Vietnam Oral Anti-Diabetic Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

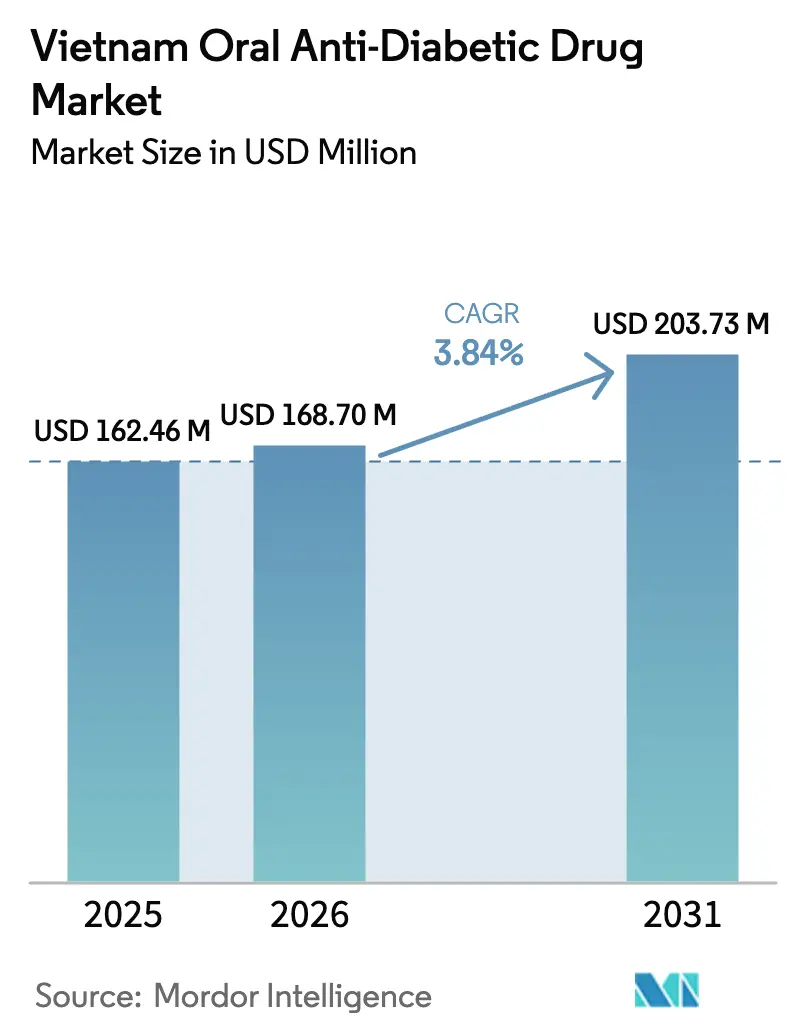

| Base Year Market Size (2025) | USD 162.46 Million |

| Market Size (2026) | USD 168.7 Million |

| Market Size (2031) | USD 203.73 Million |

| Growth Rate (2026 - 2031) | 3.84% CAGR |

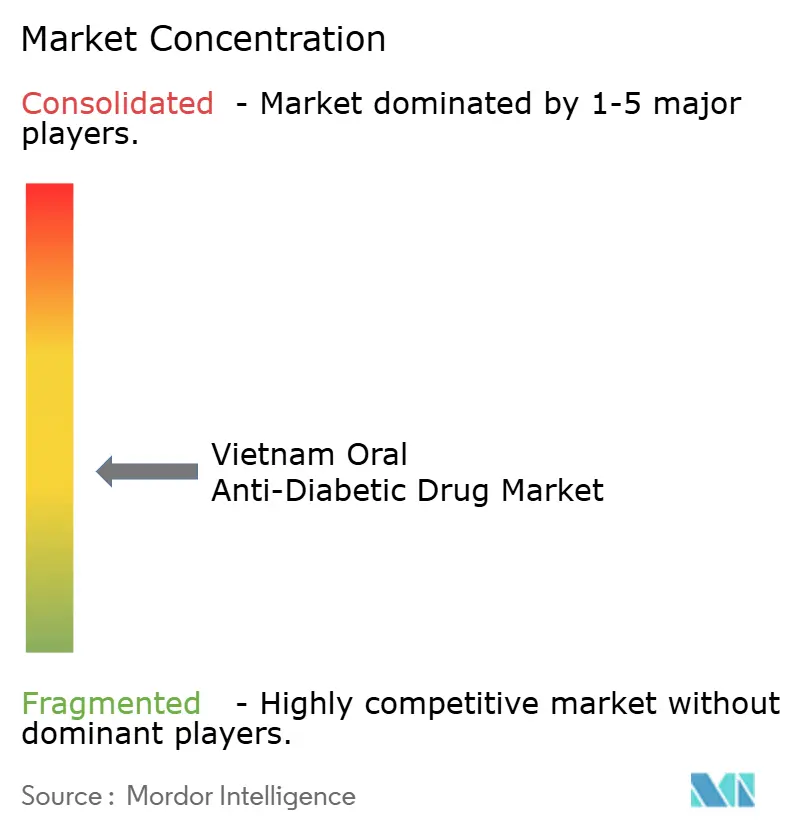

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Oral Anti-Diabetic Drug Market Analysis by Mordor Intelligence

The Vietnam oral anti-diabetic drug market size in 2026 is estimated at USD 168.7 million, growing from 2025 value of USD 162.46 million with 2031 projections showing USD 203.73 million, growing at 3.84% CAGR over 2026-2031. Demand is sustained by a 6% diabetes prevalence among 97.3 million inhabitants, growing diagnosis rates, and expanding reimbursement coverage [1]Tran Bao Vuong, "High prevalence of prediabetes and type 2 diabetes, and identification of associated factors, in high-risk adults in Vietnam: A cross-sectional study," Diabetes Epidemiology and Management, sciencedirect.com. The moderate growth reflects a healthcare system shifting toward chronic-disease management, an urban middle class willing to pay for newer therapies, and policy goals to raise domestic pharmaceutical output to 80% by 2030. Multinational corporations continue to introduce innovative products, yet local manufacturers gain ground through cost-efficient production and regulatory incentives. Digital health adoption and pharmacy-chain expansion reshape distribution, while the safety profiles of older drug classes encourage uptake of newer molecules. Regulatory price ceilings and quality-control concerns temper revenue growth but also create white-space opportunities for high-quality generics.

Key Report Takeaways

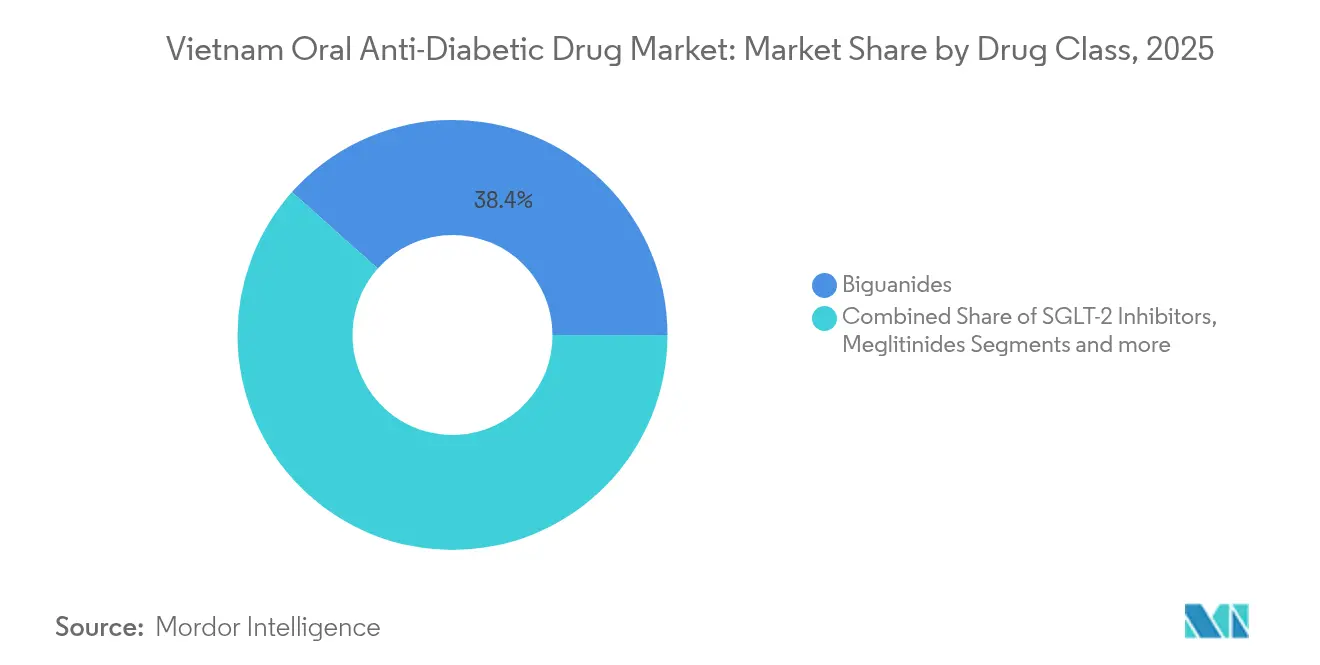

- By drug class, biguanides led with 38.42% of Vietnam oral anti-diabetic drug market share in 2025; SGLT-2 inhibitors are projected to grow at a 4.47% CAGR through 2031.

- By age group, adults held 68.31% of the Vietnam oral anti-diabetic drug market in 2025, while the geriatric segment is expected to expand at a 4.54% CAGR to 2031.

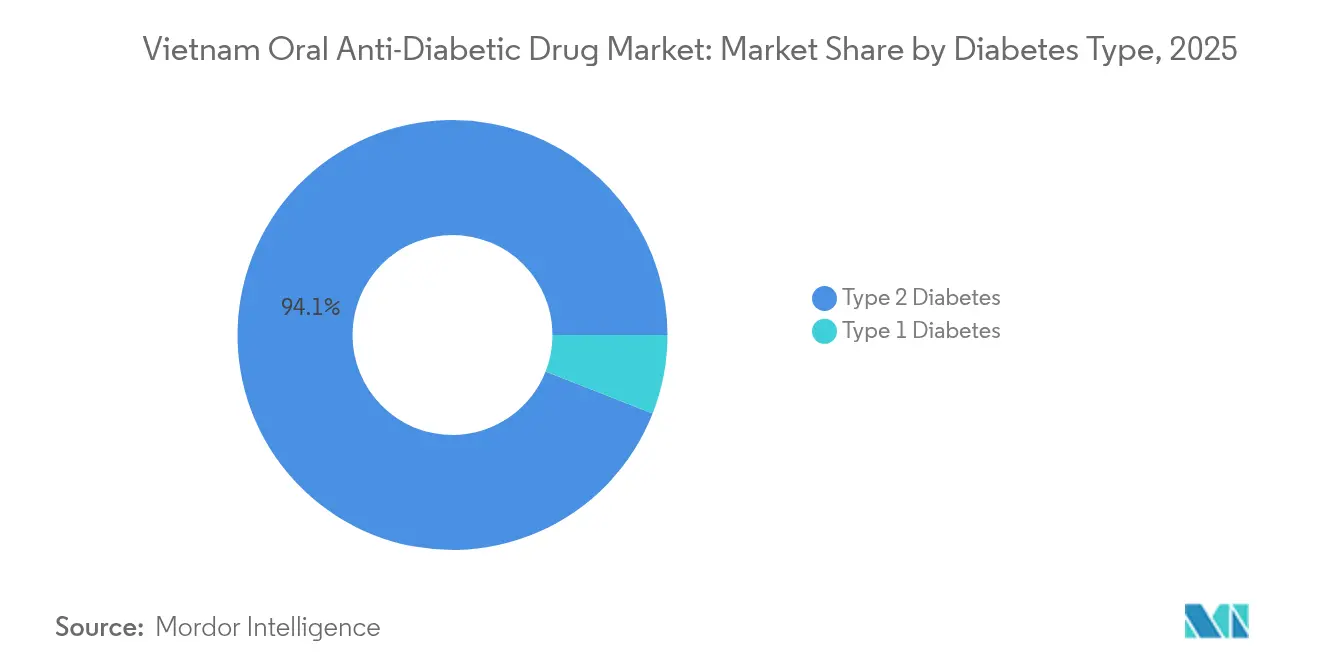

- By diabetes type, Type 2 accounted for 94.05% of the Vietnam oral anti-diabetic drug market size in 2025 and shows the highest 4.49% CAGR outlook.

- By distribution channel, hospital pharmacies captured 69.58% revenue share in 2025; online pharmacies record the fastest 4.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Understanding the full system requires moving beyond Vietnam boundaries into a wider international view. Mordor Intelligence captures the global oral anti-diabetic drugs market scope in its worldwide coverage.

Vietnam Oral Anti-Diabetic Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Type-2 Diabetes | +1.2% | National, concentrated in urban areas | Long term (≥ 4 years) |

| Expansion Of National Health-Insurance Reimbursement | +0.8% | National, with enhanced coverage in rural areas | Medium term (2-4 years) |

| Growing Urban Middle-Class Healthcare Spending | +0.6% | Ho Chi Minh City, Hanoi, Da Nang | Medium term (2-4 years) |

| Launch Of Novel Fixed-Dose Combination OADs | +0.4% | National, early adoption in tier-1 cities | Short term (≤ 2 years) |

| Employer-Sponsored Diabetes Screening Programs | +0.3% | Urban centers, industrial zones | Short term (≤ 2 years) |

| Rice-Fortification Policy Sustaining Glycaemic Load | +0.2% | Rural areas, food-insecure regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Type-2 Diabetes

Vietnam’s diabetes burden continues to intensify as urbanization and dietary change drive metabolic syndrome. Projections indicate a 21.1% relative rise in prevalence by 2045, making Vietnam one of the fastest-growing diabetes markets among middle-income countries [2]Centers for Disease Control and Prevention, “Global Diabetes Projections,” cdc.gov . Gestational diabetes affects 22.8% of pregnancies, creating future demand for chronic therapy. Processed-food consumption raises average glycemic load in urban diets, especially among the expanding middle class. Earlier onset of disease lengthens lifetime drug use, and rice-fortification programs aimed at malnutrition may unintentionally sustain high glycemic intake. Together these factors underpin long-run demand in the Vietnam oral anti-diabetic drug market.

Expansion of National Health-Insurance Reimbursement

The amended Health Insurance Law effective July 2025 increases coverage to 100% for vulnerable groups and removes referral barriers, enabling direct specialist access. With 90% insurance penetration but 43% out-of-pocket spending, reimbursement expansion meaningfully lowers financial hurdles for modern therapies. Ho Chi Minh City’s insurance authority is reviewing high-priced products with duplicative active ingredients, signaling tougher cost controls. Nevertheless, clearer reimbursement rules reduce uncertainty for investors and favor uptake of generics and value-added combinations across the Vietnam oral anti-diabetic drug market.

Growing Urban Middle-Class Healthcare Spending

Per-capita pharmaceutical outlay is projected to jump from USD 60.80 in 2021 to USD 88.30 by 2026. Premium traditional-medicine sales at Traphaco climbed 49% in 2024, illustrating willingness to pay for wellness products. Retail chains integrate electronic prescriptions and appointment booking; An Khang’s service links 70+ hospitals, improving chronic-care convenience. The VNeID national app further embeds pharmacy services into daily life, supporting adherence. Rising discretionary income and digital convenience together fuel incremental volumes in the Vietnam oral anti-diabetic drug market.

Launch of Novel Fixed-Dose Combination OADs

Early combination therapy outperforms stepwise titration, driving demand for fixed-dose products. Vietnam approved 692 domestically produced drugs in 2025, including sitagliptin-metformin blends. Simplified registration under the 2025 Pharmacy Law cuts time-to-market, and Imexpharm plans 16 new high-tech launches targeting complex formulations. These advances position domestic firms to co-lead innovation in the Vietnam oral anti-diabetic drug market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety & Side-Effect Profile of Certain OAD Classes | -0.6% | National, higher impact in rural areas | Medium term (2-4 years) |

| Competitive Uptake Of GLP-1 Ras & Insulin | -0.4% | Urban centers, private healthcare facilities | Short term (≤ 2 years) |

| MOH Price-Control Ceilings on Reimbursed Drugs | -0.5% | National, stronger impact on public hospitals | Long term (≥ 4 years) |

| Rising Use of Traditional Herbal Alternatives | -0.3% | Rural areas, traditional medicine regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Safety & Side-Effect Profile of Certain OAD Classes

Polypharmacy affects 7.8% of older diabetes patients, heightening adverse-event risk. Fatal lactic acidosis from herbal products adulterated with undisclosed biguanides exposed regulatory gaps and raised public concern. Sulfonylurea-linked hypoglycemia remains a barrier in settings lacking immediate medical support. Resistance patterns in diabetic-foot infections underscore broader tolerability issues [3]Tan To Anh Le, "Treatment outcomes, antibiotic selection, and related factors in the management of diabetic foot infections in Vietnam," Endocrine and Metabolic Science, sciencedirect.com. Consequently, prescribers shift toward newer drugs with safer profiles, restraining expansion of legacy segments in the Vietnam oral anti-diabetic drug market.

Competitive Uptake of GLP-1 RAs & Insulin

Novo Nordisk reported 52% global GLP-1 sales growth, while Eli Lilly prepares Mounjaro rollouts across key emerging markets. Superior efficacy and cardiometabolic benefits make injectable treatments increasingly attractive for urban patients. As Vietnamese insurance gradually includes advanced therapies, substitution threatens traditional OAD volumes, especially among treatment-naïve cohorts in premium facilities. The Vietnam oral anti-diabetic drug market therefore faces share erosion where affordability barriers recede.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biguanides Retain the Largest Share Amid SGLT-2 Momentum

Biguanides held 38.42% of Vietnam oral anti-diabetic drug market share in 2025 due to metformin’s entrenched first-line status. SGLT-2 inhibitors, supported by renal-cardio benefits, are forecast to post a 4.47% CAGR, making them the fastest riser. Sulfonylureas remain relevant for cost-sensitive patients, though hypoglycemia risks curb growth. DPP-4 inhibitors gain urban popularity for once-daily dosing. AstraZeneca’s partnership with FPT Long Châu to broaden dapagliflozin counseling shows multinationals leveraging domestic chains. The segment’s diversification demonstrates evolving therapeutic preferences within the Vietnam oral anti-diabetic drug market.

Early 2025 FDA approval of dapagliflozin for chronic kidney disease enlarges its addressable base, while domestic approvals of sitagliptin-metformin blends highlight growing local capability. Thiazolidinediones lose ground amid safety scrutiny, whereas meglitinides preserve a niche in flexible meal-time dosing. The “others” category, including next-generation combinations, signals further innovation potential as regulatory pathways streamline.

By Age Group: Geriatric Growth Outpaces Adult Dominance

Adults commanded 68.31% revenue in 2025, yet the geriatric cohort posts the highest 4.54% CAGR, echoing Vietnam’s transition toward an aging society. Polypharmacy and comorbidities require simplified regimens, spurring demand for fixed-dose combinations. Community screening programs by Merck Healthcare Vietnam and Long Châu underscore attention to older populations.

Herbal co-usage by 40.8% of patients complicates pharmacovigilance, reinforcing the need for education and monitoring. National EMR deployment by September 2025 will improve oversight and adherence, supporting growth in the Vietnam oral anti-diabetic drug market size for geriatric care.

By Diabetes Type: Type 2 Remains the Core Driver

Type 2 diabetes contributed 94.05% of the Vietnam oral anti-diabetic drug market in 2025 and is set for a 4.49% CAGR. Cost-effectiveness studies favor gliclazide-based control, yet comparative research shows faster glycemic improvement with sitagliptin add-on therapy.

High undiagnosed prevalence (18.3% of high-risk adults) leaves room for volume expansion as screening intensifies. Government targets for 80% of diagnosed patients achieving HbA1c < 7.0% add policy impetus. Cardiovascular and renal comorbidity prevalence further boosts demand for multi-benefit OADs across the Vietnam oral anti-diabetic drug market size.

By Distribution Channel: Digital Platforms Accelerate Online Uptake

Hospital pharmacies retained 69.58% share in 2025, reflecting specialist-led prescriptions. Online pharmacies deliver a 4.87% CAGR, propelled by e-commerce reforms permitting OTC sales and growing consumer confidence. Studies indicate 77.5% intent to continue online purchases.

Integration of prescriptions within the VNeID app creates a unified health ecosystem, fostering adherence. Retail chains combine offline convenience with digital services, enabling omnichannel coverage across the Vietnam oral anti-diabetic drug market.

Geography Analysis

Regional disparities shape demand across the Vietnam oral anti-diabetic drug market. Ho Chi Minh City and Hanoi lead consumption owing to concentrated tertiary hospitals, specialist endocrinologists, and higher disposable income. The Mekong Delta’s aging agricultural populace presents an emerging growth pocket as rural clinics upgrade under universal coverage programs. Northern provinces benefit from proximity to new production hubs, including a bio-pharma park in Thai Binh Province that reduces logistics costs.

Electronic medical records nationwide by September 2025 will harmonize care standards, enabling cross-regional prescription tracking. Local health-insurance authorities exert price oversight: Ho Chi Minh City’s scrutiny of high-cost drugs may pivot prescribers toward generics.

Rural regions show higher reliance on herbal medicine, competing with OAD uptake but also highlighting opportunities for education campaigns. Coastal provinces face transport challenges that favor tele-pharmacy solutions, aligning with the online growth trend. Collectively, these dynamics create a patchwork of opportunities and constraints across the Vietnam oral anti-diabetic drug market.

Mordor Intelligence examines the oral anti-diabetic drugs market across diverse other regional markets as well, including Europe, Asia, and Latin America, while also offering granular country-level perspectives for Philippines, Thailand, Italy, Mexico, India, and New Zealand and more.

Competitive Landscape

The Vietnam oral anti-diabetic drug market displays moderate fragmentation. Novo Nordisk dominates globally but competes locally with DHG Pharma, Traphaco, Imexpharm, and other domestic producers. Multinationals capitalize on R&D strength, introducing advanced classes like SGLT-2 inhibitors and GLP-1 analogs. Local companies leverage lower costs, government incentives, and EU-GMP plants to supply high-quality generics.

Partnerships typify recent strategy: Vinapharm’s plan to double its stake in Sanofi Vietnam illustrates deeper foreign-local collaboration. AstraZeneca’s alliance with FPT Long Châu uses pharmacist training to expand dapagliflozin reach. Digital health investments, automated factories, and data analytics differentiate competitors, while rural penetration remains an untapped frontier.

Technology adoption accelerates: AI-enabled demand forecasting and blockchain supply-chain tracking reduce counterfeits, addressing quality-control restraints. Domestic firms invest in complex formulations, such as Imexpharm’s EU-GMP antibiotics pipeline, signaling ambition beyond basic generics. The result is a dynamic, innovation-oriented Vietnam oral anti-diabetic drug market.

Vietnam Oral Anti-Diabetic Drug Industry Leaders

-

Astrazeneca

-

Astellas

-

Eli Lilly

-

Sanofi

-

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Circular No. 12/2025/TT-BYT streamlined marketing authorization for drugs and medicinal materials, shortening approval timelines

- April 2025: Ministry of Health approved nationwide electronic medical records rollout by September 2025, standardizing diabetes monitoring

- April 2025: FPT Long Châu and AstraZeneca launched a partnership to promote dapagliflozin education and a “3-in-1” cardio-renal-metabolic treatment model.

Vietnam Oral Anti-Diabetic Drug Market Report Scope

Orally administered antihyperglycemic drugs reduce blood glucose levels. They are often used in type 2 diabetes care. Vietnam's oral anti-diabetic drug market is segmented into drugs. The report offers the market size in value terms in USD and Volume in terms of Unit for all the abovementioned segments.

| Biguanides |

| Sulfonylureas |

| Meglitinides |

| Thiazolidinediones |

| Alpha-Glucosidase Inhibitors |

| DPP-4 Inhibitors |

| SGLT-2 Inhibitors |

| Others |

| Adults |

| Pediatric |

| Geriatric |

| Type 1 Diabetes |

| Type 2 Diabetes |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| By Drug Class | Biguanides |

| Sulfonylureas | |

| Meglitinides | |

| Thiazolidinediones | |

| Alpha-Glucosidase Inhibitors | |

| DPP-4 Inhibitors | |

| SGLT-2 Inhibitors | |

| Others | |

| By Age Group | Adults |

| Pediatric | |

| Geriatric | |

| By Diabetes Type | Type 1 Diabetes |

| Type 2 Diabetes | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies |

Key Questions Answered in the Report

What is the current size of the Vietnam oral anti-diabetic drug market?

The market stands at USD 168.7 million in 2026 and is projected to reach USD 203.73 million by 2031.

Which drug class leads the Vietnam oral anti-diabetic drug market?

Biguanides dominate with 38.42% share in 2025, reflecting metformin’s first-line status.

How fast are SGLT-2 inhibitors growing in Vietnam?

SGLT-2 inhibitors are forecast to expand at a 4.47% CAGR through 2031, the fastest among oral classes.

What distribution channel is growing the quickest?

Online pharmacies deliver the highest CAGR at 4.87%, driven by e-commerce adoption and supportive regulation.

Why is the geriatric segment important for future growth?

Vietnam’s aging population pushes the geriatric segment to a 4.54% CAGR, creating demand for simplified, safer therapies.

How will new insurance rules affect the market?

Expanded reimbursement from July 2025 lowers patient costs and is likely to boost prescription volumes, particularly for newer generics and value-added combinations.

Page last updated on: