Vietnam Cross-Border E-commerce Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

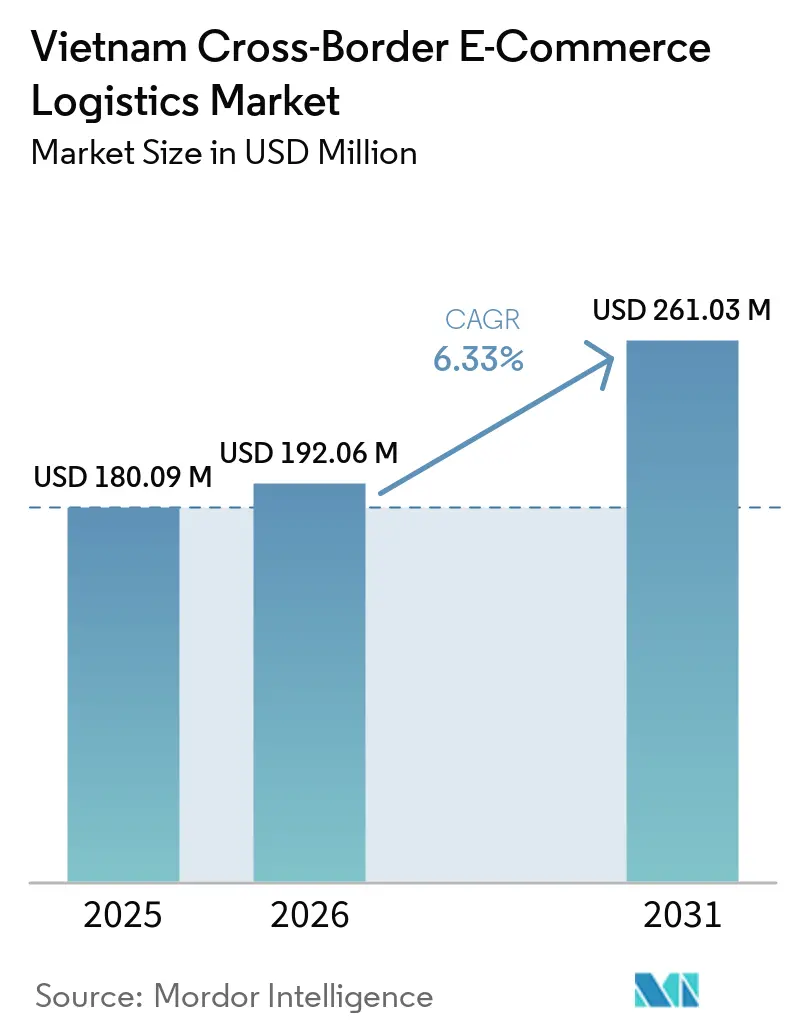

| Base Year Market Size (2025) | USD 180.09 Million |

| Market Size (2026) | USD 192.06 Million |

| Market Size (2031) | USD 261.03 Million |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Cross-Border E-commerce Logistics Market Analysis by Mordor Intelligence

The Vietnam Cross-Border E-commerce Logistics Market size was valued at USD 180.09 million in 2025 and is estimated to grow from USD 192.06 million in 2026 to reach USD 261.03 million by 2031, at a CAGR of 6.33% during the forecast period (2026-2031).

The Vietnam Cross-Border E-commerce Logistics Market is expanding within a trade system that moved past USD 930 billion in total import and export turnover in 2025, while online cross-border trade remained at USD 4.45 billion, which shows that digital cross-border logistics still serves a relatively small share of Vietnam’s wider trade base and therefore has room to deepen over time. Policy is now shaping the operating model more directly, because Decision No. 2229/QĐ-TTg set a national logistics development path through 2035, including modern logistics centers and stronger investment in e-commerce warehousing and connected infrastructure. The new Law on E-Commerce No. 122/2025/QH15, effective from July 1, 2026, also raises the compliance threshold for platform-linked logistics activity, especially through legal entity, consumer protection, and implementation requirements that favor operators with formal systems and reporting capability. The Vietnam Cross-Border E-commerce Logistics Market is also being pulled by structural demand from import parcel flows and by a faster export push from Vietnamese MSMEs, especially where logistics providers can combine clearance, warehousing, and fulfillment instead of offering transport alone. This leaves the Vietnam Cross-Border E-commerce Logistics Market in a phase where compliance strength, bonded capacity, and service integration matter more than scale in parcel movement alone.

Key Report Takeaways

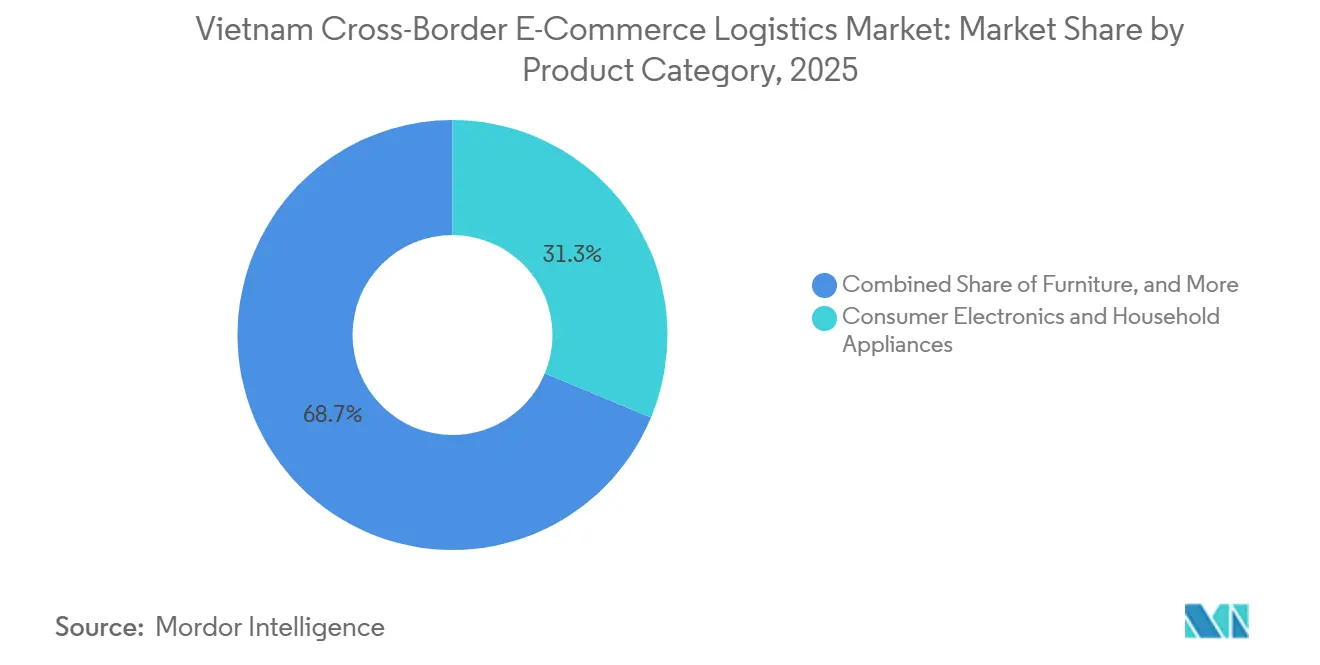

- By product category, consumer electronics and household appliances held 31.26% of the Vietnam Cross-Border E-commerce Logistics Market share in 2025, while personal and household care are projected to expand at a 7.32% CAGR through 2031.

- By logistics function, transport accounted for 67.94% of the Vietnam Cross-Border E-commerce Logistics Market size in 2025, while value-added services are forecast to grow at an 11.50% CAGR through 2031.

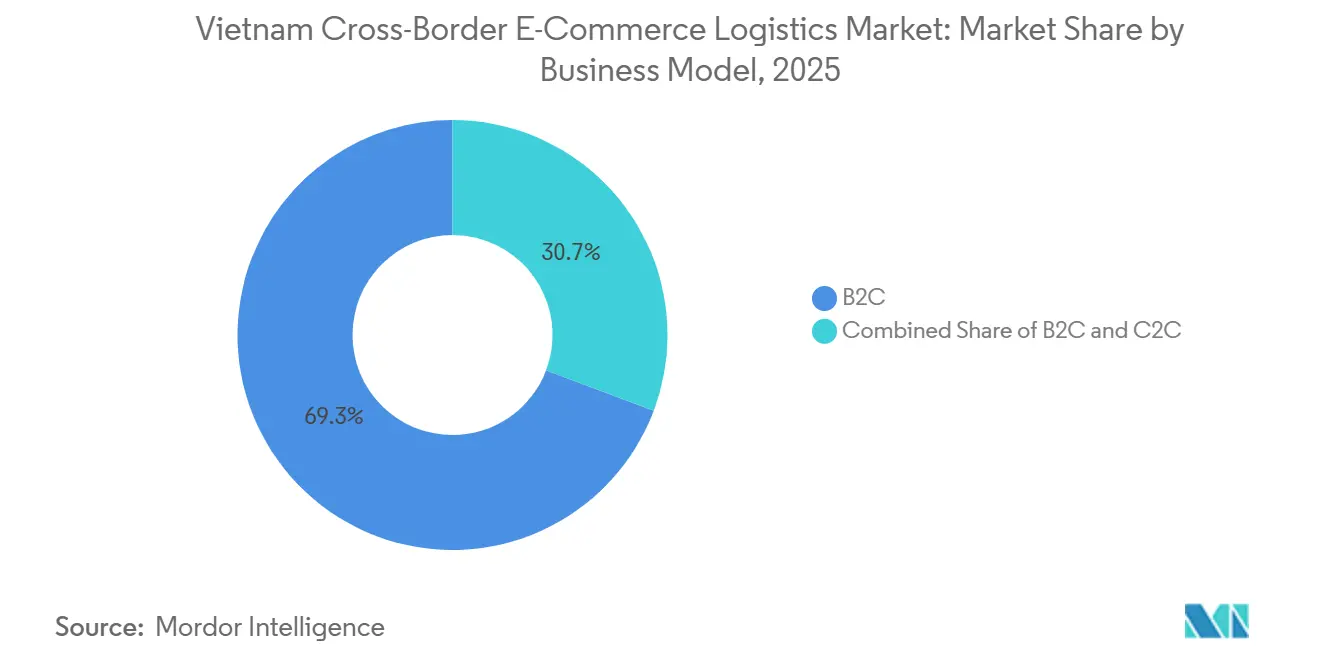

- By business model, B2C held 69.26% of the Vietnam Cross-Border E-commerce Logistics Market share in 2025, while B2C is projected to record the highest CAGR at 19.12% through 2031.

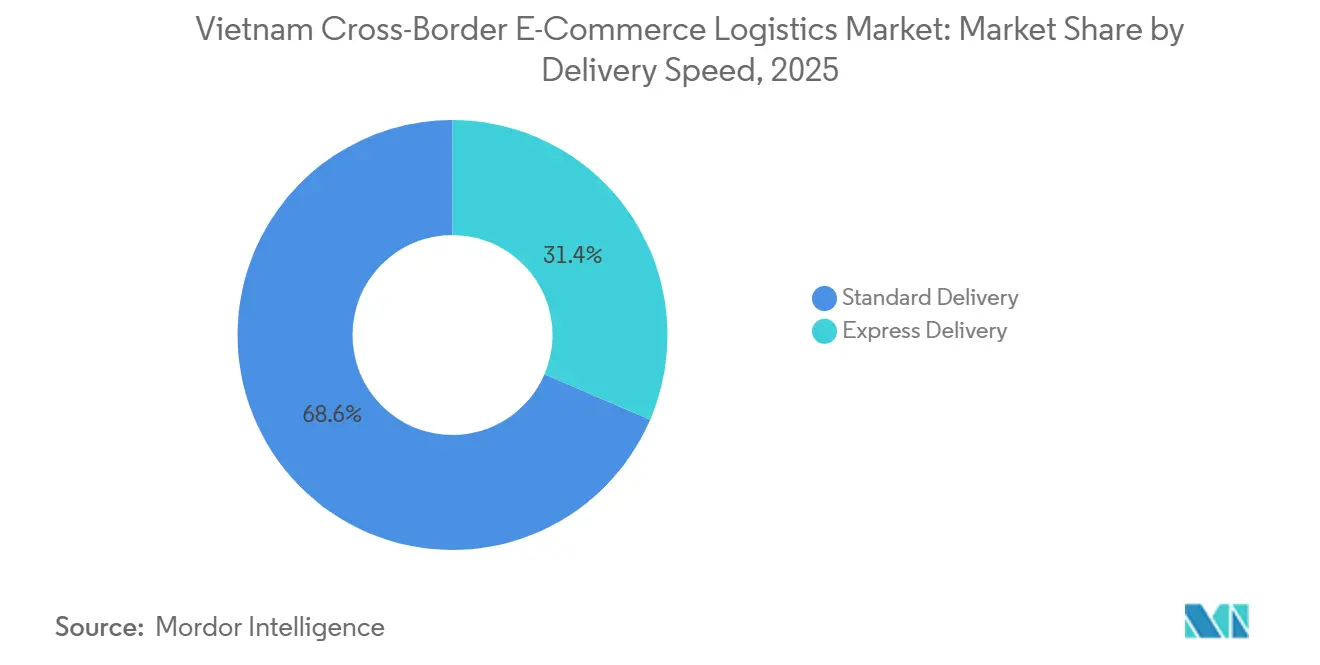

- By delivery speed, standard delivery accounted for 68.56% of the Vietnam Cross-Border E-commerce Logistics Market share in 2025, while express delivery is forecast to advance at a 9.36% CAGR through 2031.

- By flow direction, inbound logistics represented 58.10% of the Vietnam Cross-Border E-commerce Logistics Market size in 2025, while outbound logistics is projected to grow at a 7.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Cross-Border E-commerce Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Policy-Backed Formalization of Cross-Border Seller Ecosystems | +1.20% | National, with concentration in Hanoi, Ho Chi Minh City, and Da Nang corridors | Medium term (2-4 years) |

| Marketplace-Led Import Parcel Expansion From North Asia | +1.50% | APAC core, with concentration on the Vietnam-China corridor and spillover to SEA | Short term (≤ 2 years) |

| Export Scaling for Furniture and Fashion MSMEs | +0.90% | National export corridors, with early gains in Binh Duong, Dong Nai, and Hanoi | Medium term (2-4 years) |

| Rising Electronics and Beauty Parcel Density | +1.10% | Urban centers including Ho Chi Minh City and Hanoi, with spillover to Tier 2 cities | Short term (≤ 2 years) |

| Single-Window Customs Digitization and Bonded Inventory Enablement | +0.80% | Hai Phong and Ho Chi Minh City port clusters, plus national customs border gates | Medium term (2-4 years) |

| Cross-Border Service-Layer Growth In Returns, Compliance, and DDP/DDU Support | +0.60% | National, with highest penetration in B2C-heavy e-commerce corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Policy-Backed Formalization of Cross-Border Seller Ecosystems

Vietnam’s regulatory setting moved from scattered rules toward a more integrated framework across 2025 and 2026. The Law on E-Commerce No. 122/2025/QH15 was adopted in December 2025 and took effect on July 1, 2026, while the implementation plan assigns ministries and local authorities clear responsibilities for review, training, and follow-on decrees. The draft law process also made cross-border platform accountability more explicit by requiring foreign platforms to establish or authorize a legal entity in Vietnam for taxation, dispute handling, and consumer protection support[1]“MoIT Leader Presents the Government’s Submission on the Draft Law on E-Commerce,” Ministry of Industry and Trade, moit.gov.vn. That change matters for the Vietnam Cross-Border E-commerce Logistics Market because parcel flows connected to formal marketplaces are more likely to move through licensed operators with traceable systems than through gray-channel networks. The same policy cycle is linked to the national e-commerce development plan for 2026 to 2030, which supports digital infrastructure, logistics improvement, and more transparent cross-border trade conditions. As a result, the Vietnam Cross-Border E-commerce Logistics Market is likely to favor carriers that can connect platform compliance, customs documentation, and fulfillment data into one operating stack.

Marketplace-Led Import Parcel Expansion from North Asia

Inbound parcel demand continues to be shaped by the close link between North Asian supply and Vietnamese online consumption. Official association material shows that Vietnam’s online cross-border trade base remains small relative to total trade, which means even modest gains in platform-led imports can lift parcel density quickly when consumer adoption broadens. The new tax treatment for low-value imports also changes how these parcels move, because every inbound shipment now carries VAT handling obligations that push operators toward more structured import processes. This makes bonded and bulk-clearance models more attractive than fragmented express-only handling for very high parcel counts. In practice, the Vietnam Cross-Border E-commerce Logistics Market benefits when large operators can pre-position stock, clear in bulk, and shorten delivery windows without losing control over documentation.

Export Scaling for Furniture and Fashion MSMEs

Export activity is becoming a more visible growth engine for digital logistics in Vietnam. Industry association material cited in the supplied draft shows furniture e-commerce exports are expected to grow at 20% annually between 2024 and 2029, while fashion is expected to grow at 26% annually over the same period, which is materially faster than many traditional export channels. The Vietnam Cross-Border E-commerce Logistics Market, therefore, faces a gradual shift in the mix, with export-support functions such as pickup, consolidation, document management, and returns becoming increasingly important for MSMEs that sell directly to overseas buyers. WTO Center Vietnam also noted that cross-border e-commerce is moving from a sales channel toward a stronger export pillar, especially for firms looking to shift from outsourced production toward direct selling and brand control[2]“Cross-Border E-Commerce, From a Sales Channel to a New Pillar of Exports,” WTO Center Vietnam, wtocenter.vn. This gives logistics providers a larger role in seller enablement, because smaller exporters often need service bundles rather than standalone freight. Over time, the Vietnam Cross-Border E-commerce Logistics Market should see stronger demand from operators that can make export compliance and fulfillment more usable for smaller furniture and fashion shippers, not just large brands.

Rising Electronics and Beauty Parcel Density

Consumer electronics and household appliances formed the largest product category, supporting the Vietnam Cross-Border E-commerce Logistics Market because both categories are well-suited to parcelized movement, repeat ordering, and stronger service monetization through faster handling and cleaner customs processing. Electronics imports benefit from established supply links with regional manufacturing centers, while beauty demand is supported by cross-border direct-to-consumer purchasing and repeat consumption behavior. The Vietnam Cross-Border E-commerce Logistics Market, therefore, gains when operators can manage faster lead times in dense urban corridors without losing economics in secondary cities. The commercial logic is simple because dense, higher-value parcels can absorb premium service layers better than low-value general merchandise can.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Logistics and Reverse-Logistics Cost Burden | -0.70% | National, with the sharpest effect on Vietnam-US and Vietnam-EU outbound corridors | Short term (≤ 2 years) |

| Customs, Tax, and Destination-Market Compliance Complexity | -0.50% | Global outbound routes, especially the US, EU, and Japan | Medium term (2-4 years) |

| Removal of Low-Value Import VAT Exemption | -0.80% | National, concentrated on high-volume inbound parcel corridors from China | Short term (≤ 2 years) |

| Bulky-Product Return and Damage Economics | -0.30% | Outbound furniture and large appliance corridors, especially North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Logistics and Reverse-Logistics Cost Burden

Cost remains one of the clearest operating limits for sellers and logistics providers. VCCI material in the supplied draft states that cross-border goods often face landed costs that are 30%-50% higher than those for locally held inventory, once duties, VAT, and transport are included, which directly reduces the room to compete on low-ticket items. The Vietnam Cross-Border E-commerce Logistics Market is particularly exposed on export routes, where first-mile collection outside Hanoi and Ho Chi Minh City still adds cost before international transit even begins. Reverse logistics is even harder because international returns require coordination across multiple carriers, customs touchpoints, and local inspection steps that are not yet standardized. Government-linked discussions have already identified nearby overseas logistics hubs and bonded storage as part of the answer, indicating that the cost issue is not a marginal problem but a structural one. Until that network matures, the Vietnam Cross-Border E-commerce Logistics Market will remain less efficient for low-value export parcels and more reliant on operators that can spread compliance and handling costs across larger shipment pools.

Customs, Tax, and Destination-Market Compliance Complexity

Compliance complexity remains a second major restraint because outbound growth exposes Vietnamese sellers to several destination regimes at the same time. The supplied ADB reference noted that cross-border e-commerce tax treatment differs widely across jurisdictions, which means Vietnamese operators must stay current with several import systems rather than one harmonized framework[3]“Taxing Cross-Border E-Commerce Supplies, Lessons from Value-Added and Goods and Services Tax Policies in Australia and Viet Nam,” Asian Development Bank, adb.org. At the same time, Vietnam is still updating its own customs and digital control structure, with 2026 marked as the critical year for amending the Customs Law and shifting fully toward a digital customs model. The Vietnam Cross-Border E-commerce Logistics Market, therefore, operates in an environment where policy progress is real, but operating rules are still moving and require frequent system updates. This is manageable for larger integrators with internal compliance teams, but it is harder for smaller providers that depend on manual processes or seller-supplied documentation. As export volumes rise, the Vietnam Cross-Border E-commerce Logistics Market will likely see a wider performance gap between carriers that price compliance correctly and carriers that treat it as an afterthought.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Electronics Anchors Revenue While Beauty Drives the Next Growth Wave

Consumer electronics and household appliances accounted for 31.26% of the Vietnam Cross-Border E-commerce Logistics Market in 2025, making the segment the main revenue driver for parcelized cross-border activity. This position reflects a favorable operating profile that combines relatively high unit values, repeat demand, and strong sourcing links with North Asian manufacturing ecosystems. In the Vietnam Cross-Border E-commerce Logistics Market, electronics also support better monetization for customs brokerage, careful handling, and faster delivery options, as buyers are less price-elastic in fulfillment than in basic commodity categories. The category fits well with import-driven demand. Consumer electronics, therefore, do more than add volume because they help sustain service mix and route density in lanes where cross-border lead time matters. That role gives the segment an outsized influence on network design across urban gateways and bonded processing points.

Personal and household care are the fastest-growing product categories, with a 7.32% CAGR through 2031, indicating that future growth is moving beyond large electronics baskets into more frequent, brand-led parcel flows. The Vietnam Cross-Border E-commerce Logistics Market benefits from this shift because beauty parcels are dense, easier to package, and often more compatible with repeat cross-border ordering than bulky goods are. That makes the category important for express services, especially when demand expands beyond Hanoi and Ho Chi Minh City into secondary urban centers. Fashion and lifestyle also remain strategically relevant, because Vietnam serves both as an import destination and as a production base for export-oriented sellers seeking direct international access. Furniture, by contrast, offers strong value per shipment but also exposes the Vietnam cross-border e-commerce logistics industry to more difficult return economics, damage risk, and overseas warehousing requirements. Foods and beverages add another specialized layer, because compliance, product integrity, and in some cases temperature control create higher entry barriers than those in standard parcel delivery.

By Logistics Function: Transport Dominance Masks a Shift Toward Integrated Services

Transport held 67.94% of the Vietnam Cross-Border E-commerce Logistics Market size in 2025, which confirms that physical movement across borders remains the core of the market. This is not surprising, because every digital order still depends on linehaul, port or airport handling, and last-mile execution before any higher-margin service can be sold. The segment also captures the effect of Vietnam’s position between regional manufacturing centers and export destinations, which keeps transport demand structurally high across both import and export lanes. Within the Vietnam Cross-Border E-commerce Logistics Market, transport therefore remains the foundational function that determines timing, route economics, and service reliability. Standard delivery reinforces that point because a large portion of parcel volume still moves on cost-led rather than speed-led terms. In short, transport continues to anchor the market even as service sophistication around it rises.

Value-added services and others are projected to grow at an 11.50% CAGR through 2031, making it the fastest-moving functional area in the Vietnam Cross-Border E-commerce Logistics Market. This shows that shippers and platforms increasingly want integrated handling of returns, DDP and DDU choices, customs support, and seller-facing orchestration rather than basic movement alone. Official policy direction also supports that evolution, because the national logistics roadmap calls for stronger investment in e-commerce warehouses, digital tools, and integrated service models. Customs digitization strengthens the same trend by rewarding providers that can submit, manage, and reconcile data efficiently across multiple steps. As that operating model spreads, the Vietnam cross-border e-commerce logistics industry becomes less defined by freight movement alone and more by who can turn regulatory and operational complexity into a usable service layer. This is why transport still leads today, while value-added services are likely to capture more of the profit pool over time.

By Business Model: B2C Concentrates Volume and Shapes Operating Priorities

B2C held 69.26% of the Vietnam Cross-Border E-commerce Logistics Market share in 2025 and therefore represented the largest business model within the market. B2C also recorded the fastest projected expansion at a 19.12% CAGR through 2031, which means the segment leads on both current scale and future momentum. This pattern reflects the role of major marketplaces in aggregating demand, standardizing checkout, and channeling both import and export parcels through more formal logistics rails. In the Vietnam Cross-Border E-commerce Logistics Market, B2C traffic sets the pace for delivery expectations, return policies, and seller onboarding requirements more than any other model does. It also creates high parcel concentration in urban corridors, which helps large operators build route density and service consistency. The combination of scale and growth makes B2C the main reference point for network planning across the market.

The same concentration also creates pressure, because strong marketplace influence tends to compress the room available for independent carriers to set prices freely. Large sellers and platform-linked networks have stronger bargaining power, which shifts value toward carriers that can prove service quality, compliance, and national reach. B2B remains important for furniture, commercial shipments, and steadier contract volumes, but its growth rate is lower and its operating profile is less tied to fast parcel turnover. C2C remains limited because cross-border individual selling is still more likely to pass through intermediated marketplace structures than through truly standalone international shipping. The new e-commerce law supports a more traceable operating environment for platform-linked activity, including foreign platform accountability and broader implementation rules[4]“Roadmap to Making Logistics a Pillar of Vietnam’s Economy in the Period 2025-2035 and Vision 2050,” Vietnam Government Portal, vietnam.vn. As a result, the Vietnam Cross-Border E-commerce Logistics Market is likely to remain B2C-led, while B2B offers selective margin opportunities for providers that are willing to manage more complex cargo and compliance needs.

By Delivery Speed: Standard Delivery Holds Volume While Express Gains Economic Weight

Standard delivery accounted for 68.56% of the Vietnam Cross-Border E-commerce Logistics Market size in 2025, which confirms that cost sensitivity still shapes a large share of parcel decisions. This dominance is tied to the volume of economy-oriented import parcels and to product categories where speed does not justify a major price premium. The Vietnam Cross-Border E-commerce Logistics Market still serves many baskets where shoppers accept longer lead times in exchange for lower total order cost, especially for low to mid-value goods. Standard service also aligns with bulk import models and consolidated routing strategies that became more relevant after the low-value VAT exemption was removed. For operators, that means standard delivery remains essential for maintaining shipment scale even if it does not drive the highest margin per parcel. It is likely to stay the backbone of volume over the near term.

Express delivery, however, is projected to grow at a 9.36% CAGR through 2031 and is becoming more important to the revenue mix of the Vietnam Cross-Border E-commerce Logistics Market. This is closely linked to higher consumer expectations, more time-sensitive categories, and stronger export use cases where delivery speed supports seller credibility abroad. FedEx’s direct-serve move in June 2025 and its later partnership with Viettel Post in April 2026 both show that leading networks are investing in stronger service control and wider national pickup and delivery reach for cross-border flows. Those actions matter because express growth depends on more than international air capacity, it also depends on domestic handoff quality and customs coordination. As electronics and beauty continue to gain weight, the Vietnam Cross-Border E-commerce Logistics Market should see express capture a larger share of value even if standard retains most parcels by count. The result is a market where volume and profitability may increasingly diverge by speed tier.

By Flow Direction: Imports Anchor Current Revenue While Exports Drive the Faster Upside

Inbound logistics represented 58.10% of the Vietnam Cross-Border E-commerce Logistics Market share in 2025, which made imports the largest flow direction in the market. This reflects the present structure of online cross-border shopping in Vietnam, where consumers continue to buy imported electronics, beauty products, and fashion from nearby production centers. The Vietnam Cross-Border E-commerce Logistics Market is, therefore, still anchored by import flows that move through platform-heavy and increasingly formalized networks. This gives operators a dependable parcel base, but it also means a large portion of activity is tied to policy changes that affect inbound taxation, customs treatment, and bonded handling. The repeal of the low-value import VAT exemption on February 18, 2025, reinforces that reality by increasing administrative processing for inbound express parcels. Imports, therefore, remain the core of present market value, even as the economics of how those imports are processed continue to shift.

Outbound logistics is the fastest-growing segment, with a 7.32% CAGR through 2031, and represents the main longer-term growth path for the Vietnam Cross-Border E-commerce Logistics Market. Export growth also broadens logistics demand into pickup, consolidation, documentation, and after-sales support, which are more service-intensive than simple import parcel delivery. Government and company activity supports that direction, including greater emphasis on digital customs, logistics centers, and export connectivity. For that reason, the Vietnam Cross-Border E-commerce Logistics Market is likely to remain import-led in size while becoming increasingly export-led in strategic value.

Geography Analysis

Asia-Pacific is the most important corridor in the Vietnam Cross-Border E-commerce Logistics Market because it combines the largest import parcel base with the shortest and most operationally efficient cross-border routes. China remains central to that structure through manufacturing supply, while Japan, South Korea, Australia, and ASEAN markets add both import and export depth. The Vietnam Cross-Border E-commerce Logistics Market also benefits from ASEAN digital customs and certificate exchange mechanisms, which reduce documentation friction on intra-regional trade lanes. That makes Asia-Pacific the corridor with the best mix of scale, proximity, and administrative practicality. For imports, it supports the continued weight of electronics and beauty parcels into Vietnam. For exports, it offers a more manageable route structure for MSMEs that are not ready for the cost and complexity of long-haul Western markets.

North America is the highest-value export corridor, even though it is not the largest in volume. The supplied draft notes that the United States accounted for more than 22% of Vietnam’s online export market in 2025, which gives this route strong strategic weight despite higher compliance and transport complexity. FedEx’s direct-serve transition in 2025 and its 2026 partnership with Viettel Post were both aligned with improving cross-border connectivity and national operating coverage for international shipments from Vietnam. In the Vietnam Cross-Border E-commerce Logistics Market, North America therefore represents a corridor where service quality and customs discipline matter more than sheer parcel count. This is especially true for furniture, fashion, and electronics sellers that use speed and reliability as part of their commercial offer. The route is attractive, but it remains exposed to airfreight cost, returns friction, and destination-market compliance.

Europe is the third major corridor and remains important for both premium inbound goods and outward shipments from Vietnamese exporters. The EVFTA framework supports commercial relevance, but the corridor still demands strong documentation and cost discipline, especially for smaller sellers. The Vietnam Cross-Border E-commerce Logistics Market treats Europe as a route where sea-linked and warehouse-linked solutions can be more important than simple parcel speed, particularly for furniture and other bulky goods. Middle East and Africa remain earlier-stage but are gradually moving onto the map as platform-linked export possibilities broaden. South America still has a limited role and is served more opportunistically than through dedicated cross-border infrastructure. Taken together, these patterns show that the Vietnam Cross-Border E-commerce Logistics Market is geographically diversified in opportunity, but not yet in equal maturity across corridors.

Competitive Landscape

The Vietnam Cross-Border E-commerce Logistics Market remains moderately fragmented, with no single player controlling the field across import parcels, export fulfillment, warehousing, compliance, and nationwide delivery. Global integrators such as DHL, FedEx, Maersk, and Kuehne+Nagel compete on international network control, customs capability, and deeper service integration. Chinese-backed and regional networks compete more aggressively on high-volume parcel economics and close linkage with Asian sourcing ecosystems. Domestic carriers such as Viettel Post, VNPost, GHN, and GHTK remain important because they control or influence critical first-mile and last-mile execution inside Vietnam. This layered structure means competition is shaped by operating role as much as by brand scale. In practice, the Vietnam Cross-Border E-commerce Logistics Market rewards partnership models because very few companies can optimize every part of the chain alone.

Recent official company actions show how firms are trying to strengthen these positions. FedEx designated Viettel Post as its National Network Provider in Vietnam from April 26, 2026, with Viettel Post handling nationwide pickup and delivery, warehouse operations, and customs clearance coordination to improve network efficiency and service reach. FedEx had already shifted to a direct-serve presence in Vietnam from June 2, 2025, which gave it greater operational control and broader access to local shippers through its own operating model. Vietnam Post Logistics also expanded its strategic partnership with Hanjin Group in September 2025 toward air freight and international e-commerce logistics, with a stated focus on fulfillment, warehousing, cross-border shipping, and post-sale support. These moves show that network depth, domestic coverage, and service integration are converging rather than staying separate competitive lanes. In the Vietnam Cross-Border E-commerce Logistics Market, the better-positioned companies are those that can connect international reach with reliable execution inside Vietnam.

Technology and compliance are also becoming stronger differentiators. Vietnam Post Logistics partnered with Phenikaa-X in October 2025 to co-develop smart warehouse systems using autonomous robotics and AI-powered warehouse management, which shows domestic operators are investing in process efficiency rather than relying only on route scale. The same company also signed a strategic agreement with Samsung Welstory Vietnam in April 2025 around cold chain, warehousing, and digital supply chain management, which broadens its service profile into more specialized logistics handling. At the market level, the new e-commerce law and customs digitization reforms raise the minimum standard for data handling, traceability, and legal responsibility. That will likely pressure smaller carriers that depend on manual or lightly integrated processes. The Vietnam Cross-Border E-commerce Logistics Market is therefore becoming more selective, not because there is one dominant operator, but because compliance and systems investment are rising faster than many smaller firms can match.

Vietnam Cross-Border E-commerce Logistics Industry Leaders

DHL Group

FedEx

United Parcel Service of America, Inc. (UPS)

Viettel Post

Giao Hang Tiet Kiem (GHTK)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: JD.com's 618 Grand Promotion first deployed large-item fulfillment capabilities in Vietnam, Singapore, and Malaysia, recording a doubling of overall order volume year-on-year in the first 52 hours of the promotion; sales of large appliances and furniture increased by more than 7 times year-on-year in Vietnam.

- April 2026: FedEx designated Viettel Post as its National Network Provider in Vietnam effective April 26, 2026, targeting approximately 2 million annual shipments and 26,000+ tonnes of cargo, connecting Vietnam to 220+ countries and territories. This represents the most significant cross-border network restructuring by a global integrator in Vietnam's express market in recent years.

- January 2026: iHerb completed its acquisition of Vitacost from The Kroger Co., strengthening iHerb's health supplement product portfolio and fulfillment network, which supplies Vietnamese consumers across its cross-border DTC channel.

- November 2025: Shopee signed a Memorandum of Understanding with Vietnam's iDEA to launch Shopee EZXports: Vietnam Everywhere, a 2-year initiative to train 2,000 Vietnamese MSMEs, launch a Vietnam Pavilion across Southeast Asian Shopee markets, and roll out a Vietnam Digital Export Week campaign.

Vietnam Cross-Border E-commerce Logistics Market Report Scope

| Foods and Beverages |

| Personal and Household Care |

| Fashion and Lifestyle (Accessories, Apparel, Footwear) |

| Furniture |

| Consumer Electronics and Household Appliances |

| Other Products |

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing, Distribution and Inventory Management | |

| Value-added Services and Others |

| B2C |

| B2B |

| C2C |

| Express |

| Standard |

| Outbound (Exports) | North America |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa | |

| South America | |

| Inbound (Imports) | North America |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa | |

| South America |

| By Product Category | Foods and Beverages | |

| Personal and Household Care | ||

| Fashion and Lifestyle (Accessories, Apparel, Footwear) | ||

| Furniture | ||

| Consumer Electronics and Household Appliances | ||

| Other Products | ||

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing, Distribution and Inventory Management | ||

| Value-added Services and Others | ||

| By Business Model | B2C | |

| B2B | ||

| C2C | ||

| By Delivery Speed | Express | |

| Standard | ||

| By Flow Direction | Outbound (Exports) | North America |

| Europe | ||

| Asia-Pacific | ||

| Middle East and Africa | ||

| South America | ||

| Inbound (Imports) | North America | |

| Europe | ||

| Asia-Pacific | ||

| Middle East and Africa | ||

| South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for Vietnam cross-border e-commerce logistics?

The market is forecast to reach USD 261.03 million by 2031 from USD 192.06 million in 2026, expanding at a 6.33% CAGR over 2026-2031.

Which business model is driving the strongest growth in Vietnam?

B2C is both the largest and fastest-growing model, with 69.26% share in 2025 and a projected 19.12% CAGR through 2031.

Which product category currently contributes the most revenue?

Consumer electronics and household appliances led with 31.26% share in 2025, supported by strong import flows and favorable parcel economics.

Why are value-added services gaining importance in cross-border fulfillment?

Value-added services are projected to grow at an 11.50% CAGR because sellers and platforms increasingly need returns handling, compliance support, and DDP or DDU execution.

What is changing in Vietnam’s policy environment for online cross-border trade?

The 2025 logistics strategy and the 2026 e-commerce law are pushing the sector toward more formal, traceable, and compliance-heavy operating models.

Is Vietnam still more import-led or export-led in cross-border e-commerce logistics?

It is still import-led in current value, with inbound flows at 58.10% share in 2025, but outbound logistics is growing faster at a 7.32% CAGR.

Page last updated on: