Virtual Ward Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

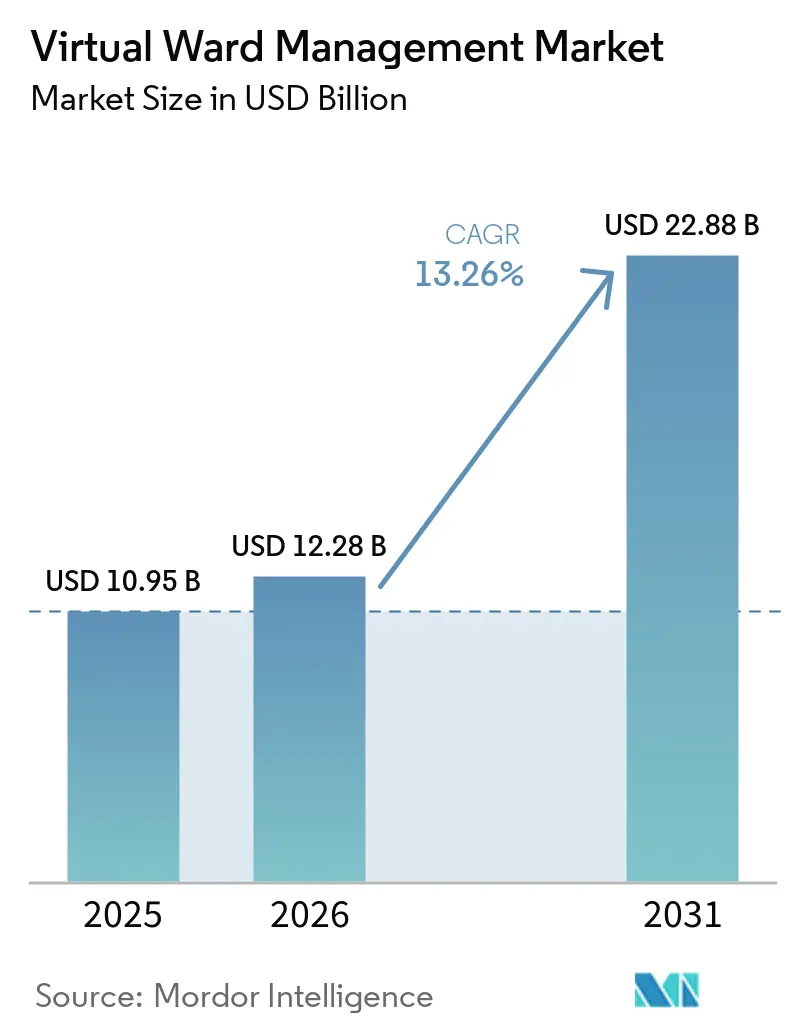

| Market Size (2026) | USD 12.28 Billion |

| Market Size (2031) | USD 22.88 Billion |

| Growth Rate (2026 - 2031) | 13.26% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Virtual Ward Management Market Analysis by Mordor Intelligence

The Virtual Ward Management Market size is projected to expand from USD 10.95 billion in 2025 and USD 12.28 billion in 2026 to USD 22.88 billion by 2031, registering a CAGR of 13.26% between 2026 to 2031.

The virtual ward management market is expanding because hospital systems are using it as a practical substitute for physical bed capacity rather than as a stand-alone digital health upgrade. Occupancy strain, delayed discharges, and workforce shortages are pushing providers to move clinically stable patients into monitored home-based pathways that cost less than inpatient care and can be deployed faster than building new ward space. Reimbursement support is also becoming more durable, especially in the United States and the United Kingdom, which gives health systems more confidence to invest in command centers, care pathways, and monitoring workflows at scale. The next phase of the virtual ward management market is also being shaped by a clearer separation between clinical workflow software and home-device logistics, which is raising the value of integrated service models and partnerships that can manage both care coordination and last-mile kit fulfillment. Evidence from wearable-based deterioration detection is also widening the software and analytics opportunity, even as cybersecurity, compliance, and data governance costs continue to slow adoption in markets where reimbursement is still less stable.

Key Report Takeaways

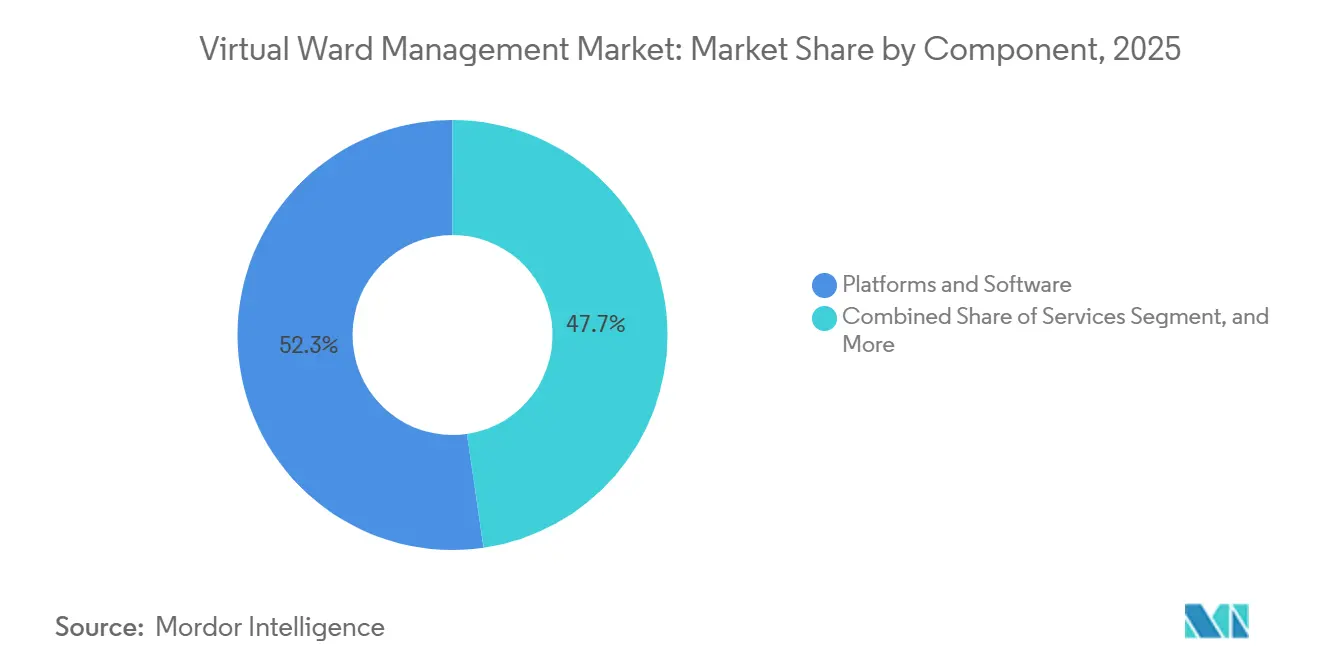

- By component, platforms and software led with a 52.32% share in 2025, while services are projected to expand at a 14.27% CAGR through 2031.

- By technology, telehealth and virtual consultation held 35.73% in 2025 and is also the fastest-growing segment with a 13.76% CAGR through 2031.

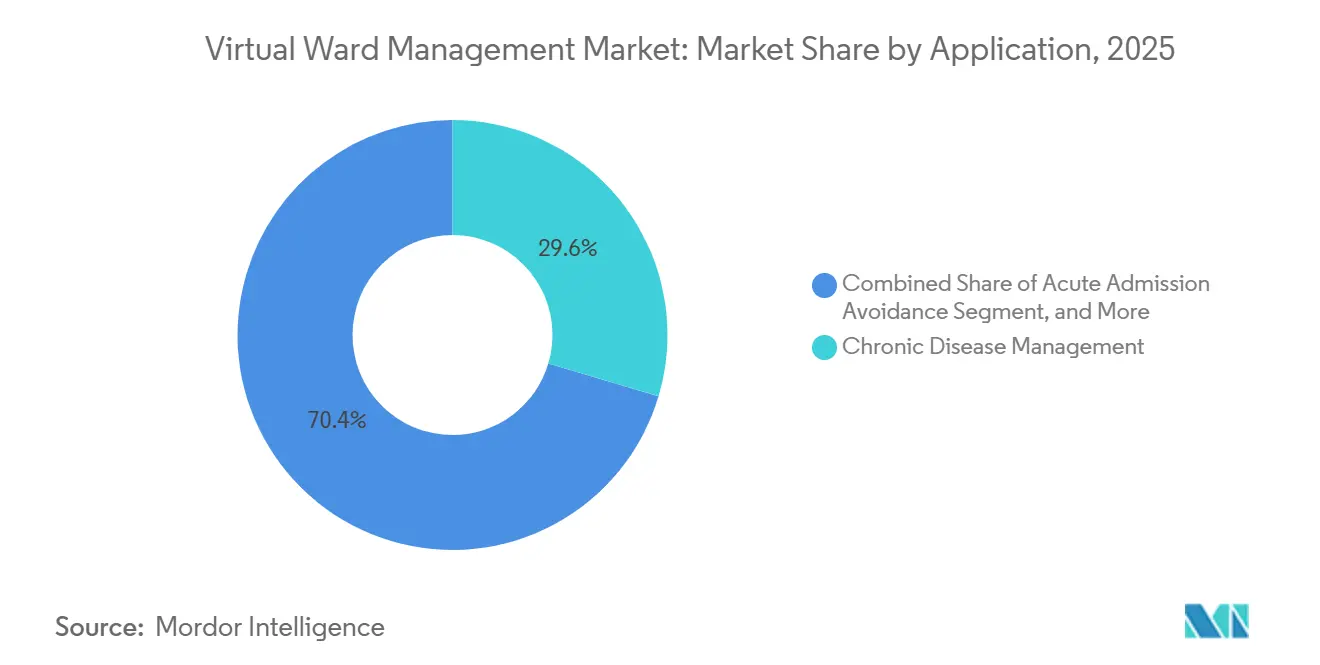

- By application, chronic disease management accounted for 29.57% in 2025, while post-acute and early supported discharge is forecast to grow at a 15.36% CAGR through 2031.

- By end user, hospitals and health systems held 43.08% in 2025, while community and home healthcare providers recorded the highest projected CAGR at 17.38% through 2031.

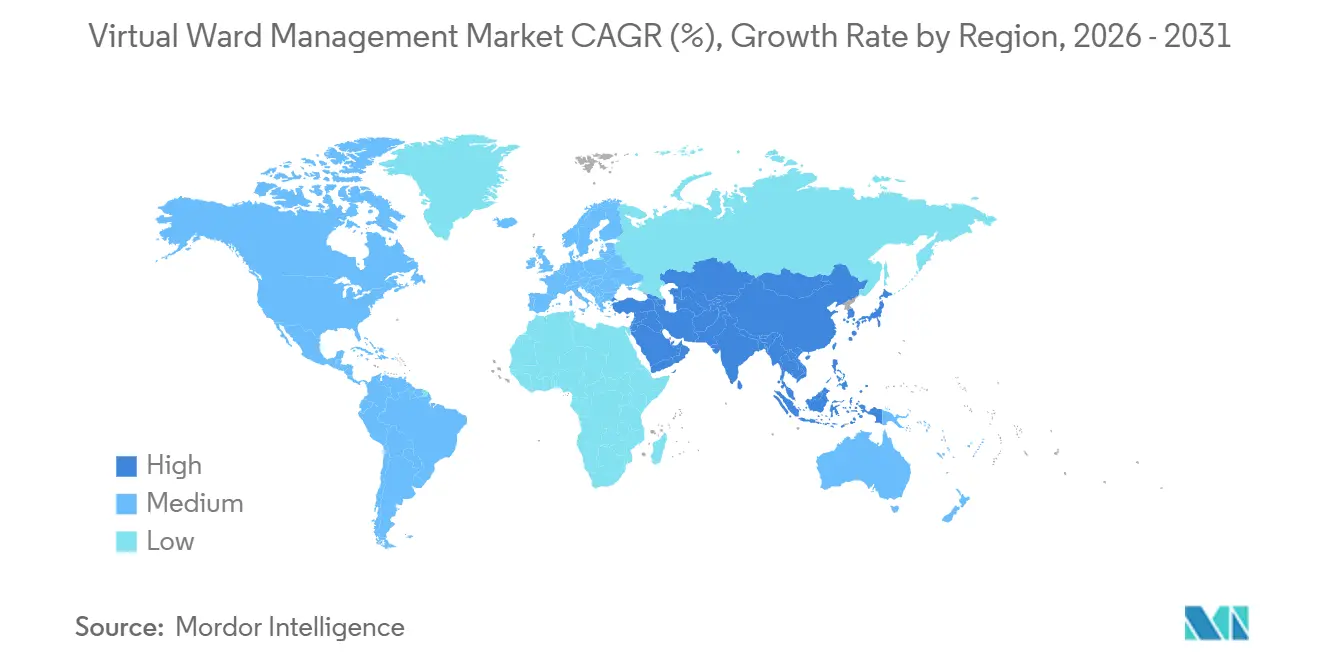

- By geography, North America led with 39.64% in 2025, while Asia-Pacific is expected to advance at a 15.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Virtual Ward Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hospital Capacity and Staffing Pressure | +3.2% | Global, with highest intensity in UK, US, and Germany | Short term (≤ 2 years) |

| Aging and Multimorbidity Burden | +2.8% | Global, acute in Japan, Germany, Italy, and South Korea | Long term (≥ 4 years) |

| Reimbursement Normalization for Hospital-At-Home | +2.5% | North America and Europe | Medium term (2-4 years) |

| RPM and AI-Enabled Deterioration Detection | +2.1% | North America, UK, APAC core, with spill-over to MEA | Medium term (2-4 years) |

| Occupancy and Admission-Avoidance KPI Pressure | +1.5% | UK, Europe, with spill-over to APAC | Short term (≤ 2 years) |

| Home Diagnostics and Logistics Orchestration Demand | +1.2% | North America and UK, spill-over to EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hospital Capacity and Staffing Pressure

Hospital bed shortages and nursing gaps are moving the virtual ward management market from an optional innovation model into a procurement priority. Ochsner Health’s acute care at home program, launched in 2024, saved more than 1,000 bed-days in less than 1 year by diverting admissions and observation stays into home-based care supported by a virtual physician and an in-person care unit.[1]American Medical Association, “Lawmakers Extend CMS Hospital-at-Home Waiver for Five Years,” AMA News Wire, ama-assn.org NHS Greater Manchester’s Hospital@Home program reached 883 beds and served a population of 3.2 million, and it cared for more than 19,000 patients in the first 8 months of 2025 with an average episode length of 7.5 days. NHS England also faced an estimated 1.15 million delayed-discharge bed-days per month in 2024, which kept clinically ready patients in hospital because social care and home support were not in place fast enough. In that setting, the virtual ward management market gains ground because virtual capacity can be added in months, while physical bed expansion usually takes a multi-year capital cycle.

Aging and Multimorbidity Burden

The virtual ward management market is increasingly built around older patients with overlapping conditions rather than around short, one-time recovery episodes. A 2025 study in Frontiers in Public Health reported that China’s population aged 60 and above reached 297 million, or 21.1% of the total, by the end of 2023, and it is projected to reach 500 million by 2050.[2]Xiaohua Zhou, Lina Chen, Xu Lou, Ying Li, and Bobo Han, “Construction of Community Home-Based Older Adult Care Service Model Based on Modular Design Concept,” Frontiers in Public Health, frontiersin.org The same study found significantly higher demand for community home medical services among chronically ill individuals and disabled individuals, with regression coefficients of 0.3 and 0.5, respectively, which points to steady demand for continuous home monitoring and care coordination. In Singapore, a retrospective study published in JMIR Formative Research in May 2026 reviewed 4,857 calls handled by the National University Health System Virtual Care Centre and found a mean caller age of 70.5 years, while 63.7% of medical queries were resolved without physical escalation. This pattern supports a broader shift in the virtual ward management market toward frailty support, chronic care navigation, and home-based management of patients who need frequent observation but not continuous inpatient intervention.

Reimbursement Normalization for Hospital-At-Home

The virtual ward management market is benefiting from the move from temporary waivers to longer reimbursement visibility in several leading health systems. The US Consolidated Appropriations Act, 2026 extended the CMS Acute Hospital Care at Home waiver through September 2030, and the American Medical Association reported that the program now spans 366 approved programs across 139 health systems in 37 states. Scotland announced GBP 85 million, or USD 107 million, in July 2025 to expand Hospital at Home capacity to 2,000 beds by December 2026, which shows that public funding is moving beyond pilots into service buildout. Germany’s Hospital Transformation Fund under the KHVVG makes telemedical network structures eligible for investment from 2026 to 2035, which gives hospitals a clearer path to fund virtual care infrastructure.[3]Peter Bauske, “Krankenhaus Bethanien Solingen Vernetzt Sich,” RZV, rzv.de As reimbursement becomes more durable, providers are more willing to commit to command centers, clinical staffing, and long-term workflow redesign, although this same shift also raises the compliance burden because payment is increasingly tied to measurable outcomes and stronger governance.

The virtual ward management market is also being shaped by a move from passive monitoring to predictive clinical support. A March 2026 Nature Medicine study showed that a transformer-based model applied to Apple Watch data detected heart failure worsening with an AUROC of 0.8, compared with 0.5 for existing cardio fitness algorithms, and it identified risk with a median lead time of 7.4 days before unplanned healthcare use. The same study found that every 10% decline in wearable-derived peak exercise capacity was associated with a hazard ratio of 3.6 for unplanned healthcare utilization, which matters because early recognition is what makes high-acuity home pathways clinically workable. Biofourmis reported in November 2024 that its platform analyzes more than 120 real-time biomarkers and supported a 50% reduction in 30-day readmissions at Lee Health after deployment of remote patient monitoring and home-based hospital care. Even so, the virtual ward management market still faces a practical limit because some high-density heart failure monitoring protocols generate more than 5 GB of data per patient per week, and many community settings are not yet equipped to process that volume efficiently.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement Inconsistency Outside Lead Markets | -1.8% | Middle East, Africa, South America, Southeast Asia | Medium term (2-4 years) |

| Cybersecurity and Clinical Governance Burden | -1.2% | Global | Short term (≤ 2 years) |

| Home Suitability and Caregiver Readiness Gaps | -0.8% | Global, most acute in APAC rural areas and MEA | Long term (≥ 4 years) |

| Device Logistics and EPR Interoperability Friction | -0.6% | Global, most acute in fragmented provider markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Inconsistency Outside Lead Markets

Outside the United States, the United Kingdom, and a limited group of European markets, the virtual ward management market still faces uneven reimbursement pathways. Japan’s FY2024 telemedicine research report from the Ministry of Health, Labour and Welfare found that 84% of institutions offering D-to-D remote pathology diagnosis received no government subsidy for operating costs, and remuneration-sharing terms were undefined in most contracts. France placed telesurveillance reimbursement into common law for chronic conditions in 2023, but acute virtual care pathways still have narrower formal payment coverage, which slows scale outside the main urban corridors. South Korea only moved to full legal telemedicine permission in February 2024 after a healthcare labor disruption, which shows that regulatory opening there has been reactive rather than built around a fully planned payment architecture. This leaves vendors in the virtual ward management market with a costly country-by-country expansion model that weakens the scale efficiency that home-based care should otherwise offer.

Cybersecurity and Clinical Governance Burden

Cybersecurity and clinical governance remain practical barriers for the virtual ward management market because remote care depends on continuous data exchange across homes, devices, and provider systems. NHS England’s Data Security and Protection Toolkit Version 8.0 took effect in July 2025 and incorporated Cyber Assessment Framework requirements from the UK National Cyber Security Centre for health system technology providers. That change has made end-to-end encryption, access controls, and recurring security audits standard procurement requirements for NHS-facing suppliers, and the draft notes that this can add 8% to 15% to compliance operating costs for smaller providers. In France, cloud infrastructure for hospital data also requires HDS certification together with RGPD compliance, which creates a dual regulatory burden for non-EU entrants. The virtual ward management market is therefore seeing buyers ask for stronger independent outcome validation and clearer accountability for AI-supported deterioration alerts before approving wider deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Drive the Installed Base, Services Define the Growth Curve

Platforms and software represented 52.32% of the virtual ward management market size in 2025, which made this the largest component category. In the virtual ward management industry, providers are favoring software-led deployments because these systems fit more easily into existing electronic patient record environments than stand-alone device stacks. Clinical command center tools, care coordination dashboards, and virtual ward applications sit at the center of current procurement because they determine how patients are identified, escalated, and documented. Vendor selection is therefore tied closely to interoperability with hospital EPR systems, especially Epic and Cerner environments, because fragmented workflows reduce clinical efficiency. Devices and peripherals remain necessary for acute monitoring, but they are facing more pressure as validated consumer wearables begin to cover use cases that once depended on proprietary medical sensors.

Services are the fastest-growing component in the virtual ward management market, with a projected CAGR of 14.27% from 2026 to 2031. That pattern reflects a structural outsourcing trend because many health systems can fund technology but still do not have enough staff to run a 24/7 virtual command center on their own. Health Recovery Solutions expanded this bundled approach in March 2026 through its acquisition of Rimidi, which added cardiometabolic chronic care capabilities and direct integration of CGM data from Dexcom, FreeStyle Libre, and Eversense into EHR workflows. Current Health’s March 2026 logistics partnership with Cardinal Health’s Velocare solution also highlighted how device delivery, setup, retrieval, and supply management are becoming a separate but essential service layer in the virtual ward management market. The component mix is therefore shifting from one-time technology purchase decisions toward recurring service relationships that combine monitoring, workflow management, and home logistics into a single operational package.

By Technology: Telehealth Anchors the Market While AI Analytics Reshapes Clinical Protocols

Telehealth and virtual consultation held 35.73% of the technology segment in 2025 and is also projected to expand at a 13.76% CAGR through 2031. This is the only segmentation type in which the largest segment and the fastest-growing segment are the same, which shows that telehealth in the virtual ward management market is still scaling rather than flattening. The segment benefits from both clinician familiarity and broadening reimbursement, which makes it easier to insert remote consultation into acute and post-acute pathways than it is to redesign the care model around a new device category. Teladoc Health launched its enhanced 24/7 Care service in January 2026 through the Prism platform, and the company said the service supports real-time provider-to-provider specialist consultation and resolves more than 95% of member concerns in a single session across its integrated care base. That matters for the virtual ward management market because acute virtual pathways depend on fast access to clinical judgment, not just on passive data transmission.

Remote patient monitoring and AI analytics are the technology layers where differentiation is now moving fastest in the virtual ward management industry. Predictive deterioration alerts, automated documentation, and risk stratification tools are shifting from pilots into day-to-day deployment because they can reduce escalation delays and clinical documentation burden. Huma expanded this direction in 2025 through the acquisition of Aluna, which added FDA-cleared respiratory monitoring tools for asthma and COPD management across more than 150 US health systems and 500,000 contracted lives. Interoperability remains the clearest unmet need because most virtual ward deployments still pull data from multiple devices and platforms, and weak connector coverage between monitoring tools and hospital records raises deployment cost and slows clinical adoption.

By Application: Chronic Care Dominates Volume, Post-Acute Pathways Deliver the Fastest Expansion

Chronic disease management accounted for 29.57% of the application mix in 2025, making it the largest use case in the virtual ward management market. This lead comes from the high monitoring frequency and high readmission risk attached to patients with heart failure, COPD, diabetes, hypertension, and other long-duration conditions. The economics are also more durable in chronic care because preventing even a small number of admissions can justify a full-year subscription model for monitoring and navigation. Health Recovery Solutions reinforced this direction in March 2026 when it acquired Rimidi and brought cardiometabolic management and CGM integration deeper into the EHR workflow. That move shows that application demand in the virtual ward management market is not centered only on early discharge, but also on multi-month disease management that sits between outpatient review and hospital admission.

Post-acute and early supported discharge is the fastest-growing application, with the virtual ward management market size for this segment projected to expand at a 15.36% CAGR from 2026 to 2031. This segment is growing because it directly addresses bed turnover pressure and helps health systems move stable patients out of acute wards sooner without ending structured clinical oversight. Current Health’s launch of virtual ICANS assessments in December 2025 also showed how post-discharge monitoring is expanding into more complex specialty pathways, including remote neurotoxicity assessment for CAR-T and bispecific therapy patients through a 24/7 clinical command center. Acute admission avoidance and frailty care are also gaining relevance where public systems track occupancy and delayed discharge as operating priorities, especially in NHS-style settings. The application mix in the virtual ward management market is therefore broadening from general medical step-down into specialty, elderly, and chronic pathways that need close observation without constant physical bed use.

By End User: Hospitals Lead Procurement Today, Community Providers Will Shape the Next Phase

Hospitals and health systems held 43.08% of the virtual ward management market share in 2025, which kept them as the largest end-user group. Their leadership reflects procurement scale, access to capital budgets, and authority over the clinical pathways that determine who can be treated at home and under what escalation rules. Integrated delivery networks and provider groups follow because they can use virtual infrastructure across multiple sites and can align home-based monitoring with population health goals. Government programs and payers remain a smaller direct buyer base today, but in waiver-based models they increasingly shape the commercial structure through payment rules and pathway eligibility. In practical terms, hospitals still anchor most deployments in the virtual ward management market because they own the command center model and the acute care protocols that community partners later use.

Community and home healthcare providers are the fastest-growing end-user segment, with a projected CAGR of 17.38% from 2026 to 2031. This trajectory suggests that the virtual ward management market will gradually move away from being hospital-centered in daily operations, even if hospitals remain the main authorizing institutions. Inbound Health reported in September 2025 that structured workflow-based patient identification improved admissions by 76%, which shows how community-based operators can raise utilization once pathways are standardized. As more chronic and post-acute monitoring shifts into community settings, vendors that rely only on hospital procurement may face lower pricing power unless they can show stronger outcomes, better workflow integration, or a more complete service model.

Geography Analysis

North America accounted for 39.64% of the virtual ward management market size in 2025, which kept it as the largest regional segment. The region benefits from the longest runway of formal payment support because the CMS Acute Hospital Care at Home waiver now runs through 2030. The American Medical Association reported that 366 approved hospital-at-home programs are now spread across 139 health systems in 37 states, which shows that the market has moved beyond limited pilot concentration. The pace of deployment by major providers, including Cleveland Clinic, Tampa General Hospital, and Penn Medicine, reflects an operating scale that is being built on reimbursement continuity rather than on one-off innovation funding. Canada adds supportive provincial momentum, while Mexico remains at an earlier adoption stage with more limited systemwide rollout.

Europe remains the second-largest region in the virtual ward management market, led by the United Kingdom, Germany, and France. Germany’s Virtual Hospital NRW became nationally available from January 2025, and its broader hospital transformation framework recognizes telemedical network structures as eligible infrastructure, which gives operators a direct policy route for investment. The United Kingdom continues to push service scale through formal virtual ward capacity targets, and Scotland’s July 2025 funding package for 2,000 beds by end-2026 reinforced that national commitment. France is widening procurement pathways through its hospital investment plan and through public purchasing channels, such as the RESAH selection of Rofim’s telemedicine platform for the Innovative Digital Solutions market.

Asia-Pacific is projected to grow at a 15.92% CAGR from 2026 to 2031, making it the fastest-growing regional segment in the virtual ward management market. The region is expanding because aging populations, urban hospital crowding, and improving digital infrastructure are pushing governments and providers to build home-based alternatives to inpatient care. China’s Guangdong Second Provincial General Hospital described a 5G Smart Home Ward model that combines IoT, AI, cloud computing, and clinical-grade wearables into a home-based equivalent of inpatient monitoring with secure transmission into the hospital record. South Korea is also extending remote monitoring into home hospitalization models, including the April 2026 pilot partnership between Sciths and Yonsei Song Clinic for community-based service delivery. The Middle East and Africa and South America remain earlier-stage markets, but government-backed digital health infrastructure in GCC countries and longer-term public procurement opportunities in Brazil keep them relevant for later expansion.

Competitive Landscape

The virtual ward management market remains moderately fragmented at the platform layer, while parts of the device and infrastructure stack are becoming more concentrated through scale partnerships and enterprise procurement. Specialist vendors such as Doccla, Huma, Health Recovery Solutions, Biofourmis, and Current Health compete on pathway depth, monitoring design, workflow integration, and managed service capability, while larger medtech groups use existing hospital relationships and installed clinical ecosystems to strengthen their position. Philips illustrated that enterprise approach in May 2026 when a consortium including Philips, Cuviva, and Vingmed was selected by Karolinska University Hospital for Region Stockholm’s first region-wide hospital-at-home program, covering up to 15,000 patients annually under an agreement that can run for up to 8 years. Huma’s May 2025 acquisition of Aluna, together with its stated M&A partnership with Eckuity Capital, showed how vendors are trying to broaden their coverage across respiratory, chronic, and remote care pathways rather than remaining focused on a narrow monitoring niche. Current Health’s logistics partnership with Cardinal Health in March 2026 also made clear that competitive strength in the virtual ward management market now depends on more than software alone because device deployment, retrieval, and supply chain execution have become part of the purchasing decision.

Competition is increasingly centered on who can offer the most complete operational stack with the fewest workflow breaks. The separation between clinical workflow software and device logistics is becoming more visible, and buyers are favoring vendors or partnerships that can reduce the burden of coordinating multiple suppliers across equipment, monitoring, escalation, and transport. Teladoc’s January 2026 expansion of its enhanced 24/7 Care service showed that telehealth players are also moving closer to acute and longitudinal care orchestration by adding specialist consultation, pharmacy benefit checks, and integrated preventive gap identification. That overlap is pulling telehealth platforms, RPM vendors, and medtech companies into adjacent parts of the same commercial space within the virtual ward management market.

There is still room for interoperability orchestration, rural deployment models, and oncology-focused pathways beyond the first wave of specialty monitoring. AI-enabled deterioration detection also remains a live battleground because validated wearables and predictive models could weaken the pricing power that proprietary sensor stacks once enjoyed. Current Health’s December 2025 launch of virtual ICANS assessments showed that specialty pathways can create new competitive space where clinical complexity is high, and home monitoring requirements are more demanding. At the same time, interoperability gaps still slow execution because most deployments rely on several data streams and are only as strong as the weakest system connection. No single vendor in the virtual ward management market currently controls the entire stack across reimbursement alignment, command center operations, monitoring hardware, analytics, logistics, and specialty pathway design. That keeps competitive pressure high and makes proof of operational performance, procurement fit, and clinical workflow integration more important than simple device breadth or software feature count.

Virtual Ward Management Industry Leaders

Agyle Health

Dignio

Health Recovery Solutions

Philips

Teladoc Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Philips, in consortium with Cuviva and Vingmed, was selected by Karolinska University Hospital for Region Stockholm's first region-wide hospital-at-home program, covering up to 15,000 patients annually across a population of over 2 million. The agreement runs up to 8 years and delivers continuous ECG, blood pressure, and oxygen saturation monitoring with near-real-time clinician access.

- March 2026: Health Recovery Solutions (HRS) acquired Rimidi, a chronic disease management company specializing in diabetes and cardiometabolic care. The acquisition integrates continuous glucose monitoring (CGM) capabilities, including Dexcom, FreeStyle Libre, and Eversense, directly into EHR workflows, extending HRS's addressable market from post-acute RPM to longitudinal chronic care management.

- March 2026: Current Health announced a logistics integration partnership with Cardinal Health's Velocare solution to scale hospital-at-home programs, streamlining last-mile fulfillment, installation, and retrieval of in-home clinical monitoring kits to reduce care team burden and lower program operating costs.

- January 2026: Teladoc Health launched enhanced 24/7 Care powered by its Prism platform, enabling real-time provider-to-provider specialist consults, real-time pharmacy benefit checks, and HIE-integrated preventive care gap identification for over 100 million Americans.

Global Virtual Ward Management Market Report Scope

The Virtual Ward Management Market encompasses the hardware, software, and services that enable healthcare providers to deliver hospital-level care to patients in their own homes. It acts as a clinical alternative to traditional inpatient wards, preventing hospital admissions or facilitating early discharge.

The Virtual Ward Management Market is Segmented by Component (Platforms and Software, Services, Devices and Peripherals), Technology (RPM, Telehealth, AI and Analytics, Interoperability), Application (Chronic Disease, Post-Acute, Acute Avoidance, Frailty, Surgical, Oncology), End User (Hospitals, IDNs, Community Providers, Payers), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in Value (USD)

| Platforms and Software |

| Services |

| Devices and Peripherals |

| Remote Patient Monitoring |

| Telehealth and Virtual Consultation |

| AI and Analytics |

| Interoperability and Workflow Orchestration |

| Chronic Disease Management |

| Post-Acute and Early Supported Discharge |

| Acute Admission Avoidance |

| Frailty and Elderly Care |

| Surgical Pathway Monitoring |

| Oncology and Specialty Pathways |

| Hospitals and Health Systems |

| Integrated Delivery Networks and Provider Groups |

| Community and Home Healthcare Providers |

| Payers and Government Programs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Platforms and Software | |

| Services | ||

| Devices and Peripherals | ||

| By Technology | Remote Patient Monitoring | |

| Telehealth and Virtual Consultation | ||

| AI and Analytics | ||

| Interoperability and Workflow Orchestration | ||

| By Application | Chronic Disease Management | |

| Post-Acute and Early Supported Discharge | ||

| Acute Admission Avoidance | ||

| Frailty and Elderly Care | ||

| Surgical Pathway Monitoring | ||

| Oncology and Specialty Pathways | ||

| By End User | Hospitals and Health Systems | |

| Integrated Delivery Networks and Provider Groups | ||

| Community and Home Healthcare Providers | ||

| Payers and Government Programs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving demand for virtual ward management solutions globally?

The main demand drivers are hospital bed pressure, nursing shortages, aging patient populations, and stronger reimbursement support in markets such as the United States and the United Kingdom.

How large is the virtual ward management market by 2031?

The virtual ward management market is forecast to reach USD 22.88 billion by 2031, up from USD 10.95 billion in 2025, with a 13.26% CAGR from 2026 to 2031.

Which component category leads spending in this space?

Platforms and software lead the market with a 52.32% share in 2025 because health systems prioritize workflow, command center, and EPR-connected software over stand-alone device deployment.

Which application area is expanding fastest?

Post-acute and early supported discharge is the fastest-growing application, with a projected CAGR of 15.36% through 2031, because providers need to reduce delayed discharge and free bed capacity faster.

Which end users are likely to shape the next phase of growth?

Hospitals and health systems remain the largest buyers today, but community and home healthcare providers are projected to grow fastest at 17.38% CAGR as care-at-home models mature.

Page last updated on: