Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

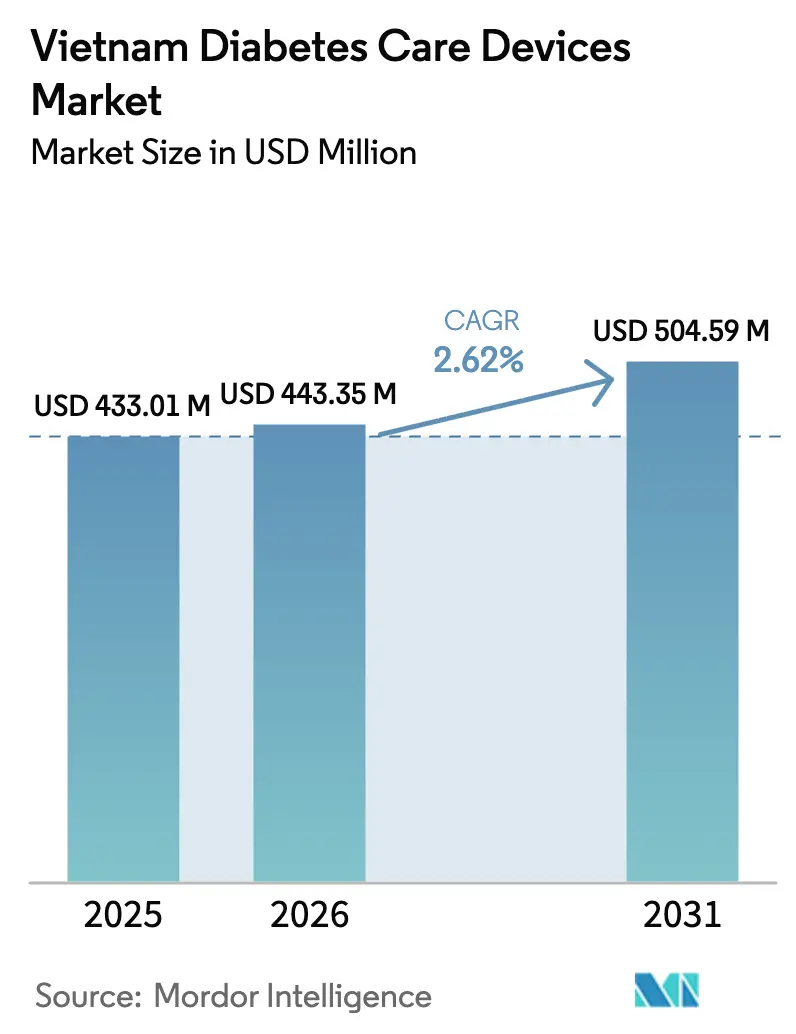

| Base Year Market Size (2025) | USD 433.01 Million |

| Market Size (2026) | USD 443.35 Million |

| Market Size (2031) | USD 504.59 Million |

| Growth Rate (2026 - 2031) | 2.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Diabetes Care Devices Market Analysis by Mordor Intelligence

The Vietnam Diabetes Care Devices Market size is expected to grow from USD 433.01 million in 2025 to USD 443.35 million in 2026 and is forecast to reach USD 504.59 million by 2031 at 2.62% CAGR over 2026-2031.

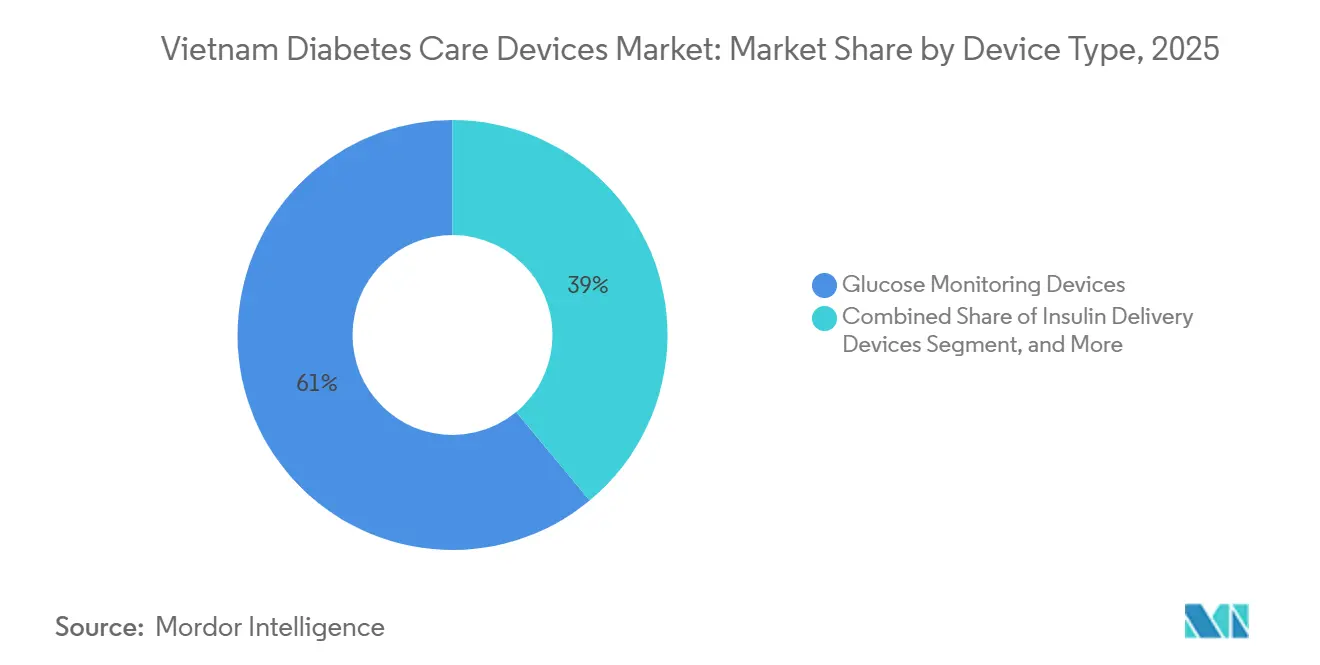

The rising incidence of both Type 1 and Type 2 diabetes, expanding insurance coverage, and a steady shift toward self-care are sustaining demand, even as affordability constraints temper headline growth. Glucose monitoring devices led the Vietnam diabetes devices market with a 61.01% market share in 2025, but insulin delivery devices are advancing faster as pediatric Type 1 cases climb and reimbursement pathways for pens and syringes improve. The Vietnam diabetes devices market also benefits from e-pharmacy deregulation, telemedicine roll-outs, and targeted domestic manufacturing incentives that aim to reduce the country’s >90% import dependence, yet price-sensitive users still ration test-strip consumption, slowing unit growth. Competitive intensity remains moderate: multinationals dominate premium technology, while local firms are moving into mid-tier continuous glucose monitors, creating a two-speed trajectory in the Vietnam diabetes devices market.

Key Report Takeaways

- By device category, glucose monitoring commanded 61.01% of the Vietnam diabetes devices market share in 2025, while insulin delivery is projected to register the fastest 3.35% CAGR through 2031.

- By diabetes type, Type 2 accounted for 84.56% of the Vietnam diabetes devices market size in 2025, whereas Type 1 devices are set to expand at a 4.56% CAGR to 2031.

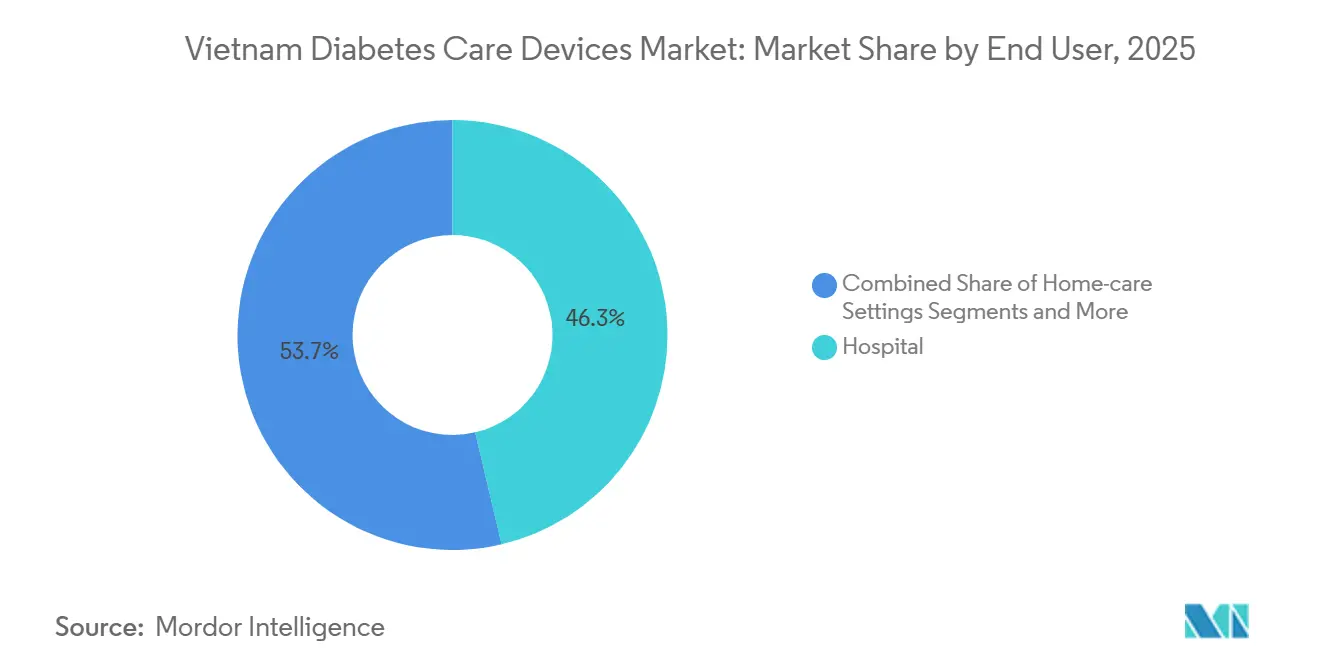

- By end user, hospital accounted for 46.34% of the Vietnam diabetes devices market in 2025, and home-care settings are forecast to grow at a 3.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Diabetes Care Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes Prevalence & Urban Lifestyles | +0.9% | National, concentrated in Hanoi, HCMC, Da Nang | Medium term (2-4 years) |

| Increasing Healthcare Expenditure & UHC Expansion | +0.7% | National, with urban-rural coverage gaps narrowing | Long term (≥ 4 years) |

| Growing Adoption of Self-Monitoring & Wearables | +0.5% | Urban centers (Hanoi, HCMC), spill-over to secondary cities | Short term (≤ 2 years) |

| Domestic Manufacturing Initiatives Cut Import Costs | +0.3% | National, policy-driven with Hanoi and HCMC manufacturing hubs | Long term (≥ 4 years) |

| Tele-Medicine & E-Pharmacy Policies Widen Rural Access | +0.4% | Rural and remote provinces, ethnic minority areas | Medium term (2-4 years) |

| Medical Tourism Boosts Demand for Advanced Tech | +0.2% | HCMC, Hanoi, Da Nang medical tourism hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence & Urban Lifestyles

Vietnam’s adult diabetes prevalence rose to 3.6% in 2025, translating to 2.5 million diagnosed cases and another 37.8% undiagnosed. Urban residents aged 15–59 face 1.86 times higher odds of diabetes than rural peers, showing how dietary westernization and sedentary work patterns accelerate risk.[1]PubMed, “Urban–Rural Diabetes Risk in Vietnam,” pubmed.ncbi.nlm.nih.gov Northern Vietnam recorded 0.77 Type 1 cases per 100,000 children in 2025, and more than 57% of presentations were in ketoacidosis, proving that monitoring gaps remain wide. For the Vietnam diabetes devices market, this epidemiological burden splits demand between affordable glucometers for mass Type 2 management and premium pumps plus continuous glucose monitors for pediatric Type 1 care. Device makers that align their portfolios with these divergent needs stand to capture the next wave of growth in Vietnam's diabetes device market.

Increasing Healthcare Expenditure & UHC Expansion

National health spending climbed from USD 24.7 billion in 2024 toward a projected USD 57.1 billion by 2029, reflecting an 18.3% CAGR that outpaces GDP growth.[2]International Trade Administration, “Vietnam Pharmaceutical Industry Updates,” trade.gov Insurance now covers 91–94% of citizens, yet out-of-pocket payments still make up roughly 40% of total outlays, capping uptake of advanced devices. Health Insurance Law 51/2024 and Circular 22/2024 streamlined reimbursement for Class C and D devices, improving the processing of claims for glucometers and insulin pens. Decree 188/2025 mandates electronic claims from 2026 and prioritizes local procurement, signaling political will to widen access while containing costs. Collectively, these reforms enlarge the addressable Vietnam diabetes devices market but favor products priced for mass insurance schedules over top-tier imported tech.

Growing Adoption of Self-Monitoring & Wearables

A 2024 study linked home glucometer ownership to a 2.59 odds ratio for better self-care practices. Abbott’s FreeStyle Libre, launched in 2021, and FPT Medicare’s locally distributed 3P CGM, launched in November 2024, demonstrate the expansion of continuous monitoring options. Yet, with average annual diabetes spending at USD 418, CGM adoption remains clustered among affluent urbanites, leaving vast untapped potential once subsidy levels rise. Integration of telehealth and pharmacist counseling through the Abbott–FPT Long Chau alliance (October 2025) highlights how omnichannel care models are reshaping the Vietnam diabetes devices market toward connected ecosystems.

Domestic Manufacturing Initiatives Cut Import Costs

Vietnam targets 80% self-sufficiency in medicines by 2030 and seeks similar momentum in devices. Decree 07/2023 simplified Class B registrations, and multinationals such as Omron filed local conformity requests in June 2025 to qualify for procurement preferences. While no domestic firm yet produces insulin or advanced sensors, assembly of glucometers and pen components is scaling, and Decree 188/2025 grants tenders extra points for locally made products. Over time, this policy mix can compress landed costs and increase price-elasticity of demand in the Vietnamese diabetes devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Cost & Limited Reimbursement | -0.6% | National, acute in rural and low-income urban areas | Medium term (2-4 years) |

| Regulatory Delays for Imported Devices | -0.3% | National, affecting all importers and distributors | Short term (≤ 2 years) |

| Shortage of Trained Educators Outside Cities | -0.2% | Rural provinces, ethnic minority regions | Long term (≥ 4 years) |

| Data-Security Concerns for CGM Adoption | -0.1% | Urban early adopters, privacy-conscious segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device Cost & Limited Reimbursement

Median glucometer prices are USD 35.18, and strips cost USD 0.27–0.56 each, equal to several days’ wages for low earners. Pumps cost USD 7,000–9,000, far exceeding covered benefits, so only wealthier families adopt them. Although Circular 22/2024 reimburses selected insulin pens and syringes, CGMs remain mostly uncovered, constraining volume in the Vietnam diabetes devices market.

Regulatory Delays for Imported Devices

Despite harmonization efforts, approvals for Class C and D products still stretch 24–36 months, deterring the rapid entry of hybrid closed-loop systems.[3]Luat Vietnam, “Circular 22/2024 on Medical Device Reimbursements,” luatvietnam.vn Novo Nordisk’s 2024 upgrade to full FIE status trimmed internal lead time, yet multinationals still face multilayer distributor rules that prolong time-to-market. These lags slow refresh cycles and limit the pace at which new technology lifts the Vietnam diabetes devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Category: Insulin Delivery Momentum Accelerates

Glucose monitoring devices accounted for 61.01% of the Vietnam diabetes devices market share in 2025, but insulin delivery is forecast to grow at a 3.35% CAGR, outpacing overall growth. Rising pediatric Type 1 diagnoses and streamlined reimbursement for pens under Circular 22/2024 underpin this shift. The Vietnam diabetes devices market for insulin pens is growing as analog formulations gain favor over human insulin, while pumps remain a niche due to high out-of-pocket costs. Continuous glucose monitors add value to pen-based regimens; however, strip-dependent glucometers remain dominant among Type 2 patients who test less frequently to manage costs, underscoring that unit volumes hinge on consumable affordability within the Vietnam diabetes devices market size calculus.

Insulin pens provide easier dosing and fewer training barriers than vials, aligning with clinician guidelines issued after the 2024 Novo Nordisk-MOH memorandum. Domestic distributors are exploring contract assembly to tap into Decree 188/2025 procurement incentives, suggesting that pen prices could soften in the near term. CGM manufacturers court the same premium cohort, and the Abbott-Medtronic interoperability initiative foreshadows hybrid closed-loop systems entering Vietnam, albeit for the top decile of earners. For mass segments, cost-effective meters bundled with discounted strips will continue anchoring the Vietnam diabetes devices market share landscape.

By Diabetes Type: Pediatric Type 1 Drives Premium Uptake

Type 2 diabetes generated 84.56% of 2025 demand, yet devices targeting Type 1 are on track for a 4.56% CAGR, nearly double the aggregate rate. Hospitals now report a tenfold increase in pediatric caseloads compared with a decade ago, making basal-bolus pens and CGMs essential. This accelerates revenue concentration in higher-value modalities even though Type 1 accounts for fewer absolute users in the Vietnam diabetes devices market.

Novo Nordisk-backed clinical protocols standardize pump candidacy, and insurers are reviewing pilot reimbursements for sensor-augmented therapy, signaling incremental traction. Type 2 patients remain strip-centric, yet as obesity rates rise, more adults shift to basal insulin, lifting pen volumes. Undiagnosed and poorly controlled Type 2 cases now 37.8% and 71.1% respectively represent latent demand that Vietnam diabetes devices market players can unlock through affordable starter kits and tele-counseling.

By End-user: Hospital Dominance Yielding to Home-care Growth

Hospitals accounted for 46.34% of device value in 2024, underscoring Vietnam’s traditional hospital-centric care model. Inpatient wards rely on ward meters and have begun rotating CGM sensors during acute admissions to prevent hypoglycaemia. Yet the proportion is slowly eroding as national insurance incentivises primary health stations to manage stable cases nearer to where people live.

Commune health stations in Ho Chi Minh City demonstrated that 80% of mild diabetes cases can be safely followed without referral, releasing beds for complex tertiary care. Home use thus registers the fastest growth at 3.89% CAGR, driven by teleconsult platforms that integrate prescription renewal, remote glucometer uploads, and same-day courier supply of consumables. The Vietnam diabetes care devices market size generated by home-care channels could overtake small-town hospital revenue by 2030 if current momentum holds. Ambulatory surgical centres, still a minor slice, gain relevance as new day-procedure hubs for insulin pump implantation open in private hospital networks, illustrating the expanding continuum of device-supported care.

Geography Analysis

Urban hubs dominate device spend. Ho Chi Minh City posts the highest patient pool, with 18.3% diabetes prevalence among screened high-risk adults, and private centers like Cardiff Diabetes Center stock hybrid closed-loop systems. Hanoi follows, buoyed by the National Children’s Hospital’s 200-plus annual Type 1 caseload, spurring adoption of pumps and CGMs. Da Nang and tourist corridors leverage medical tourism, attracting 300,000 foreign visitors annually, to justify premium inventory and English-language support, reinforcing brand presence for multinationals in the Vietnam diabetes devices market.

Rural provinces lag because only one-quarter of commune health stations handle non-communicable disease prevention, and travel costs deter regular follow-up. Telemedicine statutes and the national electronic prescription system aim to narrow gaps by 2027, yet uneven broadband coverage and low digital literacy are slowing the rollout. The Asian Development Bank’s plan to equip 685 health stations with point-of-care devices is behind schedule, revealing procurement bottlenecks that are delaying rural penetration of Vietnam's diabetes devices market.

Ethnic minority regions face compounded barriers: physician density is lowest, insurance co-pay exemptions often fail in practice, and language differences impede education. Technology solutions like smartphone-linked glucometers could leapfrog infrastructure, but high unit prices and limited training resources currently restrain uptake. Companies that localize apps and subsidize devices via micro-insurance may unlock incremental growth pockets within the Vietnam diabetes devices market over the next five years.

Competitive Landscape

Three global insulin giants, Novo Nordisk, Eli Lilly, and Sanofi, control a significant portion of low-income-country insulin volume, yet in Vietnam, because biosimilars and local distributors discount human insulin. Abbott has led continuous monitoring since its 2021 FreeStyle Libre debut and has reinforced its footprint through the October 2025 FPT Long Chau partnership, which bundles telehealth and training. Novo Nordisk’s July 2024 upgrade to full FIE status grants direct import rights, reducing channel layers and enabling faster rollout of analog pens. Roche and Medtronic rely on capacity-building programs with the Ministry of Health, positioning themselves as technology partners rather than mere suppliers, which enhances stickiness in the Vietnam diabetes devices market.

Domestic challengers emerge. FPT Medicare’s 3P CGM, launched in 2024, undercuts imported sensors and uses local 4G modules for real-time data, a template that other Vietnamese conglomerates may follow. Sinocare Vietnam distributes dual glucose-uric acid meters, broadening its value-tier offerings, while NIPRO Vietnam maintains its Japanese-quality positioning. Procurement rules that favor locally assembled units could swing tenders toward these regional firms, squeezing multinational margins within segments of the Vietnam diabetes devices market.

Strategic moves illustrate differentiation. Abbott joined forces with Medtronic in August 2024 to integrate FreeStyle Libre sensors with automated insulin delivery algorithms, protecting the premium corner. Novo Nordisk co-developed national Type 1 guidelines to embed pen and analog use into standard protocols. Omron’s local manufacturing facilities aim to achieve cost advantages in blood-pressure and potentially glucose devices. As policy nudges amplify local sourcing, hybrid models of multinational IP plus Vietnamese final assembly are likely to define the next competitive phase of the Vietnam diabetes devices market.

Vietnam Diabetes Care Devices Industry Leaders

Medtronic

Abbott Diabetes Care

Dexcom Inc.

Novo Nordisk A/S

Roche Diabetes Care

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Novo Nordisk Vietnam Ltd. shipped its first products as a foreign-invested enterprise, enabling wider distribution of innovative insulin delivery systems

- March 2024: The Ministry of Health extended existing import licences for medical devices until June 2025 under Decree No. 04/2025/NĐ-CP, temporarily lowering administrative barriers for new entrants

Vietnam Diabetes Care Devices Market Report Scope

Diabetes is a medical condition that arises when the level of glucose, also known as blood sugar, in your bloodstream becomes excessively high. Glucose serves as the primary source of energy for the patient's body. While patient's bodies can produce glucose, it is also obtained from the food they consume. Insulin, a hormone produced by the pancreas, facilitates the entry of glucose into your cells, where it is utilized as a source of energy. To manage or monitor patients use diabetes devices. Vietnam Diabetes Care Devices Market is segmented into devices and Monitoring Devices. The report offers the value (in USD) and volume (in Units) for the above segments.

By Device Category

| Glucose Monitoring Devices | Self-Monitoring Blood Glucose (SMBG) Devices | Glucometers |

| Test Strips | ||

| Lancets | ||

| Continuous Glucose Monitoring (CGM) Devices | Sensors | |

| Durables (Receivers & Transmitters) | ||

| Insulin Delivery Devices | Insulin Pens | |

| Insulin Pumps | ||

| Insulin Syringes | ||

| Jet Injectors | ||

| Other Diabetes-Care Devices | ||

By Diabetes Type

| Type 1 Diabetes |

| Type 2 Diabetes |

| Gestational & Others |

By End User

| Hospital |

| Specialty Clinics |

| Home Care Settings |

| Other End Users |

| By Device Category | Glucose Monitoring Devices | Self-Monitoring Blood Glucose (SMBG) Devices | Glucometers |

| Test Strips | |||

| Lancets | |||

| Continuous Glucose Monitoring (CGM) Devices | Sensors | ||

| Durables (Receivers & Transmitters) | |||

| Insulin Delivery Devices | Insulin Pens | ||

| Insulin Pumps | |||

| Insulin Syringes | |||

| Jet Injectors | |||

| Other Diabetes-Care Devices | |||

| By Diabetes Type | Type 1 Diabetes | ||

| Type 2 Diabetes | |||

| Gestational & Others | |||

| By End User | Hospital | ||

| Specialty Clinics | |||

| Home Care Settings | |||

| Other End Users | |||

Key Questions Answered in the Report

How fast is the Vietnam diabetes devices market expected to grow to 2031?

It is projected to rise from USD 0.44 billion in 2026 to USD 0.50 billion by 2031, registering a 2.62% CAGR.

Which product category is expanding the quickest?

Insulin delivery devices are forecast to outpace overall growth at a 3.35% CAGR through 2031 as Type 1 incidence rises.

What share do glucose monitoring devices hold?

They accounted for 61.01% of 2025 revenue, making them the largest segment in the Vietnam diabetes devices market.

What policy changes most affect reimbursement?

Circular 22/2024 and Health Insurance Law 51/2024 broaden coverage for Class C and D devices and remote services, easing patient cost burden.

Page last updated on: