Offshore Mooring System Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.8 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

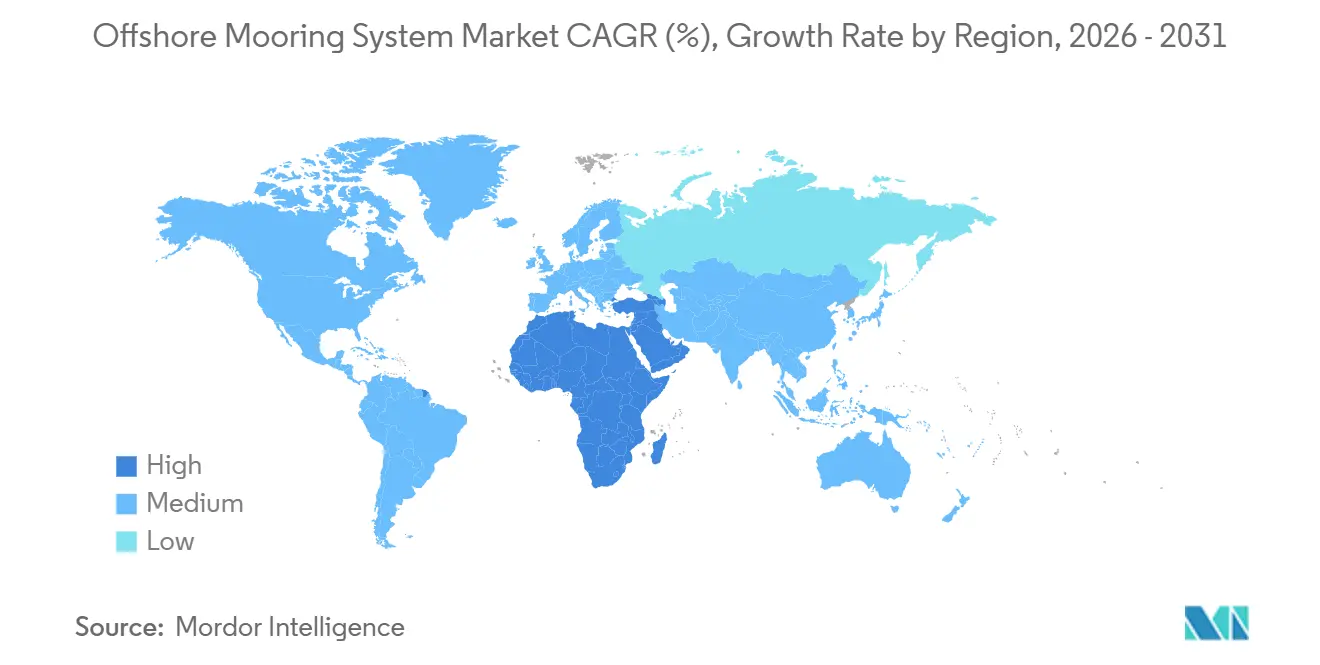

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

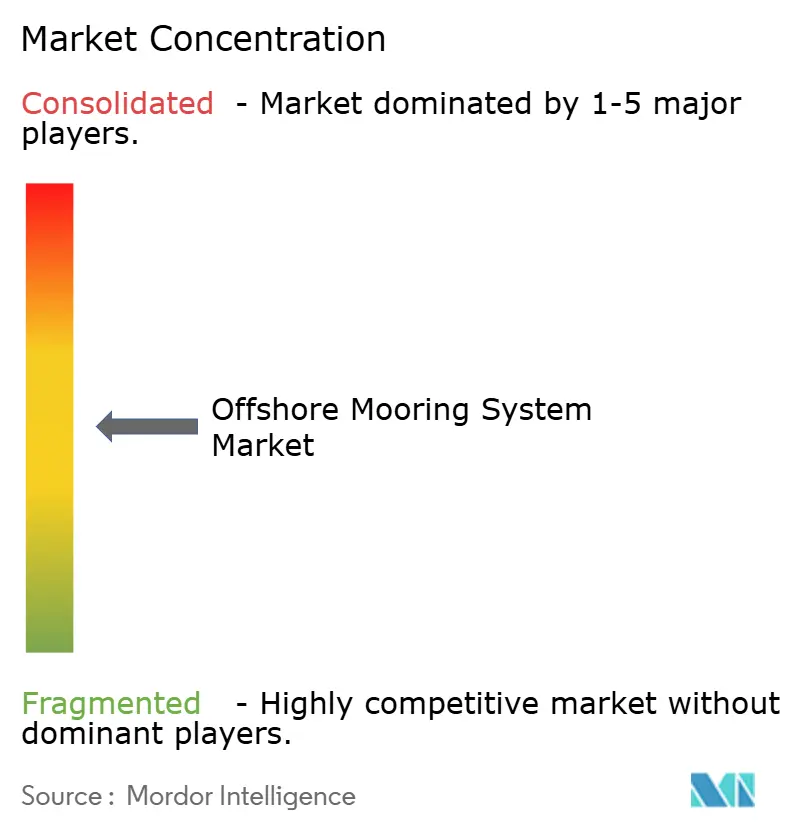

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Offshore Mooring System Market Analysis by Mordor Intelligence

The Offshore Mooring System Market size is projected to be USD 1.73 billion in 2025, USD 1.8 billion in 2026, and reach USD 2.18 billion by 2031, growing at a CAGR of 3.89% from 2026 to 2031. The sector is shifting from its historic reliance on deep-water oil production toward a dual-track demand profile that also includes pre-commercial floating wind arrays above 50 MW and deep-water gas developments in the Eastern Mediterranean and Mozambique. Deep-water projects between 400 m and 1,500 m captured 45.2% of 2025 revenue, while ultra-deep deployments beyond 1,500 m are expanding at 4.8% a year as operators chase pre-salt reserves in Brazil and frontier gas fields off Mozambique. Anchors retained the single-largest component share at 34.9% in 2025, yet synthetic fiber ropes are advancing at 5.4% annually because they trim suspended weight and extend fatigue life relative to steel chains. Asia-Pacific led with 37.8% of 2025 installations on the back of China’s cylindrical FPSO roll-out and South Korea’s growing floating wind pipeline, whereas the Middle East and Africa registered the fastest regional growth at a 4.7% CAGR as Qatar’s North Field expansion and East Mediterranean gas finds ramp up.

Key Report Takeaways

- By Mooring Type, Spread Mooring accounted for 25.5% of the offshore mooring system market share in 2025, and the Catenary segment is forecast to log a 4.3% through 2031.

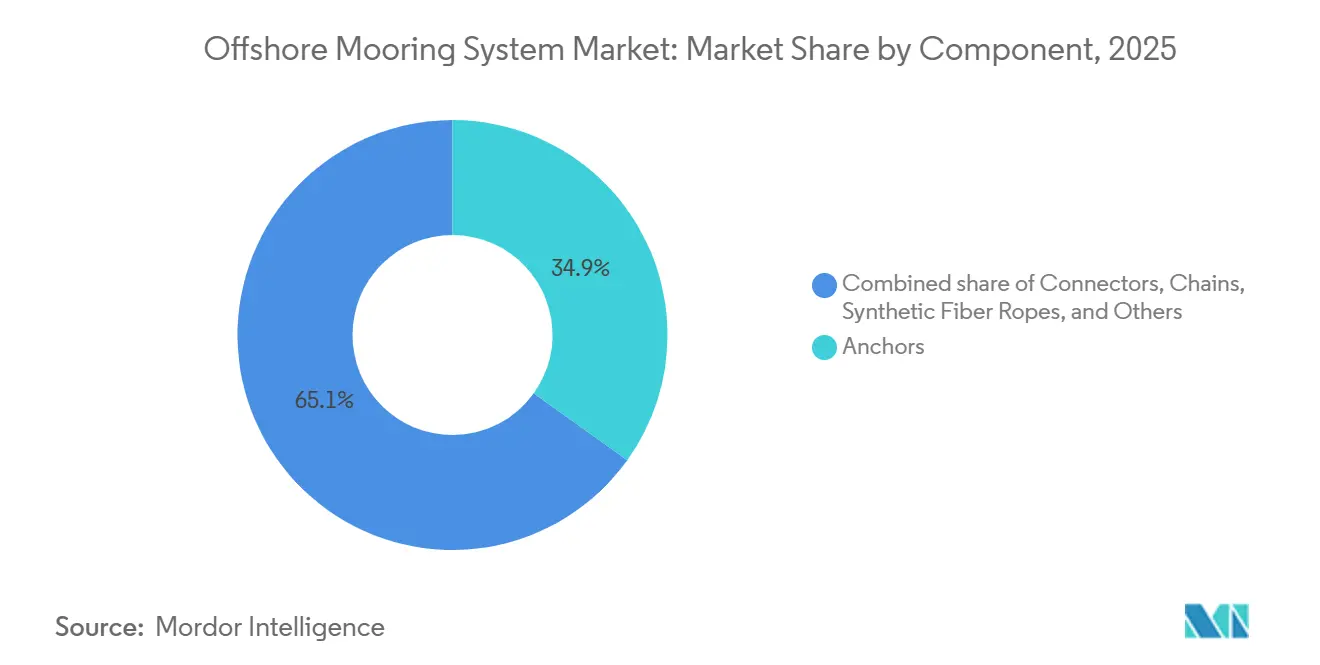

- By component, anchors accounted for 34.9% of the 2025 revenue pool, while synthetic fiber ropes are projected to increase at a 5.4% CAGR during 2026-2031.

- By depth, deep-water installations commanded 45.2% of the offshore mooring system market share in 2025; the ultra-deep segment is forecast to log a 4.8% CAGR through 2031.

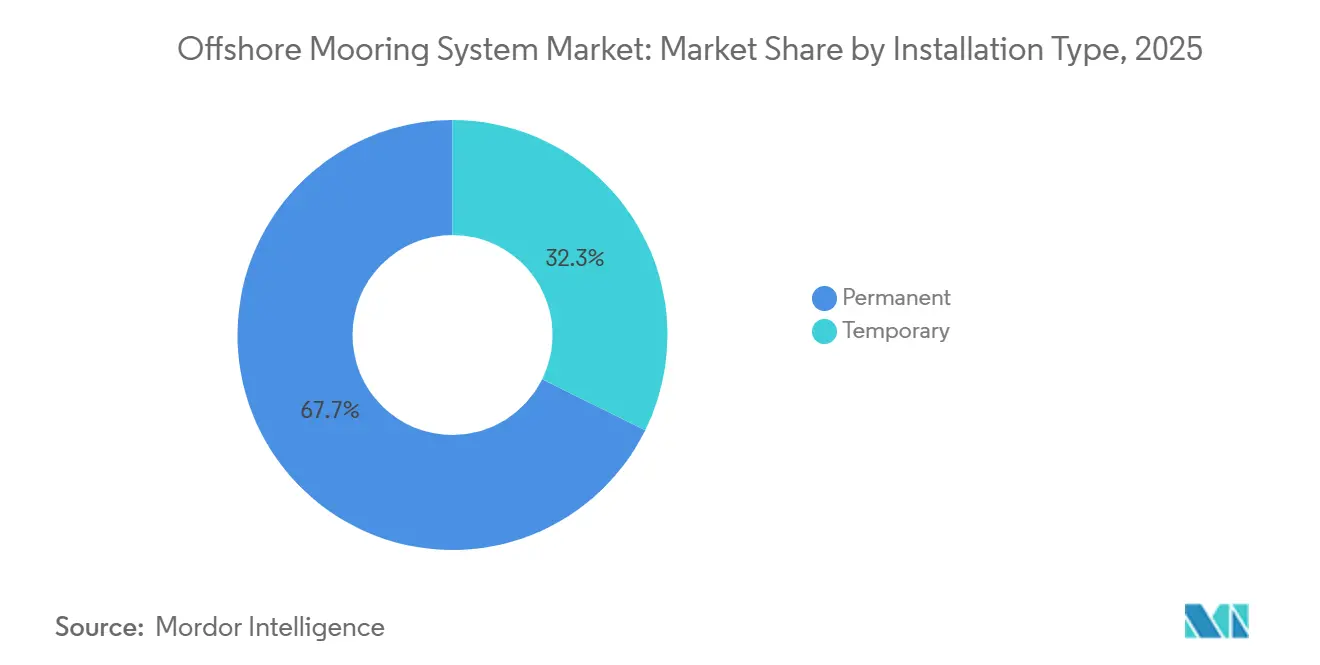

- By installation type, permanent systems represented 67.7% of 2025 activity, but temporary spreads are projected to rise at a 4.1% CAGR over the forecast horizon.

- By application, FPSOs led with 39.4% of 2025 installations, whereas spar platforms are poised for a 5.2% CAGR through 2031.

- By geography, Asia-Pacific captured 37.8% of 2025 revenue, whereas the Middle East and Africa is set to post the fastest 4.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Offshore Mooring System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising FPSO backlog in Brazil & Guyana | +1.20% | South America, with spillover to West Africa | Medium term (2-4 years) |

| Growing CAPEX on deep-water gas in East Med & Mozambique | +0.90% | Middle East & Africa, Southern Europe | Long term (≥ 4 years) |

| Surge in pre-commercial floating wind arrays (≥50 MW) | +1.40% | Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Rapid uptake of polyester & HMPE ropes to cut weight | +0.70% | Global, led by North Sea and Gulf of Mexico | Short term (≤ 2 years) |

| Digital twins for mooring fatigue monitoring (AI-enabled) | +0.50% | Global, early adoption in Norway and UK | Long term (≥ 4 years) |

| Multipurpose energy-island hubs needing hybrid moorings | +0.60% | North Sea, Baltic Sea, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising FPSO Backlog in Brazil & Guyana

Brazil’s pre-salt provinces and Guyana’s Stabroek Block collectively host more than 900,000 bpd of production, creating record demand for purpose-built FPSOs that rely on advanced catenary and taut-leg mooring systems. Operators such as SBM Offshore and MODEC are setting new benchmarks for integrating mooring hardware with subsea architecture, which influences global specification frameworks for load management, corrosion protection, and digital monitoring. As FPSO counts in the region climb toward ten units in service by 2030, supply-chain pressure on anchor forging and chain manufacturing is intensifying, underpinning a positive demand trajectory for the offshore mooring systems market. The regional cluster also acts as a live testbed for predictive-maintenance analytics that shorten inspection campaigns and mitigate failure risk in high-current, high-fatigue environments. These learnings are expected to cascade into newbuild projects worldwide and relax design conservatism without compromising safety margins.

Growing CAPEX on Deep-water Gas in East Med & Mozambique

Total 2024-2025 committed expenditure exceeds USD 12 billion across Aphrodite, Leviathan Phase 2, and Coral South FLNG, prompting bespoke mooring designs able to withstand LNG off-take loads and emergency disconnection scenarios(1)Source: Chevron Corporation, “Leviathan Phase 2 Update,” chevroncorp.gcs-web.com . Ultra-deep settings above 1,500 m require hybrid arrangements that combine high-grade chain in touch-down zones with low-weight HMPE sections to maintain vertical compliance while curbing topside motion. Regulatory focus on rapid gas-to-market schedules compels early procurement, pushing mooring system specification to front-end engineering design (FEED). Consequently, project developers emphasize standardization of load cells, position reference sensors, and quick-release connectors to hedge against vessel scarcity. This dynamic is expected to introduce transferable module designs across future floating LNG builds, reinforcing growth prospects for the offshore mooring systems market.

Surge in Pre-commercial Floating Wind Arrays (≥50 MW)

Japan’s JERA placed a 2025 tension-leg floating wind project in 120 m water, while South Korea’s 1.125 GW KF Wind concession will install catenary moorings across 100-150 m depths. DNV projects global floating wind capacity to reach 250 GW by 2050 from 100 MW in 2024, catalyzing demand for lightweight, reusable moorings that enable turbine maintenance without heavy-lift vessels(2)Source: DNV, “Floating Offshore Wind: The Power to Commercialize,” dnv.com . France’s PAREF initiative demonstrates how shared anchors and polyester-chain hybrids can reduce hardware mass by up to 35%, accelerate hook-up, and limit seabed disturbance. Because wind turbines generate cyclical thrust loads rather than constant horizontal forces, mooring layouts require enhanced damping and state-of-charge monitoring to avoid resonance. Consequently, digital twins integrating nacelle load data with station-keeping models are becoming standard features. These developments steer the offshore mooring systems market toward products optimized for lower vertical loads, simplified installation, and environmental stewardship.

Rapid Uptake of Polyester & HMPE Ropes to Cut Weight

Samson’s SURESHIELD-EPX and Lankhorst’s hybrid constructions deliver up to 50% installation-time savings by reducing lift counts and vessel mobilization days.(3)Source: Samson Rope Technologies, “SURESHIELD-EPX Product Note,” samsonrope.com Operators initially restrict application to depths where chain-out mass is prohibitive, but performance verification data accelerates broader adoption. Weight savings enable smaller anchor-handling tug supply vessels, slash fuel burn, and lower CO₂ emissions targets, factors increasingly embedded in tender scoring. The trend redistributes value from steel-chain forges to advanced fiber producers, reshaping supply-chain bargaining power within the offshore mooring systems market. Complementary connector technologies now feature integrated bend-limiter sleeves and fiber-compatible sockets, mitigating abrasion and enabling 20-year design lives even under high-fatigue regimes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-lead chain & anchor forging capacity bottlenecks | -0.80% | Global, acute in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Cost overruns from subsea installation vessel scarcity | -0.60% | North America, North Sea, West Africa | Medium term (2-4 years) |

| Insurance premiums rising after recent mooring failures | -0.40% | Global, concentrated in North Sea and Gulf of Mexico | Short term (≤ 2 years) |

| End-of-life decommissioning liability uncertainty | -0.50% | North Sea, Gulf of Mexico, mature basins | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long-lead Chain & Anchor Forging Capacity Bottlenecks

Anchor chain lead times have widened from 12-15 months to 18-24 months for diameters above 120 mm, and stockless anchor deliveries exceed 200 tons each, stressing Asia-Pacific forges operating near peak capacity. The backlog constrains project scheduling flexibility, compels early material reservations, and inflates working capital needs for fabricators. Integrated contractors such as Saipem7 now hedge risk by acquiring minority stakes in chain suppliers, illustrating vertical integration as a mitigation pathway. Smaller engineering boutiques dependent on spot procurement face erosion of competitiveness, which could slow overall expansion of the offshore mooring systems market in the near term.

Cost Overruns from Subsea Installation Vessel Scarcity

Day rates for heavy-lift subsea installation units have surpassed USD 500,000, with newbuilds like the Charybdis wind-turbine installation vessel costing USD 715 million. Limited fleet renewal and yard congestion postpone delivery slots, forcing developers to compromise on optimal weather windows, extend hook-up campaigns, or shift to phased mooring installation strategies. Vessel scarcity disproportionately impacts floating wind projects that require simultaneous handling of turbine foundations and moorings, amplifying balance-of-plant cost volatility. Consequently, procurement models now emphasize modular, pre-assembled mooring packages that minimize deck re-rigging and crane lifts, a shift that may temper the restraint’s negative drag on the offshore mooring systems market beyond 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mooring Type: Catenary Configurations Gain Share

Catenary systems expanded at 4.3% in 2025, overtaking the offshore mooring system market growth rate as floating-wind projects gravitate toward their lower CAPEX and simpler hardware. Spread moorings held 25.5% of 2025 revenue for FPSO station-keeping, yet single-point variants are preferred in West Africa, where weathervaning trims line loads by 30%.

Semi-taut designs surface in floating wind, valued for a smaller seabed footprint. Operators increasingly combine types; Trelleborg’s tandem scheme on three Angola FPSOs allows offloading while preserving spread integrity. Suppliers marketing modular spreads that pivot among catenary, semi-taut, and taut-leg choices without redesign gain a commercial edge.

By Component: Synthetic Ropes Disrupt Anchor Dominance

Anchors captured 34.9% of 2025 revenue, yet ropes are advancing 5.4% per year, lifting the offshore mooring system market size for synthetic components. Vryhof’s STEVPRIS and VLA anchors proved holding capacities above 1,500 t in soft clay across Congo and Trinidad awards. Steel chain still rules the lower catenary in the market as hybrid spreads shorten overall chain length.

Connectors fueled by demand for 2,000 t break-load shackles that pair with HMPE ropes. Integration is a differentiator: Cortland’s AeroLock bundles rope and connector, cutting vessel time and boosting supplier margin.

By Depth: Ultra-Deep Water Pulls Investment

Ultra-deep installations beyond 1,500 m are logging a 4.8% CAGR and expanding offshore mooring system market share among operators targeting Brazil’s pre-salt and Mozambique’s gas. Deep-water projects between 400 m and 1,500 m still generated 45.2% of 2025 revenue, sustained by Gulf of Mexico and West Africa FPSOs.

Shallow-water fields below 400 m are decelerating as mature basins hit late-life decline. Advances in polyester and HMPE ropes extend feasible catenary depths past 3,000 m, further eroding the old depth-based design tiers.

By Installation Type: Temporary Systems Serve Exploration Surge

Permanent moorings delivered 67.7% of 2025 installations, reinforced by 20-25-year field lives that amortize high upfront spend. Temporary spreads are growing 4.1% on the back of frontier exploration in Guyana, Suriname, and Namibia, enlarging the offshore mooring system market size for leased equipment. Rental models price a complete 8-line spread at USD 2-3 million per year, against USD 12-15 million to buy.

Quick-release connectors from Bexco cut rig move time by two days, saving USD 150,000 per move. Floating-wind pilots still lean on permanent lines to sidestep regulatory gray areas; suppliers able to certify 2-5-year rope life under cyclic loads can open a new revenue stream.

By Application: Spar Platforms Resurge in Hurricane Zones

FPSOs led 2025 uptake at 39.4%, but spars are pacing a 5.2% CAGR through 2031 thanks to superior motion damping in hurricane-prone Gulf of Mexico blocks.

Semisubs, versatile workhorses of the offshore industry, are projected to capture a significant share of the market by 2031. In contrast, tension-leg platforms are struggling with modest growth, hindered by the challenges posed by soft seabeds on tether geotechnics. The demand for anchors surges with turbine counts, overshadowing the need for a single FPSO. As the offshore mooring system market diversifies, suppliers who craft bespoke wind-specific moorings, rather than merely adapting designs from the oil sector, stand to gain the most.

Geography Analysis

Asia-Pacific commanded 37.8% of 2025 revenue, led by China’s cylindrical FPSOs, South Korea’s KF Wind concession, and Japan’s JERA tension-leg pilot. Shinan-Ui and Nakwol wind farms validated 80-120 m catenary designs in 2025, demonstrating how local subsidies transform prototypes into commercial scale. India’s Tamil Nadu and Gujarat coastlines show floating economics even in 40-60 m, expanding supplier pipelines beyond oil projects.

The Middle East and Africa are the fastest-growing regions at 4.7% CAGR, energized by Qatar’s North Field, East Med gas, and Mozambique’s Coral North FLNG, whose 2,000 m polyester taut-legs raised regional demand for digital fatigue models. Saudi Aramco’s 90 m Marjan field expansion applied deep-water mooring tech in shallow water to shrink seabed footprint. Angola and Nigeria continue tandem offloading adoption, reinforcing anchor-connector demand.

Denmark’s Bornholm and Belgium’s Princess Elisabeth energy islands together add 6.5 GW of hybrid mooring scope by 2030. Norway’s tightened 2025 rules oblige operators to post decommissioning security, steering designs toward lighter synthetic lines that trim removal cost by 30%. Europe is forecast to cross an inflection in 2028 when floating-wind installations eclipse oil and gas moorings.(4)Danish Energy Agency, “Bornholm Energy Island Feasibility,” ens.dk

Competitive Landscape

The Offshore Mooring System Market is expected to be moderately fragmented. Component specialists, Vryhof Anchors, Trelleborg, Mampaey Offshore, and Lankhorst Ropes, compete on anchor holding power, rope fatigue resilience, and connector reliability. Trelleborg’s December 2024 takeover of Mampaey integrates anchors, connectors, and fendering under one roof, a scale play aimed at floating-wind bids.

Digital twins form the next wedge. TU Delft showed 92% fatigue-prediction accuracy in 2025 by fusing sensor data with physics engines, extending inspection from five to seven years. Equinor applied a similar twin on Hywind Scotland, pre-empting a connector failure. Smaller firms such as First Subsea (subsurface buoys) and Franklin Offshore (quick-release connectors) capture niche demand ignored by volume players. DNV’s 2025 standard now mandates synthetic-rope fatigue validation, favoring suppliers with in-house test benches over those outsourcing certification.

Offshore Mooring System Industry Leaders

SBM Offshore

MODEC Inc.

BW Offshore

Delmar Systems

SOFEC Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SBM Offshore secured a contract from Petrobras for the Almirante Tamandaré FPSO, which is designated for Brazil's pre-salt Búzios field. The FPSO features mooring systems designed for water depths of 2,100 meters and a production capacity of 180,000 barrels per day. This development reinforces Brazil's position as the largest FPSO market and validates the use of hybrid catenary-synthetic rope configurations in ultra-deep water.

- July 2025: Saipem and Subsea7 have officially completed their merger, creating a new global energy engineering and services powerhouse called Saipem7. The combined entity brings together two of the world’s leading offshore engineering and construction firms, with a staggering EUR 43 billion order backlog, making it one of the largest players in the subsea and energy infrastructure sector.

- June 2025: Technip Energies recently announced that it will lead the French floating wind R&D project called PAREF, which emphasizes the development of reusable anchoring systems to reduce costs and environmental impact. The project is funded under France 2030 and will provide anchoring technology for the NextFloat floating wind initiative.

- April 2025: Chevron officially commences production at its Ballymore deepwater project in the Gulf of Mexico. The subsea tieback connects three wells to the existing Blind Faith facility, with expected output of up to 75,000 barrels of oil per day. This milestone underscores the growing uptake of deepwater mooring and subsea technologies in large‑scale offshore developments.

Global Offshore Mooring System Market Report Scope

An offshore mooring system is a station-keeping structure that secures floating platforms, rigs, or vessels to the seabed using anchors and lines, which may consist of chains, wires, or synthetic ropes. These systems provide stability, prevent drifting, and maintain position against forces such as wind, waves, and currents. The primary types of mooring systems include catenary, taut-leg, and turret mooring.

The Offshore Mooring System Market is segmented into mooring type, component, depth, installation type, application, and geography. By mooring type, the market is segmented into spread, single point, dynamic positioning, catenary, taut leg, semi-taut, and others. By component, the market is segmented into anchors, connectors, chains, synthetic fiber ropes, buoys, and others. By depth, the market is segmented into shallow water (≤400 m), deep water (400–1500 m), and ultra-deep water (>1500 m). By installation type, the market is segmented into permanent and temporary systems. By application, the market is segmented into FPSO, TLP, semi-submersibles, spar, floating wind, and others. The report also covers the market size and forecasts for the offshore mooring system market in 21 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Spread Mooring |

| Single Point Mooring |

| Dynamic Positioning |

| Catenary |

| Taut Leg |

| Semi-taut |

| Others |

| Anchors |

| Connectors |

| Chains |

| Synthetic Fiber Ropes |

| Buoys |

| Others |

| Shallow Water (Up to 400 m) |

| Deep Water (400 to 1 500 m) |

| Ultra-Deep Water (Above 1 500 m) |

| Permanent |

| Temporary |

| Floating Production Storage and Offloading (FPSO) |

| Tension Leg Platforms (TLP) |

| Semi-submersibles |

| Spar Platforms |

| Floating Wind Turbines |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Mooring Type | Spread Mooring | |

| Single Point Mooring | ||

| Dynamic Positioning | ||

| Catenary | ||

| Taut Leg | ||

| Semi-taut | ||

| Others | ||

| By Component | Anchors | |

| Connectors | ||

| Chains | ||

| Synthetic Fiber Ropes | ||

| Buoys | ||

| Others | ||

| By Depth | Shallow Water (Up to 400 m) | |

| Deep Water (400 to 1 500 m) | ||

| Ultra-Deep Water (Above 1 500 m) | ||

| By Installation Type | Permanent | |

| Temporary | ||

| By Application | Floating Production Storage and Offloading (FPSO) | |

| Tension Leg Platforms (TLP) | ||

| Semi-submersibles | ||

| Spar Platforms | ||

| Floating Wind Turbines | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the offshore mooring system market in 2031?

The offshore mooring system market is forecast to reach USD 2.18 billion by 2031.

Which region is expected to grow the fastest through 2031?

The Middle East and Africa is projected to record the highest 4.7% CAGR due to gas developments in Qatar, Israel, and Mozambique.

Why are synthetic fiber ropes gaining traction in mooring spreads?

Polyester and HMPE ropes cut suspended weight by up to 70% and lower top tension by 40%, enabling lighter hardware and cheaper installation vessels.

How does floating wind influence anchor demand?

A gigawatt-scale floating wind farm can require five times more anchors than a single FPSO because each turbine needs three to four lines.

Which application segment is expanding the quickest?

Spar platforms are advancing at a 5.2% CAGR owing to superior stability in hurricane-prone basins such as the Gulf of Mexico.

What role do digital twins play in mooring operations?

Hybrid physics-AI twins predict fatigue with 92% accuracy, extending inspection intervals from five to seven years and lowering lifecycle cost by up to 20%.

Page last updated on: