Advanced Energy Storage Systems Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

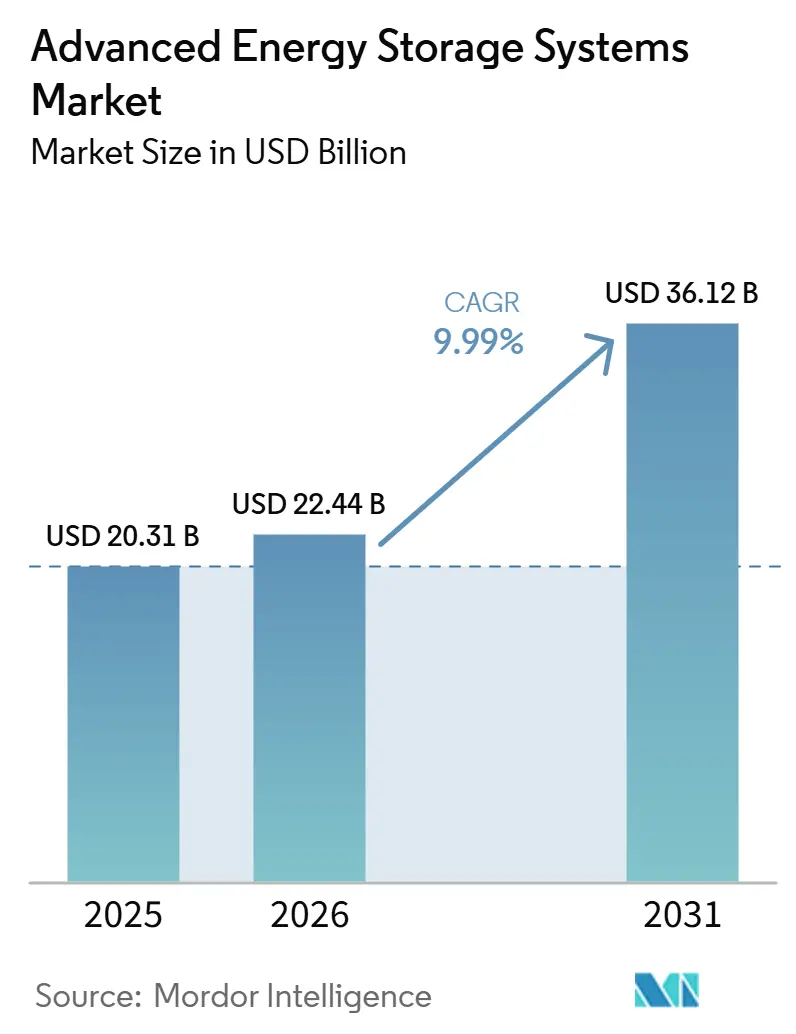

| Market Size (2026) | USD 22.44 Billion |

| Market Size (2031) | USD 36.12 Billion |

| Growth Rate (2026 - 2031) | 9.99% CAGR |

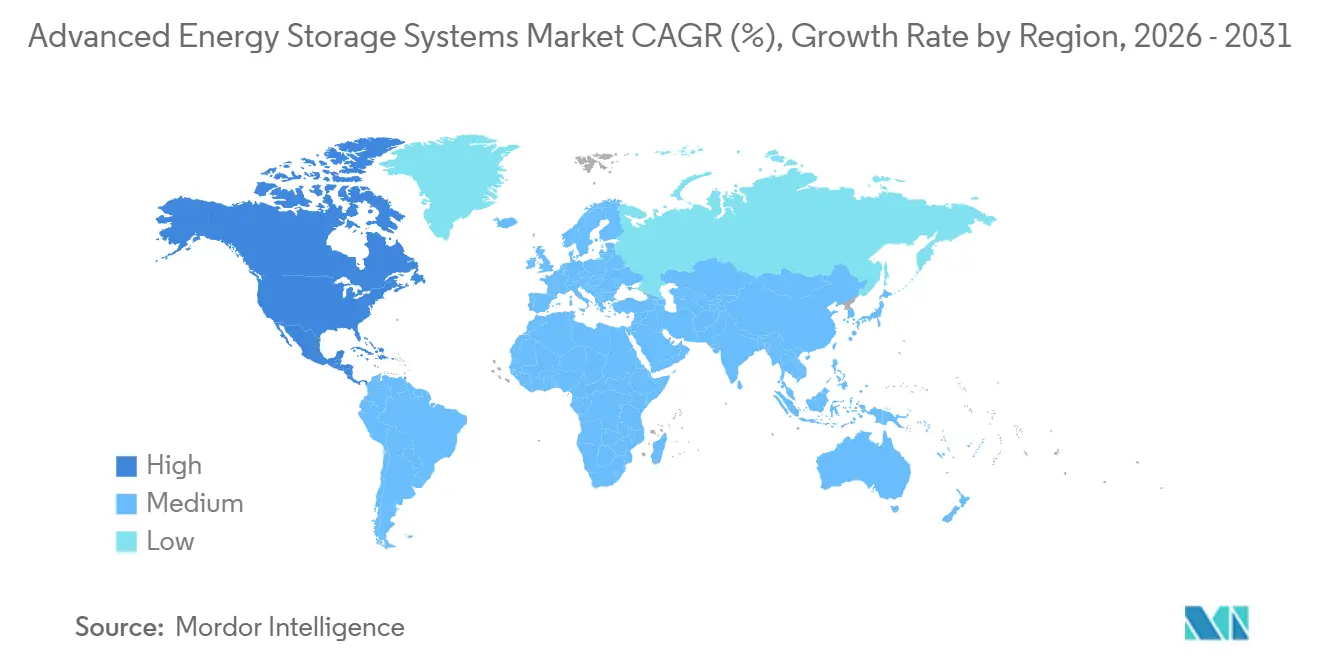

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

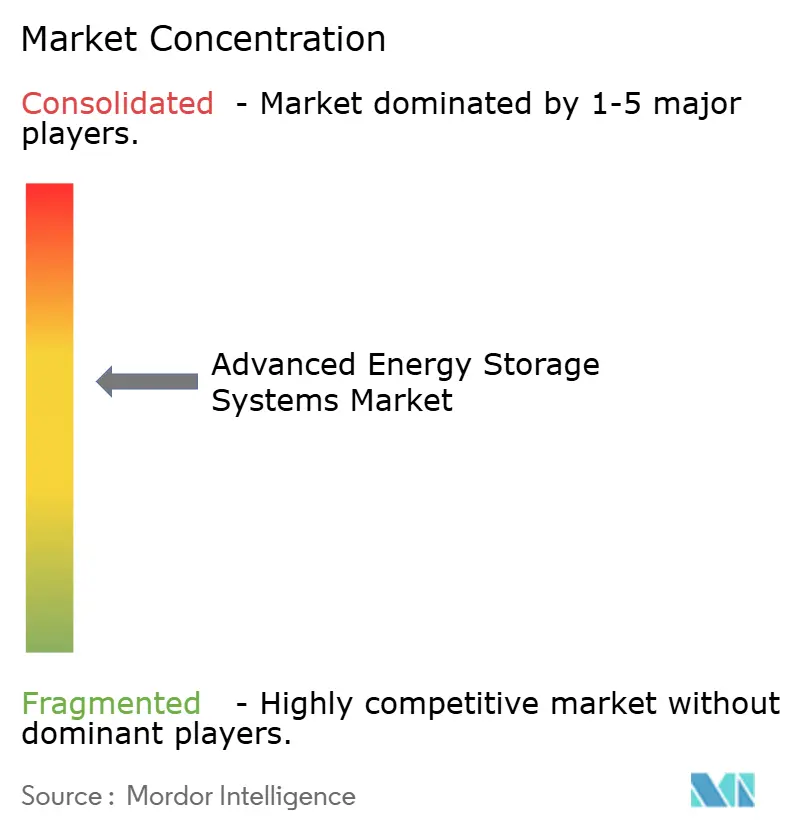

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Energy Storage Systems Market Analysis by Mordor Intelligence

The Advanced Energy Storage Systems Market size is expected to increase from USD 20.31 billion in 2025 to USD 22.44 billion in 2026 and reach USD 36.12 billion by 2031, growing at a CAGR of 9.99% over 2026-2031. Business models that combine grid-scale batteries with software-driven revenue stacking are driving most of this growth, while EV-gigafactory scale keeps lowering stationary pack costs and shortening payback periods.[1]“Battery Pack Prices Fall to USD 108/kWh,” Bloomberg, bloomberg.com Safety regulations such as NFPA 855 are tightening, yet compliance spending is catalyzing design innovation rather than dampening demand.[2]“NFPA 855 2026 Edition,” Financial Times, ft.com Utilities are still the largest buyers, but behind-the-meter deployments are rising as virtual power plant platforms aggregate residential and commercial batteries into tradable grid assets.[3]“Second-Life EV Batteries Install at USD 220-320/kWh,” Wall Street Journal, wsj.com Regionally, Asia-Pacific commands the largest share today, though North America is expanding fastest because the Inflation Reduction Act tax credits are linking domestic content rules with long-term offtake contracts.[4]“CATL Expands Ningde Complex,” Reuters, reuters.com

Key Report Takeaways

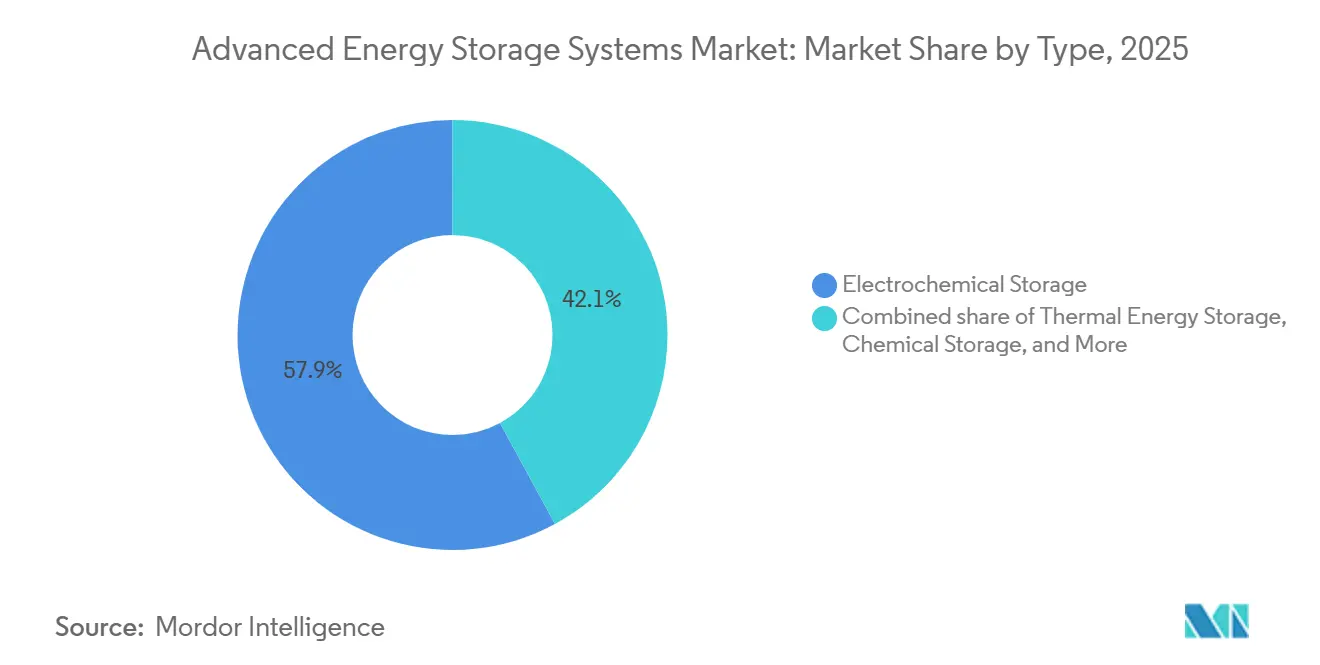

- By type, electrochemical storage led with 57.9% of the advanced energy storage systems market share in 2025, while chemical storage is expected to advance at a 13.3% CAGR through 2031.

- By application, grid storage commanded 40.4% share of the advanced energy storage systems market size in 2025, and EV infrastructure is projected to expand at an 18.6% CAGR to 2031.

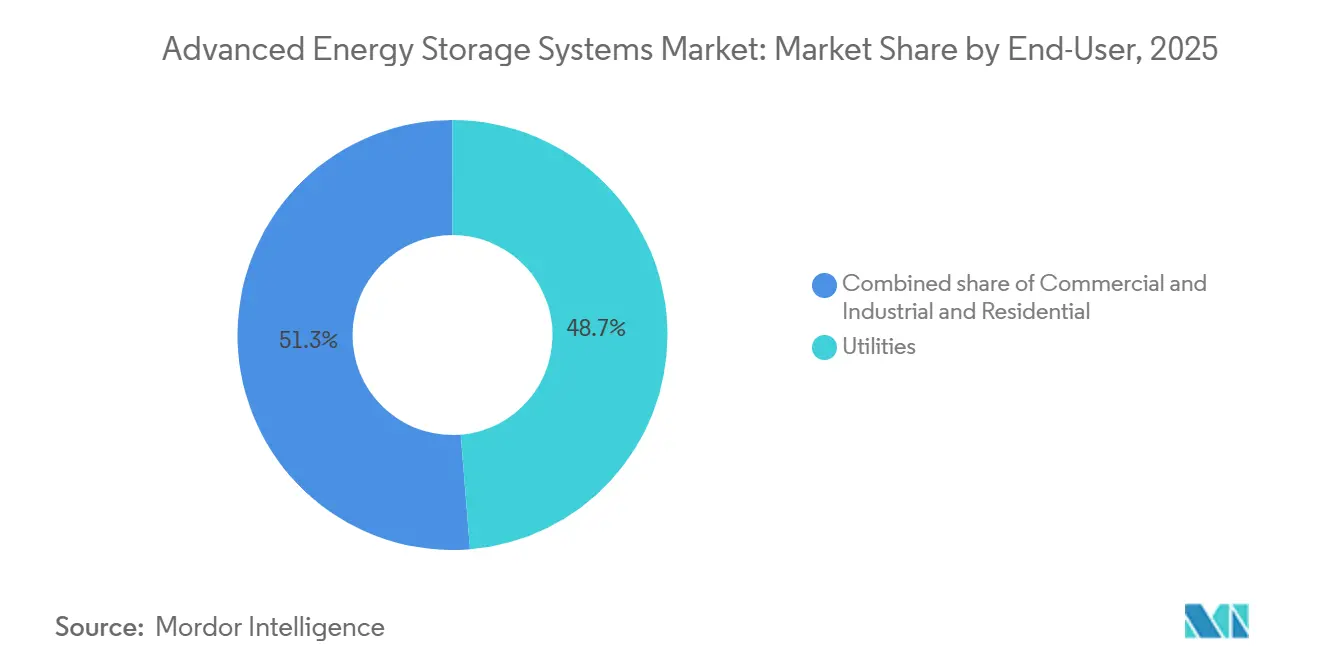

- By end-user, utilities held 48.7% share of the advanced energy storage systems market size in 2025, whereas residential deployments are expected to grow at a 17.9% CAGR through 2031.

- By geography, Asia-Pacific captured 46.2% revenue in 2025, and North America is projected to grow at 14.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Advanced Energy Storage Systems Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decline in lithium-ion battery cost | +2.80% | Global, cost leadership in China and South Korea | Short term (≤ 2 years) |

| Global clean-energy mandates | +2.40% | North America, EU, China, India | Medium term (2-4 years) |

| Revenue stacking in ancillary markets | +1.60% | North America, UK, Australia | Medium term (2-4 years) |

| EV-scale manufacturing efficiencies | +1.90% | Global, led by China | Short term (≤ 2 years) |

| Second-life EV packs | +1.10% | North America, Europe, Japan | Medium term (2-4 years) |

| AI-driven dispatch | +1.30% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in Lithium-Ion Battery USD /kWh

Average lithium-ion pack prices fell to USD 108 per kWh in 2025 and are projected at USD 105 per kWh in 2026, while large utility procurements already secure sub-USD 70 per kWh pricing at the pack level. Cathode shifts toward lithium iron phosphate have removed cobalt exposure and improved cycle life, letting 4-hour projects clear merchant arbitrage markets without subsidies. Scale advantages at CATL’s Ningde base produced 69 GWh in 2024, setting a volume benchmark competitors must match. The cost curve is flattening, and future savings hinge on solid-state or sodium-ion breakthroughs that are in the pilot stage. Cell maker, therefore, integrates downstream to secure margin, pressuring pure-play integrators to focus on software value.

Global Clean-Energy Mandates & Storage Procurement Targets

Extension of the U.S. investment tax credit through 2032 combines with state targets such as California’s 16.9 GW requirement and New Jersey’s 2 GW goal, generating a visible pipeline that derisks finance. Europe’s REPowerEU includes Germany’s 17.5 GW and the UK’s 50 GW ambitions, while China demands storage equal to up to 20% of renewable nameplate capacity. These mandates embed batteries into every new solar and wind business case and push developers to preorder systems 18-24 months ahead, tightening supply chains. IEC 62933 performance standards and ISO 22600 safety protocols are becoming universal bid prerequisites, formalizing quality thresholds.

Revenue Stacking in Ancillary-Service Markets

PJM, ERCOT, and the UK now let batteries concurrently trade energy, frequency, and capacity, boosting internal rates of return by 10-15 percentage points compared with single-use assets. AI tools from Fluence and Tesla predict price spikes hours, swinging assets between services within 15-minute settlements, and raising forecast accuracy to 98%. This turns storage into a dynamic trading book that simultaneously meets grid reliability targets and investor yield hurdles. Liberalized markets gain most because vertically integrated utilities lack transparent price signals.

EV-Scale Manufacturing Lowering Stationary Costs

Global automotive cell output passed 1,200 GWh in 2025. Plants such as BYD’s 130 GWh and LG’s 16 GWh Arizona lines allocate up to 15% of production to stationary orders, bringing automotive cost curves to the grid segment. Shared supply chains, dry electrode processing, and cell-to-pack integration migrate into stationary cabinets within 12-18 months, shortening innovation cycles. A risk emerges if EV sales taper, potentially stranding capacity and slowing price declines.

Restraints Impact Analysis of Advanced Energy Storage Systems Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-mineral price volatility | -1.80% | Global, acute in EU and North America | Short term (≤ 2 years) |

| Thermal-runaway and fire-safety costs | -1.20% | Global, strictest in North America and EU | Medium term (2-4 years) |

| US-EU trade barriers and local content | -0.90% | North America, EU | Medium term (2-4 years) |

| Competition from long-duration non-battery | -0.70% | North America, China, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Price & Supply Volatility

Cobalt jumped 240% in 2025 after export quotas in the Democratic Republic of Congo cut shipments, while lithium carbonate swung between USD 12 000 and USD 28 000 per metric ton on Chinese demand uncertainty. Nickel saw the opposite trend as Indonesian output depressed prices, threatening future supply if high-cost mines stay idle. Battery makers respond with lithium iron phosphate adoption, which removes cobalt and nickel risk but introduces phosphate dependencies. Multi-year offtake contracts and upstream joint ventures are now standard, favoring vertically integrated giants that can prepay mines for security of supply.

Thermal-Run-Away & Fire-Safety Compliance Costs

NFPA 855 (2026) requires hazard-mitigation analysis, adding USD 15-25 per kWh in balance-of-plant cost. UL 9540A 6th Edition further tightens propagation tests, forcing wider module spacing and upgraded cooling designs. Insurance premiums rise 20-30% for uncertified systems, making third-party validation compulsory. Smaller sub-10 MWh projects find it harder to amortize these compliance costs, nudging developers toward utility-scale builds or certified turnkey products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Advanced Energy Storage Systems Market Segment Analysis

By Type:

Electrochemical Dominance, Chemical UpswingElectrochemical systems held 57.9% of the advanced energy storage systems market share in 2025, supported by lithium iron phosphate cells priced near USD 105 per kWh and life cycles beyond 8 000 cycles. The advanced energy storage systems market size attached to electrochemical chemistries, therefore, scales fastest where a four-hour duration can clear merchant spreads. Flow batteries and sodium-sulfur solutions address 6-10-hour windows, yet high temperature or vanadium costs confine uptake to niches. Over the forecast, incremental cost declines and standardized containers will let electrochemical portfolios expand into critical-peak applications, although long-duration roles increasingly migrate to chemical or mechanical formats.

Chemical pathways grow at a 13.3% CAGR as green hydrogen and synthetic fuels become grid-stability backstops rather than marginal peak shavers. Mitsubishi Power’s 317 MW Utah project blends cavern storage with 220 MW of electrolyzers, proving that multiday discharge can reach IRRs competitive with peaking gas. Thermal and mechanical variants, from molten-salt tanks to compressed-air caverns, remain constrained by site geology and permitting but fetch lower USD-per-kWh numbers for eight-hour-plus applications, ensuring a diversified mix within the advanced energy storage systems market.

By Application:

Grid Mainstay, EV Infrastructure SurgeGrid storage commanded 40.4% revenue in 2025 as utilities use batteries to absorb renewable spikes and defer transmission upgrades. Although IRRs are slim in oversupplied hubs like ERCOT, mandatory co-location rules under FERC Order 2023 keep batteries embedded in every new renewable asset, anchoring the advanced energy storage systems market size to utility procurement. Capacity bids often include four-hour batteries as standard, aligning with capacity payment structures and lowering curtailment.

EV infrastructure is the fastest riser, expanding at an 18.6% CAGR to 2031 as charge-point operators add on-site batteries for demand-charge control while simultaneously trading frequency services. The dual revenue pathway creates superior returns that conventional utility-scale systems cannot replicate. Industrial energy management, backup power, and off-grid microgrids also expand as diesel parity tips below USD 300 per kW installed.

By End-user:

Utilities Anchor, Residential AscendsUtilities retained 48.7% of the advanced energy storage systems market share in 2025, using 100 MW batteries to postpone USD 200 million substation expansions and save up to USD 80 million net present value. Yet four-year interconnection queues and land scarcity are shifting attention to behind-the-meter opportunities, proving that grid deferral alone cannot sustain volume growth.

Residential deployments rise at a 17.9% CAGR as virtual power plants aggregate thousands of Powerwall and Enphase units into multi-gigawatt fleets that bid into wholesale markets. Hardware prices from USD 8 000 per home and incentive programs such as California’s SGIP offset up-front cost, turning suburban houses into dispatchable grid capacity. Commercial and industrial users fill the middle ground through storage-as-a-service contracts that outsource capex while capturing tariff arbitrage.

Geography Analysis

APAC Advanced Energy Storage Systems Market

Asia-Pacific captured 46.2% revenue in 2025, underpinned by China’s vertically integrated value chain, where CATL, BYD, and EVE Energy collectively surpassed 300 GWh of annual output. Provincial mandates that every renewable plant include 15-20% storage create recurring demand, and mega projects such as Shandong’s 3.5 GW installation demonstrate execution at scale. Japan pursues sodium-sulfur for long-duration resilience, and India’s PLI scheme funds gigafactories that will feed Southeast Asian pipelines, ensuring the advanced energy storage systems market remains anchored in the region.

North America Advanced Energy Storage Systems Market

North America grows at 14.5% CAGR on the back of Inflation Reduction Act tax credits and domestic content bonuses that tilt procurement toward local manufacturing, including Tesla’s 40 GWh Megapack line and LG’s Arizona expansion. ERCOT overtook California in yearly additions during 2025 as performance-based ancillary prices reward sub-second response assets. Canada and Mexico follow with policy-backed auctions targeting renewable firming.

EMEA and South America Advanced Energy Storage Systems Market

Europe’s 50 GW UK goal, 17.5 GW German target, and made-in-EU procurement thresholds force developers to balance supply security with 15-20% higher capex linked to local assembly. Nordic pumped hydro provides seasonal balancing, while Eastern Europe eyes lithium storage to stabilize growing solar pipelines. South America readies its first large tenders in Brazil and Argentina, banking on hybrid solar-storage to curb curtailment. The Middle East and Africa accelerate as Saudi Arabia grid-connected 7.8 GWh of batteries in January 2026, setting a regional record

Competitive Landscape

The market is moderately concentrated. CATL, BYD, Tesla, LG Energy Solution, and Samsung SDI anchor cell supply, while Fluence, Sungrow, and Hitachi Energy bundle hardware with software and long-term services. AI dispatch has become the differentiator that lets integrators command premium pricing even when module costs commoditize. Government incentives are pulling Asian players to build local lines, as seen with LG's Arizona and Sungrow's Poland plants, tightening the link between policy compliance and market access. Disruptors such as Form Energy and ESS Inc. target iron-air and iron flow chemistries that promise 100-hour duration, while Energy Vault deploys gravity storage for locations where land is cheaper than lithium.

Energy storage strategies are transitioning from hardware commoditization to software differentiation. Fluence Energy's 10.8 GW backlog relies on service contracts, while Tesla's vertical integration captures value chain margins. Emerging disruptors like ESS Inc. and Invinity Energy Systems innovate with flow batteries. Patent filings by CATL and LG Energy Solution focus on solid-state electrolytes. Policies in North America and Europe drive local production investments by Asian manufacturers to maintain market access.

Advanced Energy Storage Systems Industry Leaders

Tesla Energy

Sungrow

CATL

Fluence

BYD

- *Disclaimer: Major Players sorted in no particular order

Advanced Energy Storage Systems Market Companies Covered in this Report

- Tesla, Inc.

- Siemens AG

- LG Energy Solution

- Fluence Energy, Inc.

- Samsung SDI Co., Ltd.

- General Electric Company

- BYD Company Ltd.

- Hitachi Energy

- Panasonic Holdings Corporation

- Saft Groupe S.A.

- VARTA AG

- Mitsubishi Power

- NGK Insulators, Ltd.

- ESS Inc.

- EnerSys

- Hydrostor Inc.

- Ambri Inc.

- Invinity Energy Systems

- Energy Vault Holdings, Inc.

- Stryten Energy

- Contemporary Amperex Technology Co. Ltd. (CATL)

- Sungrow Power Supply Co., Ltd.

- EVE Energy Co., Ltd.

- HyperStrong Technology

- CRRC Zhuzhou Institute

Recent Industry Developments in Advanced Energy Storage Systems Market

- March 2026: Tesla and LG Energy Solution formed a USD 4.3 billion joint venture for a 50 GWh lithium iron phosphate plant in Michigan, leveraging Inflation Reduction Act credits.

- March 2026: Huawei Digital Power and Aggreko won a USD 180 million contract to build a 110 MWp solar plus 120 MWh storage project in Minas Gerais, Brazil.

- March 2026: Argentina opened a 700 MW, USD 700 million storage tender to ease Patagonia wind curtailment.

- February 2026: Sungrow committed EUR 230 million for a 12.5 GWh battery factory and 20 GW inverter line in Poland.

Global Advanced Energy Storage Systems Market Report Scope

An Advanced Energy Storage System (AESS) encompasses modern technologies that store energy generated at one time for later use, offering improved efficiency, faster response times, and greater capacity compared to traditional storage methods.

The Advanced Energy Storage Systems Market is segmented into type, application, end-user, and geography. By type, the market is segmented into electrochemical, thermal, mechanical, chemical, and hybrid energy storage systems. By application, the market is segmented into grid storage, renewable integration, backup power, EV infrastructure, industrial, off-grid, and residential applications. By end-user, the market is segmented into utilities, commercial and industrial, and residential sectors. The report also covers the market size and forecasts for the advanced energy storage systems market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

Segmentation Overview

| Electrochemical Storage | Lithium-ion Batteries |

| Sodium-Sulfur Batteries | |

| Flow Batteries | |

| Lead-acid Batteries | |

| Nickel-based Batteries | |

| Thermal Energy Storage | Sensible Heat |

| Latent Heat | |

| Thermochemical | |

| Mechanical Storage | Pumped Hydro Storage |

| Compressed-Air (CAES) | |

| Flywheel Storage | |

| Chemical Storage | Hydrogen |

| Synthetic Natural Gas | |

| Ammonia | |

| Hybrid Storage Systems |

| Grid Storage |

| Renewable Integration |

| Backup Power Systems |

| Electric-Vehicle Infrastructure |

| Industrial Energy Management |

| Off-grid and Remote Area Storage |

| Residential Storage |

| Utilities |

| Commercial and Industrial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Electrochemical Storage | Lithium-ion Batteries |

| Sodium-Sulfur Batteries | ||

| Flow Batteries | ||

| Lead-acid Batteries | ||

| Nickel-based Batteries | ||

| Thermal Energy Storage | Sensible Heat | |

| Latent Heat | ||

| Thermochemical | ||

| Mechanical Storage | Pumped Hydro Storage | |

| Compressed-Air (CAES) | ||

| Flywheel Storage | ||

| Chemical Storage | Hydrogen | |

| Synthetic Natural Gas | ||

| Ammonia | ||

| Hybrid Storage Systems | ||

| By Application | Grid Storage | |

| Renewable Integration | ||

| Backup Power Systems | ||

| Electric-Vehicle Infrastructure | ||

| Industrial Energy Management | ||

| Off-grid and Remote Area Storage | ||

| Residential Storage | ||

| By End-user | Utilities | |

| Commercial and Industrial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the advanced energy storage systems market expected to grow through 2031

Revenue is projected to rise from USD 22.44 billion in 2026 to USD 36.12 billion by 2031, reflecting a 9.99% CAGR over the 2026-2031 period

Which storage technology holds the largest share today

Electrochemical batteries, primarily lithium iron phosphate, controlled 57.9% share in 2025

What region is adding capacity the quickest

North America leads growth at a 14.5% CAGR thanks to Inflation Reduction Act incentives and ERCOT ancillary market revenues

Why are second-life EV batteries gaining traction

Repurposed packs install at roughly half the cost of new cells and shorten payback to 3-5 years for commercial buyers

What is the main regulatory hurdle for utility-scale batteries

Updated NFPA 855 and UL 9540A fire-safety standards add USD 15-25 per kWh in compliance cost and require large-scale thermal-runaway testing

Which companies dominate software-driven dispatch optimization

Fluence Energy with its Mosaic platform and Tesla with Autobidder lead in AI-based revenue stacking solutions

Page last updated on: