Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

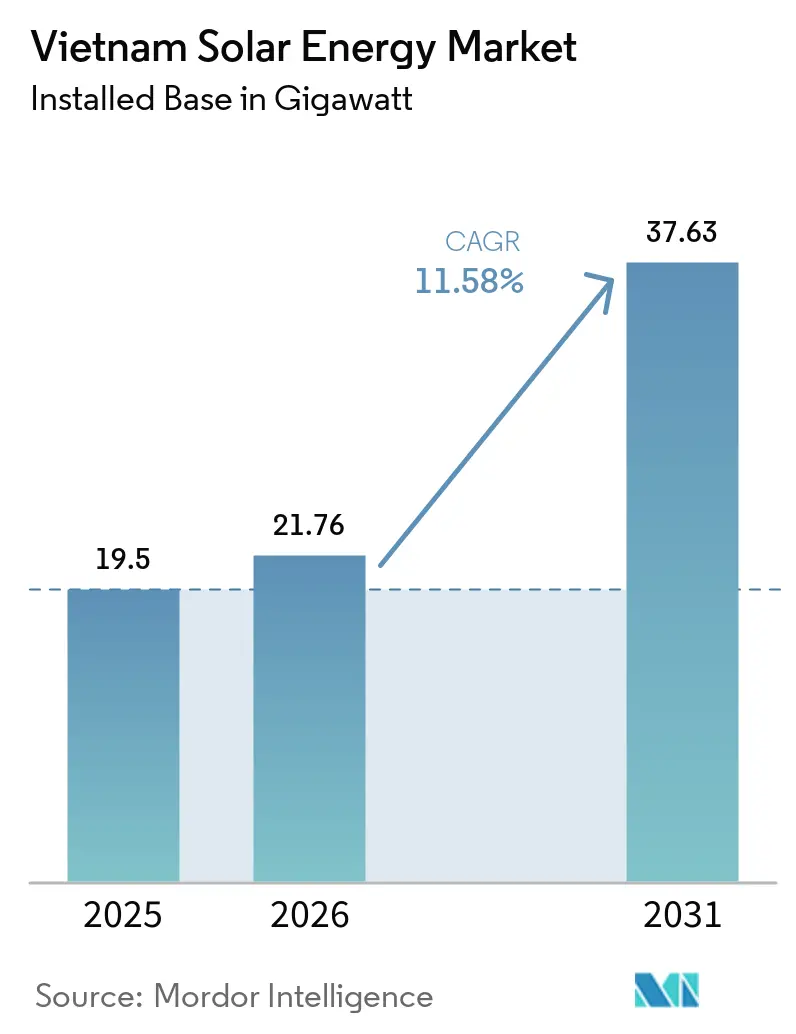

| Base Year Market Size (2025) | 19.5 gigawatt |

| Market Volume (2026) | 21.76 gigawatt |

| Market Volume (2031) | 37.63 gigawatt |

| Growth Rate (2026 - 2031) | 11.58% CAGR |

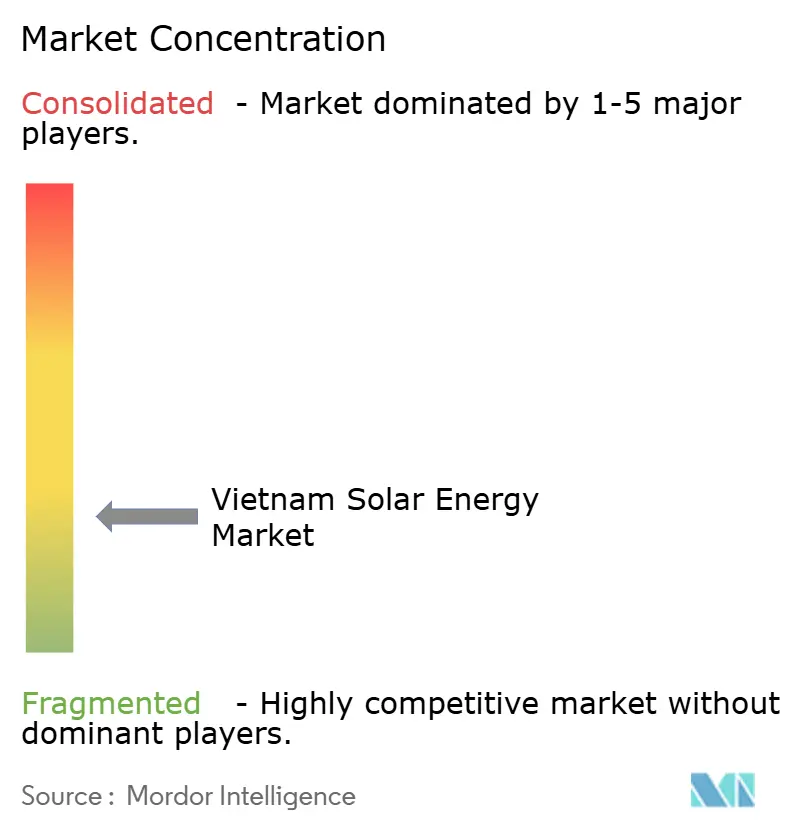

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Solar Energy Market Analysis by Mordor Intelligence

The Vietnam Solar Energy Market size was valued at 19.5 gigawatt in 2025 and estimated to grow from 21.76 gigawatt in 2026 to reach 37.63 gigawatt by 2031, at a CAGR of 11.58% during the forecast period (2026-2031).

The upward curve reflects policy recalibration following the 2020 feed-in tariff (FIT) sunset, the expansion of Power Development Plan VIII (PDP8), and ongoing module-cost deflation. Competitive land auctions for floating arrays, the rollout of direct power-purchase agreements (DPPAs), and data-center procurement for 24×7 clean power underpin demand momentum, while transmission build-outs and FIT uncertainty temper near-term commissioning risk. Module capex fell 36% between 2020 and 2024, compressing utility-scale levelized costs below USD 0.04 per kWh in high-insolation provinces, and concessional climate-finance pipelines are amplifying the private sector's appetite. Despite grid congestion in the south and execution bottlenecks for large projects, hybrid solar-plus-storage mandates and corporate offtake commitments position the Vietnam solar energy market for double-digit growth through 2030.

Key Report Takeaways

- By technology, solar photovoltaic captured 100.00% of the Vietnam solar energy market share in 2025 and is forecast to grow at an 11.58% CAGR through 2031.

- By grid type, on-grid systems commanded 99.88% of installed capacity in 2025, while the off-grid segment is projected to expand at a 15.12% CAGR to 2031.

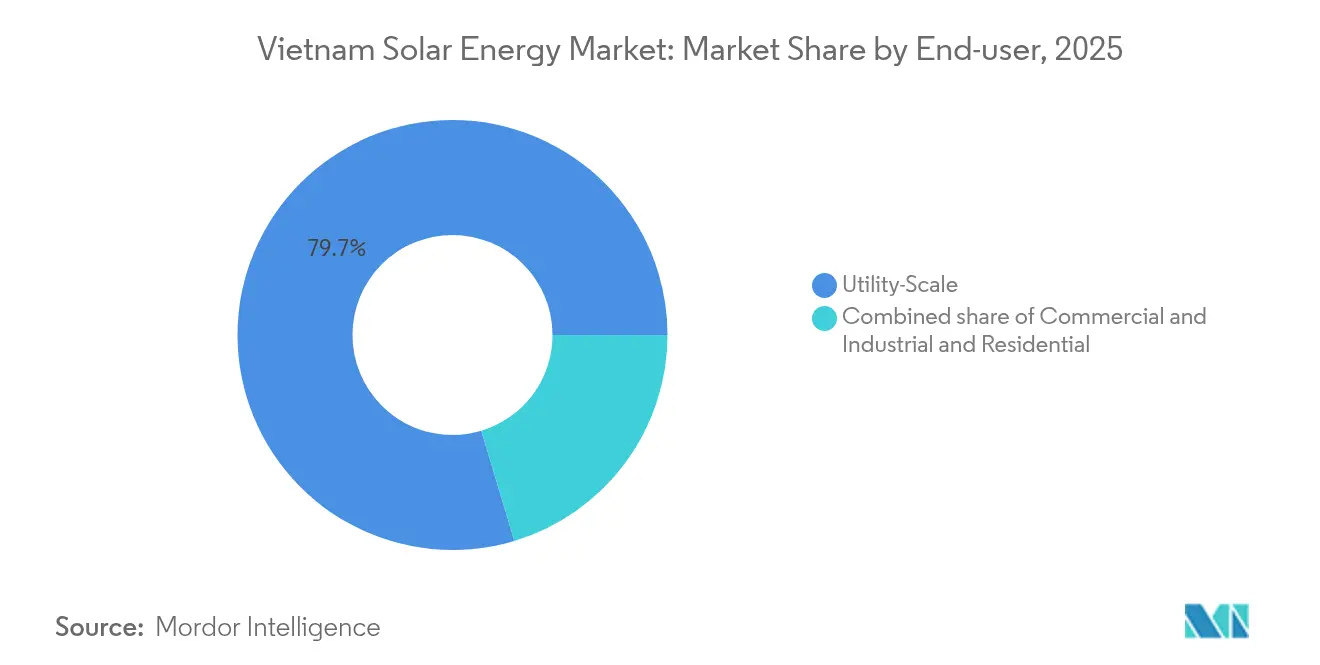

- By end-user, utility-scale projects accounted for 79.65% of the Vietnam solar energy market size in 2025; commercial and industrial installations are expected to advance at a 14.26% CAGR over 2026-2031 under the DPPA framework.

- Geographically, Ninh Thuan, Binh Thuan, and Tay Ninh provinces accounted for roughly 64.50% of the 2025 capacity; the northern provinces are the fastest-growing cluster, with a forecast 12.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidized feed-in tariffs & rooftop net-metering schemes | +1.80% | National, with higher uptake in Ho Chi Minh City, Hanoi, Da Nang | Short term (≤ 2 years) |

| Power Development Plan VIII upsizing solar target to 34 GW by 2030 | +3.20% | National, priority in Ninh Thuan, Binh Thuan, Tay Ninh | Long term (≥ 4 years) |

| Corporate PPAs & green-loan pipelines accelerating C&I demand | +2.40% | Industrial zones in southern provinces | Medium term (2-4 years) |

| Declining capex of Tier-1 PV modules (-36% 2020-24) | +2.10% | Global supply chain, nationwide deployment | Short term (≤ 2 years) |

| Surge in data-center build-outs with 24×7 renewables procurement | +1.60% | Ho Chi Minh City, Hanoi metro | Medium term (2-4 years) |

| Provincial land-use auctions favoring floating PV | +1.30% | Mekong Delta, Central Highlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Power Development Plan VIII Upsizing Solar Target to 34 GW by 2030

Decision 768, issued in April 2025, reset the PDP8, raising the 2030 solar ceiling to 46.5-73.4 GW and mandating battery energy storage equal to at least 10% of the nameplate capacity with a 2-hour duration.(1)Ministry of Industry and Trade, “Decision 768/QD-TTg on PDP8 Revision,” moit.gov.vn Developers now finance lithium-ion arrays costing USD 200-250 per kWh, adding USD 40-50 million to a 100 MW plant, yet unlocking evening-peak tariffs 30-40% above midday rates. Ninh Thuan and Binh Thuan have streamlined permits for projects exceeding the storage threshold, whereas northern provinces lag due to weaker grid infrastructure. Electricity Vietnam estimates that USD 15 billion in new transmission is required to absorb PDP8 volumes, but the annual spend averages only USD 1.2 billion, implying that deployment will likely track the plan’s lower bound. The policy nonetheless anchors long-term visibility for the Vietnam solar energy market, guiding provincial land auctions and private-sector financing structures.

Corporate PPAs & Green-Loan Pipelines Accelerating C&I Demand

Decree 80/2024 unlocked DPPAs for consumers topping 200,000 kWh per month, and within six months, 24 projects totaling 1.77 GW entered the approval queue. Textile, electronics, and food processors are chasing tariff hedges and ESG credentials, favoring virtual PPAs that avoid private-line build costs of USD 0.5-2 million per kilometer. The World Bank committed USD 500 million in 2024 for renewable integration, while the Asian Development Bank disbursed USD 1.7 billion during 2023-24 for rooftop solar and microgrids.(2)Asian Development Bank, “Climate Finance in Southeast Asia 2024,” adb.org Hyperscalers such as Google and Microsoft expect to contract close to 300 MW of dedicated solar by 2027 to meet 24×7 carbon-free goals. The expansion of solar energy is also supporting demand from the vietnam data center power sector through clean and reliable power integration. Although the 200,000 kWh threshold limits SME participation, the decree accelerates the commercial pivot within the Vietnam solar energy market.

Surge in Data-Center Build-Outs with 24×7 Renewables Procurement

Vietnam’s data-center pipeline is on track to add 500-700 MW of IT load by 2028, requiring a firm renewable supply to satisfy corporate net-zero pledges. Developers are structuring 15-20 year load-following PPAs pairing solar with wind and 4-6 hour batteries to achieve 99.99% uptime. Google’s planned Ho Chi Minh City facility is negotiating a 150 MW virtual PPA blending 60% solar, 30% wind, and 10% biomass at a USD 0.055 per kWh strike price, 15% below the prevailing industrial tariff. AWS aims for an 85% renewable fraction at its Hanoi site through a 50 MW rooftop-plus-ground-mount array and a 20 MW battery. These bespoke offtake structures reinforce the premium C&I sub-segment and diversify revenue streams within the Vietnam solar energy market.

Declining Capex of Tier-1 PV Modules (-36% 2020-24)

Tier-1 polysilicon module prices declined to USD 0.10 per watt in 2024 from USD 0.16 in 2020, driven by the adoption of TOPCon technology and wafer-thickness reductions. Capital expenditure for utility-scale projects in southern Vietnam now ranges from USD 0.55 to USD 0.65 per watt, pushing levelized costs below USD 0.04 per kWh in Ninh Thuan and Binh Thuan. Bifacial modules deliver 10-15% yield gains, as evidenced by Trung Nam Group’s 450 MW plant achieving an 82% performance ratio in 2024. Rooftop installations experience payback times of 5-6 years despite the FIT lapse, catalyzing self-consumption under Decree 135/2024. However, reliance on imports exposes the Vietnam solar energy market to trade-policy shocks that could reverse the cost curve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion & curtailment in Southern Vietnam | -2.30% | Ninh Thuan, Binh Thuan, Tay Ninh | Short term (≤ 2 years) |

| Uncertain FIT step-down & price-cap regime | -1.80% | National, new-build economics | Medium term (2-4 years) |

| Shortage of local Tier-1 EPC capacity post-2026 | -1.20% | Nationwide, acute in north-central provinces | Long term (≥ 4 years) |

| Investor skepticism on roof structural integrity | -0.90% | Ho Chi Minh City, Hanoi, Da Nang | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion & Curtailment in Southern Vietnam

Solar output in Ninh Thuan and Binh Thuan already exceeds local demand, and the 500 kV backbone operates near thermal limits, forcing Electricity Vietnam to curtail up to 60% of excess generation in 2020.(3)Electricity Vietnam, “Grid Curtailment Report 2024,” evn.com.vn Curtailment averages 15-25% during dry-season peaks, undermining project returns. The planned HVDC reinforcement, worth USD 15 billion, will not be fully online until 2027, leaving new capacity exposed to dispatch risk. Lenders now insist on curtailment insurance, adding 50-75 basis-point spreads to debt. Mandatory 10% battery storage helps time-shift energy but cannot offset multi-day oversupply events, keeping this restraint a prominent drag on the Vietnam solar energy market.

Uncertain FIT Step-Down & Price-Cap Regime

The December 2020 FIT expiry left 85 projects, totaling several gigawatts, in limbo, with developers awaiting auction guidelines that have been repeatedly delayed, most recently until October 2024. Legacy FIT levels are facing a possible retroactive review, which could jeopardize USD 13 billion in investor value. Proposed ceiling prices of VND 1,500-1,700 per kWh (USD 0.061-0.069) are insufficient for lower-insulation northern sites, skewing new capacity toward the south. Electricity Vietnam has withheld USD 110 million in payments over commissioning disputes, denting confidence. Until auctions are operational, the Vietnam solar energy market relies on corporate PPAs and self-consumption niches, constraining utility-scale pipelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Dominance Precludes CSP Entry

Solar photovoltaic systems controlled the entire 19.5 GW base in 2025, and continued capex declines support an 11.58% CAGR to 2031. Concentrated solar power remains commercially unviable in Vietnam because the country lacks the direct-normal irradiance required for thermodynamic efficiency. Utility-scale ground mounts in Ninh Thuan utilize single-axis trackers to achieve 12-18% yield gains, whereas urban rooftops rely on module-level power electronics to minimize shading losses. Floating PV on hydropower reservoirs broadens the siting palette and leverages existing transmission. The rapid uptake of TOPCon and heterojunction modules, already accounting for 35% of 2024 shipments, reduces balance-of-system costs. CSP's higher capital intensity of USD 3,000-4,000 per kW, compared to USD 550-650 for PV, together with humidity-driven optical losses, negates its prospects through 2031, cementing photovoltaic primacy in the Vietnam solar energy market.

Innovation accelerates as developers deploy bifacial modules and DC-coupled batteries via hybrid inverters that yield round-trip efficiencies of 92-94%. String-inverter architectures are replacing central units in plants exceeding 50 MW, enhancing fault tolerance and facilitating incremental capacity additions. Battery mandates reshape procurement: 45 MW/90 MWh stacks paired with 450 MW solar farms now clear investment hurdles under peak-tariff spreads, signaling a hybridized roadmap for Vietnam's solar energy market.

By Grid Type: Off-Grid Acceleration from Low Base

In 2025, bolstered by a 99.5% electrification rate and favorable legacy FIT economics, Vietnam's on-grid systems achieved an impressive 99.88% capacity delivery. These installations interconnect at 22 kV or 110 kV nodes and comply with QCVN 52:2016 voltage and frequency ride-through rules. Off-grid capacity, although small, is projected to rise at a 15.12% CAGR as mountain provinces favor microgrids over grid extensions costing more than USD 50,000 per kilometer. Telecom towers and aquaculture ponds replace diesel gensets with solar-battery kits, slashing operating costs. Decree 135/2024 strengthens self-consumption and indirectly boosts behind-the-meter autonomy for industrial users seeking outage resilience. Falling battery prices, currently USD 120-140 per kWh in 2024 and trending toward USD 80-100 by 2028, will render off-grid solar cheaper than new grid miles beyond 15 km, thereby widening the distributed niche within the Vietnam solar energy market.

By End-User: C&I Gains on Utility-Scale Incumbents

Utility-scale projects retained 79.65% of the installed volume in 2025, following the FIT rush; however, commercial and industrial systems are expected to book a faster 14.26% CAGR through 2031. Rooftop arrays between 500 kW and 10 MW dominate commercial and industrial (C&I) uptake, securing 70-90% self-consumption and selling no more than 20% surplus to the grid, as per Decree 135/2024. Industrial retail tariffs rose 8% in March 2024 and are expected to face annual hikes of 5-7%, sharpening the economic case for on-site generation. Data centers represent the premium sub-segment, contracting bespoke solar-plus-storage bundles at blended tariffs roughly 10-15% above standard commercial and industrial (C&I) rates due to reliability premiums. Residential solar, constrained by upfront costs and a 20% net metering cap, remains below 1% of total capacity. Execution risk around roof loading persists for pre-2010 buildings, as reinforcement can add 15-25% to capital cost, although third-party ownership models ease balance-sheet pressures. Collectively, these trends diversify demand channels and fortify the Vietnam solar energy market against policy volatility.

Geography Analysis

The southern provinces of Ninh Thuan, Binh Thuan, and Tay Ninh supplied roughly 64.50% of the total capacity in 2025, owing to 5.5-6.0 kWh/m²/day insolation and ample land parcels. Yet transmission congestion curtails 15-25% of midday output, eroding returns. The planned 2,000 MW HVDC link, scheduled for 2027, will partially unlock stranded generation; however, until then, curtailment insurance burdens financing costs. The Mekong Delta is emerging as a floating-PV cluster; An Giang, Dong Thap, and Kien Giang are auctioning reservoir surfaces, enabling 10-12 GW of potential and bypassing land-use conflicts. Here, water-based cooling enhances performance ratios and reduces evaporation, providing agricultural co-benefits that expedite provincial approvals.

Northern provinces, including Hanoi and Hai Phong, trail in absolute capacity yet are poised for a 12.98% CAGR through 2031, driven by hyperscaler data-center procurement and electronics manufacturing clusters adopting DPPAs. Lower insolation and higher land premiums elevate levelized costs to USD 0.055-0.065 per kWh, roughly 30-40% above southern benchmarks, making premium PPA pricing critical. The Central Highlands pursues hybrid solar-hydro schemes co-located with reservoirs, allowing pumped-storage synergies and evening-peak arbitrage. Provincial permitting varies: Ninh Thuan fast-tracks projects exceeding the PDP8 storage quota, whereas northern jurisdictions impose lengthy environmental reviews, which can stretch timelines by 6-12 months. Such divergences influence the developer's risk calculus and shape the spatial evolution of the Vietnamese solar energy market.

Competitive Landscape

The Vietnam solar energy market is moderately fragmented: the top five developers, Trung Nam Group, BIM Group, T&T Group, VU Phong Energy, and Xuan Cau Holdings, control around 40% of utility-scale capacity. International module majors Longi, Trina Solar, JA Solar, and Canadian Solar supply over 85% of panels, while domestic manufacturing hovers near 1 GW per year via Boviet Solar, exposing supply chains to import-policy shifts. Competitive strategies converge on vertical integration, international-local partnerships, and DPPA-driven corporate contracting. Floating PV, solar-plus-storage for data centers, and off-grid microgrids represent white-space opportunities.

Berkeley Energy C&I Solutions and SkyX Solar are tilting the C&I segment toward third-party ownership, absorbing capital expenditures (capex) and leveraging tax shields. Technology differentiation intensifies as bifacial TOPCon modules, single-axis trackers, and DC-coupled batteries deliver performance ratios above 82% and push levelized costs below USD 0.04 per kWh in prime sites. Yet a looming shortage of Tier-1 EPC bandwidth post-2026 threatens schedule slippage as pipeline backlogs clear once FIT clarity returns. Developers signing fixed-price module deals now risk margin compression if labor and steel inflate during execution, underscoring the execution-risk premium inside the Vietnam solar energy market.(5)VnExpress, “Vietnam Solar Developers Ranking 2024,” vnexpress.net

Vietnam Solar Energy Industry Leaders

Vietnam Sunergy Joint Stock Company

Sharp Energy Solutions Corporation

Berkeley Energy Commercial & Industrial Solutions

Tata Power Solar Systems Ltd.

Song Giang Solar Power Joint Stock Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Government of Vietnam issued Decision 768, revising Power Development Plan VIII to increase the solar capacity target to 46,459-73,416 MW by 2030.

- October 2024: The Ministry of Industry and Trade issued Decree 135/2024 to promote rooftop solar self-consumption, limiting excess electricity sales to the grid to 20% and setting a target of 2,600 MW for rooftop solar by 2030.

- March 2024: Trung Nam Group has commissioned a 450 MW utility-scale solar project in Ninh Thuan province. The project utilizes bifacial TOPCon modules and single-axis tracking systems, achieving a performance ratio of 82%, which is approximately 4 percentage points higher than monofacial PERC counterparts.

- February 2024: The Asian Development Bank allocated USD 1.7 billion in climate finance to Vietnam for the period 2023-2024. This includes concessional loans for rooftop solar systems with payback periods of less than seven years and off-grid microgrids in ethnic-minority communities.

Vietnam Solar Energy Market Report Scope

Solar energy is the heat and radiant light from the Sun that can be harnessed through technologies such as solar power (used to generate electricity) and solar thermal energy (used for applications like water heating).

The Vietnam Solar Energy Market is segmented by technology, grid type, and end-user. By technology, the market is segmented into solar Photovoltaic, concentrated solar power. By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial, Industrial, and residential. The report also covers the market size and forecasts for Vietnam.

For each segment, market sizing and forecasts have been conducted based on installed capacity (GW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

What is the installed solar capacity in Vietnam as of 2026?

The Vietnam solar energy market size was 21.76 GW of cumulative capacity in 2026.

How fast is Vietnam’s solar sector expected to grow?

Capacity is forecast to reach 37.63 GW by 2031, corresponding to an 11.58% CAGR during 2026-2031.

Which technology dominates Vietnamese projects?

Solar photovoltaic systems hold 100.00% of capacity, while concentrated solar power remains absent due to unsuitable irradiance.

How do direct power-purchase agreements support development?

Decree 80/2024 allows large industrial users to contract renewables directly, driving a 1.77 GW project pipeline within six months of launch.

What are the key geographic hubs for solar deployment?

Ninh Thuan, Binh Thuan, and Tay Ninh provinces account for about 64.50% of existing capacity, though northern provinces are the fastest-growing cluster.

How will mandatory battery storage affect new projects?

PDP8 requires storage equal to 10% of solar nameplate capacity with 2-hour duration, raising capex but enabling higher-value evening dispatch.

Page last updated on: