Wind Turbine Gearbox Repair And Refurbishment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.28 Billion |

| Market Size (2031) | USD 6.43 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

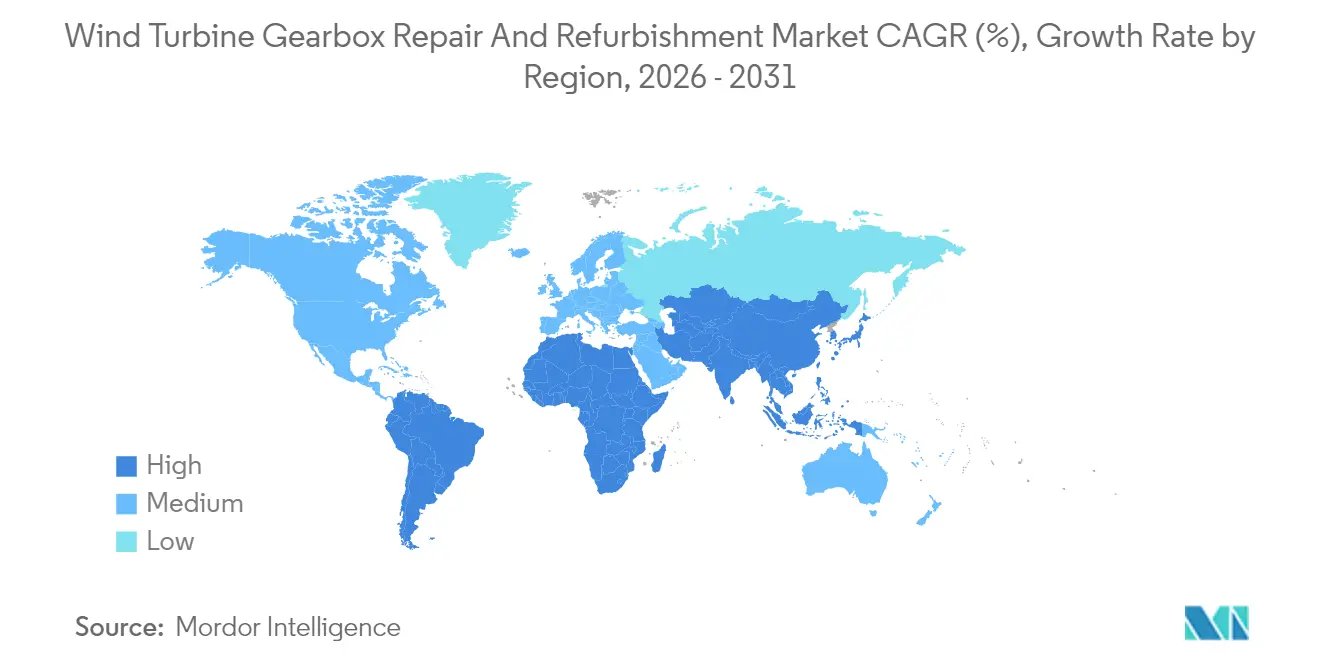

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wind Turbine Gearbox Repair And Refurbishment Market Analysis by Mordor Intelligence

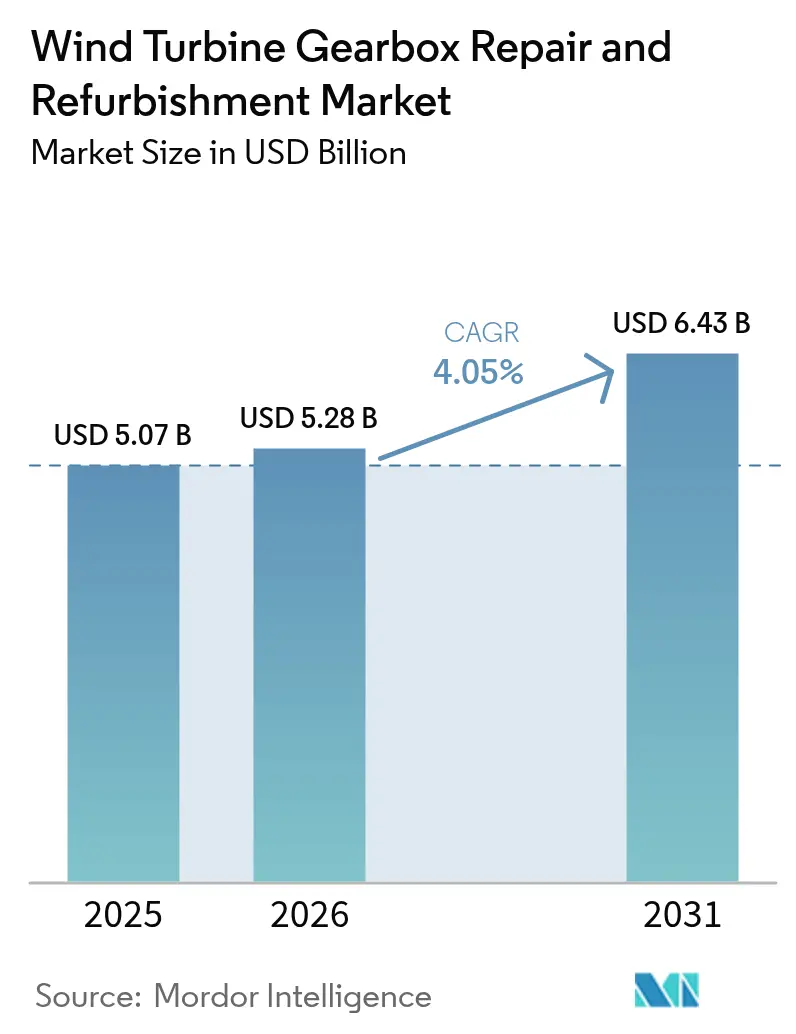

Wind Turbine Gearbox Repair And Refurbishment Market size in 2026 is estimated at USD 5.28 billion, growing from 2025 value of USD 5.07 billion with 2031 projections showing USD 6.43 billion, growing at 4.05% CAGR over 2026-2031.

This advance emerges from the collision of aging onshore fleets, capacity-constrained gearbox manufacturing, and escalating demand for uptime guarantees. The European fleet’s demographic shift, an 18-month post-pandemic lead time for new gearboxes, and insurance-driven service protocols align to make repair economics more attractive than outright replacement. Independent service providers (ISPs) are leveraging multibrand expertise to erode the incumbent position of original equipment manufacturers (OEMs). Meanwhile, offshore turbines bring higher ticket values and logistics costs exceeding 30% of total maintenance spend, pushing providers to refine exchange-pool and uptower repair models. As data-driven predictive maintenance spreads from Asia Pacific to other regions, operators gain the ability to intervene weeks before catastrophic bearing failures, preserving annual energy production and lowering the levelized cost of electricity.

Key Report Takeaways

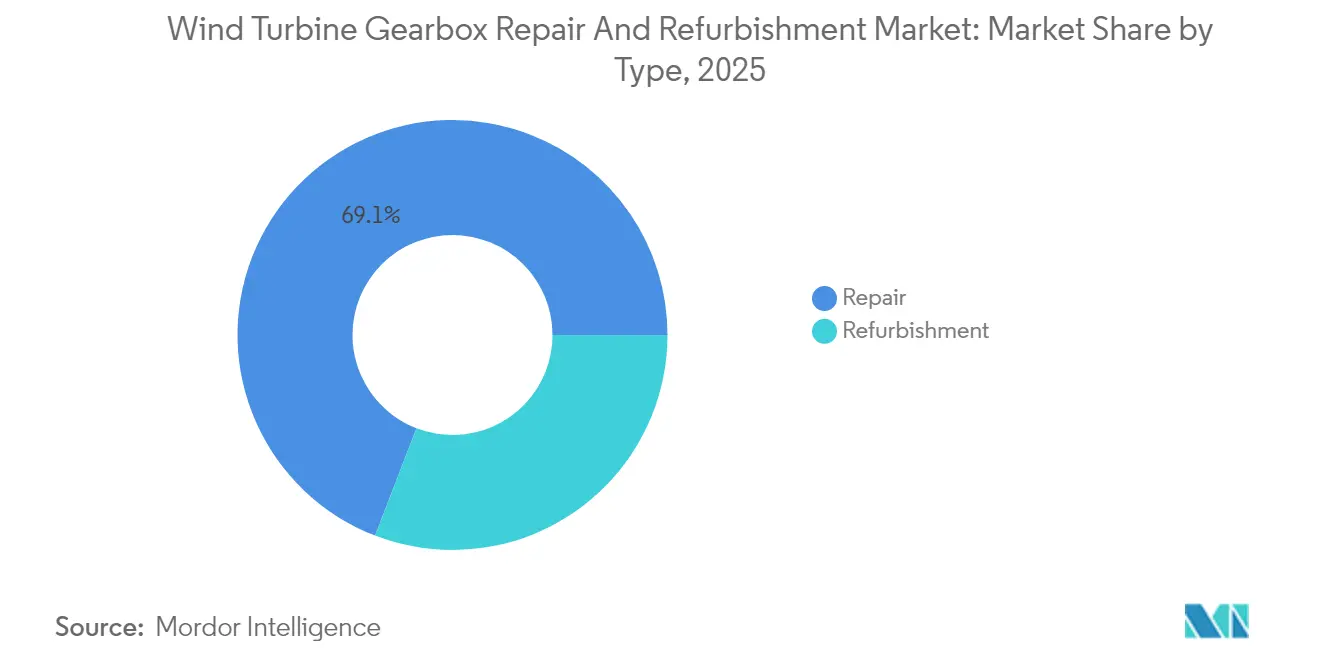

- By type, repair held 69.14% of the wind turbine gearbox repair and refurbishment market share in 2025, while refurbishment is forecast to expand at a 4.7% CAGR to 2031.

- By gearbox failure component, bearings captured 60.55% of 2025 repair orders; gear components will see a 4.95% CAGR through 2031.

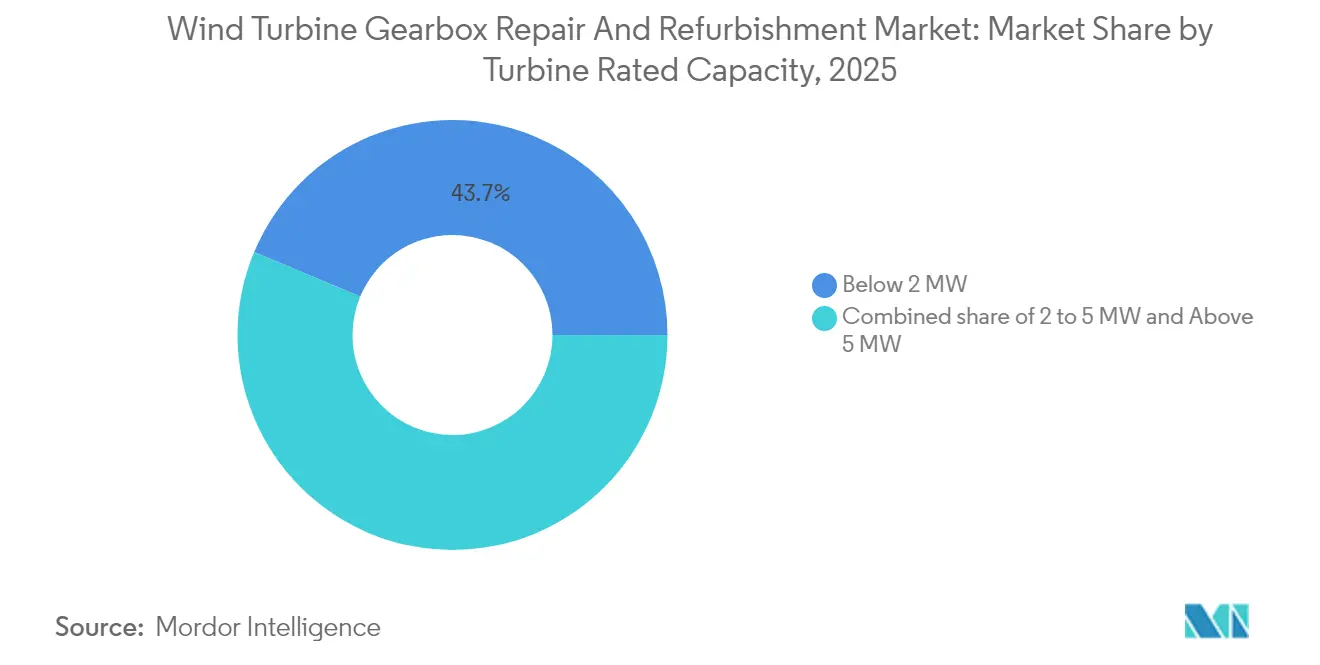

- By turbine rated capacity, the below 2 MW segment accounted for 43.70% of the wind turbine gearbox repair and refurbishment market size in 2025, whereas the above 5 MW segment is expanding at a 4.65% CAGR.

- By service provider, OEM service divisions commanded a 58.05% share in 2025, yet Independent Service Providers (ISP) are advancing at a 5.3% CAGR.

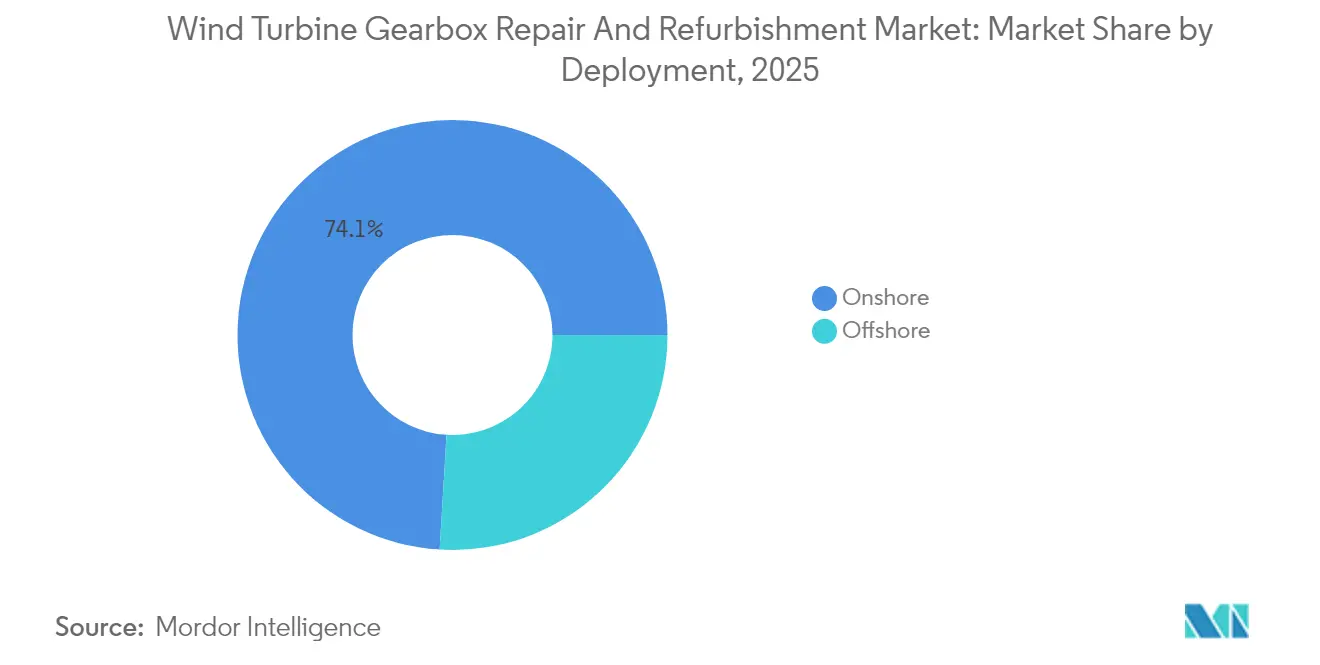

- By deployment, offshore represented 25.95% of 2025 revenue and is poised for the fastest 6.85% CAGR to 2031.

- By geography, Europe accounted for 37.45% revenue in 2025; Asia Pacific is set to grow at a 6.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wind Turbine Gearbox Repair And Refurbishment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid ageing of >10-year onshore turbine fleet | 1.20% | Global, concentrated in Europe & North America | Medium term (2-4 years) |

| OEM-backed global repair-hub roll-outs | 0.80% | Global, with focus on North America & Europe | Long term (≥ 4 years) |

| Shift from time-based to data-driven predictive maintenance contracts | 0.60% | APAC core, spill-over to Europe & North America | Medium term (2-4 years) |

| Scarcity of new gearbox supply & 18-month lead-time post-COVID | 0.90% | Global | Short term (≤ 2 years) |

| Insurance-mandated proactive repairs to lower outage payouts | 0.40% | Europe & North America primarily | Medium term (2-4 years) |

| Modular, exchange-pool business models cutting crane hours by 35-50% | 0.30% | Global, early adoption in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Ageing of Over 10-Year Onshore Turbine Fleet

Installations commissioned between 2010-2014 are now hitting the 7-10-year window when gearboxes typically demand major intervention.[1]University of Birmingham, “Gearbox Failure Analysis in Ageing Wind Turbines,” birmingham.ac.uk The absence of advanced condition monitoring on many legacy turbines pushes operators toward reactive repairs that cost USD 250,000-300,000 each. Europe feels the crunch first because early wind build-outs in Germany and Denmark created synchronized maintenance cycles. This demographic swell will intensify through 2027, ensuring sustained demand for the wind turbine gearbox repair and refurbishment market.

OEM-Backed Global Repair-Hub Roll-Outs

OEMs invest in centralized remanufacturing hubs to shorten turnaround times and capture aftermarket margins. GE Vernova earmarked USD 100 million for gearbox refurbishment capacity in Amarillo, Texas, under a broader USD 600 million U.S. supply-chain program. Siemens Gamesa runs a Spanish refurbishment plant that completes 10-week overhaul cycles for Eneco’s Princess Amalia farm. Centralized hubs maintain specialized tooling for planetary gear repairs and enable predictive inventory stocking, further enlarging the wind turbine gearbox repair and refurbishment market.

Shift from Time-Based to Data-Driven Predictive Maintenance Contracts

Sensor and machine-learning advances let operators detect temperature spikes, vibration anomalies, and lubrication faults days before failure. Predictive strategies cut direct O&M costs by 8% and lost production by 11% when a quarter of major failures are preempted. Asian developers equip new turbines with SCADA-linked condition monitoring, then contract for availability-based service. Diagnostic vendors such as Kavaken use case libraries to improve root-cause accuracy, further embedding predictive culture across the wind turbine gearbox repair and refurbishment industry.

Scarcity of New Gearbox Supply & 18-Month Lead Time

Raw-material bottlenecks and niche manufacturing capacity have stretched gearbox delivery times to 18 months. Operators cannot tolerate such downtime, so they opt for refurbishment or exchange-pool solutions in which pre-overhauled units sit in regional depots ready for swap-out. Scarcity also sparks in-situ repair innovations that avoid full gearbox removal, elevating service share for ISPs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated migration to direct-drive turbines eliminating gearboxes | -0.70% | Global, led by offshore developments | Long term (≥ 4 years) |

| High logistics cost for offshore gearbox handling (>30% of ticket) | -0.50% | Offshore markets globally | Medium term (2-4 years) |

| Limited availability of class-certified refurbishment facilities in LATAM & MEA | -0.30% | LATAM & MEA regions | Long term (≥ 4 years) |

| IP-restricted design data hindering multi-brand repairs | -0.20% | Global, particularly affecting ISPs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Migration to Direct-Drive Turbines Eliminating Gearboxes

Offshore developers prefer direct-drive configurations that remove the gearbox and improve reliability, especially where access is difficult. Peer-reviewed comparisons show geared turbines incur 9.3% higher OPEX per MW than direct-drive counterparts.[2]Wiley Online Library, “OPEX Comparison of Direct-Drive and Geared Turbines,” onlinelibrary.wiley.comYet rare-earth magnet requirements and higher capital expense confine adoption to large offshore projects, limiting near-term displacement of the existing geared fleet.

High Logistics Cost for Offshore Gearbox Handling

Ocean-based repairs demand heavy-lift vessels priced over USD 100,000 daily and restricted by weather windows. ScienceDirect studies estimate that logistics accounts for over 30% of offshore gearbox tickets. Floaters add complexity because jack-up vessels cannot anchor, raising innovation demand for autonomous maintenance platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Repair Dominance Drives Current Revenue

The wind turbine gearbox repair and refurbishment market for repair services reached USD 3.51 billion in 2025, 69.14% of total revenue. Operators historically run gearboxes to failure, favoring quick repairs that restore availability. Refurbishment, however, is advancing at 4.7% CAGR as asset owners seek extended warranties and lifecycle gains. GE Vernova’s Spanish hub embeds engineering upgrades into refurbished drivetrains, cutting repeat interventions and signalling a strategic pivot toward proactive overhauls. The segment evolution shows how the wind turbine gearbox repair and refurbishment market balances immediate uptime needs with long-term asset optimization.

Refurbishment’s higher materials scope allows bearing upgrades, gear re-profiling, and lubrication redesigns targeting known failure modes. Insurers often grant longer coverage on refurbished units, enhancing owner economics. With aging fleets entering their second decade, refurbishment will progressively narrow the revenue gap to repair across the wind turbine gearbox repair and refurbishment industry.

By Gearbox Failure Component: Bearing Failures Dominate Service Demand

Bearings triggered 60.55% of failures in 2025, driving specialized replacement and lubrication services. Contaminants, variable loads, and micro-pitting cause premature wear, making bearing health the focal point of predictive analytics. Gear tooth damage follows at a smaller share, yet a 4.95% CAGR will be seen as white-etching cracks gain industry attention. Lubrication-system optimization can avoid up to 50% of energy loss and extend component life. Service providers that master bearing diagnostics and flush-and-fill services capture the bulk of near-term value in the wind turbine gearbox repair and refurbishment market.

By Turbine Rated Capacity: Sub-2 MW Fleet Drives Current Activity

Sub-2 MW turbines generated 43.70% of 2025 gearbox work orders because early-generation machines now reach maintenance-intensive years. India’s Repowering Policy incentivizes overhauls across 25.4 GW of such capacity, guaranteeing a 1.5× output uplift after refurbishment. While mainstream 2-5 MW turbines form a diverse middle cohort requiring multibrand know-how, >5 MW machines deliver the fastest 4.65% CAGR thanks to rising installation rates and high-value gearboxes. Service providers segment their offerings accordingly: legacy specialists tackle ageing 1-2 MW fleets, whereas OEMs and tier-one ISPs build expertise for newer multi-megawatt classes.

By Service Provider: OEM Advantage Faces ISP Challenge

OEM divisions retained 58.05% of 2025 revenue on the strength of design IP and installed-base contracts. Yet ISPs’ 5.3% CAGR underscores a cost-driven shift in owner preferences. Deutsche Windtechnik manages more than 7,100 turbines across multiple brands, illustrating the scale that independent models can achieve. Utilities with large portfolios keep small in-house shops for critical repairs, but most outsource heavy work, reinforcing the wind turbine gearbox repair and refurbishment market’s dual-track structure.

By Deployment: Onshore Volume Versus Offshore Growth Potential

Onshore turbines contributed 74.05% of 2025 revenue, supported by easy crane access and mature supply lines. Although only 25.95% in 2025, offshore is projected for a 6.85% CAGR during 2026-2031. Logistics costs above 30% per job compel operators to use exchange-pool gearboxes delivered by purpose-built service vessels. Dual-gearbox concepts permit continued generation during maintenance, though at higher capex. This split shapes provider strategy: onshore specialists focus on rapid response and cost control; offshore experts sell reliability at premium rates.

Geography Analysis

Europe delivered 37.45% of global revenue in 2025, reflecting the continent’s early adoption and now-aging fleet. Policies such as WindEurope’s Clean Industrial Deal push domestic servicing capacity to protect competitiveness. Offshore wind in the North Sea lifts demand for advanced logistics and uptower repair tools. Predictive maintenance roll-outs gain regulatory favor, ensuring steady workload growth inside the wind turbine gearbox repair and refurbishment market.

Asia Pacific is the fastest-growing region at 6.55% CAGR to 2031. China’s vast fleet is shifting from warranty to multiyear service agreements that emphasize predictive monitoring, while India’s Repowering Policy funnels sub-2 MW turbines into refurbishment pipelines. Domestic champions like Goldwind collaborate with ISPs on component exchange pools, but technology-transfer rules preserve local content advantages.

North America maintains a sizeable installed base serviced by OEM hubs like GE Vernova’s Amarillo remanufacturing facility, ensuring fast turnaround for U.S. operators. Latin America, the Middle East & Africa remain nascent, constrained by limited class-certified workshops, yet maturing fleets promise incremental demand across the wind turbine gearbox repair and refurbishment market.

Competitive Landscape

Competition rests on multibrand technical capability, turnaround speed, and predictive analytics. GE Vernova’s USD 600 million U.S. manufacturing program underscores OEM reliance on aftermarket profit streams. Siemens Gamesa, ZF Friedrichshafen, and Flender leverage design data to secure long-term service deals. ISPs such as Moventas and Connected Wind Services carve share by offering cost-effective uptower repairs and bearing retrofits. Patent activity in uptower planet-gear extraction and AI-driven vibration diagnostics signals sustained technological differentiation. Exchange-pool models require capital depth, favoring larger groups; however, niche providers can win on agility within local markets.

As fleets age, owners tender multibrand, multi-year contracts that blend condition-monitoring, remote diagnostics, and on-site interventions. Players integrating all three under a unified service envelope will capture sticky revenue streams, cementing their place in the wind turbine gearbox repair and refurbishment industry.

Wind Turbine Gearbox Repair And Refurbishment Industry Leaders

Siemens Gamesa Renewable Energy SA

GE Vernova

ZF Friedrichshafen AG

Moventas Gears Oy

SKF Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: GE Vernova announced a nearly USD 600 million investment in U.S. facilities, including USD 100 million for gearbox remanufacturing capacity in Amarillo, Texas.

- February 2025: NGC won the Gold Prize for its 20-22 MW medium-speed transmission-chain gearbox, featuring rigid integration and segmented maintenance design.

- January 2025: GE Vernova secured >1 GW in repower orders across the U.S., using U.S.-manufactured nacelles and drivetrains.

- November 2024: SANY Renewable Energy signed 1.624 GW equipment contracts with JSW Group and Sembcorp, expanding its global presence.

Global Wind Turbine Gearbox Repair And Refurbishment Market Report Scope

The wind turbine gearbox repair and refurbishment market include:

| Repair |

| Refurbishment |

| Bearings |

| Gears |

| Shafts and Housings |

| Others (Seals, Lubrication system) |

| Below 2 MW |

| 2 to 5 MW |

| Above 5 MW |

| OEM Service Divisions |

| Independent Service Providers (ISP) |

| In-house Utility Workshops |

| Onshore |

| Offshore |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Repair | |

| Refurbishment | ||

| By Gearbox Failure Component | Bearings | |

| Gears | ||

| Shafts and Housings | ||

| Others (Seals, Lubrication system) | ||

| By Turbine Rated Capacity | Below 2 MW | |

| 2 to 5 MW | ||

| Above 5 MW | ||

| By Service Provider | OEM Service Divisions | |

| Independent Service Providers (ISP) | ||

| In-house Utility Workshops | ||

| By Deployment | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the wind turbine gearbox repair and refurbishment market by 2031?

The market is expected to reach USD 6.43 billion by 2031, supported by a 4.05% CAGR.

Which region is growing the fastest?

Asia Pacific is forecast to grow at 6.55% CAGR thanks to China’s ageing fleet and India’s repowering policy.

Why do bearings account for the majority of gearbox failures?

Variable loads, contamination, and lubrication challenges make bearings the most vulnerable component, driving 60.55% of 2025 failures.

How are exchange-pool programs changing maintenance economics?

They cut crane time by up to 50% by swapping a failed gearbox for a pre-refurbished unit, then overhauling the removed gearbox off-site.

Do direct-drive turbines threaten the gearbox service market?

Yes, over the long term, especially offshore, but higher capital costs and rare-earth supply constraints temper immediate adoption, so existing geared fleets will still need service for 15-20 years.

What distinguishes refurbishment from repair?

Refurbishment involves a comprehensive overhaul with component upgrades that extend warranty coverage, whereas repair focuses on fixing the immediate failure to restore operation.

Page last updated on: