Vessel Energy Storage System Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

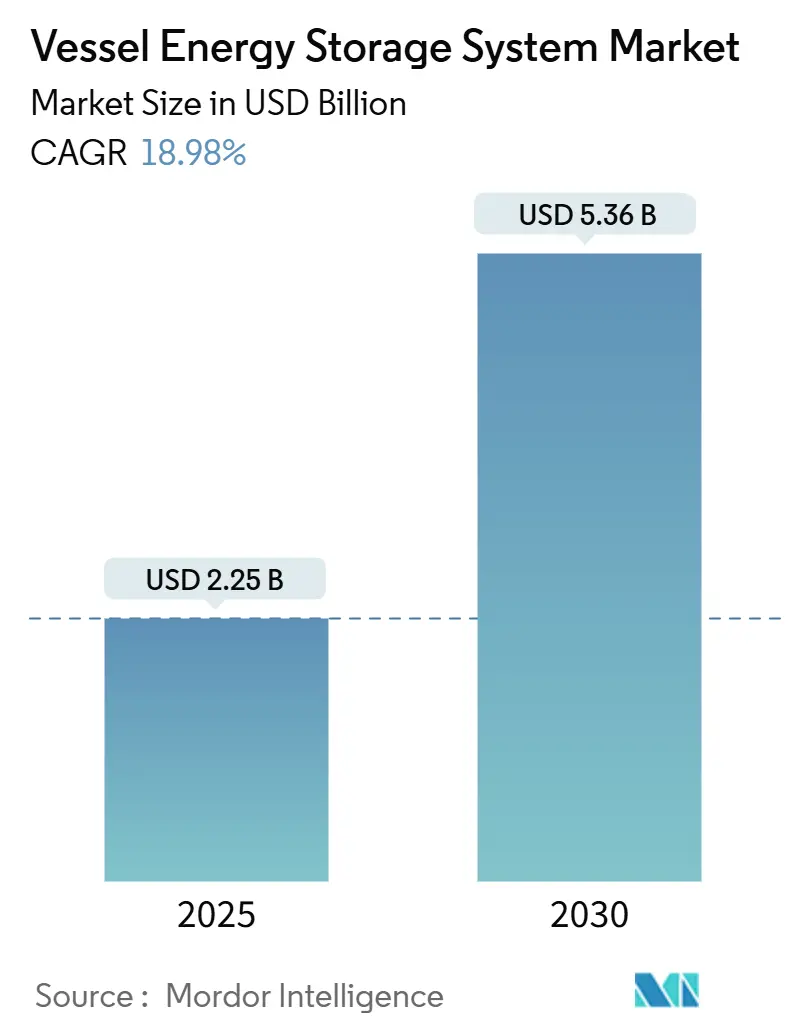

| Market Size (2025) | USD 2.25 Billion |

| Market Size (2030) | USD 5.36 Billion |

| Growth Rate (2025 - 2030) | 18.98% CAGR |

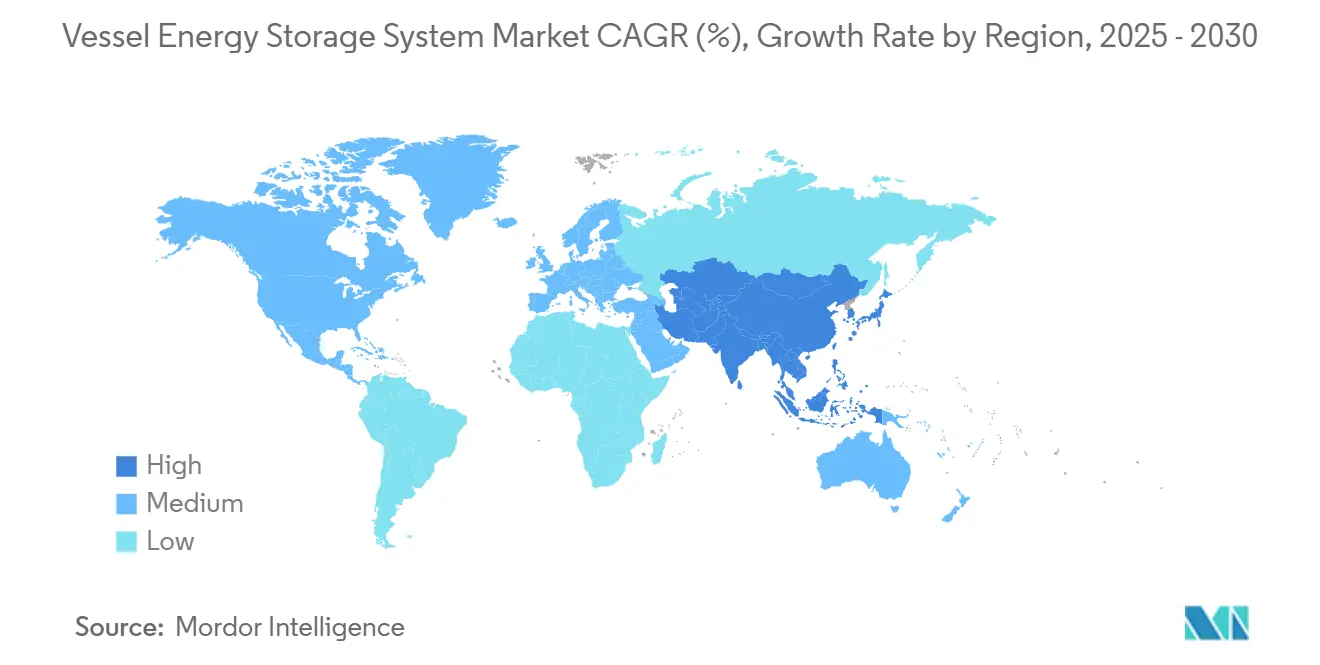

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vessel Energy Storage System Market Analysis by Mordor Intelligence

The Vessel Energy Storage System Market size is estimated at USD 2.25 billion in 2025, and is expected to reach USD 5.36 billion by 2030, at a CAGR of 18.98% during the forecast period (2025-2030).

Accelerating demand comes from International Maritime Organization (IMO) greenhouse-gas rules that restrict under-performing vessels, lithium-ion cost erosion, and rapid uptake of digital energy-management platforms. Operators now frame battery installations as profit centers that unlock flexible sailing profiles and shore-power revenues rather than as compliance expenses. Passenger-centred operators value the quieter ride and lower vibration of electric propulsion, while defense fleets seek battery power for stealth. Across regions, North America capitalizes on naval procurement budgets, Europe aligns with FuelEU Maritime mandates, and Asia-Pacific leverages its battery manufacturing base to scale ferry and submarine projects rapidly. Counterforces include insurer fire-risk premiums and capital-cost hurdles, yet innovative leasing models and inherently safer chemistries are easing both.

Key Report Takeaways

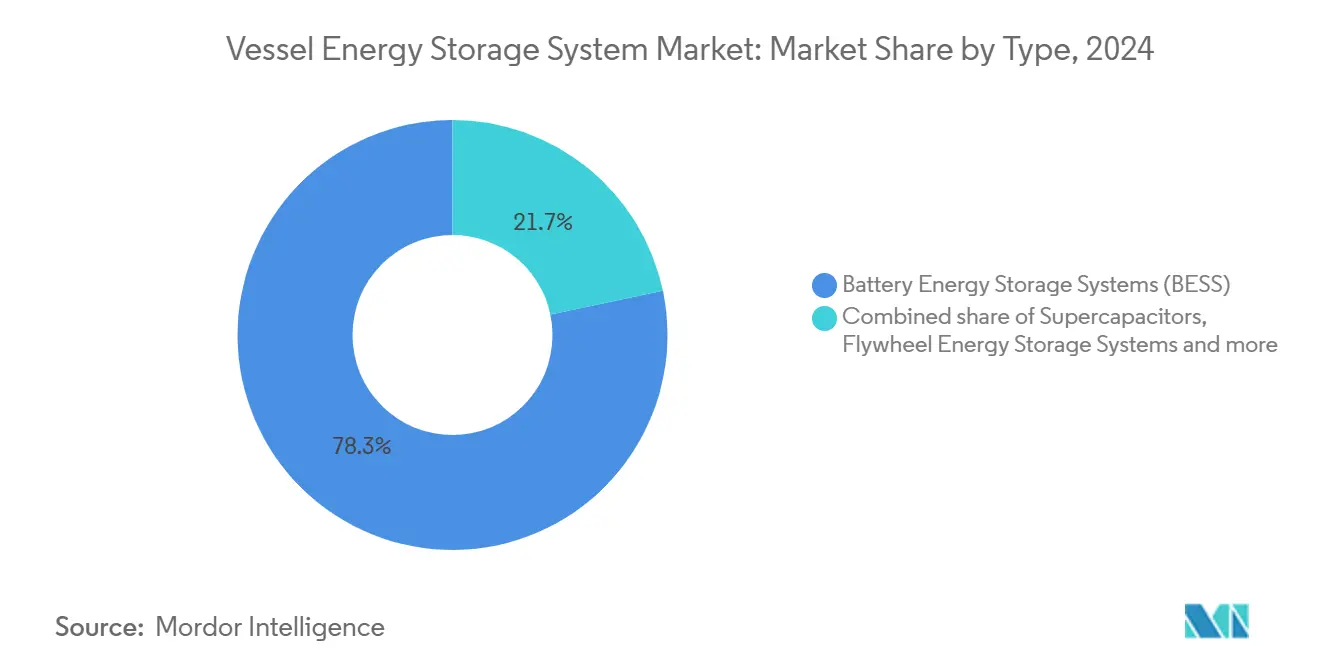

- By type, battery energy storage systems (BESS) led with 78.3% revenue share of the vessel energy storage system market size in 2024, while supercapacitors are projected to accelerate at a 21.5% CAGR through 2030.

- By energy source, hybrid configurations commanded 54.8% ofthe vessel energy storage system market share in 2024; fuel‐cell solutions are forecast to expand at a 35.7% CAGR between 2025 and 2030.

- By installation, newbuilds accounted for 81.9% of 2024 sales; retrofit programs posted the fastest 23.6% CAGR thanks to immediate Carbon Intensity Indicator penalties.

- By vessel type, passenger ships captured 38.6% of 2024 revenue; naval vessels posted the highest 22.2% CAGR to 2030.

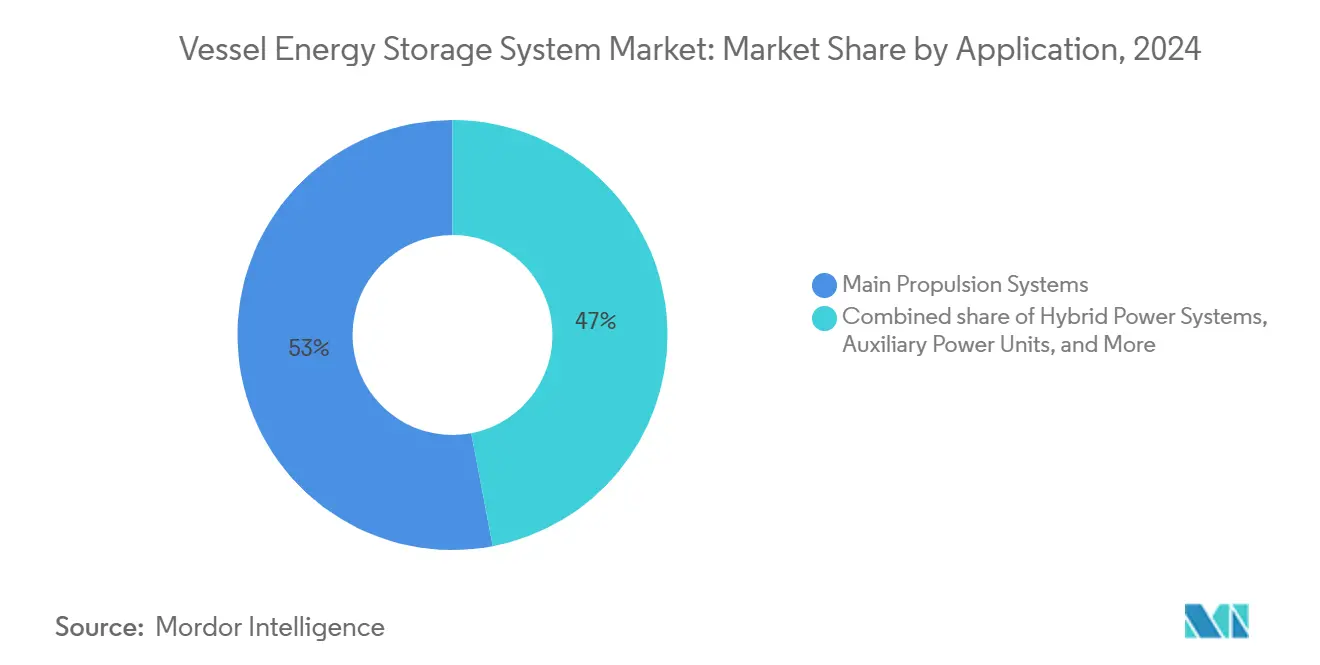

- By application, main-propulsion platforms represented 53.0% of 2024 demand; hybrid-power systems post a 21.0% CAGR over the same horizon.

- By geography, North America held 34.5% share in 2024 while Asia-Pacific heads the growth league at a 24.8% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vessel Energy Storage System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent IMO GHG & CII regulations | +4.20% | Global | Medium term (2-4 years) |

| Rapid decline in lithium-ion $/kWh | +3.80% | Global | Short term (≤ 2 years) |

| Acceleration of hybrid/fully-electric ferry programmes | +2.90% | Europe & Asia-Pacific | Medium term (2-4 years) |

| Port electrification & cold-ironing incentives | +2.10% | North America & Europe | Long term (≥ 4 years) |

| CII penalty-driven retrofit demand | +3.50% | Global | Short term (≤ 2 years) |

| Digital-twin EMS unlocking ESS ROI | +1.80% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent IMO GHG & CII Regulations

The IMO’s 2024 net-zero framework imposes operational ratings that limit port access and raise insurance premiums for inefficient ships, turning compliance into an existential cost for owners. FuelEU Maritime adds a 2025 renewable-fuel mandate for vessels above 5,000 GT in EU waters, further tightening margins. Energy storage lets operators shift propulsion loads, trim peak emissions on sensitive routes, and secure preferred charter rates. Revised life-cycle emissions guidelines now credit battery-enabled efficiency gains, turning early adopters into competitive frontrunners.

Rapid Decline in Lithium-Ion $/kWh

Marine-grade lithium iron phosphate packs have crossed the parity line with diesel gensets on high-cycle routes, driven by automaker scale and safer chemistries. Solid-state prototypes already hit 190 Wh/kg while maintaining IP67 waterproof integrity. Sodium-ion alternatives from DEFORD remove lithium-price exposure, and advanced battery-management systems now orchestrate charge cycles with real-time route analytics, squeezing out every kilowatt-hour of value.

Acceleration of Hybrid/Fully-Electric Ferry Programs

China’s super-capacitor ferry, Denmark’s Ellen, and Norway’s national fleet prove commercial viability, slashing operating expense by up to 30% on fixed routes. Shared shore-charging hubs multiply return on individual vessel investments. Standardization, from Nordic class rules to interoperable connectors, dismantles earlier adoption barriers and positions the vessel energy storage system market for replication across commuter corridors worldwide.

Port Electrification & Cold-Ironing Incentives

California, Rotterdam, and Singapore now reward vessels that shut generators at berth. The U.S. Department of Energy’s Blue Economy roadmap tags onboard storage as the lynchpin between coastal renewables and resilient grids.(1)Source: U.S. Department of Energy, “Blue Economy Initiative,” energy.govVessels equipped with high-capacity batteries capture grid-services revenue, schedule charging on off-peak tariffs, and even deliver emergency power ashore during outages, elevating the commercial logic of the vessel energy storage system market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ESS CAPEX vs diesel gensets | -2.80% | Global | Short term (≤ 2 years) |

| On-board volume-weight constraints | -1.90% | Global | Medium term (2-4 years) |

| Lithium carbonate price volatility | -1.50% | Global | Short term (≤ 2 years) |

| Marine insurer fire-risk premium | -2.20% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High ESS CAPEX vs Diesel Gensets

Complete marine battery systems still demand investments near USD 175,000 per MW, straining operators with tight cash flows. Conventional loan structures undervalue future fuel savings and expose owners to technology-obsolescence fears. Battery-as-a-service contracts and performance-guarantee leases are emerging to transfer upfront risk to specialist financiers, gradually softening this restraint.

Marine Insurer Fire-Risk Premium

Lithium-fire incidents have prompted Lloyd’s and Allianz to impose new suppression and training standards, pushing insurance costs upward.(2)Source: Allianz Global Corporate & Specialty, “Lithium-Battery Risks in Marine,” allianz.com Safer LFP chemistries and rigorous type approvals are trimming premiums, but data scarcity still inflates actuarial models. As the loss record stabilizes, insurers are expected to recalibrate rates, particularly for vessels employing compartmentalized, gas-safe battery rooms certified by DNV and ABS.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Battery Leadership Catalyzes Innovation

Battery Energy Storage Systems controlled 78.3% of the vessel energy storage system market share in 2024 as measured by installed value, largely due to automotive learning curves that cut delivered marine pack prices below USD 450 per kWh. That dominance translates into a substantial 21.5% CAGR pipeline through 2030, driven by solid-state promises of higher density and lower fire risk. In parallel, supercapacitors prosper in ultrafast charge-discharge ferry routes, and flywheels serve naval pulse-power niches where infinite cycling is paramount. Compressed air energy storage (CAES) remains restricted by hull-volume penalties, while vanadium flow batteries recently earned ABS technology qualification for long-duration offshore research vessels. Start-ups now promote hybrid packs that blend capacitors, lithium, and flow cells into a single rack, offering operators a best-of-all-worlds profile without sacrificing space.

The vessel energy storage system market sees battery integrators chasing maritime-specific safety certifications such as DNV’s Propagation Test A. Top suppliers bundle batteries with proprietary fire-suppression, cooling, and data analytics layers to differentiate beyond raw kilowatt-hour pricing. Licensing military-grade lithium thermal-runaway barriers into commercial ferries is narrowing the technology gulf between defense and civilian segments, expanding addressable opportunities for battery vendors.

By Energy Source: Hybrid Architectures Dominate the Transition

Hybrid systems took 54.8% of the total 2024 revenue as owners hedge propulsion risk by pairing batteries with diesel or LNG engines, allowing compliance on coastal legs without jeopardizing trans-ocean autonomy. Fuel cells, posting a 35.7% CAGR, ride the momentum of hydrogen bunkering corridors emerging across Scandinavia and Japan. Renewable-only platforms, though still niche, gain traction through photovoltaic decks and auxiliary wind rotors feeding onboard batteries. Conventional engines now operate increasingly in generator-optimizing “spinning reserve” modes, cutting fuel burn by up to 20% when linked to energy storage.

Innovation centers on control software that arbitrates between multiple generations and storage devices in real time. Corvus Energy’s inherently gas-safe fuel-cell module earned DNV approval in 2024, catalyzing integration of hydrogen stacks into ferry and offshore support hulls. PowerX’s battery tanker concept reimagines ships as mobile storage assets, underlining how the vessel energy storage system market stretches beyond propulsion into floating grid infrastructure.

By Installation Configuration: Retrofit Wave Builds Momentum

Newbuild projects still controlled 81.9% of 2024 deployments, benefitting from clean-sheet naval architecture that positions battery rooms low and central for optimal stability. Yet retrofit activity is accelerating at a 23.6% CAGR because CII penalties take effect quicker than shipyard queues permit new deliveries. Containerized battery pallets, launched through programs like LOC-NESS, shorten yard stays to mere days, allowing owners to target the worst-rated hulls first.

The economic calculus favors retrofits whenever remaining hull life exceeds five years and daily fuel spend tops USD 7,000. Digital-twin modeling predetermines module placement down to centimeter tolerances, de-risking structural modifications and cabling runs. Classification bodies have streamlined plan-approval workflows for repeatable containerized packages, cutting administrative lead-times by 40%.

By Vessel Type: Defense Electrification Spurs Breakout Growth

Passenger operators led the 2024 revenue table with 38.6% share, capitalizing on silent running, low-vibration cabins, and port-emission incentives.(3)Source: Samsung SDI, “High-Energy Maritime Batteries,” samsungsdi.com Though smaller in unit count, Naval platforms book a leading 22.2% CAGR as submarines and surface combatants pursue near-silent endurance. Cargo ships enter energy-storage upgrades primarily to avoid Emission Control Area surcharges, while fishing and offshore support vessels value lower maintenance and improved crew comfort. Research ships join the “Others” category, using batteries to eliminate generator noise that can corrupt scientific sensors.

Military demand accelerates technology maturity: Hanwha Ocean’s submarine battery trial for the Korean Navy features 40% higher power density than commercial packs, technology likely to cascade into civilian hulls once declassified. Passenger ferry operators, meanwhile, set benchmarks in charge-cycle throughput, offering valuable duty-cycle data to the wider vessel energy storage system market.

By Application: Propulsion Systems Steer Budget Priorities

Main propulsion projects captured 53.0% of the 2024 investment, reflecting the pivot toward full or partial electric drive lines in short-sea corridors. Hybrid-power trains, the fastest-growing application at 21.0% CAGR, give owners operational agility under evolving regional rules. Batteries assigned to auxiliary loads extend generator maintenance cycles by 800 hours annually and improve hotel-load efficiency during layovers. Emergency-power packages meet SOLAS requirements while doubling as peak-shaving resources during maneuvering.

Regenerative braking during harbor deceleration and crane loading now back-feeds into onboard storage, squeezing extra returns from existing capital. Integrated energy-management suites present a single interface across propulsion, hotel, and cargo-handling subsystems, standardizing crew training and simplifying compliance audits.

Geography Analysis

North America led 34.5% of 2024 revenues, boosted by the U.S. Navy’s USD 45 million LOC-NESS program and California’s cold-ironing rules that penalize auxiliary-engine use at berth. Shipbuilders across the Gulf Coast integrate battery rooms as standard options on new PSV orders, and Canadian Great Lakes operators retrofit bulk carriers to meet forthcoming provincial carbon caps.

Europe benefits from FuelEU Maritime’s renewable-fuel thresholds and Norway’s fully-electric ferry network, producing a dense ecosystem of class rules, yard experience, and financing instruments. Hybrid tug pilots in Rotterdam and tri-fuel cruise concepts in the Baltic accelerate technology diffusion. European battery suppliers partner with wind-farm developers to bid combined vessel-plus-grid services, blurring sector lines and expanding the vessel energy storage system market.

Asia-Pacific records the steepest 24.8% CAGR, underpinned by China’s battery-cost leadership and South Korea’s naval contracts. Japan’s PowerX envisions battery tankers moving offshore wind power to consumption centers, showcasing new revenue models. Subsidies for zero-emission inter-island ferries across Indonesia and the Philippines open significant downstream demand, while Australia’s Blue Highway concepts integrate vessel storage into coastal hydrogen value chains.

Competitive Landscape

The vessel energy storage system market remains moderately fragmented: the top five players account for roughly 32% of installed capacity, leaving room for regional specialists. ABB, Wärtsilä, Siemens Energy, and Corvus package turnkey propulsion, while Samsung SDI, CATL, BYD, and LGES supply cells under marine-specific safety regimes. Partnerships dominate strategy—Samsung SDI allies with Hanwha Ocean on naval packs, and ABB integrates AYK Energy’s prismatic modules into cruise retrofits.

Differentiation drifts from raw cell pricing toward integrated safety, cyber-secure EMS software, and lifecycle guarantees. Vendors now offer performance-based service agreements that monetize uptime rather than kilowatt-hours sold. New entrants focus on niche chemistries—sodium-ion from DEFORD, vanadium flow from Shift Clean Energy—and modular racking for retrofits. As class-society testing matures, quoting times shorten and bidding pools widen, pressuring incumbents to refresh offerings every design cycle.

Regulatory endorsement is a decisive moat; DNV, ABS, and Lloyd’s approvals become passports to international bids. Players investing early in gas-safe designs or military-grade propagation barriers lock in premium margins across civilian segments. Collectively, these dynamics keep price competition tempered and sustain technology-innovation cycles that underpin the vessel energy storage system market.

Vessel Energy Storage System Industry Leaders

Corvus Energy

Wärtsilä Corp.

ABB Ltd.

Siemens Energy AG

Leclanché SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AYK Energy marine battery systems received validation from DNV, enhancing their credibility in the marine energy storage sector and enabling broader market adoption.

- April 2025: Samsung SDI and Hanwha Ocean announced plans to test a jointly developed lithium-ion battery system for submarines with the South Korean Navy in Q3 2025, potentially revolutionizing naval propulsion systems.

- April 2025: DEFORD New Power Co. launched marine sodium-ion batteries including the NA1260, NA1270, and NA12100 Pro models, offering high cycle life and integrated battery management systems for marine applications.

- September 2024: Corvus Energy received DNV type approval for its inherently gas-safe marine fuel cell system, marking a significant advancement in marine energy storage technology.

- August 2024: NYK signed a basic agreement for marine transport of approximately 200,000 metric tons of green ammonia annually from India to Japan, emphasizing commitment to sustainable energy supply chains.

Global Vessel Energy Storage System Market Report Scope

| Battery Energy Storage Systems (BESS) |

| Supercapacitors |

| Flywheel Energy Storage Systems |

| Compressed Air Energy Storage (CAES) |

| Others |

| Renewable Energy Sources |

| Conventional Energy Sources |

| Hybrid Systems |

| Fuel Cells |

| Others |

| Newbuild |

| Retrofit |

| Cargo Ships |

| Passenger Ships |

| Naval Vessels |

| Fishing Vessels |

| Offshore Support Vessels |

| Others |

| Auxiliary Power Units |

| Main Propulsion Systems |

| Emergency Power Supply |

| Renewable Energy Integration |

| Hybrid Power Systems |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Battery Energy Storage Systems (BESS) | |

| Supercapacitors | ||

| Flywheel Energy Storage Systems | ||

| Compressed Air Energy Storage (CAES) | ||

| Others | ||

| By Energy Source | Renewable Energy Sources | |

| Conventional Energy Sources | ||

| Hybrid Systems | ||

| Fuel Cells | ||

| Others | ||

| By Installation Configuration | Newbuild | |

| Retrofit | ||

| By Vessel Type | Cargo Ships | |

| Passenger Ships | ||

| Naval Vessels | ||

| Fishing Vessels | ||

| Offshore Support Vessels | ||

| Others | ||

| By Application | Auxiliary Power Units | |

| Main Propulsion Systems | ||

| Emergency Power Supply | ||

| Renewable Energy Integration | ||

| Hybrid Power Systems | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which technology currently leads commercial adoption of vessel batteries?

Battery Energy Storage Systems dominate with a 78.3% share in 2024 due to lithium-ion cost declines and mature safety certifications.

How fast is Asia-Pacific growing in marine battery demand?

The region registers a 24.8% CAGR through 2030, the fastest globally, propelled by Chinese ferry electrification and Korean naval programs.

What drives retrofit activity in existing fleets?

Immediate Carbon Intensity Indicator penalties and modular containerized battery racks are pushing retrofit growth at a 23.6% CAGR.

Are fuel cells poised to overtake batteries in ships?

Fuel cells grow briskly at 35.7% CAGR but still rely on emerging hydrogen bunkering networks; batteries remain the primary energy buffer.

How do port electrification mandates influence investment?

Shore-power rules reward vessels that can switch off generators, making large onboard batteries essential for both emissions reduction and grid-service revenues.

Page last updated on: