Veterinary Parasiticides Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

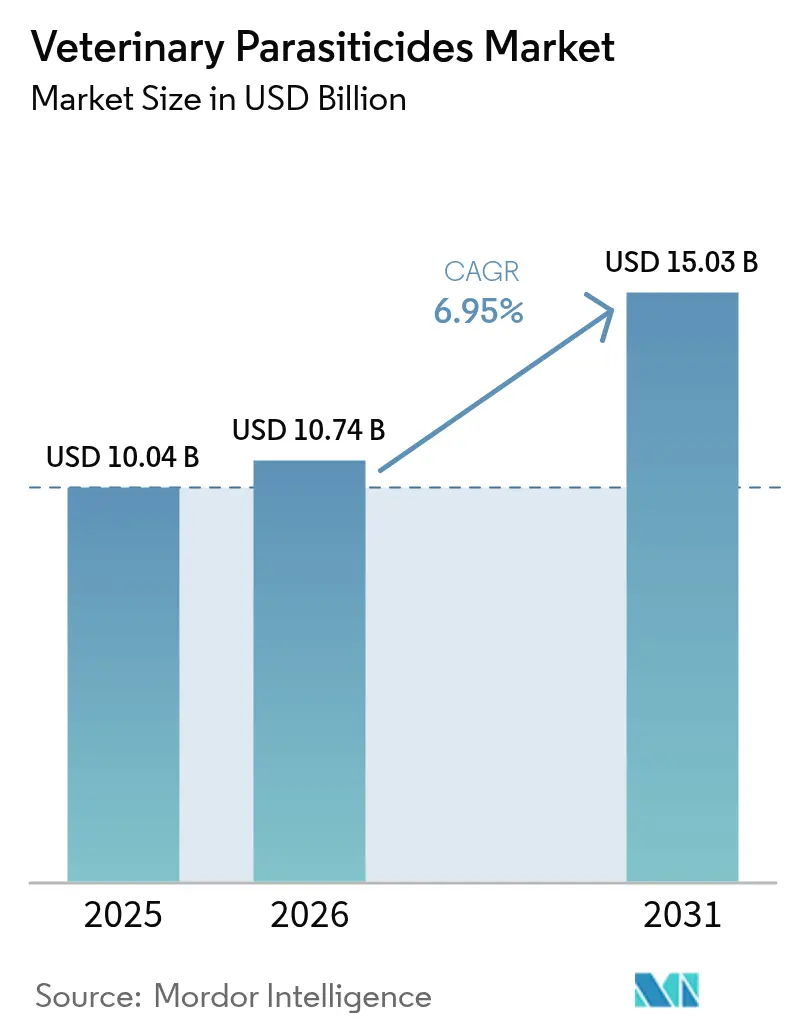

| Market Size (2026) | USD 10.74 Billion |

| Market Size (2031) | USD 15.03 Billion |

| Growth Rate (2026 - 2031) | 6.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Parasiticides Market Analysis by Mordor Intelligence

The veterinary parasiticides market size was valued at USD 10.04 billion in 2025 and estimated to grow from USD 10.74 billion in 2026 to reach USD 15.03 billion by 2031, at a CAGR of 6.95% during the forecast period (2026-2031). Robust demand stems from rising pet ownership, climate-driven parasite range expansion, and steady livestock productivity investments. Regulatory approvals for broad-spectrum tablets and long-acting injectables, long-acting treatment protocols, and raise compliance. Digital diagnostics guide precise therapy selection, while emerging generic competition follows the macrocyclic-lactone patent's expiration. Resistance threats and stricter environmental evaluations temper growth but accelerate innovation in novel modes of action, delivery systems, and combination products across the veterinary parasiticides market.

Key Report Takeaways

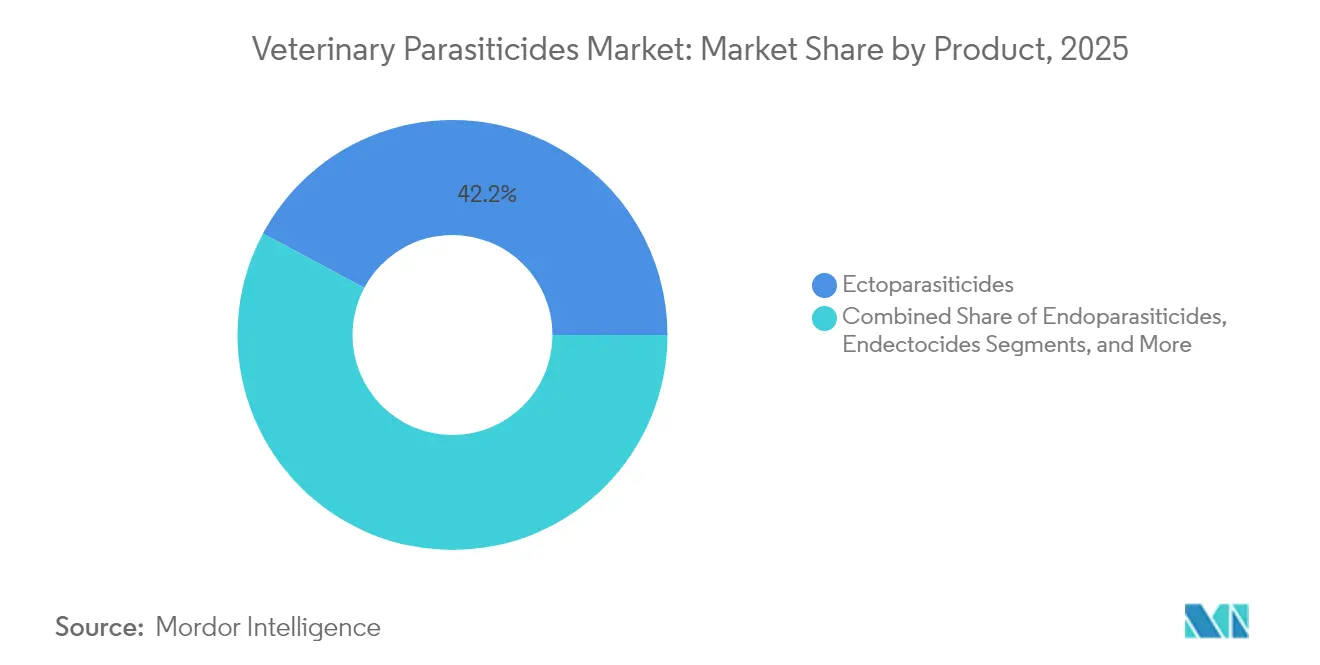

- By animal type, companion animals led with 57.62% revenue share in 2025; the dogs segment is projected to expand at 10.12% CAGR through 2031.

- By product type, ectoparasiticides held 42.18% revenue share in 2025; combination therapies are forecast to grow at 10.78% CAGR to 2031.

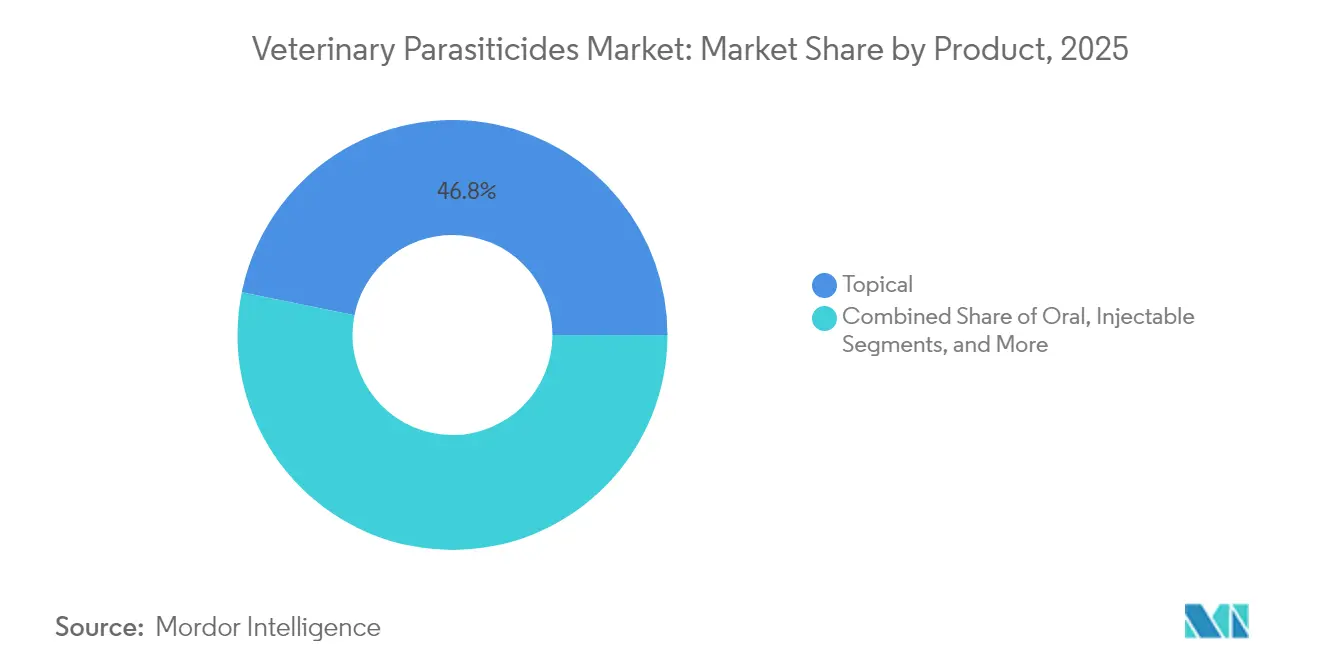

- By mode of administration, topical spot-ons accounted for 46.82% of the veterinary parasiticides market share in 2025, while long-acting injectables are advancing at a 12.18% CAGR through 2031.

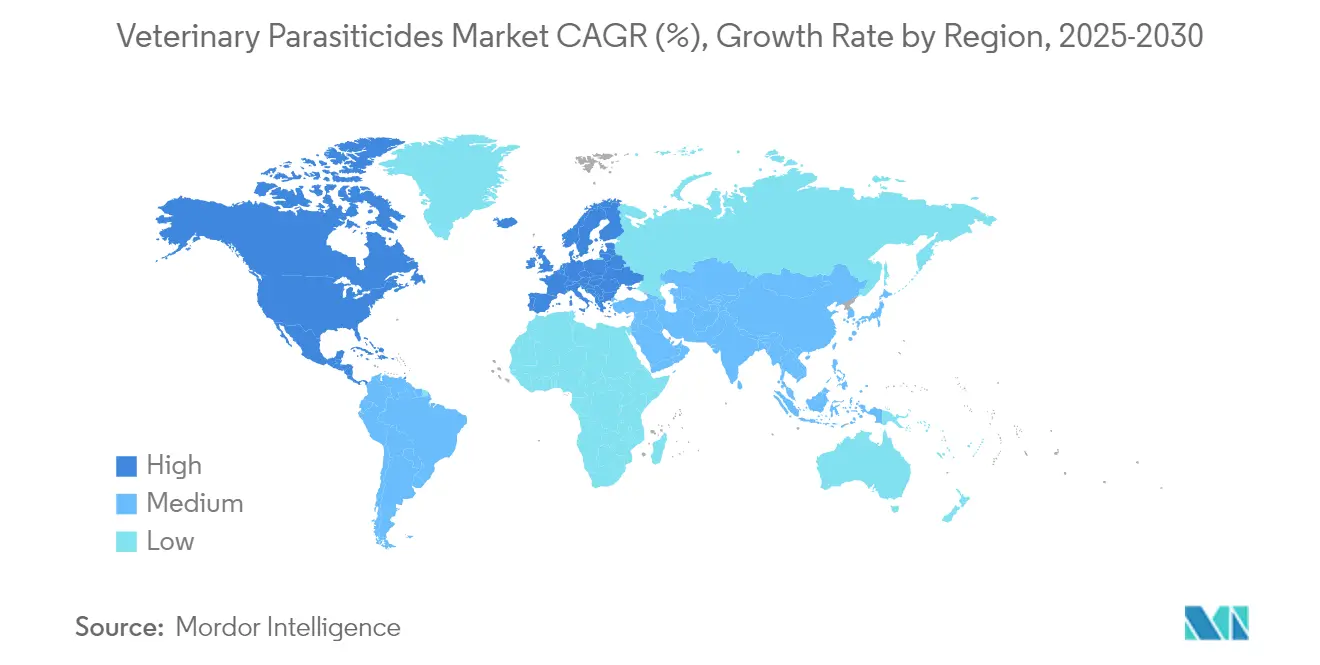

- By region, North America commanded 34.62% revenue share in 2025; Asia Pacific is anticipated to register an 8.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Parasiticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of food-borne & zoonotic infections | +1.20% | Global; higher in Asia Pacific and Africa | Medium term (2-4 years) |

| Growing companion-animal adoption & humanization | +1.80% | North America and Europe core; expanding to APAC | Long term (≥ 4 years) |

| Increasing animal-health expenditure in emerging economies | +1.50% | Asia Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Macrocyclic-lactone patent expiries unlocking generics | +0.90% | Global | Short term (≤ 2 years) |

| Adoption of long-acting injectable & combo therapies | +1.10% | North America and Europe; spill-over to APAC | Medium term (2-4 years) |

| Climate-change driven expansion of parasite habitats | +0.80% | Global; acute in temperate regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Food-Borne & Zoonotic Infections

Zoonotic transmission elevates demand for preventive products as public health agencies integrate One Health priorities. Echinococcus multilocularis spread in North American canids raises human risk, driving mandatory treatment protocols. Climate change amplifies vector survivability, with Leishmania infantum transmission risk forecast to rise 71.6% in Iberia by 2060.[1]Frontiers in Veterinary Science, “Projected Expansion of Leishmania infantum Risk,” frontiersin.orgAuthorities respond with enhanced surveillance and compulsory deworming in high-risk herds. Preventive parasiticides prove more economical than outbreak management, securing long-term uptake in the veterinary parasiticides market.

Growing Companion-Animal Adoption & Humanization

Pet owner’s view pets as family members and prioritize premium preventive care. An Elanco survey found 94% of dog owners favor proactive intestinal worm treatment. The trend boosts combination products that cover internal and external parasites in a single dose. Telemedicine supports tailored regimens, and palatable chewables meet user expectations. Manufacturers improve taste, packaging, and digital engagement, lifting average selling prices across the veterinary parasiticides market.

Increasing Animal-Health Expenditure in Emerging Economies

Rising disposable income and expanding middle classes lift preventive care spending. China’s pet medical sector reached CNY 640 billion (USD 89.6 billion) in 2023, growing 17.43% year on year. Government food-safety programs promote livestock parasite control, while better distribution opens rural markets. Younger demographics in Asia Pacific sustain long-range demand, propelling regional growth in the veterinary parasiticides market.

Macrocyclic-Lactone Patent Expiries Unlocking Generics

Ivermectin’s expiry fostered price-competitive generics; upcoming cliffs for afoxolaner and fluralaner will repeat the pattern. Generic entry typically trims treatment costs by 30-50%, widening access in cost-sensitive regions. Regulators apply VICH harmonization to speed approvals.[2]Federal Register, “VICH Harmonization Activities,” federalregister.gov Innovators pivot to new chemistries and multi-mode products to preserve margins, sharpening product differentiation within the veterinary parasiticides market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Multi-Jurisdictional Regulatory Approvals | -0.80% | Global, with highest impact in EU & North America | Medium term (2-4 years) |

| Escalating Resistance To Existing Active Ingredients | -1.20% | Global, with acute impact in intensive farming regions | Short term (≤ 2 years) |

| High R&D Cost Versus Price Ceilings In Livestock Sector | -0.60% | Global, with higher impact in developing economies | Medium term (2-4 years) |

| Channel Shift To E-Commerce Squeezing Veterinary Markup | -0.40% | North America & Europe core, expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Jurisdictional Regulatory Approvals

Fragmented requirements delay launches by 18-24 months despite FDA-EMA parallel advice initiatives. Environmental risk assessments now examine dung-beetle and aquatic toxicity, raising data burdens.[3]Food and Drug Administration, “Approval of Credelio Quattro,” fda.gov Proposed US labeling rules may increase compliance costs for legacy products. Smaller firms face disproportionate hurdles, which could consolidate power among large players in the veterinary parasiticides industry.

Escalating Resistance to Existing Active Ingredients

Merck Animal Health recorded sub-90% efficacy in 76.5% of pour-on dewormer tests from 600 farms. Multidrug-resistant nematodes compel costly combination protocols and reduce single-agent volumes. Equine guidelines now recommend targeted therapy based on fecal counts extension.uga.edu. R&D budgets shift toward new modes of action and diagnostics that slow resistance, exerting cost pressure across the veterinary parasiticides market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combination Therapies Lead Innovation

Ectoparasiticides captured 42.18% of the veterinary parasiticides market share in 2025, thanks to their frontline role against ticks and fleas. Combination tablets are the fastest-growing segment at 10.78% CAGR because they merge internal and external parasite control in one dose. The veterinary parasiticides market benefits from the FDA approval of Credelio Quattro, which protects against six parasites in a single chewable. Endoparasiticides battle mounting resistance, especially in livestock. Endectocides hold a hybrid niche yet face competition from broader-spectrum newcomers. Environmental stewardship drives interest in botanical options, while nanotechnology improves solubility for hard-to-dissolve compounds, widening the innovation funnel for the veterinary parasiticides market.

The shift toward biologicals remains modest due to regulatory complexity and variable field efficacy. Still, formulations that spare dung fauna gain regulatory favor in Europe. Developers explore modes that maintain refugia populations to mitigate resistance escalation. Investment in novel actives rises as generic pressure bites into pricing for aging macrocyclic lactones. The overall trend positions combination therapies as a cornerstone for long-term growth within the veterinary parasiticides market.

By Animal Type: Companion Animals Drive Premium Growth

Companion animals delivered 57.62% of 2025 revenue, reflecting the humanization wave and greater veterinary spend per pet. Within this cohort, dogs headline expansion with a 10.12% CAGR as owners seek simplified multi-parasitic coverage. Livestock customers focus on cost-efficient control but now adopt combination dewormers to combat resistance, especially in cattle herds. The veterinary parasiticides market size for canine applications is predicted to rise steadily, given premiumization and increasing adoption rates.

In poultry, FDA-approved SAFE-GUARD AQUASOL addresses backyard flock health and broadens the ruminant-heavy portfolio feedstuffs.com. Swine and sheep operations employ targeted, selective treatment to balance efficacy with stewardship. Cat health progresses at a measured pace due to species-specific safety hurdles, yet increased indoor pet numbers boost demand. Population and diet shifts in Asia Pacific keep food-producing animals a crucial revenue pillar, ensuring balanced growth across the veterinary parasiticides market.

By Mode of Administration: Injectable Innovation Accelerates

Topical held 46.82% of 2025 revenue due to user familiarity and rapid kill profiles. Long-acting injectables outpaced all other formats with a 12.18% CAGR, spearheaded by ProHeart 12’s year-long coverage that removes monthly compliance gaps. The veterinary parasiticides market size for injectables is projected to expand as microsphere and depot technologies mature and gain regulatory acceptance.

Oral chews command owner preference for ease and palatability, prompting heavy flavoring investment. Environmental scrutiny of topical residues drives reformulation to minimize aquatic toxicity. Transdermal patches and implants progress in R&D pipelines, promising smoother plasma profiles. Oral combo products flex formulation versatility, whereas injectable combos face release-rate synchronization challenges. Together, these dynamics diversify administration choices within the veterinary parasiticides market.

By End User: Channel Disruption Reshapes Distribution

Veterinary clinics remain pivotal, with 53.6% of dog owners buying medications directly from practices in 2024. Yet e-commerce grows as Amazon and Tractor Supply scale online pet pharmacies, compressing price points. Farms prioritize bulk efficacy, buying through cooperatives and wholesaler channels. The veterinary parasiticides industry adapts with hybrid models where practices advise and online partners fulfill, maintaining professional oversight while meeting consumer convenience.

Prescription mandates protect some sales from direct retail competition, though over-the-counter sectors feel pressure. Telehealth platforms integrate diagnostics, enabling physicians to approve refills digitally. Robust demand data help manufacturers refine geographic targeting, yet channel fragmentation complicates sales crediting. Ultimately, multi-channel fluency will underpin future success in the veterinary parasiticides market.

Geography Analysis

North America generated 34.62% of 2025 revenue owing to high pet ownership, premium care adoption, and supportive regulatory paths. Coordinated FDA–Health Canada reviews streamline new product launches, while climate change lengthens parasite seasons in northern states. E-commerce advances shift purchasing toward online pharmacies, but veterinary practices retain influence through prescription authority. Premium combination tablets and annual injectables anchor revenue resilience in the region’s veterinary parasiticides market.

Asia Pacific is the fastest-growing territory with an 8.55% CAGR through 2031. China’s expanding urban pet population, Japan’s aging society preference for companion animals, and India’s vast livestock base jointly drive demand. Governments emphasize food safety, prompting more rigorous parasite-control mandates. Distribution upgrades widen rural access, and pricing tiers broaden the customer base. Regulatory reforms in China shorten time-to-market, further raising momentum for the veterinary parasiticides market.

Europe exhibits steady mid-single-digit growth, shaped by strict environmental rules and welfare standards. Sustainability goals spur interest in biologicals and reduced-impact chemistries. Brexit reshapes supply chains, rewarding firms that adapt swiftly to new import checkpoints. Latin America and the Caribbean leverage large cattle populations and competitive beef exports to adopt combination dewormers that safeguard productivity. The Middle East and Africa show nascent but promising uptake as urbanization lifts companion-animal care, although infrastructure deficits temper premium product penetration. Together, these regional currents sustain the global expansion of the veterinary parasiticides market.

Competitive Landscape

The veterinary parasiticides market is moderately concentrated. Zoetis holds roughly 20% global share, supported by USD 1.6 billion in parasiticide sales and diagnostics integration like Vetscan Imagyst. Elanco follows with a focus on six-in-one Credelio Quattro, anticipating early 2025 rollout. Merck Animal Health expands through acquisitions, recently adding VECOXAN and SENTINEL rights to deepen livestock and companion portfolios.

Innovation priorities include novel chemistries that bypass existing resistance, AI-guided diagnostics that tailor dosing, and long-acting delivery platforms. Indical Bioscience’s automated fecal analysis exemplifies data-driven disruption.

Generics pressure pricing as patents lapse, yet innovators defend margins through convenience-oriented combos and branded loyalty programs. Strategic alliances between pharma and tech firms accelerate connected-care ecosystems, embedding products within broader health-management services across the veterinary parasiticides market.

Veterinary Parasiticides Industry Leaders

Boehringer Ingelheim

Virbac

Zoetis, Inc.

Ceva Sante Animale

Merck & Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: FDA approved Simparica Trio label expansion to include prevention of flea tapeworm infections, making it the only canine combination parasiticide with this indication.

- April 2025: Vetoquinol acquired Australian rights to the Drontal and Profender product families from Elanco Animal Health, which the Australian Competition and Consumer Commission approved.

- January 2025: Elanco launched Credelio Quattro at VMX, offering six-in-one parasite protection for dogs, including tapeworms, roundworms, hookworms, heartworms, ticks, and fleas in a single monthly tablet.

- October 2024: Elanco launched Credelio Quattro at VMX, offering six-in-one parasite protection for dogs, including tapeworms, roundworms, hookworms, heartworms, ticks, and fleas in a single monthly tablet.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every branded or generic chemical or biological product that is legally approved and commercially packed to kill or repel internal or external parasites in food-producing or companion animals, valued at manufacturer selling price across topical, oral, and injectable routes.

Scope Exclusion: Flea shampoos, plant-based repellents, and medicines formulated only for humans are left out.

Segmentation Overview

- By Product Type

- Ectoparasiticides

- Endoparasiticides

- Endectocides

- Combination / Broad-spectrum Products

- Biological & Botanical Parasiticides

- By Animal Type

- Food-Producing Animals

- Cattle

- Poultry

- Swine

- Sheep & Goats

- Companion Animals

- Dogs

- Cats

- Food-Producing Animals

- By Mode of Administration

- Topical

- Oral

- Injectable

- Others

- By End User

- Veterinary Clinics & Hospitals

- Animal Farms & Production Units

- Retail & Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Phone interviews with veterinarians, integrated farm managers, and distributor buyers across North America, Europe, and fast-growing Asian markets validated desk findings, revealed on-farm compliance gaps, and gauged likely uptake of long-acting injectables through 2030.

Desk Research

Our analysts pulled livestock head-count series from FAOstat, household pet ratios from the American Veterinary Medical Association, customs codes for antiparasitic preparations from UN Comtrade, and safety alerts from the European Medicines Agency. Company 10-K filings, investor decks, and trade press flagged price swings, while papers in Parasites & Vectors clarified resistance-driven retreatment needs. We also tapped D&B Hoovers and Dow Jones Factiva for revenue splits and timely news. The sources named are illustrative; many other open and subscription materials shaped data capture and checks.

Market-Sizing & Forecasting

We begin with a top-down pool that multiplies regional livestock numbers, pet totals, and parasite prevalence by standard treatment days; then we apply blended average selling prices. Supplier roll-ups and sampled invoices give a bottom-up sense check before totals are locked. Key inputs include cattle inventory cycles, companion-animal penetration, resistance-linked retreatment rates, approval pipelines, macrocyclic-lactone dose price, and online channel share. Each driver is projected through multivariate regression with an ARIMA overlay, while scenario analysis buffers outbreak shocks.

Data Validation & Update Cycle

Outputs pass two analyst reviews; variance flags trigger source re-checks, and material events prompt interim refreshes outside our yearly revision.

Before release, an analyst reruns the latest quarter so clients receive the freshest baseline.

Why Mordor's Veterinary Parasiticides Baseline Deserves Confidence

Published estimates often diverge because firms choose different product mixes, price points, and refresh cadences. According to Mordor Intelligence, our disciplined scope choices and mid-year exchange rates keep 2025 values firmly grounded.

Key gap drivers include some publishers counting over-the-counter repellents, others layering distributor mark-ups, and a few rolling forward older FX assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.04 B (2025) | Mordor Intelligence | - |

| USD 10.19 B (2024) | Global Consultancy A | Prior-year FX, no prevalence check |

| USD 13.63 B (2025) | Industry Association B | Includes OTC shampoos |

| USD 13.70 B (2025) | Trade Journal C | Values at resale price |

In short, clear variables, multi-layer checks, and frequent refreshes let decision makers rely on our numbers with confidence.

Key Questions Answered in the Report

What is the current value of the veterinary parasiticides market?

The market is valued at USD 10.74 billion in 2026 and is projected to reach USD 15.03 billion by 2031.

Which region is growing fastest for veterinary parasiticides?

Asia Pacific is the fastest-growing region with an expected 8.55% CAGR to 2031, driven by rising pet ownership and livestock investments.

Why are long-acting injectables gaining popularity?

They offer year-long protection, remove monthly compliance gaps, and have demonstrated 100% efficacy in clinical studies.

How significant is resistance to current parasiticides?

Surveillance shows pour-on dewormers failed to meet 90% efficacy on 76.5% of tested farms, prompting wider use of combination products.

What is driving demand for combination therapies?

Pet owners seek single-dose solutions that cover multiple parasite types, and veterinarians favor simplified protocols that improve adherence.

Which product segment holds the largest share?

Ectoparasiticides accounted for 42.18% revenue share in 2025, reflecting their essential role against vectors like ticks and fleas.

Page last updated on: