Vat Photopolymerization 3D Printing Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

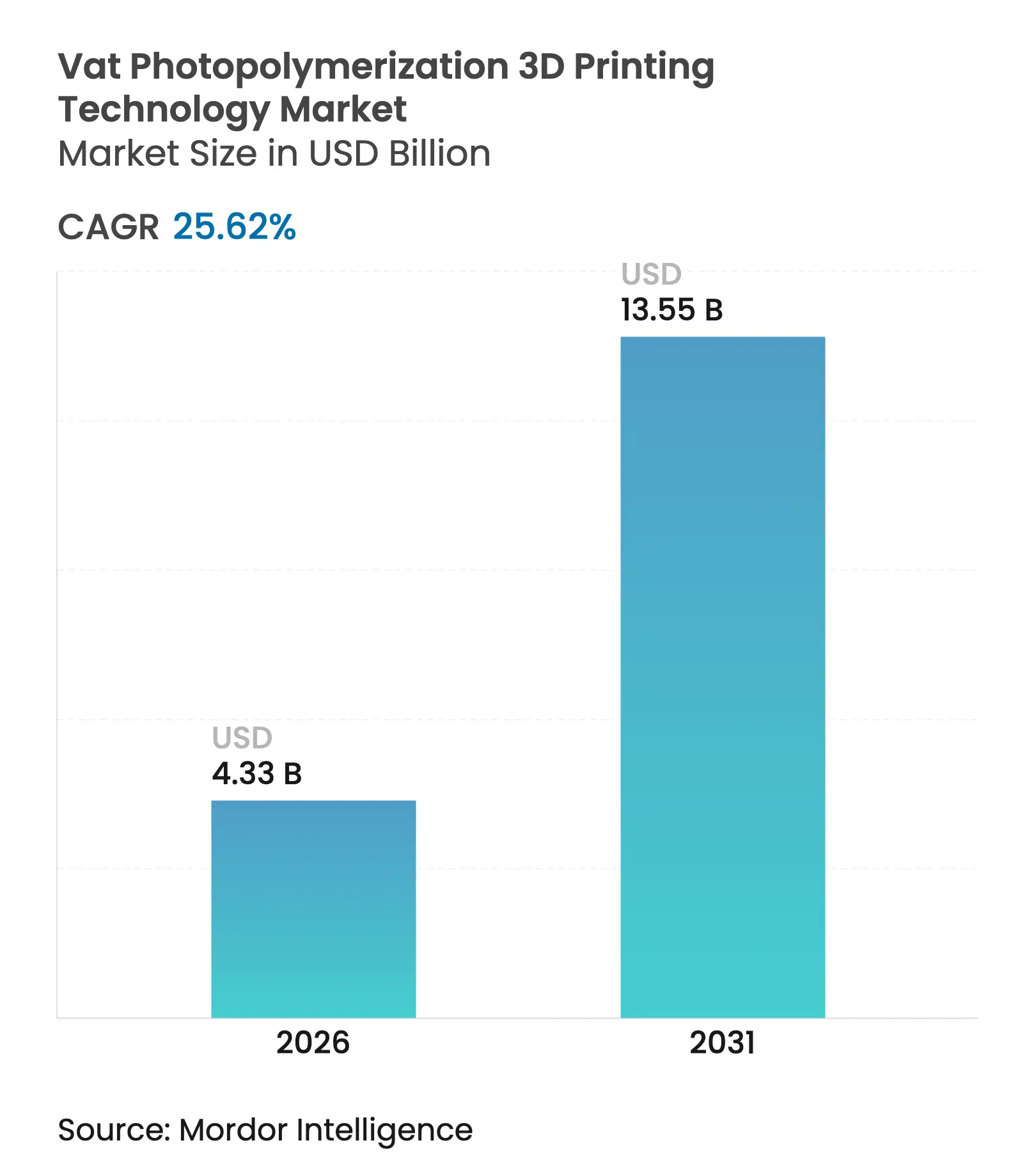

| Market Size (2026) | USD 4.33 Billion |

| Market Size (2031) | USD 13.55 Billion |

| Growth Rate (2026 - 2031) | 25.62 % CAGR |

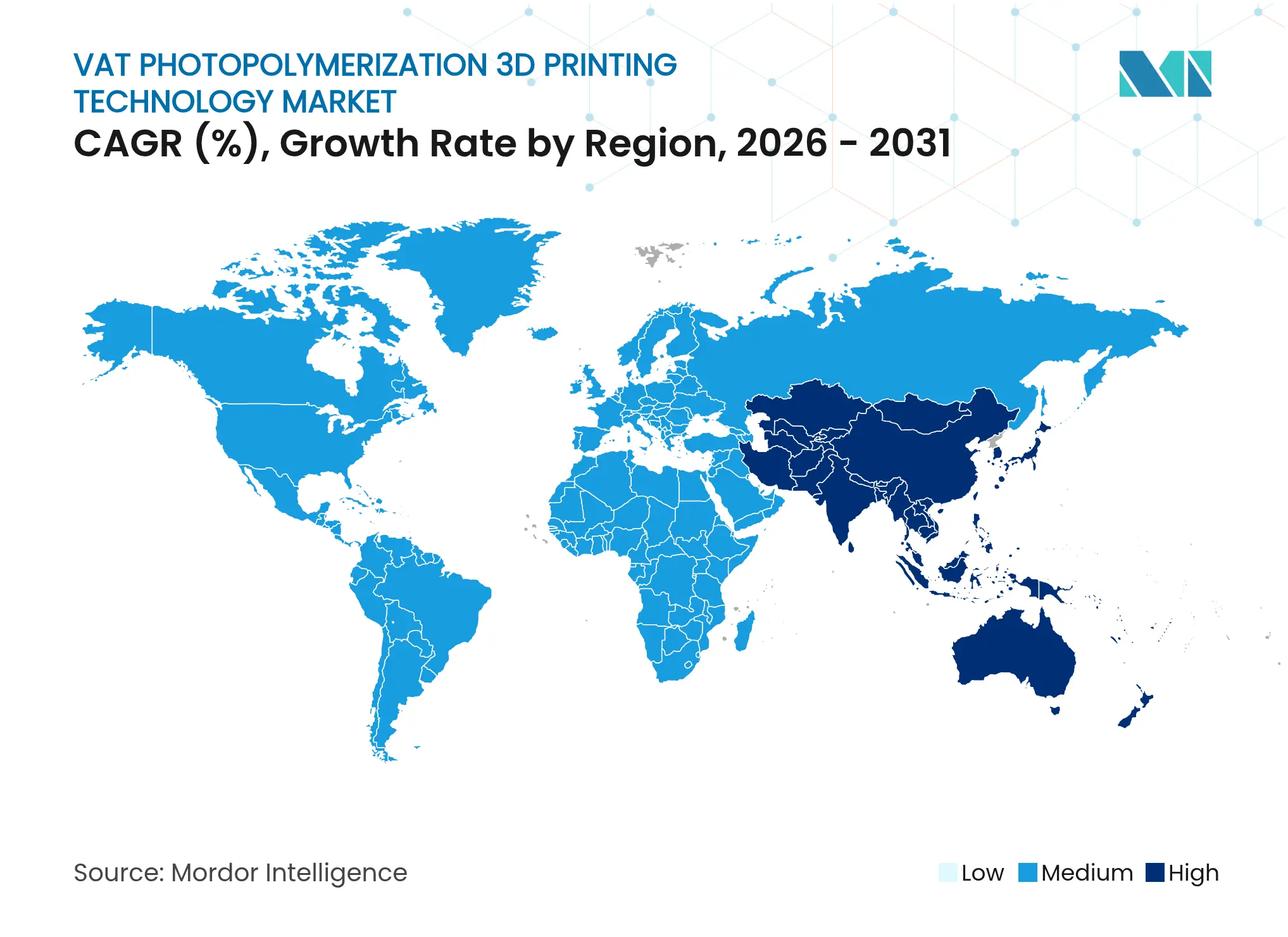

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

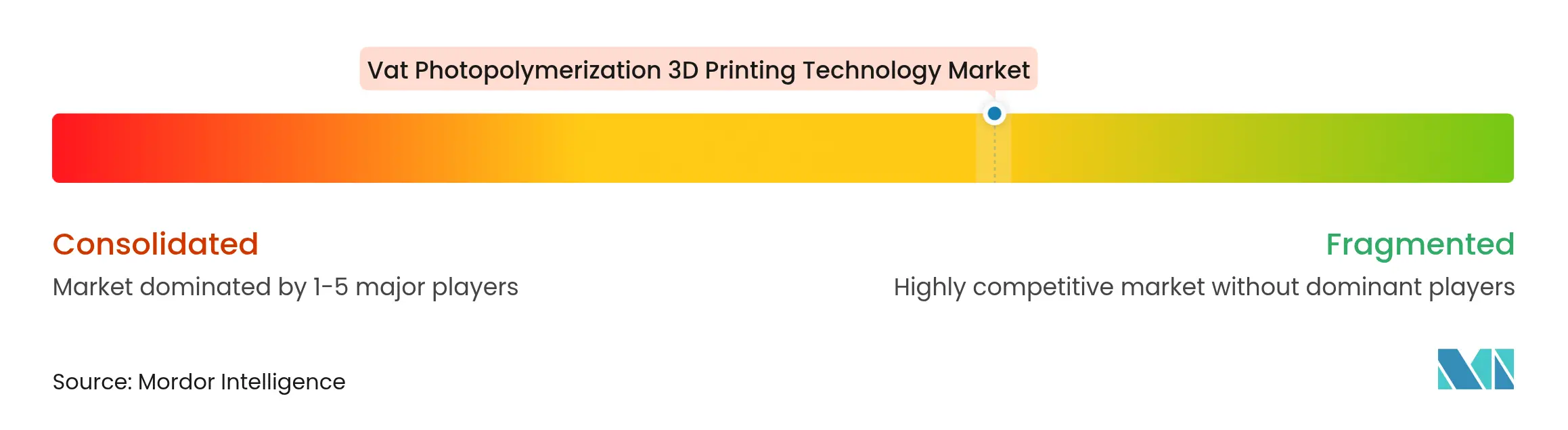

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Vat Photopolymerization 3D Printing Technology Market Analysis by Mordor Intelligence

The global vat photopolymerization 3D printing technology market size in 2026 is estimated at USD 4.33 billion, growing from 2025 value of USD 3.45 billion with 2031 projections showing USD 13.55 billion, growing at 25.62% CAGR over 2026-2031. Continuous digital light processing (CDLP), biocompatible resin breakthroughs, and the advent of sub-25 µm desktop printers are accelerating the transition from prototyping to production‐scale workflows. Growing demand for chair-side dentistry, faster LCD printer adoption, and expanding OEM–resin partnerships are redefining revenue models around high-margin consumables. North America currently leads adoption, yet public manufacturing initiatives and cost-effective hardware production position Asia-Pacific as the fastest-growing region. Competitive intensity is rising, with specialized entrants targeting application-specific niches and forcing established vendors to strengthen material–hardware integration strategies.

Key Report Takeaways

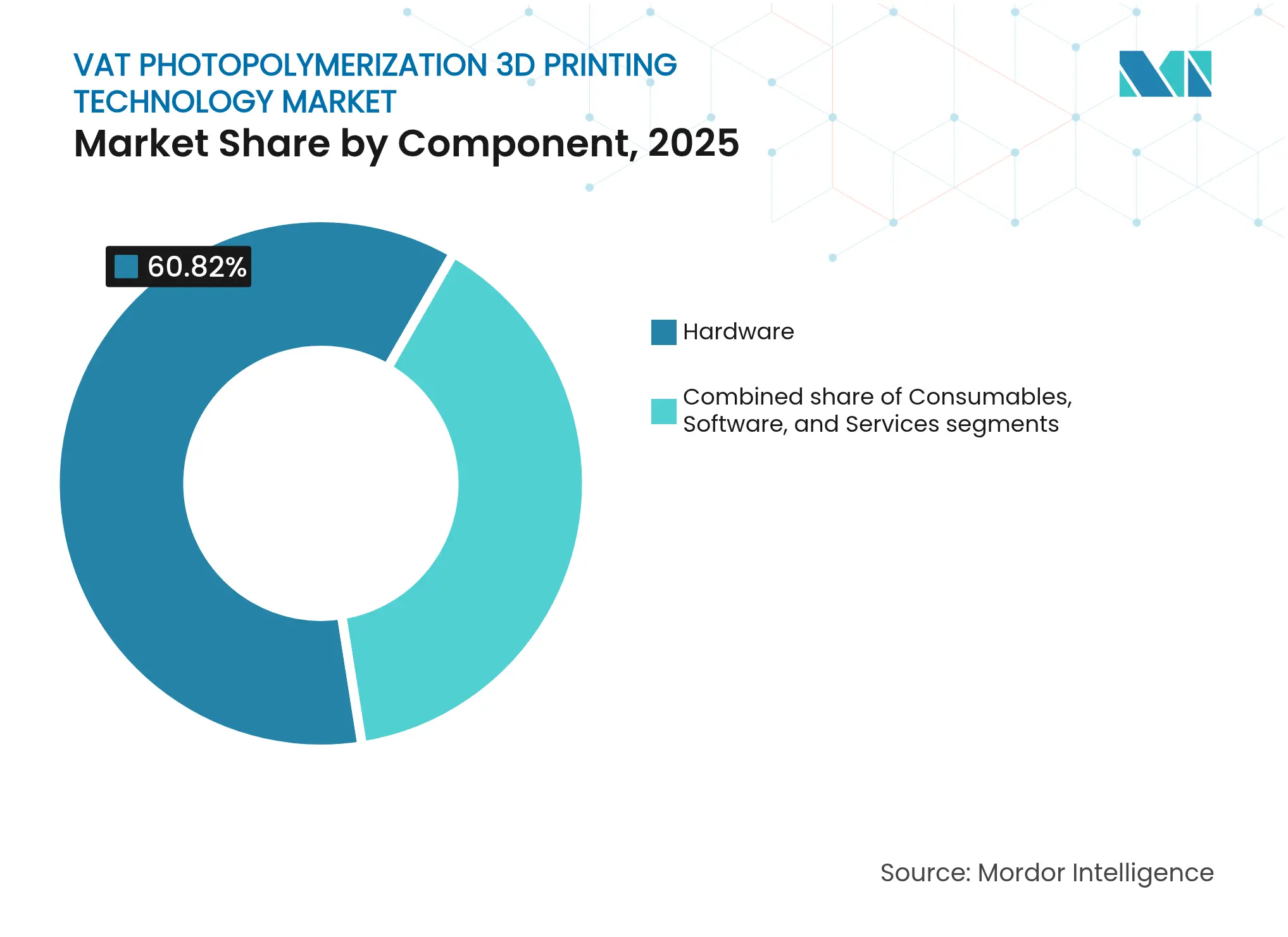

- By component, hardware led with 60.82% of the vat photopolymerization 3D printing technology market share in 2025, while consumables posted the highest growth trajectory at 27.15% CAGR.

- By technology, stereolithography captured 32.21% revenue share in 2025, whereas CDLP is forecast to expand at 26.60% CAGR through 2031.

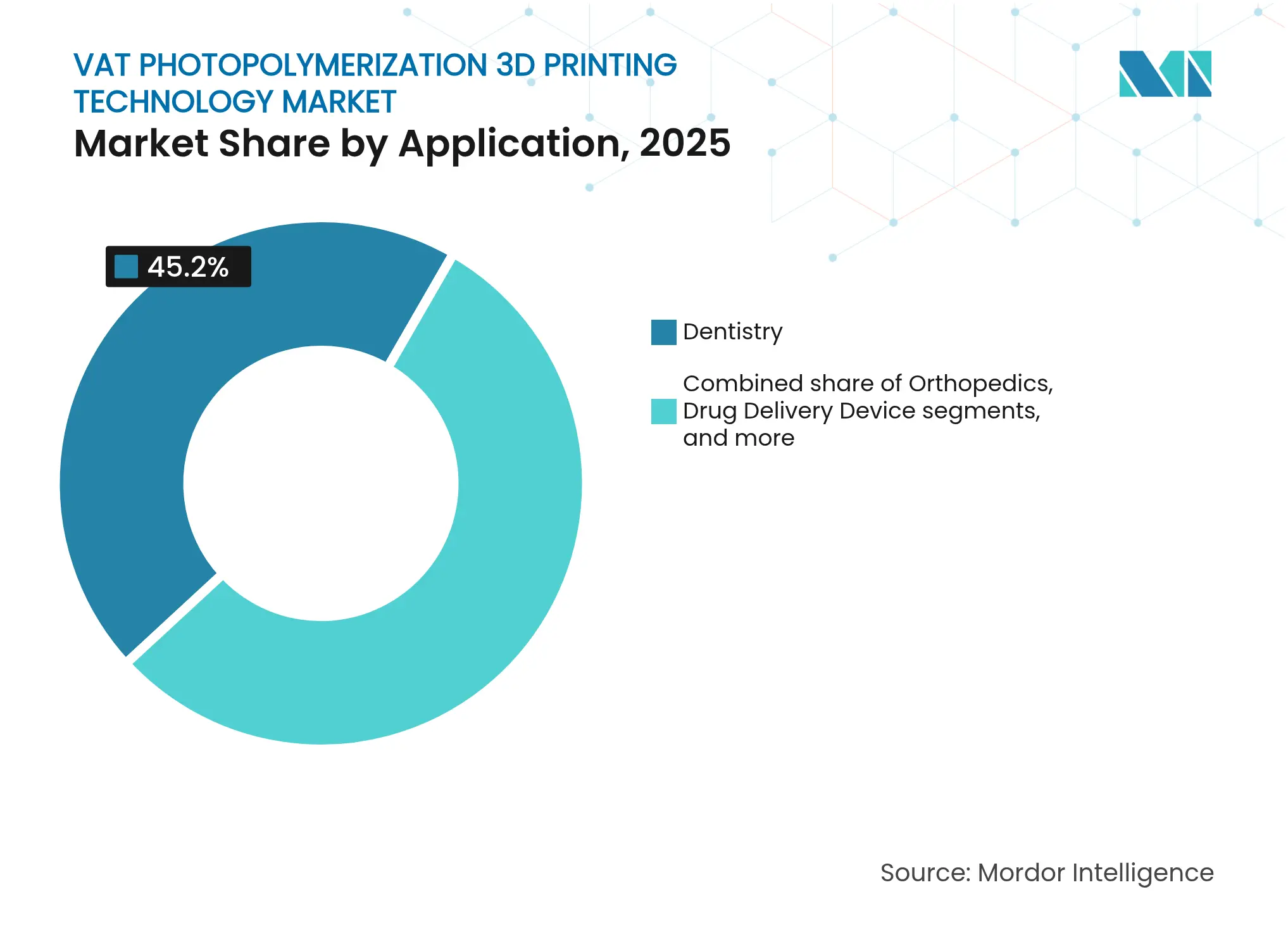

- By application, dentistry commanded 45.20% of the vat photopolymerization 3D printing technology market size in 2025; tissue engineering and bioprinting are advancing at a 27.30% CAGR.

- By geography, North America held a 40.10% share in 2025, whereas Asia-Pacific is projected to grow at a 26.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vat Photopolymerization 3D Printing Technology Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Emergence of <25 µm Desktop Printers for Chair-Side

Dentistry Workflows

Emergence of <25 µm Desktop Printers for Chair-Side

Dentistry Workflows

| +4.2% | North America & Europe, expanding to APAC | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

+4.2%

|

Geographic Relevance

:

North America & Europe, expanding to APAC

|

Impact Timeline

:

Short term (≤ 2 years)

|

OEM–Resin Open-Material Partnerships Unlocking High-Margin

Consumables

OEM–Resin Open-Material Partnerships Unlocking High-Margin

Consumables

| +3.8% | Global, with concentration in developed markets | Medium term (2-4 years) | |||

Falling Total Cost of Ownership of LCD Printers

Falling Total Cost of Ownership of LCD Printers

| +3.1% | APAC core, spill-over to emerging markets | Short term (≤ 2 years) | |||

Additive-Qualified Biocompatible Photopolymers Cleared by

Regulatory Bodies

Additive-Qualified Biocompatible Photopolymers Cleared by

Regulatory Bodies

| +2.9% | North America & EU regulatory zones | Medium term (2-4 years) | |||

Mainstream Dental Lab Consolidation Driving Printer Fleet

Upgrades

Mainstream Dental Lab Consolidation Driving Printer Fleet

Upgrades

| +2.7% | North America & Europe | Long term (≥ 4 years) | |||

EV Battery Pack Prototyping Shifting to Large-Format SLA

Tools

EV Battery Pack Prototyping Shifting to Large-Format SLA

Tools

| +1.8% | APAC manufacturing hubs, expanding globally | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Emergence of sub-25 µm desktop printers for chair-side dentistry workflows

Fast, high-resolution desktop machines allow single-visit production of surgical guides and composite crowns, shrinking traditional lab turnaround times from days to less than 30 minutes. SprintRay’s system enables output of nearly 84 crowns per hour at material costs below USD 20 each, reshaping value capture between clinics and labs. FDA clearances for definitive restorations continue to build practitioner confidence, widening adoption among risk-averse dental practices.

OEM–resin open-material partnerships unlocking high-margin consumables

Printer manufacturers increasingly collaborate with chemical suppliers to pre-qualify proprietary resins, turning one-time hardware sales into recurring consumables revenue with margins topping 70%. Desktop Metal’s qualification of INFINAM ST 6100 L exclusively for its ETEC Xtreme 8K platform illustrates the consumables lock-in potential. Such validated pairings shorten regulatory approval cycles and guarantee print consistency, compelling buyers to prioritize performance over material cost.

Falling total cost of ownership of LCD printers

LCD-based systems replace galvanometer scanners with inexpensive masked light engines, trimming acquisition prices under USD 1,000[1]Maryam Mottaghi, “A Review of 3D Printing Batteries,” Batteries, mdpi.com and reducing power consumption by 75% versus laser-based counterparts. Chinese vendors exploit local electronics supply chains to reach price points attractive to small clinics and universities, accelerating global democratization of precision manufacturing.

Additive-qualified biocompatible photopolymers cleared by regulators

Regulatory bodies now clear resins for permanent intraoral and implant-supported use, expanding addressable markets well beyond models and guides. Desktop Health’s Flexcera Smile Ultra+ received FDA 510(k) status, opening a multi-billion prosthetics opportunity for additive manufacturing. Early movers gain durable advantages[2]Noha Sabry ElMalah, “Evaluation of 3D printed nano-modified resin shear bond strength on titanium surfaces (an in-vitro study),” BMC Oral Health, bmcoralhealth.biomedcentral.com as each material clearance requires costly biocompatibility testing.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatility in Epoxy-Acrylate Feedstock Pricing

Volatility in Epoxy-Acrylate Feedstock Pricing

| -2.8% | Global, with acute impact in cost-sensitive markets | Short term (≤ 2 years) |

% Impact on CAGR Forecast

:

-2.8%

|

Geographic Relevance

:

Global, with acute impact in cost-sensitive markets

|

Impact Timeline

:

Short term (≤ 2 years)

|

Post-Cure Energy Consumption Regulations

Post-Cure Energy Consumption Regulations

| -1.9% | Europe & California, expanding to other regions | Medium term (2-4 years) | |||

Service-Bureau Overcapacity

Service-Bureau Overcapacity

| -1.4% | North America & Europe mature markets | Short term (≤ 2 years) | |||

Workplace VOC-Exposure Limits Tightening

Workplace VOC-Exposure Limits Tightening

| -1.2% | Developed markets with strict occupational safety | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatility in epoxy-acrylate feedstock pricing

Annual swings above 25% in resin input costs compel dynamic consumable pricing, eroding buyers' cost predictability. Fabricators reported shortages impacting 62% of scheduled jobs, prompting material substitutions[3]Arkema Press Release, “Arkema showcases sustainability and partnerships for 3D printing at Rapid+TCT 2024,” arkema.com that risk quality deviations.

Post-cure energy consumption regulations

European directives on industrial energy use force service providers to retrofit LED curing or heat-recovery systems, requiring capex above USD 100,000 per site. Dual-cure chemistries that reduce heat demands gain favor, advantaging vendors with proprietary low-energy workflows.

Segment Analysis

By Component: Expanding Consumables Upset Hardware Dominance

Hardware retained a 60.82% of the vat photopolymerization 3D printing technology market share in 2025, on the back of industrial and professional system demand, yet repeated consumable purchases are outpacing capital sales at a 27.15% CAGR. The vat photopolymerization 3D printing technology market now relies on vertically integrated platforms bundling printers, resins, software, and post-processing units. Engineering and bio-resins command high margins due to validated mechanical performance and regulatory clearances. Post-processing solutions, often 30% of system cost, rise in importance as customers seek end-to-end compliance with sterilization and VOC standards.

Installed fleet expansion pushes resin volumes far beyond prototyping norms, supporting a shift toward subscription models for automated material replenishment. LCD printer sales pull in first-time adopters, creating a funnel for premium resin upgrades once applications mature. Overall, component diversification reduces dependence on lump-sum hardware revenue and stabilizes cash flows across economic cycles.

Note: Segment shares of all individual segments available upon report purchase

By Technology: SLA Strength Meets CDLP Momentum

Stereolithography held a 32.21% share of the vat photopolymerization 3D printing technology market size in 2025, thanks to decades-long material libraries and process know-how. Continuous digital light processing, however, posts a 26.60% CAGR, fueled by oxygen-permeable optics and dual-cure resins that allow truly isotropic parts. LCD variants gain traction for affordability but face light uniformity challenges at industrial scales. Volumetric approaches, though nascent, promise minute-level build times and could redraw technical boundaries once material chemistries mature.

SLA providers respond with larger build volumes and improved laser path optimization, while CDLP pioneers emphasize mechanical parity with injection-molded thermoplastics. Intellectual property around optics–chemistry integration forms the core competitive moat in both camps, dictating differentiation and pricing power.

By Application: Dental Maturity vs. Bioprinting Frontier

Dentistry delivered 45.20% of the vat photopolymerization 3D printing technology market share in 2025, on the strength of clear aligners, crowns, and custom impression trays. Chair-side printing cuts patient visits and lab fees, anchoring the vat photopolymerization 3D printing technology market in routine clinical practice. Meanwhile, tissue engineering and bioprinting grow at 27.30% CAGR as researchers fabricate vascularized organ models sustaining viral cultures for multi-week drug testing. Orthopedics, jewelry, and consumer products further diversify the application landscape, providing resilience against dental market saturation.

The long-term upside lies in regulated medical devices and regenerative therapies, where validated bio-inks unlock high-value patient-specific implants. As clinical evidence accumulates, payers begin reimbursing additive-produced devices, catalyzing mainstream healthcare adoption.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America controlled 40.10% of spending in 2025, with a 24.90% CAGR projected to 2031 supported by deep dental lab networks and favorable FDA pathways. The United States dominates regional revenue through R&D-intensive clusters that commercialize new material–hardware combinations rapidly. Canadian hospitals increasingly procure printers to localize prosthetics manufacturing, while Mexico’s maquiladora network integrates vat photopolymerization lines for cost-sensitive medical exports.

Europe advances at 25.20% CAGR, anchored by Germany’s Industry 4.0 programs and France’s USD 3.6 billion additive manufacturing turnover. The EU Medical Device Regulation tightens evidence thresholds, channeling demand toward vendors with compliance infrastructure and documented biocompatibility records.

Asia-Pacific exhibits the highest trajectory at 26.75% CAGR. China’s Bambu Lab and other domestic champions ship low-cost LCD units that broaden entry-level access, while Japan and South Korea refine large-format SLA optics, leveraging established electronics ecosystems. India invests in distributed digital dentistry infrastructure to serve a growing middle class. Government subsidies and cluster policies reinforce regional self-sufficiency in both hardware and resin production, intensifying competition with Western incumbents

Competitive Landscape

Market Concentration

Moderate fragmentation characterizes the vat photopolymerization 3D printing technology industry. Market leaders such as 3D Systems, Formlabs, and Carbon tilt toward vertical integration, combining proprietary materials with networked software to lock in recurring resin sales. Desktop Metal continues acquisitive expansion to fill application gaps, while emergent specialists focus on niche opportunities such as bioprinting scaffolds or large-volume automotive tooling. Asian entrants erode price points in the desktop tier, compelling Western vendors to emphasize throughput, validated performance, and regulatory assurance.

Strategic partnerships dominate the news flow: hardware-resin co-development shortens FDA review cycles and aligns incentives around lifetime customer value rather than one-time printer margins. Consolidation is gathering pace among service bureaus seeking scale economies for energy-efficient post-processing and 24-hour turnaround guarantees. Intellectual property disputes increasingly center on oxygen-permeable windows, resin photoinitiator compositions, and embedded sensor networks that optimize curing in situ.

Vat Photopolymerization 3D Printing Technology Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: 3D Systems unveiled the Figure 4 135 printer with flame-retardant Tough 75C FR Black resin for motorsport components.

- November 2024: 3D Systems introduced the PSLA 270 projector-based platform plus Wash 400F and Cure 400 post-processing units.

- October 2024: Formlabs released the Form 4L large-scale SLA printer at a USD 10,000 price point, widening professional accessibility.

- October 2024: Protolabs adopted Carbon DLS for series component production, boosting throughput for low-volume manufacturing.

Table of Contents for Vat Photopolymerization 3D Printing Technology Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Emergence of Less Than 25 µm Desktop Printers for Chair-Side Dentistry Workflows

- 4.2.2OEM-Resin Open-Material Partnerships Unlocking High-Margin Consumables

- 4.2.3Falling Total Cost of Ownership of LCD Printers

- 4.2.4Additive-Qualified Biocompatible Photopolymers Cleared by Regulatory Bodies

- 4.2.5Mainstream Dental Lab Consolidation Driving Printer Fleet Upgrades

- 4.2.6EV Battery Pack Prototyping Shifting to Large-Format SLA Tools

- 4.3Market Restraints

- 4.3.1Volatility in Epoxy-Acrylate Feedstock Pricing

- 4.3.2Post-Cure Energy Consumption Regulations

- 4.3.3Service-Bureau Overcapacity

- 4.3.4Workplace VOC-Exposure Limits Tightening

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Component

- 5.1.1Hardware

- 5.1.1.1Desktop Printers

- 5.1.1.2Professional Printers

- 5.1.1.3Industrial Printers

- 5.1.1.4Post-Processing Equipment

- 5.1.2Consumables

- 5.1.2.1Standard Resins

- 5.1.2.2Engineering Resins

- 5.1.2.3Bio-Resins

- 5.1.2.4Ceramic-filled & Composite Resins

- 5.1.3Software

- 5.1.4Services

- 5.2By Technology

- 5.2.1Stereolithography (SLA)

- 5.2.2Digital Light Processing (DLP)

- 5.2.3Continuous Digital Light Processing (CDLP)

- 5.2.4Other Technologies

- 5.3By Application

- 5.3.1Dentistry

- 5.3.1.1Aligners & Retainers

- 5.3.1.2Surgical Guides

- 5.3.1.3Crowns, Bridges & Dentures

- 5.3.2Orthopedics

- 5.3.2.1Implants

- 5.3.2.2Pre-surgical Models

- 5.3.3Tissue Engineering & Bioprinting

- 5.3.4Drug Delivery Devices

- 5.3.5Other Applications

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Competitive Benchmarking

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.13D Systems Inc.

- 6.4.2Anycubic

- 6.4.3Asiga

- 6.4.4B9Creations

- 6.4.5Carbon Inc.

- 6.4.6Desktop Metal

- 6.4.7DWS S.r.l.

- 6.4.8FlashForge

- 6.4.9Formlabs

- 6.4.10Kings 3D

- 6.4.11Nexa3D

- 6.4.12Peopoly

- 6.4.13Photocentric

- 6.4.14Phrozen

- 6.4.15Ray Optics Inc.

- 6.4.16SprintRay

- 6.4.17Stratasys Ltd.

- 6.4.18Suzhou RAYSHAPE Intelligent Technology Co., Ltd.

- 6.4.19Tiertime

- 6.4.20UnionTech

- 6.4.21XYZprinting

- 6.4.22Zortrax

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Vat Photopolymerization 3D Printing Technology Market Report Scope

As per the scope of the report, vat photopolymerization is a category of additive manufacturing (AM) processes that create 3D objects in medicine by selectively curing liquid resin through targeted light-activated polymerization.

The vat photopolymerization 3D printing technology market is segmented by component, technology, application, and geography. By component, the market is segmented into hardware, software, services, and materials. By technology, the market is segmented into stereolithography (SLA), digital light processing (DLP), and continuous digital light processing (CDLP). By application, the market is segmented into dentistry, orthopedics, tissue engineering, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market sizes and forecasts in value (USD) for the above segments.