Acoustic Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 162.45 Billion |

| Market Size (2031) | USD 190.81 Billion |

| Growth Rate (2026 - 2031) | 3.27% CAGR |

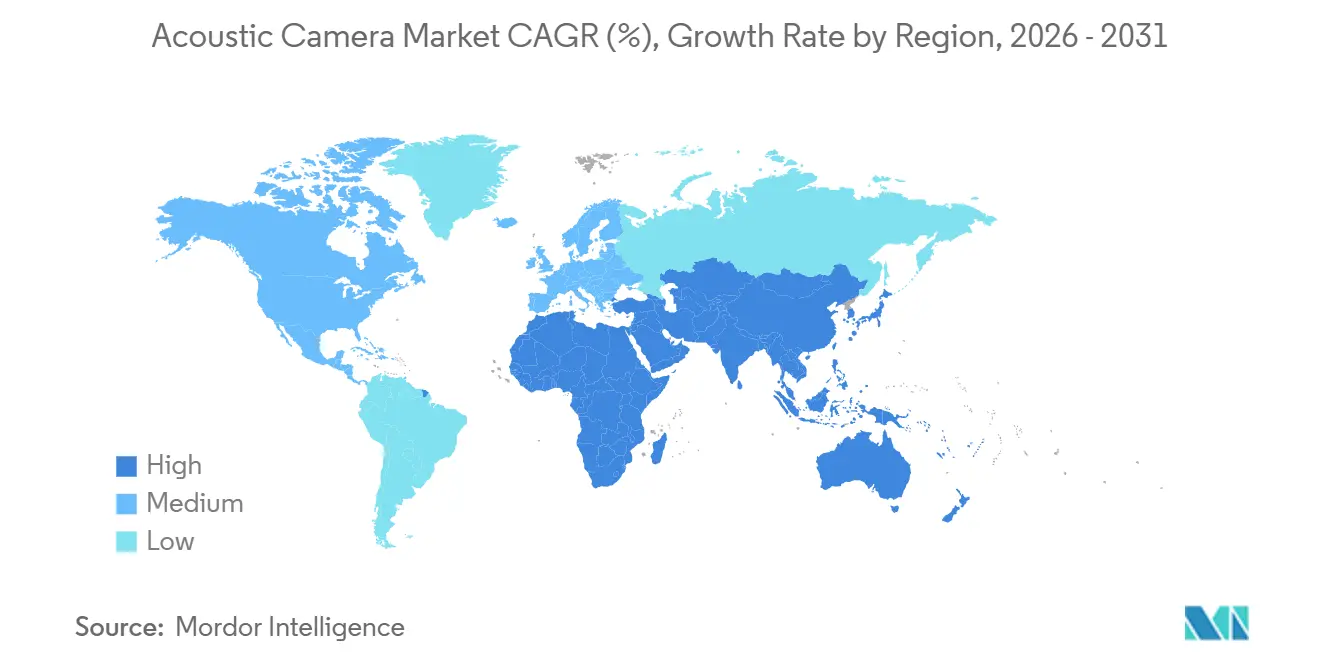

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acoustic Camera Market Analysis by Mordor Intelligence

The acoustic camera market size is projected to be USD 155.62 billion in 2025, USD 162.45 billion in 2026, and reach USD 190.81 billion by 2031, growing at a CAGR of 3.27% from 2026 to 2031. Expanding urban-noise regulations, accelerated electrification of cars and aircraft, and the arrival of sub-USD 5,000 edge-AI beamforming modules are sustaining demand despite capital-intensive hardware. Europe’s Environmental Noise Directive, North America’s automotive quiet-car rules, and Asia-Pacific’s smart-factory incentives are encouraging continuous acoustic imaging instead of handheld sound-level meters. Automotive and aerospace programs are embedding 3-D arrays into validation workflows, while smart factories stream beamforming data to edge gateways that classify faults in real time. Utilities, oil and gas operators, and renewable-energy developers are adopting drone-mounted ultrasound rigs that detect leaks from more than 50 meters away, translating avoided energy loss into measurable payback periods. Competitive rivalry remains moderate, and vendors are shifting toward software-as-a-service bundles that tie cloud analytics to installed hardware, raising switching costs but compressing replacement cycles.

Key Report Takeaways

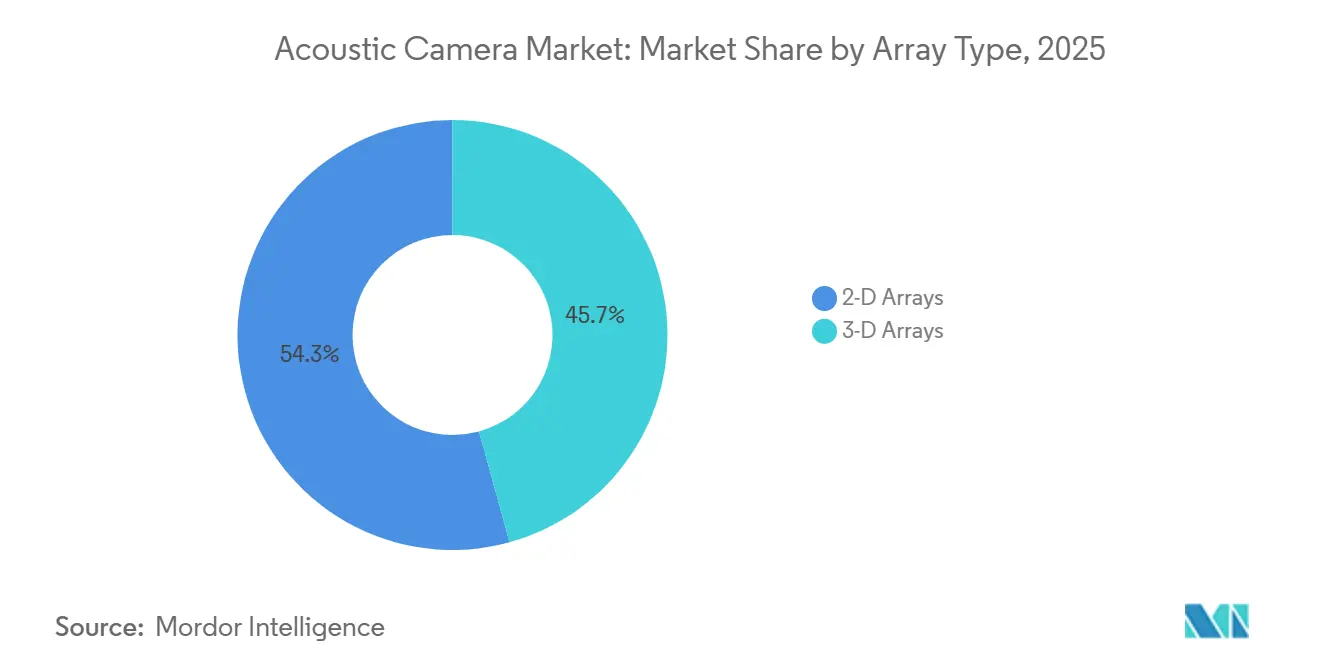

- By array type, 3-D arrays led with 45.72% revenue share in 2025; drone-mounted platforms are projected to expand at a 3.39% CAGR through 2031.

- By measurement type, far-field solutions accounted for 57.91% of the acoustic camera market share in 2025, while near-field solutions are forecast to post the fastest 3.33% CAGR to 2031.

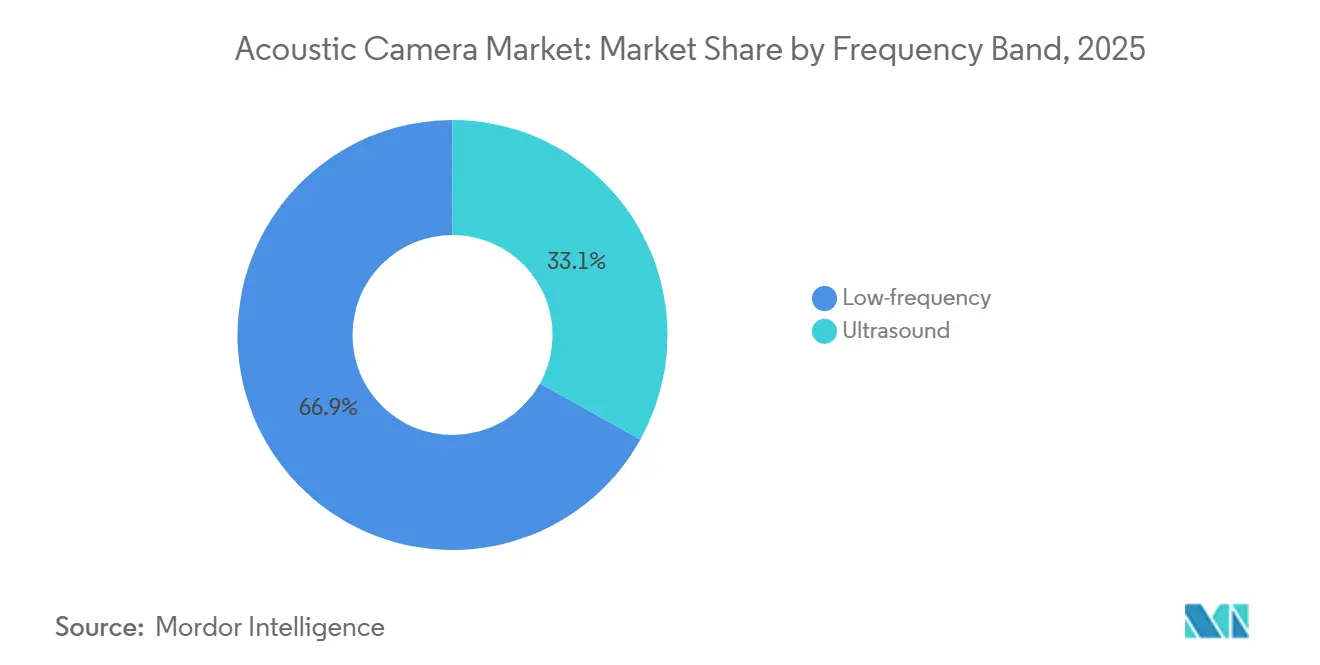

- By frequency band, low-frequency systems represented 66.92% of the acoustic camera market size in 2025; ultrasound systems are poised to grow at a 3.29% CAGR between 2026-2031.

- By deployment platform, handheld units captured 46.73% share of the acoustic camera market size in 2025, whereas drone and UAV-mounted units will record the highest 3.39% CAGR to 2031.

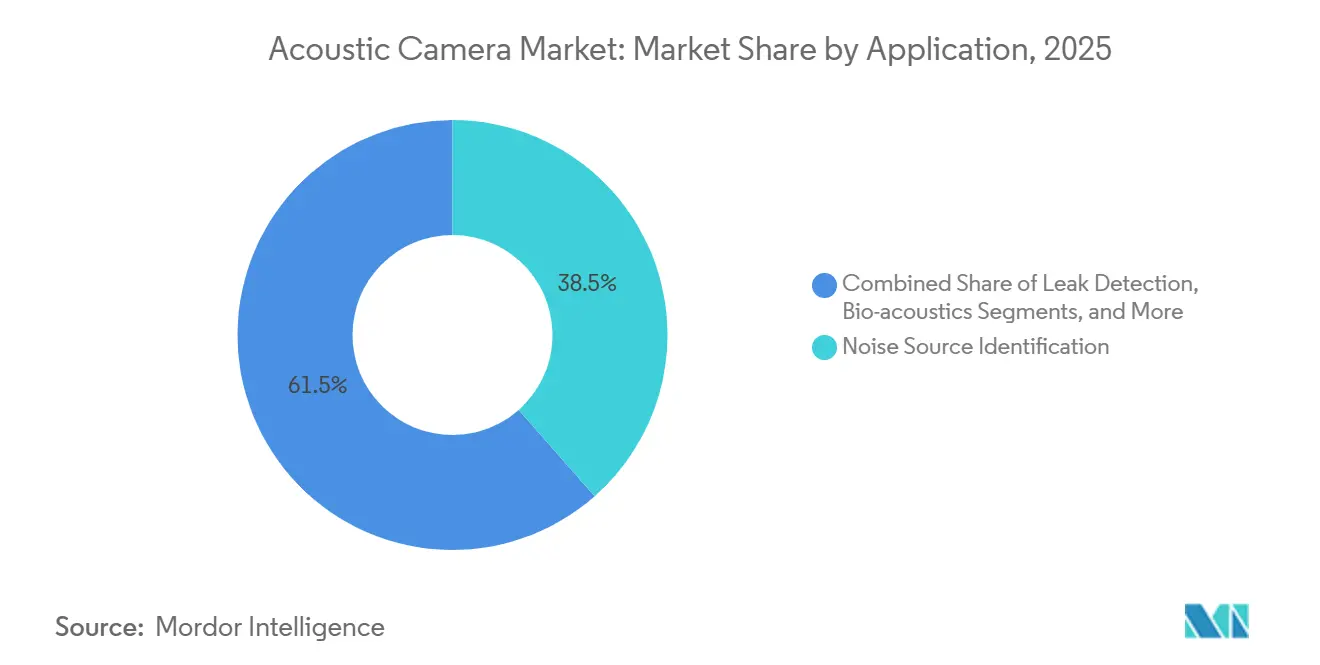

- By application, noise-source identification dominated with 38.49% share in 2025; leak-detection solutions are projected to expand at a 3.41% CAGR over 2026-2031.

- By end-user, automotive and mobility held 34.52% of the acoustic camera market share in 2025; utilities and oil-and-gas users are projected to register the fastest 3.43% CAGR to 2031.

- By geography, Europe commanded 34.82% revenue in 2025, while Asia Pacific is forecast to climb at a 3.47% regional CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acoustic Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global Urban-Noise Regulations | +0.9% | Global, with early enforcement in EU and select APAC cities | Medium term (2-4 years) |

| Rapid NVH Digitalisation in e-Mobility Platforms | +0.8% | North America, Europe, China | Short term (≤ 2 years) |

| Shift From Handheld Sound-Level Meters to Imaging Sensors on Smart Factories | +0.6% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Rising Aerospace Cabin-Comfort Certification Thresholds | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Edge-AI Beamforming Modules Enable Sub-USD 5K BOM Acoustic Cameras | +0.5% | Global | Short term (≤ 2 years) |

| Integration Into Autonomous-Robot Inspection Payloads | 0.3% | Global, with early gains in EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Urban-Noise Regulations

Municipal and national authorities are codifying more stringent ambient-noise ceilings, compelling infrastructure operators to install continuous acoustic-imaging networks rather than conduct periodic handheld surveys. The European Environmental Noise Directive forces agglomerations above 100,000 inhabitants to submit five-year acoustic maps, and similar rules in China and India define new industrial-zone decibel caps. The result is an addressable market that now spans urban-planning departments, transportation agencies, and building administrations. Acoustic cameras attribute noise to discrete machinery, lanes, or construction sites, enabling targeted mitigation that is both cheaper and faster than blanket sound-barrier installation.[1] World Health Organization, “Environmental Noise Guidelines,” who.int Vendors offering turnkey mapping services are forming partnerships with city councils, unlocking multi-year service revenues that smooth hardware demand cycles.

Rapid NVH Digitalization in E-Mobility Platforms

Battery-electric vehicles remove combustion masking noise, exposing motor whine, inverter harmonics, and tire-road interaction that passengers now perceive more clearly. Original equipment manufacturers, therefore, embed 3-D microphone arrays into chambers and on-road fleets to capture tonal content between 200 Hz and 10 kHz. Volkswagen’s Zwickau plant already images every ID-series unit during pre-production, and commercial e-truck makers are following suit. Concurrently, United Nations Regulation 138 requires audible pedestrian alerts below 20 km/h, a dual mandate that forces automakers to optimize cabin quietness without compromising external notification. This design tension drives iterative acoustic-camera testing during platform refreshes, locking in recurring instrumentation budgets.

Shift from Handheld Sound-Level Meters to Imaging Sensors on Smart Factories

Industry 4.0 programs connect fixed-mount acoustic cameras to edge gateways that fuse sound, vibration, and temperature data, reaching 94% fault-classification accuracy in servopress trials.[2]Fraunhofer IDMT, “ACME 4.0 Project,” idmt.fraunhofer.de Continuous imaging replaces walk-around inspections, cutting unplanned downtime by up to 30% and generating time-stamped evidence for ISO 55000 audits. The capital outlay, once a hurdle, is now offset by rental and subscription models; factory managers pay monthly fees that shift spending from CapEx to OpEx, easing procurement constraints. Vendors are including cloud dashboards that visualize hotspot evolution, allowing maintenance teams to prioritize interventions and justify payback within 18 months.

Rising Aerospace Cabin-Comfort Certification Thresholds

The European Union Aviation Safety Agency tightened cumulative external noise margins by 7 EPNdB for new-type certifications submitted after 2024, while airlines set interior targets below 70 dB during cruise. Airbus used acoustic cameras during A350 cabin mockup trials to identify problematic galley equipment, reducing interior sound pressure by 3 dB without adding structural weight. Far-field arrays installed on outdoor ranges help engineers reshape nacelle or pylon designs to deflect tonal peaks away from certification microphones. Given certification cycles of 7 to 10 years, each aircraft program represents a long-term revenue stream for high-channel-count acoustic-camera suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex for 3-D MEMS-Array Rigs | -0.4% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Scarcity of Field-Calibration Standards Across Regions | -0.3% | Global, fragmented enforcement | Medium term (2-4 years) |

| Patent Thickets Around Delay-and-Sum Beamforming IP | -0.2% | North America, Europe | Long term (≥ 4 years) |

| Limited Ruggedised Options for Harsh-Weather Utilities | -0.1% | APAC, Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for 3-D MEMS-Array Rigs

Three-dimensional systems with 128-384 microphones range from USD 40,000 to USD 80,000, putting them beyond the reach of many small enterprises.[3]Microflown Technologies, “Product Catalog 2025-2026,” microflown.com Leasing helps, yet total cost of ownership rises over a seven-year life. Credit-starved factories in South America and Africa still rely on handheld meters priced below USD 2,000 that provide no spatial context. FPGA availability and matched-microphone calibration remain bottlenecks to cost declines, limiting penetration in price-sensitive verticals.

Scarcity of Field-Calibration Standards Across Regions

No unified protocol governs in-situ calibration of multi-channel arrays, forcing firms to negotiate bespoke methods with national laboratories. An instrument may wait six months for re-certification, a delay that strains production schedules. Draft rules in China are not yet binding, and India lacks equivalent documents, discouraging uptake in pharmaceuticals and aerospace where traceable calibration is mandatory. Until ISO or IEC publishes a harmonized guideline, global rollouts will suffer fragmented compliance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Array Type: 3-D Arrays Dominate Volumetric Source Localization

Three-dimensional arrays captured 45.72% share in 2025 owing to their ability to localize noise in all directions without repositioning sensors, a key benefit during automotive powertrain mapping that compresses test-cell time. The acoustic camera market for 3-D arrays is projected to expand at a 3.31% CAGR through 2031 as price gaps narrow and edge-AI firmware reduces the need for processing hardware. Two-dimensional arrays remain popular in HVAC and substation audits because a 64-microphone handheld unit weighs under 3 kg and costs less than USD 20,000.

Price erosion is accelerating thanks to hybrid architectures that mix MEMS microphones for low frequencies with ultrasonic transducers for leak detection, as shown by Sorama’s 1,024-channel. The acoustic camera market continues to reward suppliers that bundle real-time spectral filters aligned with ISO 9295 guidance, allowing technicians to export compliant reports without additional software. Future adoption will hinge on integrating photon-based microphones that remove diaphragm-fatigue limits, a roadmap already signaled by optical MEMS start-ups.

By Measurement Type: Far-Field Applications Lead, Near-Field Gains in Electronics Inspection

Far-field solutions held 57.91% share in 2025 as automotive pass-by noise and aerospace flyover testing require arrays positioned beyond 1 m that align with ISO 362 and ICAO Annex 16 procedures. The acoustic camera market for near-field measurement is set to grow at a 3.33% CAGR to 2031, as electronics assemblers demand sub-10 cm spatial resolution to pinpoint board-level anomalies.

Near-field imaging lowers scrap rates in semiconductor fabs and consumer electronics lines, where a single defective solder joint can trigger latent field failures. Vendors now offer arrays with hardware that adjusts time-delay tap weights, shortening setup time. Far-field arrays, meanwhile, integrate with autonomous-vehicle test tracks, allowing multi-meter standoffs that do not disturb aerodynamic flow. Regulatory pressure from EU Type-Approval Regulation 540/2014 sustains demand for tripod-mounted solutions that work at 7.5 m and 25 m geometries.

By Frequency Band: Low-Frequency Dominates, Ultrasound Surges in Leak Detection

Systems tuned below 10 kHz captured 66.92% share in 2025 because most automotive, aerospace, and industrial machinery noise occupies the 200 Hz-8 kHz window. Ultrasound arrays above 20 kHz will grow 3.29% CAGR through 2031 as utilities adopt non-contact leak detection that identifies compressed-air losses costing manufacturers USD 3.2 billion annually.

Low-frequency arrays need larger apertures to reach narrow beamwidths, increasing footprint and weight. Ultrasound rigs achieve 5-degree resolution with 0.5 m diameters, suiting cramped utility corridors. Mid-band solutions (10-20 kHz) serve underwater ecology surveys where marine mammals vocalize; IEC 61260 filters decompose broadband data into fractional-octave outputs that biologists analyze. Suppliers that package dual-band firmware address cross-vertical use cases, future-proofing capital spend.

By Deployment Platform: Handheld Units Lead, Drone-Mounted Fastest Growth

Handheld systems accounted for 46.73% of the market share in 2025 because single-operator portability enables rapid HVAC audits, electrical inspections, and building services checks. Drone-mounted payloads, however, are on track for a 3.39% CAGR to 2031, cutting aerial inspection costs at power lines and pipelines by up to 70%. The acoustic camera market size for tripod and fixed-mount platforms remains stable around 35% as smart-factory users value always-on data streams.

Robot-integrated deployments are emerging as factories deploy quadruped platforms with 64-microphone arrays to navigate hazardous areas where human entry is restricted. FAA Part 107 rule changes that relax beyond-visual-line-of-sight flights will spur additional demand by allowing utilities to fly ultrasound rigs along hundreds of kilometers of transmission corridors. Vendors focused on ruggedization, dust sealing, and high-temperature tolerance will gain share in desert and offshore environments.

By Application: Noise-Source Identification Largest, Leak Detection Fastest Growth

Noise-source identification represented 38.49% share in 2025 because automotive NVH labs and aerospace cabin tests mandate tonal-component isolation before adding damping treatments. Leak detection will post a 3.41% CAGR over 2026-2031 as energy-efficiency mandates quantify compressed-air waste; ultrasound imaging detects hiss points that vibration or thermal tools miss.

Mechanical-fault diagnostics benefit from fusing acoustic-beamforming data with accelerometer feeds inside unified dashboards, lowering false-positive rates that plague vibration-only systems. Bio-acoustics and R&D niches, though small, drive specification-class instrumentation that often pioneers features later mainstreamed into industrial variants. Software roadmaps that push AI classifiers to the edge will tilt adoption further toward applications with clear monetary payback.

By End-User Industry: Automotive Leads, Utilities Post Fastest Growth

Automotive and mobility captured 34.52% share in 2025, reflecting deep NVH budgets and tight UNECE 138 compliance for pedestrian alerts in electric cars. Utilities and oil-and-gas will expand at 3.43% CAGR to 2031 as pipeline integrity programs and substation transformer checks adopt ultrasound payloads that prevent unplanned outages exceeding USD 1 million.

Aerospace and defense continue to buy high-channel-count arrays for multi-year aircraft and rotorcraft certification programs. Semiconductor and electronics lines deploy near-field imaging for board-level fault isolation, saving costly rework. Smart-manufacturing verticals integrate acoustic cameras with digital twins within Siemens- and Rockwell-promoted MES frameworks, while renewable-energy operators use drone rigs to inspect wind-turbine blades and solar inverters in regions with limited technician access.

Geography Analysis

Europe retained 34.82% share in 2025, anchored by the Environmental Noise Directive and a concentrated aerospace cluster spanning Toulouse, Hamburg, and Filton. Germany, the United Kingdom, and France collectively house more than half of the region’s NVH laboratories, and EASA’s CS-36 Amendment 6 is forcing engine makers to retrofit outdoor test ranges with 384-channel arrays. Spain and Italy are secondary growth centers thanks to drone-mounted ultrasound cameras used for renewable-energy inspections on wind farms in Andalusia and Lombardy. European accreditation bodies enforce ISO 9614 traceability more strictly than peers elsewhere, which increases calibration costs yet elevates measurement credibility for export-oriented manufacturers.

Asia-Pacific is projected to achieve the fastest 3.47% CAGR through 2031 because China’s New Energy Vehicle roadmap, Japan’s semiconductor investment surge, and South Korea’s smart-factory subsidies align to expand the acoustic camera market. Shanghai, Guangzhou, and Chongqing host joint-venture plants where NVH validation is now mandatory for electric models targeting domestic and export sales. South Korean conglomerates embed BATCAM FX arrays across multiple Hyundai plants, while India’s Make in India initiative accelerates handheld adoption in Chennai auto clusters. ABB’s partnership with Seoul-based Cochl deploys machine-listening AI on robots across Asian chemical and steel facilities, demonstrating high fault-detection accuracy.

North America held a considerable share in 2025, propelled by U.S. aerospace and defense programs such as the F-35 and 777X that require long-range far-field arrays for certification testing. Canadian utilities fly drone-borne ultrasound rigs along pipelines in Alberta and British Columbia, cutting helicopter costs. South America, the Middle East, and Africa together account for a small share, with Brazil’s Petrobras and Saudi Aramco piloting offshore leak-detection systems. Dubai’s smart-city projects integrate fixed-mount cameras into urban noise networks, yet harsh climate challenges microphone reliability, limiting deeper penetration.

Competitive Landscape

Market concentration is moderate; the five leaders-Hottinger Bruel and Kjaer, Teledyne FLIR, Siemens Digital Industries Software, Fluke Corporation, and Microflown Technologies a considerable combined share in 2025. Teledyne’s November 2025 purchase of NL Acoustics broadens its reach into underwater and bio-acoustics, signaling ongoing consolidation. Siemens now bundles Simcenter Testlab subscriptions with hardware, elevating switching costs for automotive and aerospace clients. Fluke supports robot integration, enabling autonomous inspections in hazardous zones with Boston Dynamics’ Spot quadruped robot.

Emerging entrants focus on AI classifiers and novel microphone technologies. Syntiant’s acquisition of Knowles’ MEMS unit marries neural-decision processors to microphone arrays, pushing beamforming to the edge. Optical MEMS innovators such as sensiBel and XARION bypass piezoelectric patents, offering extended bandwidth and temperature resilience. RESONIKS raised capital to commercialize acoustic weld inspection in automotive body shops, promising a 15% reduction in scrap.

Pricing bifurcation persists, handheld 2-D arrays trend below USD 15,000, while 384-channel 3-D rigs exceed USD 60,000 due to FPGA and calibration overhead. Vendors pursue subscription models that smooth revenue and lower entry barriers, but customers weigh OpEx premiums against CapEx savings. Cross-licensing deals, such as the 2024 accord between Microflown and HBK, reduce litigation risk yet underscore the complex patent landscape around delay-and-sum algorithms.

Acoustic Camera Industry Leaders

Hottinger Brüel & Kjær Sound & Vibration Measurement A/S

gfai tech GmbH

Teledyne FLIR LLC

Fluke Corporation

SM Instruments Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Teledyne Technologies acquired a majority stake in NL Acoustics, expanding into marine research and defense acoustic imaging.

- November 2025: XARION Laser Acoustics secured funding from In-Q-Tel to scale diaphragm-free optical microphones.

- September 2025: Syntiant Corporation acquired Knowles Corporation’s Consumer MEMS Microphones business for USD 150 million, marrying ultra-low-power neural processors with high-performance transducers.

- March 2025: ABB and Cochl partnered to embed AI listening algorithms into robotic inspections across Asia-Pacific industrial sites.

Global Acoustic Camera Market Report Scope

An acoustic camera is an imaging device that is used to locate sound sources and characterize these sound sources. The acoustic camera consists of a group of microphones, also called a microphone array, that is simultaneously acquired to represent the sound sources' location.

The Acoustic Camera Market Report is Segmented by Array Type (2-D Arrays and 3-D Arrays), Measurement Type (Near-Field and Far-Field), Frequency Band (Low-frequency below 10 kHz and Ultrasound above 20 kHz), Deployment Platform (Hand-held, Tripod/Fixed-mount, Drone/UAV-mounted, and Robot-integrated), Application (Noise Source Identification, Leak Detection, Mechanical Fault Diagnostics, Bio-acoustics, and Research and Development), End-user Industry (Automotive and Mobility, Aerospace and Defense, Electronics and Semiconductor, Energy and Power, Smart Manufacturing, Utilities/Oil and Gas, and Other Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 2-D Arrays |

| 3-D Arrays |

| Near-Field |

| Far-Field |

| Low-frequency |

| Ultrasound |

| Hand-held |

| Tripod / Fixed-mount |

| Drone / UAV-mounted |

| Robot-integrated |

| Noise Source Identification |

| Leak Detection |

| Mechanical Fault Diagnostics |

| Bio-acoustics |

| Research and Development |

| Automotive and Mobility |

| Aerospace and Defense |

| Electronics and Semiconductor |

| Energy and Power |

| Smart Manufacturing |

| Utilities / Oil and Gas |

| Other Industries |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Array Type | 2-D Arrays | |

| 3-D Arrays | ||

| By Measurement Type | Near-Field | |

| Far-Field | ||

| By Frequency Band | Low-frequency | |

| Ultrasound | ||

| By Deployment Platform | Hand-held | |

| Tripod / Fixed-mount | ||

| Drone / UAV-mounted | ||

| Robot-integrated | ||

| By Application | Noise Source Identification | |

| Leak Detection | ||

| Mechanical Fault Diagnostics | ||

| Bio-acoustics | ||

| Research and Development | ||

| By End-user Industry | Automotive and Mobility | |

| Aerospace and Defense | ||

| Electronics and Semiconductor | ||

| Energy and Power | ||

| Smart Manufacturing | ||

| Utilities / Oil and Gas | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the acoustic camera market by 2031?

The acoustic camera market is projected to reach USD 190.81 billion by 2031, growing at a 3.27% CAGR from 2026.

Which region shows the fastest growth for acoustic camera demand?

Asia-Pacific leads growth with a forecast 3.47% CAGR through 2031

Why are 3-D arrays important in acoustic applications?

3-D arrays localize noise sources in all three dimensions without sensor repositioning, which saves time during automotive and aerospace validation.

How are drone-mounted acoustic cameras used in utilities?

Utilities attach ultrasound payloads to drones to detect gas and air leaks along pipelines and power lines, reducing helicopter inspection costs by up to 70%.

What drives adoption of ultrasound frequency bands?

Ultrasound systems above 20 kHz excel at detecting compressed-air and steam leaks, offering quick payback by minimizing energy waste and unplanned downtime.

Page last updated on: