Well Cementing Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 11.6 Billion |

| Market Size (2031) | USD 14.98 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Well Cementing Services Market Analysis by Mordor Intelligence

The Well Cementing Services Market size was valued at USD 11.02 billion in 2025 and estimated to grow from USD 11.6 billion in 2026 to reach USD 14.98 billion by 2031, at a CAGR of 5.25% during the forecast period (2026-2031).

Demand strength reflects sustained unconventional drilling, the restart of deep-water projects, and mandated well-integrity rules that elevate specialty cement usage. Automated cementing fleets, digital twins, and real-time downhole sensing enhance placement accuracy and reduce non-productive time, providing service providers with a cost-efficiency story that resonates with operators focused on capital discipline. Refracturing programs across North American shale and early CO₂-storage well buildouts diversify revenue streams, while rising offshore activity in Brazil, the Gulf of Mexico, and West Africa broadens geographic exposure. Pricing pressure remains a watch point, yet vertical integration and technology-centric differentiation offset margin risk for the largest suppliers.

Key Report Takeaways

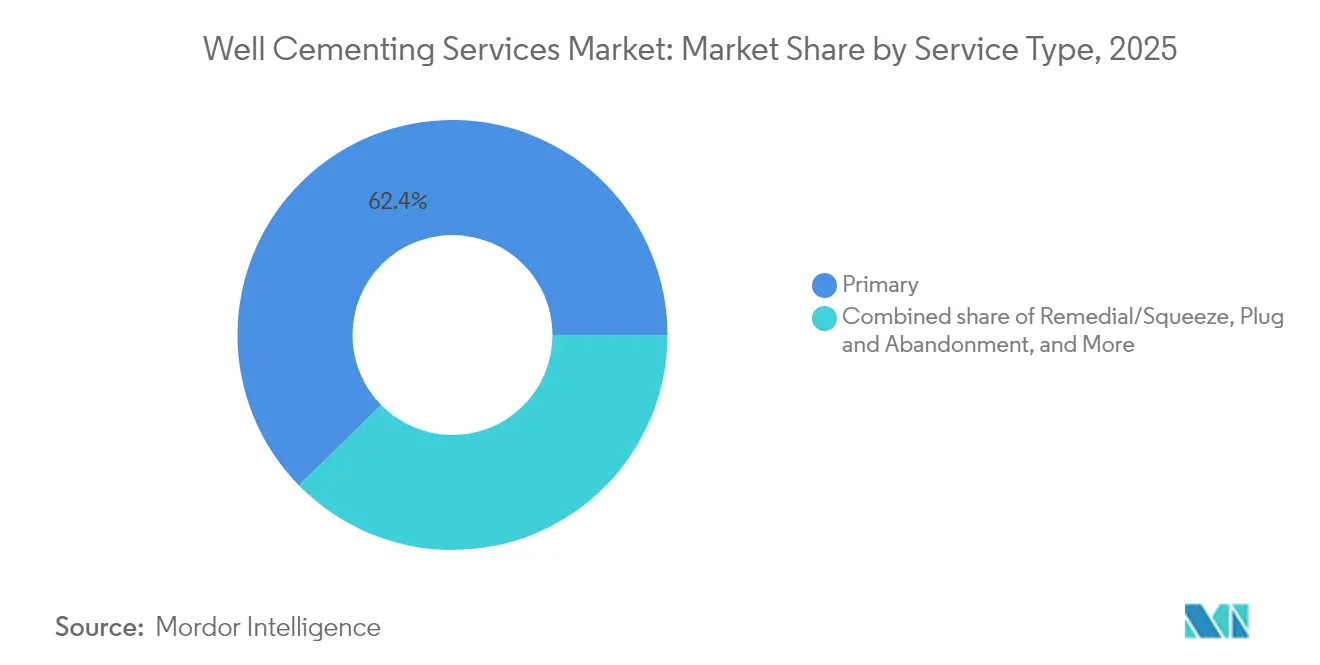

- By service type, primary cementing held 62.35% of the well cementing services market share in 2025; remedial and squeeze cementing is projected to expand at a 6.52% CAGR to 2031.

- By well type, horizontal wells accounted for 43.12% of the well cementing services market size in 2025 and are projected to advance at a 5.66% CAGR through 2031.

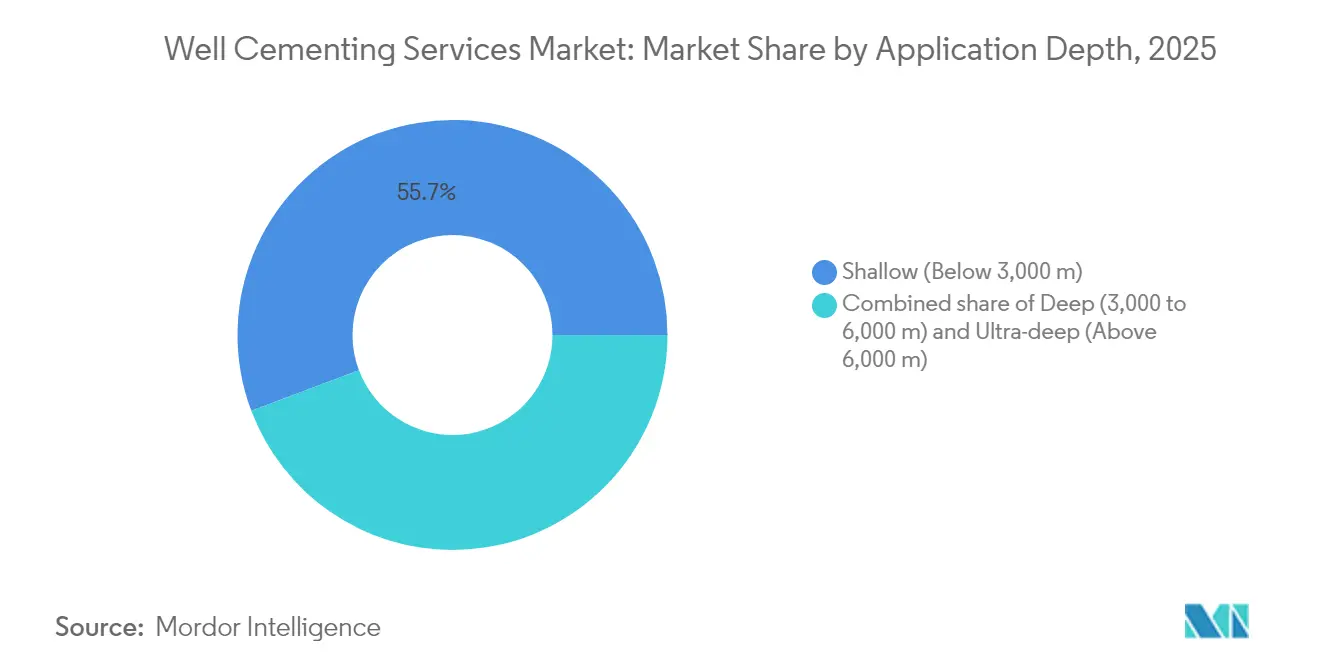

- By application depth, ultra-deep wells represent the fastest trajectory with an 8.26% CAGR through 2031, while shallow wells remained the largest revenue contributor at 55.74% in 2025.

- By location of deployment, the offshore segment is forecast to rise at a 7.58% CAGR to 2031, whereas onshore operations commanded 68.72% of 2025 revenue.

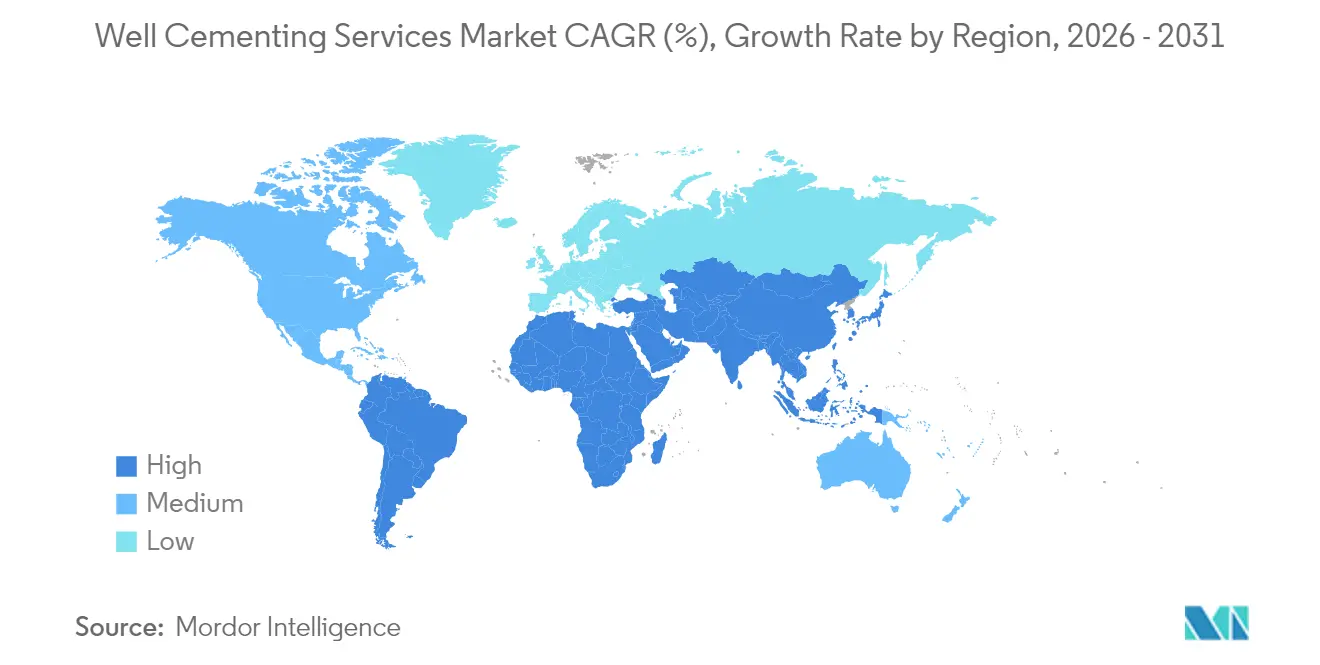

- By geography, the Middle East and Africa region is set to post the fastest 7.24% CAGR through 2031, while North America led with 36.95% revenue share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Well Cementing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging unconventional well completions | 1.20% | North America core, spill-over to Argentina | Medium term (2-4 years) |

| Revival of offshore deep-water FIDs 2025-2028 | 0.80% | Gulf of Mexico, Brazil, West Africa | Medium term (2-4 years) |

| Mandatory well-integrity regulations | 0.60% | Asia-Pacific & Middle East | Long term (≥4 years) |

| Accelerated refrac programs | 0.70% | Eagle Ford, Permian Basin | Short term (≤2 years) |

| Fully-automated cementing units | 0.40% | Early adoption in North America & Europe | Long term (≥4 years) |

| CO₂-storage injection-well build-out | 0.50% | North America & Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surging Unconventional Well Completions Drive Market Expansion

Horizontal shale and tight-formation drilling dominate North American activity and now shape overseas programs in Argentina’s Vaca Muerta. Extended-reach laterals require fiber-reinforced slurries that tolerate cyclic fracturing loads and mitigate lost circulation. Field pilots of foamed cement in low-pressure gradients demonstrated superior flow characteristics and lower formation damage compared to conventional systems.[1]ACS Omega Journal, “Performance of Foamed Cement in Shale Formations,” pubs.acs.org Larger-diameter casing programs elevate pump-rate demand, a shift that suppliers accommodate with high-horsepower automated units. The technological envelope developed for shale is transferable to emerging unconventional plays, providing a repeatable expansion avenue for the well-cementing services market.

Revival of Offshore Deep-Water Projects Accelerates Service Demand

More than 100 deep-water wells under a USD 800 million integrated contract between SLB and Petrobras illustrate the upcoming workload in Brazil’s Campos, Santos, and Espírito Santo basins. Ultra-deep jobs operate at temperatures of up to 525 °F and pressures exceeding 18,000 psi, necessitating shrink-on-heat spacer systems to prevent trapped annulus pressure.[2]OnePetro Library, “Heat-Activated Shrink Spacer for Deepwater Cementing,” onepetro.org Managed-pressure drilling enables cement placement in narrow pore-pressure margins, while digital twins cut commissioning time by validating designs before rig deployment. This technology mix underpins incremental revenue for the well-cementing services market as offshore final investment decisions move forward.

Mandatory Well Integrity Regulations Reshape Regional Markets

Asia-Pacific and Middle East regulators mandate dual-barrier designs, regular pressure test records, and certified high-temperature slurries that exceed API 5CT and 10th edition cement testing criteria.[3]American Petroleum Institute, “Specification 5CT 10th Edition,” api.org Digital well-integrity management systems incorporating analytics and artificial intelligence automate barrier verification and maintenance scheduling. Over 20,000 idle offshore wells identified for abandonment require compliant cement plugs, creating sustained remedial demand. These mandates lock in baseline activity for the well-cementing services market even when drilling cycles soften.

Accelerated Refracturing Programs Boost Remedial Cementing

Eagle Ford refracs delivered triple-digit returns for operators who deploy cemented liners to isolate depleted clusters and reopen new stages. Economic screening suggests that U.S. refracs could increase daily production by 1.28 million barrels of oil and 10.8 billion cubic feet of gas, with costs running 60-70% of those for new wells. Coiled-tubing conveyed diversion agents and high-rate pumps reduce trip time and cost. As asset maturity increases, remedial cementing’s share of the well cementing services market grows faster than that of primary work.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Service-price deflation cycles post-2026 | -0.90% | Global, acute in North America | Medium term (2-4 years) |

| Stringent ESG capital-allocation hurdles | -0.70% | Europe & North America | Long term (≥4 years) |

| Loss-circulation in ultra-deep HP/HT wells | -0.40% | Deep-water regions | Long term (≥4 years) |

| Geothermal-cement R&D diverting budgets | -0.30% | Geothermal-active regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Service-Price Deflation Cycles Challenge Profitability

Operator consolidation means fewer tenders and tougher bargaining leverage, pushing day rates down just as suppliers absorb higher R&D and raw material costs. U.S. exploration and production capital plans fell to USD 61.7-65.4 billion in 2024 from USD 66 billion in 2023.[4]Oil & Gas Journal, “US E&P Spending Outlook 2024,” ogj.com SLB’s ChampionX buy targets USD 400 million annual synergies to offset this margin squeeze. Pricing relief will hinge on rig-count recovery, but that may lag as larger producers prioritize dividends over volume growth.

Stringent ESG Capital Allocation Constrains Investment Decisions

Supermajors now allocate larger shares of capex to lower-carbon ventures. ExxonMobil maintains a total spending range of USD 23-25 billion, with a preference for CCUS and hydrogen assets. Upstream drilling, which drives the well cementing services market, faces tougher hurdle rates, especially in Europe, where regulatory scrutiny is intense. Yet, CCUS well construction partially compensates for lost hydrocarbon work, highlighting the advantages of technology overlap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Primary Cementing Dominates Despite Remedial Growth

Primary cementing generated the largest revenue in 2025 as every new well requires an initial barrier. In absolute terms, this segment underpins two-thirds of the well-cementing services market. Remedial work, however, posts the faster 6.52% CAGR as mature fields worldwide tackle annular pressure and water-shutoff challenges.

Technology differentiation now centers on CO₂-resistant additives, stage-cementing tools certified under API 19AC, and real-time density control. Halliburton’s Fidelis stage cementer, rated to 350°F, illustrates product evolution for multistage unconventional completions. These innovations enable service companies to capture value beyond basic pump time, thereby sustaining pricing power amid competitive bids in the well cementing services market.

By Well Type: Horizontal Wells Lead Growth Trajectory

Horizontal wells captured 43.12% of 2025 revenue thanks to prolific shale plays that use long laterals and high cluster counts. This configuration boosts top-line volumes because larger cement jobs are required to seal extended annuli, and centralization requirements intensify demand for hardware. Vertical wells remain common in conventional projects and CO₂ injection schemes; however, growth is tilting toward horizontals that deliver higher recovery.

Advances, such as Baker Hughes' XtremeSet formulation, tailored for HP/HT horizontals, improve strength retention at 20,000 psi. Uniform placement along a 10,000-ft lateral now benefits from rotating scratcher subs and real-time fluid modeling. These capabilities deepen service intensity, expanding the value pool for the well-cementing services market.

By Application Depth: Shallow Wells Dominate, Ultra-Deep Shows Promise

Shallow wells, those below 3,000 m, still account for over half of segment revenue because they encompass most shale, tight-oil, and conventional onshore wells worldwide. Standard Class G cements meet technical needs, enabling efficient mass production. Deep wells between 3,000 and 6,000 m, widespread in offshore basins, require high-density, low-permeability blends with silica flour to combat strength retrogression.

The ultra-deep subset above 6,000 m is small in volume but posts the quickest 8.26% CAGR. Self-healing epoxies resist micro-annulus development under repeated pressure-temperature cycling, while thixotropic spacers prevent gas intrusion at extreme conditions. Suppliers who field-test these blends gain an early-mover edge in the well-cementing services market.

By Location of Deployment: Onshore Dominance with Offshore Acceleration

Onshore projects accounted for 68.72% of 2025 revenue, as dense rig fleets in the United States, Canada, and the Middle East executed high-volume campaigns. Grid-powered cementing units, such as Hummingbird, reduce fuel costs and emissions, meeting operator ESG targets while trimming operating expenses. The reach of automated bulk plants further improves job readiness and slurry consistency.

Offshore, the 7.58% CAGR reflects a backlog of Brazilian pre-salt, Nigerian deep-water, and Gulf of Mexico projects. All-electric subsea systems and integrated managed-pressure drilling packages now couple with cementing spreads to ensure barrier reliability in narrow operating windows. As these technologies standardize, offshore contribution to the well cementing services market will climb even in lower-price scenarios.

Geography Analysis

North America maintains clear leadership, powered by shale productivity gains, rapid rig mobilization, and an established supply chain of bulk blending plants and pressure-pumping assets. Horizontal laterals now surpass 10,000 feet in the Permian, increasing slurry volumes per well and expanding the revenue base for the well-cementing services market. Electrified field equipment aligns with rising sustainability mandates, helping operators lower their Scope 1 emissions.

The Middle East and Africa region benefits from tier-one carbonate reservoirs that require complex HP/HT cementing and from aggressive gas-capacity additions to support domestic power demand. Mandatory barrier-verification rules and heavy sour-gas chemistry spur the adoption of corrosion-resistant cements, raising average job value. Deep-water discoveries in Namibia, Senegal, and the eastern Mediterranean add frontier upside for the well cementing services market.

The Asia-Pacific region shows steady gains as Malaysia and Indonesia sanction new offshore developments, and as China and Australia test shale pilot wells. A regulatory push for full-life-cycle well-integrity management increases remedial demand, while high geothermal gradients in Indonesia accelerate high-temperature R&D investments. Europe concentrates its spending on plug-and-abandonment campaigns in the North Sea and on geothermal wells in Iceland and Germany, balancing lower hydrocarbon drilling. South America relies on Brazil’s pre-salt drilling cadence and Argentina’s Vaca Muerta growth to anchor regional momentum.

Competitive Landscape

Halliburton, SLB, and Baker Hughes account for a combined majority of global revenue, leveraging integrated portfolios that include surface logging, drilling fluids, and production chemistry. Halliburton’s LOGIX platform enhances job repeatability through remote density control and predictive maintenance, providing operators with confidence in barrier compliance. SLB’s ChampionX integration adds production and artificial-lift synergies, unlocking cross-selling at minimal capital intensity.

Pricing power remains under pressure from operator consolidation; however, technology-led service differentiation helps protect margins. Baker Hughes secured a multi-year Brazilian plug-and-abandonment contract covering cementing, wireline, and intervention services valued at hundreds of millions of dollars. Smaller specialists thrive in niche areas such as expandable casing or lightweight cement additives, but face hurdles scaling automation investments.

Digitalization is the primary competitive battleground. Generative AI engines analyze historical cement job data to recommend optimal slurry blends, while digital twins simulate fluid dynamics in real-time. Early adopters lower design iterations, thereby shrinking well construction costs and strengthening the long-term appeal of the well-cementing services market.

Well Cementing Services Industry Leaders

Schlumberger Ltd

Halliburton Company

Baker Hughes Company

China Oilfield Services

Weatherford International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Baker Hughes won a multi-year Petrobras contract for workover and plug-and-abandonment services, commencing in 1H 2025.

- June 2025: Chevron and Halliburton deployed ZEUS IQ™ intelligent fracturing technology in pilot wells in Colorado.

- April 2025: Baker Hughes introduced Hummingbird™ 100% electric land cementing unit for emissions-free operations.

- December 2024: SLB secured a USD 800 million integrated services award from Petrobras for more than 100 deep-water wells.

Global Well Cementing Services Market Report Scope

Essentially, well-cementing consists of two principle operations, primary cementing and remedial cementing. Primary cementing involves placing a cement sheath between the casing and the formation. The purpose of remedial cementing is to repair and abandon wells by injecting cement into strategic well locations after primary cementing has been completed.

Well Cementing Services Market is segmented by location of deployment, type, and geography. By location of deployment, the market is segmented into onshore and offshore. By type, the market is segmented into primary, remedial, and others. The report also covers the market size and forecasts for the Well Cementing Services Market across major regions. The market size and forecasts for each segment have been done regarding revenue (USD billion).

| Primary |

| Remedial/Squeeze |

| Plug and Abandonment |

| Liner-Tie/Stage Cementing |

| Vertical |

| Directional |

| Horizontal |

| Shallow (Below 3,000 m) |

| Deep (3,000 to 6,000 m) |

| Ultra-deep (Above 6,000 m) |

| Onshore |

| Offshore |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Service Type | Primary | |

| Remedial/Squeeze | ||

| Plug and Abandonment | ||

| Liner-Tie/Stage Cementing | ||

| By Well Type | Vertical | |

| Directional | ||

| Horizontal | ||

| By Application Depth | Shallow (Below 3,000 m) | |

| Deep (3,000 to 6,000 m) | ||

| Ultra-deep (Above 6,000 m) | ||

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the well cementing services market?

The well cementing services market size reached USD 11.6 billion in 2026 and is projected to rise to USD 14.98 billion by 2031.

Which region leads global revenue?

North America led with 36.95% revenue share in 2025, driven by high unconventional drilling density.

What segment is growing the fastest?

Ultra-deep well cementing posts the fastest 8.26% CAGR thanks to frontier exploration and geothermal projects.

How are ESG pressures affecting demand?

Stricter ESG capital allocation slows some hydrocarbon drilling but lifts demand for CCUS and high-integrity cement systems that limit environmental risk.

What role does automation play in cementing services?

Automated units like Halliburton’s LOGIX™ and Baker Hughes’ Hummingbird™ improve slurry accuracy, cut crew exposure, and support cost-efficient operations.

How consolidated is the competitive landscape?

Three integrated providers control more than 65% of global revenue, but niche specialists remain influential in high-end additives and regional markets.

Page last updated on: