Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

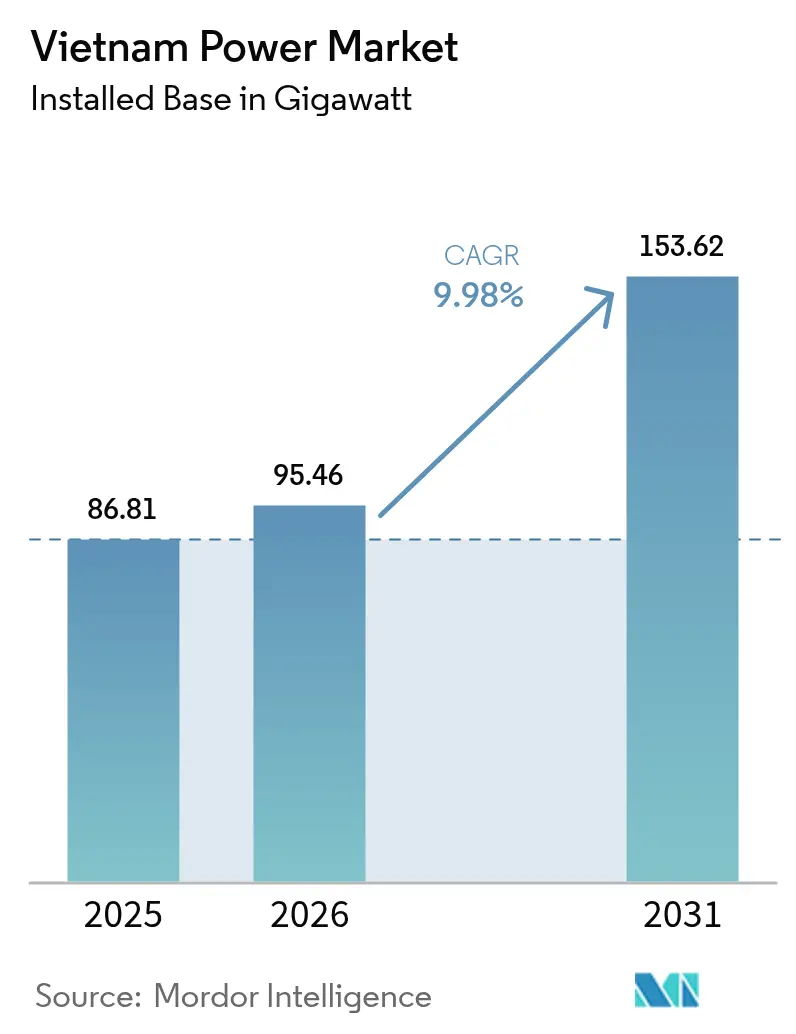

| Base Year Market Size (2025) | 86.81 gigawatt |

| Market Volume (2026) | 95.46 gigawatt |

| Market Volume (2031) | 153.62 gigawatt |

| Growth Rate (2026 - 2031) | 9.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Power Market Analysis by Mordor Intelligence

The Vietnam Power Market size is expected to grow from 86.81 gigawatt in 2025 to 95.46 gigawatt in 2026 and is forecast to reach 153.62 gigawatt by 2031 at 9.98% CAGR over 2026-2031.

The Vietnamese power market is on a rapid build trajectory. A USD 136 billion policy push under Power Development Plan 8 (PDP-8) underpins this acceleration, targeting 28–36% renewable energy by 2030 and 74–75% by 2050. Industrial electrification, data-center proliferation, and post-2023 blackout energy-security pledges are lifting capital spending, while new Direct Power Purchase Agreement (DPPA) rules open space for private renewable producers to transact directly with large users. Transmission upgrades, the above 500 kV backbone in particular, remove the grid bottlenecks that once stranded half of the installed capacity and forced 2.56 billion kWh of imports from China in 2024. A moderate competitive landscape dominated by state-owned EVN is evolving as international developers anchor offshore-wind pilots and LNG projects.

Key Report Takeaways

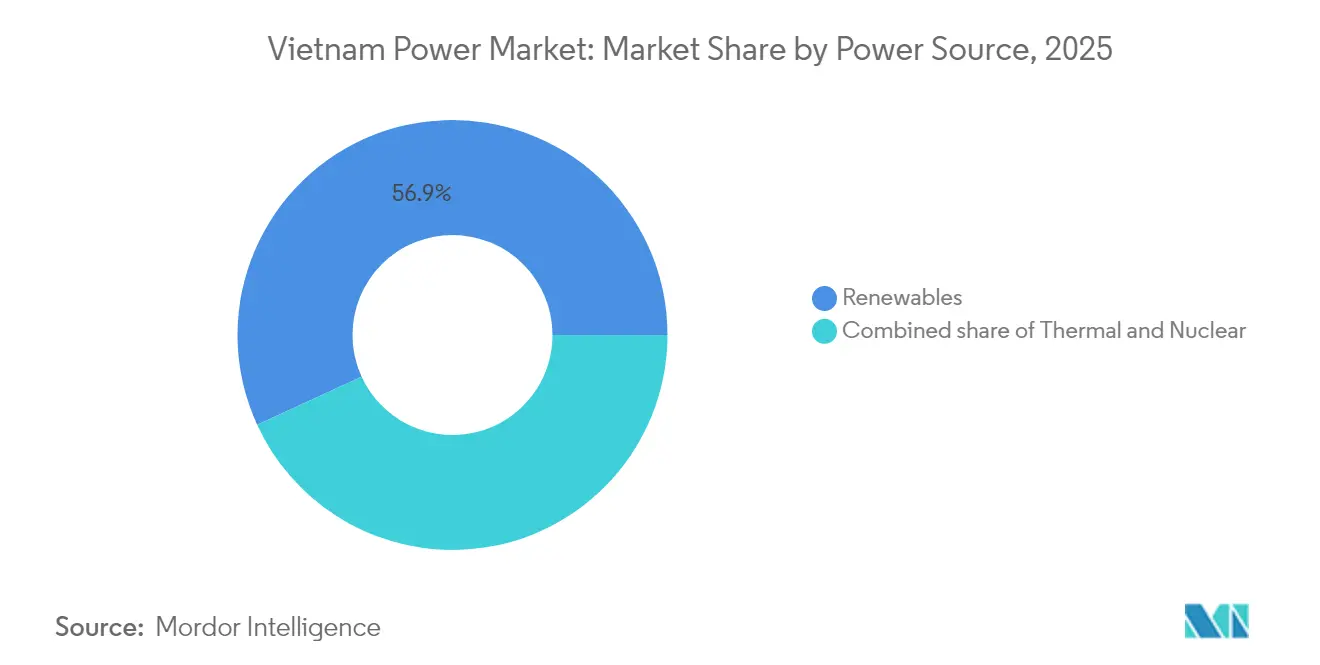

- By power source, renewables held 56.85% of the Vietnam power market share in 2025 and are projected to advance at an 11.46% CAGR through 2031.

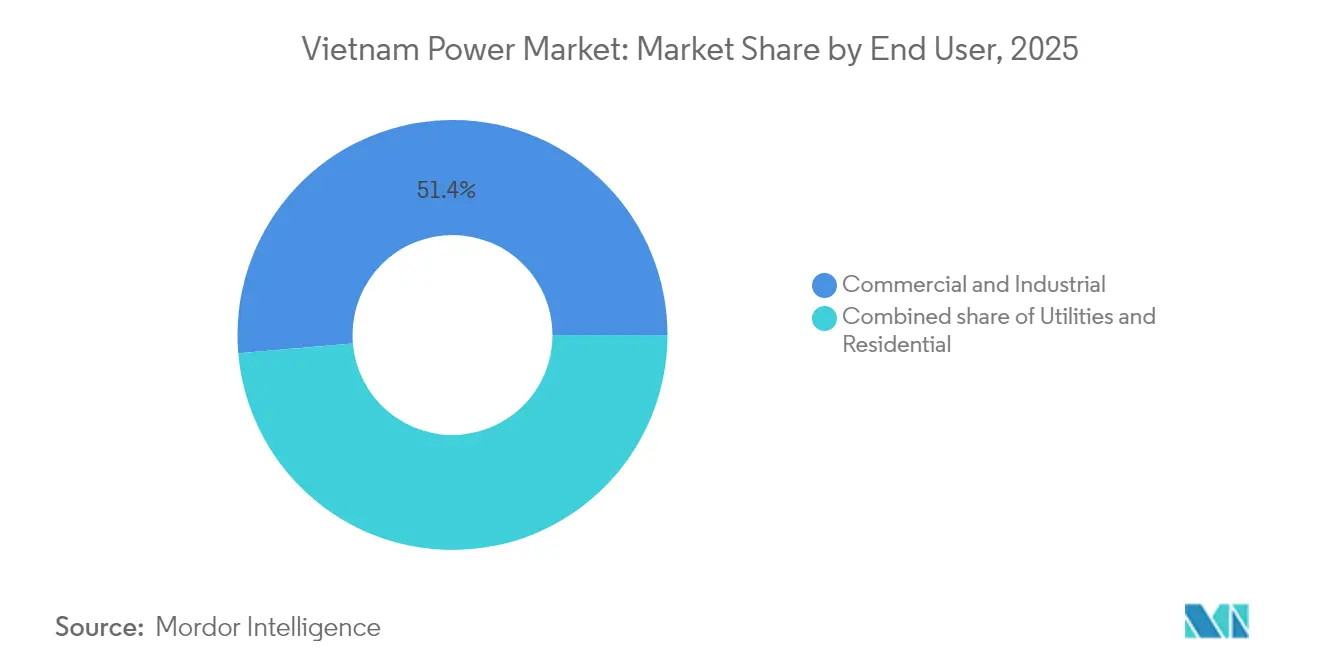

- By end user, commercial and industrial consumers accounted for 51.35% of the Vietnam power market size in 2025 and are tracking an 11.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid industrialisation-led electricity demand surge | +3.20% | National, with concentration in southern industrial zones (Ho Chi Minh City, Binh Duong, Dong Nai) | Medium term (2-4 years) |

| Government renewable-energy targets & FITs | +2.80% | National, offshore wind concentrated in central and southern coastal provinces | Long term (≥ 4 years) |

| PDP-8-driven FDI inflow in generation & grid | +2.10% | National, with priority transmission corridors linking northern hydropower to southern demand centers | Medium term (2-4 years) |

| Grid-modernisation funding (ADB, JICA) | +1.80% | National, with smart-grid pilots in Hanoi and Ho Chi Minh City | Long term (≥ 4 years) |

| Offshore-wind auction pipeline unlock | +1.50% | Central and southern coastal provinces (Binh Thuan, Ba Ria-Vung Tau, Tra Vinh) | Long term (≥ 4 years) |

| Data-centre boom raising flexible-generation need | +1.30% | National, with clusters emerging in Hanoi, Ho Chi Minh City, and Da Nang | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Industrialisation-Led Electricity Demand Surge

Industrial production jumped 8.4% 2024, lifting nationwide electricity use to 1 billion kWh in late May and prompting EVN to deploy demand-response programs.(1)Nguyen Lan, “Manufacturing Output and Electricity Use Surge,” VietnamPlus, vietnamplus.vn The semiconductor sector alone is valued at USD 18.23 billion in 2024 and is expanding at 11.48% CAGR, an outcome of Vietnam’s “Silicon Delta” policy that targets 45% of output from high-tech goods by 2030. South Korea reclaimed the top-investor slot in early 2025, with SK Group allocating multibillion-dollar budgets to LNG and small-modular reactors. Meeting the government’s 8% GDP objective for 2025 requires 12–16% yearly additions to generation, magnifying the Vietnam power market dependency on fast-track grid projects. Foreign investors now cite a stable electricity supply as a precondition for high-tech plant siting.

Government Renewable-Energy Targets & FITs

The revised PDP-8 sets a 500.4–557.8 billion kWh consumption band for 2030 while mandating that renewables claim 28–36% of the mix, signaling a pivot away from coal dominance. New price caps place onshore wind at VND 1,959.4/kWh (USD 0.078) in the north and near-shore projects at VND 1,987.4/kWh (USD 0.079), restoring investor visibility after years of stalled guidance.(2)Nguyen Quang, “Vietnam Issues Wind FITs for 2025,” Ministry of Industry and Trade, moit.gov.vnYet simultaneous retroactive tariff cuts threaten USD 13 billion in operating solar and wind assets, sparking protests from international developers. Decree 57/2025 introduced DPPAs, allowing private generators to bypass EVN and transact directly with qualified consumers, a reform expected to lower state-budget strain and quicken renewable deployment. These shifts align Vietnam with the ASEAN Power Grid vision that foresees clean sources covering up to 50% of regional output by 2030.

PDP-8-Driven FDI Inflow in Generation & Grid

Total infrastructure outlays are projected to climb 40% to USD 36 billion in 2025, with more than four-fifths tagged for power generation and transmission upgrades. Flagship deals include Huadian’s USD 2.4 billion green-hydrogen hub in Quang Tri and Vingroup’s USD 5.5 billion LNG complex in Hai Phong. On the grid side, the VND 7,410 billion (USD 300 million) 500 kV Lào Cai–Vĩnh Yên line will move 3,000 MW of northern hydro output when it goes live in September 2025. Equipment localization is gathering momentum; CS Wind is spending USD 200 million on a wind-tower plant in Long An to meet local offshore wind demand. Storage has emerged as a parallel play, with T&T Group targeting 2 GWh of annual battery output by 2026.

Grid-Modernisation Funding (ADB, JICA)

ADB has earmarked USD 16.5 billion for climate-resilient infrastructure, and Prime Minister Pham Minh Chinh requested additional support for large energy schemes during the April 2025 meetings. Completed upgrades have added 1,000 MW of reactive compensation across 20 substations ahead of the 2025 dry-season peak. JICA co-finances the 1,500 MW Quang Ninh LNG station developed by PetroVietnam Power, Tokyo Gas, and Marubeni, due online in 2026-2027. EVN reports 100% online customer-service coverage and AI-enhanced monitoring, trimmed outage times by 320% year-on-year. Extra 500 kV corridors will also carry 9,360–12,100 MW of imports from Laos, priced at USD 0.0695/kWh for hydroelectric flows

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow PPA approval & regulatory uncertainty | -1.80% | National, with particular impact on renewable project development | Short term (≤ 2 years) |

| ESG-driven coal-financing squeeze | -1.30% | National coal-fired generation, with phase-out pressure by 2050 | Long term (≥ 4 years) |

| Land-acquisition conflicts for solar farms | -0.90% | Central and southern provinces with agricultural land competition | Medium term (2-4 years) |

| Import-dependency for high-voltage equipment | -0.70% | National transmission infrastructure development | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Slow PPA Approval & Regulatory Uncertainty

Around USD 13 billion in wind and solar assets are at risk after auditors found misapplied FIT rules and suspended new PPAs pending review, prompting exits by Enel, Equinor, and Ørsted despite Vietnam’s headline plan to double capacity by 2030. A 6 GW offshore-wind zone was removed from the latest PDP-8 draft, deepening perceptions of policy volatility. Transmission approvals are equally sluggish; government data show only 2 of 16 mandated grid projects met 2024 timelines. These delays restrain the Vietnam power market’s tempo in the short run.

ESG-Driven Coal-Financing Squeeze

International lenders continue to tighten coal exposure, pressuring Vietnam’s plan to retire the fuel by 2050. Achieving net-zero requires USD 650 billion, much of it for biomass or ammonia conversions at existing coal sites. The JETP framework will channel concessional funds, but the gap remains wide; the Nam Dinh coal project is emblematic, losing ACWA Power in 2023 and now eyeing LNG repowering. Despite constraints, coal consumption set a record in 2024, revealing tensions between short-term reliability and long-term ESG compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Renewables Outpace Thermal Transition

Renewables delivered 56.85% of installed capacity in 2025, underscoring their status as the anchor of the Vietnam power market. The segment is forecast to compound at 11.46% annually through 2031 as solar rooftops scale, onshore wind spreads across the Central Highlands, and offshore wind turbines begin to populate typhoon-exposed coastal waters. Solar already totals 19.4 GW, yet curtailment surpasses 15% in Ninh Thuan and Binh Thuan during the dry season when local lines overload. High curtailment has prompted developers to pair new projects with battery storage, a trend facilitated by PDP-8’s target of 10–16 GW of batteries by decade-end. Offshore wind’s 6 GW 2030 target equates to 1.2 GW of annual installs starting in 2026, demanding prompt port upgrades and localized supply chains. Together, these trends point to an expanded Vietnam power market size at the segment level that will eclipse thermal additions within three years.

Thermal capacity remains relevant but is losing ground. Coal units ran at a 68% capacity factor in 2024 as merit-order rules favored cheaper wind and hydropower. New coal projects lack financing, and depleting offshore gas fields hinder gas-fired growth. The government, therefore, places nuclear back on the table with preliminary 4-6.4 GW plans for the 2030-2035 horizon, though finance and public acceptance remain hurdles. In the interim, combined-cycle gas and large-scale batteries are set to bridge the capacity gap and provide ramping support, shaping a technology mix that allows the Vietnam power market to continue its rapid growth while lowering emissions intensity.

By End User: Commercial and Industrial Dominance Persists

Commercial and industrial buyers consumed 51.35% of electricity in 2025 and are growing at 11.08% annually, making them the single most important demand center for the Vietnam power market. Semiconductor fabs run continuous processes and account for rising spot prices during industrial peak hours. Direct power purchase agreements now allow multinationals to lock in renewable electricity at fixed prices over 15-20 years, accelerating procurement pipelines that could reach 4 GW by 2028. Manufacturers are also installing rooftop arrays to hedge tariff hikes, further entwining production competitiveness with energy strategy.

Utilities and residential users occupy the remainder of demand but advance at a slower 7.95% CAGR. Household consumption per capita reached 2,400 kWh in 2024, a level now constrained by cross-subsidized tariffs and lingering distribution losses of 6.8%. Tariff reform is under ministerial review, and any upward adjustment would narrow the affordability gap between industrial and residential customers. Distribution-loss reduction programs, including smart meters and automated substations, are slated to shave technical losses toward a 5.5% regional benchmark, freeing capacity that can support the Vietnam power market without new generation.

Geography Analysis

Southern Vietnam, led by Ho Chi Minh City, Binh Duong, and Dong Nai, accounted for 47.85% of national electricity consumption in 2025 and registered the fastest peak-load growth. Local generation trails demand by around 2 GW, so the region draws heavily on 500 kV lines from northern hydropower plants. These corridors run at 92% utilization during evening peaks, forcing EVN to curtail central-region renewables to preserve grid stability. Upcoming transmission upgrades financed by ADB aim to relieve the choke point and unlock latent renewable capacity destined for the Vietnam power market.

The northern grid serves Hanoi, Hai Phong, and Quang Ninh. Coal plants supplied 57.35% of northern demand in 2025, but financing curbs and stricter emissions rules are accelerating a pivot to gas and cross-border imports. A 500 kV intertie with Laos, commissioned in June 2024, now enables up to 5,000 GWh of hydropower imports each year. Cross-border trade stabilizes supply during dry seasons when domestic hydropower recedes, illustrating the benefits of regional market integration for the Vietnamese power industry.

The central region hosts most of the nation’s solar and wind projects but suffers the highest curtailment rates. Transmission expansion is therefore synchronized with offshore wind rollout, ensuring that power produced along the coast can reach load centers inland and to the south. PDP-8 also contemplates subsea HVDC links that could shuttle surplus clean power to Malaysia and Thailand under the ASEAN Power Grid vision. Such infrastructure would position the Vietnam power market as both a net importer and net exporter at different times of the year, reinforcing energy security while monetizing renewable surpluses.

Competitive Landscape

The Vietnamese power market remains moderately concentrated. EVN controls transmission and distribution, but DPPA rules effective March 2025 allow private generators to strike direct deals with large users, lowering barriers for new entrants. Domestic groups such as T&T, Trung Nam, and Bamboo Capital scaled quickly on local financing and EPC know-how, yet technology partnerships drive true edge; PetroVietnam’s alliance with JERA on ammonia co-firing and Tokyo Gas-Marubeni’s Quang Ninh LNG consortium signal a shift toward integrated value chains.

European incumbents that once led offshore-wind pipelines have partially withdrawn over policy risk, opening doors for Asian investors and domestic utilities to capture acreage. Equipment localization reduces lead times: CS Wind’s Long An plant will supply regional tower demand, while Siemens Energy and GE bid to localize turbine assembly to meet PDP-8 local-content targets. The storage space is nascent but strategic; T&T aims to command a 40–50% national share with 2 GWh of annual battery output by 2026, competing with Chinese and Korean suppliers.

Digitalization now differentiates incumbents. EVN Southern Power’s AI roll-out lifted customer engagement metrics by 320% year-on-year, and the utility is piloting blockchain-based DPPA settlement for rooftop producers. New entrants that marry technology with project execution, such as Sigenergy in behind-the-meter storage, could capture emerging niches as the Vietnam power market matures.(4)Vietnam Electricity, “Annual Report 2025,” evn.com.vn

Vietnam Power Industry Leaders

Vietnam Electricity

General Electric

AES Mong Duong Power Company Limited

Mekong Energy Company Ltd

Jera Co Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: PetroVietnam Power has awarded an Engineering, Procurement, and Construction (EPC) contract to a consortium of Doosan Enerbility and PECC2 for the 1,155 MW Ô Môn IV combined cycle gas turbine (CCGT) power plant project.

- June 2025: Vingroup, through a consortium with VinEnergo, is indeed embarking on its largest energy venture to date with a USD 5.5 billion LNG power plant project in Hai Phong, Vietnam. This project, part of Vingroup's broader renewable energy and LNG power initiatives, aims to address Vietnam's growing energy demands and potential power shortages.

- May 2025: Vietnam Electricity (EVN) has increased retail electricity tariffs by 4.8%, raising the average price to VND 2,200/kWh (USD 0.087).

- April 2025: The Prime Minister of Vietnam approved an adjustment to the National Power Development Plan (PDP8), allocating USD 136 billion and establishing a renewable energy share of 28-36% by 2030.

Vietnam Power Market Report Scope

Power is generated through various primary sources such as coal, hydro, solar, thermal, etc. In utilities, it's a step before its delivery to its end users. Then the process is followed by transmission and distribution. Under this, the power generated is distributed via high-voltage lines (transmission lines) and low-voltage lines (distribution lines) as per the requirement of the end user.

The Vietnamese power market is segmented by power source and end-user. By power source, the market is segmented into thermal, including coal, natural gas, oil, and diesel; nuclear; renewables, including solar, wind, hydro, geothermal, biomass & waste, tidal. By end-user, the market is segmented into utilities, commercial and industrial, and residential.

The report also covers the market size and forecasts for the Vietnam Power Market in terms of GW for all the above segments.

By Power Source

| Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) |

By End User

| Utilities |

| Commercial and Industrial |

| Residential |

By T&D Voltage Level (Qualitative Analysis only)

| High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) |

| Medium-Voltage Distribution (13.2 to 34.5 kV) |

| Low-Voltage Distribution (Up to 1 kV) |

| By Power Source | Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear | |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) | |

| By End User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By T&D Voltage Level (Qualitative Analysis only) | High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) | |

| Medium-Voltage Distribution (13.2 to 34.5 kV) | |

| Low-Voltage Distribution (Up to 1 kV) |

Key Questions Answered in the Report

How large is the Vietnam power market today?

Installed capacity reached 95.46 GW in 2026 and is forecast to climb to 153.62 GW by 2031, reflecting a 9.98% CAGR.

Which segment holds the largest slice of national demand?

Commercial and industrial customers consumed 51.35% of electricity in 2025 and remain the dominant demand center through 2031.

What role will offshore wind play in future supply?

PDP-8 sets a 6 GW offshore wind target for 2030, requiring about 1.2 GW of annual installations from 2026 onward.

How is grid congestion being resolved?

ADB-financed 500 kV lines and JICA-backed smart-grid pilots aim to ease bottlenecks and cut curtailment, especially between central solar hubs and southern load centers.

What new procurement option is available to large power users?

The Electricity Law of 2024 authorizes direct power purchase agreements that allow industrial buyers to contract renewable generators outside EVN’s retail tariff.

Why is coal capacity shrinking?

ESG-driven financing restrictions have stranded nearly 10 GW of planned coal projects, prompting a pivot to gas, renewables, and batteries.

Page last updated on: