Next-Generation Energy Storage Systems Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.48 Billion |

| Market Size (2031) | USD 3.9 Billion |

| Growth Rate (2026 - 2031) | 9.49% CAGR |

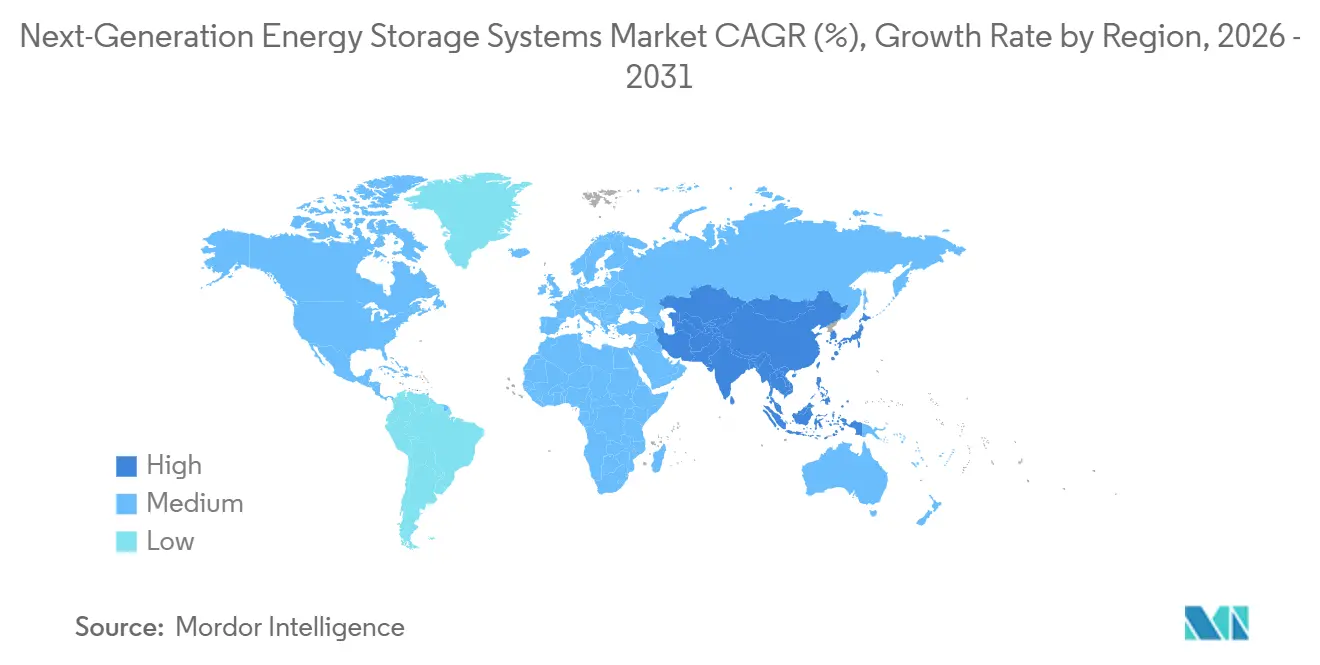

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Next-Generation Energy Storage Systems Market Analysis by Mordor Intelligence

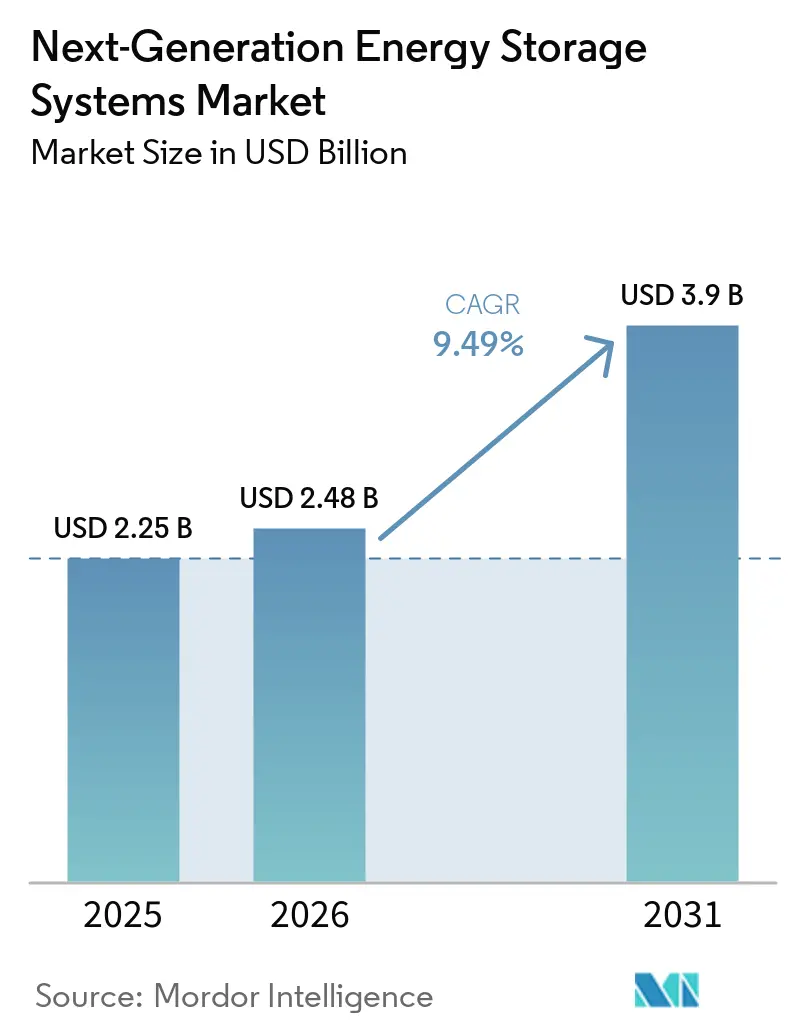

The next-generation energy storage systems market size is projected to expand from USD 2.25 billion in 2025 and USD 2.48 billion in 2026 to USD 3.9 billion by 2031, registering a CAGR of 9.49% between 2026 and 2031. Solid-state batteries already dominate commercial discussions because their 400-500 Wh/kg energy density unlocks 700-mile passenger-vehicle ranges and creates an entry point for electric aircraft certification. Grid operators continue to absorb four-hour lithium-ion systems, yet policy-driven mandates for longer-duration assets are redirecting capital toward iron-air and iron-flow chemistries that can discharge for 8-100 hours. Asia-Pacific anchors demand, supported by China’s impending national solid-state battery standard and South Korea’s USD 40 billion K-Battery program. Meanwhile, the Inflation Reduction Act’s USD 35 per kWh production tax credit has turned the United States into the world’s fastest-growing manufacturing hub for new chemistries, even as Europe tightens recycling rules that require 50% lithium recovery by 2027.

Key Report Takeaways

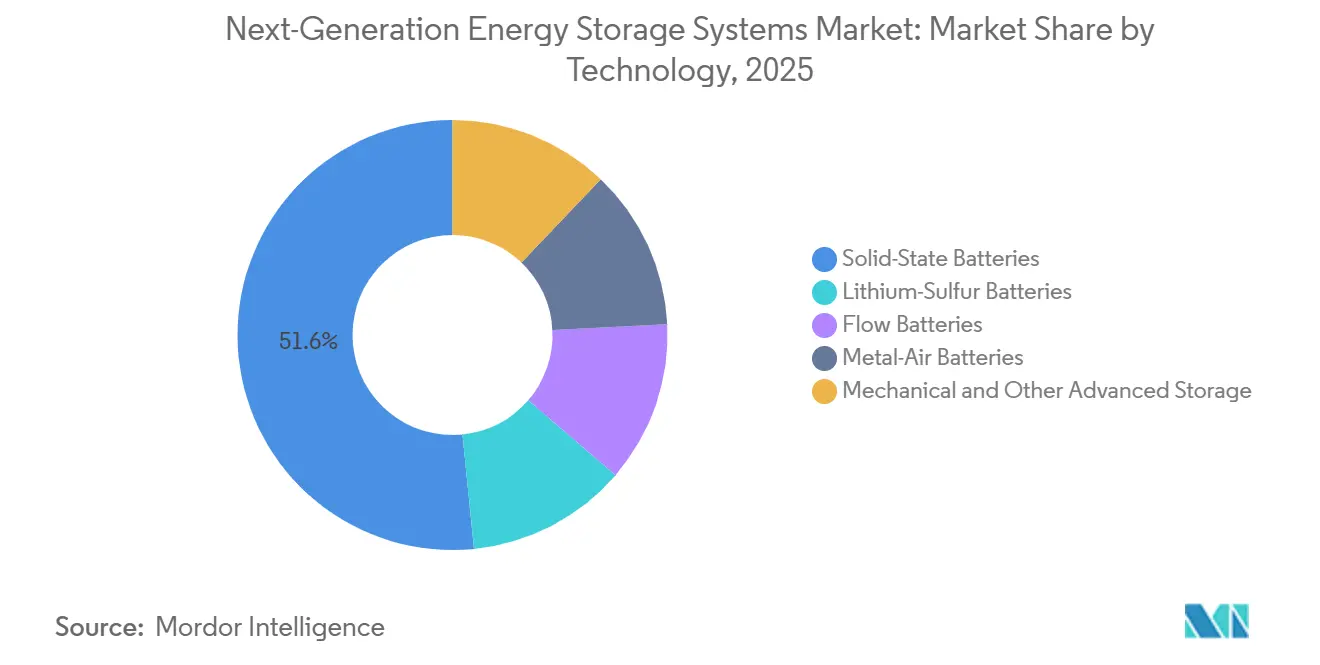

- By technology, solid-state batteries led with 51.6% of the next-generation energy storage systems market share in 2025 and are projected to expand at a 9.9% CAGR between 2026 and 2031

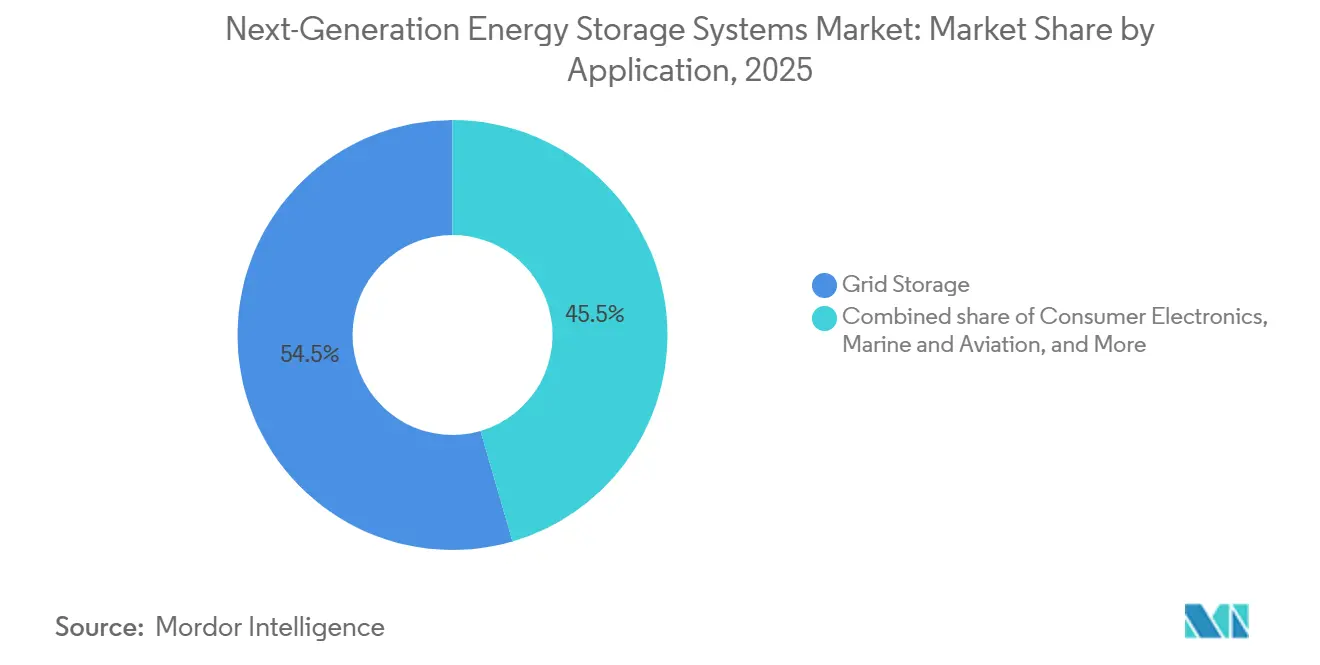

- By application, grid storage accounted for 54.5% share of the next-generation energy storage systems market size in 2025, and marine and aviation segments are projected to expand at a 17.8% CAGR between 2026 and 2031, the fastest pace among all use cases.

- By geography, Asia-Pacific held 45.1% revenue share in 2025 and is forecast to grow at a 10.1% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Next-Generation Energy Storage Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV production targets by global automakers | +2.1% | Asia-Pacific core, spill-over to North America & Europe | Medium term (2-4 years) |

| Renewable-integration mandates for grid operators | +1.8% | Global, with early concentration in North America & EU | Long term (≥ 4 years) |

| Rapid $/kWh cost decline in solid-state & flow chemistries | +2.4% | Global | Medium term (2-4 years) |

| Defense demand for high-energy batteries for unmanned systems | +0.7% | North America, selective APAC | Short term (≤ 2 years) |

| Circular-economy incentives for critical-material recovery | +1.2% | EU core, expanding to North America & China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging EV Production Targets by Global Automakers

Manufacturers are compressing development cycles for high-energy chemistries. BYD plans sulfide-based solid-state pilot output in 2027 and mass output by 2030 at roughly 400 Wh/kg, a 60% uplift on its Blade Battery platform.[1]Staff Reporter, “Solid-State Batteries Edge Toward Parity With Lithium-Ion,” Reuters, reuters.com CATL is piloting 500 Wh/kg condensed batteries that could debut in electric aircraft fleets starting in 2027.[2]Energy Desk, “Asia Drives New Battery Standard,” Bloomberg, bloomberg.com Toyota maintains a 2027-2028 launch window for a 745-mile solid-state pack promising 10-minute charging. Supportive public funding, such as the U.S. Department of Energy’s USD 16 million 2024 grant round, lowers pilot-line risk and aligns policy with automaker roadmaps.[3]Research Team, “DOE Awards for Solid-State Manufacturing,” U.S. Department of Energy, energy.gov Collectively, these moves advance the timeline by which solid-state cells must cross the USD 100 per kWh cost threshold to displace liquid-electrolyte lithium-ion technology.

Renewable-Integration Mandates for Grid Operators

Re-written wholesale-market rules now treat storage as capacity, not an ancillary service. FERC Orders 841 and 2222 require regional markets to let batteries bid into energy, capacity, and ancillary-service auctions. States such as New York, Massachusetts, and New Jersey together target 13 GW of deployments by 2030, reinforcing long-duration purchase agreements. Flow-battery suppliers have exploited the opening: ESS Tech secured a USD 9.9 million U.S. Air Force award for 27 MWh iron-flow units, while Form Energy broke ground on a 1,500 MWh iron-air plant that can discharge for 100 hours, capabilities beyond four-hour lithium-ion systems. With NREL projecting lithium-ion system costs at USD 243 per kWh by 2035, the cost gap narrows as duration lengthens.

Rapid USD/kWh Cost Decline in Solid-State & Flow Chemistries

BloombergNEF reported 2025 lithium-ion pack prices at USD 108 per kWh, while stationary systems slipped to USD 70 per kWh because energy density is less critical off-vehicle. Solid-state pilots still run at USD 150-200 per kWh, but QuantumScape’s anode-free architecture eliminates graphite, trimming materials cost by roughly 25%. Flow batteries achieve marginal costs below USD 50 per kWh for every extra hour beyond the base eight-hour tank, a scaling trait that pure-energy chemistries lack. China’s national standard, due in July 2026, will shorten certification cycles, a policy that historically cuts manufacturing costs within two years of adoption. The Department of Energy’s Long-Duration Earthshot sets a USD 0.05 per kWh system target that, once met, positions flow batteries to compete directly with pumped storage hydro.

Defense Demand for High-Energy Batteries for Unmanned Systems

The Pentagon’s performance envelope extends beyond civilian requirements. South 8 Technologies received USD 1.6 million to develop LiGas cells that operate from -60 °C to +60 °C, enabling Arctic and desert drone missions. NexTech Batteries won a USD 1.9 million Space Force contract for 400 Wh/kg lithium-sulfur prototypes destined for high-altitude platforms. GM Defense pilots solid-state packs in tactical microgrids where energy density outweighs long cycle life. ARPA-E’s 2024 JOULES program allocated USD 15 million in pursuit of 1,000 Wh/kg targets that, if met, would triple the endurance of current unmanned aerial systems. Military procurement thus provides early revenue that de-risks commercial rollout.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety & thermal-runaway risks in high-energy chemistries | -1.4% | Global | Short term (≤ 2 years) |

| Critical-metal supply-chain volatility | -1.1% | Global, acute in North America & EU | Medium term (2-4 years) |

| Manufacturing scale-up hurdles for solid electrolytes | -0.9% | Global | Medium term (2-4 years) |

| End-of-life stewardship uncertainty for novel chemistries | -0.5% | EU core, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety & Thermal-Runaway Risks in High-Energy Chemistries

High-profile recalls keep insurance premiums elevated. General Motors, Fisker, Mercedes-Benz, and Rivian collectively recalled more than 120,000 EVs in 2024 over battery-fire concerns.[4]Vehicle Recall Database, “Battery-Related Recalls 2024,” National Highway Traffic Safety Administration, nhtsa.gov UL 9540A and IEC 62619 standards provide test pathways, but solid-state cells lack large-sample operating histories, delaying underwriting approvals. NFPA 855 installation codes add USD 20-30 per kWh in protection costs that early-stage chemistries can ill afford. Dendrite growth in lithium-metal anodes remains an unresolved failure mode, although ceramic separators and electrolyte additives show promise in lab trials. Until field data accumulate, buyers will discount unproven chemistries.

Critical-Metal Supply-Chain Volatility

Lithium carbonate prices collapsed from USD 80,000 per ton in 2022 to USD 10,000-12,000 per ton in 2024-2025, curbing miner capex and sowing the seeds for shortages when solid-state scaling begins in 2028-2030. Cobalt trades far below its 2022 peak yet still relies on the Democratic Republic of Congo for 70% of supply, exposing buyers to geopolitical shocks. China's grip on 60% of lithium refining amplifies Western anxieties, prompting domestic-content rules in the United States and the European Union. Cell makers respond by shifting toward lithium-iron-phosphate and manganese-rich chemistries, but premium applications still require nickel-manganese-cobalt or lithium-metal variants. Without diversified mining investment, price spikes could stall adoption curves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solid-State Dominance Masks Niche Gains

Solid-state batteries represented 51.6% of the next-generation energy storage systems market share in 2025 and are forecast to post a 9.9% CAGR through 2031, highlighting their pull from premium automotive and emerging electric-aviation programs. The next-generation energy storage systems market size attached to solid-state chemistry is poised to expand rapidly once costs fall below USD 100 per kWh, a parity point most analysts peg for 2028. QuantumScape’s oxide electrolyte, which eliminates the graphite anode, trims material cost by a quarter and improves volumetric density, while Solid Power’s sulfide pathway delivers higher ionic conductivity but demands moisture-free handling. Toyota, Samsung SDI, and LG Energy Solution all target commercial releases between 2027 and 2029, ensuring a crowded field long before the technology reaches scale.

Flow, lithium-sulfur, and metal-air chemistries occupy specialist roles rather than direct competition. ESS Tech’s iron-flow platform commands the 8-24-hour stationary niche, and Form Energy’s 100-hour iron-air system is opening a seasonal-shift frontier. Lithium-sulfur, valued for its 400 Wh/kg density, draws aerospace interest; Airbus, for instance, collaborates with Sion Power on demonstration cells. Zinc-air suppliers such as Zinc8 position their low-cycle systems for rural micro-grids. Mechanical gravity storage from Energy Vault targets ultra-long durations in markets with cheap land. Collectively, these alternatives ensure the next-generation energy storage systems market remains technology-diverse even as solid-state leads volumes.

By Application: Marine & Aviation Outpace Grid Storage

Grid storage controlled 54.5% of 2025 revenue, the core of the next-generation energy storage systems market size, because utilities continue to buy four-hour lithium-ion assets that satisfy capacity and ramping needs. New York’s indexed storage credits, alongside ISO market access, sustain project pipelines that favor familiar chemistries. Yet, as renewable penetration deepens, the value of 8-100 hour duration rises, bringing iron-flow and iron-air contenders into procurement conversations.

Marine and aviation deliveries, while a smaller base, will compound at 17.8% CAGR to 2031, the steepest trajectory across all end uses. International Maritime Organization rules require a 70% greenhouse-gas cut by 2050, accelerating battery ferries and short-sea shipping retrofits, segments already served by Corvus Energy’s more than 1,000 marine installations. In electric aviation, Joby and Archer target Federal Aviation Administration certification windows in 2025-2026, demanding pack gravimetric densities over 400 Wh/kg. Solid-state and lithium-sulfur chemistries can meet those requirements, positioning the next-generation energy storage systems market to diversify revenue away from grid accounts.

Geography Analysis

Asia-Pacific, holding 45.1% of the 2025 turnover, underpins almost half the next-generation energy storage systems market size. The region should grow at 10.1% CAGR thanks to China’s July 2026 solid-state battery standard, South Korea’s USD 40 billion K-Battery initiative, and Japan’s continued 4680 roll-outs. CATL and BYD together forecast more than 1.2 TWh of capacity by 2030, and combined pilot lines for condensed and sulfide chemistries could enter series production by 2027. Seoul-based LG Energy Solution and Samsung SDI bridge Asian scale with Western partnerships, anchoring supply between Chinese dominance and U.S. policy incentives.

North America’s share expands on the back of the Inflation Reduction Act’s Section 45X, which rebates USD 35 per kWh for domestic cell output plus 30% investment tax credits for factories. LG Energy Solution’s USD 5.5 billion Arizona complex and Panasonic’s Kansas expansion together exceed 57 GWh of announced capacity slated for 2026, while Ford/SK and Tesla add further gigawatt-hour volumes. Federal energy-market rules, Orders 841, 2222, and 901, harmonize battery participation, and state targets create a 13 GW demand floor through 2030, ensuring visibility for developers beyond automotive offtake.

Europe operates within a tightening regulatory frame that rewards recyclers and penalizes high-carbon supply chains. The Battery Regulation’s carbon-footprint labeling and material-recovery thresholds raise compliance costs that favor vertically integrated producers. Northvolt’s 2024 restructuring highlighted financing hurdles, but its Ett plant still aims for 60 GWh of annual capacity. Automotive Cells Company advances three gigafactories totaling 120 GWh by 2030, while the U.K.’s Faraday Institution funds solid-state and sodium-ion R&D. Elsewhere, lithium-rich South America eyes mid-decade refining, and Middle East developers weigh long-duration storage for desert renewables, but volumes remain embryonic through 2026.

Competitive Landscape

The global next-generation energy storage systems market is moderately consolidated. Incumbent lithium-ion providers, CATL, LG Energy Solution, Samsung SDI, Panasonic Energy and BYD, retain scale advantages yet face rising competition from pure-play innovators. QuantumScape and Solid Power advance oxide and sulfide electrolytes, Form Energy pursues iron-air duration strategies and ESS Tech packages iron-flow chemistry for microgrids. Competitive vectors now align around three themes: automaker joint development, government pilot funding and closed-loop recycling. CATL’s 500 Wh/kg aviation pack and BYD’s sulfide road map signal incumbents’ readiness to leapfrog startups.

Automotive offtake contracts mitigate scale-up risk. BMW and Ford back Solid Power; Volkswagen supports QuantumScape; Stellantis and Mercedes bankroll ACC in Europe. Government contracts provide bridging revenue: the U.S. Air Force funds ESS Tech installations, while the Space Force bankrolls lithium-sulfur research at NexTech. Recycling joint ventures, such as Northvolt’s Revolt Ett and Redwood Materials’ tie-ups with automakers, lock in feedstock before virgin-metal prices rebound.

Technology differentiation remains pronounced. Mobility success hinges on gravimetric density, while stationary economics favor duration and cycle life. Start-ups like 24M license semi-solid electrodes that halve capex, whereas gravity-based Energy Vault targets ultra-long durations for desert solar storage. The policy environment, Section 45X in the United States and Battery Regulation 2023/1542 in Europe, tilts in favor of domestic producers willing to shoulder early capital intensity. Execution risk, however, remains: Northvolt’s restructuring shows that even well-funded players can stumble when scaling novel chemistries.

Next-Generation Energy Storage Systems Industry Leaders

CATL

LG Energy Solution

Tesla (Energy Storage)

QuantumScape

Panasonic Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: QuantumScape Corporation inaugurated its newly installed Eagle Line at its San Jose facility. The Eagle Line, a blend of equipment, materials, and advanced automation, serves as the foundation for producing QS technology. Central to its operation is QS's innovative Cobra process, a distinctive and scalable technique for crafting the proprietary QS separator.

- April 2025: Ørsted began constructing a 250 MW/500 MWh storage facility in Texas supplied by Tesla technology.

- March 2025: LG Energy Solution clinched a grid-scale ESS supply contract with Poland’s PGE, marking further European expansion.

- February 2025: GE Vernova and Our Next Energy signed a term sheet to produce domestic LFP modules in the United States.

Global Next-Generation Energy Storage Systems Market Report Scope

Next-Generation Energy Storage Systems (ESS) are cutting-edge technologies that store electricity, heat, or mechanical energy for future use. They prioritize higher efficiency, extended duration, enhanced safety, and reduced environmental impact compared to traditional lithium-ion batteries. Technologies such as solid-state batteries, flow batteries, and green hydrogen are pivotal in stabilizing grid fluctuations from renewable sources and promoting industrial decarbonization.

The next-generation energy storage systems market is segmented by technology, application, and geography. By technology, the market is segmented into lithium-sulfur batteries, solid-state batteries, flow batteries, metal-air batteries, and mechanical and other advanced storage. By application, the market is segmented into grid storage, consumer electronics, industrial and commercial mobility, marine and aviation, and others. The report also covers the market size and forecasts for the next-generation energy storage systems market in 20 countries across major regions. Market forecasts are provided in terms of value (USD).

| Lithium-Sulfur Batteries |

| Solid-State Batteries |

| Flow Batteries |

| Metal-Air Batteries |

| Mechanical and Other Advanced Storage |

| Grid Storage |

| Consumer Electronics |

| Industrial and Commercial Mobility |

| Marine and Aviation |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Technology | Lithium-Sulfur Batteries | |

| Solid-State Batteries | ||

| Flow Batteries | ||

| Metal-Air Batteries | ||

| Mechanical and Other Advanced Storage | ||

| By Application | Grid Storage | |

| Consumer Electronics | ||

| Industrial and Commercial Mobility | ||

| Marine and Aviation | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the global next-generation energy storage systems market ?

The next-generation energy storage systems market size is projected to expand from USD 2.25 billion in 2025 and USD 2.48 billion in 2026 to USD 3.9 billion by 2031, registering a CAGR of 9.49% between 2026 to 2031.

How fast will marine and aviation demand grow?

The combined segment is projected to expand at 17.8% CAGR between 2026 and 2031, outpacing grid, mobility and consumer electronics uptake.

Which region will contribute the most new capacity?

Asia-Pacific remains the volume leader, growing from 45.1% share in 2025 at a 10.1% CAGR on the back of Chinese and Korean investment commitments.

What U.S. policies most benefit domestic manufacturers?

Section 45X of the Inflation Reduction Act offers up to USD 35 per kWh for cells produced domestically, while Section 48C adds a 30% investment tax credit for factory build-outs.

Why is recycling critical to supply security?

EU regulations mandate up to 80% lithium recovery by 2031 and, alongside California's stewardship rules, create a guaranteed market for recycled feedstock insulated from spot-price swings.

Which chemistry targets 100-hour storage durations?

Iron-air batteries, exemplified by Form Energy's 1,500 MWh project, can discharge for roughly four days, addressing long-duration grid-balancing applications.

Page last updated on: