Managed Pressure Drilling Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

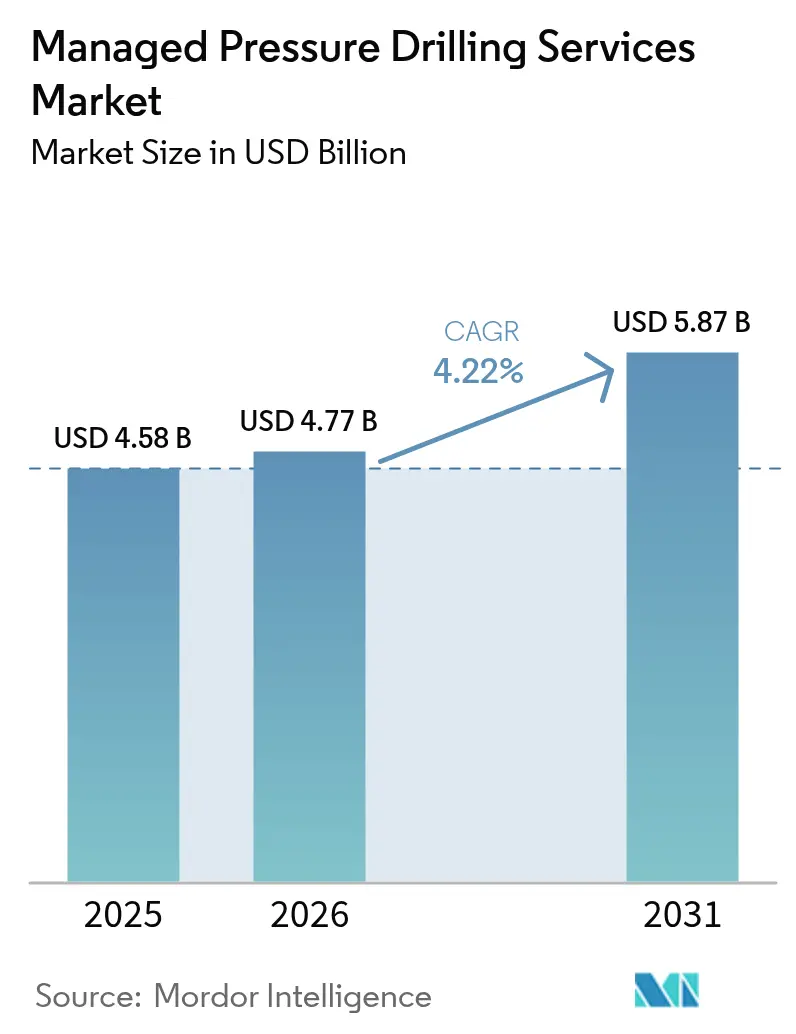

| Market Size (2026) | USD 4.77 Billion |

| Market Size (2031) | USD 5.87 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

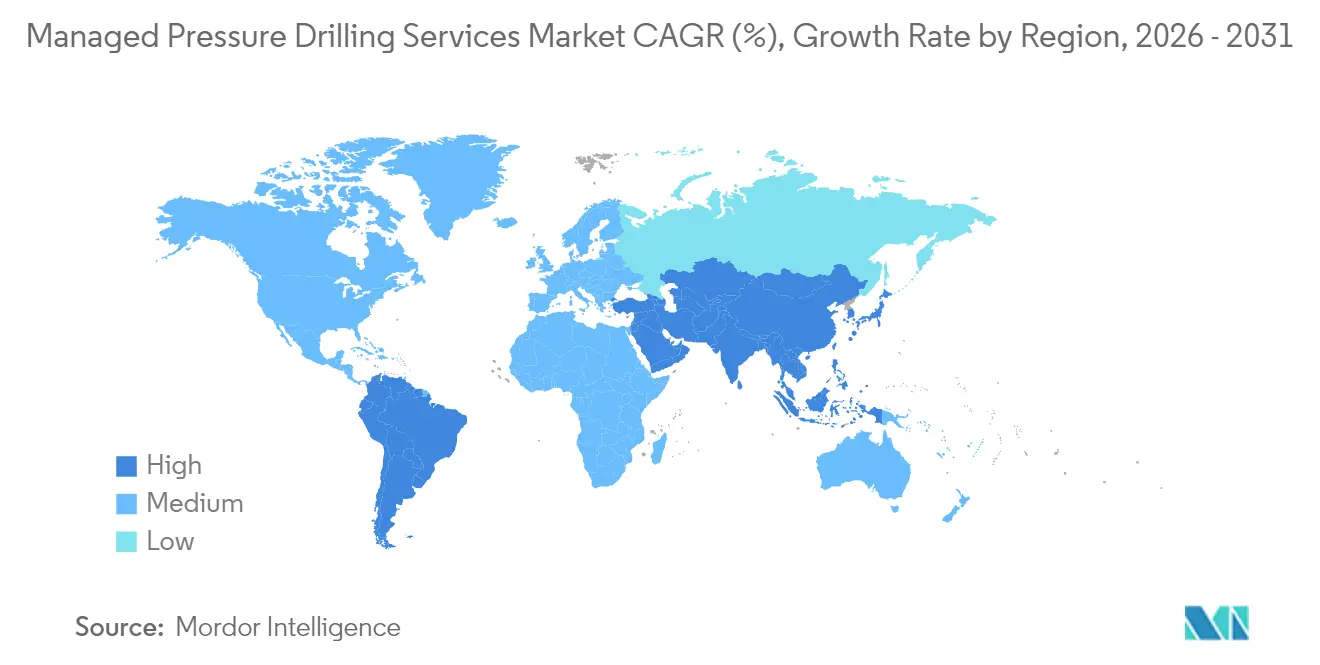

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

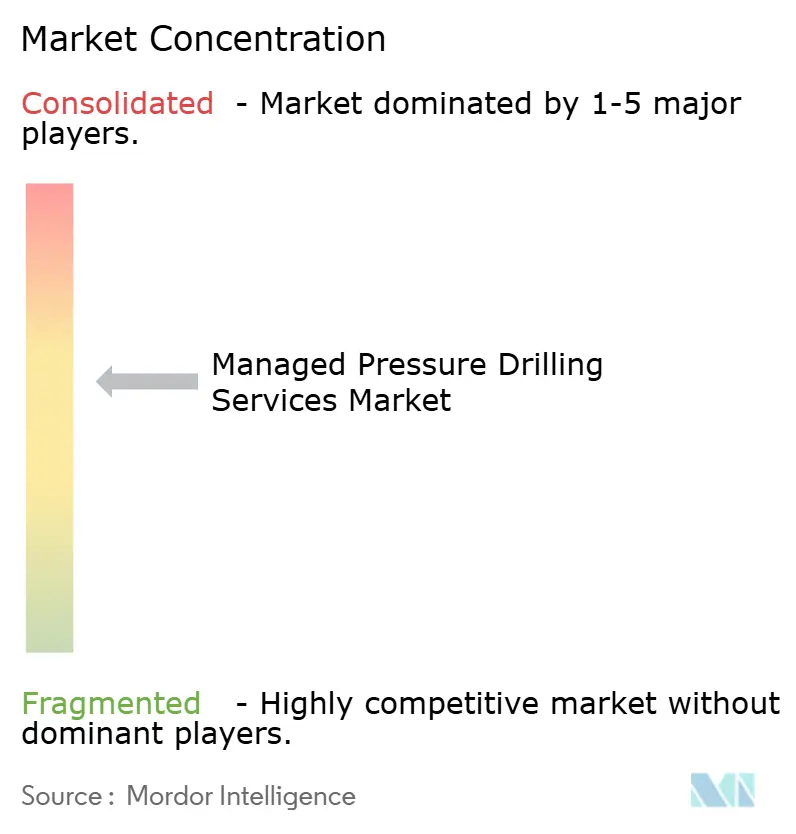

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed Pressure Drilling Services Market Analysis by Mordor Intelligence

The Managed Pressure Drilling Services market size is expected to grow from USD 4.58 billion in 2025 to USD 4.77 billion in 2026 and is forecast to reach USD 5.87 billion by 2031 at 4.22% CAGR over 2026-2031.

Industry momentum is rooted in deepwater capital expenditure recovery, surging HPHT activity, and rapid automation that lets operators manage narrower pressure margins with fewer crew. Dual-gradient innovations, carbon capture projects, and geothermal well mandates provide fresh revenue lanes, while rig-day-rate volatility and certified crew shortages temper near-term spending. Market leaders Halliburton, SLB, and Weatherford emphasise AI-enabled pressure automation to secure premium contracts, whereas niche specialists target hydrogen-ready and geothermal wells. Operators increasingly favour integrated equipment-plus-execution packages, allowing service companies to capture higher wallet share and accelerate technology upgrades.

Key Report Takeaways

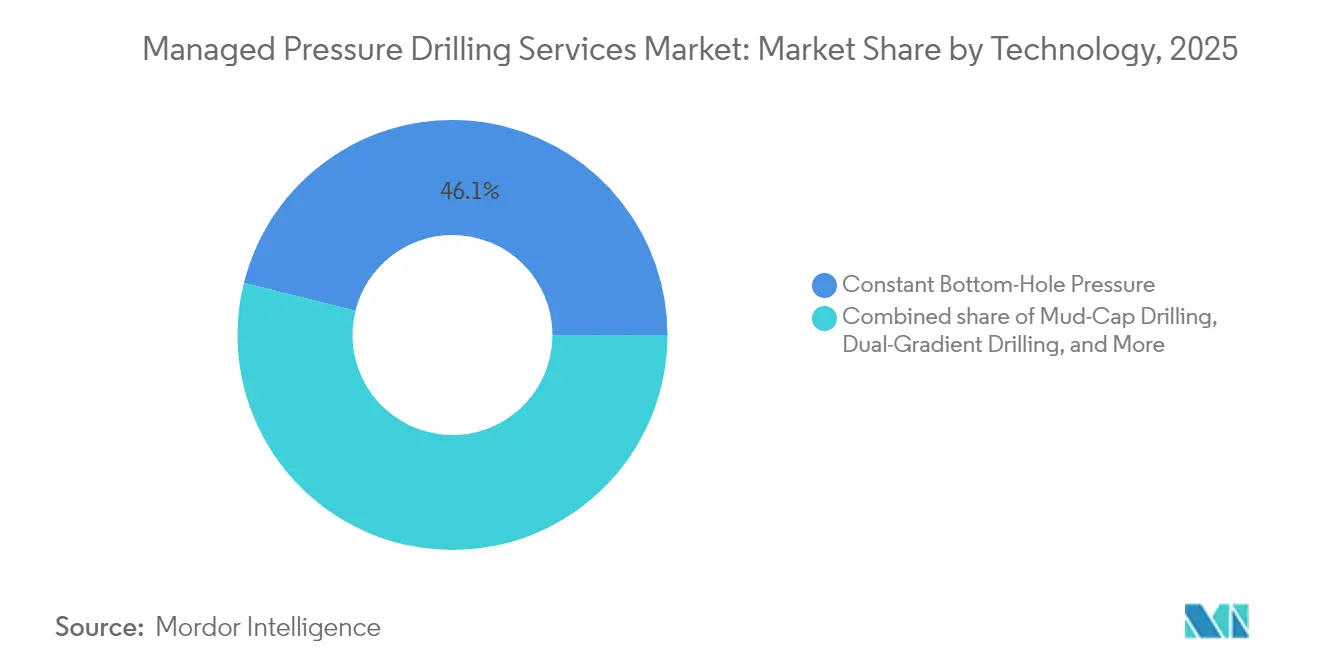

- By technology, constant bottom-hole pressure techniques led with 46.10% of managed pressure drilling services market share in 2025, while dual-gradient drilling is projected to advance at a 5.95% CAGR through 2031.

- By service type, equipment rental held 47.70% of revenue in 2025; operations and execution services are forecast to record a 5.55% CAGR to 2031 as operators seek turnkey offerings.

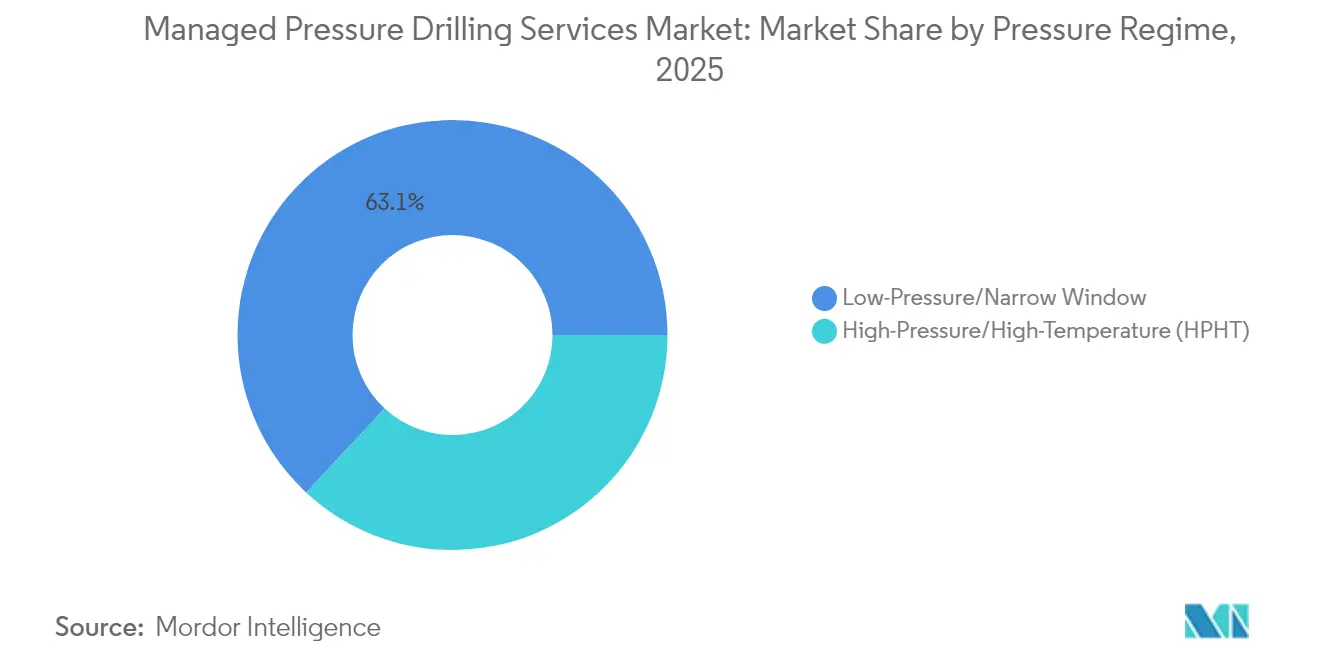

- By pressure regime, low-pressure/narrow window applications captured 63.10% share in 2025; HPHT environments are rising fastest at a 6.12% CAGR, especially across the Middle East and North Africa.

- By well type, development production wells commanded 53.20% of the managed pressure drilling services market size in 2025, whereas wildcat/exploration wells are set to expand at a 6.02% CAGR.

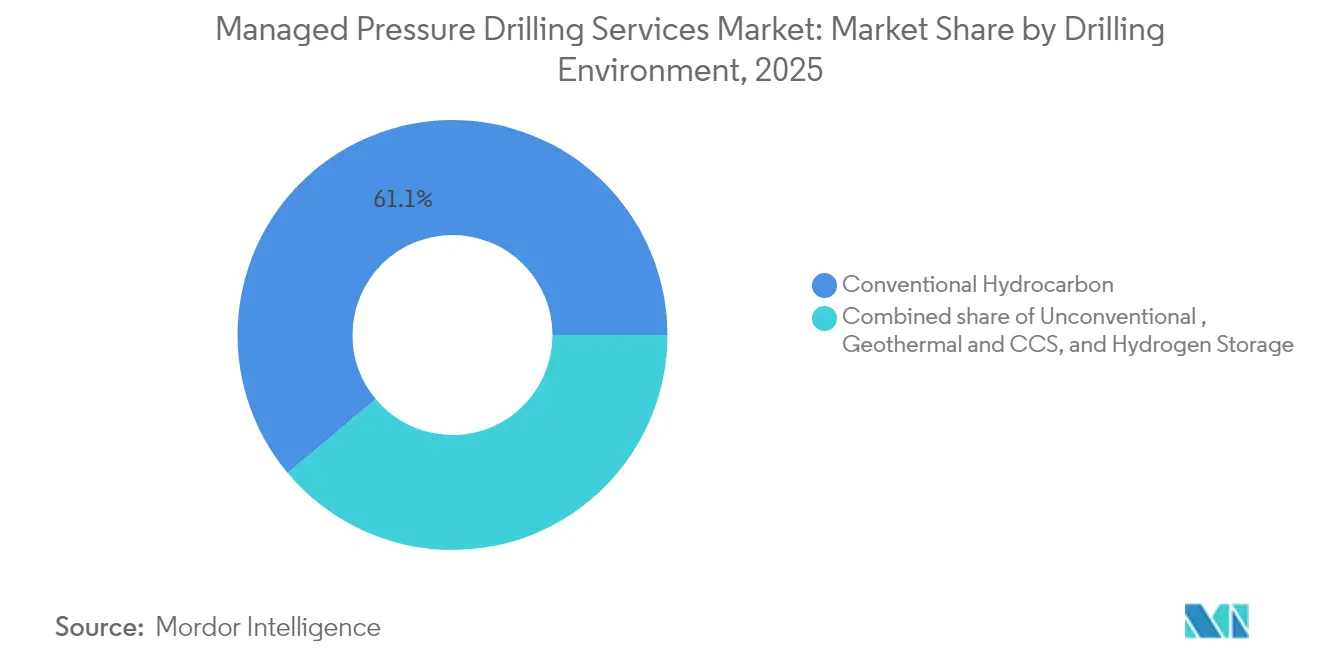

- By drilling environment, conventional hydrocarbon projects kept 61.10% share in 2025, but unconventional formations are growing at 6.35% CAGR, driven by North American shale refracs and European geothermal wells.

- By application, onshore projects represented 64.50% of 2025 revenue, and offshore developments are expected to climb at a 5.72% CAGR on the back of deepwater sanctions recovery.

- By geography, North America led with 38.10% revenue share in 2025, while Asia-Pacific is forecast to post the fastest 6.82% CAGR to 2031 on heightened unconventional drilling in China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Managed Pressure Drilling Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating deep-water CAPEX rebound | +1.2% | Gulf of Mexico, Brazil, West Africa | Medium term (2-4 years) |

| Surge in HPHT well development in MENA | +0.8% | Middle East & North Africa; spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Post-2025 shale refrac wave in North America | +0.6% | Permian & Eagle Ford basins | Short term (≤ 2 years) |

| AI-driven downhole pressure automation | +0.5% | Early use in North America & North Sea | Medium term (2-4 years) |

| CCS & hydrogen-ready well design standards | +0.3% | North America & EU; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Mandatory MPD adoption for EU geothermal | +0.2% | European Union; potential global standardisation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Deep-water CAPEX Rebound

Sanctioned deepwater budgets have exceeded USD 200 billion annually since 2022, reversing the 2015-2020 investment drought and fuelling fresh demand for managed pressure drilling services market deployments[1]Journal of Petroleum Technology, “Deepwater CAPEX Resurgence Spurs MPD Demand,” jpt.spe.org. Chevron’s USD 5.7 billion Anchor project illustrates the shift, employing 20,000 psi systems that rely on sophisticated MPD to drill safely in ultra-narrow windows. Drillship utilisation nearing 97% in 2025 prioritises rigs fitted with advanced pressure control, allowing contractors to command premium dayrates. Each sanctioned deepwater campaign typically entails multiple MPD-enabled wells across exploration, appraisal, and production phases, compounding service demand. Technology differentiation remains a pivotal competitive lever for service providers positioning for multi-year contract backlogs.

Surge in HPHT Well Development in MENA

National oil companies across the Middle East and North Africa target reservoirs exceeding 15,000 psi and 350 °F, where managed pressure drilling services market solutions become indispensable for safe wellbore construction. Automated rotary and slide drilling executed in Oman by Halliburton and Nabors underscores how AI-enhanced MPD is fast becoming standard operating practice [2]Halliburton, “Automated Rotary & Slide Drilling in Oman,” halliburton.com. Regulatory frameworks in Saudi Arabia, the UAE, and Qatar now require MPD on wells surpassing defined pressure thresholds, accelerating adoption. As HPHT projects proliferate, service providers with proven HPHT toolkits and crew availability enjoy a clear advantage.

Post-2025 Shale Refrac Wave in North America

North American producers are pivoting capital toward refracturing legacy shale wells to amplify recovery, unlocking up to USD 2 billion in value from 400 Bakken candidates alone. Devon Energy registered an 8% production uplift in Q1 2024 from Eagle Ford refracs, validating the economic payoff. Refrac operations often entail complex multi-zone pressure management that puts MPD equipment and expertise at the heart of investment decisions. Integrated equipment-plus-execution packages resonate with operators seeking predictable cost and schedule outcomes amid crew tightness.

AI-driven Downhole Pressure Automation

Real-time optimisation platforms such as Halliburton’s LOGIX deliver 30% rate-of-penetration gains while slashing manual commands by roughly 5,000 per well, highlighting the operational efficiency upside. SLB’s Neuro system recorded 25 autonomous trajectory changes in Ecuador, proving the value of machine learning for geosteering and pressure modulation. Corva’s cloud analytics cuts well costs by USD 100,000-150,000 through predictive pressure control. The cumulative effect reduces non-productive time, mitigates crew shortages, and elevates safety, amplifying the technology’s attraction across the managed pressure drilling services market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile rig-day rates squeezing MPD budgets | -0.7% | Global, particularly offshore markets | Short term (≤ 2 years) |

| Limited global pool of certified MPD crews | -0.5% | Global, acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Persistent data-ownership disputes in JV wells | -0.3% | Global, concentrated in international joint ventures | Medium term (2-4 years) |

| Stricter drilling-fluid discharge limits in offshore Arctic | -0.2% | Arctic regions, primarily Norwegian and Canadian Arctic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Rig-day Rates Squeezing MPD Budgets

Harsh-environment semisubs commanded USD 390,000-510,000 per day in 2024, a nine-year high that narrowed discretionary drilling spend. MPD services typically add 15-25% to total well costs, so sudden rate spikes lead operators to defer or downgrade deployments. Ownership models such as TotalEnergies’ majority stake in a high-spec drillship highlight efforts to tame escalating costs. While rig rates are expected to ease modestly by 2026, the boom-bust cycle underpins cautious MPD budgeting.

Limited Global Pool of Certified MPD Crews

MPD crews require blended competencies in conventional drilling, real-time data interpretation, and automated pressure control, yet global training capacity lags demand [3]OnePetro, “Global MPD Crew Competency Gaps,” onepetro.org. Local content mandates compound shortages in markets such as India, Indonesia, and Nigeria, where nationalisation targets outstrip trained personnel numbers. Crew scarcity inflates service rates and stretches project schedules, compelling contractors to accelerate simulator-based training and remote-support models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Dual-Gradient Innovation Accelerates

Constant bottom-hole pressure methods contributed 46.10% to the managed pressure drilling services market size in 2025, reflecting their broad applicability across shelf, HPHT, and onshore wells. However, dual-gradient systems are climbing at a 5.95% CAGR to 2031 as deepwater operators exploit their ability to decouple mudweight from riser pressure, lowering downhole stress and improving kick tolerance.

The dual-gradient surge coincides with integrated seabed pump deployments synchronizing with surface control loops for rapid pressure corrections. AI-linked sensors fine-tune bottomhole pressure analytics, cutting wellbore ballooning events. Mud-cap drilling remains niche for total-loss scenarios, and return-flow control methods serve laterals in shale plays, yet both benefit from the broader automation wave permeating the managed pressure drilling services market.

By Service Type: Operations Integration Drives Growth

Equipment rental held 47.70% revenue in 2025 as operators avoided capital commitments tied to specialised manifolds, chokes, and rotating control devices. The managed pressure drilling services market size for operations and execution packages is forecast to rise faster at a 5.55% CAGR, propelled by crew scarcity and risk-sharing incentives.

Integrated contracts bundle hardware with certified personnel, real-time analytics, and performance guarantees, letting operators transfer execution risk while accessing the latest toolsets. Design and engineering services maintain a stable demand, particularly for frontier HPHT and CCS wells requiring bespoke hydraulics modelling. Training and support demand is swelling as contractors race to certify national crews and enable remote operations centres.

By Pressure Regime: HPHT Applications Accelerate

Low-pressure/narrow window projects dominated with 63.10% revenue in 2025, underscoring MPD’s roots in mature fields where formation stability is critical . Yet HPHT wells are expanding at 6.12% CAGR on the back of Middle East carbonate plays, US GoM ultra-deepwater, and Asia-Pacific deep targets.

Chevron’s Anchor well illustrates the frontier as 20,000 psi-rated BOPs force simultaneous MPD integration to mitigate surge-swab risks. New US Bureau of Safety and Environmental Enforcement rules effective October 2024 elevate pressure-control compliance, strengthening HPHT MPD demand. Vendors are responding with 20,000-psi rotating heads and high-temperature elastomers, extending the managed pressure drilling services market reach.

By Well Type: Exploration Complexity Drives Innovation

Development production wells delivered 53.20% of the managed pressure drilling services market size in 2025 due to repeatable programmes in the shelf and onshore fields. Exploration wells, however, are set to expand at a 6.02% CAGR because unknown pore-pressure regimes amplify risk-reduction incentives.

Wildcat wells in Sierra Leone, Namibia, and Suriname now budget MPD from spud to mitigate blowout risk and data uncertainty. Work-over and re-entry niches grow as operators refrac shale laterals or sidetrack ageing offshore wells, requiring real-time pressure juggling around existing casing and completions.

By Drilling Environment: Unconventional Surge Continues

Conventional hydrocarbons retained a 61.10% share in 2025, yet unconventional formations are on a 6.35% CAGR trajectory as North American refracs and multi-stage shale completions seek tighter pressure windows. European geothermal wells are another bright spot. Mandatory MPD clauses now appear in French Alsace tenders, and Italian operators trial geothermal MPD to pre-empt lost-circulation and induced seismicity. Carbon storage pilot projects in the Netherlands and California deploy MPD to protect caprock integrity during CO₂ injection, marking new horizons for the managed pressure drilling services market.

By Application: Offshore Technology Push

Onshore projects generated 64.50% of 2025 revenue thanks to prolific US shale, Middle East HPHT land rigs, and Latin American heavy-oil fields. Offshore demand is projected to lift at a 5.72% CAGR, anchored by Brazil’s pre-salt, Gulf of Mexico ultra-deepwater, and West Africa frontier plays .

Floating drilling units face heave, loop-current, and riser-pressure complications, making MPD hardware integration more complex but essential. Contractors retrofit older drillships with subsea rotating devices and riser-pressure control modules to secure higher utilisation, a trend that underpins the managed pressure drilling services market’s offshore momentum.

Geography Analysis

North America preserved a 38.10% revenue lead in 2025 as shale refracs, Permian HPHT horizontals, and Gulf of Mexico ultra-deepwater wells collectively boosted MPD demand. Early adoption of AI-enabled pressure automation and an established training infrastructure keeps service costs competitive. Mexico’s Trion field, backed by SLB’s integrated drilling contract, signals deeper regional penetration of MPD for national oil companies.

Asia-Pacific is the fastest-growing managed pressure drilling services market segment, set for a 6.82% CAGR to 2031. China’s push into 8-km deep Shunbei wells and Sichuan over-pressured shales requires precise pressure envelopes to avoid H₂S influx. India’s rig count is projected to rise from 111 in 2024 to 142 by 2028, creating incremental MPD demand for offshore KG basin HPHT wells and onshore Rajasthan appraisal campaigns. Southeast Asia revives deepwater gas prospects in Malaysia and Indonesia, while Australia preps CCS pilot wells aligned with net-zero targets.

Europe shows steady growth fuelled by North Sea HPHT wells, Baltic CCS pilots, and geothermal hotspots in Germany and France. The EU’s stringent well-integrity rules embed MPD in licensing conditions for geothermal and CCS wells, reinforcing technology pull. Norway’s full-field MPD adoption standard further diffuses best practice across the continent.

The Middle East and Africa benefit from HPHT carbonate developments in Saudi Arabia and Qatar, plus emerging deepwater campaigns in Namibia and Angola. National oil company mandates and HPHT targets underpin robust demand, though crew localisation remains a bottleneck. Brazil’s pre-salt and Argentina’s unconventional Vaca Muerta drive anchor South America's growth.

Competitive Landscape

The managed pressure drilling services market is moderately fragmented. Halliburton, SLB, and Weatherford hold substantial shares, supported by global infrastructure and proprietary automation platforms. Halliburton’s LOGIX secured multiple North Sea contracts after demonstrating 30% penetration gains and lower downhole incidents. SLB’s 18-well Trion award in Mexico validates its AI-based Neuro stack and integrated service bundle strategy.

Partnerships remain critical. Halliburton teamed with Sekal to deliver the world’s first automated on-bottom drilling system for Equinor, integrating real-time hydraulics and drilling parameter optimisation. Nabors embeds MPD within its rig fleet, offering “MPD-ready” charters that shorten mobilisation schedules and cut interface risk. Enhanced Drilling captures niche Arctic and geothermal projects with sea-floor pump variants tailored for cold-water rheology.

Consolidation is ongoing. Helmerich & Payne’s USD 2 billion buyout of KCA Deutag broadens onshore reach and MPD capability, while SLB’s planned acquisition of ChampionX aims to merge drilling and completions chemistry insights with real-time pressure management. These moves herald a pivot toward vertically integrated well-construction suites that package rigs, digital workflows, and MPD in a single commercial offering, reshaping pricing and differentiation levers across the managed pressure drilling services market.

Managed Pressure Drilling Services Industry Leaders

Schlumberger Limited

Nabors Industries Ltd

Weatherford International PLC

Halliburton Company

NOV Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SLB won Woodside Energy’s ultra-deepwater Trion contract offshore Mexico, covering 18 wells with AI-enabled drilling and integrated services.

- February 2025: Halliburton and Sekal delivered the world’s first automated on-bottom drilling system for Equinor in the North Sea, merging LOGIX automation with Drilltronics.

- January 2025: SLB received multi-region deepwater awards from Shell to deploy digital drilling optimisation across the UK North Sea and the Gulf of Mexico.

- December 2024: SLB landed a USD 800 million integrated deepwater services deal from Petrobras for over 100 wells across nine rigs in Brazil.

Global Managed Pressure Drilling Services Market Report Scope

The managed pressure drilling services market report includes:

| Constant Bottom-Hole Pressure |

| Mud-Cap Drilling |

| Dual-Gradient Drilling |

| Return-Flow Control Drilling |

| Other Emerging Techniques |

| Design and Engineering |

| Equipment Rental |

| Operations and Execution |

| Training and Support |

| Low-Pressure/Narrow Window |

| High-Pressure/High-Temperature (HPHT) |

| Wildcat/Exploration |

| Development Production |

| Work-over and Re-entry |

| Conventional Hydrocarbon |

| Unconventional (Shale, Tight, CBM) |

| Geothermal |

| CCS and Hydrogen Storage |

| Onshore |

| Offshore |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Technology | Constant Bottom-Hole Pressure | |

| Mud-Cap Drilling | ||

| Dual-Gradient Drilling | ||

| Return-Flow Control Drilling | ||

| Other Emerging Techniques | ||

| By Service Type | Design and Engineering | |

| Equipment Rental | ||

| Operations and Execution | ||

| Training and Support | ||

| By Pressure Regime | Low-Pressure/Narrow Window | |

| High-Pressure/High-Temperature (HPHT) | ||

| By Well Type | Wildcat/Exploration | |

| Development Production | ||

| Work-over and Re-entry | ||

| By Drilling Environment | Conventional Hydrocarbon | |

| Unconventional (Shale, Tight, CBM) | ||

| Geothermal | ||

| CCS and Hydrogen Storage | ||

| By Application | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the managed pressure drilling services market?

The market was valued at USD 4.77 billion in 2026, with a forecast to reach USD 5.87 billion by 2031 at a 4.22% CAGR.

Which technology segment is growing the fastest?

Dual-gradient drilling is expected to post a 5.95% CAGR through 2031 due to its superior performance in deepwater wells.

Why is Asia-Pacific the fastest-growing regional market?

Aggressive ultra-deep and unconventional drilling in China plus India’s expanding rig fleet drive a projected 6.82% regional CAGR.

How are AI systems changing MPD operations?

AI platforms such as LOGIX and Neuro automate real-time pressure control, increasing penetration rates by up to 30% while reducing crew workload.

What restrains wider MPD adoption?

High rig-day-rate volatility and a limited pool of certified MPD crews are the main barriers, trimming forecast CAGR by a combined 1.2 percentage points.

Which emerging applications will boost future demand?

Carbon capture storage wells, geothermal drilling mandates in the EU, and hydrogen storage pilots are set to widen MPD’s addressable market over the next decade.

Page last updated on: