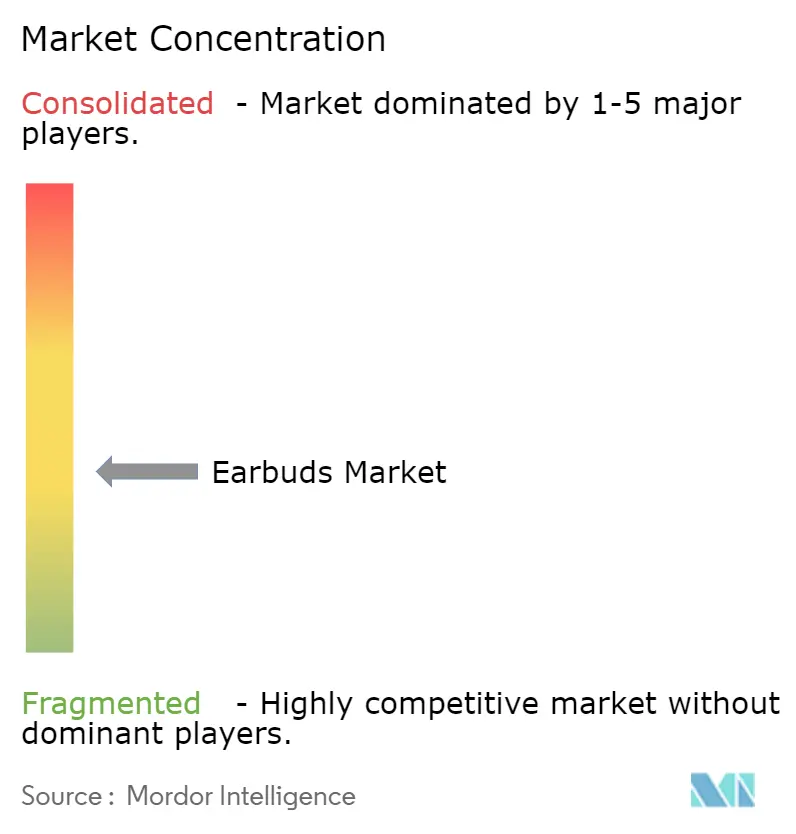

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Earbuds Market Analysis by Mordor Intelligence

The earbuds market size is expected to grow from 0.42 billion units in 2025 to 0.5 billion units in 2026 and is forecast to reach 1.21 billion units by 2031 at 19.33% CAGR over 2026-2031. Growth reflects rising demand for wellness-centric features, enterprise-grade communications, and premium acoustics woven into compact form factors. Fitness tracking, hybrid-work audio needs, and faster smartphone replacement cycles create multiple tailwinds. Manufacturers leverage Asia Pacific’s supply-chain depth to scale component integration while simultaneously reshoring strategic battery sub-assemblies. Competitive rivalry intensifies as smartphone brands, legacy audio players, and direct-to-consumer specialists introduce advanced noise cancellation, MEMS speakers, and AI-driven personalization, prompting steady feature migration from premium to value tiers.

Key Report Takeaways

- By feature, truly wireless earbuds led with 73.55% earbuds market share in 2025, and the segment is projected to grow at 19.92% CAGR through 2031.

- By geography, Asia Pacific contributed 36.80% of the earbuds market size in 2025 and is expected to expand at 19.15% CAGR to 2031.

- By distribution channel, online channels controlled 59.10% of sales in 2025 and are projected to advance at 19.25% CAGR through 2031.

- By price tier, the mid-price band (USD 50-150) captured 45.05% revenue share in 2025, while the low-price band (below USD 50) posts the fastest 21.34% CAGR over the same horizon.

- By application, fitness and sports accounted for the highest growth, moving at a 19.21% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Earbuds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising fitness-centric audio consumption | +3.2% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Shorter replacement cycles for wired earphones | +2.8% | Asia Pacific core, spill-over to global markets | Short term (≤ 2 years) |

| Smartphone and 5G penetration boost | +4.1% | Global, accelerating in Asia Pacific and emerging markets | Medium term (2-4 years) |

| Premium features filtering into low-price tiers | +3.7% | Global, pronounced in price-sensitive markets | Long term (≥ 4 years) |

| Battery component reshoring in Asia Pacific | +2.3% | Asia Pacific manufacturing hubs, global supply impact | Long term (≥ 4 years) |

| Enterprise adoption for hybrid-work audio | +2.9% | North America and Europe, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Fitness-Centric Audio Consumption

The shift toward preventive health elevates earbuds from passive listening devices to active biometric monitors. Nokia Bell Labs’ OmniBuds research platform illustrates the trajectory with integrated 9-axis IMUs, multi-wavelength PPG, and medical-grade temperature sensors that enable continuous heart-rate variability, SpO₂, and cuff-less blood-pressure tracking.[1]Nokia Bell Labs, “OmniBuds: A Sensory Earable Platform for Advanced Bio-Sensing and On-Device Machine Learning,” arxiv.org Commercial pipelines mirror the laboratory: Synseer targets late-2025 FDA clearance for HealthBuds, pairing ultrasonic in-ear sensing with privacy-preserving edge processing. These capabilities dovetail with the USD 4.4 trillion global wellness economy, supporting a 19.73% CAGR in fitness applications by transforming earbuds into indispensable workout companions and round-the-clock health sentinels.

Smartphone and 5G Penetration Boost

Global 5G rollouts and higher smartphone refresh rates unlock new audio workloads. Qualcomm’s S7 Pro XPAN platform enables high-resolution 96 kHz/24-bit streams over Wi-Fi with Bluetooth-like power draw, first commercialized in Xiaomi’s 2025 Buds 5 Pro press release. Low-latency, high-bandwidth links support spatial audio, real-time translation, and cloud-assisted AI soundscapes. Regulatory tailwinds reinforce the trend: the U.S. Federal Communications Commission mandates 100% hearing-aid compatibility for handsets by 2028, prompting tighter handset-earbud integration.

Premium Features Filtering into Low-Price Tiers

Cost curves on ANC chips, MEMS speakers, and spatial-audio DSPs allow sub-USD 50 models to match yesterday’s flagships. QCY’s partnership with USound will embed MEMS drivers in 2025 mass-market launches, improving phase response and Hi-Res certification while maintaining entry-level pricing.[2]USound GmbH, “USound Partners with QCY to Introduce MEMS Speaker Technology,” usound.comSkullcandy’s EcoBuds combine 65% recycled plastics with battery-free charging cradles at USD 26.99, proving that sustainability and advanced acoustics can coexist in value segments. The democratization enables the low-price tier’s 22.07% growth despite macro-economic uncertainties.

Enterprise Adoption for Hybrid-Work Audio

Remote and hybrid work patterns elevate professional earbud demand. EPOS ADAPT E1 integrates AI-driven ear-fit analysis built on 500,000 ear scans, earning Microsoft Teams certification and embedding device-management APIs critical for IT fleet deployments.[3]EPOS Group, “EPOS Launches ADAPT E1 and Announces Lenovo Partnership,” eposaudio.com Lenovo’s global accessory partnership with EPOS embeds unified-communications audio stacks into ThinkPad and ThinkBook arrays, broadening enterprise exposure. Jabra’s psycho-acoustic research under its BrainAdapt program documents reduced cognitive load in video meetings when optimized spatial cues are present. These developments help accelerate enterprise procurement cycles, especially in banking, consulting, and telehealth verticals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ergonomic limits for long-hour wear | -2.1% | Global, particularly affecting professional users | Medium term (2-4 years) |

| Hearing-health compliance tightening | -1.8% | North America and Europe regulatory focus | Long term (≥ 4 years) |

| Counterfeit low-cost product influx | -2.4% | Global, concentrated in emerging markets | Short term (≤ 2 years) |

| Rare-earth magnet supply volatility | -1.9% | Global supply chains, Asia Pacific manufacturing impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Low-Cost Product Influx

Customs agencies report rising seizures of fake branded earbuds that undercut legitimate players and expose consumers to safety risks. U.S. Customs and Border Protection valued recent confiscations at USD 62.6 million, representing nearly 360,000 counterfeit units, underscoring the scale of illicit trade. E-commerce marketplaces remain the primary conduit. Brand owners respond with blockchain-anchored authenticity tags and machine-vision scrapers that recognize infringements at listing upload, though the solutions are viable mainly for mid- and premium price tiers where margins offset compliance costs.

Rare-Earth Magnet Supply Volatility

Earbuds rely on neodymium-iron-boron micro-drivers for compact high-output sound. The European Commission notes that 98% of EU demand for rare-earth magnets was sourced from China in 2024, heightening exposure to geopolitical shocks. U.S. Department of Energy road-maps outline domestic extraction initiatives, yet commercial volumes remain modest. Emerging alternatives such as iron-nitride compositions from Niron Magnetics promise 70% lower lifecycle CO₂ while sidestepping rare-earth reliance, but mass-production readiness lies beyond the forecast period. Supply tightness translates into fluctuating driver costs and weighs on gross margins, especially for low-price SKUs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feature - Truly Wireless Dominance Accelerates

Truly wireless models represented 73.55% of 2025 shipments, and their 19.92% CAGR positions them as the backbone of the earbuds market. Earbuds market size for truly wireless types is on track to double by 2031 as innovations in solid-state batteries, reverse-charging cases, and low-power Wi-Fi chipsets enhance user convenience. HMD Global’s 1,600 mAh Amped Buds case triples average pack capacity without increasing thickness, underlining progress in energy density. Continuous removal of 3.5 mm ports across smartphones hastens wired attrition, concentrating R&D on untethered designs.

The technology roadmap pivots toward shape-flexible solid-state cells and ultra-wideband (UWB) radios that bolster location services. Samsung’s pilot lines for oxide-based solid-state modules forecast 20% energy-density gains, foundational for sub-4 gram earbud shells. While legacy neckband styles retain a foothold in developing markets where 30-hour runtime remains compelling, their share erodes as truly wireless bill-of-materials costs fall below USD 12.

By Price Range - Mid-Tier Stability amid Low-End Acceleration

The mid-price band maintained 45.05% of the earbuds market share in 2025 owing to equilibrium between feature depth and affordability. Earbuds market size for this tier is projected to grow at a steady clip as ANC, spatial audio, and PPG sensors migrate downward. JLab’s GO Pods ANC provide hybrid noise cancellation and 26-hour playtime at USD 36.99, demonstrating the squeeze on mid-tier differentiation.

Low-price models surge at 21.34% CAGR as component commoditization collides with emerging-market demand. Meanwhile, premium units above USD 150 face slower growth even though Apple’s AirPods line generated USD 18 billion in 2024 revenue. Sustained premium traction now depends on breakthroughs such as camera-equipped stems or AI-led adaptive acoustics rather than incremental codec upgrades. Designers therefore segment portfolios with eco-friendly materials and wellness analytics to uphold price ceilings.

By Distribution Channel - Online Momentum Builds

Digital channels accounted for 59.10% of 2025 shipments, expanding at 19.25% CAGR as vertically integrated brands favor direct-to-consumer logistics. Algorithms leverage first-party sales data for rapid SKU iteration, while web-based fit tests, such as Audiodo’s 3-minute hearing assessment embedded in CMF by Nothing’s Buds 2 Plus, mitigate “try before buy” friction. Subscription models offering periodic upgrades further lock in lifetime value.

Physical retail, however, still influences premium conversion through experiential listening booths and instant gratification. Flagship stores and pop-up kiosks integrate QR-coded journeys that feed consumers back into brand apps, illustrating omnichannel fusion rather than a binary choice. The balance favors online in markets with high logistics reliability and digital payments penetration, notably North America, Western Europe, and Korea.

By Application - Fitness Transformation Drives Growth

Music and general entertainment remain core at 40.85% share, but fitness usage is the fastest climber, reaching a 19.21% CAGR. Earbuds’ multi-sensor arrays capture heart-rate and movement data while delivering coaching cues, a combination that wearables on wrists or arms cannot match for proximity to the carotid artery. Continuous physiologic sampling also feeds telemedicine dashboards, widening addressable revenue beyond hardware sales.

Professional communication benefits from hybrid work, as unified-communications certifications unlock enterprise procurement budgets. AI beam-forming and adaptive ANC improve speech intelligibility, reducing fatigue in back-to-back calls.

Gaming and esports stay niche yet lucrative, demanding sub-45 ms latency and spatial accuracy that justify premium DSPs.

Geography Analysis

Asia Pacific leads with 36.80% share and sustains a 19.15% CAGR through 2031. Earbuds market size in the region reflects deep contract-manufacturing clusters and rising middle-class spending. Goertek’s USD 280 million Vietnam expansion adds 30 million annual earphone units for Samsung and Apple. India’s offline audio market reached INR 5,000 crore (USD 600 million) in 2024, logging 61% volume growth and signaling robust appetite for true wireless formats.

North America maintains high premium penetration, propelled by accessory attach rates among smartphone flagships. Policy-driven inclusivity also shapes demand: the FCC’s 2028 hearing-aid compatibility mandate fosters new SKUs with ambient-sound amplification and self-fitting audiogram apps. Sustainability preferences steer European consumers toward recycled-plastic housings; Sony reports earbuds using 85% recycled ABS polymers.

Latin America, the Middle East, and Africa register double-digit unit growth off a smaller base, aided by value-tier models embedding ANC and MEMS speakers. Counterfeit infiltration remains acute, prompting customs partnerships and regional warranty centers to reinforce brand trust. Infrastructure gaps in last-mile logistics and digital payments moderate online channel expansion, but smartphone uptake paves the way for accelerated adoption as economic conditions improve.

Competitive Landscape

Competitive intensity is moderate, with the top five vendors controlling an estimated 55% of shipments. Apple anchors the premium pole position through vertical integration of H2 audio silicon, seamless iOS pairing, and Find My network lock-in, translating into a USD 18 billion AirPods franchise. Xiaomi and Huawei exploit smartphone ecosystems and aggressive domestic pricing, dominating mid-price volumes across China and Southeast Asia. Sony and Bose defend audiophile niches via LDAC and proprietary noise-reduction algorithms.

Emerging challengers pursue differentiation in health tech and translation. Shokz touts bone-conduction safety for outdoor athletes, while HONOR introduced Earbuds Open with embedded AI translation across 15 languages. The supply side is consolidating: Syntiant’s USD 150 million acquisition of Knowles’ consumer MEMS microphones unit brings edge-AI neural processors under one roof, compressing the sensor-to-model stack for next-gen earables.

Investment flows spotlight hearing-enhancement convergence. Patient Square Capital injected USD 100 million into the Eargo-hearX merger, birthing LXE Hearing and magnifying scale in the over-the-counter hearing-aid category. As technical barriers rise around onboard AI and medical compliance, scale players with chipset design, regulatory expertise, and cloud ecosystems will extend their moat, while boutique labels succeed by targeting micro-niches in sports, sustainability, or fashion.

Earbuds Industry Leaders

Apple, Inc.

Xiaomi Corporation

BBK Electronics Corp. Ltd.

Samsung Electronics Co. Ltd.

Imagine Marketing Ltd. (boAt)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Creative Technology partnered with xMEMS Labs to integrate solid-state MEMS speakers promising 7× better phase consistency and lighter form factors for true wireless models.

- April 2025: Audiodo joined forces with CMF by Nothing to embed Personal Sound hearing tests in Buds 2 Plus, pushing individualized audio into mainstream price tiers.

- March 2025: Eargo and hearX completed their merger, creating LXE Hearing with USD 100 million from Patient Square Capital and forming the segment’s largest OTC hearing-aid platform.

- March 2025: HMD Global launched Amped Buds featuring a 1,600 mAh reverse-charging case, tripling typical capacity without increasing thickness.

Global Earbuds Market Report Scope

Earbuds are a pair of small hearing devices designed to be held outside the ear canal, unlike earphones. They are electroacoustic transducers that convert the electrical signal into a corresponding sound. They are typically designed to enable a single user to listen to audio.

The earbuds market is segmented by feature (wired earbuds, wireless earbuds (truly wireless)), by price range (premium range (greater than USD 150), mid range (USD 50 - USD 150), low range (less than USD 50)), by distribution channel (offline, online), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Wired Earbuds | |

| Wireless Earbuds | Truly Wireless |

| Other Wireless Earbuds |

| Premium (> USD 150) |

| Mid (USD 50 - 150) |

| Low (< USD 50) |

| Offline |

| Online |

| Fitness and Sports |

| Gaming and Esports |

| Professional and Office |

| Music and General Consumer Entertainment |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Feature | Wired Earbuds | |

| Wireless Earbuds | Truly Wireless | |

| Other Wireless Earbuds | ||

| By Price Range | Premium (> USD 150) | |

| Mid (USD 50 - 150) | ||

| Low (< USD 50) | ||

| By Distribution Channel | Offline | |

| Online | ||

| By Application | Fitness and Sports | |

| Gaming and Esports | ||

| Professional and Office | ||

| Music and General Consumer Entertainment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the expected shipment volume for earbuds in 2031?

Global shipments are projected to reach 1.21 billion units by 2031, reflecting a 19.33% CAGR from 2026 levels.

Which region will contribute the most incremental units through 2031?

Asia Pacific leads additions due to manufacturing scale and rising disposable incomes, sustaining a 19.15% CAGR.

Why are truly wireless models growing faster than other types?

Continuous battery innovations, elimination of smartphone headphone jacks, and compact charging-case designs drive the 19.92% CAGR for truly wireless units.

How are counterfeit products impacting legitimate brands?

Customs agencies seized counterfeit earbuds worth USD 62.6 million recently, which diverts revenue and imposes brand-protection costs.

Which price tier is expanding the fastest?

The sub-USD 50 band leads with a 21.34% CAGR as ANC, MEMS speakers, and recycled materials become affordable at entry levels.

How will regulatory policies influence future designs?

The FCC's 2028 hearing-aid compatibility mandate accelerates development of earbuds with ambient amplification and self-fit audiograms, especially for the U.S. market.

Page last updated on: