Vietnam Insecticide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

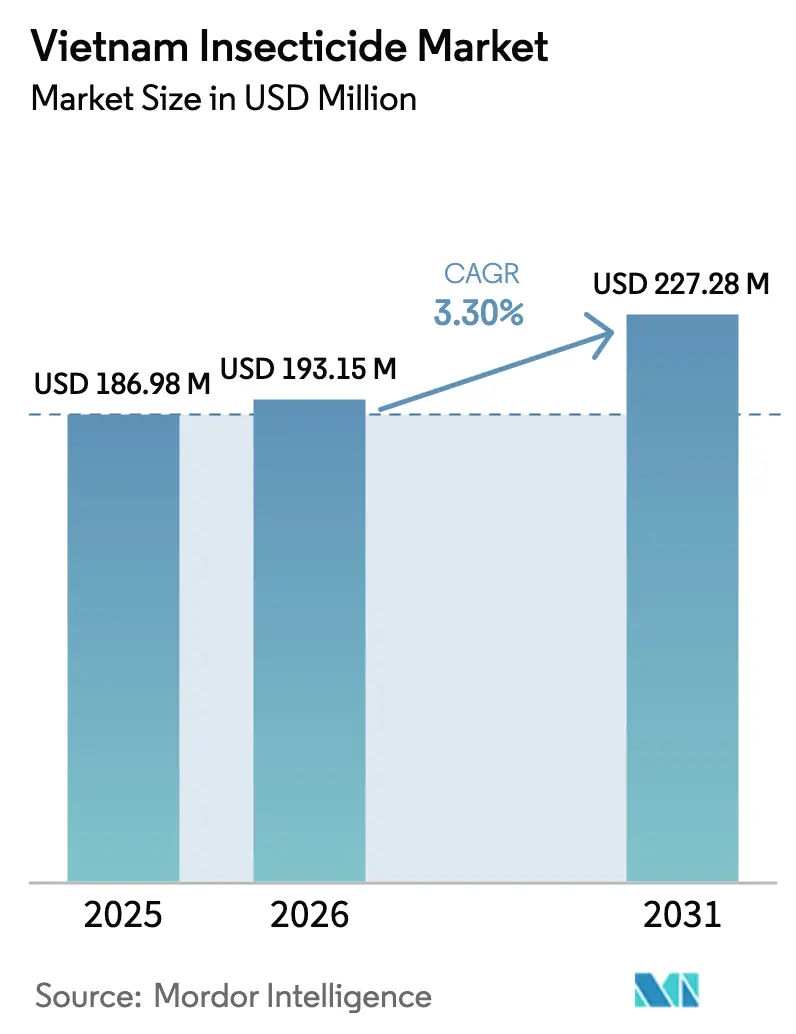

| Base Year Market Size (2025) | USD 186.98 Million |

| Market Size (2026) | USD 193.15 Million |

| Market Size (2031) | USD 227.28 Million |

| Growth Rate (2026 - 2031) | 3.30% CAGR |

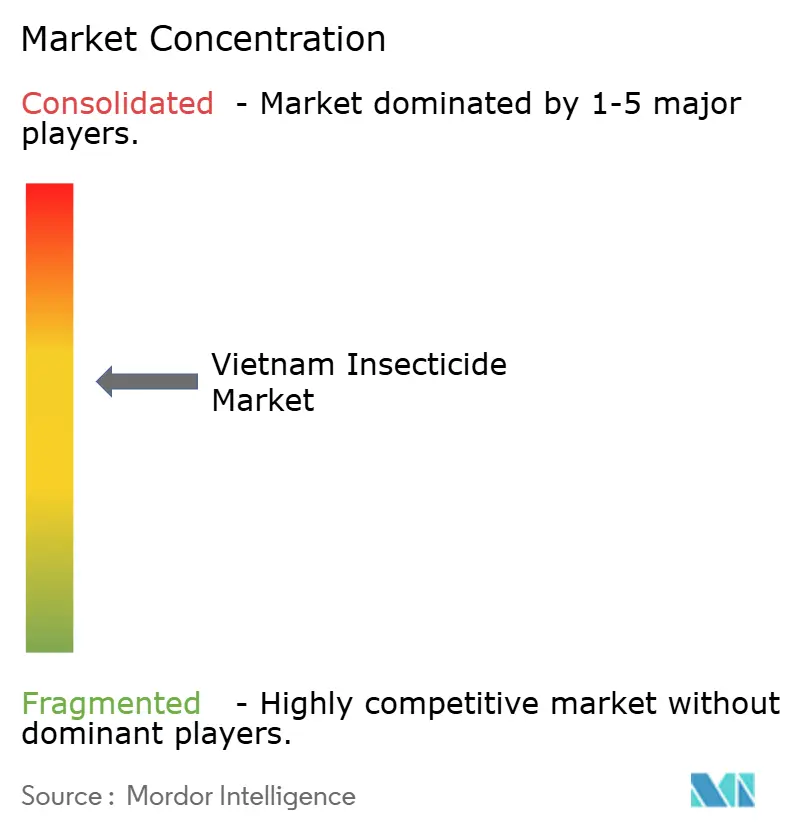

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Insecticide Market Analysis by Mordor Intelligence

The Vietnam insecticide market size is expected to grow from USD 186.98 million in 2025 to USD 193.15 million in 2026 and is forecast to reach USD 227.28 million by 2031 at 3.30% CAGR over 2026-2031. Rising pest pressure on rice, expanding fruit and vegetable acreage, and supportive digital distribution channels keep demand steady even as integrated pest management (IPM) programs temper overall volume growth. E-commerce platforms deliver genuine products at lower prices, countering the historic dominance of informal retail networks. Simultaneously, drone spraying cooperatives and QR-code authentication tools are improving application precision and brand trust, encouraging a gradual shift toward premium formulations. Multinational companies maintain strong footholds, yet nimble domestic suppliers gain share in cost-sensitive rural districts, creating a balanced but competitive ecosystem within the Vietnam insecticide market.

Key Report Takeaways

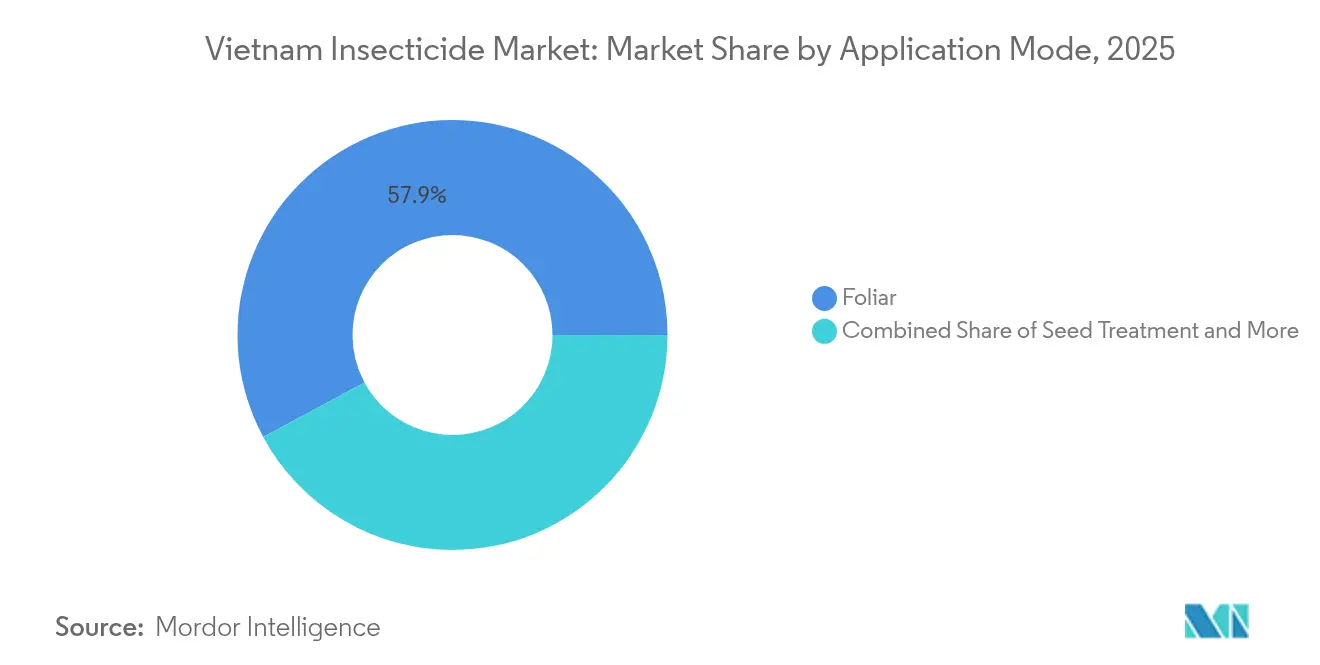

- By application mode, foliar spraying led with 57.86% of the Vietnam insecticide market share in 2025, while seed treatment is forecast to post a 3.47% CAGR through 2031.

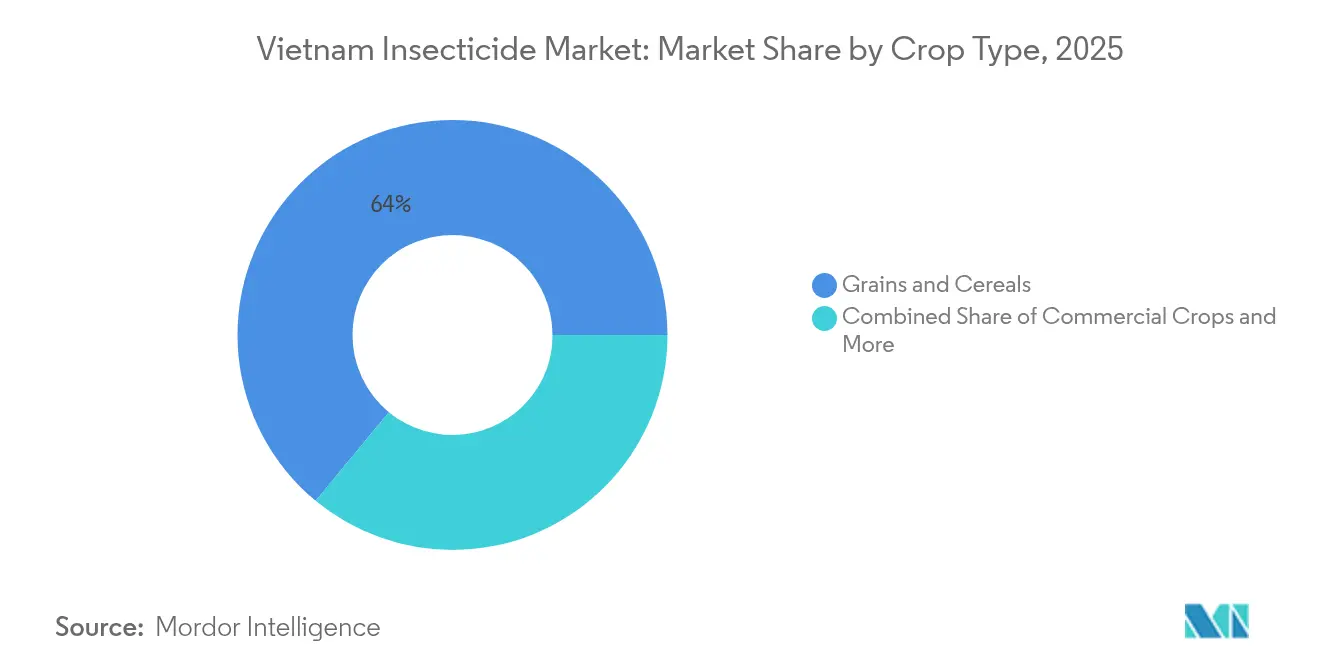

- By crop type, grains and cereals captured 64.02% share of the Vietnam insecticide market size in 2025; fruits and vegetables are advancing at a 3.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Insecticide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating brown planthopper outbreaks | +0.8% | Mekong Delta, Red River Delta | Short term (≤ 2 years) |

| Rapid switch to hybrid rice varieties demanding higher insecticide use | +0.6% | National, concentrated in major rice provinces | Medium term (2-4 years) |

| Government-backed "one must do, five reductions" IPM refresh is widening acceptance | +0.4% | National implementation with pilot provinces | Long term (≥ 4 years) |

| E-commerce ag-input platforms lowering last-mile prices for smallholder farmers | +0.5% | National, early adoption in urban-adjacent areas | Medium term (2-4 years) |

| Emergence of drone-based precision spraying cooperatives | +0.3% | Northern provinces, expanding to the Central Highlands | Long term (≥ 4 years) |

| Cross-border counterfeit clampdown raising branded product sales | +0.4% | Border provinces, spillover effects nationally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Brown Planthopper Outbreaks

During 2024, the Mekong Delta recorded densities topping 2,000 hoppers per square meter, well beyond damage thresholds; emergency foliar applications restored yield stability yet reinforced grower reliance on the Vietnam insecticide market[1]Source: Plant Protection Department, “Brown Planthopper Surveillance Report,” ppd.gov.vn. Resistance surveys show reduced efficacy of imidacloprid and thiamethoxam, steering demand toward higher-priced mixed-mode products. The government’s rapid-response advisories shortened decision time, leading farmers to favor suppliers with reliable logistics. Local distributors that guarantee 48-hour delivery saw a sales jump, underscoring logistics as a competitive lever. Stakeholders expect outbreaks to remain cyclical, ensuring the driver’s short-term pull on market value.

Rapid Switch to Hybrid Rice Varieties Demanding Higher Insecticide Use

Hybrid seeds covered 1.8 million hectares in 2024, 23% of Vietnam’s rice area, and require 15–20% more insecticide sprays owing to denser canopies and extended maturity[2]Source: International Rice Research Institute, “Hybrid Rice Expansion in Vietnam,” irri.org. This dynamic adds incremental volume and shifts preference toward systemic actives with longer residual power. Growers adopting hybrids spend roughly USD 11 more per hectare on crop protection, enlarging the premium tier of the Vietnam insecticide market. Provincial subsidies for certified hybrid seed ensure sustained adoption, locking in a multi-year demand tailwind. Suppliers bundling seed and chemical packages capture cross-selling opportunities and deepen on-farm relationships.

Government-Backed “One Must Do, Five Reductions” IPM Refresh Widening Acceptance

The refreshed IPM framework, piloted across 12 provinces in 2024, reduces blanket spraying yet encourages targeted applications with low-toxicity chemistries[3]Source: Ministry of Agriculture and Rural Development, “Vietnam Agricultural Outlook 2025,” mard.gov.vn. Demonstrations in An Giang documented a drop in volume but a yield lift, signaling that optimized timing supports value retention for the Vietnam insecticide market. Product registration now favors active ingredients with selectivity toward beneficial insects, spurring portfolio renewal among multinationals. Training modules delivered through village extension centers improve product stewardship, reinforcing brand loyalty for firms that invest in extension services.

E-Commerce Ag-Input Platforms Lowering Last-Mile Prices For Smallholder Farmers

Digital portals such as Sitto Vietnam trimmed distribution margins 15–25% in 2024, unlocking access for smallholders who had struggled with high retail mark-ups. Verified QR codes assure authenticity, eroding counterfeit presence and lifting branded share in the Vietnam insecticide market. Mobile apps integrate localized weather alerts and pest forecasts, nudging farmers toward just-in-time purchases and reducing waste. Early adopters report a 7% cost saving per season, encouraging peer uptake through word-of-mouth. Platform analytics also help suppliers refine demand planning and launch micro-pack SKUs that match small landholdings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing pesticide residue rejections | -0.7% | Export-focused provinces, spillover nationally | Short term (≤ 2 years) |

| Rapid resistance development to pyrethroids in fruit orchards | -0.5% | Central Highlands, Mekong Delta fruit regions | Medium term (2-4 years) |

| Expansion of organic certification zones | -0.3% | Northern mountains, selected coastal provinces | Long term (≥ 4 years) |

| Shrinking arable land due to industrial conversion | -0.4% | Peri-urban areas, industrial development zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Pesticide Residue Rejections

European inspectors rejected multiple durian consignments in 2024 for carbendazim and fipronil exceedances, pushing rejection cases year on year. Exporters responded by tightening supplier audits and imposing stricter pre-harvest intervals. Farmers must choose shorter-PHI products or forgo shipments, trimming near-term demand in the Vietnam insecticide market. Rapid kit testing at pack houses raises traceability expectations, favoring suppliers with low-residue portfolios. While compliance investments dent margins, they also accelerate the shift toward safer chemistries.

Rapid Resistance Development to Pyrethroids in Fruit Orchards

Monitoring revealed 60–80% survival of the oriental fruit fly after lambda-cyhalothrin treatment in 2024. Orchards faced higher labor and chemical costs as they rotated to pricier options like spinosyns. Extension agents prescribe structured rotation plans, but adoption varies, risking further resistance escalation. The restraint pressures input budgets in high-value fruit districts, softening segment growth within the Vietnam insecticide market. Yet, it simultaneously opens space for novel mode-of-action launches and integrated lures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Foliar Dominance with Seed Treatment Upside

Foliar spraying generated 57.86% of the Vietnam insecticide market share in 2025, and remains central to rice pest control during panicle initiation. Flooded paddies favor overhead boom or drone sprays that reach canopy tops where planthoppers congregate. Regular monsoon cycles produce predictable infestation peaks, reinforcing foliar reliance. Systemic seed dressings prevent early seedling losses and cut subsequent foliar cycles, explaining their fastest-growing 3.47% CAGR trajectory to 2031.

Manufacturers showcase color-coated seed treatments that double as germination markers, easing adoption. Chemigation and fumigation serve niche greenhouse and orchard uses, together representing under 10% of the Vietnam insecticide market but offering premium margins through specialized service plans. Drone-optimized low-drift formulations help foliar retain relevance by mitigating neighbor exposure concerns. Field trials funded by BASF in Dong Thap demonstrated a 15% deposit improvement on lower leaves, translating to a 4% yield benefit, thus sustaining farmer confidence in foliar technology.

By Crop Type: Rice-Centric Base and Diversifying Fruit Potential

Grains and cereals commanded 64.02% of the Vietnam insecticide market size in 2025, driven principally by rice’s three-crop annual calendar that demands roughly six insecticide applications per hectare. Government export ambitions anchor rice acreage, providing a stable baseline demand. Fruits and vegetables expanding under regional trade pacts are forecast at a 3.42% CAGR, gradually lifting their share in the Vietnam insecticide market. High farm-gate prices for dragon fruit, mango, and longan justify precision sprays and residue-compliant products, inviting premium formulations from multinationals.

Commercial crops such as coffee and pepper in the Central Highlands sustain a specialist tier where insect damage directly affects export grade. Pulse and oilseed cultivation grows modestly under crop rotation programs that manage soil fertility, generating incremental yet resilient demand. Turf and ornamental segments stay nascent but pick up as urbanization and hospitality investments demand manicured landscapes. Each crop group exhibits a unique pest spectrum, compelling suppliers to maintain diverse active ingredient portfolios and technical advisory capacity.

Geography Analysis

The Mekong Delta anchors more than half of the national rice output, making it the largest consumer of insecticides in Vietnam; intensive triple-cropping schedules coupled with high humidity generate perennial brown planthopper and stem borer challenges. Growers here favor fast-acting foliar mixtures that align with tight planting windows. Dependable waterways shorten distribution lead times, enabling just-in-time deliveries that reduce on-farm storage costs. However, environmental sensitivities around river ecosystems spur demand for low-toxicity options, a trend that multinationals leverage through stewardship campaigns.

In the Red River Delta, the average rice plot size is below 0.5 hectares, so farmers prefer smaller package sizes and multi-crop labels. Diversity in crop rotations, especially vegetables in peri-urban belts, creates a mosaic of pest dynamics that raises demand for broad-spectrum yet residue-smart solutions. Retail stores cluster around township markets, but e-commerce adoption grows fastest here owing to dense 4G coverage and higher smartphone penetration, reinforcing digital sales channels for the Vietnam insecticide market.

The Central Highlands contributes disproportionately to export earnings through coffee, pepper, and fruit. Orchards face seasonal outbreaks of berry borer and fruit fly, demanding advanced monitoring and baiting technologies. Altitude moderates humidity, extending the residual life of certain chemistries and reducing spray frequency, but export residue limits are strict. Growers thus invest in integrated programs that blend pheromone traps with selective insecticides. Drone services are popular because hilly terrain restricts tractor access, driving specialized formulation demand.

Competitive Landscape

The Vietnam insecticide market is moderate. Multinationals BASF SE, Bayer AG, Syngenta Group, Wynca Group (Wynca Chemicals), and UPL Limited capitalize on robust R&D pipelines, rigorous stewardship support, and established networks. Their collective focus on formulation upgrades, such as micro-encapsulation and drone-ready concentrates, helps retain high-value segments. Domestic players like Loc Troi Group and Sitto Vietnam prize quick product registration cycles and cost-effective packaging, anchoring them in price-sensitive rural corners of the Vietnam insecticide market.

Strategic competition revolves around field demonstrations, digital advisory platforms, and integrated offerings rather than simple price warfare. Syngenta’s 2024 launch of a mobile pest advisory app added decision support for 25,000 farmers, leading to a reported 10% lift in cross-sell rates for its foliar range. BASF invested USD 12 million in a Ho Chi Minh City technical center to speed tropical-climate formulation testing, shortening launch lead-times. Domestic firms respond by bundling crop loans with product sales, protecting customer bases through financial stickiness.

Regulation tightens entry barriers. Post-2024 amendments require environmental impact dossiers for active ingredients, a hurdle that smaller importers struggle to clear. Yet, anti-counterfeit drives benefit legitimate brands across the Vietnam insecticide market, boosting replacement demand for authentic products and improving revenue certainty. Consolidation activity remains plausible as local firms seek foreign technology and capital, while global majors aim for deeper rural penetration.

Vietnam Insecticide Industry Leaders

Bayer AG

Syngenta Group

UPL Limited

Wynca Group (Wynca Chemicals)

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: FMC Corporation received recognition from Vietnam's Ministry of Agriculture for contributions to sustainable agriculture development, highlighting the company's integrated pest management training programs and reduced-risk product introductions.

- November 2024: Corteva Agriscience partnered with the Western Highlands Agriculture and Forestry Science Institute to develop integrated pest management solutions for coffee and pepper cultivation in the Central Highlands, establishing a USD 8 million research collaboration focused on sustainable crop protection technologies and resistance management strategies.

- January 2023: Vietnam's Plant Protection Department approved 23 new insecticide formulations for registration, including several biological control products and reduced-risk synthetic chemistries designed to support the country's integrated pest management objectives while maintaining efficacy against key pests.

Vietnam Insecticide Market Report Scope

Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits & Vegetables |

| Grains & Cereals |

| Pulses & Oilseeds |

| Turf & Ornamental |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits & Vegetables | |

| Grains & Cereals | |

| Pulses & Oilseeds | |

| Turf & Ornamental |

Market Definition

- Function - Insecticides are chemicals used to control or prevent insects from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms