Vacuum Grease Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

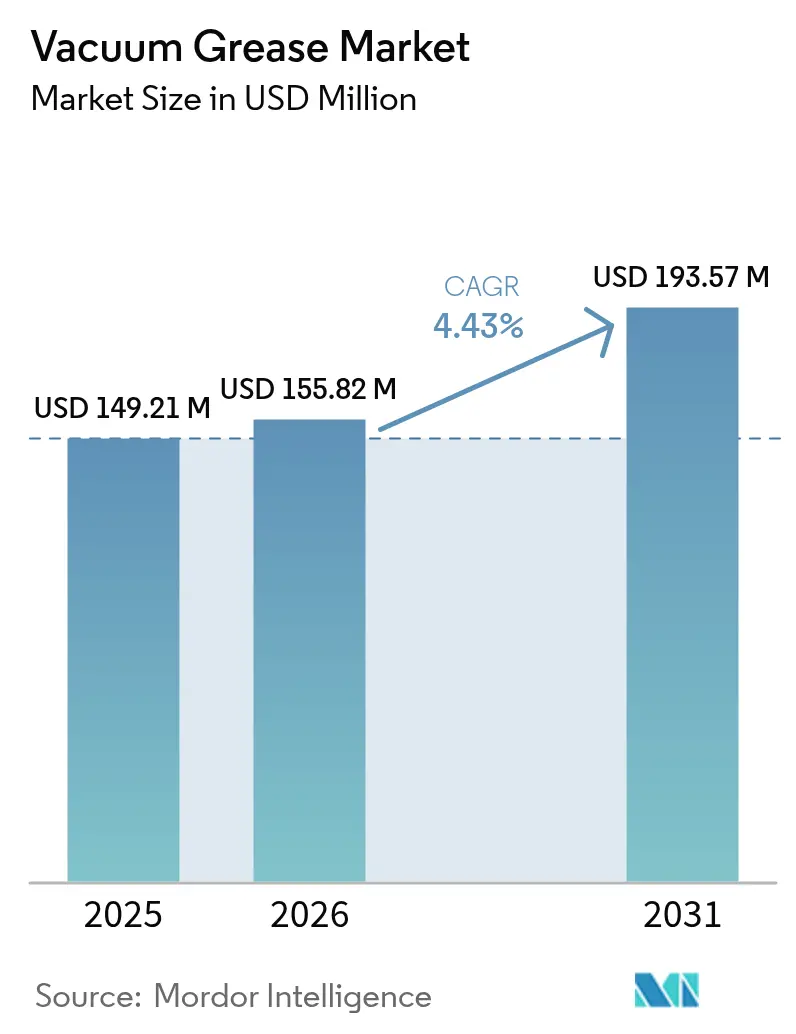

| Market Size (2026) | USD 155.82 Million |

| Market Size (2031) | USD 193.57 Million |

| Growth Rate (2026 - 2031) | 4.43% CAGR |

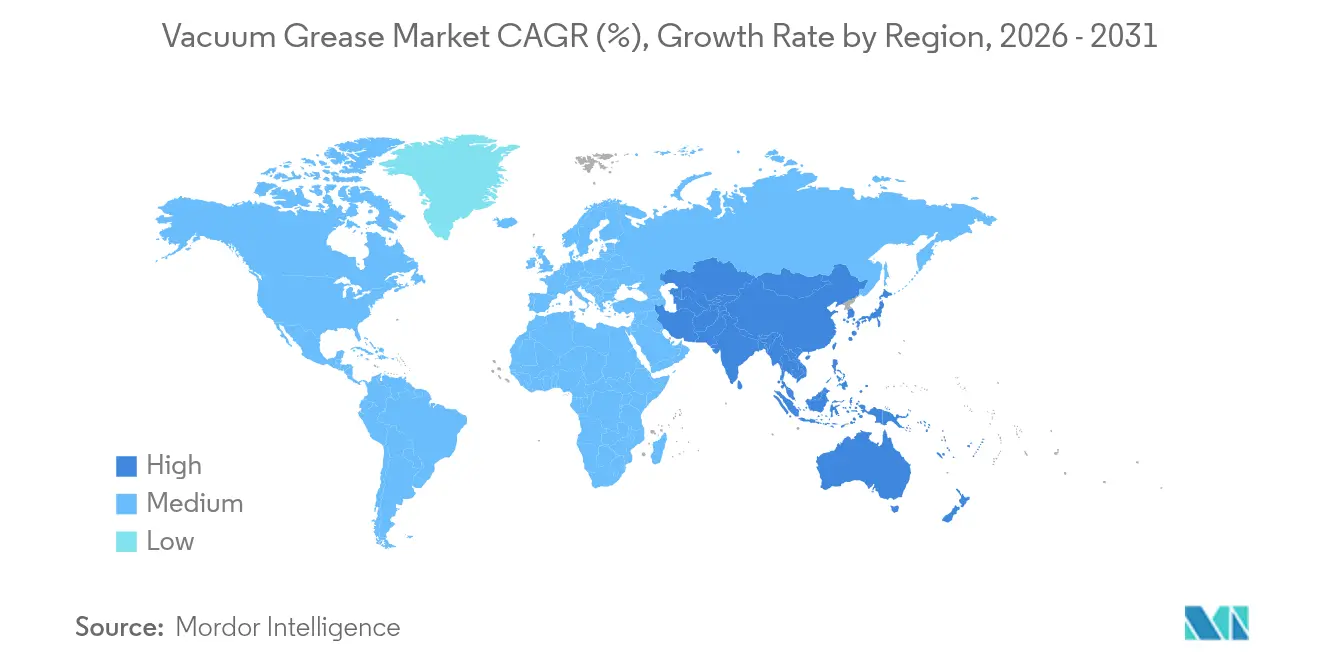

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vacuum Grease Market Analysis by Mordor Intelligence

The Vacuum Grease market size is expected to grow from USD 149.21 million in 2025 to USD 155.82 million in 2026 and is forecast to reach USD 193.57 million by 2031 at 4.43% CAGR over 2026-2031. Growth stems from the rising intensity of ultra-high-vacuum (UHV) processes in semiconductor fabrication, the accelerated deployment of freeze-dryers in biologics manufacturing, and the electrification of power-dense vehicle architectures. Fluorocarbon-based formulations led with 46.18% share in 2024 on the back of superior thermal stability, while silicone-based and hydrocarbon alternatives captured niche demand where cost or compatibility takes priority. Europe dominated with 37.54% share, propelled by regulatory frameworks that reward premium, compliant chemistries even as they pressure producers to eliminate PFAS content. Asia-Pacific, however, is recording the fastest growth due to rapid expansion of fabs and pharmaceutical plants coupled with sustained capital investment in industrial automation.

Key Report Takeaways

- By type, fluorocarbon-based products accounted for 45.62% of vacuum grease market share in 2025 and remain the fastest-growing category at a 4.62% CAGR through 2031.

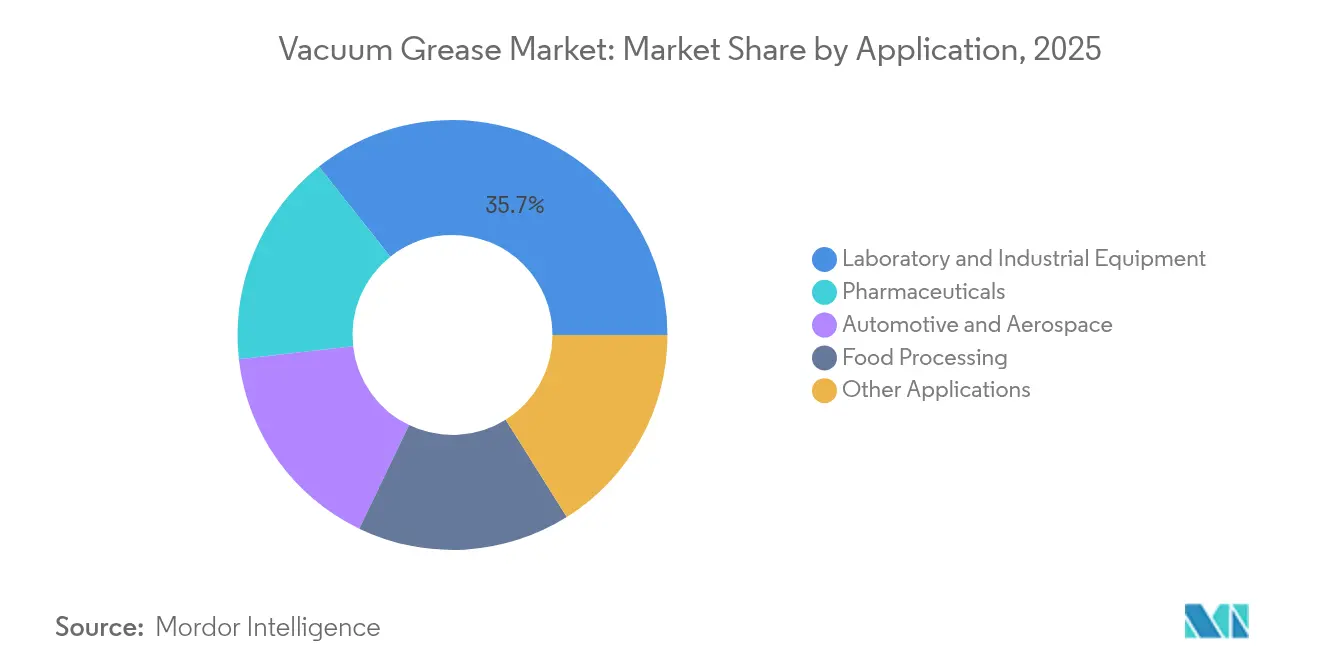

- By application, laboratory and industrial equipment held 35.67% of the vacuum grease market size in 2025, whereas the pharmaceutical segment is on track for a 4.87% CAGR to 2031.

- By geography, Europe contributed 37.02% of global revenue in 2025, while Asia-Pacific is expanding the fastest with a 5.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vacuum Grease Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of High-Vacuum Processes in Semiconductor Manufacturing | +1.2% | Asia-Pacific core, spill-over to North America and EU | Medium term (2-4 years) |

| Rising Adoption in Pharmaceutical Freeze-Drying Equipment | +0.8% | Global, with concentration in North America and EU | Long term (≥ 4 years) |

| Growth of Vacuum-Assisted Food Packaging | +0.5% | Global, particularly strong in APAC and North America | Medium term (2-4 years) |

| Shift to PFAS-Free Formulations Driven by Emerging Regulation | +0.3% | EU leading, North America following | Short term (≤ 2 years) |

| Demand For Dielectric Greases in EV Power Electronics | +0.4% | Global, with early gains in China, EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of High-Vacuum Processes in Semiconductor Manufacturing

Shrinking device geometries below 5 nm amplify the need for contamination-free environments, thereby raising per-fab consumption of vacuum grease. Advanced packaging steps such as chemical and physical vapor deposition require robust sealing solutions that withstand cycling between ambient and UHV without outgassing. CAdoption of 300 mm and larger wafers, plus 2.5D/3D integration, further multiplies grease volumes per tool, while suppliers such as Nye Lubricants publish TML < 1% and CVCM < 0.10% specifications to match zero-defect targets.

Rising Adoption in Pharmaceutical Freeze-Drying Equipment

Lyophilization is entrenched in biologics production, elevating demand for FDA-compliant greases that sustain vacuum integrity over long cycles. Hydrophobic vial coatings can trigger boiling under vacuum, prompting formulation refinements to mitigate surface freezing anomalies[1]Klevens et al., “Effect of Vial Hydrophobicity on Lyophilization,” MDPI, mdpi.com. DuPont’s MOLYKOTE grades are formulated for dry-pump systems, averting oil carryover while maintaining seal longevity. As manufacturers swap oil-sealed pumps for dry scroll or screw variants, specialty greases become pivotal to performance, positioning the vacuum grease market for steady pharmaceutical pull-through.

Growth of Vacuum-Assisted Food Packaging

Modified-atmosphere and vacuum skin packaging extend shelf life and nutrient retention, requiring NSF H1-registered greases compatible with 21 CFR 178.3570 thresholds. Asia-Pacific’s broader adhesives and sealants industry is forecast to reach USD 42.92 billion by 2030, underscoring spill-over adoption of vacuum technology in food processing. Compliance with multi-region rules—FDA, REACH and local statutes—favors incumbents who maintain in-house regulatory teams.

Shift to PFAS-Free Formulations Driven by Emerging Regulation

The EU is evaluating a near-total PFAS prohibition under ECHA, compelling suppliers to devise non-fluorinated greases that rival PFPE performance. FUCHS answered with the RHEOLUBE 460P series, a PAO grease thickened with lithium soap and free of fluorinated additives. Success hinges on replicating PFAS attributes—extreme thermal stability and low surface energy—without compromising volatility or chemical resistance, a hurdle that raises entry barriers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Vacuum Greases | -0.7% | Global, particularly price-sensitive emerging markets | Medium term (2-4 years) |

| Competition from Dry-Film Lubricants in UHV Systems | -0.4% | Global, concentrated in high-tech applications | Long term (≥ 4 years) |

| Regulatory Scrutiny of Fluorinated Chemistries | -0.3% | EU leading, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Vacuum Greases

Specialty greases command price points 10-20 times standard lubricants owing to tight process specifications, limited volumes and rigorous QC. Bio-based alternatives add further premium because feedstocks and refining steps are costlier. Small producers struggle to match pricing of larger peers, curbing penetration in non-mission-critical uses.

Competition from Dry-Film Lubricants in UHV Systems

Coatings of molybdenum disulfide, tungsten disulfide or diamond-like carbon meet friction coefficients of 0.02-0.05 in UHV, often beating wet greases for lifetime and outgassing. Carter Bearings markets bearings pre-treated with such coatings for scientific instruments, signalling gradual substitution in the most contamination-sensitive niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fluorocarbon Dominance Faces Regulatory Headwinds

The fluorocarbon segment accounted for 45.62% of vacuum grease market share in 2025 and is projected to compound at 4.62% through 2031, a trajectory sustained by the unmatched stability of PFPE-based products in oxygen-rich or high-temperature environments. The vacuum grease market size attributable to silicone-based alternatives is rising in applications where broad service-temperature windows offset their marginally higher outgassing. Hydrocarbon greases occupy value-driven niches, particularly in rough-vacuum regimes. European PFAS proposals have triggered stock-build behaviour among semiconductor and aerospace users, temporarily inflating demand even as R&D pivots toward compliant chemistries. DuPont’s silicone MOLYKOTE High-Vacuum Grease, certified for -40 °C to 204 °C, exemplifies non-fluorinated offerings that secure FDA alignment.

A gradual shift toward ether-free and solvent-free thickener systems is detectable in patent filings, hinting at a future where the vacuum grease market size continues to expand while the product mix tilts toward hybrid silicone-fluoropolymer matrices capable of meeting EU eco-toxicity benchmarks.

By Application: Laboratory Equipment Leads, Pharmaceuticals Accelerate

Laboratory and industrial equipment remained the largest slice, commanding 35.67% of the vacuum grease market size in 2025, underpinned by constant demand from analytical instruments, vacuum pumps and freeze pumps used in R&D hubs. Pharmaceuticals is the quickest-rising consumer, moving at a 4.87% CAGR as lyophilization lines multiply to support monoclonal antibody pipelines. This momentum is reinforced by regulatory imperatives for contamination-free processing: dry-pump upgrades eliminate oil back-streaming, placing greater functional load on sealing greases. Automotive and aerospace users increasingly specify dielectric grades that combine insulation with thermal spreading, a dual role spurred by EV and satellite electronics. Food-processing installations adopt NSF H1-approved products to satisfy HACCP audits, while the semiconductor sector—though grouped under “other applications” here—remains the most technically demanding slice, driving innovation in ultra-low-outgassing formulations that set the benchmark for the entire vacuum grease market.

Geography Analysis

Europe retained 37.02% of global revenue in 2025 as its aerospace, pharmaceutical and precision-engineering ecosystems required top-tier formulations regardless of price. Stringent chemicals policy, including the anticipated horizontal PFAS restriction, favours incumbent producers who already operate fluorine chemistry and who can fund accelerated reformulation pipelines. Germany’s diversified industrial base, ranging from automotive Tier 1s to analytical-instrument OEMs, anchors regional demand, while the Nordic region contributes outsized volumes through high-tech machining and research infrastructure.

Asia-Pacific is advancing at a 5.65% CAGR to 2031, underpinned by large-scale semiconductor fabs in China, Taiwan and South Korea, plus India’s expanding biologics manufacturing network. Each new fab entails hundreds of vacuum tools, translating into consistent consumption of premium greases per light-off cycle. Japan’s culture of preventive maintenance sustains a high per-installation spend, and ASEAN governments courting medical-device and electronics investors are spurring incremental demand. Supply chains are localising: Shell trebled grease output in Thailand to 15,000 t y-1, enabling shorter lead times and buffering currency swings.

North America delivers steady pull through from defense, space and biotech segments. The United States leads specifications for space-qualified greases subject to NASA outgassing limits, a sub-sector that commands price-insensitive procurement. Mexico’s maquiladora clusters absorb mid-grade volumes for HVAC and appliance production, whereas Canada’s resource-processing plants take specialty grades resistant to corrosive off-gassing.

Regulatory Landscape

Vacuum grease compliance is shaped by chemical inventory and restriction regimes (notably EU REACH), alongside lubricant testing and documentation norms used for customer qualification. In Europe, the microplastics restriction under REACH (Regulation (EU) 2023/2055) has direct relevance to PTFE microparticles used as thickeners in some high-performance greases. UEIL issued a January 2026 information paper detailing conditions for industrial use, including prevention of releases and downstream information requirements.

In March 2026, ECHA's Risk Assessment Committee opinion further clarified how PTFE microparticles in lubricants map to the REACH Annex XVII framework and referenced industrial-site derogations. This effectively reinforces a compliance pathway built around containment, labeling, and end-use controls. Outside the EU, country-level chemical registration requirements continue to influence market access for specialty sealing lubricants used in industrial systems. Turkey's KKDIK regime was highlighted in May 2026 guidance updates cited by industry channels, pointing to mandatory registration requirements for certain industrial sealing system lubricants by December 31, 2026, creating a fixed compliance milestone for suppliers serving petrochemical, gas processing, and related vacuum and sealing applications. Alongside these restrictions, customers and industry bodies increasingly reference standardized test and quality practices such as ISO 3987:2024 (sulfated ash in lubricants and additives) and the American Chemistry Council's April 2025 Petroleum Additives Product Approval Code of Practice, supporting tighter, documented QC expectations even when products are ultimately qualified through application-specific outgassing and cleanliness targets.

Value Chain Analysis

The vacuum grease value chain begins with base oils (hydrocarbon, silicone, or PFPE) and specialty thickeners and additives that control vapor pressure, stability, and compatibility, with fluorinated components and PTFE-based thickeners forming a critical input set for ultra-high-vacuum grades. Formulation know-how and access to high-purity feedstocks are core differentiators, since semiconductor and aerospace users screen products against strict contamination and outgassing requirements, pushing suppliers toward tighter raw-material specifications and batch-to-batch traceability.

Manufacturing typically uses batch kettles or continuous in-line systems. Unit operations commonly include precise metering, saponification (for soap-thickened systems), water removal, base-oil dilution, and homogenization or milling, followed by in-line deaeration to reduce entrained gases and stabilize rheology. Downstream, distribution runs through direct OEM and fab and biopharma channels for premium grades and through specialty distributors serving labs and maintenance markets, where packaging, cleanliness controls, and documentation (SDS, regulatory declarations, and application validation data) matter alongside physical logistics. Qualification cycles in semiconductor tools and dry-pump lyophilization equipment create pull for consistent supply and clean manufacturing protocols, with the most exposed bottlenecks tied to availability and lead times for high-purity PFPE and performance thickeners used in low-outgassing formulations.

Competitive Landscape

The vacuum grease market is moderately fragmented: the top ten suppliers account for an estimated 40-43% of global revenue. Competitive advantage stems from proprietary chemistry, clean-room blending capability and the regulatory dossiers required for FDA, NSF, REACH or MIL-SPEC qualification. DuPont, DAIKIN and Solvay leverage broad fluoropolymer portfolios to service aerospace and semiconductor clients who demand consistent batch-to-batch purity. FUCHS demonstrated resilience by posting EUR 434 million EBIT in 2024, proving that value lies in application depth rather than volume leadership[2]FUCHS SE, “FUCHS Group Annual Report 2024,” fuchs.com .

Strategic moves in 2024-2025 reveal emphasis on capacity localisation and portfolio widening. Shell’s investment in Thai grease production mitigates freight-cost exposure and serves regional OEMs. SKF acquired John Sample Group’s lube division to deepen penetration in South-East Asian vacuum markets. Meanwhile, R&D pipelines are crowded with PFAS-free projects as regulatory timelines tighten; early-stage candidates include lithium-complex greases thickened with boron-nitride nano-fillers targeting outgassing parity with PFPE incumbents. Start-ups focusing on bio-sourced esters present low-carbon propositions but still face hurdles on volatility and thermal cycling before penetrating mission-critical niches.

Patent activity indicates a pivot toward cross-linkable fluorine-containing elastomers that improve mechanical stability at seal interfaces, as illustrated by US 4243770A. Market rivalry is thus less about price and more about the speed at which producers can validate reformulations in customer equipment under real-world duty cycles.

Vacuum Grease Industry Leaders

The Chemours Company

DuPont (MOLYKOTE)

FUCHS

Freudenberg

Solvay SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is opening around formulations and documentation packages that fit tightening EU attention on PFAS-related chemistries and microplastics, without compromising the low-outgassing performance demanded in UHV processes. UEIL's January 2026 guidance on the EU microplastics restriction and ECHA RAC's March 2026 positioning on PTFE microparticles in lubricants increase the value of containment-oriented use instructions, downstream communication, and reformulations that reduce microplastic release risk. Suppliers able to offer validated alternatives where PTFE or fluorinated components face constraints gain leverage with European industrial buyers that already screen products against REACH-aligned requirements.

On the demand side, semiconductor vacuum environments remain a high-value arena for differentiated greases, supported by product actions such as FUCHS Lubricants Co. introducing the NYETORR 6300 Series PFPE greases in March 2026 specifically for semiconductor vacuum and temperature conditions. Adjacent process-environment needs in energy-storage manufacturing also support niche products engineered for extreme dryness and contamination control, as shown by NOK Kluber Co., Ltd. unveiling a low-dew-point grease in March 2026 for battery-manufacturing environments with very low dew points. Sustainability-driven materials substitution remains another visible initiative: an open innovation challenge focused on sustainable materials to replace petroleum jelly in specialty vacuum grease production signals continued efforts to diversify feedstocks and reduce exposure to petroleum-derived inputs, creating room for suppliers to qualify new chemistries while maintaining vapor-pressure and thermal-cycling performance.

Recent Industry Developments

- March 2026: FUCHS Lubricants Co. introduced the NYETORR 6300 Series PFPE greases for semiconductor vacuum environments, emphasizing low outgassing performance for temperature- and contamination-sensitive processes. The launch adds competitive pressure around high-purity PFPE portfolios and strengthens the link between fab qualification cycles and premium grease demand.

- September 2025: DuPont updated the Safety Data Sheet for MOLYKOTE High Vacuum Grease, reinforcing the compliance documentation and traceability that regulated customers require for use in vacuum and clean manufacturing environments. SDS refresh cycles can influence customer re-qualification workflows and distributor readiness, especially where REACH- and facility-level chemical management programs are audited.

- April 2024: FUCHS acquired LUBCON Group, expanding its specialty lubricants portfolio and formulation capabilities relevant to high-performance niches, including vacuum grease applications. The acquisition supports broader application engineering coverage and can accelerate the rollout of compliant product alternatives as end users tighten specifications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the vacuum grease market covers revenue earned from grease formulated to lubricate, seal, and protect components operating under vacuum or near-vacuum conditions, where low vapor pressure and chemical stability matter for performance.

Scope exclusions: We exclude vacuum pump oils, general-purpose greases not qualified for vacuum duty, and equipment hardware sales unless bundled as a separately priced vacuum grease product.

Segmentation Overview

- By Type

- Silicone-based

- Fluorocarbon-based

- Hydrocarbon-based

- By Application

- Laboratory and Industrial Equipment

- Automotive and Aerospace

- Pharmaceuticals

- Food Processing

- Other Applications (Semiconductors and Electronics Manufacturing, Energy, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the first structure of the market and to sanity-check demand signals that show up in vacuum-intensive industries. We reviewed public sources such as US EPA materials guidance, ECHA regulatory updates for restricted chemistries, USITC import and export statistics, and OECD industrial indicators to understand where production activity is trending.

To keep the model grounded in what is actually used, we also referred to sources such as USGS materials notes, peer-reviewed tribology and vacuum-technology journals, and publicly available standards bodies documentation for vacuum practices. Company annual reports, investor presentations, and product technical datasheets were used to map product positioning, typical pack sizes, and application fit. Where available, we used paid subscriptions for company financials and intelligence, patent lookups, and shipment-level trade checks to reduce blind spots. These examples are not exhaustive, and many other public sources were also reviewed for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating where vacuum grease is consumed and how pricing behaves across grades and package formats. We spoke with manufacturers, distributors, and procurement and maintenance teams in labs, pharma processing, and industrial vacuum equipment, and we tested assumptions with technical users in automotive, aerospace, and electronics supply chains across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 16% | APAC: 47% |

| Mid tier: 46% | Functional/Unit leaders: 25% | EMEA: 32% |

| Smaller Players: 19% | Managers: 59% | Americas: 21% |

Market-Sizing & Forecasting

Sizing started with a top-down build where end-use activity indicators were translated into a realistic demand pool for vacuum-compatible grease, and then converted into value using typical consumption rates and price bands by chemistry. Inputs that mattered most included the installed base and utilization of vacuum systems in laboratories and industrial equipment, semiconductor and electronics production momentum, freeze-drying and aseptic processing intensity in pharmaceuticals, aerospace and automotive maintenance cycles, and observed shifts between silicone and fluorocarbon chemistries when higher temperature or chemical resistance is required.

Once the first total was formed, we corroborated it with selective bottom-up approximations, such as supplier and distributor channel checks, sampled price per gram across common pack sizes, and regional mix checks for applications that consistently use vacuum seals. Where the bottom-up evidence was thinner, the gap was handled by using conservative ranges agreed during interviews and by anchoring to trade flows and public manufacturing indicators.

For forecasting, scenario analysis was applied around two practical drivers, namely industrial output linked to vacuum equipment usage and chemistry-related compliance pressures that can shift product mix and average selling price. Assumptions were adjusted only after primary respondents confirmed direction and magnitude, and then the model was re-run to ensure totals stayed consistent across regions and applications.

Data Validation & Update Cycle

Validation was done in layers so obvious issues got caught early and subtle ones were not missed later. We compared outputs against independent signals like trade movement, public production indices for vacuum-reliant industries, and observed price corridors, and then we rechecked any sharp regional swings or step changes in ASP.

Before sign-off, the model goes through multi-step analyst review where assumptions, units, and currency conversions are checked for consistency across the time series. When a material event shows up, such as a major regulatory update affecting fluorocarbon chemistries or an abrupt feedstock price move, respondents are re-contacted to confirm whether the impact is structural or temporary. Reports are refreshed annually, with interim updates when needed, and a final pre-delivery pass is completed so clients receive the most current view.

Mordor Intelligence's Vacuum Grease Market Estimate Compared With Other Published Estimates

Published market values for vacuum grease can vary even when the topic name looks identical, because firms may lock pricing at different points in time, convert currencies on different month averages, or apply different rules for what counts as a true vacuum-grade product.

In a refresh-led view, the spread often comes from how frequently assumptions are revalidated, especially when the product mix shifts between silicone and fluorocarbon chemistries and when pack-size driven pricing changes the effective ASP. By running fresh price checks and re-testing application usage with recent interviews before finalizing currency timing, the estimate used by Mordor Intelligence tends to stay closer to what buyers see in current procurement cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 155.82 M (2026) | |

| Industry Research Publisher A | USD 148.92 M (2024) | Uses a different base year and a longer forward window, and the price build appears to lean on a fixed starting ASP without clearly showing interim refresh checks for chemistry mix and pack-size effects. |

| Industry Research Publisher B | USD 139.10 M (2023) | Starts earlier and may apply broader bulk-chemicals framing, which can pull pricing and inclusion rules toward older procurement conditions and create a lower starting value when converted to current dollars. |

Taken together, the table shows that timing choices and pricing logic can move the headline number more than most readers expect. Our approach keeps the sizing traceable to clear demand signals, realistic usage patterns, and update checks that limit drift when the market mix and pricing change year to year.

Key Questions Answered in the Report

What is the current vacuum grease market size?

The vacuum grease market size reached USD 155.82 million in 2026.

Which type of vacuum grease holds the largest market share?

Fluorocarbon-based formulations led with 45.62% share in 2025.

Which application segment is growing the fastest?

Pharmaceutical freeze-drying is expanding at a 4.87% CAGR to 2031.

Why is Asia-Pacific the fastest-growing region?

Rapid semiconductor fab construction and expansion of biologics manufacturing drive a 5.65% CAGR in the region.

How are PFAS regulations influencing product development?

Imminent PFAS bans are prompting suppliers to invest in PFAS-free chemistries that replicate the thermal and chemical stability of fluorocarbon products.

Page last updated on: