VoLTE Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 86.84 Billion |

| Market Size (2031) | USD 513.23 Billion |

| Growth Rate (2026 - 2031) | 42.65% CAGR |

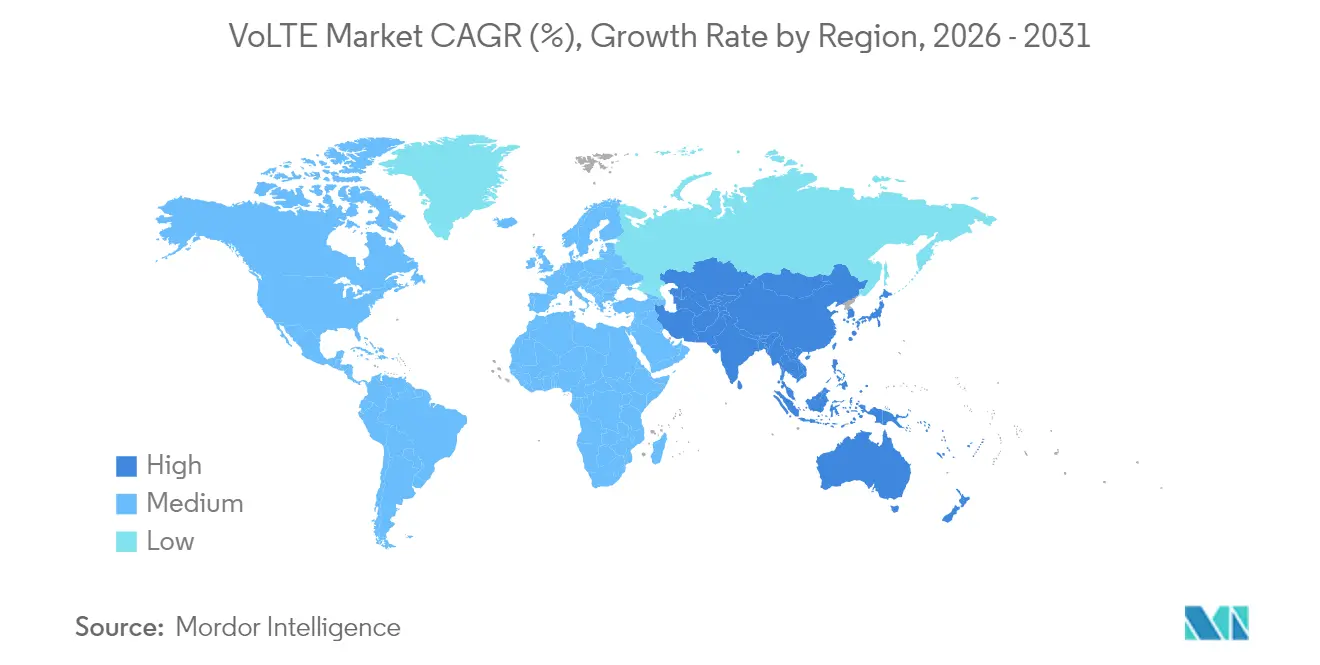

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

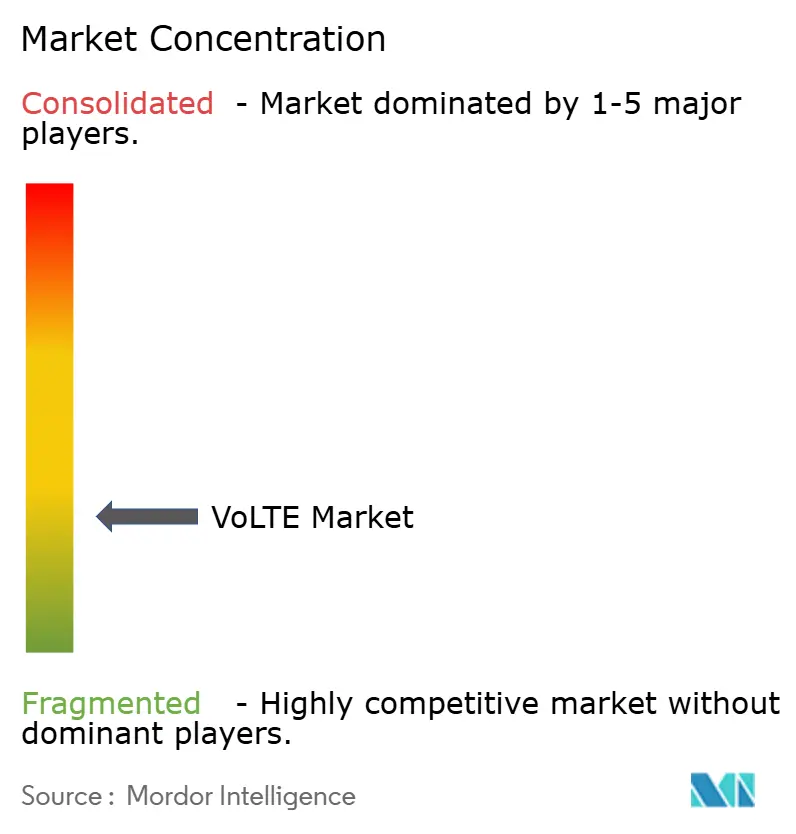

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

VoLTE Market Analysis by Mordor Intelligence

The VoLTE Market size was valued at USD 60.88 billion in 2025 and estimated to grow from USD 86.84 billion in 2026 to reach USD 513.23 billion by 2031, at a CAGR of 42.65% during the forecast period (2026-2031).

Explosive adoption follows the switch-off of 3G networks, spectrum refarming for 5G, and operators’ need to deliver high-quality voice on all-IP infrastructure. Operators that complete VoLTE migration improve spectrum efficiency, cut legacy operating costs, and secure a fallback voice layer for 5G NSA deployments. North America’s early LTE maturity and aggressive 3G sunsets underpin its 40% 2024 revenue share, while Asia-Pacific’s massive subscriber base and state-sponsored digital initiatives drive the fastest 47.2% CAGR. Commercial subscribers dominate with 41.2% share, yet government and public-safety users expand at 45.3% CAGR because mission-critical agencies require resilient broadband voice. Technology migration is at an inflection point: Circuit-Switched Fallback still carries 60% of 2024 calls, but Voice over IMS leads future growth at 46.2% CAGR, highlighting the strategic pivot to native IP voice solutions.

Key Report Takeaways

- By geography, North America held 39.45% of VoLTE market share in 2025; Asia-Pacific is forecast to expand at a 45.8% CAGR through 2031.

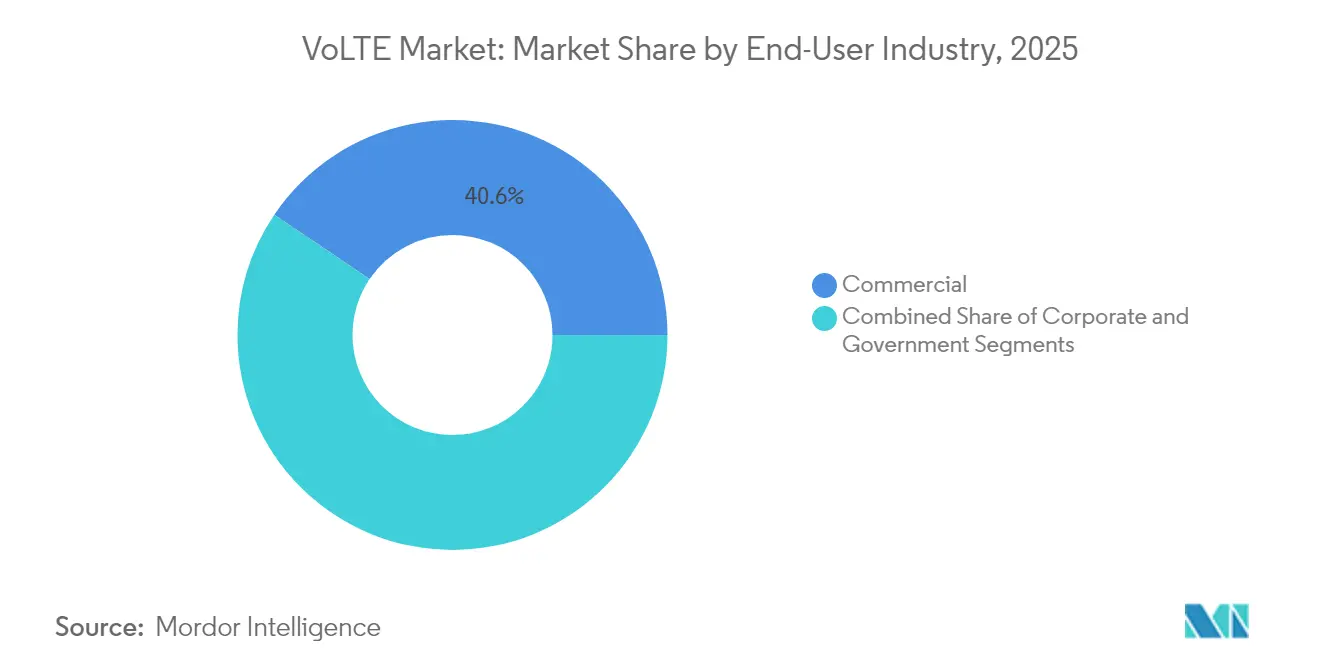

- By end-user, the Commercial segment led with 40.55% revenue share in 2025; Government applications are advancing at a 43.9% CAGR to 2031.

- By technology, Circuit-Switched Fallback accounted for 59.2% share of the VoLTE market size in 2025, while Voice over IMS is projected to grow at a 44.3% CAGR through 2031.

- By device, Smartphones commanded 66.85% share of the VoLTE market size in 2025; IoT Modules & Wearables are expanding at a 45% CAGR between 2026-2031.

- By operator type, Mobile Network Operators captured 71.55% of VoLTE market share in 2025; Private/Enterprise LTE networks record the highest 43.8% CAGR through 2031.

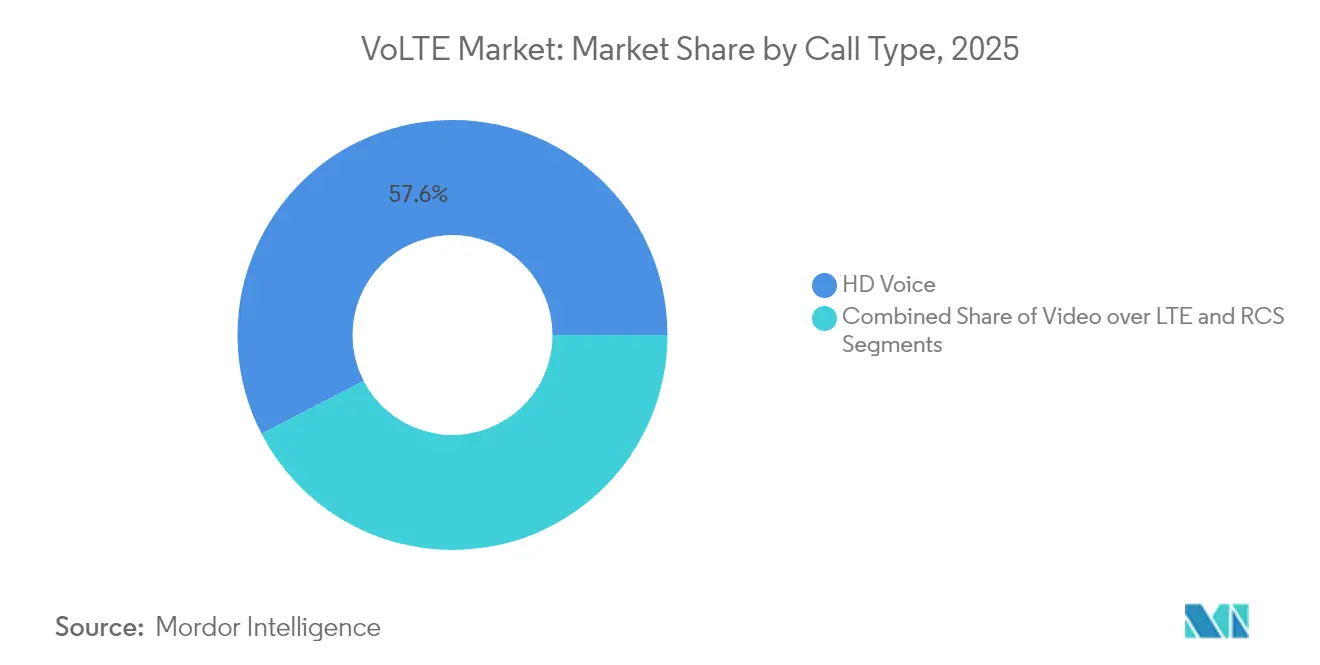

- By call type, HD Voice represented 57.60% of revenue in 2025; Rich Communication Services adoption is rising at a 47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global VoLTE Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-speed mobile broadband voice demand | +8.2% | Global (North America & APAC focus) | Medium term (2-4 years) |

| LTE coverage & smartphone penetration | +7.8% | Primarily APAC; MEA & Latin America spill-over | Long term (≥ 4 years) |

| 3G regulatory sunsets | +9.1% | North America & EU first, then APAC | Short term (≤ 2 years) |

| Enterprise private-LTE for mission-critical voice | +6.5% | North America, Western Europe, select APAC | Medium term (2-4 years) |

| eSIM-centric device ecosystem | +4.3% | Global premium devices | Long term (≥ 4 years) |

| 5G NSA fallback requirement | +8.7% | Markets with advanced 5G rollouts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing LTE Network Coverage & Smartphone Penetration

LTE now covers around 95% of populations in developed economies and continues to scale across emerging markets. Smartphone penetration surpassed 74% worldwide in 2024, and most 5G-capable devices ship with VoLTE enabled out-of-box. Operators migrate voice traffic to VoLTE to reclaim 3G spectrum and lower operating costs. Wider rural LTE footprints in India and Brazil, often co-funded by governments, extend VoLTE to previously underserved communities. The alignment of network readiness, device capability, and policy incentives positions VoLTE as the default voice layer during the 4G-to-5G transition.

Regulatory Sunset of 3G Networks Accelerating VoLTE Migration

The FCC’s mandated 3G switch-off schedule and Europe’s 2025 sunset recommendation eliminate fallback circuit-switched voice, compelling operators to provision.[1]European Communications Committee, “Report 335 on 3G Sunset,” cept.org Rapid spectrum refarming for 5G and stringent E911 location-accuracy rules make VoLTE implementation non-negotiable. Equipment vendors gain from brisk IMS core upgrades, and operators report quicker pay-back on VoLTE CAPEX through lower energy costs and reduced legacy maintenance. [2]National Emergency Number Association, “E911 Phase II Requirements,” nena.org

Enterprise Private-LTE Adoption for Mission-Critical Voice

Factories, logistics hubs, and public-safety agencies replace patchy Wi-Fi and narrowband radio with private LTE voice that guarantees deterministic quality of service. The Citizens Broadband Radio Service in the United States accelerates deployments by offering lightly licensed spectrum. Integrated VoLTE supports industrial automation alerts, push-to-talk for first responders, and voice-controlled robotics, broadening the addressable opportunity beyond traditional consumer subscribers.

5G NSA Deployments Requiring VoLTE for Fallback Voice Continuity

Non-Standalone 5G relies on LTE anchoring for voice. Operators rolling out 5G NR must also optimize VoLTE to avoid dropped calls during inter-radio handoffs. Until full Voice over 5G standards mature post-2027, VoLTE remains the mandatory voice layer in dual-connectivity networks, sustaining investment momentum and reinforcing its relevance well into the 2030 horizon. [3]Ericsson AB, “5G Core and VoLTE Interworking,” ericsson.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited awareness in low-income nations | -3.2% | Sub-Saharan Africa, parts of South Asia, rural Latin America | Long term (≥ 4 years) |

| Roaming/inter-operator interoperability | -2.8% | Global business-travel corridors | Medium term (2-4 years) |

| Voice over 5G cannibalization risk | -4.1% | Early 5G SA markets | Long term (≥ 4 years) |

| Battery drain & QoS in dense networks | -2.3% | Urban small-cell clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Awareness and Slow Adoption in Low-Income Nations

Subscribers in low-income regions prioritize basic connectivity, so VoLTE’s value proposition remains unclear. Feature-phone prevalence and device affordability gaps stall migration even where LTE coverage exists. Operator campaigns must emphasize tangible benefits such as clearer audio and simultaneous voice-data functionality while aligning with government digital-literacy drives.

Roaming/Inter-Operator Interoperability Challenges

Bilateral roaming deals and inconsistent IMS implementations cause call drops for international travelers. The GSMA’s VoLTE roaming specs progress slowly, and operators incur high testing costs to certify each pairing. Until roaming is seamless, some subscribers fall back to OTT apps, undermining VoLTE’s reliability perception.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Government Drives Mission-Critical Adoption

Government agencies accounted for a 43.9% CAGR through 2031, though the Commercial segment retained the largest 40.55% share of VoLTE market size in 2025. Federal and municipal bodies adopt VoLTE to modernize public-safety communications, integrate broadband push-to-talk, and meet stringent security mandates. First responders in the United States migrate to FirstNet’s VoLTE-enabled broadband, enabling multimedia situational awareness.

Expanding smart-city programs employ VoLTE as a resilient fallback for IoT telemetry and emergency alerts. Defense departments deploy encrypted VoLTE on private networks to simplify voice procurement and maintenance. Commercial enterprises leverage existing smartphone fleets to embed HD voice into unified communications, supporting hybrid work and customer-service workflows without heavy hardware investments.

By Device Category: IoT Expansion Beyond Traditional Voice

Smartphones retained 66.85% of VoLTE market share in 2025, yet IoT Modules and Wearables log the strongest 45% CAGR. Asset trackers integrate VoLTE modules to relay voice alarms during intrusions, while smartwatches gain autonomous calling functions. Automakers embed VoLTE for automatic crash notification and concierge calling, adding incremental service revenue for operators and OEMs.

Lower-cost feature phones with VoLTE widen addressable bases in emerging markets where OTT voice alternatives consume excessive data. Enterprise IoT deployments require carrier-grade voice for control-room escalation during system faults, converting machines into voice end-points and enlarging the VoLTE market.

By Technology: Voice over IMS Gains Momentum

Circuit-Switched Fallback held 59.2% of 2025 revenues, but Voice over IMS is forecast to expand at a 44.3% CAGR, underscoring operators’ move toward IP-native voice that trims parallel network costs. The VoLTE market size for Voice over IMS platforms is set to triple by 2031 as IMS cores become cloud-native and deploy over off-the-shelf hardware.

Single-Radio Voice Call Continuity ensures seamless hand-offs between LTE and legacy 2G coverage, maintaining quality during transition. As confidence in all-IP voice rises, dual-radio architectures decline, freeing handset battery life and simplifying RF design. Long-term, IMS adoption unlocks RCS and video-over-LTE services that raise ARPU.

By Call Type: RCS Transforms Communication Experience

HD Voice supplied 57.60% of 2025 call revenue, delivering full-band audio as the new baseline. RCS traffic, however, is projected to grow at 47% CAGR as operators bundle file sharing, location pins, and group chat into the native dialer. The VoLTE market size for RCS features benefits from enterprise interest in verified sender IDs and rich messaging campaigns.

Video over LTE adoption advances on ubiquitous front-camera smartphones and expanding network capacity. Enhanced call types position carriers as credible alternatives to OTT apps by merging voice, messaging, and content in a single trusted channel.

By Operator Type: Private Networks Emerge as Growth Driver

Mobile Network Operators controlled 71.55% revenue in 2025, but Private/Enterprise LTE installations grow at a 43.8% CAGR as factories, airports, and mines deploy stand-alone networks. The VoLTE market share captured by private operators accelerates in the United States, where CBRS spectrum facilitates dedicated networks without nationwide carrier dependence.

Managed-service alliances—such as AT&T and Microsoft’s Azure private 5G offering—simplify turn-key VoLTE for enterprises. MVNOs depend on host carriers’ IMS implementations, so their competitive edge lies in value-added applications rather than network control.

Geography Analysis

North America commanded 39.45% of 2025 revenue on the back of complete LTE footprints, early smartphone saturation, and FCC-driven 3G sunsets. Operators, including Verizon and AT&T, finalized nationwide VoLTE rollouts and now target latency optimization to support low-latency voice applications. Canadian carriers leverage shared rural infrastructure programs to extend VoLTE coverage into sparsely populated regions, while Mexico’s reform-driven spectrum auctions speed up LTE deployment.

Asia-Pacific is forecast to grow at 45.8% CAGR, buoyed by China’s 500 million-subscriber VoLTE network and India’s Digital India program that subsidizes 4G handsets. Regional giants like Reliance Jio lead with zero-charge VoLTE calling plans, illustrating how inexpensive voice can accelerate adoption. Japan and South Korea exploit dense urban fiber backhaul to layer RCS and ultra-low-latency video over standard VoLTE, attracting premium subscribers.

Europe’s coordinated 3G sunset roadmap supports cross-border roaming efforts that bolster traveler confidence in VoLTE continuity. Middle East governments invest in smart-city blueprints, using VoLTE to back up IoT telemetry and emergency services in high-rise clusters. Africa and Latin America trail in revenue terms yet present untapped opportunities as universal service funds finance LTE rollouts and handset affordability programs.

Competitive Landscape

The VoLTE market features moderate concentration. Three global vendors - Ericsson, Nokia, and Samsung - dominate IMS core supply, while top operators hold strong regional clout. North American carriers capitalize on premium network positioning and patented VoLTE optimizations to counter OTT migration. In Europe, infrastructure-sharing mandates reduce duplication but intensify retail competition, spurring innovative RCS-based customer-experience offerings.

Equipment vendors pivot to cloud-native, software-as-a-service IMS models that slash deployment times for emerging operators and private-network owners. Patent portfolios around SR-VCC and codec optimization enable royalty streams, reinforcing barriers to entry. Disruptive entrants deliver lightweight IMS cores running on Kubernetes, allowing small carriers to launch VoLTE without heavyweight hardware. Strategic moves include Verizon’s USD 2.1 billion VoLTE quality upgrade plan, Nokia’s USD 1.8 billion Airtel IMS contract, and AT&T-Microsoft’s managed private-LTE alliance.

VoLTE Industry Leaders

AT&T Inc.

Verizon Wireless

Vodafone Group PLC

Bharati Airtel Limited

Bell Canada

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Verizon announced a USD 2.1 billion network upgrade targeting VoLTE quality and 5G voice integration.

- January 2025: Reliance Jio received a GSMA award for highest global VoLTE call success rate.

- December 2024: China Mobile completed nationwide Voice over IMS, serving over 500 million VoLTE users.

- November 2024: AT&T partnered with Microsoft to embed VoLTE in Azure private 5G networks

Global VoLTE Market Report Scope

Voice over Long-Term Evolution ( VoLTE) is a digital packet voice service that uses IMS technology for high-speed wireless communication for mobile phones, data terminals, IoT devices, and it is delivered over IP via an LTE access network. The market scope for this study consists of different end-user industries and their adoption trends of VoLTE technology. The market study also focuses on the impact of COVID-19 on the market ecosystem.

The Global Voice Over LTE (VoLTE) Market is Segmented, by End-user Industry (Corporate, Commercial, Government), and Geography.

| Corporate |

| Commercial |

| Government |

| Smartphones |

| Feature Phones |

| IoT Modules and Wearables |

| Voice over IMS (VoIMS) |

| Circuit-Switched Fallback (CSFB) |

| Single-Radio Voice Call Continuity (SRVCC) |

| Voice over LTE via GAN (VOLGA) |

| Dual-Radio / Simultaneous Voice and LTE (SVLTE) |

| HD Voice |

| Video over LTE |

| Rich Communication Services (RCS) |

| Mobile Network Operators (MNO) |

| Mobile Virtual Network Operators (MVNO) |

| Private / Enterprise LTE Networks |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By End-user Industry | Corporate | ||

| Commercial | |||

| Government | |||

| By Device Category | Smartphones | ||

| Feature Phones | |||

| IoT Modules and Wearables | |||

| By Technology | Voice over IMS (VoIMS) | ||

| Circuit-Switched Fallback (CSFB) | |||

| Single-Radio Voice Call Continuity (SRVCC) | |||

| Voice over LTE via GAN (VOLGA) | |||

| Dual-Radio / Simultaneous Voice and LTE (SVLTE) | |||

| By Call Type | HD Voice | ||

| Video over LTE | |||

| Rich Communication Services (RCS) | |||

| By Operator Type | Mobile Network Operators (MNO) | ||

| Mobile Virtual Network Operators (MVNO) | |||

| Private / Enterprise LTE Networks | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the VoLTE market in 2026?

The VoLTE market size is USD 86.84 billion in 2026.

What CAGR is forecast for VoLTE revenue through 2031?

Global revenue is projected to rise at a 42.65% CAGR from 2026-2031.

Which region is growing fastest for VoLTE adoption?

Asia-Pacific leads with a forecast 45.8% CAGR through 2031.

Which end-user segment shows the highest growth?

Government and public-safety users expand at a 43.9% CAGR as agencies adopt mission-critical broadband voice.

Why do 5G networks still depend on VoLTE?

Non-Standalone 5G leverages LTE anchors for voice, so VoLTE provides essential fallback until full Voice over 5G standards mature.

What technology segment grows quickest within VoLTE?

Voice over IMS platforms lead at a 44.3% CAGR as operators transition to native IP voice.

Page last updated on: