Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

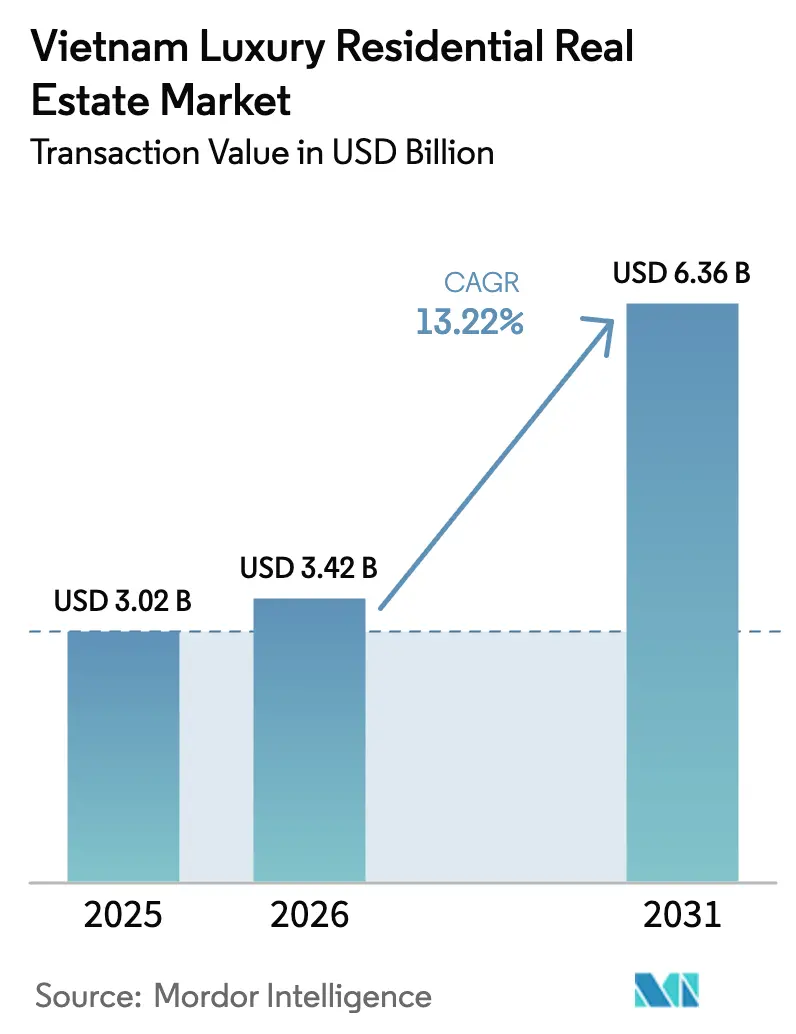

| Base Year Market Size (2025) | USD 3.02 Billion |

| Market Size (2026) | USD 3.42 Billion |

| Market Size (2031) | USD 6.36 Billion |

| Growth Rate (2026 - 2031) | 13.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Vietnam Luxury Residential Real Estate Market size was valued at USD 3.02 billion in 2025 and estimated to grow from USD 3.42 billion in 2026 to reach USD 6.36 billion by 2031, at a CAGR of 13.22% during the forecast period (2026-2031).

Growth is underpinned by a 98% surge in Vietnam’s millionaire population over the past decade, the economy’s 7.09% expansion in 2024, and an 8% GDP growth outlook for 2025[1]Henley & Partners, “Asia Pacific Wealth Report 2025,” henleyglobal.com. Vietnam luxury residential market capitalizes on Ho Chi Minh City’s wealth concentration, supportive regulatory reforms, and record infrastructure spending that tops USD 10 billion. Apartments and condominiums still dominate but villas are accelerating, while a nascent rental play signals rising yield-driven strategies. Regulatory clarity through the Land Law 2024 and digital-asset legalization from 2026 further widen capital inflows, reinforcing Vietnam luxury residential market resilience.

Key Report Takeaways

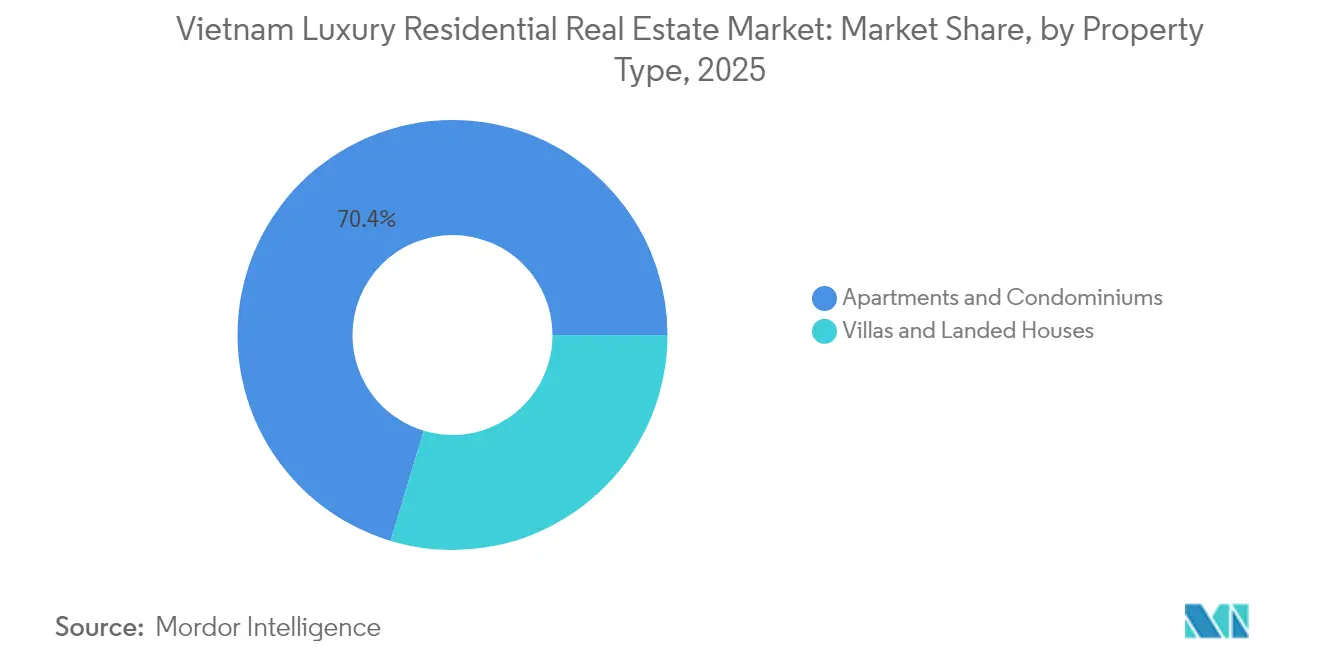

- By property type, apartments held 70.35% of Vietnam luxury residential market share in 2025, while villas and landed houses are set to grow at a 13.73% CAGR through 2031.

- By business model, the sales segment accounted for 84.35% of Vietnam luxury residential market share in 2025; the rental segment records the highest projected CAGR at 14.62% over 2026-2031.

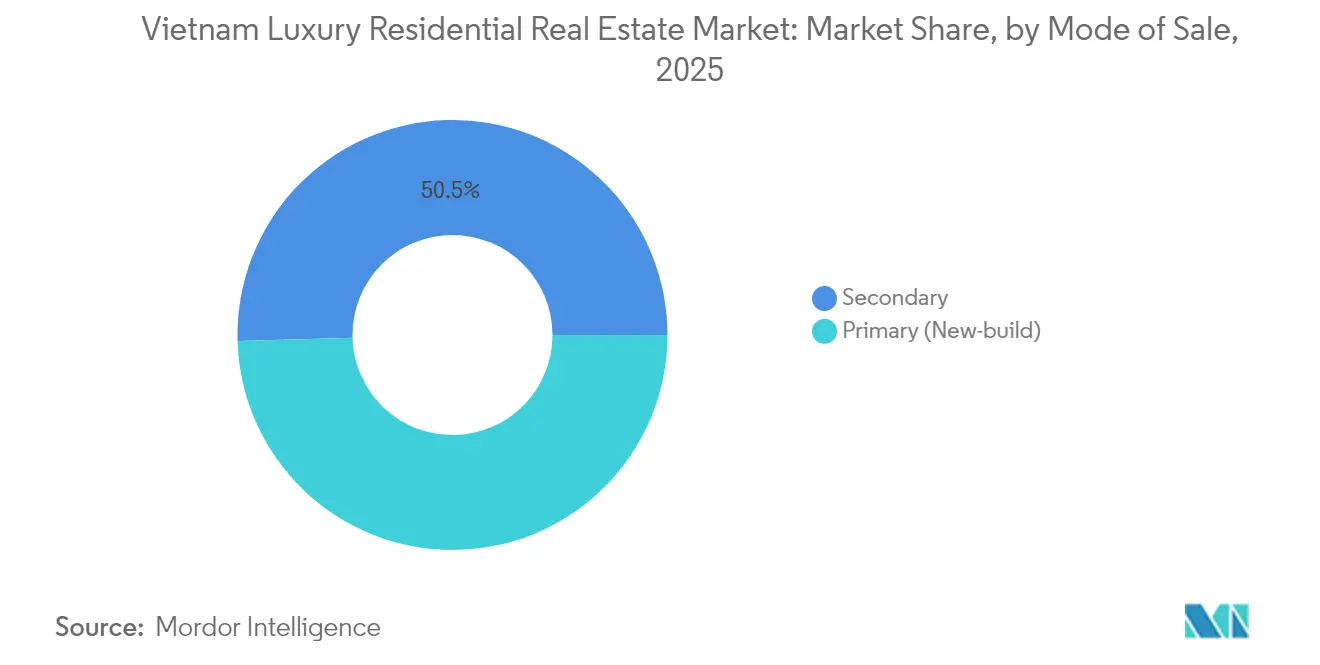

- By mode of sale, the secondary segment retained 50.45% of Vietnam luxury residential market share in 2025, yet the primary market is forecast to expand at a 14.02% CAGR to 2031.

- By city, Ho Chi Minh City led with 37.65% of Vietnam luxury residential market share in 2025, while Da Nang is projected to register a 15.02% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging affluent population & inter-generational wealth transfer | +2.1% | HCMC, Hanoi | Medium term (2-4 years) |

| Elite immigration demand & relaxed visa rules | +1.8% | HCMC, Hanoi, Da Nang | Short term (≤ 2 years) |

| Rapid urbanisation of tier-2 coastal cities | +2.3% | Central coast | Long term (≥ 4 years) |

| Tight land-use quotas in CBD districts | +1.9% | HCMC, Hanoi | Short term (≤ 2 years) |

| Green-building certification adoption | +1.2% | Major cities | Medium term (2-4 years) |

| Boom in tech-sector and crypto millionaires | +2.4% | Key tech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging affluent population drives inter-generational wealth transfer

Vietnam’s 16.1 million seniors in 2025 will exceed 20 million by 2030 as prosperity spreads. Asset transfers from first-generation entrepreneurs to younger heirs fuel continuous upgrading toward multi-generational, amenity-rich homes that blend security with lifestyle. Demand for healthcare-integrated compounds rises, creating fresh opportunities for senior-living focused estates[2]VietnamPlus, “Vietnam’s Elderly Population Tops 16 Million,” vietnamplus.vn.

Elite immigration demand & relaxed long-term visa policies for foreign investors

New 10-year investment visas shorten on-boarding time for foreign millionaires, particularly from East Asia and Europe. Flexible residency drives immediate absorption of serviced penthouses and branded coastal villas, cementing Vietnam luxury residential market as a regional safe-haven.

Rapid urbanisation of tier-2 coastal cities boosts resort-luxury projects

Da Nang and Nha Trang anchor mixed-use resort schemes as airport and expressway upgrades expand catchments. Search inquiries for Da Nang luxury apartments jumped 30% in 2024, while condotel sales rose 45%, underscoring lifestyle-led migration toward secondary hubs.

Tight land-use quotas in CBD districts push vertical luxury towers

Cap limits in HCMC District 1-3 and Hanoi’s Ba Dinh district intensify vertical land economics. Record land auctions above USD 40,000/m² support ultra-luxury towers exceeding 80 stories, embedding concierge retail, private clubs and sky parks to justify premiums in constrained cores.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding foreign-buyer taxes & ownership caps | −1.6% | National | Medium term (2-4 years) |

| Land & construction cost inflation | −2.1% | Major cities | Short term (≤ 2 years) |

| Stricter anti-money-laundering scrutiny | −1.3% | Gateway cities | Medium term (2-4 years) |

| Climate-risk-driven insurance premium surge | −0.9% | Coastal zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding foreign-buyer taxes & ownership ratio caps

Though foreign appetite remains strong, quota ceilings of 30% in condominium blocks and 250 landed homes per ward slow absorption once limits are reached. Proposed surcharge revisions could erode net returns and funnel demand toward quota-available districts.

Land & construction cost inflation pressures pricing

Steel, cement and imported fittings still price 18-22% above pre-pandemic levels. Resulting input spikes lift average HCMC luxury apartment sales to VND 120 million/m² (USD 4,800 per square meter), compelling developers into higher positioning and squeezing attainable demand[3]Vietnam Ministry of Construction, “Decision 409/QĐ-BXD,” thuvienphapluat.vn .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Apartment core with villa upshift

Apartments represent 70.35% of Vietnam luxury residential market in 2025, anchored in HCMC and Hanoi CBD stock scarcity. Prime high-rise units trade above USD 14,000/m² and achieve 75% capital appreciation across five years as transit and amenity clustering magnify liquidity. Luxury villas, though smaller in absolute count, record 13.73% CAGR to 2031, lifted by privacy preferences among tech millionaires and returning diaspora. Waterfront villa estates outside HCMC realise 10-35% premiums over in-city counterparts and deliver sturdy holiday rental income streams.

The apartment subsector benefits from developer finance plans, smart home platforms and international hotel branding, sustaining rapid sell-through even at record prices. Conversely, villa supply grows along ring roads and coastal corridors where larger land parcels allow low-density layouts, golf frontage and private berths. Vietnam luxury residential market size for villas is forecast to rise faster than urban towers, yet absolute dominance remains with apartments through 2031.

By Business Model: Sales foundation, rental emergence

Sales retained 84.35% share of Vietnam luxury residential market in 2025 as ownership culture prevails, but professional leasing clusters now expand at 14.62% CAGR on widening expatriate inflows and wealth-management focus. Average gross yields stand at 3.16% in Q1 2025, reaching 3.52% in HCMC. Institutional investors assemble portfolios of branded serviced apartments within prime nodes to secure index-linked income. Vietnam luxury residential market size allocated to rental stock is projected to double by 2031 yet remains a fraction of the sell-to-own stronghold.

Developers respond with leaseback guarantees and co-living floors to attract buy-to-let buyers. Serviced apartment occupancy in HCMC at 85% and rents at USD 42/m² per month underline robust corporate demand pipelines. Should preferential rates for young first-time buyers widen, rental velocity may moderate, but mainstream ownership incentives are not expected to undercut premium leasing in converted Grade A schemes.

By Mode of Sale: Primary vitality outpaces secondary stock

Secondary product commanded 50.45% market share in 2025, valued for immediacy and location certainty. Yet primary launches expand at 14.02% CAGR, lifting Vietnam luxury residential market size for new stock through 2031. Pre-sale absorption exceeds 80% as branded towers and ESG-certified resorts set innovation benchmarks that legacy homes cannot mirror. Primary pricing at VND 120 million/m² (USD 4,800 per square meter) in HCMC outpaces secondary by 47% yet buyers pay for warranties and sophisticated amenity stacks.

Secondary trading remains vibrant in legalised clusters of Thu Duc City where transport completion catalyses capital gains. Upgrades to dated towers prove essential to capture attention of digitally native millionaires who equate technology readiness with prestige. Consequently, owners of older flagships consider value-add refurbishments to narrow the amenity divide.

By City: HCMC pre-eminence meets Da Nang ascent

Ho Chi Minh City captured 37.65% Vietnam luxury residential market share in 2025, delivering the deepest project pipeline and hosting 7,200 resident millionaires. Ba Son peninsula and Thu Thiem peninsula pioneer skyline transformations where average primary asking climbs to VND 120 million/m²(USD 4,800 per square meter). Vietnam luxury residential market size allocation to HCMC remains pre-eminent, yet Da Nang targets a 15.02% CAGR on lifestyle magnetism and airport upgrades.

Hanoi retains cultural cachet, with Tay Ho Tay’s lake-view apartments transacting near VND 300 million/m² (USD 12,000 per square meter). Restrictions in Ba Dinh district cement scarcity premiums reaching USD 40,000/m² for bare land. Coastal Nha Trang and Cam Ranh extend demand chains as integrated resorts with private marinas attract jet-set buyers seeking diversified asset plays and leisure homes.

Geography Analysis

Vietnam luxury residential market continues to cluster in the southern metropolis. HCMC’s central land supply contraction funnels demand toward Thu Duc City and riverside corridors, yet buyers still pay for District 1 heritage addresses that regularly set national price records. Strategic infrastructure such as Ring Road 3 and Ben Luc–Long Thanh Expressway braid suburban satellite nodes into one-hour commutes, stimulating gated villa communities along the peri-urban arc. Da Nang’s runway extension and expressway matrix propel flight-time proximity to Hanoi and HCMC within 90 minutes, spurring second-home accumulation and condotel absorption. Tourism-led GDP bounce backs reinforce rental revenue visibility, assuring investors of cash-flow cover despite higher insurance charges in typhoon belts.

In the north, Hanoi’s diplomatic district scarcity incites vertical intensification around West Lake and the Metro Line 2A spine. Embassies and multinationals underwrite executive leasing, though restrictive foreign quota fill-rates impose longer waitlists. Secondary city Hai Phong leverages industrial estate build-out to nurture fresh luxury schemes anchored by international school catchments.

Central coastal provinces witness branded residence debuts where land banks enable low-rise compositions enveloped by wellness centres, golf courses and marinas. Developers incorporate coastal setback and climate-mitigation designs to meet global insurer criteria, ensuring long-run asset viability. Combining improving flight connectivity and aspirational leisure narratives, these locales broaden the footprint of Vietnam luxury residential market beyond its traditional twin poles.

Competitive Landscape

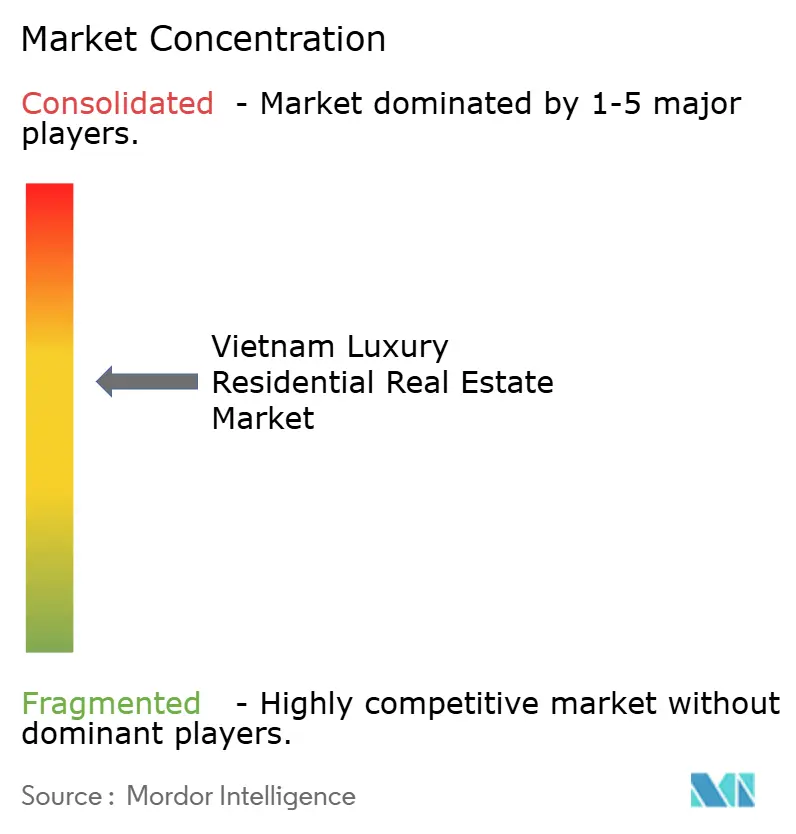

Vietnam luxury residential market remains moderately concentrated: the top five developers hold an estimated 64-67% cumulative active pipeline, warranting a market concentration score of 6. Vingroup commands scale synergy across retail, hospitality and healthcare ecosystems, enabling bundled lifestyle offerings that embed customer stickiness. Q1 2025 revenue reached USD 3.36 billion on the back of Can Gio sea-encroachment kick-off, Vietnam’s single largest luxury city-making scheme. Masterise Homes partners with Marriott International to deliver branded projects such as LUMIÈRE Riverside, registering 75% capital growth over five years and pioneering triple-glazed façade engineering. CapitaLand Vietnam deploys international capital and design discipline, while Keppel Land optimises exposure via selective divestments like the SGD 98 million sale of Saigon Centre Phase 3.

Domestic challenger SonKim Land captures design-centric niche positioning, earning “Developer of the Decade” accolades. NovaLand resumes selective launches after debt reprofiling, emphasising integrated urban townships along Ho Chi Minh City’s eastward expansion. Heightened compliance scrutiny following Van Thinh Phat’s USD 12 billion scandal reinforces due-diligence-led site acquisitions favouring transparent balance sheets. Developers angle for green-finance lines from multilaterals and ESG-mandated funds by achieving EDGE certification, which unlocks concessional debt and amplifies marketing power among environmental-conscious buyers.

Prop-tech adoption intensifies competitive arms races. Virtual walkthroughs, tokenised fractional sales pilots and smart contract based handovers enhance customer experience and differentiate contenders. Overall, brand trust, land reserve depth and funding agility define winners as Vietnam luxury residential market traverses its next investment cycle.

Vietnam Luxury Residential Real Estate Industry Leaders

DAT XANH GROUP

Vingroup

SonKim Land

CapitaLand Vietnam

Masterise Homes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vietnam passes Digital Technology Industry Law recognising crypto assets effective January 2026, paving formal pathways for crypto-sourced property purchases.

- June 2025: HDMon Holdings gains clearance for USD 995.3 million Monbay Van Don tourism complex spanning 299 hectares in Quang Ninh province.

- April 2025: Vingroup breaks ground on 2,870-hectare Vinhomes Green Paradise in Can Gio, featuring a planned 108-story tower.

- April 2025: Victory Group partners Go An Cuong and Central on The Win City in Long An, marking extension from luxury toward affordable hybrids.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Vietnam's luxury residential real estate market as all primary and secondary sales or rentals of newly built or existing dwellings that command premium positioning through prime locations, high-end finishes, branded or concierge-grade amenities, and buyer profiles in the top income deciles. Transaction values cover apartments, condominiums, villas, and landed houses across major cities and emerging resort hubs.

Scope exclusion: mid-range, affordable, and social housing units are outside the valuation universe.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-build)

- Secondary (Existing-home Resale)

- By City

- Ho Chi Minh City

- Hanoi

- Da Nang

- Nha Trang

- Other Cities

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview developers, high-net-worth property brokers, private bankers, municipal planning officers, and prop-tech suppliers across Ho Chi Minh City, Hanoi, and coastal resorts. These conversations validate pipeline sizes, achievable selling prices, rental yields, and regulatory pinch points, thereby bridging gaps left by published statistics and sharpening our model assumptions.

Desk Research

We start with foundational data points from tier-1 public bodies such as the General Statistics Office of Vietnam, Ministry of Construction, State Bank of Vietnam, and customs trade portals, which reveal macro growth, household income shifts, and foreign capital inflows. City-level supply, absorption, and price benchmarks are gathered from trade associations and real-estate consultancies, including VNREA, CBRE Vietnam, Knight Frank, and Cushman & Wakefield reports. To enrich ownership landscapes, we review land registration bulletins, patent filings for smart-home systems through Questel, and developer financials housed in D&B Hoovers. The sources cited here illustrate our approach; several additional publications, journals, and filings are also consulted throughout the desk phase.

Market-Sizing & Forecasting

A top-down demand pool is first constructed by mapping urban household income brackets against documented luxury home penetration and foreign purchase quotas. Select bottom-up checks, such as sampled average selling price multiplied by verified unit launches, help fine-tune totals. Key model inputs include HNWI population growth, mortgage rate trajectories, land availability permits, branded residence share of new launches, and historical absorption velocity. Multivariate regression aligns each driver with past market movements before an ARIMA overlay delivers the forward curve from 2025 to 2030. Data pockets with sparse disclosure are estimated through regionally comparable proxies and later back-tested with new primary findings.

Data Validation & Update Cycle

Outputs undergo variance scanning versus independent indicators like VAT collections and building material imports. Senior reviewers perform a second pass, and any anomaly triggers a call-back to field sources. Reports refresh annually, while significant policy or price shocks prompt interim revisions so clients always receive the latest view.

Why Mordor's Vietnam Luxury Residential Real Estate Baseline Earns Trust

Published figures often differ because firms pick distinct scope boundaries, driver sets, and currency treatments.

Key gap drivers include whether resale activity is counted, if branded residences are isolated or blended, the choice of VND or USD base year, and refresh cadence that may lag sharp price swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.02 B (2025) | Mordor Intelligence | - |

| USD 3.9 B (2024) | Regional Consultancy A | Excludes secondary sales and converts at fixed 2023 FX rate |

| USD 4.14 B (2025) | Trade Journal B | Counts only projects above USD 6,000 /m², narrows geography to HCMC and Hanoi |

| USD 5.0 B (2024) | Industry Association C | Uses announced pipeline instead of realized transactions, lacks price deflation for incentives |

The comparison shows that while other publishers offer useful snapshots, their narrower scopes or static assumptions inflate or compress totals. By blending inclusive coverage, current exchange rates, and a clear update rhythm, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the size of Vietnam’s luxury residential market in 2026 and how large will it be by 2031?

The market stands at USD 3.42 billion in 2026 and is projected to reach USD 6.36 billion by 2031.

Which city holds the biggest share of Vietnam’s luxury residential market?

Ho Chi Minh City leads with 37.65% market share, supported by 7,200 resident millionaires and constrained central land.

What is the expected compound annual growth rate for the market?

The overall Vietnam luxury residential market is forecast to expand at a 13.22% CAGR between 2026 and 2031.

Can foreign buyers own luxury property in Vietnam?

Yes; the Land Law 2024 (effective 2025) streamlines procedures while retaining caps of 30% of units in a condominium block and up to 250 landed houses per ward-equivalent area.

What rental yields can investors expect in prime locations?

Average gross yields were 3.52% in Ho Chi Minh City, 2.90% in Hanoi and 3.06% in Da Nang during Q1 2025.

How will digital-asset legalization affect luxury home demand?

Regulation taking effect in 2026 legitimizes crypto-to-property transactions, creating a new pool of tech and crypto millionaires looking to purchase high-end residences.

Page last updated on: