Veterinary Endoscopy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

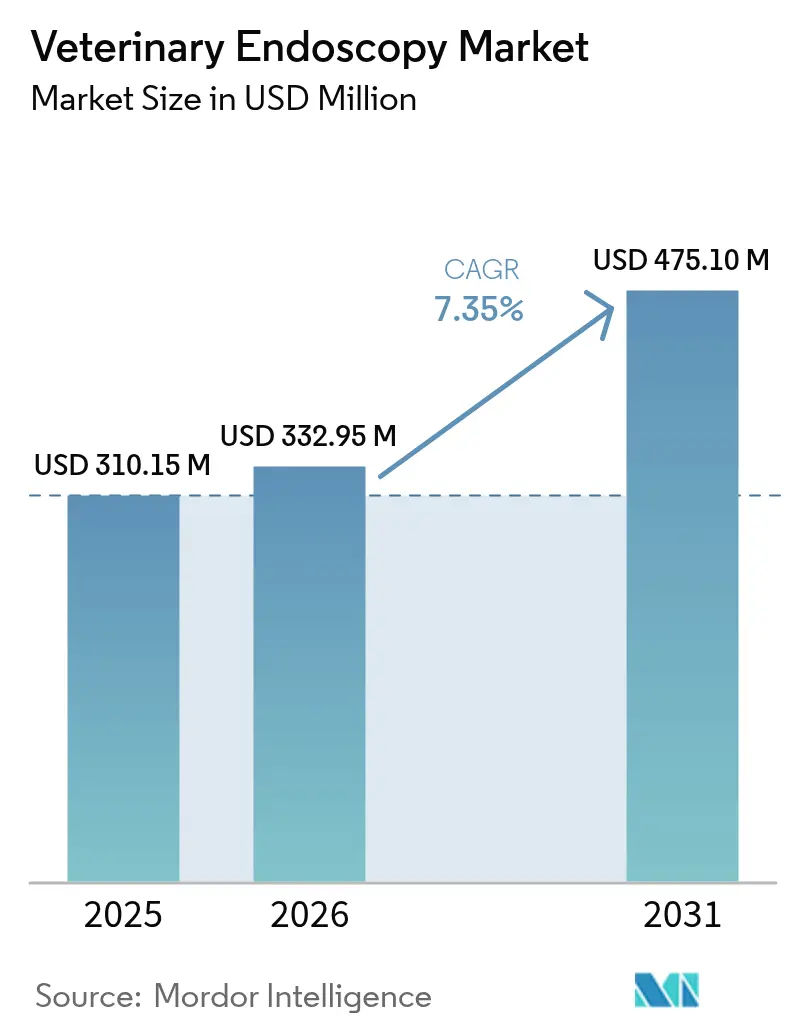

| Market Size (2026) | USD 332.95 Million |

| Market Size (2031) | USD 475.1 Million |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

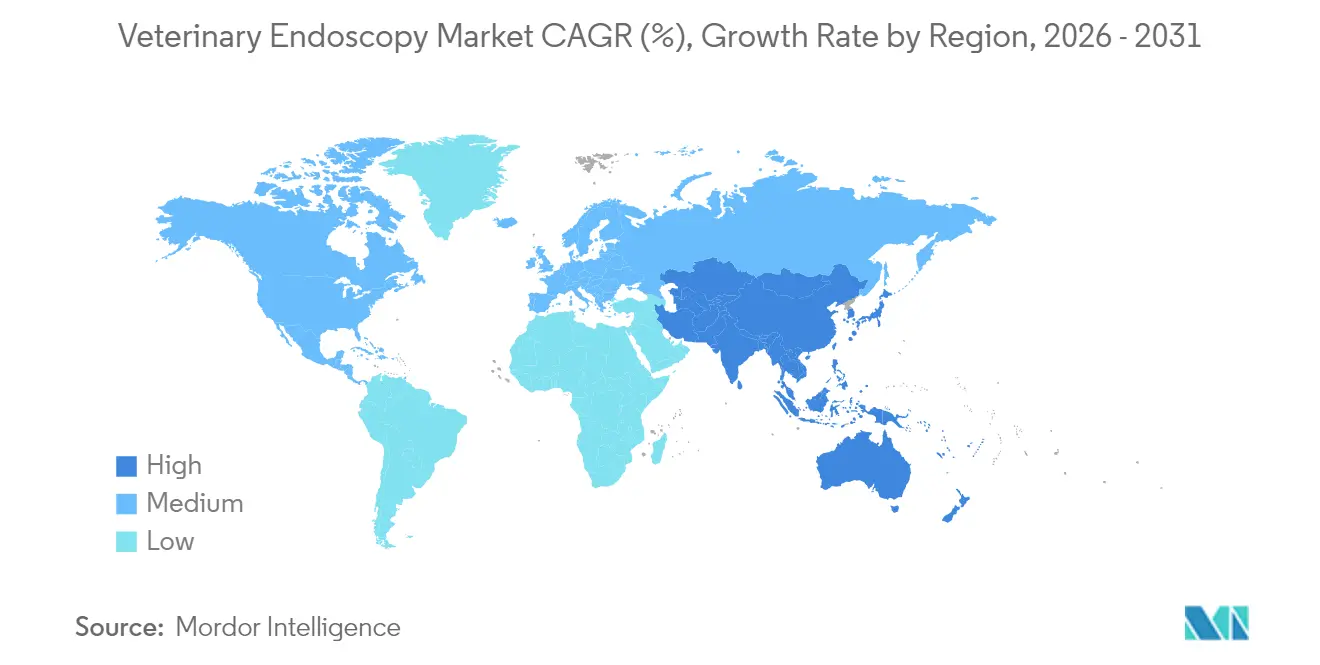

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

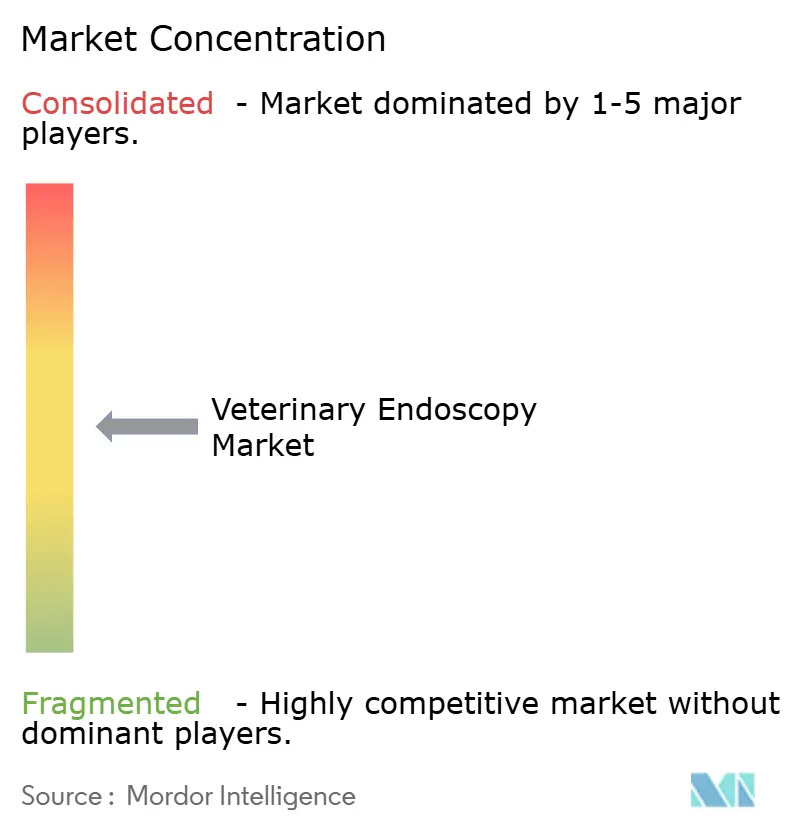

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Endoscopy Market Analysis by Mordor Intelligence

The global veterinary endoscopy market size in 2026 is estimated at USD 332.95 million, growing from 2025 value of USD 310.15 million with 2031 projections showing USD 475.1 million, growing at 7.35% CAGR over 2026-2031. Rising demand for minimally invasive diagnostics, continued miniaturization of equipment, and expanding corporate hospital networks are underpinning this steady expansion of the veterinary endoscopy market. Flexible video systems remain the technology of choice for most companion-animal and equine procedures, yet capsule devices are carving out rapid adoption niches as smaller practices seek anesthesia-free options. Regionally, North America benefits from deep specialty referral networks and high insurance penetration, while Asia-Pacific’s escalating pet ownership and disposable income are propelling the fastest regional CAGR. Competitive momentum is intensifying as diversified human-device majors and veterinary-focused specialists vie for share, but a shortage of skilled endoscopists still constrains the full potential of the veterinary endoscopy market.

Key Report Takeaways

- By product type, flexible video endoscopes commanded 45.30% revenue in 2025; capsule systems are projected to grow at an 11.2% CAGR through 2031.

- By procedure, diagnostics held 63.40% of the veterinary endoscopy market share in 2025, while therapeutic interventions are forecast to expand at a 10.1% CAGR to 2031.

- By application, gastrointestinal procedures captured 56.30% of the veterinary endoscopy market size in 2025 and orthopedic/arthroscopy is advancing at a 11.6% CAGR through 2031.

- By animal type, companion species accounted for 68.20% of 2025 revenue; bovine sub-segments lead livestock growth at a 9.3% CAGR between 2026-2031.

- By end user, hospitals and referral clinics contributed 60.40% of global revenue in 2025; ambulatory centers represent the fastest-growing channel with a 9.8% CAGR to 2031.

- By geography, North America led with a 37.60% share of 2025 global revenue, while Asia-Pacific is projected to post a 9.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Endoscopy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing GI & respiratory disease burden | +2.1% | Global, higher in North America & Europe | Medium term (2-4 years) |

| Rising pet ownership & humanization | +1.8% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Technology miniaturization & HD imaging | +1.5% | Global, early adoption in North America & Europe | Medium term (2-4 years) |

| Tele-endoscopy & cloud image platforms | +1.2% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Veterinary hospital consolidation | +1.0% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Gastrointestinal and Respiratory Disorders

Growing incidence of chronic enteropathies, inflammatory bowel disease, and lower airway disease is prompting veterinarians to adopt endoscopy as first-line diagnostics. Practices report measurably higher diagnostic yields versus radiography; one study recorded a 37% uptick in definitive GI diagnoses when endoscopy was deployed. Prolonged companion-animal lifespans also expose more animals to age-related GI pathologies, further swelling procedure volumes. Large-animal practitioners increasingly use upper airway endoscopy for racehorses and bronchoscopy for dairy herds, broadening demand beyond companion clinics. Together, these clinical trends are raising throughput and justifying equipment investment across the veterinary endoscopy market.

Pet Humanization and Premium Care Spend

Households without children are channeling discretionary income toward advanced companion-animal healthcare, reinforcing willingness to pay for endoscopic diagnostics and minimally invasive therapy. Morgan Stanley projects annual household pet outlays to hit USD 1,733 by 2030, with veterinary services the fastest-expanding line item[1]Morgan Stanley, “Pet Care Industry Outlook for 2030,” morganstanley.com. High-definition video and capsule modalities align well with owner preferences for gentle, low-scarring interventions. The converging influence of insured procedures and third-party financing platforms is also reducing upfront cost sensitivity, allowing specialty centers to market comprehensive endoscopic packages. Consequently, pet humanization continues to boost procedure frequency and revenue across the veterinary endoscopy market.

Technological Miniaturization Expanding Accessibility

Rapid reductions in scope diameter—now sub-3 mm for certain flexible units—permit safe navigation inside small mammals, birds, and reptiles. AnX Robotica’s NaviCam XS capsule is 44% smaller than prior iterations, offering smoother transit through narrow GI tracts. HD optical chips paired with LED light sources deliver mucosal detail once reserved for human systems, helping practitioners flag premalignant lesions. Small-form devices lower anesthesia requirements and fit modest clinic footprints, bringing the veterinary endoscopy market to previously underserved rural or exotic-focused practices.

Tele-Endoscopy and Cloud-Based Image Management

High-bandwidth networks now stream live procedure video to board-certified specialists for on-the-fly consults. Integrated PACS solutions archive cases to cloud repositories, allowing asynchronous review and AI-assisted pattern recognition. Early adopters report trimmed diagnosis times and enhanced training pathways for novice clinicians. The incremental revenue potential and educational value of tele-mentoring are accelerating uptake, especially in regions where local expertise is scarce.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & lifecycle costs | -1.7% | Global, heavier in emerging markets | Long term (≥ 4 years) |

| Shortage of skilled endoscopists | -1.4% | Global, acute in Asia-Pacific & MEA | Medium term (2-4 years) |

| Sterilization and infection-control challenges | -0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Equipment Costs Limiting Adoption

Entry-level HD systems can exceed USD 45,000, a hurdle for small or rural clinics battling declining foot traffic and thinning margins[2]American Veterinary Medical Association, “Less Foot Traffic at Veterinary Practices Spells Declining Revenue,” avma.org. Service contracts, scope repair, and specialty cleaning units add to lifecycle outlays, lengthening payback periods. Emerging-market practices face even steeper import duties and limited financing, stalling penetration of the veterinary endoscopy market. Vendors offering pay-per-use or leasing models are attempting to ease adoption, yet overall budget constraints remain a strong drag on market growth.

Veterinary Endoscopist Shortage

Advanced endoscopic techniques demand proficiency beyond standard curricula, and global training pipelines lag demand. Relief veterinarians now represent 9.1% of the U.S. workforce, complicating the formation of steady endoscopy teams. Emerging markets suffer compounded scarcity, forcing referral bottlenecks and long wait times. Teaching hospitals are expanding residency slots, but the lag in graduating qualified specialists continues to cap procedure volumes across the veterinary endoscopy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flexible Dominance with Capsule Upsurge

Flexible video systems delivered 45.30% of 2025 revenue, underscoring their versatility in GI, respiratory, and urogenital work. HD chip-on-tip optics provide crisp imagery, while variable stiffness insertion tubes improve maneuverability. Correspondingly, the segment captured the largest slice of the veterinary endoscopy market share. Capsule modules, although accounting for lower absolute revenue, post an 11.2% CAGR as clinics embrace anesthesia-free imaging for cats, small dogs, and exotics. The veterinary endoscopy market size for capsule devices is on track to more than double by 2030. Rigid scopes retain popularity in arthroscopy owing to durable optics and tactile control, and robot-assisted units, though nascent, attract premium equine centers exploring remote joystick manipulation.

Complementary visualization consoles and integrated AI analytics represent the second-largest revenue pool, driven by system upgrades rather than new room builds. Accessory sales—biopsy forceps, snares, retrieval baskets—generate high-margin recurring income for OEMs. The segment benefits as therapeutic procedure counts climb, knitting consumable pull-through to each intervention.

By Procedure: Diagnostics Prevail, Therapies Accelerate

Diagnostic work comprised 63.40% of global cases in 2025, supported by superior mucosal assessment over radiography. High tissue-sampling accuracy reduces exploratory surgeries and informs targeted pharmacologic regimens, reinforcing demand. Still, therapeutic endoscopy is the momentum engine, projected to log a 10.1% CAGR through 2031 as scope channels widen and accessory toolkits diversify. Stricture dilations, polyp resections, and foreign-body retrievals now performable in a single anesthetic window drive client acceptance. Combined diagnostic-therapeutic workflows compress visit counts, appealing to busy pet owners and reducing stress on animals. Manufacturers responding with torque-stable overtubes and laser-compatible working channels stand to capture the fastest-growing pocket of the veterinary endoscopy market.

By Application: GI Stronghold, Orthopedic Breakout

Gastrointestinal indications represent 56.30% of 2025 procedures, cementing the segment’s authority within the veterinary endoscopy market size. Chronic vomiting, weight loss, and dysphagia continue to channel referrals for esophagoscopy and colonoscopy. Meanwhile, orthopedic arthroscopy is expanding faster than any other niche, propelled by skeletal disease management in canine athletes and equine performance horses. A 11.6% projected CAGR mirrors improvements in 2.4 mm arthroscopes and portal access kits that protect neurovascular structures. ENT and respiratory uses maintain respectable volume due to recurrent laryngeal neuropathy diagnostics in horses and chronic rhinitis in brachycephalic dogs. Urogenital, ophthalmic, and neurologic subspecialties remain smaller but rise steadily as device miniaturization keeps lowering anatomical barriers.

By Animal Type: Companion Primacy, Livestock Catch-Up

Companion animals yielded 68.20% of 2025 turnover, with canines the single largest sub-segment given breed-specific GI disorders and larger body size that eases scope navigation. Feline volumes are stabilizing as 5 mm scopes and CO₂ insufflation mitigate airway and abdominal constraints. Within livestock, bovine applications headline at a 9.3% CAGR on the back of high-value breeding cows and dairy productivity optimization. Equine work, straddling companion and production, commands premium procedure pricing for airway endoscopy and joint inspection. Poultry and small ruminant procedures remain niche but gain research traction.

By End User: Hospital Leadership, Ambulatory Surge

Hospitals and referral centers captured 60.40% of 2025 sales, leveraging concentrated caseloads to fund multi-tower endoscopy suites. Consolidators equip flagship hubs, then funnel satellite clinic referrals, locking in utilization. Yet ambulatory and specialty centers sprout rapidly, projected to outpace hospital growth rates at 9.8% CAGR. Focused procedure capacity and lower overhead support competitive pricing, drawing elective arthroscopies and capsule studies away from general hospitals. Academic institutes hold a substantial stake as technique incubators, helped by industry donations and grant funding for novel device validation.

Geography Analysis

North America contributed 37.60% of 2025 global revenue, cementing regional supremacy for the veterinary endoscopy market. High pet insurance uptake and the world’s densest population of diplomate-level specialists sustain premium procedure demand. U.S. referral hospitals spearhead adoption of capsule and 4K imaging, while Canadian clinics lean on university affiliations for complex case overflow. Mexico’s urban corridors exhibit double-digit growth as middle-income households pivot toward Western pet-care norms.

Europe ranks second by value, buttressed by stringent welfare regulations and long-established referral networks. Germany’s engineering pedigree supports local OEM production, driving early adoption of robotic articulating scopes. The United Kingdom combines strong pet-ownership culture with robust specialty certification, fostering high per-capita procedure volumes. Mediterranean countries lag Northern peers but close gaps swiftly as specialty hospitals proliferate.

Asia-Pacific is the locomotive of global growth, slated for a 9.1% CAGR through 2031. China’s expanding middle class elevates pet medical spend, stimulating multi-site hospital chains that can amortize endoscope investments. Japan showcases advanced technique maturity, while India’s growth stems from a low base but benefits from rising urban pet populations and Western educational collaborations. Australia and South Korea sustain high-quality benchmarks, but intra-regional disparity persists as rural sectors remain underserved.

South America and the Middle East & Africa represent smaller shares yet register healthy growth as veterinary colleges upgrade curricula and corporates enter metropolitan markets. Equipment donation programs and tele-endoscopy partnerships mitigate specialist shortages, further unlocking latent demand.

Competitive Landscape

The veterinary endoscopy market features moderate fragmentation, with top suppliers controlling significant global revenue, leaving ample headroom for niche innovators. Karl Storz leverages deep optics heritage and a broad veterinary catalog to preserve lead share. Olympus repurposes human-clinical 190-series technology into animal-specific bundles, emphasizing image quality and waterproof durability. Medtronic targets high-acuity centers with slimline colonoscopes incorporating hemostasis accessories. Biovision and Dr. Fritz differentiate through veterinary-purpose designs, lighter handpieces, and exotic-species adapters.

Strategic priorities tilt toward turnkey solution sales covering consoles, scopes, disposables, training, and service contracts. OEMs forge alliances with teaching hospitals to beta-test AI diagnostic modules and capsule propulsion systems. Corporate consolidators, now the largest buyers, pressure vendors for multi-year fleet agreements at volume pricing. White-space entrants focus on pocket-scope kits for wildlife and zoo use cases, and on cloud platforms enabling remote proctoring. Overall, rivalry intensifies on image clarity, channel diameter, and ownership economics rather than pure hardware differentiation.

Veterinary Endoscopy Industry Leaders

Eickemeyer Veterinary Equipment

Olympus Corporation

Steris PLC

Dr. Fritz Endoscopy GmbH

Biovision Veterinary Endoscopy LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AnX Robotica released NaviCam XS, NaviCam XST, and ESView 3.0, introducing a capsule 44% smaller than existing models for smoother veterinary GI transit.

- October 2024: VetORSolutions listed HD endoscopy among top surgical advances, citing reduced recovery time and better visualization.

Global Veterinary Endoscopy Market Report Scope

As per the scope of the report, an endoscope is a device comprising a flexible tube with a video camera attachment inserted into the stomach or any other part of the body through the mouth or colon. In most cases, endoscopy is performed for diagnostic purposes, such as visualization and sampling abnormalities. However, this device can be used for therapeutic purposes, termed interventional endoscopy. The Veterinary Endoscopy market is Segmented by Product Type (Capsule Endoscopes, Flexible Endoscopes, Rigid Endoscopes, Robot-Assisted Endoscopes), Animal Type (Companion and Livestock), End User (Veterinary Hospitals, Academic Institutes, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Endoscopes | Capsule |

| Flexible Video | |

| Rigid | |

| Robot-assisted | |

| Visualization & Imaging Systems | |

| Accessories & Consumables |

| Diagnostic |

| Therapeutic / Interventional |

| Gastrointestinal |

| Respiratory & ENT |

| Urogenital |

| Orthopedic / Arthroscopy |

| Others |

| Companion Animals | Canine |

| Feline | |

| Equine | |

| Livestock | Bovine |

| Porcine | |

| Poultry | |

| Ovine/Caprine |

| Veterinary Hospitals & Referral Clinics |

| Ambulatory & Specialty Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Endoscopes | Capsule |

| Flexible Video | ||

| Rigid | ||

| Robot-assisted | ||

| Visualization & Imaging Systems | ||

| Accessories & Consumables | ||

| By Procedure | Diagnostic | |

| Therapeutic / Interventional | ||

| By Application | Gastrointestinal | |

| Respiratory & ENT | ||

| Urogenital | ||

| Orthopedic / Arthroscopy | ||

| Others | ||

| By Animal Type | Companion Animals | Canine |

| Feline | ||

| Equine | ||

| Livestock | Bovine | |

| Porcine | ||

| Poultry | ||

| Ovine/Caprine | ||

| By End User | Veterinary Hospitals & Referral Clinics | |

| Ambulatory & Specialty Centers | ||

| Academic & Research Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global veterinary endoscopy market in 2026?

It stands at USD 332.95 million, with projections of USD 475.1 million by 2031.

What CAGR is forecast for veterinary endoscopy through 2031?

The market is expected to grow at a 7.35% CAGR over 2026-2031.

Which product dominates current sales?

Flexible video endoscopes lead with 45.30% of 2025 revenue.

Which region shows the fastest growth?

Asia-Pacific is projected to record a 9.1% CAGR between 2026 and 2031.

Why are therapeutic endoscopy procedures growing quickly?

Expanded toolkits now allow minimally invasive retrievals, resections, and dilations, lifting therapeutic volumes at a 10.1% CAGR.

What is the biggest barrier for small clinics adopting endoscopy?

High upfront equipment costs and ongoing maintenance obligations remain the primary hurdle.

Page last updated on: