Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

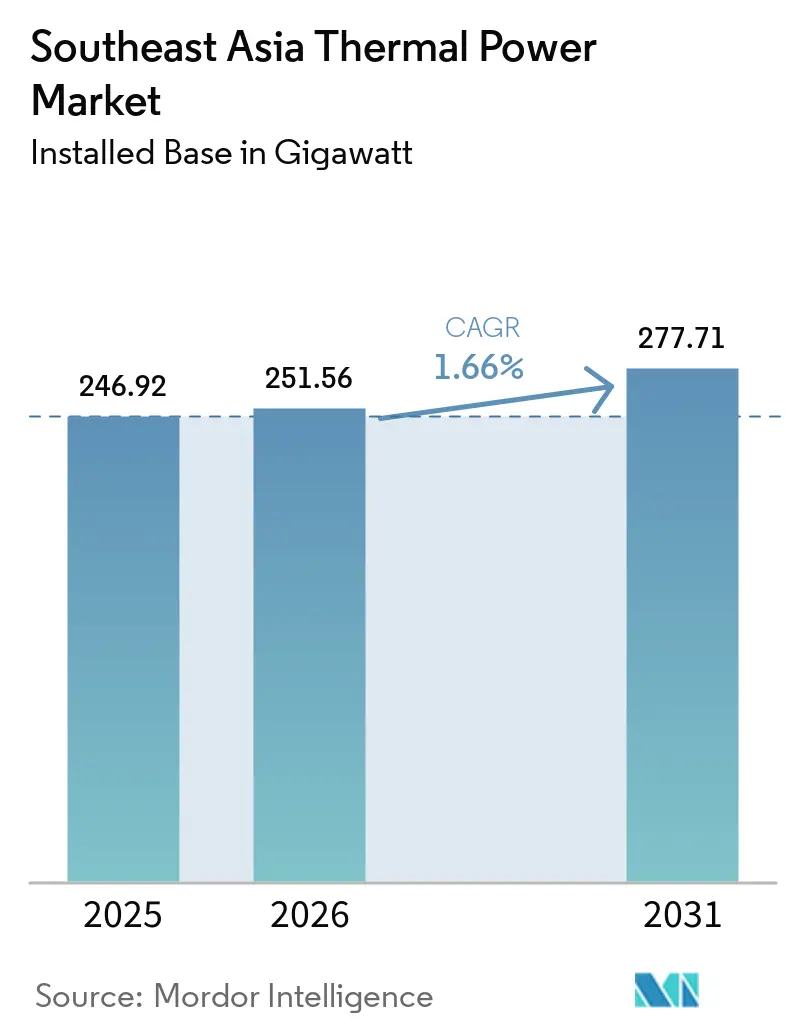

| Base Year Market Size (2025) | 246.92 gigawatt |

| Market Volume (2026) | 251.56 gigawatt |

| Market Volume (2031) | 277.71 gigawatt |

| Growth Rate (2026 - 2031) | 1.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Thermal Power Market Analysis by Mordor Intelligence

The Southeast Asia Thermal Power Market size in terms of installed base is projected to be 246.92 gigawatt in 2025, 251.56 gigawatt in 2026, and reach 277.71 gigawatt by 2031, growing at a CAGR of 1.66% from 2026 to 2031.

This modest rise hides a clear internal shift, as coal additions are slowing and new combined-cycle gas turbine projects are taking a larger share of planned commissioning. Indonesia remains the base that shapes the regional average, while Vietnam is emerging as the strongest growth center under the adjusted PDP VIII, which targets 22,524 MW of LNG-fired capacity by 2030 [1]Ministry of Industry and Trade, “Decision 768/QD-TTg,” Government of Vietnam, moit.gov.vn. The Southeast Asia thermal power market is also being reshaped by captive generation, because large industrial parks and data campuses are securing dedicated supply rather than relying only on public utility grids. State utilities still control most utility-scale development, but the independent power producer model is advancing in Vietnam and the Philippines as new LNG projects move ahead under revised contracting frameworks. Competition is tightening around access to high-efficiency gas turbine technology, which gives an advantage to large OEMs and makes execution capability more important than price alone.

Key Report Takeaways

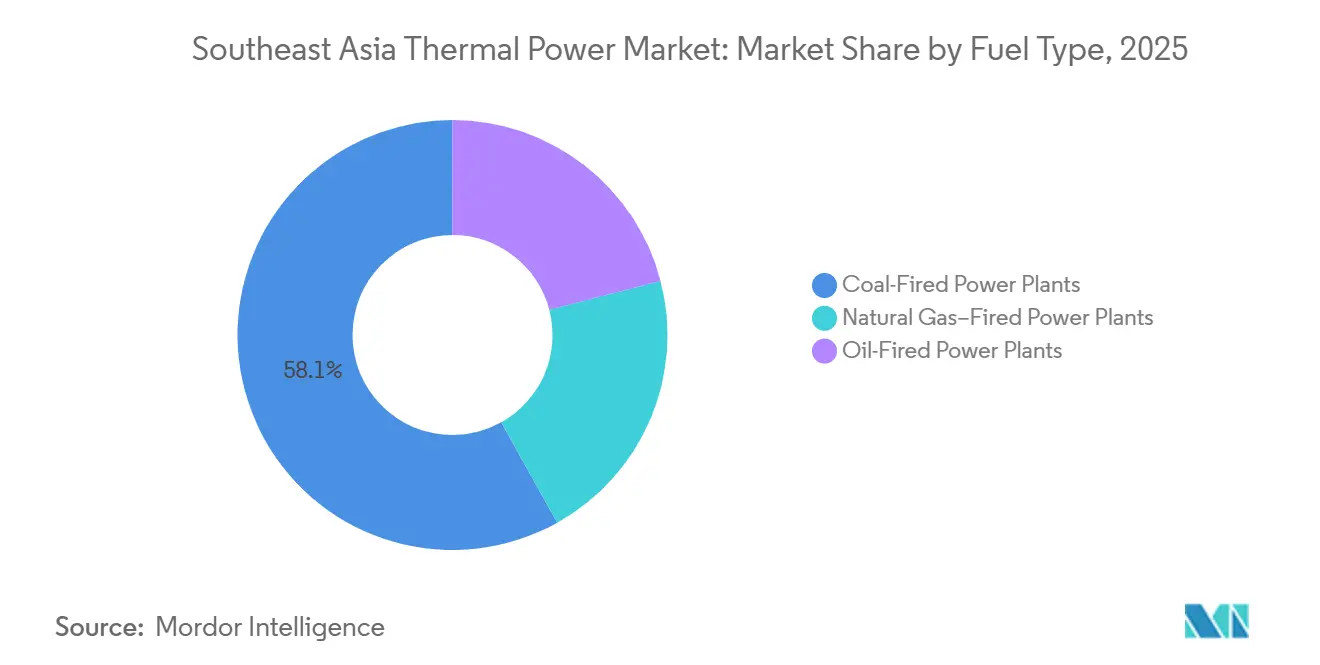

- By fuel type, coal-fired power plants accounted for 58.1% of the Southeast Asia thermal power market size in 2025, while natural gas-fired power plants are projected to expand at 4.9% CAGR through 2031.

- By technology, gas turbine and combined cycle held 48.3% share in 2025 and are projected to grow at 2.1% CAGR through 2031.

- By combustion method, turbine-based combustion held 46.1% share in 2025 and is projected to grow at 2.2% CAGR through 2031.

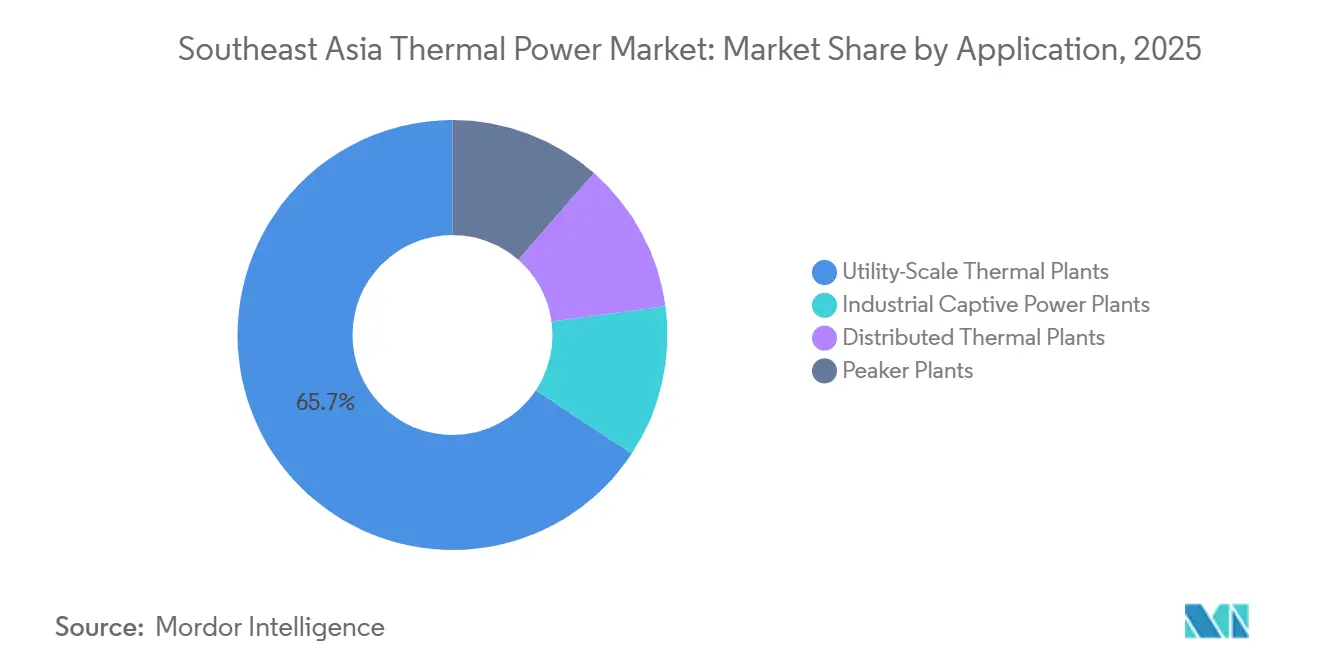

- By application, utility-scale thermal plants held 65.7% share in 2025, while industrial captive power plants are forecast to expand at 6.8% CAGR through 2031.

- By geography, Indonesia held 36.8% of the Southeast Asia thermal power market share in 2025, while Vietnam is forecast to expand at 7.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Thermal Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Baseload Demand From Industrialisation | +0.5% | Indonesia, Vietnam, Philippines, Malaysia | Short term (≤ 2 years) |

| Expansion Of LNG-To-Power Value Chains | +0.4% | Vietnam, Philippines, Malaysia, Singapore | Medium term (2-4 years) |

| Policy Focus On Grid Stability And Energy Security | +0.3% | Vietnam, Indonesia, Thailand, with spillover to Malaysia | Short term (≤ 2 years) |

| Financing Of HELE Coal By Japan And Korea | +0.2% | Indonesia, Vietnam | Medium term (2-4 years) |

| Rise Of Captive On-Site Power For Data Centres | +0.3% | Malaysia, Indonesia, Singapore | Short term (≤ 2 years) |

| Carbon-Credit Upside From Coal And Biomass Co-Firing | +0.1% | Indonesia, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Baseload Demand from Industrialisation

Manufacturing relocation is pushing concentrated electricity demand into Southeast Asian grids that were not built for such rapid industrial load growth. Indonesia is at the center of this shift, as its nickel-processing corridor and other resource-based industrial clusters require round-the-clock power and continue to favor thermal generation for reliability and cost visibility [2]Ministry of Energy and Mineral Resources, “RUPTL 2025-2034,” Government of Indonesia, esdm.go.id. In this setting, captive coal and gas plants remain the preferred option because they can deliver firm output at the scale needed by smelters and other continuous-process facilities. Captive coal capacity in Indonesia reached 16.6 GW in 2024, and another 14 GW was either planned or under construction, which shows how industrial demand is expanding outside the grid-connected coal moratorium framework. This shadow build-out means the Southeast Asia thermal power market is larger in practice than public utility statistics alone would suggest.

Expansion of LNG-to-Power Value Chains

Vietnam’s LNG-to-power program moved from policy ambition to project execution in 2026. PetroVietnam Power’s Nhon Trach 3 and 4 plants entered commercial operation on January 5, 2026, as the country’s first LNG-fired facility, using GE Vernova 9HA.02 turbines and a 25-year LNG supply contract with PV Gas. EVN then moved ahead with the Quang Trach II EPC contract, and the Ca Na LNG project reached financial close in April 2026 as the first LNG project selected through international competitive bidding under PDP VIII. The main challenge is not only fuel supply or equipment access, but also whether power purchase agreements can allocate risk in a way that supports project finance. Vietnam’s Energy Regulatory Authority stated in May 2026 that current PPAs still do not provide adequate risk-sharing between the state and investors.

Policy Focus on Grid Stability & Energy Security

Energy security became the main near-term driver of capacity planning across the Southeast Asia thermal power market in 2026. Vietnam’s Resolution 253/2025/QH15, effective March 1, 2026, gave urgent thermal and gas projects a faster approval route and allowed investor selection without competitive bidding for facilities deemed critical to energy security. Indonesia also signaled that coal will remain a primary fuel, and PLN’s latest long-term plan still points to 406 TWh of fossil-fuel-based electricity by 2034. This approach reflects concern over both system stability and foreign exchange exposure, because LNG imports add direct balance-sheet risk for governments managing external financing needs. As a result, coal and gas continue to be treated as reliability assets even while renewable targets are rising.

Rise of Captive On-Site Power for Data Centres

Data center growth is creating a new thermal demand base that sits partly outside traditional utility planning models. Malaysia had 3,800 MW of completed data center projects across 29 developments by September 2025, and load utilization increased sharply within the same year as new facilities ramped up operations. This new demand is lifting baseload needs around Klang Valley and Johor, where operators place a premium on reliability and low outage risk. Indonesia is also building AI-ready capacity, and low industrial electricity tariffs continue to support captive coal and gas solutions for large digital campuses. For the Southeast Asia thermal power market, this means demand growth is shifting toward industrial parks and digital infrastructure that often seek dedicated supply instead of depending only on public grids.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter ESG Lending And Multilateral Exit | -0.3% | Regional, with stronger effect in Indonesia, the Philippines, and Vietnam | Short term (≤ 2 years) |

| Rapid LCOE Decline Of Solar-Battery Hybrids | -0.4% | Singapore, Philippines, Thailand, Vietnam, Cambodia | Medium term (2-4 years) |

| Upstream Gas Decline In Indonesia And Malaysia Raising Supply Risk | -0.2% | Indonesia and Peninsular Malaysia | Medium term (2-4 years) |

| ASEAN Power-Grid Trade Curbing New Thermal Builds | -0.2% | ASEAN-wide, with early effects in Singapore and the Laos to Thailand corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter ESG Lending and Multilateral Exit

Financing conditions are tighter than they were earlier in the decade, even though natural gas still qualifies as a transition fuel under the ASEAN Taxonomy for Sustainable Finance. The 2025 divestment scorecard still showed large cumulative coal and gas financing in the region through 2024, with international banks and JBIC continuing to play major roles in project support. The harder constraint now comes from multilateral and blended-finance structures, because early retirement models still struggle when governments resist recognizing unrecovered capital losses. The cancellation of the Cirebon-1 early-retirement effort showed that even high-profile transition structures can fail when political alignment and compensation terms do not hold. This leaves the Southeast Asia thermal power market in a financing middle ground where gas remains bankable in many cases, but coal retirement is still slow and difficult.

Rapid LCOE Decline of Solar-Battery Hybrids

Solar and storage economics are improving quickly across Southeast Asia, and this is shortening the period in which new thermal plants look commercially secure. The pressure is strongest in systems with good solar resources and high LNG exposure, including the Philippines, Vietnam, and parts of Thailand. The 2026 LNG price shock widened the cost gap further because gas-fired generation costs respond immediately to fuel spikes, while solar project economics move far less in the short term. This does not remove the near-term need for thermal baseload and flexible backup, but it weakens the case for long-life unabated coal units and marginal gas projects. Biomass and ammonia co-firing requirements for aging coal units add another layer of compliance cost that further reduces the long-run appeal of existing assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Gas Momentum Builds Against a Coal Foundation

Coal-fired power plants held 58.1% share of installed thermal capacity in 2025, which kept coal as the largest fuel base in the Southeast Asia thermal power market. That dominance remained anchored by Indonesia’s 57 GW fleet and by Vietnam’s continued reliance on coal within its existing generation mix. New coal development outside Indonesia has already slowed sharply, and the most visible recent proposals have been tied to captive industrial use rather than utility-grid expansion. Natural gas-fired power plants are the fastest-growing fuel segment, with 4.9% CAGR projected through 2031 as LNG-to-power pipelines move forward in Vietnam, Malaysia, and the Philippines.

Vietnam’s operating mix still showed how far the transition has to go, because EVN reported that coal thermal contributed 52.8% of electricity output in the first quarter of 2026, while gas turbines contributed 7%. Even so, that gap is likely to narrow as LNG plants move from contract award to operation over the next several years. Oil-fired plants remain a residual part of the mix and continue to serve emergency peaking roles in the Philippines and in remote Indonesian island systems where grid and fuel options remain limited. The Southeast Asia thermal power market is therefore still coal-heavy in the near term, but its new-build path is moving toward gas, efficiency, and greater fuel flexibility.

By Technology: Combined Cycle's Efficiency Premium Commands Investment

Gas turbine and combined cycle technology claimed 48.3% of installed thermal capacity in 2025, and it is projected to grow at 2.1% CAGR through 2031. This position reflects decades of investment in Singapore, Thailand, and Malaysia, where gas-based fleets were built earlier and where efficiency standards are now steering replacement decisions toward modern combined-cycle assets. The next phase of growth is coming less from single mega projects and more from a broad wave of medium-scale replacements for aging open-cycle gas units. Steam cycle plants still hold a large base because they represent most of the coal fleet in Indonesia and Vietnam, and many of those assets will remain operational through the forecast period.

Utilities are trying to extend the relevance of steam-cycle assets through ultra-supercritical upgrades and biomass co-firing programs. PLN Energi Primer Indonesia supplied 460,368 tonnes of biomass for co-firing in the first quarter of 2026 after supplying 2.4 million tonnes during 2025, which shows that retrofit activity is moving from the pilot stage to broader execution. Combined heat and power remains underused in the Southeast Asia thermal power industry, even though industrial clusters in Johor and Selangor are well suited to facilities that can supply both electricity and process heat. Mitsubishi Power’s O Mon 4 award in Vietnam, using JAC-series gas turbines with combined-cycle efficiency above 64%, shows that the Southeast Asia thermal power industry is rewarding high-efficiency platforms that can make older steam-cycle assets look less competitive over time.

By Combustion Method: Turbine Dominance Signals a Maturing Fleet

Turbine-based combustion accounted for 46.1% of the Southeast Asia thermal power market size within the combustion method split in 2025, and it is projected to grow at 2.2% CAGR through 2031. This lead reflects the strong preference for gas turbines in new thermal additions, especially where grid operators need faster ramping and more flexible output to support rising renewable penetration. Pulverized fuel combustion still represents most of the legacy coal fleet across Indonesia and Vietnam, so it remains a major part of operating capacity even as its share of new investment falls. Recent project choices show that the coal fleet is not being abandoned immediately, but it is being pushed toward higher-efficiency configurations and lower-emission operating standards.

The Quang Trach 1 project in Vietnam illustrates this path, because the 1,400 MW ultra-supercritical coal plant synchronized its first unit to the grid in April 2026 and was reported to be operating at emissions levels well below the permitted limit. Fluidized bed combustion keeps a role in smaller industrial and fuel-flexible applications, particularly where biomass co-firing or mixed-fuel use makes boiler adaptability more valuable. Gasification and internal combustion engine systems remain niche technologies and mainly serve remote grids or pre-commercial project concepts in markets such as Indonesia, Myanmar, and islanded systems in the Philippines. The Southeast Asia thermal power market is therefore moving toward turbine-led growth, while older boiler-based combustion methods are being retained mainly where sunk capital and fuel access still favor continued operation.

By Application: Industrial Captive Power Disrupts the Utility Model

Utility-scale thermal plants held 65.7% share in 2025, but industrial captive power plants are forecast to expand at 6.8% CAGR through 2031 and are changing where new demand appears. The first driver is Indonesia’s resource-processing build-out, where nickel, aluminum, and petrochemical operations continue to favor dedicated thermal supply over dependence on grid expansion. Captive coal capacity in Indonesia reached 16.6 GW in 2024, with another 14 GW under construction or in planning, which points to sustained off-grid or semi-grid thermal development around industrial corridors. The second driver is digital infrastructure, where large data campuses in Malaysia and Indonesia are adding dense loads that prioritize uninterrupted power and often seek dedicated arrangements rather than relying entirely on utility networks.

Within the Southeast Asia thermal power industry, utility-scale plants still anchor procurement because state-owned utilities in Indonesia, Vietnam, Thailand, and Malaysia continue to lead large project development. Distributed thermal plants also remain relevant in the archipelagic systems of Indonesia and the Philippines, where diesel-to-gas switching is still a live policy and operating priority. Peaker plants are a smaller but important growth area, especially in Vietnam and the Philippines, where the rise of solar capacity is increasing the need for gas turbines that can respond within minutes rather than hours. The Southeast Asia thermal power market is therefore keeping its utility base, but its fastest expansion is now coming from industrial and digital loads that increasingly organize power supply around site-specific reliability needs.

Geography Analysis

Indonesia held 36.8% of the Southeast Asia thermal power market share in 2025, while Vietnam is projected to record the fastest growth at 7.9% CAGR through 2031. Indonesia remains the anchor market because its capacity decisions have the biggest effect on the regional average. PLN’s RUPTL 2025-2034 allocates 16.6 GW to new fossil fuel capacity, including 6.3 GW of coal and 10.3 GW of gas, within a broader 69.5 GW planned addition program. Captive coal growth around nickel-processing parks continues to expand thermal capacity outside the traditional grid-connected perimeter, which makes Indonesia’s actual thermal trajectory stronger than the utility-only pipeline suggests. Malaysia is shifting more decisively toward gas, but that transition still depends on LNG infrastructure expansion and on how effectively the country manages domestic gas supply constraints.

Thailand and Singapore faced some of the sharpest cost pressure from the 2026 LNG price shock because gas makes up a large share of their thermal systems, and that exposure brought energy security concerns back to the front of planning decisions. Vietnam is set to deliver the fastest expansion in the Southeast Asia thermal power market size at 7.9% CAGR through 2031, supported by fast electricity demand growth and a clear LNG build pipeline under the adjusted PDP VIII. Coal still produced 52.8% of Vietnam’s electricity output in the first quarter of 2026, but the Quang Trach power center alone is expected to add 4,400 MW when its coal and LNG units are all online. The Philippines presents a different risk profile, because its coal-heavy generation mix remains exposed to imported fuel dependence while Japanese-backed modernization efforts are testing ammonia co-firing and other decarbonization pathways.

Singapore occupies a distinct role as a regulatory and technology benchmark rather than a major growth market for capacity additions. The 600 MW hydrogen-capable CCGT planned at Pulau Seraya sets an efficiency and fuel-flexibility benchmark for newer regional gas projects, with initial capability to co-fire up to 50% hydrogen with natural gas. The rest of Southeast Asia, including Myanmar, Cambodia, Laos, and Brunei, retains a modest but still important thermal base made up mostly of small coal and diesel units. Cross-border hydropower flows from Laos and new ASEAN grid funding could gradually reduce the need for incremental thermal builds in parts of Thailand and Malaysia, but that effect will be slower than the near-term expansion now underway in Indonesia and Vietnam.

Competitive Landscape

The Southeast Asia thermal power market is moderately concentrated at the utility-ownership level, but it remains fragmented across EPC contracting, fuel supply, and equipment layers. PT PLN, EVN, and EGAT still control most utility-scale thermal generation in their home systems, and those positions continue to be protected by long-term power purchase structures and state planning mandates. This keeps national champions at the center of dispatch and procurement even as private capital becomes more active in selected LNG and captive projects. In advanced gas turbines, GE Vernova, Siemens Energy, and Mitsubishi Power dominate new orders and long-term service contracts for the largest combined-cycle developments. Long lead times and slot reservation agreements have become a real barrier for smaller OEMs in the Southeast Asia thermal power market, especially where efficiency requirements are rising and project schedules are tight.

The first open area is mid-scale combined heat and power for manufacturing clusters in Vietnam and Malaysia, where the economics are improving, but no single regional platform provider has emerged. The second is fast-response gas peakers in Vietnam and the Philippines, where utilities need flexible backup as solar additions increase. The third is coal-plant decarbonization services, including biomass co-firing, transition-credit structuring, and ammonia qualification for existing fleets. These niches matter because competition in the Southeast Asia thermal power market is shifting toward execution speed, technical performance, and lifecycle service capability rather than simple upfront equipment pricing.

Several recent strategic moves show how this competition is evolving. Mitsubishi Power’s reservation agreement with Malakoff for two M701JAC turbines in Malaysia showed that developers are locking in supply years before final EPC award to reduce delivery risk. erex’s April 2026 MOU with Vinacomin to commercialize biomass co-firing across 1,585 MW of Vietnamese coal capacity showed a service-led route into the installed fleet instead of competing only for new-build projects. GE Vernova’s selection for the planned Hai Phong LNG plant, together with its earlier deployment at Nhon Trach 3 and 4, shows how leading OEMs are combining project wins with long-term service positions across the Southeast Asia thermal power market.

Southeast Asia Thermal Power Industry Leaders

PT PLN (Persero)

Vietnam Electricity (EVN)

Electricity Generating Authority of Thailand (EGAT)

Malakoff Corporation Berhad

Tenaga Nasional Berhad

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: erex Co., Ltd. and Vinacomin Power Holdings signed an MOU to commercialise biomass co-firing at the 110 MW Na Duong and 115 MW Cao Ngan coal plants in Vietnam, targeting 20% to 30% co-firing ratios and 92,000 tonnes per year of carbon credits by fiscal year 2028. The agreement is structured under Japan’s Joint Crediting Mechanism.

- April 2026: An investment and business agreement was signed for the USD 2.18 billion Ca Na LNG-fired thermal power plant, a 1,500 MW CCGT in Khanh Hoa Province, Vietnam. The project was the first LNG power project selected via international competitive bidding under PDP VIII and targets commercial operation by 2030.

- April 2026: Vietnam’s Quang Trach 1 thermal power plant, a 1,400 MW ultra-supercritical coal project, achieved grid synchronization of Unit 1 and targeted commercial operation in May 2026. The EPC consortium includes Mitsubishi Corporation, Hyundai Engineering and Construction, and Construction Corporation No. 1, under a VND 30.23 trillion agreement, equivalent to USD 1.3 billion.

- March 2026: GE Vernova and VinEnergo Energy Joint Stock Company signed a technology selection agreement for Vietnam’s planned Hai Phong LNG facility, a 1,600 MW Phase I gas-fired project using GE Vernova 9HA.02 gas turbines and H78 generators. Commercial operation is targeted for the end of 2030.

Southeast Asia Thermal Power Market Report Scope

Thermal power generation is the process of generating electricity using direct heat from burning fuel or steam created by burning oil, natural gas, coal, and others to rotate generators and create electricity.

The Southeast Asia Thermal Power Market is segmented into fuel type, technology, combustion method, application, and geography. By fuel type, the market is segmented into coal-fired, gas-fired, and oil-fired power generation. By technology, the market is segmented into steam cycle, gas turbine/combined cycle (CC), and combined heat and power (CHP) systems. By combustion method, the market is segmented into pulverized fuel (PF), fluidized bed combustion (FBC), gasification, internal combustion engine (ICE), and turbine-based systems. By application, the market is segmented into utility-scale, captive, distributed, and peaker power generation. The report also covers the market size and forecasts for the Southeast Asia thermal power market in 6 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of volume (GW).

By Fuel Type

| Coal-Fired Power Plants |

| Natural Gas-Fired Power Plants |

| Oil-Fired Power Plants |

By Technology

| Steam Cycle-Based |

| Gas Turbine/Combined Cycle |

| Combined Heat and Power (CHP) |

By Combustion Method

| Pulverized Fuel (PF) Combustion |

| Fluidized Bed Combustion |

| Gasification |

| Internal Combustion Engines |

| Turbine-Based Combustion |

By Application

| Utility-Scale Thermal Plants |

| Industrial Captive Power Plants |

| Distributed Thermal Plants |

| Peaker Plants |

By Geography

| Vietnam |

| Indonesia |

| Philippines |

| Thailand |

| Malaysia |

| Singapore |

| Rest of Southeast Asia |

| By Fuel Type | Coal-Fired Power Plants |

| Natural Gas-Fired Power Plants | |

| Oil-Fired Power Plants | |

| By Technology | Steam Cycle-Based |

| Gas Turbine/Combined Cycle | |

| Combined Heat and Power (CHP) | |

| By Combustion Method | Pulverized Fuel (PF) Combustion |

| Fluidized Bed Combustion | |

| Gasification | |

| Internal Combustion Engines | |

| Turbine-Based Combustion | |

| By Application | Utility-Scale Thermal Plants |

| Industrial Captive Power Plants | |

| Distributed Thermal Plants | |

| Peaker Plants | |

| By Geography | Vietnam |

| Indonesia | |

| Philippines | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the projected size of Southeast Asia thermal power by 2031?

The Southeast Asia thermal power market is projected to reach 277.71 GW by 2031, rising from 251.56 GW in 2026 at a 1.66% CAGR.

Which fuel segment is growing fastest in Southeast Asia thermal power?

Natural gas-fired power plants are the fastest-growing fuel segment, with projected CAGR of 4.9% through 2031, supported by LNG-to-power projects in Vietnam, Malaysia, and the Philippines.

Why does Indonesia matter so much for regional thermal capacity?

Indonesia held 36.8% of installed regional capacity in 2025 and its RUPTL 2025-2034 still includes 16.6 GW of new fossil-fuel additions, making it the largest single influence on regional averages.

Why is Vietnam the main growth frontier through 2031?

Vietnam is forecast to grow at 7.9% CAGR through 2031, backed by fast power demand growth and an LNG pipeline that includes PDP VIII targets of 22,524 MW by 2030.

What is changing in application demand across the region?

Utility-scale plants still held 65.7% share in 2025, but industrial captive power plants are forecast to grow at 6.8% CAGR as nickel processing and data center loads expand.

Who leads equipment supply for large gas-fired projects in the region?

GE Vernova, Siemens Energy, and Mitsubishi Power lead advanced gas turbine supply for major CCGT projects, and their technology access and delivery slots are becoming key competitive barriers.

Page last updated on: