Virtual Reality (VR) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

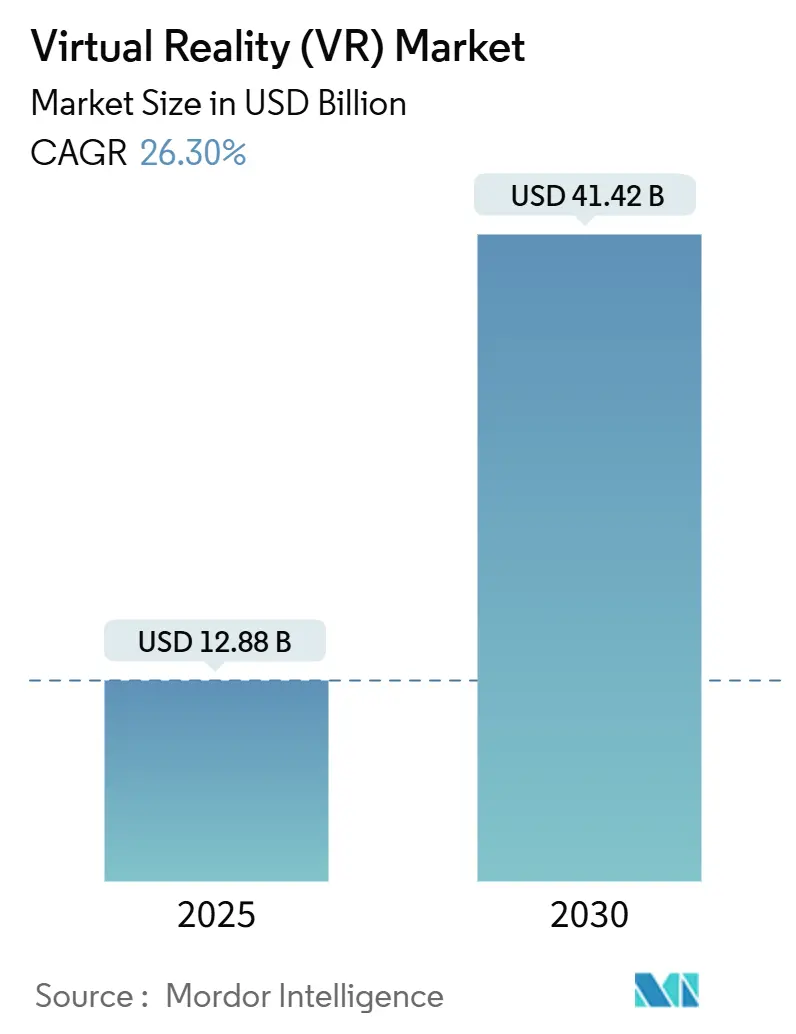

| Market Size (2025) | USD 12.88 Billion |

| Market Size (2030) | USD 41.42 Billion |

| Growth Rate (2025 - 2030) | 26.30% CAGR |

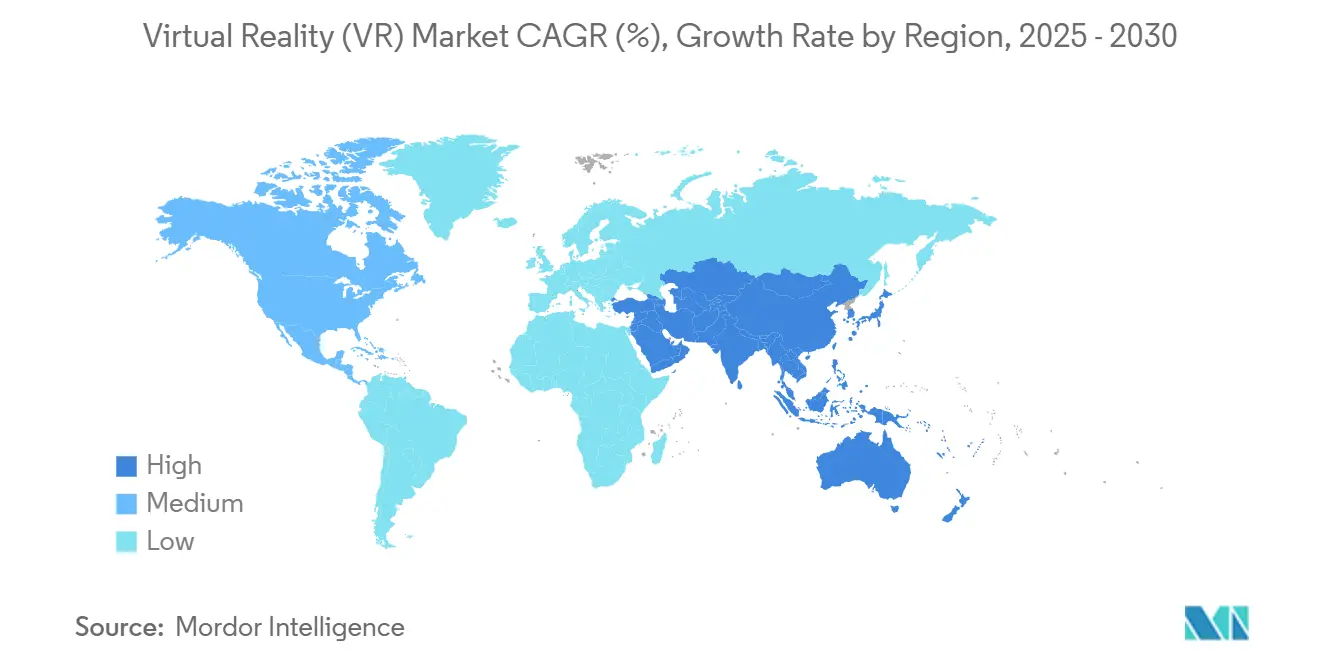

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Virtual Reality (VR) Market Analysis by Mordor Intelligence

The Virtual Reality market size is estimated at USD 12.88 billion in 2025 and is projected to reach USD 41.42 billion by 2030, advancing at a 26.30% CAGR. Rapid enterprise adoption of immersive training platforms, rising availability of mixed-reality–ready processors, and maturing 5G edge infrastructure underpin this expansion. Corporate net-zero pledges accelerate demand for virtual-first events, while regulatory clearances for therapeutic applications extend the technology’s reach beyond entertainment. Hardware innovation remains vital, yet software and services gain momentum as organizations prioritize tailored content, robust analytics, and seamless integration with learning-management systems.

Key Report Takeaways

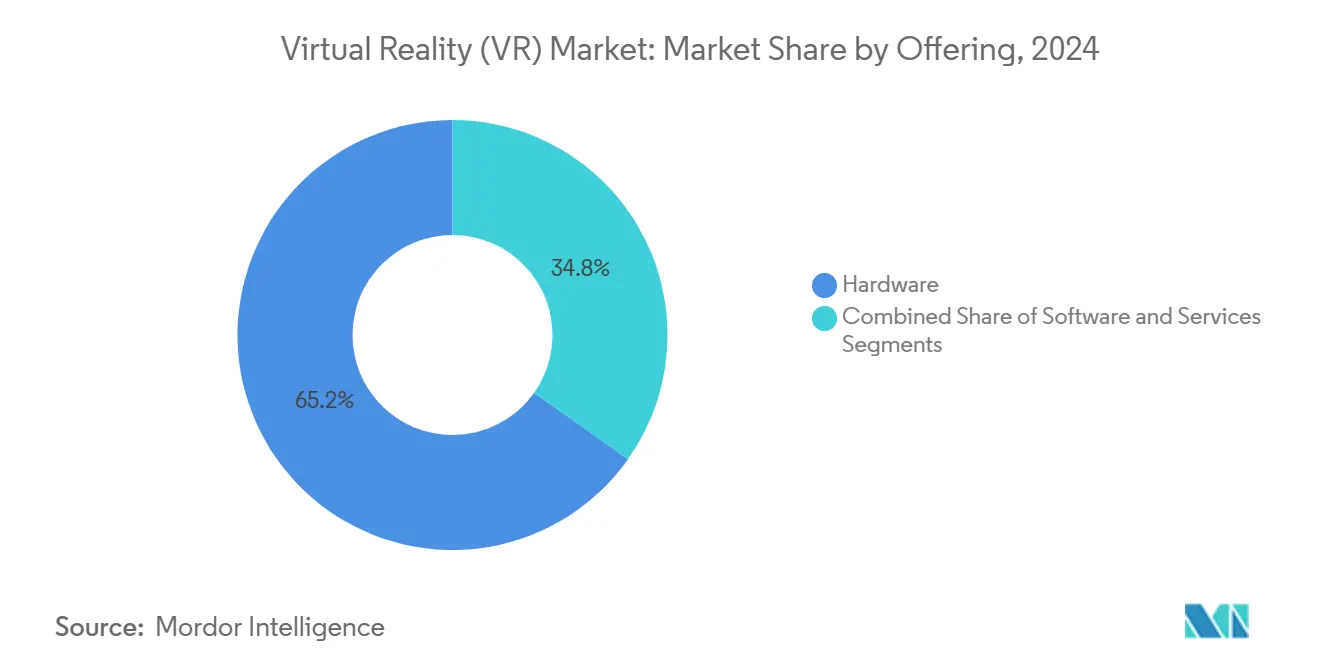

- By offering, hardware led with 65.2% revenue share in 2024; software is forecast to expand at a 27.7% CAGR through 2030.

- By device form factor, standalone head-mounted displays captured 45.3% of Virtual Reality market share in 2024, while standalone systems are projected to grow at 26.5% CAGR.

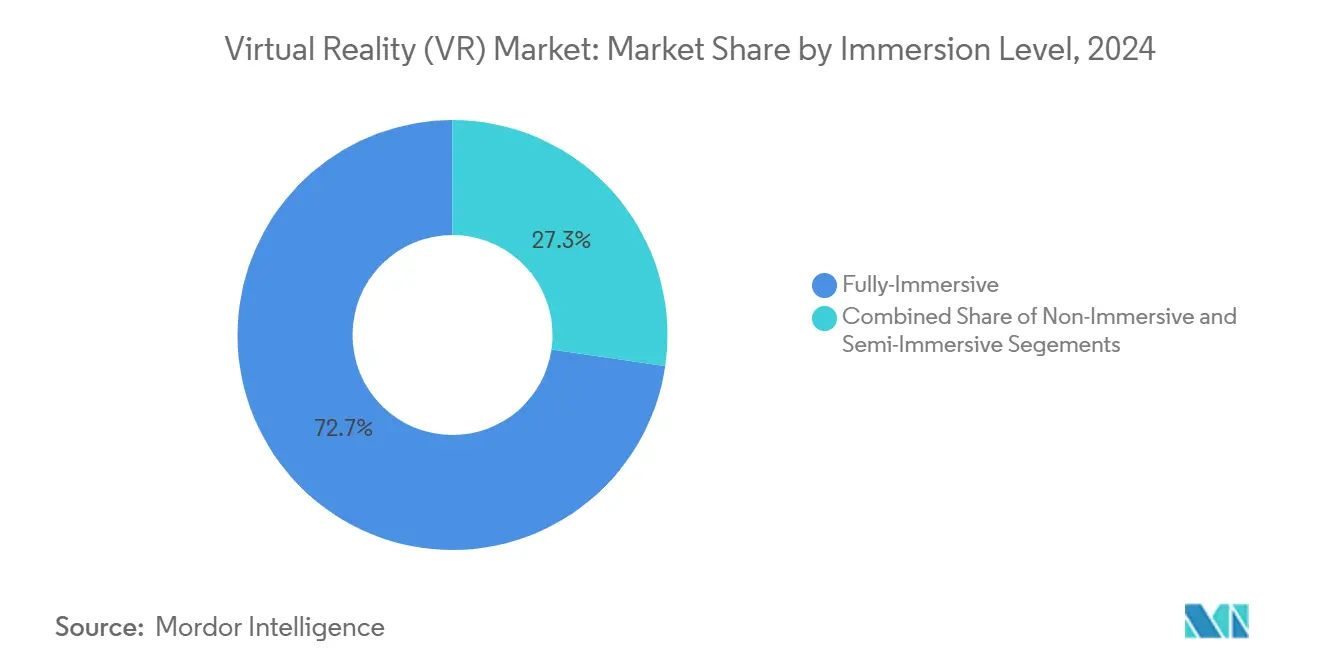

- By immersion level, fully immersive experiences held 72.7% share of the Virtual Reality market size in 2024, whereas non-immersive solutions are advancing at a 27.1% CAGR.

- By end-user industry, gaming accounted for 48.3% revenue share in 2024; healthcare is poised for the fastest 28.2% CAGR to 2030.

- By geography, North America commanded 35.9% revenue in 2024, but Asia-Pacific is set to grow the quickest at 26.4% CAGR.

Global Virtual Reality (VR) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising enterprise-wide VR training adoption | +8.2% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Mainstreaming of mixed reality-ready GPUs and SoCs | +6.1% | Global, concentrated in tech hubs | Short term (≤ 2 years) |

| 5G/Edge-powered untethered streaming of VR content | +4.7% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Corporate Net-Zero pledges driving virtual-first events | +3.8% | North America and EU primarily | Long term (≥ 4 years) |

| Regulatory approvals for VR-based mental-health therapies | +2.9% | North America, expanding to EU | Short term (≤ 2 years) |

| Ultrasound-haptics enabling controller-free interaction | +1.5% | Global, early adoption in enterprise | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Enterprise-Wide VR Training Adoption

Organizations roll out full-scale VR training programs after pilot success, citing a 75% reduction in training time and a 275% jump in learner confidence versus conventional methods. Boeing recorded a 75% cut in training hours, and Delta Air Lines raised technician proficiency checks by 5,000%. Break-even arrives at 375 learners and becomes 52% more cost-effective once cohorts exceed 3,000. Over 75% of Fortune 500 companies now embed VR in learning strategies, including Walmart’s retail simulations and the U.S. Army’s mental-health modules, while Japanese insurers such as SOMPO deploy VR hazard simulations to curb workplace incidents. The outcome is stronger knowledge retention and safer on-the-job performance, cementing training as the principal enterprise gateway into the Virtual Reality market.

Mainstreaming of Mixed-Reality-Ready GPUs and SoCs

Next-generation chipsets like Qualcomm’s Snapdragon XR2+ Gen 2 deliver 4.3 K-per-eye resolution and orchestrate a dozen cameras for spatial mapping, bringing flagship performance to mid-range headsets. [1]Qualcomm Technologies, Inc. "Qualcomm Accelerates New Wave of Mixed Reality Experiences with Snapdragon XR2+ Gen 2," qualcomm.com Apple’s Vision Pro employs dual chips to drive 23 million-pixel micro-OLED panels, illustrating processing demand curves. Display components alone add USD 530 to unit costs, so dynamic foveated rendering and eye-tracking become essential for efficiency. Samsung’s three-way alliance with Google and Qualcomm signals mainstream commercialisation of these silicon advances, progressively lowering price points and broadening access to the Virtual Reality market.

5G/Edge-Powered Untethered Streaming of VR Content

Cloud rendering over 5G SA networks removes the tether, delivering sub-20 ms motion-to-photon latency that curbs cybersickness. Verizon’s GPU-orchestrated edge platform supports advanced lighting and real-time ray tracing.[2]Verizon "Verizon develops new 5G edge technology that will revolutionize mobility for virtual reality (VR)," verizon.comAcademic studies show end-to-end delay drops 30% and communication lag halves when edge nodes host rendering workloads. Joint demonstrations by Ericsson, AT&T, NVIDIA, and Qualcomm confirm multi-user 8 K streams while saving 80% bandwidth relative to legacy methods. European universities already conduct architecture seminars with cardboard viewers backed by local edge servers, evidencing cost-effective scalability for the Virtual Reality market.

Corporate Net-Zero Pledges Driving Virtual-First Events

Corporate sustainability commitments accelerate virtual event adoption as organizations recognize that virtual events produce 40 times fewer emissions than in-person gatherings, directly supporting net-zero carbon targets.[3] Ivent Pro "Decoding the Environmental Impact of Virtual Events." ivent-hq.com Virtual conferences emit forty times fewer greenhouse gases than physical gatherings, aligning neatly with corporate sustainability targets. Platforms such as Touchcast quantify emissions savings, prompting companies to substitute travel-heavy town-halls with immersive digital venues.Beyond carbon reductions, firms report lower venue, travel, and catering expenses while reaching larger global audiences. This dual benefit positions virtual events as a durable growth vector within the broader Virtual Reality market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersickness and long-term vestibular concerns | -3.2% | Global, particularly affecting new users | Short term (≤ 2 years) |

| Eye-box heat build-up limiting continuous usage | -2.1% | Global, hardware-dependent | Medium term (2-4 years) |

| Scarcity of AAA-grade VR content outside gaming | -1.8% | Global, content development lag | Medium term (2-4 years) |

| Data-privacy compliance costs for eye-tracking analytics | -1.4% | EU and North America primarily | Long term (≥ 4 years) |

Source: Mordor Intelligence

Cybersickness and Long-Term Vestibular Concerns

Motion-to-photon discrepancies trigger nausea, headache, and disorientation, discouraging extended sessions. Sensory-conflict research pinpoints combined visual-vestibular mismatch as the main cause, intensified in mobile VR where device sway adds complexity. FDA guidelines for medical-grade headsets mandate prominent nausea warnings, highlighting clinical gravity. Hardware makers pursue higher refresh rates and latency cuts, yet physiological limits persist. Enterprises mitigate risk through shorter modules, raising content design costs and dampening near-term Virtual Reality market growth.

Eye-Box Heat Build-Up Limiting Continuous Usage

High-resolution panels and multi-core processors sit millimetres from the face, generating heat that erodes comfort. Premium devices such as Vision Pro adopt sophisticated heat-pipe systems, but sustained workloads still warm the eye-box. The compromise between resolution and thermals forces organisations to schedule cooling breaks, eroding productivity gains. Continued research into low-power micro-LED displays and active cooling remains critical for broader adoption in the Virtual Reality market.

Segment Analysis

By Offering: Hardware Infrastructure Drives Initial Deployment

Hardware dominated revenue at 65.2% in 2024 as companies invested in headsets, rendering PCs, and tracking peripherals required for rollouts. Complete enterprise kits range from USD 1,300 for entry setups to over USD 100,000 for high-end simulators, reflecting capital-intensive onboarding in the early Virtual Reality market. Meta’s Reality Labs booked USD 1.08 billion Q4 2024 revenue but maintained heavy R&D spend, illustrating the cost of pushing hardware boundaries.

Software, advancing at a 27.7% CAGR, now benefits from no-code and low-code platforms that let non-technical staff build simulations within days. Unity and Unreal streamline content pipelines, fuelling a service ecosystem of instructional designers and XR integrators. The result is rising attach rates between device shipments and content licences, gradually tilting revenue mix toward recurring software and services inside the Virtual Reality market.

Note: Segment shares of all individual segments available upon report purchase

By Device Form Factor: Standalone Systems Enable Workplace Mobility

Standalone headsets held 45.3% revenue in 2024 and retain the quickest 26.5% CAGR as cable-free operation matches agile workspace norms. Firms avoid dedicated VR labs by issuing all-in-one units that boot instantly and log into mobile device-management stacks. Tethered rigs persist for photoreal industrial design and pilot simulators that demand maximum GPU horsepower. The screenless-viewer niche survives in ultra-budget deployments, whereas CAVE environments remain specialised research installations for oil and gas or defence.

Meta’s Quest 3S launch confirmed demand for lighter standalone options, yet lacklustre holiday traction underlined a hard ceiling without fresh content. Apple reportedly builds a lower-priced Vision headset near the USD 1,500 bracket, signalling ongoing price elasticity challenges. Competitive dynamics suggest cost-effective standalone innovations will steer mainstream uptake within the Virtual Reality market.

By Immersion Level: Full Immersion Dominates Despite Non-Immersive Growth

Fully immersive experiences controlled 72.7% of 2024 revenue, reinforced by their ability to block distractions and simulate hazardous tasks safely. Automotive plants, for instance, run 1:1 scale paint-shop drills where chemical risks otherwise preclude live practice. Non-immersive solutions, though smaller today, expand fastest at 27.1% CAGR by overlaying digital twins onto physical environments without isolating users, making them ideal for collaborative design reviews.

Sony’s flip-up XR headset embodies this duality by permitting real-world visibility on demand. Research indicates skills acquisition improves most under deep immersion, while information-overlay tasks benefit from mixed or augmented approaches. Vendors therefore bundle multiple view modes in one device, widening appeal and sustaining engagement across training cycles of the Virtual Reality market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Healthcare Emerges as Enterprise Growth Driver

Gaming still generated 48.3% of 2024 spend, yet healthcare posted the highest 28.2% CAGR on the back of FDA-cleared therapies for pain and mental health, plus cadaver-free surgical rehearsal. Hospitals adopt VR triage drills to cut error rates, while insurers reimburse exposure therapy sessions delivered in clinics. Education and training providers embed VR modules to boost learner attention fourfold compared with standard e-learning, mirroring corporate patterns.

Retailers roll out virtual stores to showcase assortments without expensive square footage. Real-estate developers preview unbuilt apartments, closing sales earlier in project cycles. Military agencies digitise live-fire exercises into simulation pods, reducing ammunition spend and environmental impact. These diverse use cases reinforce healthcare’s strategic importance while retaining gaming as a reliable baseline in the Virtual Reality market.

Geography Analysis

North America held 35.9% of 2024 revenue due to mature healthcare systems, early 5G coverage, and proactive corporate learning cultures. Federal defence contracts further anchor domestic demand as agencies test soldier readiness modules. Silicon Valley’s start-up pipeline stimulates headset and software innovation, feeding a robust reseller channel.

Europe follows with strong automotive and industrial clusters that rely on VR for design validation and worker safety drills. Regulatory clarity on medical devices and data privacy safeguards lend confidence to healthcare deployments. Regional funding programs such as Horizon Europe back applied research, expanding academic-industry partnerships.

Asia-Pacific records the briskest 26.4% CAGR, propelled by Chinese provincial subsidies, Japanese workplace-safety mandates, and South Korean smart-manufacturing initiatives. China launched over 100 new VR attractions in 2024, integrating cultural IP into multisensory experiences. Japanese firms like Jolly Good partner with global universities to distribute clinical training modules, while India’s edtech sector pilots VR STEM labs in rural districts.

Latin America and the Middle East and Africa represent emergent pockets where bandwidth and cost constraints presently slow uptake. Nonetheless, universities in Brazil and Saudi Arabia explore 5G-enabled distance education, laying early groundwork. Government digital-economy visions hint at future investment waves that could lift regional contributions to the overall Virtual Reality market.

Competitive Landscape

The Virtual Reality market shows moderate fragmentation. Meta leads consumer shipments but shoulders cumulative operating losses beyond USD 58 billion since 2020, underlining long-term commitment over near-term profit. Apple positions Vision Pro at USD 3,499 for premium productivity niches, leveraging brand equity to justify pricing. Sony, HTC, and Pico address discrete needs from enterprise design reviews to location-based entertainment, while Samsung readies a Google-powered headset to re-enter the field.

Vertical integration emerges among hardware firms that now bundle app stores, analytics dashboards, and device-management suites. Meta’s partnership with defence contractor Anduril widens exposure to military budgets, reflecting diversification beyond consumer play. Chipmakers like Qualcomm invest in ultrasound haptic patents to secure component-level moats and licence revenue.

Software specialists target industry pain points: ArborXR acquired InformXR to merge headset fleet control with learner analytics, and Click Therapeutics secured FDA clearance for prescription VR migraine therapy. White-space remains in non-gaming AAA content, industrial workflow connectors, and thermally efficient optics. Competitive intensity is therefore expected to escalate as incumbent tech giants and nimble start-ups chase the same adjacencies within the Virtual Reality market.

Virtual Reality (VR) Industry Leaders

-

Lenovo Group Ltd

-

Samsung Electronics Co. Ltd.

-

Sony Corporation

-

Pico Interactive Inc.

-

Meta Platforms (Meta Quest)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Infinite Reality secured USD 3 billion in funding, raising its valuation to USD 12.25 billion following acquisitions of Landvault and The Drone Racing League.

- January 2025: Infinite Reality and Google Cloud began a five-year partnership to scale immersive digital experiences across e-commerce, sports, and education.

- February 2025: Meta reported USD 1.08 billion in Q4 2024 Reality Labs revenue, the division’s highest to date.

- April 2025: Click Therapeutics received FDA marketing authorisation for CT-132, a prescription digital therapeutic for episodic migraine.

- May 2025: ArborXR bought InformXR and launched ArborXR Insights after closing a USD 12 million Series A round.

Global Virtual Reality (VR) Market Report Scope

Virtual reality (VR) technology, a computer-simulated reality creating an artificial environment, is increasingly used in applications like education, gaming, and AI. This immersive multimedia offers a 3D virtual world, enhancing learning experiences and gaming environments. AI integration further enriches the virtual environment. The development of the metaverse, a collective shared space combining VR, augmented reality, mixed reality, and brain-computer interface, promises an interactive virtual reality experience. The gaming sector dominates the VR market segmented by hardware, end-user, and geography, with North America leading due to the presence of numerous startups focusing on computer-generated reality technologies.

The market is defined by the revenue accrued from the sale of virtual reality solutions to different end-user verticals worldwide.

The virtual reality (VR) market is segmented by type (hardware (tethered HMDs, standalone HMDs, and screenless viewer) and software), end-user industry (gaming, media and entertainment, retail, healthcare, military and defense, real estate, and education), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Offering | Hardware | |||

| Software | ||||

| Services | ||||

| By Device Form Factor | Tethered HMD | |||

| Stand-alone HMD | ||||

| Screenless Viewer | ||||

| CAVE / Immersive Rooms | ||||

| By Immersion Level | Non-Immersive | |||

| Semi-Immersive | ||||

| Fully-Immersive | ||||

| By End-User Industry | Gaming | |||

| Media and Entertainment | ||||

| Healthcare | ||||

| Education and Training | ||||

| Military and Defense | ||||

| Retail and eCommerce | ||||

| Real Estate and Architecture | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Egypt | ||||

| Rest of Africa | ||||

| Hardware |

| Software |

| Services |

| Tethered HMD |

| Stand-alone HMD |

| Screenless Viewer |

| CAVE / Immersive Rooms |

| Non-Immersive |

| Semi-Immersive |

| Fully-Immersive |

| Gaming |

| Media and Entertainment |

| Healthcare |

| Education and Training |

| Military and Defense |

| Retail and eCommerce |

| Real Estate and Architecture |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Virtual Reality market?

The Virtual Reality market stands at USD 12.88 billion in 2025.

How fast is the Virtual Reality market growing?

The market is forecast to grow at a 26.30% CAGR, reaching USD 41.42 billion by 2030.

Which segment will see the quickest growth in the next five years?

Software associated with VR experiences is projected to rise at a 27.7% CAGR as enterprises demand scalable content.

Why is healthcare adoption accelerating?

FDA approvals for therapeutic and surgical-training applications validate clinical efficacy, driving a 28.2% CAGR in healthcare spending.

What remains the biggest hurdle to enterprise VR rollouts?

Cybersickness, caused by sensory mismatch, continues to limit session length and user acceptance despite advances in refresh rates and latency reduction.

Page last updated on: June 20, 2025