Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

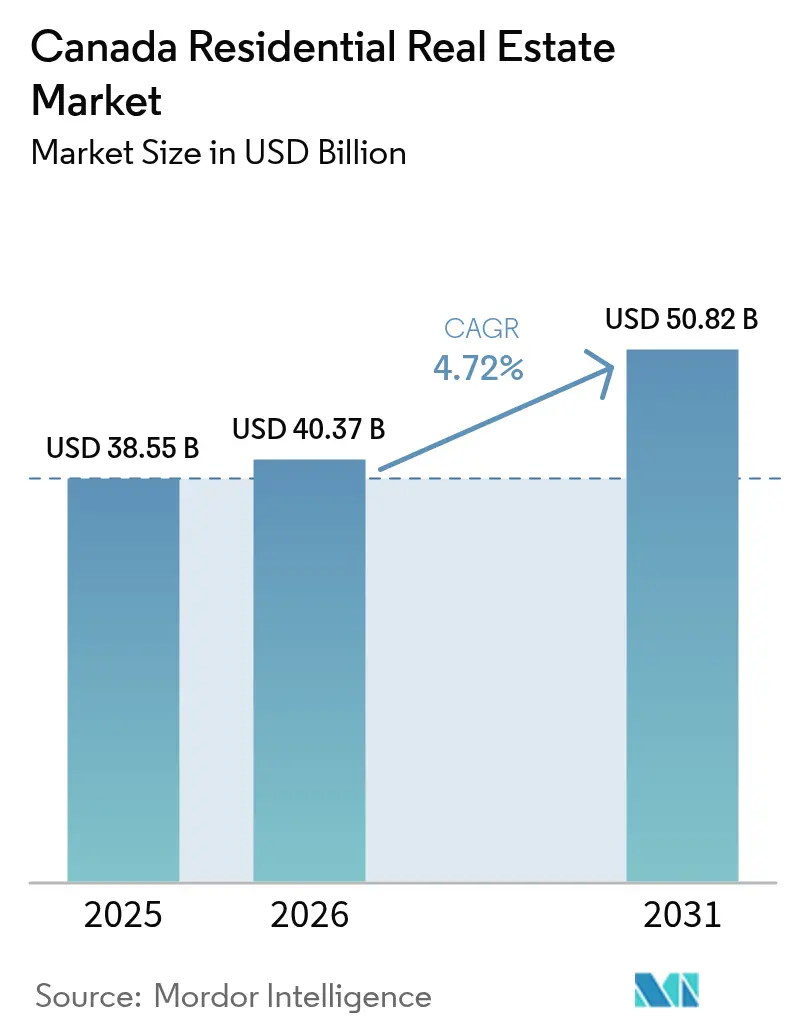

| Base Year Market Size (2025) | USD 38.55 Billion |

| Market Size (2026) | USD 40.37 Billion |

| Market Size (2031) | USD 50.82 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

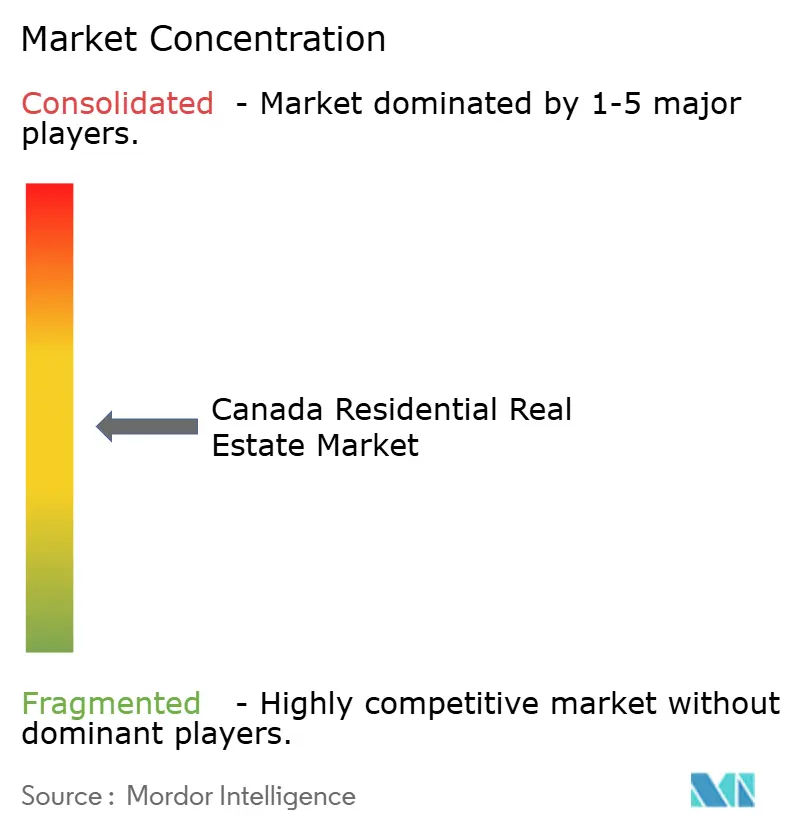

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Residential Real Estate Market Analysis by Mordor Intelligence

Canada residential real estate market size in 2026 is estimated at USD 40.37 billion, growing from 2025 value of USD 38.55 billion with 2031 projections showing USD 50.82 billion, growing at 4.72% CAGR over 2026-2031. A surge in immigration, combined with funding that favors purpose-built rental developments, is lifting demand faster than new supply in several provinces. Technology-led construction methods such as modular and mass-timber mid-rises are shortening build times, while institutional investors channel more capital into rental formats to secure steady cash flows. Alberta is capturing migrants priced out of Ontario and British Columbia, and regulatory changes—chiefly possible adjustments to the mortgage stress test—could widen mortgage access and revive purchase activity. Ongoing cost inflation in materials, labor, and insurance tempers near-term profits, yet large players are countering through scale efficiencies and digital property-management tools.

Key Report Takeaways

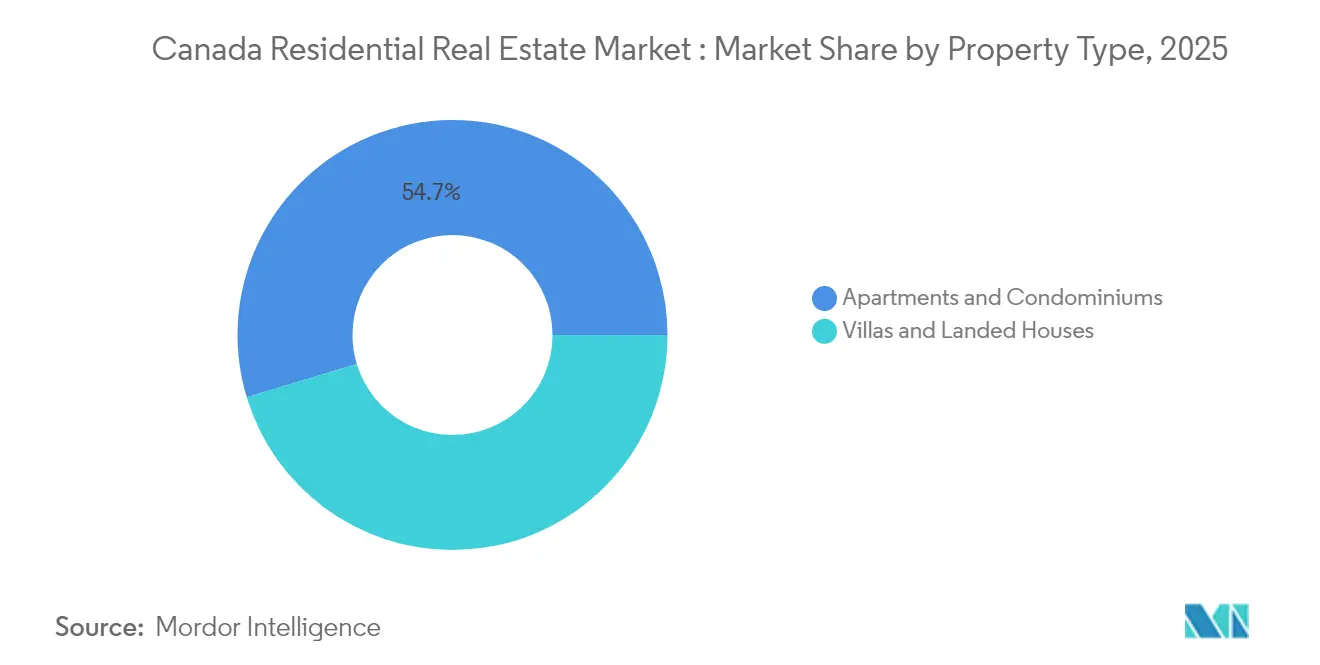

- By property type, apartments and condominiums led with a 54.68% revenue share of the Canada residential real estate market in 2025; apartments and condominiums recorded the fastest growth at a 4.93% CAGR through 2031.

- By price band, mid-market assets held 51.34% of the Canada residential real estate market share in 2025, while the affordable segment is projected to expand at 5.02% CAGR to 2031.

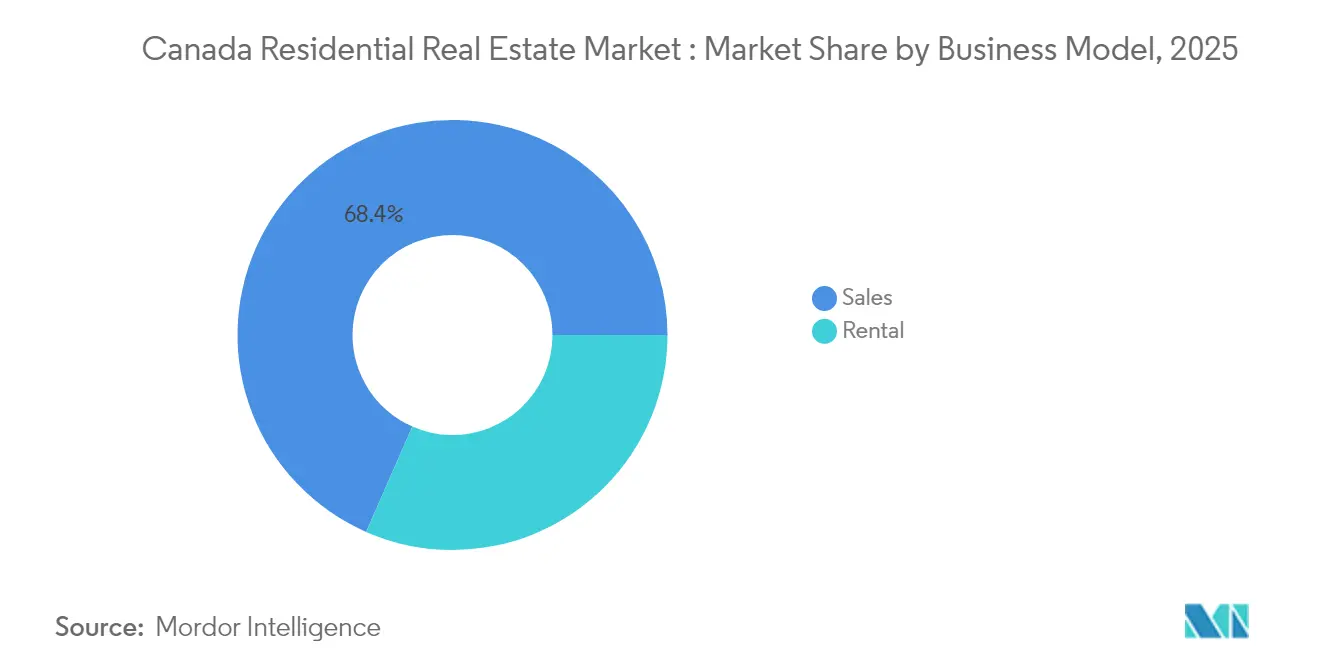

- By business model, sales transactions captured 68.42% of the Canada residential real estate market size in 2025; the rental model shows the highest momentum with a 5.08% CAGR forecast through 2031.

- By mode of sale, the secondary market accounted for 71.35% of the Canada residential real estate market in 2025, whereas primary new-build sales are set to climb at 4.95% CAGR.

- By province, Ontario commanded 35.58% of the Canada residential real estate market size in 2025; Alberta is the fastest-growing province at 5.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Immigration-fuelled household formation outpacing supply | +1.2% | Ontario & British Columbia; spillover to Alberta | Medium term (2-4 years) |

| Federal and provincial funding for purpose-built rentals | +0.8% | National; largest in major urban centers | Long term (≥4 years) |

| Transit-oriented rezoning unlocking urban landbanks | +0.7% | Ontario & British Columbia | Long term (≥4 years) |

| Modular & mass-timber mid-rises compressing build cycles | +0.6% | National; early uptake in Ontario & BC | Medium term (2-4 years) |

| Institutional shift to single-family rental portfolios | +0.5% | National; focus on growth markets | Long term (≥4 years) |

| CMHC green-financing incentives for net-zero multifamily | +0.4% | National; strongest in environmentally progressive provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Immigration-fuelled household formation outpacing supply

Canada’s population crossed 40 million in 2024, and newcomers continue to push annual household formation beyond the current construction pace, especially in Ontario and British Columbia. Intensifying demand spills into Alberta as 18,400 young workers relocated there in 2024, easing—but not eliminating—pressure on traditional gateways. Although recent caps on temporary residents modestly reduce inflows, the federal target of 485,000 permanent residents in 2025 underpins sustained demand. This demographic momentum is reinforcing price upside and attracting institutional equity seeking a hedge against inflation. At the same time, affordability gaps widen, prompting government subsidies aimed at first-time buyers.

Federal and provincial funding for purpose-built rentals

Ottawa’s USD 15 billion Apartment Construction Loan Program and the USD 4.4 billion Housing Accelerator Fund collectively increase capital access and accelerate municipal approvals[1]Canada Mortgage and Housing Corporation, “Housing Accelerator Fund: Program Details,” Canada Mortgage and Housing Corporation, cmhc-schl.gc.ca. Provincial action amplifies results: Quebec’s incentive package boosted rental housing starts 30% in 2024. These supply-side programs move beyond earlier demand-side subsidies, prompting developers to pivot toward long-term rental income over one-time sales. The structural shift is visible in 35% of completions now being purpose-built rentals, the highest ratio since 1992.

Modular & mass-timber mid-rises compressing build cycles

The Build Canada Homes program earmarks USD 25 billion to accelerate factory-built housing, aiming for 500,000 new homes a year. Updated building codes permit 18-storey mass-timber structures, and early adopters in Ontario and British Columbia report 50% faster build times and 20% cost savings relative to concrete alternatives. Beyond speed, prefabrication addresses labor constraints and lowers embodied carbon, positioning modular projects for preferential green-finance rates from CMHC.

Institutional shift to single-family rental portfolios

Blackstone Real Estate’s privatization of Tricon Residential underscores growing appetite for single-family rentals triconresidential.com. Purpose-built subdivisions designed for renting are scaling because they balance detached-home demand with unaffordable ownership costs. Pension funds and insurers favor the predictable cash flows and limited turnover risk associated with these assets, often combining them with professionalized management platforms for operational efficiencies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Build-cost inflation from skilled-labor shortages | -0.9% | National; acute in urban cores | Short term (≤2 years) |

| OSFI mortgage stress-test tightening | -0.6% | National; largest in high-priced markets | Medium term (2-4 years) |

| Municipal development-charge escalations (GTA) | -0.3% | Greater Toronto Area | Medium term (2-4 years) |

| Rising insurance premiums on high-rise condos (BC) | -0.1% | British Columbia urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Build-cost inflation from skilled-labor shortages

Construction costs are 51% above pre-pandemic levels, eroding pro formas and forcing schedule extensions. Retirements outpace apprentice entries, and immigration policies still emphasize knowledge-based talent rather than trades. In response, Ottawa introduced 55-year insured construction loans, but developers in Ontario and British Columbia still cite labor scarcity as their biggest barrier to breaking ground. Alberta benefits from a more mobile workforce that tempers wage spikes, yet national supply chains for steel and glazing remain tight, keeping material costs elevated.

OSFI mortgage stress-test tightening

The regulator continues to enforce the higher of the contract rate plus 2 percentage points or 5.25% as the qualifying rate. While rates began easing in early 2025, the qualifying hurdle still sidelines many first-time buyers. Proposed loan-to-income limits could further restrict lender portfolios, especially in Toronto and Vancouver where average mortgage sizes exceed six times household income. Although OSFI signaled it may lift the test for uninsured mortgages by late 2025, any interim tightening could slow deal velocity and nudge demand toward rentals[2]Office of the Superintendent of Financial Institutions, “Residential Mortgage Underwriting Practices and Procedures,” Office of the Superintendent of Financial Institutions, osfi-bsif.gc.ca.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Apartments and Condominiums led Density Strategy

Apartments command 54.68% of the Canada residential real estate market in 2025 and are forecast to post a 4.93% CAGR to 2031. Developers gravitate to multifamily because CMHC’s insured debt lowers equity requirements, while municipal up-zoning away from single-family exclusivity supports higher-density formats.

Strong institutional appetite anchors this trend. REITs pursue purpose-built rentals that meet ESG mandates and match long-duration liabilities. Modular construction and mass-timber systems shorten delivery cycles, partially offsetting land-price inflation in core markets. Detached-home builders concentrate on outlying suburbs where land costs remain manageable, but the value proposition rests on commute tolerance and fewer transit options.

By Price Band: Affordable Housing Accelerates

Mid-market units represented 51.34% of the Canada residential real estate market share in 2025, yet affordable housing is projected to be the fastest-growing slice at 5.02% CAGR. Government policy now ties infrastructure grants to municipal progress on affordability, pushing cities to expedite approvals for below-market rents.

Developers secure tax abatements and density bonuses by designating 20%-30% of units as affordable, improving blended project returns. Institutional investors, mindful of social-impact mandates, view affordable housing as a hedge against cyclical downturns because waitlists provide durable occupancy. Luxury products still attract foreign buyers in niche areas, but higher transfer taxes and vacancy levies cap speculative momentum.

By Business Model: Rental Momentum Builds

Sales remained the majority with 68.42% of the Canada residential real estate market in 2025, but rentals will outpace at a 5.08% CAGR. CMHC’s 95% loan-to-cost construction financing slashes equity needs for rental developments, nudging merchant builders to retain completed assets.

Pension funds emphasize stabilized cash flows, and REITs grow via forward-purchase agreements that de-risk developers’ exits. Strong rent growth—nationally 7.4% in 2024—supports coverage ratios even amid cost inflation. Homeownership aspirations are moderating as borrowers struggle to pass stress-test hurdles, redirecting demand toward well-amenitized rental communities.

By Mode of Sale: Primary Market Narrows Inventory Gap

Secondary transactions comprised 71.35% of the Canada residential real estate market in 2025, but primary new-build sales will rise at 4.95% CAGR as first-time buyer programs favor newly completed housing.

Federal policy now permits 30-year insured amortizations for new-construction purchases, reducing monthly payments. Developers leverage advanced marketing platforms and virtual tours to pre-sell units earlier, aiding construction financing. Energy-efficiency codes give new builds an operating-cost edge over older stock, swaying cost-conscious buyers toward the primary market despite higher sticker prices.

Geography Analysis

Ontario accounted for 35.58% of the Canada residential real estate market in 2025. Development charges in the Greater Toronto Area, which average USD 165,000 per condo unit, constrain feasibility and lengthen timelines, pushing some activity to surrounding municipalities. Immigration keeps net household formation high, but affordability challenges sustain the rental surge and suppress the ownership rate.

British Columbia stabilizes after deploying transit-oriented zoning and foreign-buyer taxes. Vancouver’s removal of minimum-parking rules near rapid transit allows denser infill, yet high-rise insurance premiums continue to elevate operating expenses. Mass-timber approvals for 18-storey towers reduce structural costs and carbon footprints, positioning the province as a laboratory for next-generation green development.

Alberta posts the fastest growth at 5.08% CAGR to 2031. Calgary’s benchmark price of USD 591,100 remains accessible relative to Toronto and Vancouver, and provincial budget surpluses fuel infrastructure expansions that entice migrants. Edmonton benefits from a 4.8% population increase in early 2024, translating into stronger absorption of both sales and rentals.

Quebec enjoys renewed momentum as single-family median prices near USD 450,000 keep ownership within reach for local buyers. A streamlined online permit portal launched in 2024 cut average approval times by 30 days, reducing carrying costs. Purpose-built rentals dominate new starts in Montréal as institutional capital targets stable yields backed by long-term leases.

Atlantic Canada and smaller prairie markets experience steady inflows from international graduates and remote workers. Lower entry prices balance thinner job markets, while modest construction pipelines protect against over-supply. However, limited contractor capacity could slow delivery of larger multifamily projects unless provincial training programs scale up the trades workforce.

Regulatory Landscape

Canada's residential real estate is governed by a split framework. Provinces oversee land and property rights, planning, and tenancy rules, while federal bodies influence demand and credit conditions through mortgage policy, mortgage insurance, and fiscal housing programs. Key federal levers include OSFI's mortgage underwriting framework (including the qualifying-rate stress test) and the Prohibition on the Purchase of Residential Property by Non-Canadians Act, which continues to constrain non-resident demand in selected buying channels.

From 2024 to 2026, federal action leaned more toward supply-side delivery and financing. Budget 2024 reinforced renter protections and homebuilding targets, and in 2026 the federal government advanced the Build Canada Homes platform, including the January 2026 national submission portal for project intake and the February 2026 introduction of the Build Canada Homes Act to establish the agency as a permanent Crown corporation focused on affordable housing delivery. Separately, revised CMHC regulatory capital guidelines took effect January 1, 2026, and in March 2026 the federal government introduced Bill C-26, proposing CAD 1.713 billion in payments to provinces and territories to reduce cost barriers and increase housing supply.

Value Chain Analysis

In Canada, the residential real estate value chain starts with land assembly and entitlement, including zoning amendments, site plan approvals, and permitting. It then moves into project finance (banks, CMHC-insured lending, and capital markets), design and engineering, materials and equipment procurement, and construction via general contractors and specialty trades, before shifting to sales and leasing through broker networks and developer channels. After completion, the chain extends into building operations, property management, maintenance, insurance, valuation, and transaction services, with REITs, pension funds, and other institutional buyers increasingly providing takeout capital for purpose-built rentals.

Execution risk tends to concentrate mid-chain, where permitting timelines and construction inputs can destabilize schedules and pro formas. Industry and policy evidence cited in the report points to persistent cost pressure in key materials since 2020 and ongoing fragmentation across subcontracting and supplier layers, which raises coordination overhead and supports a move toward industrialized delivery models. Federal programs linked to Build Canada Homes and CMHC financing are explicitly prioritizing factory-built approaches (modular and mass timber), reinforcing a procurement and delivery pathway that consolidates purchasing, standardizes designs, and reduces on-site labor intensity for multi-unit housing.

Competitive Landscape

The Canada residential real estate market exhibits moderate fragmentation. The leading players—Brookfield Asset Management, CAPREIT, Tridel Group, First Capital REIT, and Minto Apartment REIT drive the market with their strategic operations. Brookfield skillfully navigates market cycles by utilizing global capital pools to develop master-planned communities that harmoniously integrate office, retail, and rental towers. CAPREIT, on the other hand, emphasizes asset recycling by selling non-core suburban properties and reinvesting the proceeds into new affordable rental projects, supported by CMHC.

Technology is a core differentiator. Tridel deploys off-site modular components to cut 15% from build schedules in the Greater Toronto Area. First Capital uses digital twins for predictive maintenance, extending asset lifespans and optimizing capital-expenditure timing. Minto pilots IoT-enabled energy-management systems that reduce utility costs up to 18%, aligning with tenant ESG preferences.

Consolidation is strengthening buyer power in niche sectors. Forum REIIF’s USD 1.69 billion acquisition of Alignvest Student Housing creates the nation’s largest privately held student portfolio, positioning the group to negotiate bulk service agreements and cross-market leasing rights. Blackstone’s take-private of Tricon Residential signals a bet on single-family rentals’ secular growth. Mid-sized regional developers respond by forming joint ventures to share risk and access cheaper institutional debt.

Canada Residential Real Estate Industry Leaders

Brookfield Asset Management

CAPREIT

Tridel Group

Mattamy Homes

QuadReal Property Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Purpose-built rental and mixed-income multifamily development continues to represent the clearest opportunity where capital, programs, and delivery models align. Federal supply initiatives such as Build Canada Homes (operationally launched in January 2026) and CMHC financing tools support developers and landlords pursuing rental formats, while municipal transit-linked intensification creates investable nodes for higher-density projects. In 2026, market evidence includes major groundbreakings for rental-led communities, including Fengate Asset Management and LiUNA breaking ground in July 2026 on West Orchard Urban Rentals in Ottawa (425 homes at the New Orchard LRT station), and Canderel commencing Forêt Forest Hill in Toronto (a 1,310-suite, three-tower master-planned community).

Industrialized construction and standardized approvals are a second area of focus, with policy signaling favoring modular and mass-timber mid-rises and catalog-style designs that shorten timelines and reduce cost volatility. That approach also points upstream to supply chain development, such as expanded prefabrication capacity and partnerships among developers, building supplies dealers, and specialty manufacturers. In addition, large-scale community revitalization and public-private delivery models provide a steady pipeline for affordability-linked inventory, particularly in high-demand metros where projects can blend market and affordable units with city and CMHC participation.

Recent Industry Developments

- April 2026: Tridel opened the Atkinson Co-Operative residence at 130 Augusta Avenue in Toronto as part of the Alexandra Park revitalization, delivering 103 affordable and replacement rental homes. The delivery highlights how large-scale urban renewal projects are being used to add rental supply while meeting affordability and replacement-housing obligations.

- May 2025: The federal government launched the Build Canada Homes program with a USD 25 billion commitment to finance factory-built housing. This accelerated focus on modular and industrialized delivery strengthens the pipeline for purpose-built rentals and can shift procurement toward repeatable designs and off-site manufacturing capacity.

- June 2024: Canada's population crossed 40 million, reflecting the pace of immigration-driven household formation feeding housing demand in major provinces. The demographic step-up increases pressure on new supply delivery and reinforces institutional interest in rental formats where absorption is supported by persistent household growth.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the annual value created from residential property transactions in Canada, covering both new-build and resale homes, and the rental component converted to a comparable annual value so sales and rentals can be viewed together.

Scope exclusions: Pure land banking, student dormitories, serviced apartments, and commercial mixed-use floor area are excluded from this sizing.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Price Band

- Affordable

- Mid-Market

- Luxury

- By Mode of Sale

- Primary

- Secondary

- By Business Model

- Sales

- Rental

- By Region (Province)

- Ontario

- Quebec

- British Columbia

- Alberta

- Rest of Canada

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build a clean starting point for Canada housing activity and pricing, and to keep definitions consistent across provinces. We referenced public or official sources such as Statistics Canada tables on housing, income, and population, Canada Mortgage and Housing Corporation releases on starts, completions, and rental conditions, Bank of Canada rate decisions and credit-market commentary, and provincial land registry or assessment publications where available.

To translate activity into market value and to sanity-check turning points, we also reviewed real estate board and association releases, municipal open-data portals for permits and development pipelines, and peer-reviewed housing and urban economics research to understand repeatable relationships. Developer-level context was taken from company filings and investor presentations, followed by reputable press and regulatory notices to place timing around policy changes. Where public documents did not provide enough coverage on private participants, paid subscriptions for company financials and news intelligence were used. The sources listed here are illustrative only, and many other public documents and datasets were also reviewed to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary discussions were run with a mix of developers, brokers, lenders, property managers, and housing market advisors to test what the desk research was suggesting and to fill gaps that do not show up clearly in public tables. Since Canada varies widely by province and city, we also checked assumptions on price momentum, absorption, rental pressure, and policy impacts across major metros and secondary markets, so the final model does not rely on one local story.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 20% | |

| Mid tier: 48% | Functional/Unit leaders: 32% | |

| Smaller Players: 20% | Managers: 48% |

Market-Sizing & Forecasting

The sizing starts with a top-down reconstruction of Canada residential demand, where housing transaction volumes and prevailing price benchmarks are used to estimate annual value, and rental activity is converted into an annualized value so it can be compared fairly with sales. Once the headline number is formed, it is checked using selective bottom-up approximations, such as sampled project-level price points, developer pipeline and absorption commentary, and channel checks on typical closing values.

Key inputs used in the model include existing home sales counts, housing starts and completions, benchmark home prices and their mix shifts, mortgage rates and credit availability signals, population growth and household formation, and rental market tightness indicators like vacancy rates and rent growth. These variables help separate a year where prices rose but volumes softened from a year where volumes recovered at a different price point.

For forecasting, we mainly apply scenario analysis supported by light time-series smoothing to avoid overreacting to one quarter of volatility, and then assumptions are reviewed with primary respondents to keep them realistic. When bottom-up checks are incomplete for smaller provinces or thinly reported sub-markets, the gap is handled through proportional allocation tied to observed activity shares and then revalidated against independent housing indicators.

Data Validation & Update Cycle

Validation is done through multiple passes where model outputs are compared against independent signals like national housing accounts, lending and rate trends, and reported price benchmarks, and then outliers are investigated before sign-off. If a major variance appears, the underlying drivers are rechecked, assumptions are adjusted, and follow-up primary calls are triggered to confirm whether the shift is structural or temporary.

The report is refreshed annually, and interim updates are made when policy moves, rate changes, or housing market shocks materially alter volumes or pricing. Before delivery, a final review pass is completed so clients receive the latest view based on newly released public data and the newest feedback from market participants.

Mordor Intelligence's Canada Residential Real Estate Market Size Versus Other Published Estimates

Published market sizes for Canada residential real estate can look far apart because the word market gets treated differently, and the math changes depending on whether the source counts transaction value, total housing stock value, or a wider real estate bucket. Timing also matters, since base years, exchange-rate timing, and fast-moving price cycles can shift a value even when the underlying housing activity is similar.

By tracking sales volumes, benchmark prices, and rent and vacancy signals each update cycle, Mordor Intelligence keeps the total tied to annual transaction activity with rental value annualized for comparability. Some sources roll residential into an overall Canada real estate total that can include land and commercial property, which makes the result much larger than a residential-only transaction flow view. Another common reason is that rental gets treated as an asset value proxy instead of an annualized stream, which changes the unit of measurement and inflates the headline number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 38.55 B (2025) | |

| Global Consultancy A | USD 327.70 B (2025) | Reports the broader Canada real estate market (with residential presented inside a wider scope that can include commercial, land, and industrial), so the value is not directly comparable to residential transaction flow value. |

| Industry Publisher B | USD 951.38 B (2025) | Uses a much wider valuation base that appears closer to housing stock value or a broad revenue boundary, rather than annual transaction value plus annualized rental activity. |

The table shows that the largest gaps come from what is being valued and how rental activity is handled, not just from forecasting style. When the market is linked back to observable annual transactions, price benchmarks, and rental tightness indicators, the sizing stays transparent and can be repeated consistently year after year.

Key Questions Answered in the Report

What is the current Canadian real estate market size?

The market was valued at USD 40.37 billion in 2026 and is projected to reach USD 50.82 billion by 2031.

Which segment is growing fastest within the Canadian real estate market?

Purpose-built rentals lead with a 5.08% CAGR thanks to CMHC loan programs and institutional capital inflows.

Why is Alberta the fastest-growing province?

Housing affordability, job diversification, and net in-migration drive Alberta’s 5.08% CAGR outlook.

What regulatory change could most affect buyers in 2025?

OSFI’s potential removal of the mortgage stress test for uninsured loans may expand borrowing capacity later in 2025.

Page last updated on: