Vietnam Recycling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

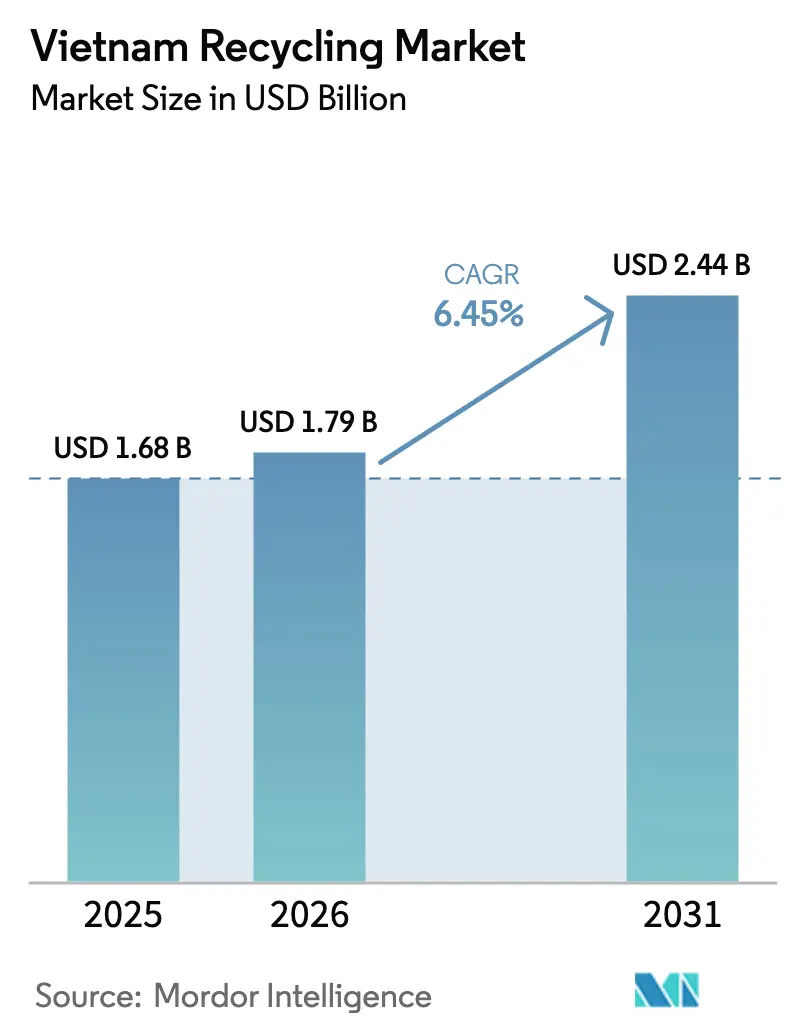

| Base Year Market Size (2025) | USD 1.68 Billion |

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

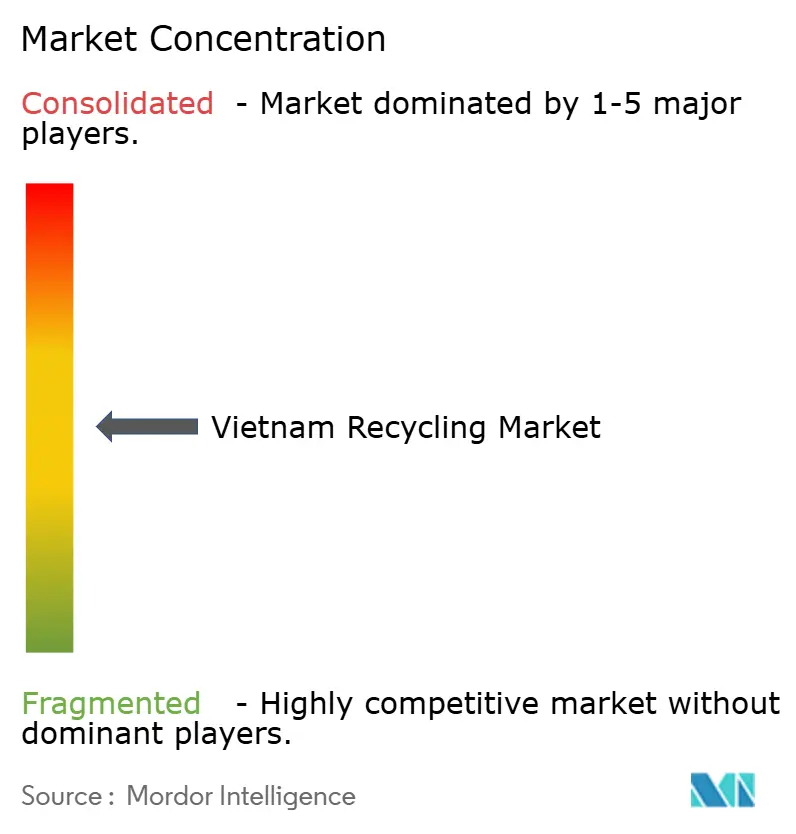

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Recycling Market Analysis by Mordor Intelligence

The Vietnam Recycling Market size is expected to grow from USD 1.68 billion in 2025 to USD 1.79 billion in 2026 and is forecast to reach USD 2.44 billion by 2031 at 6.45% CAGR over 2026-2031. This trajectory demonstrates how circular-economy policies, foreign direct investment in waste-to-energy assets, and mandatory Extended Producer Responsibility (EPR) rules are converting previously informal waste streams into formal supply chains. Early compliance spending by brand owners has improved collection finance, while emerging chemical recycling projects promise higher material yields from textile and battery waste. Rapid industrialization in northern and southern corridors keeps feedstock volumes high, and technology partnerships with multinationals lower the learning curve for local processors. At the same time, competitive pressure comes from the informal sector, whose pricing advantages still dominate many collection routes[1]Ministry of Industry & Trade, “Vietnam Recycling Market Development Outlook 2025,” MOIT Bulletin, moit.gov.vn.

Key Report Takeaways

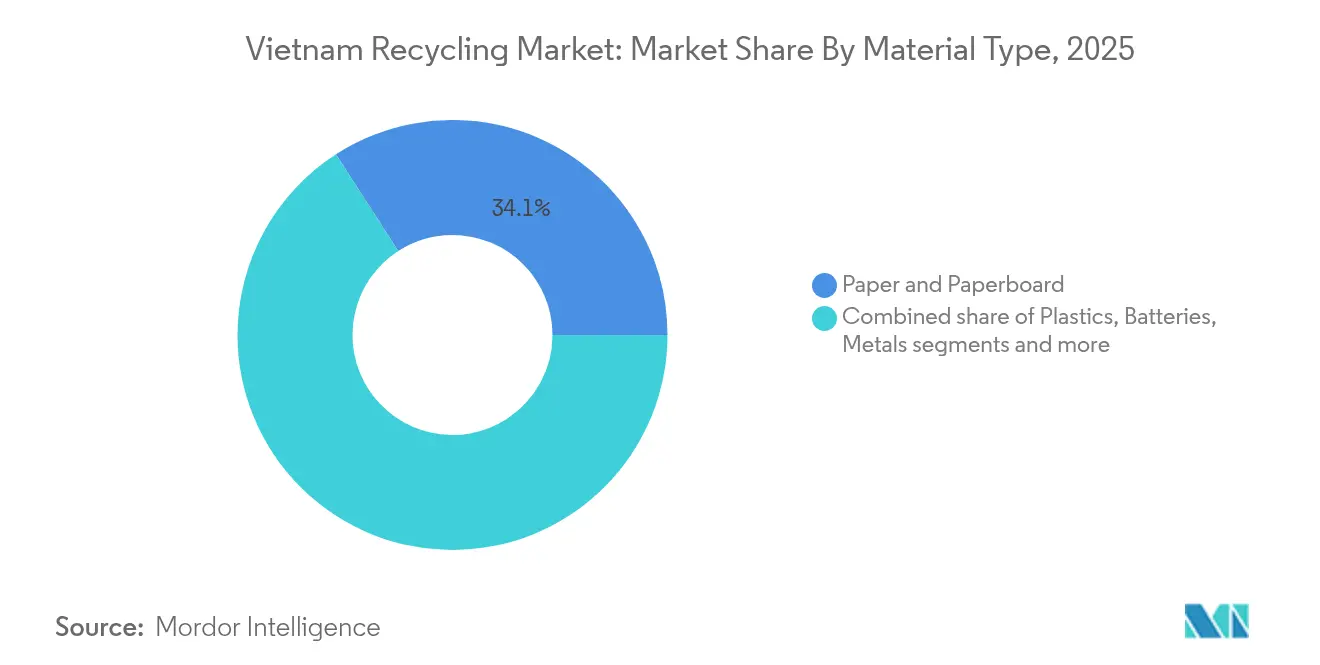

- By material type, Paper & Paperboard accounted for 34.12% share of the Vietnam recycling market size in 2025; Batteries are advancing at an 8.52% CAGR through 2031.

- By source, Industrial waste held 38.35% share of the Vietnam recycling market size in 2025, whereas Residential collection is growing at a 5.35% CAGR to 2031.

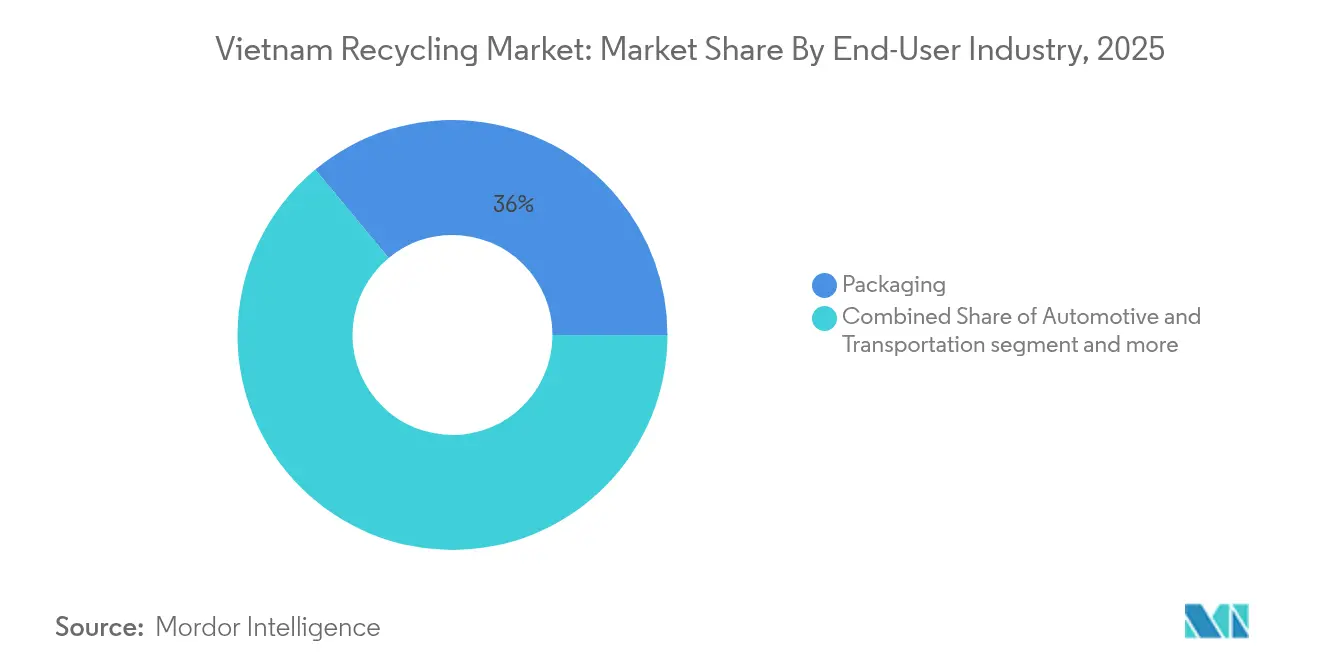

- By end-user industry, Packaging commanded 36.02% revenue share in 2025, and Electrical & Electronics is set to expand at a 6.18% CAGR through 2031.

- By recycling process, Mechanical recycling led with 68.25% share in 2025; Chemical/Advanced recycling is the fastest-growing process at a 7.58% CAGR.

- By geography, Northern Vietnam led with 41.95% of the Vietnam recycling market share in 2025, while Southern Vietnam is forecast to expand at a 7.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Recycling Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory EPR decrees driving formal collection financing | +1.8% | Nationwide | Short term (≤ 2 years) |

| Rapid brand-led demand for rPET & rHDPE packaging in southern industrial corridors | +1.2% | Southern Vietnam | Medium term (2-4 years) |

| Surge in FDI for waste-to-energy plants around the Hanoi–Hai Phong growth pole | +1.1% | Northern Vietnam | Medium term (2-4 years) |

| Booming electronics manufacturing cluster triggering formal e-scrap feedstock | +0.9% | National hubs | Long term (≥ 4 years) |

| Textile exporters’ zero-waste commitments accelerating fiber recycling | +0.8% | Central & Southern Vietnam | Medium term (2-4 years) |

| Construction & demolition waste reuse targets | +0.7% | Major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory EPR Decrees Driving Formal Collection Financing

Vietnam’s EPR framework, enforced since January 2024 under Decree 08/2022/ND-CP, sets minimum recovery rates of 20% for carton paper and 22% for aluminum packaging, compelling producers to finance recycling either directly or via third-party organizations. PRO Vietnam has grown to more than 30 member companies and collaborates with the National University of Ho Chi Minh City to design material-recovery technology. Companies can meet obligations by running in-house plants, outsourcing to certified recyclers, or paying into the Environmental Protection Fund, each path funneling fresh capital into formal systems. Although small rural districts still rely on informal collectors, EPR rules have already lifted private investment in baling stations and material-recovery facilities, narrowing the supply gap for plastics and fiber[2]Ministry of Natural Resources & Environment, “Decree 08/2022/ND-CP on Extended Producer Responsibility,” Official Gazette, monre.gov.vn.

Rapid Brand-Led Demand for rPET & rHDPE Packaging in Southern Industrial Corridors

Brand owners producing beverages, cosmetics, and household goods inside Ho Chi Minh City’s industrial zones are now contractually obliged to lift recycled-content ratios to satisfy export rules in the European Union and North America. Duy Tan’s USD 60 million Long An facility, able to process 100,000 tons of used bottles per year, illustrates how premium demand offsets higher processing costs even when virgin resin prices soften. The plastics market is forecast to climb from 10.92 million tons in 2024 to 16.36 million tons by 2029, reinforcing a structural pull for food-grade recyclate. Because only 25% of post-consumer plastic is currently captured for recycling, brands have begun underwriting collection hubs, offering volume-based incentives to informal pickers, and signing multi-year off-take contracts with certified processors. Such actions explain why the Vietnam recycling market continues to draw technology partners focused on recycled polymers.

Surge in FDI for Waste-to-Energy Plants Around the Hanoi–Hai Phong Growth Pole

Concessionary loans from the Asian Development Bank and the International Finance Corporation are financing large-scale incineration units that both treat waste and generate grid power. Hanoi’s Soc Son plant processes 5,000 tons per day and exports 75 MW, while the IFC-backed Cuu Yen project in Bac Ninh will handle 500 tons daily and supply 11.6 MW. These facilities secure long-term feedstock contracts with municipalities, providing predictable revenue streams for recyclers that pre-sort materials before combustion. The clustering of projects near ports and power lines lowers logistics costs and explains why Northern Vietnam remains the biggest regional contributor to the Vietnam recycling market.

Booming Electronics Manufacturing Cluster Triggering Formal E-Scrap Feedstock

Vietnam hosts some of Samsung’s largest plants worldwide, plus expanding assembly lines for Apple suppliers and contract manufacturers. Formal e-scrap capacity is below 40 kt/year, yet plant upgrades by TES-AMM and new permits for ISO-compliant smelters are closing the gap. VinFast’s partnership with Li-Cycle sends spent lithium-ion packs to hydrometallurgical facilities that recover cobalt, nickel, and lithium, an advanced process that supports high-value circular loops. With more than 11 million tons of batteries forecast to retire globally by 2035, local processors are positioning themselves to become regional hubs for cathode-active-material extraction.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Informal Sector Controlling > 60% Supply of Recyclables | -1.8% | National, concentrated in rural and peri-urban areas | Short term (≤ 2 years) |

| Coupled Virgin-Recyclate Resin Pricing Discouraging rPolymer Uptake | -1.1% | Industrial zones, Southern and Northern Vietnam | Medium term (2-4 years) |

| Undercapacity of Licensed E-Waste & Battery Treatment Facilities (<40 kt/yr) | -0.9% | National, acute in electronics manufacturing hubs | Long term (≥ 4 years) |

| Land-Scarcity Limiting Modern MRF & Landfill Upgrades in Tier-1 Cities | -0.7% | Hanoi, Ho Chi Minh City, major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Informal Sector Controlling More Than 60% Supply of Recyclables

Roughly 16,000 waste pickers and thousands of “craft villages” collect, sort, and sell recyclables outside formal channels. They handle more than 30% of municipal waste in big cities and an even higher share in peri-urban areas. While their work is indispensable, it erodes the quality and traceability brands need for export-compliant recycled content. The United Nations Development Programme and the Norwegian Embassy have funded pilot material-recovery facilities in Quang Ninh and Kien Giang that integrate informal workers, but scaling these models nationwide remains complex. Until supply chains are formalized, processors will face shortages and inconsistent bale quality, limiting throughput even as demand climbs.

Coupled Virgin-Recyclate Resin Pricing Discouraging rPolymer Uptake

When crude oil prices fall, virgin polyethylene and PET resins become cheaper, shrinking the price premium that recyclers must earn for cost-effective operations. Duy Tan reports 40-45% material loss in bottle-to-bottle reprocessing, pushing up unit costs and widening the price gap with virgin resin. Commodity buyers in export-oriented manufacturing often choose lower-priced virgin inputs, particularly when procurement contracts prioritize cost over sustainability. Without stabilizing mechanisms such as recycled-content tax incentives or public-sector purchasing quotas, the Vietnam recycling market will struggle to convert stated demand into actual sales volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Paper Leads While Batteries Surge

Paper & Paperboard represented 34.12% of the Vietnam recycling market share in 2025, reflecting the constant flow of corrugated boxes and wrapping used in export packaging. Domestic mills buy baled paper at predictable volumes, and EPR rules secure minimum recovery targets for cartons. Standardized grades mean baling stations achieve high commercial recovery rates, which helps the Vietnam recycling market maintain stable margins. Imports of recovered fiber remain low, keeping local prices attractive for collectors and mills. Meanwhile, the Batteries segment is projected to register an 8.52% CAGR, the fastest among materials, as electric motorcycles, cars, and consumer electronics proliferate. VinFast’s cell-take-back program and Li-Cycle’s hydrometallurgical line create industrial-scale outlets for spent lithium-ion packs, ensuring end-of-life pathways for high-value metals. Since batteries carry strict handling rules, formal processors gain a competitive moat over informal scrap yards.

The paper segment’s dominance rests on established mill capacity in northern and southern industrial belts, where logistics costs stay low and quality control is simpler. Large exporters now specify recycled-content liners to meet buyer sustainability policies, underpinning demand. Battery recycling, by contrast, involves sophisticated fire-suppression, cryogenic, or water-based systems, translating into higher capital intensity. Investors view these barriers as an opportunity to capture above-average margins if feedstock availability remains steady. As a result, both materials one mature, one nascent illustrate the dual structure of the Vietnam recycling market, where scale and technology coexist to meet diverging customer requirements.

By Source: Industrial Dominance Meets Residential Growth

Industrial activities supplied 38.35% of the Vietnam recycling market size in 2025 thanks to electronics, textiles, and automotive assembly clusters that generate homogeneous, high-volume scrap. Factories often use on-site balers or compaction units, lowering contamination and easing downstream processing. Long-term service contracts give recyclers predictable cash flows, enabling investments in automated sorting and shredding. Residential waste is the fastest-growing source at a 5.35% CAGR as city governments roll out mandatory separation guidelines and neighborhood collection points. Deposit-return pilots for PET bottles in Ho Chi Minh City show redemption rates above 80%, reflecting strong consumer engagement.

Industrial supremacy mirrors Vietnam’s export-oriented economy, characterized by large-scale industrial parks where waste generators agree to year-round supply commitments. Residential growth, however, is essential for filling the gap in paper and flexible-plastic feedstock because household waste remains under-collected. EPR levies fund awareness campaigns and subsidies for color-coded bins to improve source separation. International donors, including the Norwegian Government, finance digital-tracking platforms that pay informal workers directly, channeling material into certified facilities. Together, these trends diversify feedstock intake, making the Vietnam recycling market less vulnerable to single-sector shocks.

By End-User Industry: Packaging Leads Electronics Expansion

Packaging accounted for 36.02% of the Vietnam recycling market size in 2025, driven by rising exports of consumer goods requiring corrugated boxes, shrink film, and pallets. Decree 08/2022/ND-CP forces brand owners to recover a share of their packaging, creating guaranteed off-take volumes for processors. Electrical & Electronics is forecast to outpace all other end-users at a 6.18% CAGR to 2031, fueled by the relocation of global contract manufacturers into Vietnam. Samsung’s accelerated carbon-neutrality program includes strict waste-recovery key-performance indicators, sending circuit boards, plastics, and metals into formal channels.

Packaging’s leadership owes to streamlined logistics: box plants and label converters often sit inside or near industrial parks, simplifying backhaul of scrap. Processors rely on established fiber and PET sorting lines that deliver predictable purity levels. Electronic waste, although smaller in tonnage, offers higher revenue per kilogram because of gold, copper, and critical minerals within printed-circuit assemblies. Formal e-scrap operators such as TES-AMM deploy automated shredders and eddy-current separators to recover these metals at scale. Hence, packaging secures baseline tonnage, while electronics generate margin upside, together reinforcing the growth story of the Vietnam recycling market.

By Recycling Process: Mechanical Maturity Meets Chemical Innovation

Mechanical recycling dominated with 68.25% market share in 2025, reflecting decades of investment in shredders, granulators, and washing lines for single-polymer streams like PET and HDPE. These plants supply food-grade flake or pellet to beverage and detergent companies, closing the loop on high-volume packaging. Chemical/Advanced recycling is the fastest-growing process at a 7.58% CAGR, underpinned by textile and multi-layer plastic waste that mechanical methods cannot handle effectively. Syre’s depolymerization technology converts polyester garments back to monomers without degrading fiber quality, while pilot pyrolysis units target mixed polyolefin films.

Mechanical dominance stems from lower capital costs and wide raw-material availability. Operators often retrofit imported equipment sourced from Japan or Europe and reach breakeven at modest scales. Conversely, chemical routes demand precise process controls, higher energy inputs, and downstream purification, elevating entry barriers but also producing virgin-quality output. Both approaches co-exist in the Vietnam recycling market: mechanical lines maximize throughput for mass-market goods, whereas chemical plants unlock value from complex or contaminated waste streams. As regulatory standards tighten purity requirements, chemical recycling is likely to cannibalize select mechanical feedstocks, shifting the technology mix over time.

Geography Analysis

Northern Vietnam commanded 41.95% of total revenue in 2025, thanks to the Hanoi–Hai Phong industrial corridor’s dense manufacturing footprint and early deployment of waste-to-energy infrastructure. The Soc Son facility, operating at 5,000 tons per day and generating 75 MW, anchors formal waste flows that support upstream paper and plastics sorting lines. Samsung’s main phone and display campuses in Bac Ninh and Thai Nguyen contribute stable e-scrap volumes, while cross-border proximity to China helps equipment suppliers install high-speed balers and optical sorters quickly. Although informal collectors remain prominent in peri-urban districts, municipal public-service contracts now include penalties for uncontrolled dumping, pushing recyclable material into compliant transfer stations.

Central Vietnam is emerging as a strategic node following Syre’s USD 1 billion polyester recycling complex in Binh Dinh, the largest facility of its type in Southeast Asia. Textile clusters in Da Nang and Hue will backhaul cutting scraps to Binh Dinh, replacing virgin PET imports. Provincial governments are offering tax holidays and land-lease incentives to lure supplementary sorting yards and logistics hubs. Though still a mid-sized market, Central Vietnam benefits from highway upgrades and coastal ports that keep freight costs competitive. Forecast models point to mid-single-digit growth, making the region a diversification play for investors seeking exposure beyond the traditional north-south axis.

Southern Vietnam posts the fastest expected CAGR at 7.08% through 2031, powered by Ho Chi Minh City’s consumer base and export-oriented industrial parks in Long An and Binh Duong. Duy Tan’s bottle-to-bottle plant has become a showcase for circular packaging, while pilot anaerobic-digestion units convert food waste into biogas and organic fertilizer for peri-urban farms. PRO Vietnam’s headquarters facilitate coordination among 30 brand owners that collectively financed the recovery of 64,000 tons of packaging in 2024. International aid programs fund deposit-return pilots in Kien Giang, demonstrating the feasibility of rural plastic-capture models. Southern Vietnam thus offers simultaneous opportunities in high-margin polymers and decentralized organics management, reinforcing its role as the growth engine of the Vietnam recycling market.

Competitive Landscape

Competitive intensity is moderate. State-owned enterprise URENCO dominates municipal collection in Hanoi, while VietCycle leads in scrap-paper aggregation contracts tied to packaging mills. Global players such as Veolia and SUEZ secure service concessions for high-profile sites, leveraging proprietary sorting and leachate-control solutions to win government tenders. Their presence forces local firms to match international safety and quality standards, gradually formalizing operations across the Vietnam recycling market.

Strategy revolves around vertical integration and technology partnerships. Duy Tan shifted from producing virgin bottles to running a full bottle-to-bottle line, capturing margin along the value chain. VinFast’s alliance with Li-Cycle allows on-shore recovery of critical minerals, reducing reliance on foreign refiners. Similarly, PRO Vietnam aggregates producer levies and reinvests funds into shared infrastructure, de-risking capex for smaller brands that cannot build plants on their own. Forward-purchase agreements from multinational consumer-goods companies guarantee off-take, enabling processors to secure cheaper debt and accelerate plant commissioning.

Mergers and acquisitions are likely as regulations squeeze smaller operators that lack the capital to upgrade equipment or obtain environmental permits. Chemical-recycling entrants require deep pockets, encouraging joint ventures with material-science firms or private-equity-backed developers. Market observers expect consolidation around material-specific champion plastics, metals, fibers each serving export-compliant supply chains. As certification and traceability become non-negotiable for global buyers, the competitive advantage will shift toward processors that can deliver data-rich, audited feedstock at scale, redefining success within the Vietnam recycling market.

Vietnam Recycling Industry Leaders

-

DUYTAN Recycling Corporation

-

VietCycle Corporation

-

Urenco (Hanoi Urban Environment Co.)

-

GreenHub Vietnam

-

Dong Tien Paper Mill

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SYRE Impact AB obtained investment certification for a USD 1 billion polyester recycling complex in Binh Dinh, adding 250,000 tons of annual capacity.

- June 2025: PRO Vietnam signed a partnership with the National University of Ho Chi Minh City to co-develop EPR technologies.

- May 2025: VinFast expanded its Li-Cycle partnership for large-format battery recycling.

- April 2025: UNDP and the Norwegian Embassy launched circular-waste projects in Quang Ninh and Kien Giang.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Vietnam recycling market as the regulated collection, sorting, and re-processing of post-consumer and post-industrial paper, plastics, metals, glass, e-waste, and organics into secondary feedstock that re-enters manufacturing supply chains.

Scope exclusion: energy-from-waste plants, landfill gas capture, and any trade of unprocessed scrap sit outside this value pool.

Segmentation Overview

-

By Material Type

- Paper & Paperboard

- Plastics

- Metals

- Glass

- Electronics (E-waste)

- Batteries

- Organics & Compostables

- Construction & Demolition Debris

- Textiles

- Other Materials (rubber, etc.)

-

By Source

- Residential

- Commercial (Retail, Offices, etc.)

- Industrial (hazardous & non-hazardous)

- Other Sources (Institutional, Heatlhcare, Agricultural, etc.)

-

By End-User Industry

- Packaging

- Automotive & Transportation

- Electrical & Electronics

- Food & Beverage

- Construction

- Retail (E-commerce, Fashion)

- Others (agriculture, energy, etc.)

-

By Recycling Process

- Mechanical Recycling

- Chemical / Advanced Recycling

- Biological (Composting/Anaerobic Digestion)

- Thermal (Pyrolysis, Gasification)

- Others (Electrochemical & Metallurgical Processes, Semi-automated Sorting)

-

By Geography

- Northern Vietnam (Red River Delta + Northeast)

- Central Vietnam (North-Central, Central Coast)

- Southern Vietnam (Southeast + Mekong Delta)

Detailed Research Methodology and Data Validation

Primary Research

Phone and on-site interviews with municipal officers, formal recyclers, informal collectors, converters, and brand sustainability leads in Hanoi, Ho Chi Minh City, and southern hubs let us test price points, plant load factors, and informality shares. Short web polls of packaging and electronics producers sharpen rPET, rHDPE, and recycled-pulp demand signals.

Desk Research

We begin with General Statistics Office waste audits, customs HS-code ledgers, and Ministry of Natural Resources circular-economy bulletins to anchor yearly tonnage and recovery yields. Industry materials, Vietnam Paper & Pulp Association recovery ratios, Institute of Marine Environment leakage surveys, and UNDP circular roadmaps enrich trend understanding. Our analysts then verify company scale, investment news, and trade lanes through D&B Hoovers, Dow Jones Factiva, and Volza shipment feeds. These examples show breadth; many further outlets informed the worksheet, and Mordor's paid databases supplied hard-to-find financials.

Market-Sizing & Forecasting

Mordor analysts open with a top-down rebuild of national waste, apply documented collection rates, contamination losses, and material yields, then reconcile totals with bottom-up spot checks such as sampled recycler revenues and average selling price multiplied by output. Core inputs include EPR levy inflows, industrial output index, virgin-to-recycled resin price spread, import-quota ceilings, and packaging demand growth. A multivariate regression on these drivers underpins 2025-2030 projections, while scenario tests show effects of policy lags or accelerated FDI.

Data Validation & Update Cycle

Outputs run through variance checks against customs statistics and commodity decks, pass peer review, and refresh each year; interim updates trigger when new regulation or capacity shocks move the baseline. Our approach keeps clients current without overreacting to short-term noise.

Why Mordor's Vietnam Recycling Baseline Earns Trust

Published estimates diverge because firms choose different material baskets, price bases, or refresh cadences. Some fold waste-to-energy revenue into recycling, others quote plastics only, and a few upscale volumes without reconciling EPR cash flows or import caps.

The comparison shows why decision-makers lean on us: our scope mirrors real material-recovery economics, our steps are traceable to public data plus on-ground interviews, and regular refreshes keep figures dependable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.68 bn (2025) | Mordor Intelligence | - |

| USD 2.05 bn (2024) | Global Consultancy A | Adds waste services and landfill credits |

| USD 18.6 bn (2025) | Trade Journal B | Counts recycled-content packaging value chain |

| USD 0.17 bn (2022) | Research Boutique C | Tracks plastics only |

The comparison shows why decision-makers lean on us: our scope mirrors real material-recovery economics, our steps are traceable to public data plus on-ground interviews, and regular refreshes keep figures dependable.

Key Questions Answered in the Report

What is the current value of the Vietnam recycling market?

The market is valued at USD 1.79 billion in 2026 and is projected to reach USD 2.44 billion by 2031.

Which material is recycled the most in Vietnam?

Paper & Paperboard is the largest material segment, holding 34.12% of total revenue in 2025.

Why are batteries the fastest-growing recycling segment?

Electric-vehicle expansion and producer take-back rules push battery recycling to an 8.52% CAGR through 2031.

How does Extended Producer Responsibility impact companies?

Decree 08/2022/ND-CP obliges producers to finance collection or pay fees, catalyzing formal recycling investments.

Which region grows the fastest in Vietnam’s recycling landscape?

Southern Vietnam shows the highest forecast CAGR of 7.08% thanks to industrial parks near Ho Chi Minh City.

What technologies dominate recycling processes?

Mechanical recycling holds 68.25% share today, but chemical recycling is growing the quickest at 7.58% CAGR.

Page last updated on: