Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

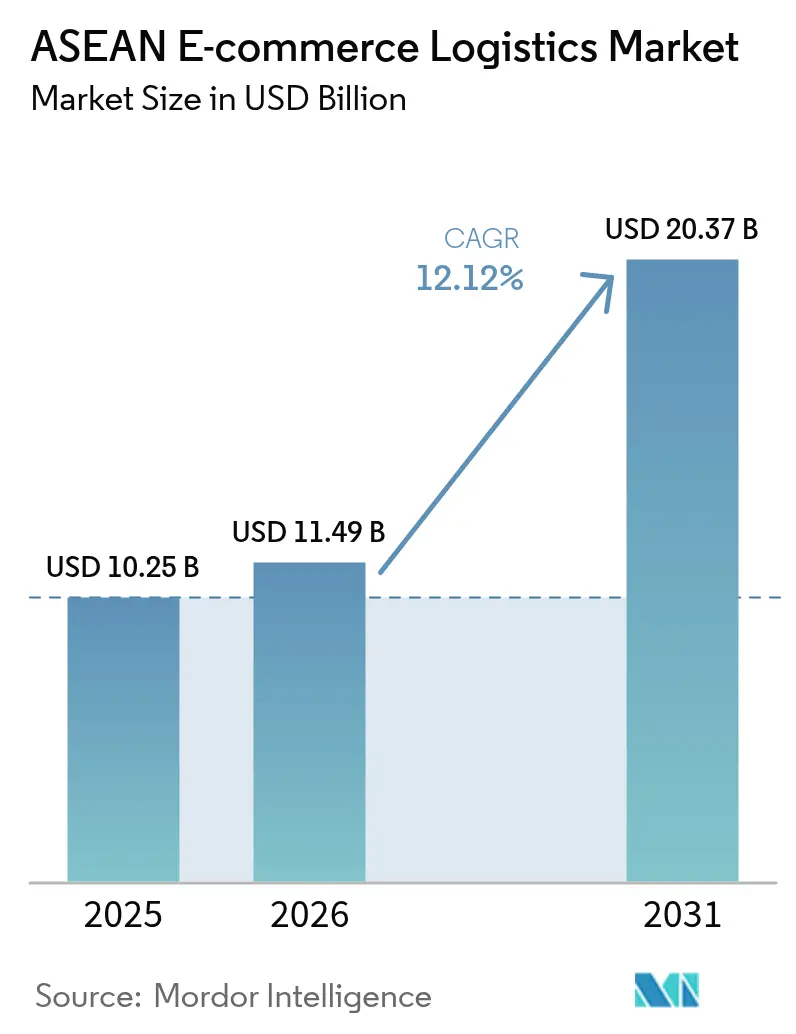

| Base Year Market Size (2025) | USD 10.25 Billion |

| Market Size (2026) | USD 11.49 Billion |

| Market Size (2031) | USD 20.37 Billion |

| Growth Rate (2026 - 2031) | 12.12% CAGR |

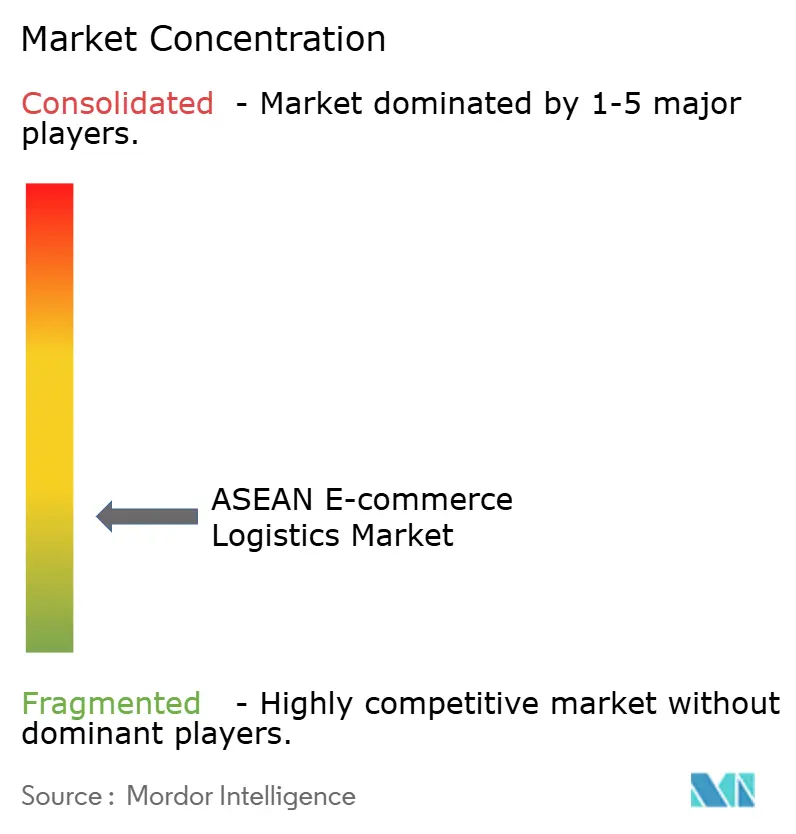

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN E-commerce Logistics Market Analysis by Mordor Intelligence

The ASEAN E-commerce Logistics Market size was valued at USD 10.25 billion in 2025 and estimated to grow from USD 11.49 billion in 2026 to reach USD 20.37 billion by 2031, at a CAGR of 12.12% during the forecast period (2026-2031).

Platform consolidation, social-commerce momentum, and digital-payment ubiquity are accelerating parcel volumes, while infrastructure projects such as Indonesia’s Tol Laut corridor expand multimodal capacity. Same-day and cross-border services are the fastest-rising niches, supported by dark-store networks, AI-driven routing, and the partial roll-out of the ASEAN Single Window. Competitive intensity remains moderate as regional specialists, platform-owned arms, and global integrators battle for share; technology investment and neutral, multi-platform positioning increasingly influence contract awards. Structural headwinds labor shortages, regulatory fragmentation, and urban congestion taxes temper margins even as autonomous warehouses and electric two-wheelers alleviate cost pressures.

Key Report Takeaways

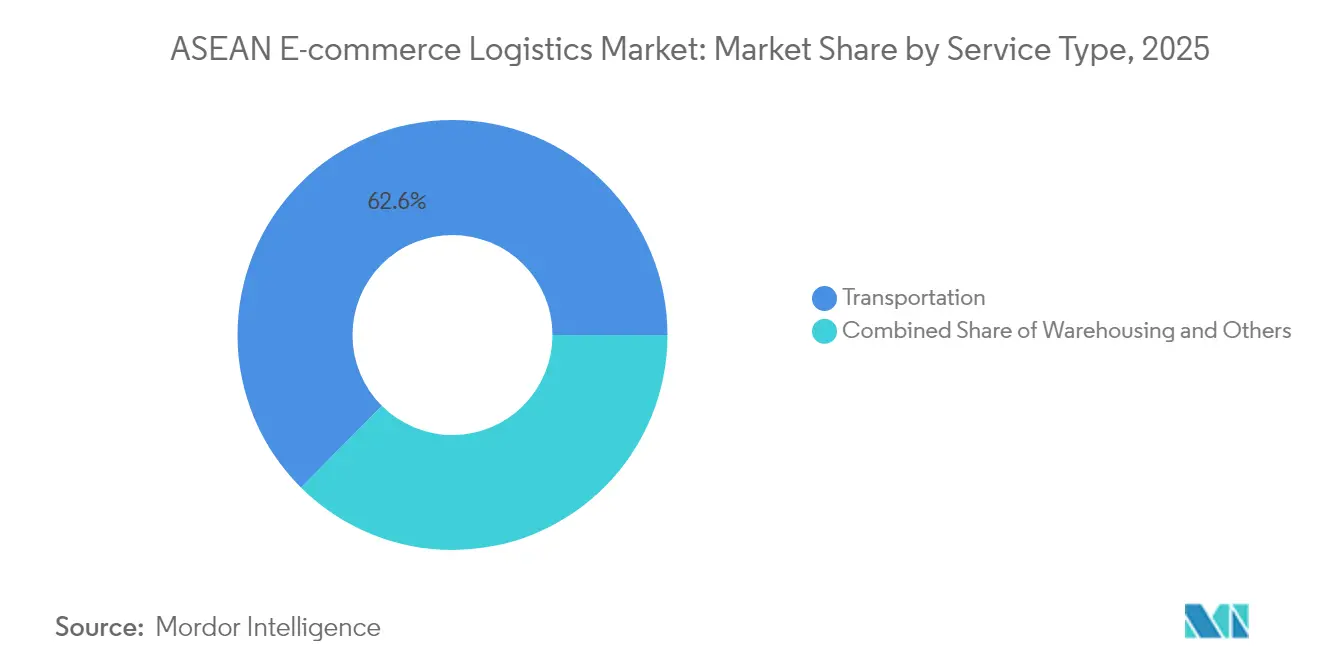

- By service, transportation led with 62.55% of the ASEAN e-commerce logistics market share in 2025.

- Warehousing & fulfillment is projected to expand at an 8.09% CAGR through 2031.

- By business model, B2C held 68.20% share of the ASEAN e-commerce logistics market size in 2025.

- C2C transactions record the highest projected CAGR at 8.77% through 2031.

- By destination, domestic logistics commanded 62.70% share of the ASEAN e-commerce logistics market size in 2025, while cross-border flows are advancing at a 7.03% CAGR.

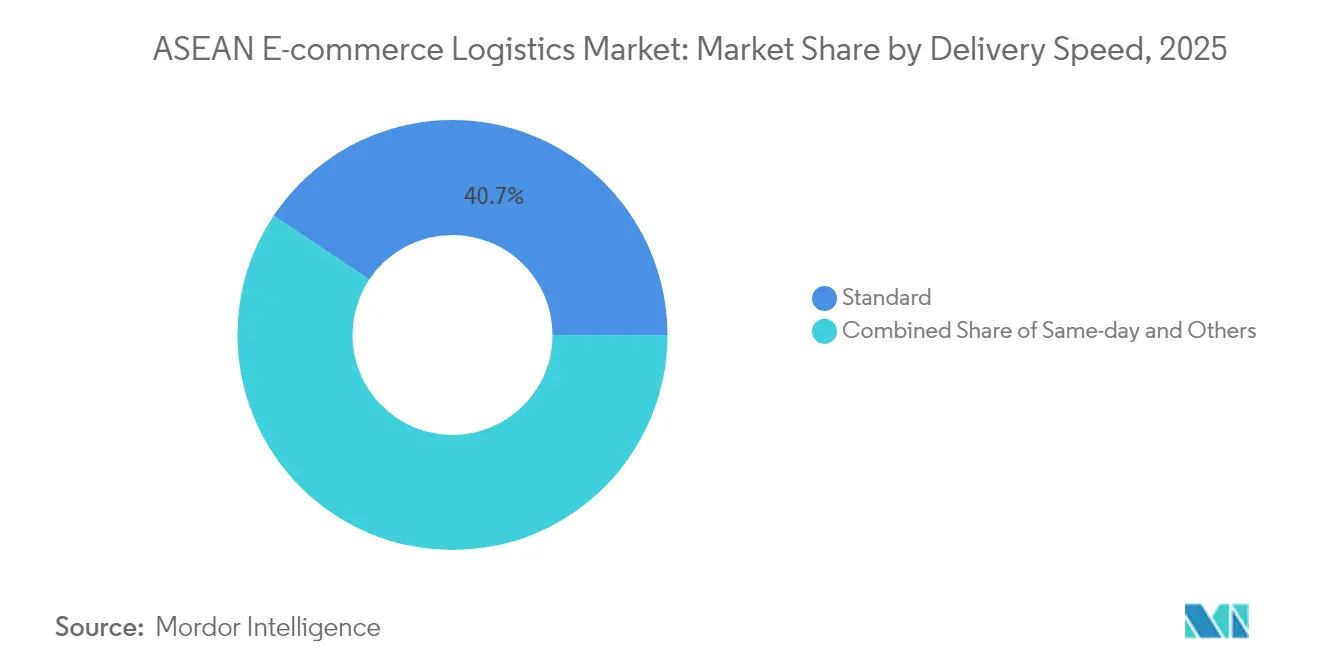

- By delivery speed, same-day fulfillment is growing at 7.39% CAGR through 2031.

- By product category, fashion & lifestyle captured 26.60% of the ASEAN e-commerce logistics market share in 2025; foods & beverages is expanding at 7.80% CAGR.

- Indonesia, the largest country market, accounted for 30.80% share in 2025; Vietnam posts the fastest growth at 6.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN E-commerce Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated growth of ASEAN-based e-commerce marketplaces | 3.2% | Indonesia, Thailand, Vietnam, Philippines | Medium term (2-4 years) |

| Rapid expansion of BNPL & digital wallets boosting checkout-conversion | 2.1% | Global ASEAN, strongest in Singapore, Malaysia | Short term (≤ 2 years) |

| Government-funded national logistics corridors | 1.8% | Indonesia, Vietnam, Thailand | Long term (≥ 4 years) |

| Rising cross-border social-commerce flows within CLMV sub-region | 1.5% | Cambodia, Laos, Myanmar, Vietnam | Medium term (2-4 years) |

| On-demand dark-store networks enabling 2-hour delivery windows | 1.3% | Urban centers: Jakarta, Bangkok, Ho Chi Minh City, Manila | Short term (≤ 2 years) |

| Gen-AI-driven route-optimisation lowering per-parcel cost by >12% | 1.1% | Technology-advanced markets: Singapore, Malaysia, Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Growth of ASEAN-Based E-Commerce Marketplaces

Shopee’s 28.4% social-commerce share and TikTok Shop’s viral selling model concentrate traffic on integrated checkout-logistics rails, shifting parcel flows toward venues that can support split payments and real-time tracking. IDC forecasts regional GMV of USD 325 billion by 2028, with digital payments reaching 94%, eliminating cash-handling delays. The end of exclusive deals such as J&T Express–Shopee Indonesia forces carriers to diversify and invest in neutral APIs that accept orders from multiple storefronts. Cross-border marketplace integration worth USD 14.6 billion by 2028 drives demand for multi-currency settlement and harmonised customs workflows. Logistics providers able to plug simultaneously into several mega-platforms capture disproportionate volume as winner-take-all dynamics escalate[1]“Tol Laut Maritime Logistics Program,” Government of Indonesia, indonesia.go.id.

Rapid Expansion of BNPL and Digital Wallets Boosting Checkout Conversion

Digital wallets already settle 34% of logistics-sector invoices and accelerate order frequency by cutting checkout friction. BNPL widens consumer credit access; transaction-level analysis across 1 billion users links the product to higher basket sizes and merchant acceptance in card-scarce markets. In Indonesia, pay-later schemes lift impulsive fashion purchases, whereas COD persists among risk-averse shoppers, obliging carriers to operate dual workstreams for prepaid and cash segments. Wallet usage is set to pass 50% of global e-commerce by 2025, intensifying working-capital complexity for last-mile firms that settle funds to merchants, couriers, and platforms in near real time[2]“Opening the Black Box of Digital Wallets,” Cong et al., cepr.org.

Government-Funded National Logistics Corridors

Public capex lowers structural bottlenecks across the ASEAN e-commerce logistics market. Indonesia’s Tol Laut maritime network, expanded from 6 to 30 routes, narrows inter-island price gaps by up to 20%. The China-Laos Railway cuts Kunming–Vientiane freight time from three days to under 15 hours, opening new land links for CLMV sellers. Thailand’s land-bridge plan, slated for 2028–2030, could shave two days off Gulf-to-Andaman shipping. Vietnam channels USD 40 billion annually into logistics assets yet still pays logistics costs exceeding 20% of GDP, underscoring the magnitude of unfinished capacity. Private 3PLs leverage state-built corridors to scale at lower capital intensity while expanding rural reach.

Rising Cross-Border Social-Commerce Flows Within CLMV

Social-first platforms turn Cambodia, Laos, Myanmar, and Vietnam into micro-export hubs, unlocking arbitrage on labor and product sourcing. Regional social-commerce GMV may hit USD 42 billion by 2025, outpacing traditional shopping carts. The China-Laos Railway provides an overland option for time-sensitive parcels previously relegated to slower sea freight. Digital wallets and BNPL flatten cross-border payment pain points, while micro-fulfillment centers near border zones shorten cycle times. Logistics firms capturing CLMV flows gain an early stake in an ecosystem still lightly penetrated by global giants[3]“ASEAN Single Window Progress Report,” ASEAN Secretariat, asean.org.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented customs clearance rules across ASEAN single window | -1.8% | Cross-border operations, particularly Indonesia-Malaysia-Thailand corridor | Medium term (2-4 years) |

| Chronic middle and last-mile labour shortages in tier-2/3 cities | -2.3% | Vietnam, Philippines, Indonesia rural areas | Long term (≥ 4 years) |

| Escalating urban congestion taxes raising last-mile costs | -1.2% | Jakarta, Manila, Bangkok | Short term (≤2 years) |

| Elevated logistics cost structures above global benchmarks | -1.4% | Vietnam, Philippines, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Customs Clearance Rules Across ASEAN Single Window

Only nine members exchange ASEAN Customs Declaration Documents, forcing carriers to juggle redundant paperwork that erodes same-day and next-day promises. Vietnam’s 2025 traffic rules lifted logistics costs 10% and cut on-time rates below 90%. SMEs lacking dedicated brokers struggle most, curbing export participation. Divergent requirements from ISO 9001 mandates to country-specific licensing delay broader harmonisation and keep cross-border fulfillment expensive.

Chronic Middle- and Last-Mile Labor Shortages in Tier-2/3 Cities

Vietnam alone needs 2.2 million additional logistics workers by 2030, yet qualified staff meet just 10% of demand. Across ASEAN, 85% of carriers report shortages, forcing overtime premiums that cut margins. Aging dock crews and high churn rates inflate training spend and safety risks. Automation offsets some gaps, but capital constraints delay deployment outside top metros.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Scale Sustains Dominance

Transportation accounts for 62.55% of 2025 revenue, anchoring the ASEAN e-commerce logistics market size amid the archipelago geography of Indonesia and the Philippines. Road fleets leverage trans-Java and pan-Thailand highways to trim line-haul latency, while rail gains share following the China–Laos link that slashes Kunming-Vientiane lead time. Air freight remains the go-to for high-value electronics, and sea lanes support bulk cross-border orders. The ASEAN e-commerce logistics market share of warehousing & fulfillment, though smaller, grows swiftly as dark-store grids inside Jakarta, Bangkok, and Ho Chi Minh City shorten promise windows to two hours. Automated picking lifts throughput 50-60%, and AI slotting blends same-day SKUs with slower movers. Value-added services kitting, custom labels present niche margins as platforms seek differentiated unboxing.

The segment outlook favors transport firms that digitalize fleets, integrate parcel-level visibility, and hedge fuel price swings via electric light-commercial vehicles. Fulfillment operators investing in mezzanine robotics amortize capex over accelerating parcel density. Market entrants may piggyback government corridors rather than replicate network depth, adopting asset-light models that subcontract middle mile while owning customer-facing tech.

By Business Model: B2C Scale Meets C2C Agility

B2C maintains 68.20% of 2025 value thanks to Shopee, Lazada, and Tokopedia scale, underpinning predictable line-haul and hub capacity. Checkout digitalization at 94% removes COD float, simplifying cash cycles. Yet C2C, buoyed by TikTok Shop’s viral engines, logs an 8.77% CAGR, forcing carriers to master doorstep pickup and variable parcel sizing. Same-day SLA expectations transfer platform urgency onto lightly formalized sellers.

Hybrid logistics APIs that accept C2C waybills while reserving space on B2C trunk routes unlock utilisation gains. B2B, though the smallest slice, matures as wholesalers digitize replenishment and experiment with BNPL credit, creating steady pallet flows into provincial depots.

By Destination: Domestic Scale vs. Cross-Border Potential

Domestic lanes represent 62.70% of 2025 revenue, aided by Indonesia’s Tol Laut coastal ferries that narrow price dispersion islands-wide. Jakarta’s congestion tariffs, however, lift city-center delivery cost profiles, nudging carriers toward suburban micro-hubs. Cross-border parcels clock a 7.03% CAGR, powered by the ASEAN e-commerce logistics market size increment tied to intra-SEA shoppers. Partial ASEAN Single Window adoption reduces paperwork yet still mandates manual intervention at several borders, capping speed gains.

Providers that pre-clear duties, integrate multi-currency wallets, and position stock at bonded hubs capture early mover advantage. Fulfillment players combine Malaysia’s free-trade zones with Singapore’s air-cargo links to aggregate demand before final-mile injection in CLMV.

By Delivery Speed: Same-Day Premium Ups the Stakes

Standard (3-5 days) retains 40.65% of shipments as budget-minded consumers accept slower arrivals outside tier-1 cities. Same-day revenue, however, rises at 7.39% CAGR, propped by two-hour grocery promises. The ASEAN e-commerce logistics market size for rapid modes scales as grocers and pharmacy apps subsidize shipping to snag loyalty. Next-day occupies a middle ground, relying on overnight trucking corridors; its growth hinges on highway reliability and night-time driving waivers.

Investments pivot to micro-fulfillment nodes, bike couriers, and AI batching to shave dwell time. Carriers weigh premium tariff upticks against asset-utilisation challenges, especially when weather or road closures strain two-hour commitments.

By Product Category: Fashion Leadership, Food Momentum

Fashion & lifestyle tops 26.60% share, buttressed by large SKU assortments, light weight, and high return rates that spur reverse-logistics opportunities worth USD 947.36 billion globally by 2032. Foods & beverages charts 7.80% CAGR on the back of quick-commerce baskets; cold-chain mileage and leftover shelf life dictate dynamic route sequencing. Personal-care SKUs ride wellness trends, while consumer electronics leverage insured shipping and installation upsells. Furniture, bulky yet margin rich, pushes carriers toward white-glove crews and assembly add-ons, aligning with home-improvement spending in suburban ASEAN.

Geography Analysis

Indonesia’s 30.80% share mirrors its 270 million-strong consumer base and dispersed islands that mandate sea-road-air blends. Tol Laut’s 30 vessels reduce inter-island freight premiums and invite 3PLs to penetrate outer provinces. Congestion taxes in Jakarta, however, nudge operators toward electric bikes exempt from peak-hour surcharges, raising capex but trimming variable cost.

Thailand and Vietnam spearhead growth. Bangkok’s land-bridge vision could bypass the Malacca choke point by 2029, redirecting intra-ASEAN flows through southern seaports. Vietnam, sitting on USD 40-42 billion logistics turnover, endures elevated cost-to-GDP ratios and a 2.2 million-worker gap, propelling automation outlays. Traffic regulations enacted in 2025 lifted cost curves yet catalyzed route-optimisation investments.

Philippines, Malaysia, and Singapore play specialist roles. Metro Manila pushes standard delivery windows beyond 48 hours due to chronic gridlock, but English fluency eases international coordination. Malaysia’s free zones host UPS-Ninja Van’s cross-border sortation, coupling global networks with local last mile. Singapore remains the region’s bonded-hub of choice for high-value electronics and fashion re-exports, commanding premium storage rents yet guaranteeing same-day regional uplift.

Rest-of-ASEAN markets-Cambodia, Laos, Myanmar, Brunei see social-commerce-led orders climb as the China–Laos Railway’s 15-hour run beats traditional trucking. Logistics players that embed customs brokerage and omnichannel APIs into smaller economies position for outsize returns once income levels rise.

Competitive Landscape

The ASEAN e-commerce logistics market exhibits moderate fragmentation. J&T Express’s decision to drop Shopee exclusivity unveiled vulnerability in single-platform reliance and triggered a reshuffle of lane volumes. Ninja Van anchors regional last mile but fights financial strain, evident in 2024 wage delays, as subsidised shipping erodes margins.

Differentiation pivots on tech depth. Providers deploying Gen-AI route optimisation cut per-parcel cost over 12% and uplift on-time rates to 97% in pilot metros. Robotics-rich warehouses process 50% more orders per square foot, allowing fulfillment specialists to underbid manual peers. Cross-border mastery compliance automation, multi-currency billing—emerges as the next frontier, especially with social-commerce merchants seeking frictionless export.

Regulations add gatekeeping layers: ISO 9001 mandates in Singapore and Malaysia restrict entry to smaller couriers, whereas Indonesia favours local licensing and data-hosting rules. Consolidation continues via M&A: Amilo bought Thailand’s Sivadon, CJ Logistics allied with Ninja Van, and UPS partnered Ninja Van in Malaysia to fuse global reach with local know-how. Chinese giants JD Logistics and Cainiao scout ASEAN depots, raising the bar on automation and price transparency.

ASEAN E-commerce Logistics Industry Leaders

J&T Express

Ninja Van

Deutsche Post DHL Group

Shopee Xpress

Lazada Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: J&T Express ended its exclusive partnership with Shopee Indonesia, opening the lane to competing carriers.

- April 2024: CJ Logistics signed a comprehensive pact with Ninja Van to scale cross-border services.

- August 2024: UPS and Ninja Van formed a strategic Malaysian partnership to serve export-oriented SMEs.

- August 2024: Singapore’s Amilo acquired Thailand’s Sivadon Logistics, boosting warehousing footprint.

ASEAN E-commerce Logistics Market Report Scope

E-commerce logistics refers to the transportation service provided to the online retail market. A complete background analysis of the ASEAN e-commerce logistics market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The ASEAN E-commerce Logistics Market is segmented By Service (Transportation, The report covers the ASEAN E-commerce Logistics Market Size and statistics. The market is Segmented By Service (Transportation, Warehousing and Inventory Management, and Value-added Services (Labeling, Packaging, etc.)), Business (B2B and B2C), Destination (Domestic and International/Cross-border), Product (Fashion and Apparel, Consumer Electronics, Home Appliances, Furniture, Beauty and Personal Care Products, and Other Products (Toys, Food Products, etc.)), and Country (Singapore, Thailand, Vietnam, Indonesia, Malaysia, Philippines, and the Rest of ASEAN). The report offers the market size in value terms in USD for all the abovementioned segments.

By Service

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing and Fulfilment | |

| Value-Added Services (Labelling, Packaging, Kitting) |

By Business Model

| B2C |

| B2B |

| C2C |

By Destination

| Domestic |

| Cross-border (international) |

By Delivery Speed

| Same-day (less than 24 h) |

| Next-day (24-48 h) |

| Standard (3-5 days) |

| Others (more than 5 days) |

By Product Category

| Foods and Beverages |

| Personal and Household Care |

| Fashion and Lifestyle (accessories, apparel, footwear) |

| Furniture |

| Consumer Electronics and Household Appliances |

| Other Products |

By Country

| Indonesia |

| Thailand |

| Vietnam |

| Philippines |

| Malaysia |

| Singapore |

| Rest of ASEAN (Cambodia, Laos, Myanmar, Brunei) |

| By Service | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing and Fulfilment | ||

| Value-Added Services (Labelling, Packaging, Kitting) | ||

| By Business Model | B2C | |

| B2B | ||

| C2C | ||

| By Destination | Domestic | |

| Cross-border (international) | ||

| By Delivery Speed | Same-day (less than 24 h) | |

| Next-day (24-48 h) | ||

| Standard (3-5 days) | ||

| Others (more than 5 days) | ||

| By Product Category | Foods and Beverages | |

| Personal and Household Care | ||

| Fashion and Lifestyle (accessories, apparel, footwear) | ||

| Furniture | ||

| Consumer Electronics and Household Appliances | ||

| Other Products | ||

| By Country | Indonesia | |

| Thailand | ||

| Vietnam | ||

| Philippines | ||

| Malaysia | ||

| Singapore | ||

| Rest of ASEAN (Cambodia, Laos, Myanmar, Brunei) |

Key Questions Answered in the Report

What is the current value of the ASEAN e-commerce logistics market?

The market is valued at USD 11.49 billion in 2026 and is projected to reach USD 20.37 billion by 2031.

Which service segment is growing the fastest?

Warehousing & fulfillment leads growth with an 8.09% CAGR as dark-store and automation investments rise.

How fast is cross-border e-commerce logistics expanding?

Cross-border flows are forecast to advance at a 7.03% CAGR, driven by social-commerce integration and customs digitalization.

Why are digital wallets important for logistics operators?

Wallets settle 34% of sector payments, reduce checkout friction, and require carriers to manage real-time fund splits.

Which country shows the highest growth momentum?

Vietnam posts the fastest national CAGR at 6.22%, supported by manufacturing exports and rising domestic GMV.

How does labor availability affect logistics costs?

Chronic shortages, especially in tier-2/3 cities, lift wages and training spend, reducing margins until automation scales.

Page last updated on: