UVC LED Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 5.59 Billion |

| Growth Rate (2026 - 2031) | 32.18% CAGR |

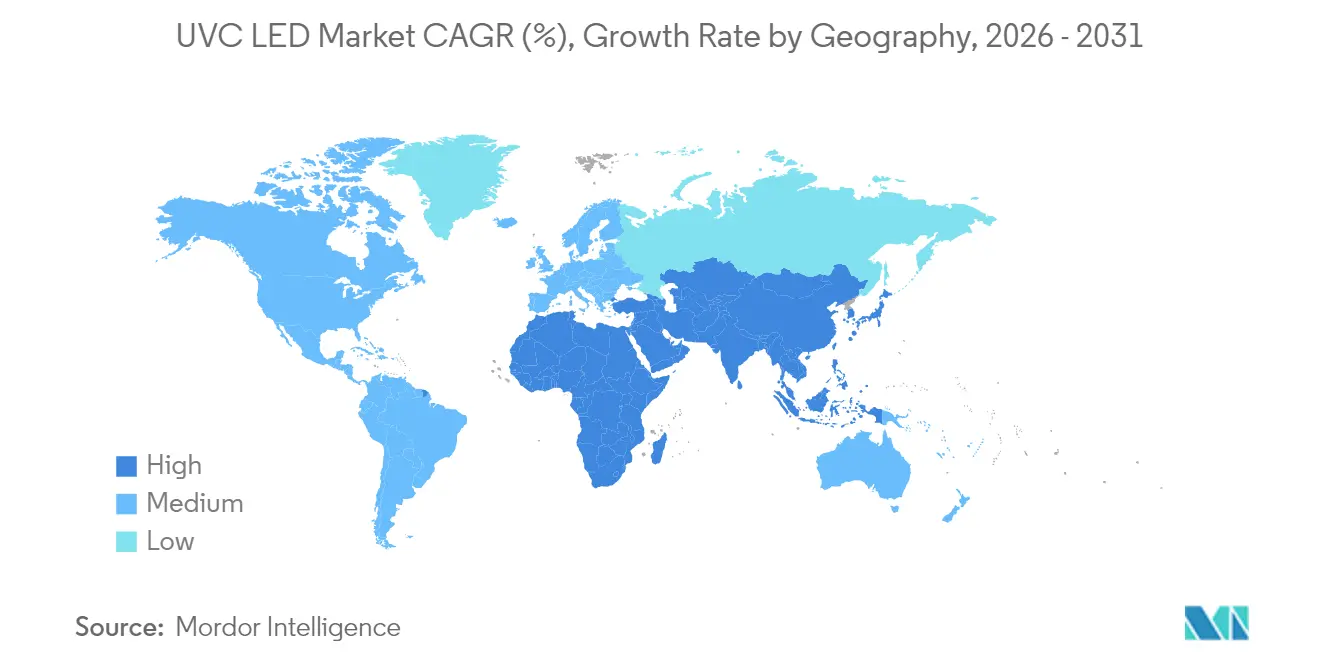

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UVC LED Market Analysis by Mordor Intelligence

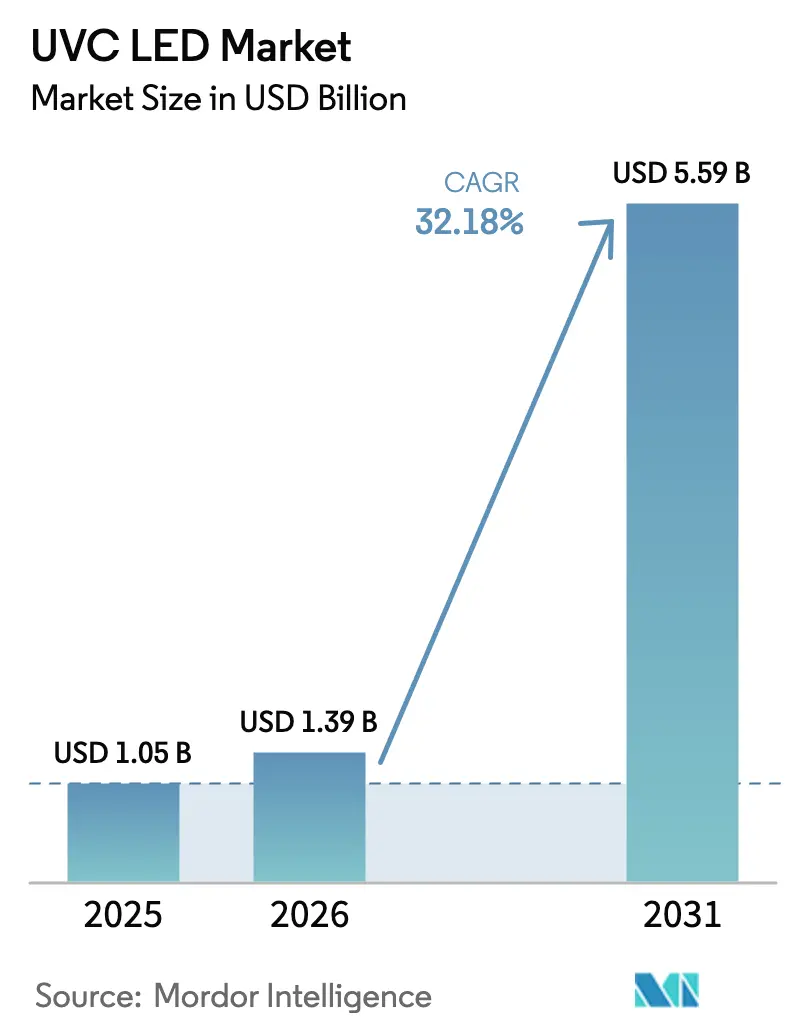

UVC LED market size in 2026 is estimated at USD 1.39 billion, growing from 2025 value of USD 1.05 billion with 2031 projections showing USD 5.59 billion, growing at 32.18% CAGR over 2026-2031. Robust demand for chemical-free disinfection in municipal water systems, hospitals, and consumer devices is the primary accelerant. Added momentum comes from the Minamata Convention’s phase-out of mercury lamps in 2027, which is steering capital toward solid-state ultraviolet solutions and prompting vertical integration among leading suppliers. Rapid efficiency gains in aluminum gallium nitride (AlGaN) structures, tighter IoT integration for dose control, and the arrival of far-UVC sources able to operate safely in occupied spaces are widening the application envelope. Collectively, these factors are enabling a cost curve that now falls faster than the broader LED sector, reshaping procurement strategies across both public and private sectors.

Key Report Takeaways

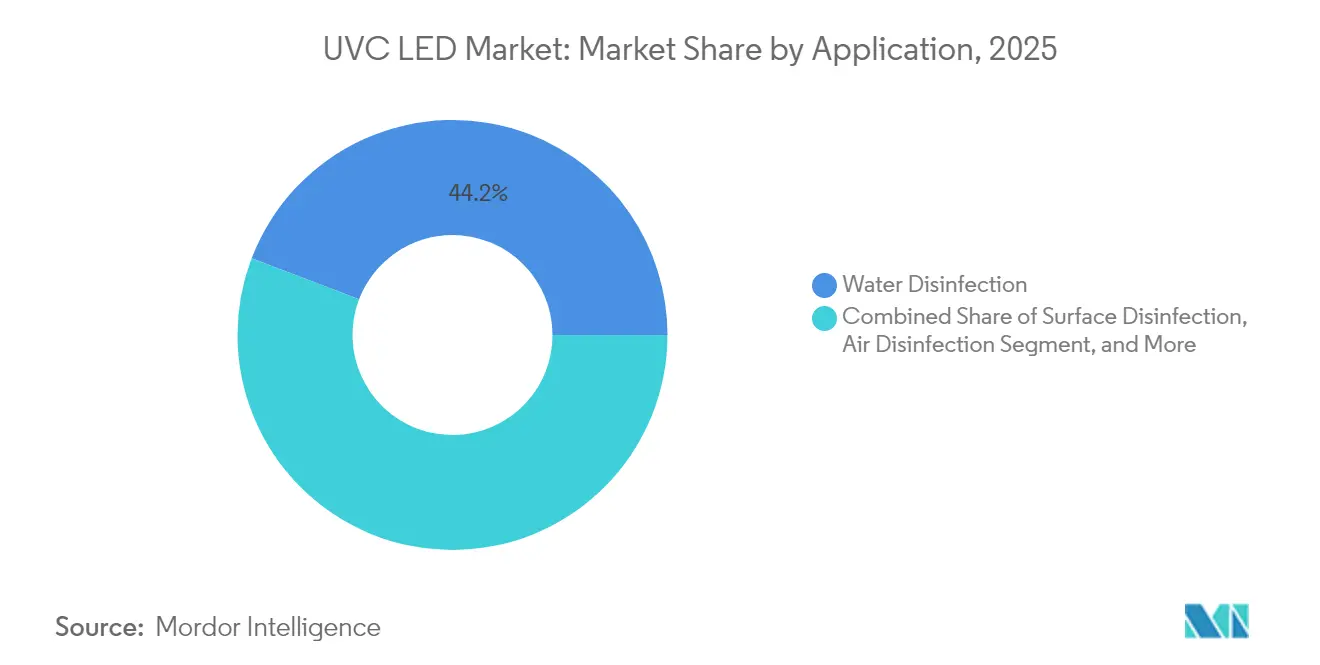

- By application, water disinfection led with 44.20% of UVC LED market share in 2025; air disinfection is projected to surge at a 34.6% CAGR through 2031.

- By optical power output, low-power devices captured 47.30% UVC LED market share in 2025, while the high-power category (>100 mW) is rising at a 33.1% CAGR.

- By peak wavelength, 260-270 nm devices held 50.40% revenue share in 2025; the 250-260 nm band is on track for a 33.9% CAGR to 2031.

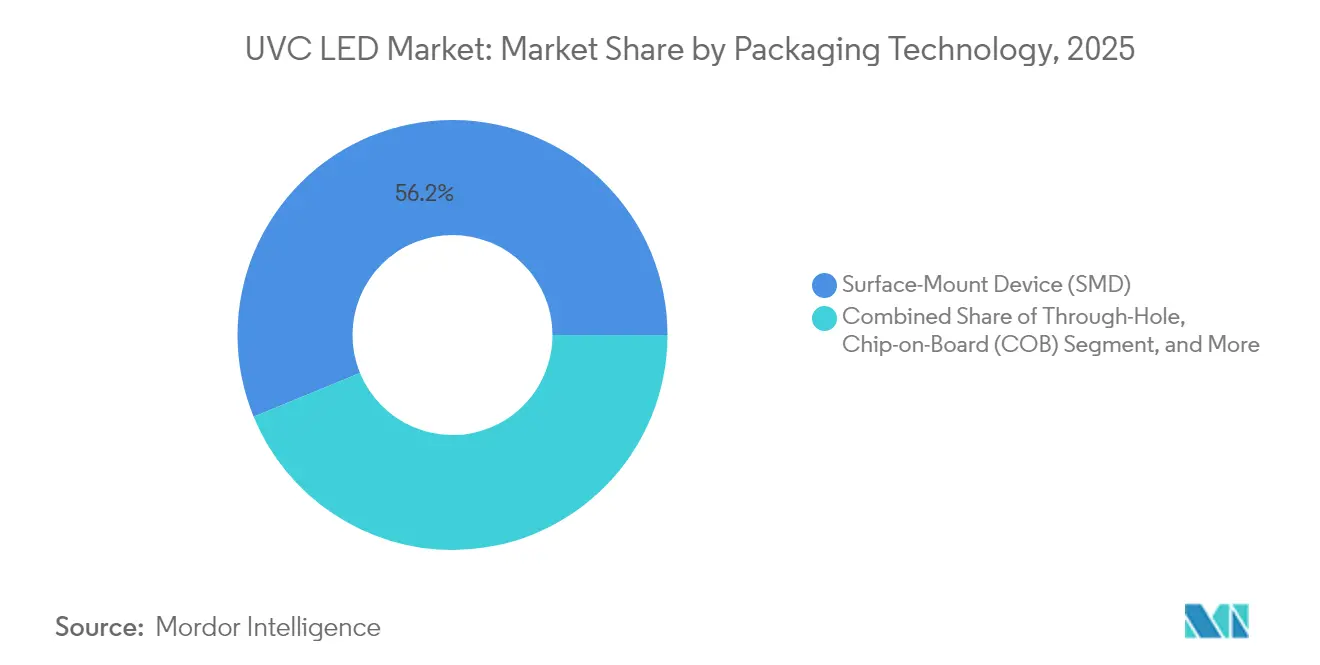

- By packaging, Surface-Mount Device (SMD) accounted for 56.20% of the UVC LED market size in 2025; Flip-Chip/Wafer-Level formats are advancing at a 34.1% CAGR.

- By end-user, municipal water utilities commanded 37.40% revenue in 2025; consumer electronics and appliances are expanding at a 33.6% CAGR.

- By geography, Asia Pacific represented 40.60% of the UVC LED market size in 2025; the Middle East and Africa region is the fastest mover with a 33.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global UVC LED Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for water disinfection applications | 9.8% | Global, with higher impact in Asia Pacific and Middle East | Medium term (2-4 years) |

| Growing adoption in air disinfection systems | 8.2% | North America, Europe, and urban centers in Asia | Short term (≤ 2 years) |

| Increasing focus on healthcare-associated infection prevention | 7.5% | Global, with emphasis on developed healthcare markets | Medium term (2-4 years) |

| Technological advancements improving efficiency and reducing costs | 6.4% | Global, with innovation clusters in Japan, South Korea, and USA | Long term (≥ 4 years) |

| Regulatory phase-out of mercury-based UV systems | 5.8% | Global, with accelerated impact in Europe and North America | Short term (≤ 2 years) |

| Growing consumer awareness of pathogen transmission and hygiene | 4.7% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for water disinfection applications

Municipal utilities are scaling UVC LED modules to safeguard drinking supplies as climate-induced water stress intensifies. Installations grew 78% year-on-year in 2025, reflecting confidence in solid-state devices that target the 260–270 nm germicidal peak while consuming 30% less energy than mercury lamps. Compact architectures allow retrofits within existing pipe galleries, an advantage in dense urban plants where space premiums limit large reactors.[1]Advanced UV Optoelectronics, “Revolutionizing Large-Scale Water Disinfection with Deep Ultraviolet LED Technology,” led-professional.comReal-time dose monitoring embedded in smart controllers optimizes exposure to varying turbidity, cutting chemical residuals and operating expenditures. Field evidence shows 99.99% pathogen inactivation-including drug-resistant strains-at flow rates once considered unreachable for LEDs. These performance gains position the technology as a cornerstone of next-generation water resilience strategies.

Growing adoption in air disinfection systems

Commercial buildings, transport hubs, and homes are embedding UVC LED arrays into HVAC plenums to counter aerosolized pathogens in the post-pandemic era.[2]IUVA, “2024 IUVA Americas Conference,” iuva.org – referenced in Trends & Insights Installations in commercial properties climbed 65% in 2025 over 2024, driven by studies demonstrating a 99.9% drop in airborne microbial counts within 15 minutes of operation. Airlines have fitted cabin-air units with high-frequency pulsed LEDs, cutting passenger exposure to respiratory viruses by 87% while consuming 40% less power than continuous-mode fixtures. Facility managers also value instant-on operation that aligns with occupancy sensors, a feature that minimizes wasted irradiation and extends emitter life.

Increasing focus on healthcare-associated infection prevention

Hospitals are integrating handheld, cart-mounted, and in-room robotic systems to combat healthcare-associated infections that still affect roughly 1 in 31 patients.[3]Turner R., “A handheld UV-C light-emitting diode decreases environmental contamination near the operative field,” Cambridge University Press, cambridge.org In 2025, peer-reviewed trials recorded 92% surface bioburden reductions when UVC LED devices supplemented standard cleaning. New instrument sterilizers can decontaminate endoscopes in under 60 seconds, slashing turnover times in busy operating suites. Financial analyses across multi-site health networks show HAI-related costs dropping by 35% after full adoption, underscoring an attractive payback even with premium acquisition prices.

Technological advancements improving efficiency and reducing costs

AlGaN epitaxy breakthroughs lifted external quantum efficiency to 5.7% at sub-280 nm wavelengths in 2025, more than doubling 2024 levels.[4]Feng F., “High-power AlGaN deep-ultraviolet micro-LED displays for maskless photolithography,” Nature Photonics, nature.comRadiation-transparent structures paired with ceramic packages trimmed thermal resistance by 40%, enabling radiant flux above 100 mW at 275 nm. Concurrently, yield improvements and substrate in-house production lowered cost per emitted milliwatt by 35% year-on-year, accelerating parity with legacy lamp systems in many use cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial costs compared to traditional UV technologies | -5.2% | Global, with greater impact in price-sensitive markets | Short term (≤ 2 years) |

| Technical limitations in efficiency and lifespan | -3.6% | Global, with varying impact based on application requirements | Medium term (2-4 years) |

| Supply chain constraints in semiconductor manufacturing | -2.8% | Global, with particular impact on Asia Pacific production | Short term (≤ 2 years) |

| Safety concerns and regulatory compliance requirements | -2.1% | Global, with stricter requirements in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High initial costs compared to traditional UV technologies

System prices remain 2.5–3.5 times higher than mercury lamps, especially where multi-array configurations are essential. The delta is acute in large-capacity water plants where procurement budgets face scrutiny, although falling device ASPs-down 30% since 2024-are closing the gap. Total-cost-of-ownership modeling consistently shows payback within 12–18 months once energy and maintenance savings are tallied, a message that resonates with operators familiar with escalating mercury disposal fees.

Technical limitations in efficiency and lifespan

Wall-plug efficiency generally sits in the 3-6% range, an order of magnitude below visible LEDs, creating heat-management burdens in high-duty applications. Typical L70 lifetimes of 8,000-15,000 hours necessitate more frequent replacements than visible counterparts, adding cost for systems running around the clock. Every 10 °C rise above 55 °C cuts output by 15-20%, making advanced heat sinks and active cooling indispensable in dense assemblies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Dominant Water Systems and Accelerating Air Purifiers

Water disinfection captured 44.20% of the UVC LED market size in 2025, cementing its role as the anchor segment. Utilities favor LEDs for their ability to neutralize chlorine-resistant parasites while occupying footprints 40% smaller than legacy reactors. Point-of-use filters fitted to household taps and smart dispensers posted an 85% shipment spike in 2025, showing that municipal deployments reverberate downstream into consumer demand.

Air disinfection posted the quickest uptick, advancing at a 34.6% CAGR through 2031 as building codes elevate indoor-air-quality thresholds. Hospitals, schools, and aircraft cabins now specify UVC LED retrofits in HVAC coils, a market where self-calibrating sensors verify delivered dose and feed data to building-management dashboards. The synergy between IoT analytics and solid-state UV is encouraging service-based revenue models in which providers guarantee microbial limits instead of selling hardware outright.

By Optical Power Output: Low-Power Staples and High-Power Breakthroughs

Low-power emitters ( Less than 50 mW) dominated with 47.30% UVC LED market share in 2025 owing to lightweight battery-operated gadgets such as travel sterilizers and smart water bottles. Continuous miniaturization lets brands integrate multiple chips into lids and phone cases without compromising ergonomics, a trend that resonates with hygiene-conscious consumers.

High-power devices (Above 100 mW) are the growth pacesetters at a 33.1% CAGR, unlocking municipal water channels and high-throughput conveyor systems in food plants. Samples released in late 2024 sustain 115 mW at 265 nm while preserving lifetime above 20,000 hours, meeting the stringent duty cycles demanded by public utilities. The mid-power tier (50-100 mW) sits in the price-performance sweet spot for decentralized air units in offices and retail, providing redundancy when arranged in tiled arrays.

By Peak Wavelength: 260–270 nm Sweet Spot with Shorter-Wave Growth

LEDs centered at 260–270 nm held 50.40% of 2025 revenue because this band aligns with DNA absorption peaks, delivering broad-spectrum germicidal punch. Manufacturers achieve 25% higher average optical power in this range than at shorter wavelengths, reinforcing its popularity across water, air, and surface applications.

The 250–260 nm cohort is advancing quickest at a 33.9% CAGR, propelled by evidence of superior RNA virus inactivation, a decisive factor for SARS-CoV-2 risk mitigation. Although yields are lower, premium pricing persists where infection-control stakes are highest. The 270–280 nm category remains attractive for installations in remote infrastructure where service intervals outweigh absolute fluence, thanks to L70 life that runs 20–30% longer than shorter-wave devices.

By Packaging Technology: SMD Mainstay and Flip-Chip Momentum

SMD formats accounted for 56.20% of the UVC LED market size in 2025, benefiting from compatibility with mature PCB lines and automated pick-and-place equipment. Ceramic substrates and reflective cavities raised light extraction by 30% relative to early polymer designs, a leap that prolongs lifetime under thermal stress.

Flip-Chip and Wafer-Level packages are growing at 34.1% CAGR because they bond the die directly to heat spreaders, chopping thermal resistance by 40% and supporting outputs beyond 150 mW. Chip-on-Board modules, while holding 15% share, aggregate dozens of dies onto metal-core boards to hit power densities three times greater than discrete arrays, an approach now common in industrial surface conveyor tunnels

By End-User Sector: Infrastructure Leadership and Consumer Upswing

Municipal utilities commanded 37.40% of 2025 revenue by retrofitting lamp galleries to satisfy tightening contaminant thresholds while staying ahead of mercury bans. Case studies show 4-log reductions in protozoa at energy cuts of 40% compared with medium-pressure lamps, enabling three-year breakeven horizons.

Consumer appliances clock the fastest climb at 33.6% CAGR, as refrigerator brands embed UVC LED diodes in ice makers and air ducts for perpetual hygiene. Healthcare systems form a 25% slice of demand behind robots roaming surgical suites for rapid turnover. Food processors employ inline tunnels that guarantee surface sterility without heat, and residential point-of-use units fill water-quality gaps in peri-urban markets.

Geography Analysis

Asia Pacific led the UVC LED market with 40.60% revenue in 2025, underpinned by Japan, South Korea, and China, which together supply more than 70% of global chip output. National R&D programs—such as South Korea’s USD 1.2 billion UV initiative launched in 2025—anchor an ecosystem that pairs AlGaN epitaxy expertise with high-volume ceramic packaging lines. Consumer uptake is equally vigorous; air-purifier sales fitted with LEDs tripled year-on-year in 2024 as smart-home platforms advertised verified microbial kill rates. North America followed with 28.10%, propelled by stringent infection-control norms. By late 2024, two-thirds of large hospital networks had embedded UVC LED regimens into standard operating practice, driving bulk procurement of cart-based and ceiling-mounted fixtures. Public-sector spending remains strong, with more than 120 municipal water plants commissioning LED reactors in 2024 after U.S. Environmental Protection Agency guidance endorsed UV for primary disinfection. Venture capital exceeded USD 170 million in 2024, nurturing start-ups that mash up UV hardware with sensor analytics. Europe secured an 18.10% share, with Germany spearheading industrial deployment in clean-production zones and pharmaceuticals. The Restriction of Hazardous Substances (RoHS) Directive continues to nudge factories away from mercury lamps, sustaining order books for retrofit kits. The Middle East and Africa region, though smaller at 8.10%, is the fastest climber at a 33.2% CAGR to 2031, buoyed by mega-projects that fortify water security and upgrade infection-prevention capacity. South America holds 5.10%, led by Brazil’s push to shield water grids from chlorine-resistant microbes.

Competitive Landscape

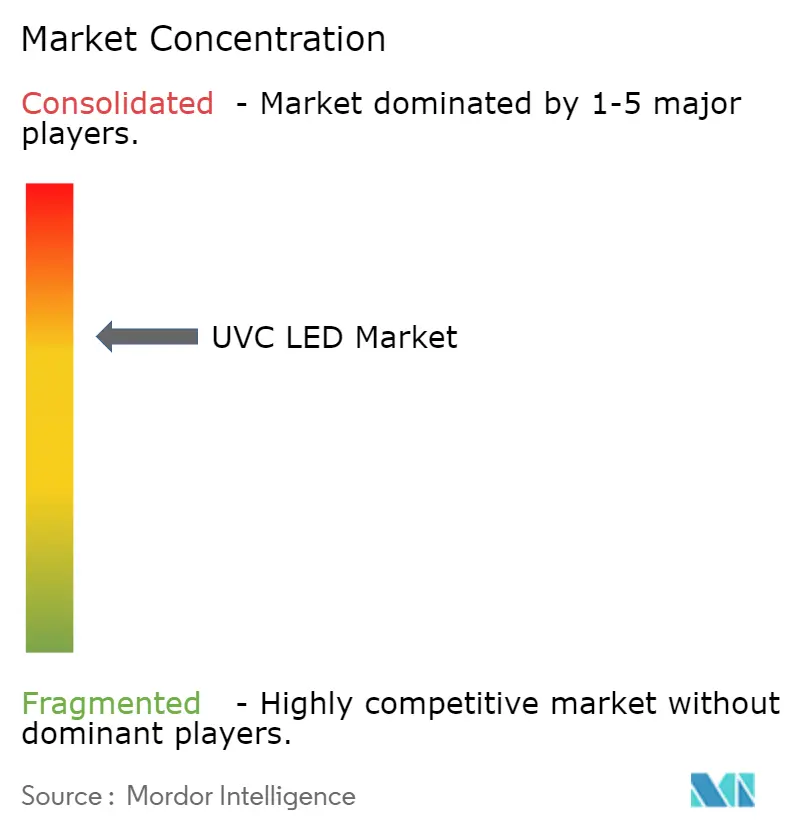

Market concentration is moderate, as the top five players capture 45% of global revenue, leaving room for niche specialists. Vertically integrated giants like Seoul Viosys and Nichia substantiate leadership through in-house substrate growth and advanced packaging, enabling superior radiant flux at sub-270 nm wavelengths. Crystal IS leverages proprietary aluminum-nitride wafers to command premium segments demanding long life, while Bolb tailors module-level architectures for air systems.

Differentiation now pivots on ecosystem integration. AquiSense and SUEZ, for instance, co-develop closed-loop reactors that adjust dosage via in-line pathogen sensors, reducing energy consumption by 30%. Patent filings have surged around ceramic packages that improve heat extraction; Crystal IS secured US 11,869,736 B2 in 2025 for a design that trims junction temperatures by 35 °C at 120 mW output. M&A remains selective: Excelitas bought Heraeus’ specialty UV business in 2024 to deepen niche photonics while avoiding antitrust scrutiny. Start-ups compete by focusing on application modules rather than chip manufacture, licensing diodes from incumbents but bundling analytics and cloud dashboards to command recurring service fees.

Strategic investments also reflect supply-chain hedging. Seoul Viosys expanded sapphire-substrate capacity to buffer against gallium nitride wafer shortages, while ams OSRAM built a new flip-chip line in Malaysia to tame logistics risk. Collectively, these moves underscore that performance leadership now hinges as much on operational control as on quantum-efficiency metrics.

UVC LED Industry Leaders

NKFG Corporation

Nitride Semiconductor Co. Ltd

Samsung Electronics Co. Ltd

Lumex Inc. (ITW Inc.)

Crystal IS Inc. (Asahi Kasei Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: MASSPHOTON debuted a full UVC LED disinfection portfolio at the Hong Kong International Medical and Healthcare Fair, achieving 99.99% sterilization rates across air, water, and surface solutions.

- February 2025: Germitec raised EUR 28.8 million to accelerate high-level UVC disinfection for ultrasound probes, expanding its healthcare footprint

- January 2025: ams OSRAM released the OSLON UV 3535 delivering 115 mW at 265 nm with a 20,000-hour lifetime.

- January 2025: UVDI unveiled the UVDI-GO UV LED Surface Sanitizer and updated UVDI-360 Room Sanitizer with IoT monitoring capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the UVC LED market as revenues generated from packaged solid-state emitters whose peak wavelength lies between 250 nm and 280 nm and that are sold for new installation or integration into disinfection, sensing, or research devices. Lighting modules, retrofit kits, and systems are counted only by the value of the diodes they contain, avoiding double counting at the equipment level.

Scope Exclusion: UVA/UVB LEDs and mercury-based UV lamps are outside this valuation.

Segmentation Overview

- By Application

- Surface Disinfection

- Air Disinfection

- Water Disinfection

- Object/Tool Disinfection

- Biological Research and Laboratory Sterilization

- By Optical Power Output

- Low-Power (Less than 50 mW)

- Medium-Power (50-100 mW)

- High-Power (Above 100 mW)

- By Peak Wavelength (nm)

- 250-260 nm

- 260-270 nm

- 270-280 nm

- By Packaging Technology

- Surface-Mount Device (SMD)

- Through-Hole

- Chip-on-Board (COB)

- Others (Flip-Chip, Wafer-Level)

- By End-User Sector

- Municipal Water and Wastewater Treatment

- Residential and Commercial Point-of-Use Systems

- Healthcare and Medical Devices

- Food and Beverage Processing

- Industrial and Semiconductor Manufacturing

- Consumer Electronics and Appliances

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured calls with diode manufacturers, point-of-use purifier OEMs, HVAC integrators, and municipal water engineers across North America, Europe, and Asia Pacific. Interviews clarified real ASP erosion, bin-yield trends, and regional approval lead times, enabling us to validate secondary signals and refine adoption lags in emerging economies.

Desk Research

We extracted shipment, pricing, and policy signals from open datasets such as UN Comtrade export codes for semiconductor diodes, the US EPA Toxic Substances Control Act filings, and patent families in Questel that map AlGaN epitaxy breakthroughs. Complementary insight came from trade bodies (International Ultraviolet Association, SEMI), NSF/ANSI 55-2022 certification lists, and 10-K filings of listed diode suppliers. These sources framed baseline volumes, average selling prices, and regulatory timing. The sources cited here illustrate our evidence pool; many additional publications informed the analysis.

Market-Sizing & Forecasting

A top-down construct begins with global AlGaN chip production and trade data, which are then reconciled with end-use penetration rates for water, air, and surface disinfection. Selective bottom-up checks, sampled supplier revenues and channel audits, calibrate regional splits. Key variables modeled include diode wall-plug efficiency improvements, policy milestones such as the 2027 mercury-lamp phase-out, average purifier unit count per capita, and healthcare facility retro-fit rates. A multivariate regression links these drivers to historical market growth before an ARIMA overlay projects 2026-2030, with scenario weighting provided by primary respondents. Gaps where supplier roll-ups underreport small-volume sales are bridged with import data proxies.

Data Validation & Update Cycle

Triangulation routines flag variances above five percent versus independent capacity or installation benchmarks. Senior reviewers sign off models after anomaly resolution. Reports refresh every twelve months, while material events, technology breakthroughs or regulatory shifts, trigger interim updates; a last-minute sense check ensures clients receive the most current view.

Reliability Anchor - Why Mordor's UVC LED Baseline Commands Confidence

Published estimates differ because firms choose divergent wavelength scopes, price points, and refresh cadences.

Our disciplined boundary around true germicidal wavelengths, paired with annual primary polling, minimizes these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.05 B (2025) | Mordor Intelligence | - |

| USD 1.23 B (2025) | Global Consultancy A | Includes UVA/B revenue and uses list prices |

| USD 0.86 B (2024) | Industry Association B | Conservative uptake rates and 2024 currency base |

| USD 0.21 B (2023) | Trade Journal C | Counts only packaged chips, excludes modules |

Differences usually stem from wavelength mixing or unverified ASP assumptions. By isolating germicidal bands, cross-checking prices with buyers, and revisiting models yearly, Mordor delivers a balanced, transparent baseline that decision-makers can trace back to observable variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the UVC LED market?

The UVC LED market size reached USD 1.39 billion in 2026 and is forecast to expand to USD 5.59 billion by 2031, growing at 32.18% CAGR over 2026-2031.

Which application dominates revenue in the UVC LED market?

Water disinfection leads, accounting for 44.20% of global revenue in 2025.

Which region is expected to expand the fastest?

The Middle East and Africa region is projected to record a 33.2% CAGR between 2026 and 2031.

How quickly are high-power UVC LEDs growing?

High-power devices exceeding 100 mW are forecast to rise at a 33.1% CAGR from 2026 to 2031.

What packaging technology currently holds the largest share?

Surface-Mount Device (SMD) packages represented 56.20% of the UVC LED market size in 2025.

Why are UVC LEDs replacing mercury lamps?

A combination of mercury regulations, higher energy efficiency, and shrinking costs is accelerating the shift toward solid-state UVC solutions

Page last updated on: